Superconducting Wire Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 1.7 Billion |

| Market Size (2031) | USD 2.18 Billion |

| Growth Rate (2026 - 2031) | 5.10% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Superconducting Wire Market Analysis by Mordor Intelligence

The superconducting wire market was valued at USD 1.62 billion in 2025 and is estimated to grow from USD 1.70 billion in 2026 to USD 2.18 billion by 2031, at a CAGR of 5.10% during the forecast period 2026 to 2031. The market serves low-, medium-, and high-temperature conductor families across medical imaging, energy and power, research, transportation, electronics, and data centers, with the latter now moving from evaluation to early commercialization. The market benefits from stable Magnetic Resonance Imaging (MRI) demand, while fusion awards and urban grid programs create larger order swings when projects move from testing to procurement. High-temperature superconductor (HTS) wire has become central to the market because fusion magnets, grid cables, and high-density power distribution require performance that standard conductors cannot provide under the same current and field conditions. The medical segment is also shifting, as hospitals and radiology suppliers move toward higher-field, helium-free magnet platforms, which support longer-term supply agreements rather than spot buying. The market faces challenges, including high conductor and cryogenic system costs, uneven manufacturing yield in Rare Earth Barium Copper Oxide (REBCO) tape, and project-driven buying cycles that can create long gaps between large awards.

Key Report Takeaways

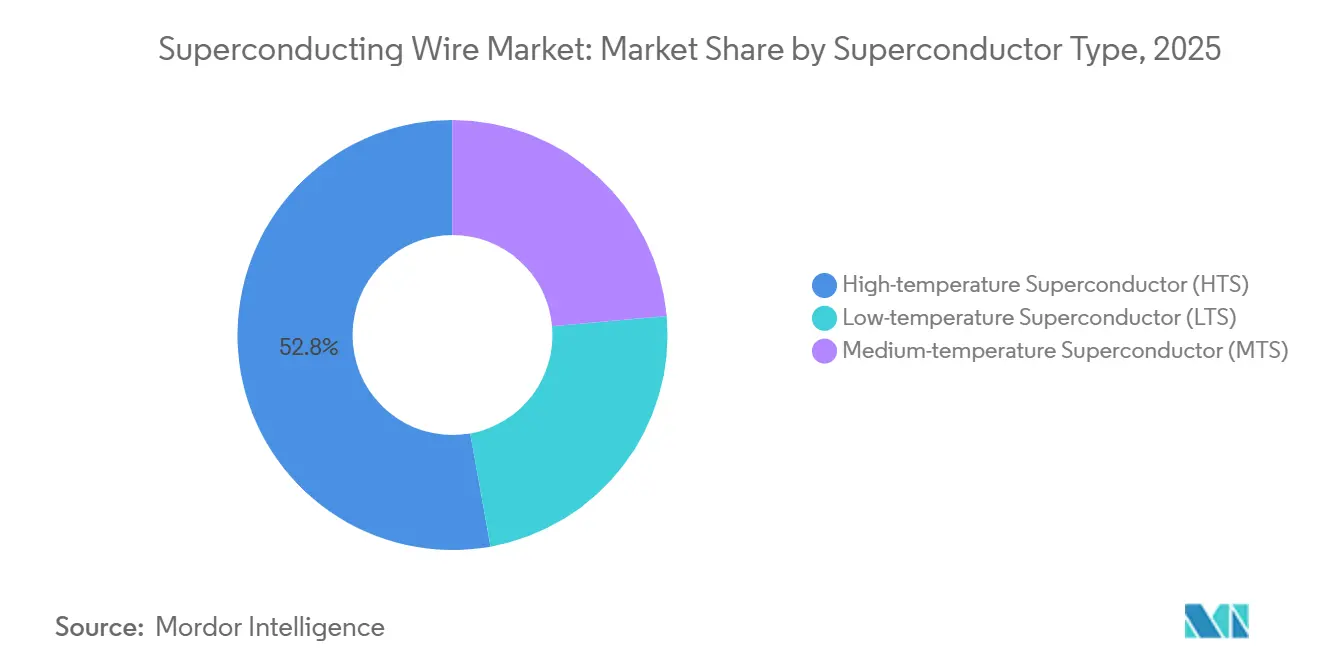

- By superconductor type, High-temperature superconductor (HTS) held 52.82% of the Superconducting wire market size in 2025 and is projected to grow at a 10.82% CAGR through 2031.

