Super High Frequency Communication Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 3.46 Billion |

| Market Size (2030) | USD 7.54 Billion |

| Growth Rate (2025 - 2030) | 16.87% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Super High Frequency Communication Market Analysis by Mordor Intelligence

The Super High Frequency Communication market reached USD 3.46 billion in 2025 and is forecast to register a 16.87% CAGR, increasing the market size to USD 7.54 billion by 2030. The commercialization of the 24 GHz – 57 GHz spectrum, modernization of Ka-band military radar, rapid rollouts of low-earth-orbit (LEO) constellations, and AI-optimized beamforming chipsets are reinforcing demand curves across telecommunications, defense, automotive, and security verticals. Early regulatory approvals for millimeter-wave backhaul, particularly in North America and the Asia Pacific, cut deployment lead times and underpin private-sector capital expenditure. Equipment vendors gain cost advantages by migrating to highly integrated SiGe and GaN processes, while network operators unlock new revenue pools by layering value-added services over dense small-cell grids. These factors, alongside rising automotive radar mandates and smart-factory connectivity, position the Super High Frequency Communication market for sustained double-digit expansion through the decade.

Key Report Takeaways

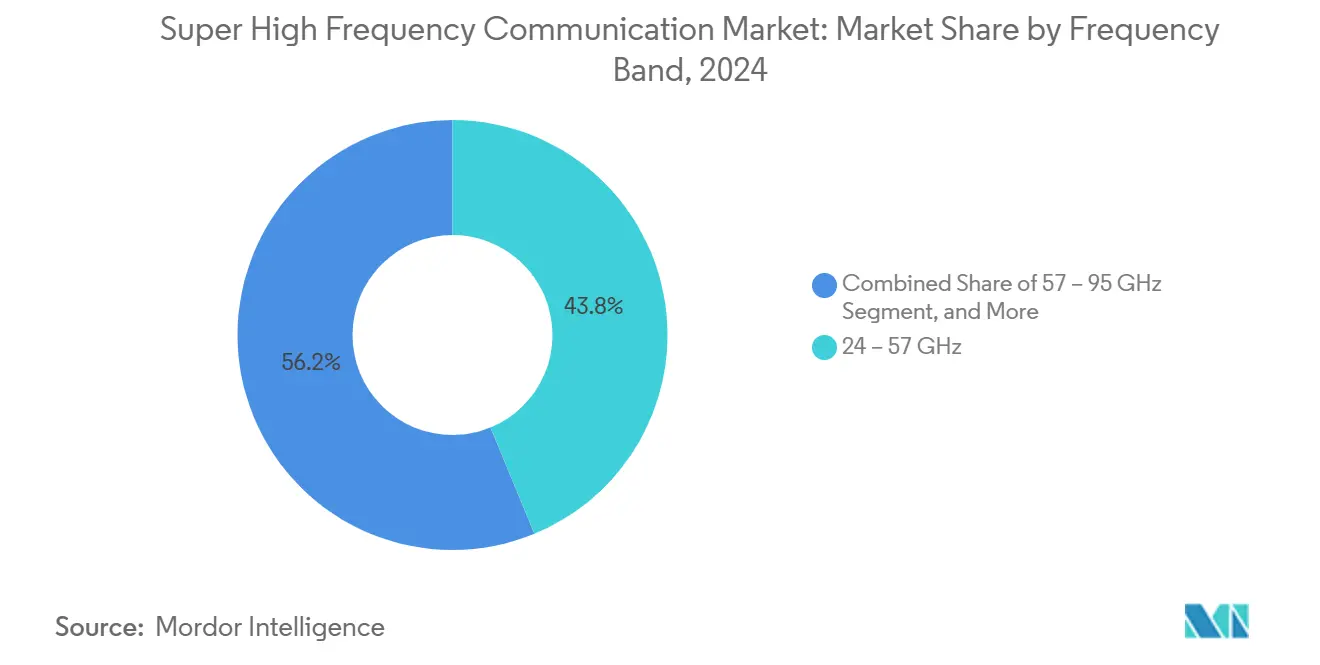

- By frequency band, 24 GHz – 57 GHz systems led with a 43.78% share of the Super High Frequency Communication market in 2024, while 57 GHz – 95 GHz platforms are projected to advance at a 17.16% CAGR through 2030.

- By component, antennas and transceiver modules accounted for a 39.73% share of the Super High Frequency Communication market size in 2024; communication and networking subsystems are set to grow at the fastest rate, with a 17.36% CAGR.