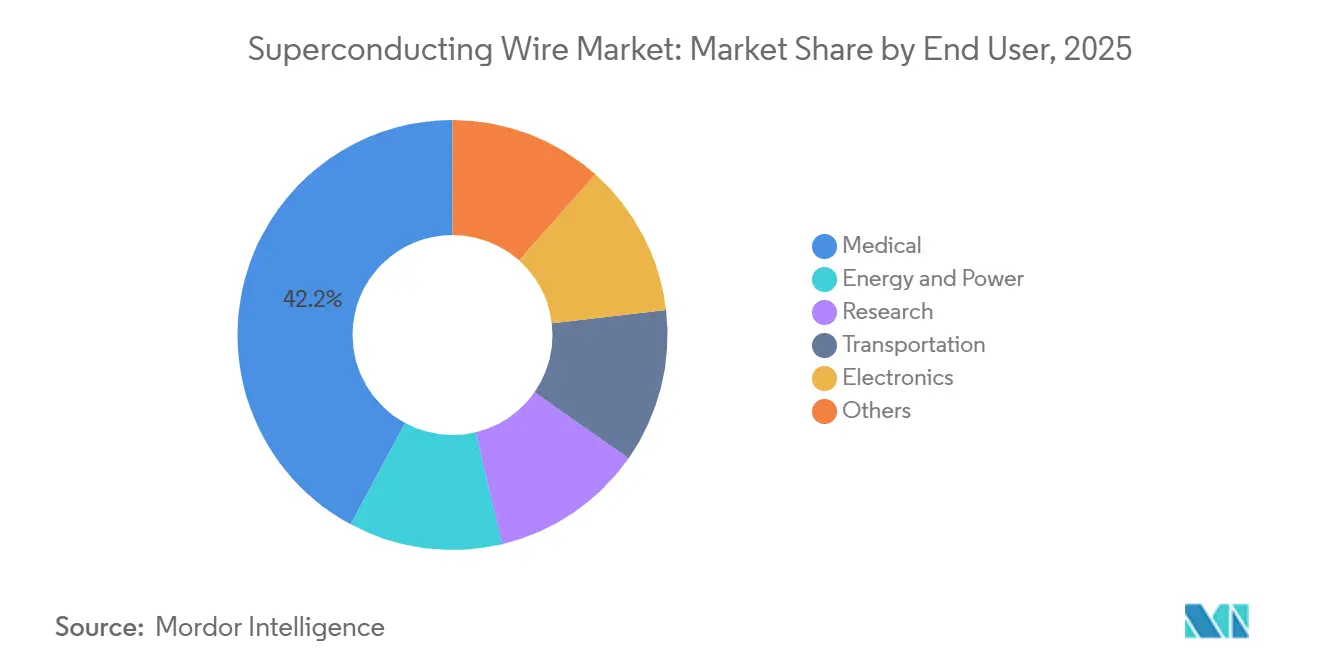

- By end user, medical held 42.15% of global revenue in 2025, while energy and power are expected to record the highest CAGR at 10.51% through 2031.

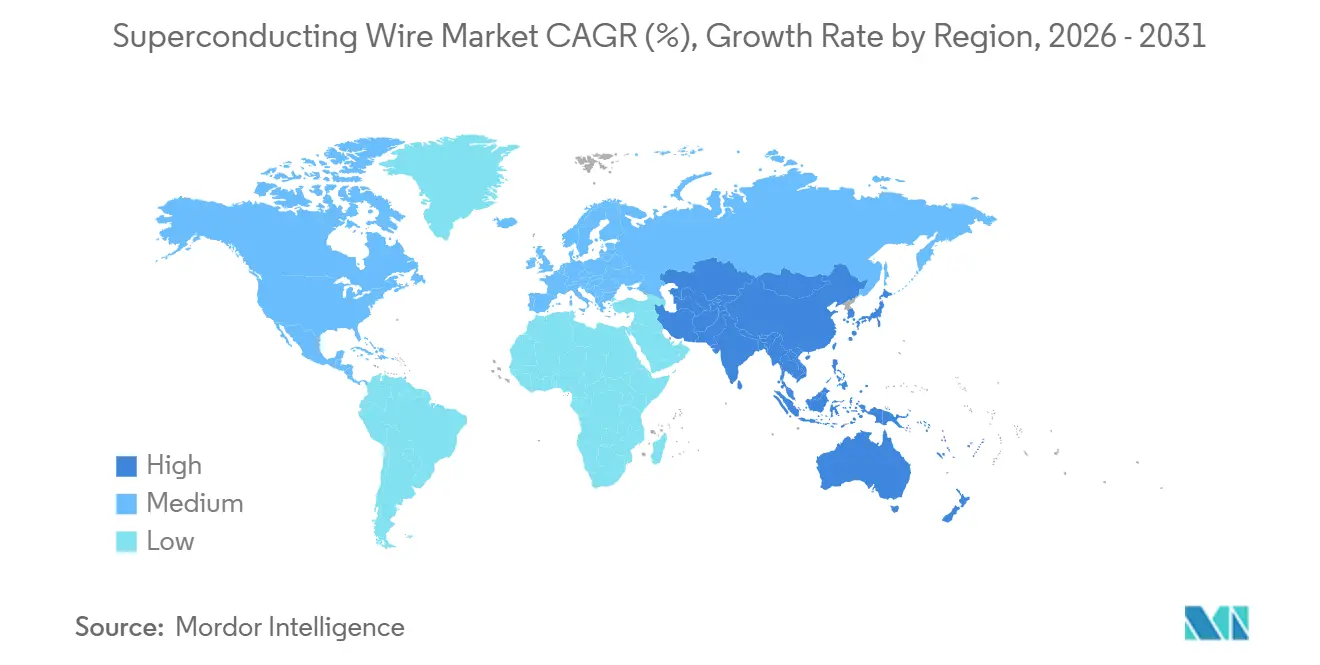

- By geography, Asia-Pacific held 38.65% of revenue in 2025 and is also forecast to post the fastest regional CAGR at 9.81% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Superconducting Wire Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| MRI Installed-Base Upgrade and Shift to Higher-Field, Helium-Free Magnet Platforms | +1.2% | Global, concentrated in North America, Western Europe, and East Asia | Medium term (2-4 years) |

| Grid Modernization and Urban High-Temperature Superconductor (HTS) Cable Deployment for Renewable Integration | +0.9% | Europe, North America, and China | Long term (≥ 4 years) |

| Fusion and High-Field Magnet Programs Driving Large-Volume HTS Procurement | +0.8% | Global, with project hubs in the United Kingdom, the United States, Japan, and Italy | Long term (≥ 4 years) |

| Hyperscale Data Center Adoption of HTS Busbars and Cabling for Artificial Intelligence (AI) Workloads | +0.6% | North America, Europe, and East Asia | Short term (≤ 2 years) |

| Electric Aviation and Next-Generation Cryogenic Propulsion Systems | +0.5% | North America and Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

MRI Installed-Base Upgrade and Transition to Higher-Field, Helium-Free Magnet Platforms

Medical imaging provides dependable demand for the superconducting wire market, with growth increasingly driven by upgrades within the installed base rather than by scanner count alone. The transition from 1.5 tesla to 3.0 tesla platforms increases wire content per magnet assembly and tightens performance requirements for field stability in persistent mode. Helium-free magnet development is also changing product specifications, as newer systems require conductors that perform reliably under revised cooling architectures. In January 2026, Bruker secured USD 500 million in multi-year agreements with two global healthcare companies to supply high-performance superconductors for next-generation MRI systems, indicating that procurement is shifting toward program-based commitments. This pattern provides the superconducting wire market with a more stable demand floor and reduces short-term volatility that is more common in project-driven applications.

Grid Modernization and Urban HTS Cable Deployment to Integrate Renewable Energy

The superconducting wire market is gaining utility relevance as dense urban networks require additional capacity without the delays and costs associated with new rights-of-way. NKT's 15-kilometer, 110-kV SuperLink cable system in Munich completed extensive testing in 2025, demonstrating that HTS cables can transmit more than 500 MW within a standard distribution corridor. In November 2025, Nexans joined the SupraMarine consortium to develop a high-voltage alternating current (HVAC) superconducting subsea transmission demonstrator for offshore wind links, with testing planned by 2028[1]U.S. Department of Energy Office of Scientific and Technical Information, “Process Innovations for High Temperature Superconducting (HTS) Wire Manufacturing,” DOE OSTI, osti.gov . These programs move the superconducting wire market away from isolated pilots and toward planned infrastructure projects with formal delivery schedules. The policy environment in Europe further supports this direction, as renewable integration targets and corridor congestion are pushing utilities toward solutions that add power capacity within existing footprints.

Fusion and High-Field Magnet Programs are Driving Large-Volume HTS Procurement

Fusion procurement is shaping the upper end of the superconducting wire market, as commercial developers require qualified wire in long lengths and cannot rely on laboratory-scale supply. The Fusion Industry Association reported that fusion-sector procurement spending increased 24% in 2025, with 75% of fusion suppliers making capacity investments ranging from USD 30,000 to USD 65 million. In February 2025, Commonwealth Fusion Systems and Type One Energy signed a licensing agreement granting Type One Energy exclusive rights to use CFS HTS cable technology for stellarator fusion magnets. The superconducting wire market now has a premium tier where pricing is determined by in-field critical current, mechanical strain tolerance, and piece-length consistency, rather than price alone. The U.S. Department of Energy's October 2025 fusion roadmap provides suppliers with a clearer federal demand horizon, reducing the risk associated with adding capacity for future orders.

Hyperscale Data-Center Adoption of HTS Busbars and Cabling for AI-Driven Workloads

The superconducting wire market has opened a new demand channel in data center power distribution, as AI facilities require higher current capacity within compact electrical layouts. In 2025, Microsoft stated that high-temperature superconductors were being evaluated as a practical option for data center power systems rather than as a research-only concept. A 2026 IEEE study found that an HTS tape busbar design for a 10-MW data center could reach cost parity with conventional AC layouts after five years, driven by lower cooling and transmission-loss costs. In April 2026, Tokamak Energy and The BE Company reported that replacing copper with HTS in data center power distribution could reduce power losses by up to 90% at the busway level and free up up to 9% of additional IT capacity per facility. This combination of energy savings, space efficiency, and commercial relevance gives the superconducting wire market a shorter-cycle demand channel compared to fusion or grid infrastructure.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Conductor Unit Costs and Cryogenic Balance-Of-Plant Expenses | -1.0% | Global, most acute in price-sensitive markets across South and Southeast Asia and South America | Medium term (2-4 years) |

| Scale-Up Yield and Quality Consistency Challenges in REBCO Tape Manufacturing | -0.7% | Global, most acute in North America and Europe, where domestic High-Temperature Superconductor (HTS) capacity remains limited | Medium term (2-4 years) |

| Lumpy, Project-Led Procurement Cycles Between Program Awards | -0.5% | Global, especially in fusion and grid cable geographies | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Conductor Unit Costs and Cryogenic Balance-Of-Plant Expenses Limit Deployment Outside Capital-Project Settings

The superconducting wire market faces a cost barrier, as technically proven systems are often difficult to justify economically once the full cryogenic package is included. The U.S. Department of Energy's manufacturing improvement program targets an HTS wire cost below USD 50 per kiloampere-meter; however, technical analysis presented in 2025 indicated that even this level remains more than 10 times above the threshold required for broad grid deployment[2]Nexans, “SupraMarine Consortium to Launch an Innovation Project Connecting Distant Offshore Wind Farms to Land,” Nexans Press Release, nexans.com . Cost pressure does not stem solely from the wire, as cryocoolers, vacuum-jacketed conduits, and liquid nitrogen handling add significant capital and operating costs to each installation. This limits much of the superconducting wire market to applications where performance offers a clear premium, such as MRI, fusion, or targeted grid upgrades, rather than broad network replacement. Helium supply concentration also remains a concern for low-temperature superconductor (LTS)-based applications, adding procurement risk for hospitals and infrastructure planners that require predictable lifecycle costs.

Scale-Up Yield and Quality Consistency Challenges in Rare Earth Barium Copper Oxide (REBCO) Tape Manufacturing Restrict Volume Production Capacity

Manufacturing scale remains a constraint in the superconducting wire market, as output growth is only viable when reel lengths and current performance remain consistent across commercial deliveries. Research presented in 2025 indicated that global HTS production capacity would need to increase from 3,000-5,000 kilometers per year to more than 20,000 kilometers per year to support a single compact fusion system at commercial scale. The same research found that volume expansion alone would deliver only a 3.6-fold reduction in unit cost, indicating that process improvements are still required to reach target economics. Furukawa Electric launched a New Energy and Industrial Technology Development Organization (NEDO) project in October 2025 to improve the precision of multifilament wire manufacturing and to complete prototyping and evaluation of a 4-layer SCSC-IFB assembled HTS conductor by March 2026, demonstrating that suppliers are addressing this bottleneck. Until yield improves at commercial throughput, the superconducting wire market will continue to face a gap between demand visibility and practical supply availability.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Superconductor Type: HTS Consolidates Dual Leadership in Share and Growth Rate

HTS held 52.82% of the superconducting wire market share in 2025 and is expected to grow at a 10.82% CAGR through 2031, making it both the largest and fastest-growing conductor category in the superconducting wire market. This position is driven by structural demand in fusion magnets, urban cable systems, and data center busbars, where higher operating temperatures and stronger field performance support use cases that LTS cannot serve as efficiently. The segment is centered on REBCO and YBCO, with first-generation BSCCO tapes still relevant in selected applications where system design and qualification paths are already established. SuperPower, Fujikura, and SuNam are investing in fusion-grade products, and SuperPower stated in 2025 that its FM-grade wire was targeting stronger critical current performance at 20 K and 20 tesla, which aligns with high-field demand in the superconducting wire industry. This technical capability gives HTS a stronger pricing position than standard conductor classes when buyers are procuring for performance-critical programs.

LTS remains relevant in the superconducting wire market because NbTi wire is deeply embedded in clinical MRI manufacturing, and existing OEM qualifications reduce the short-term case for replacement. MTS, led by magnesium diboride wire, is building a position in the superconducting wire industry where intermediate-temperature cooling offers a practical cost balance for specialized systems. NASA awarded Hyper Tech Research a Small Business Innovation Research (SBIR) contract in 2024 to advance fine-filament MgB2 wire for high-power-density aircraft motors, which supports the long-range electric aviation theme associated with this category. Across all three material classes, IEC TC90 standardization is becoming increasingly important as documented performance consistency shapes public-sector and program-led procurement requirements in the superconducting wire market.

By End User: Medical Anchors Volume While Energy and Power Redefine the Growth Trajectory

Medical accounted for 42.15% of the superconducting wire market in 2025, indicating that hospitals and radiology suppliers remain the largest demand base. This position rests on the global installed base of MRI systems, where higher-field upgrades in North America and Western Europe are occurring alongside first-generation capacity additions in South and Southeast Asia. The result is a broad procurement mix that supports both mature Low Temperature Superconductor (LTS) products and selected high-performance conductors for helium-free magnet designs. Research demand remains smaller but steady, as accelerator and laboratory programs procure through disciplined multi-year cycles that provide suppliers with clearer planning visibility. Transportation, electronics, and other end uses are still at earlier stages of commercial development, yet they hold potential where power density, system footprint, and thermal limits are prioritized over lowest upfront cost.

Energy and power are expected to grow at a 10.51% CAGR through 2031, making it the fastest-growing end-user segment in the superconducting wire market. This growth is tied to projects in urban cable transmission, renewable integration, and fault-management infrastructure where conventional solutions face space and thermal constraints. The Munich SuperLink project and the SupraMarine offshore demonstrator illustrate how this end-user segment is moving from research validation to planned network investment. This shift reduces the superconducting wire market's dependence on medical demand and provides High Temperature Superconductor (HTS) producers with a larger route to scale if system costs continue to improve.

Geography Analysis

Asia-Pacific held 38.65% of the superconducting wire market share in 2025 and is expected to expand at a 9.81% CAGR through 2031, making it both the largest and fastest-growing regional market. Japan supports this position through its established producer base, led by Sumitomo Electric, Fujikura, and Furukawa Electric, and through the long-term Chuo Shinkansen superconducting maglev program. JR Central stated in 2025 that the project cost had exceeded JPY 7 trillion (USD 48 billion), which keeps transportation-related superconducting development prominent across the regional supply chain. China is scaling domestic Rare Earth Barium Copper Oxide (REBCO) tape production to reduce reliance on imported High-Temperature Superconducting (HTS) material, while South Korea continues to build manufacturing capacity for cable and tape applications. Hyosung TNC's March 2026 partnership with CAN Superconductors indicates that Korean firms are expanding capacity domestically and positioning for direct access to the European market.

North America and Europe account for a significant share of the highest-value HTS procurement in the superconducting wire market, as both regions combine fusion funding, advanced medical Original Equipment Manufacturer (OEM) activity, and grid demonstration programs. In the United States, the Department of Energy (DOE) fusion roadmap published in October 2025 provides a multi-decade investment framework that supports long-range demand planning for wire suppliers. AMSC reported in May 2026 that its 12-month order backlog exceeded USD 280 million and quarterly revenue topped USD 85 million, reflecting strong institutional demand for advanced power infrastructure in North America. Europe remains relevant through Germany's SuperLink project, the United Kingdom's fusion programs, and France's role in the SupraMarine consortium and broader research networks. Public grid and clean energy programs in both regions support higher-value procurement, even as purchase cycles remain uneven.

South America, the Middle East, and Africa remain smaller contributors to the superconducting wire market, though demand profiles vary across these regions. Brazil and Argentina are more closely linked to research demand and early grid-resilience work than to large-scale commercial cable deployment. Saudi Arabia and the UAE are investing in advanced energy infrastructure, creating a potential pathway for superconducting applications, although the technology has not yet become a direct budget line in most current utility programs. South Africa adds a research-driven demand base through the Square Kilometre Array project and related specialized superconducting components, while much of the rest of the region remains tied primarily to imported medical imaging systems rather than domestic manufacturing or grid projects.

Competitive Landscape

The superconducting wire market is moderately consolidated in low-temperature products, with broader fragmentation in high-temperature products, creating a split competitive structure across the value chain. Japanese suppliers, particularly Sumitomo Electric, Fujikura, and Furukawa Electric, hold strong positions in NbTi output due to long qualification histories with medical OEM customers and integrated production capabilities that newer entrants have not yet matched. The HTS segment is more dispersed, with suppliers in the United States, South Korea, China, Russia, Germany, and other parts of Europe competing on current density, reel length, and application-specific qualification rather than solely on price. This distinction is significant because buyers in fusion and grid projects are now including tighter technical conditions in procurement, thereby protecting experienced suppliers that can demonstrate repeatable in-field performance. It also means the market still offers room for mid-tier producers that can extend piece lengths beyond 300 meters without compromising quality consistency.

Recent strategic moves indicate that competition in the superconducting wire market is shifting toward application breadth as much as installed volume. Bruker's January 2026 multi-year MRI supply agreements show how established suppliers are securing program-based demand around helium-free and next-generation magnet platforms rather than relying on shorter purchasing cycles. Furukawa Electric and Tokamak Energy announced in June 2026 that they were advancing collaboration on high-temperature superconducting (HTS) tape capability in the United Kingdom, pointing to closer alignment between wire development and fusion program requirements. Hyunsung TNC's March 2026 partnership with CAN Superconductors further illustrates that suppliers are using cross-border production and R&D ties to secure market access and build regional supply flexibility. These moves suggest that the next competitive layer in the market will be shaped by which suppliers can qualify across medical, fusion, grid, and data center applications without losing manufacturing discipline.

A second competitive filter is forming around process control, standards compliance, and the ability to manage uneven order timing. Rare Earth Barium Copper Oxide (REBCO) producers that can document stable output, maintain certified quality systems, and supply full-length reels with repeatable current performance will hold an advantage as procurement processes become more formal. International Electrotechnical Commission Technical Committee 90 (IEC TC90) standardization supports this trend, as shared test language reduces information gaps between established suppliers and newer entrants. At the same time, project-led buying continues to create long demand gaps between major awards, meaning balance sheet strength and customer mix will remain important even for technically capable participants. Overall, the superconducting wire market remains competitive on technology first, but procurement credibility is becoming equally important in winning large contracts.

Superconducting Wire Industry Leaders

Bruker

Sumitomo Electric Industries, Ltd.

Fujikura Ltd.

FURUKAWA ELECTRIC CO., LTD.

Luvata

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Hyunsung TNC (South Korea) entered a strategic partnership and R&D service agreement with CAN Superconductors s.r.o. (Czech Republic), a European HTS materials manufacturer. The agreement established a joint research and production hub to provide Hyunsung TNC direct access to the European market and the global superconducting materials supply chain.

- November 2025: Nexans formed the SupraMarine consortium with Air Liquide, CentraleSupélec, ITP Interpipe, and French grid operator RTE to develop an HVAC superconducting subsea power transmission system. The system is designed to connect offshore wind farms to the coast via HTS cables cooled by liquid nitrogen, with demonstrator testing planned by 2028, targeting the commercialization of subsea HTS transmission at industrial scale.

Global Superconducting Wire Market Report Scope

Superconducting wires are specialized electrical conductors that exhibit zero electrical resistance when cooled below their critical temperatures. They carry significantly higher current densities than copper, making them suitable for high-field medical imaging, large-scale scientific research, and compact urban power transmission.

The superconducting wires market is segmented by superconductor type, end user, and geography. By superconductor type, the market is segmented into low-temperature superconductor (LTS), medium-temperature superconductor (MTS), and high-temperature superconductor (HTS). By end user, the market is segmented into medical, energy & power, research, transportation, electronics, and others. The report also covers the market size and forecasts for superconducting wires in 18 countries across major regions. The market sizes and forecasts are provided in terms of value (USD).

| Low-temperature Superconductor (LTS) |

| Medium-temperature Superconductor (MTS) |

| High-temperature Superconductor (HTS) |

| Medical |

| Energy & Power |

| Research |

| Transportation |

| Electronics |

| Others |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Rest of Middle-East and Africa |

| By Superconductor Type | Low-temperature Superconductor (LTS) | |

| Medium-temperature Superconductor (MTS) | ||

| High-temperature Superconductor (HTS) | ||

| By End User | Medical | |

| Energy & Power | ||

| Research | ||

| Transportation | ||

| Electronics | ||

| Others | ||

| By Geography | Asia-Pacific | China |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is current market size of Superconducting Wire Market?

The superconducting wire market was valued at USD 1.62 billion in 2025 and is estimated to grow from USD 1.70 billion in 2026 to USD 2.18 billion by 2031, at a CAGR of 5.10% during the forecast period 2026 to 2031.

Which conductor type leads revenue and growth?

HTS leads both, with 52.82% revenue share in 2025 and a projected 10.82% CAGR through 2031.

Why does medical imaging remain so important for demand?

Medical accounted for 42.15% of revenue in 2025 because MRI systems remain the largest installed base, and the shift to higher-field and helium-free magnets is increasing wire requirements.

What is driving the fastest end-user expansion?

Energy and power are growing fastest at a 10.51% CAGR through 2031 because utilities are testing and planning HTS cable systems to enhance urban grid capacity and integrate renewables.

Page last updated on: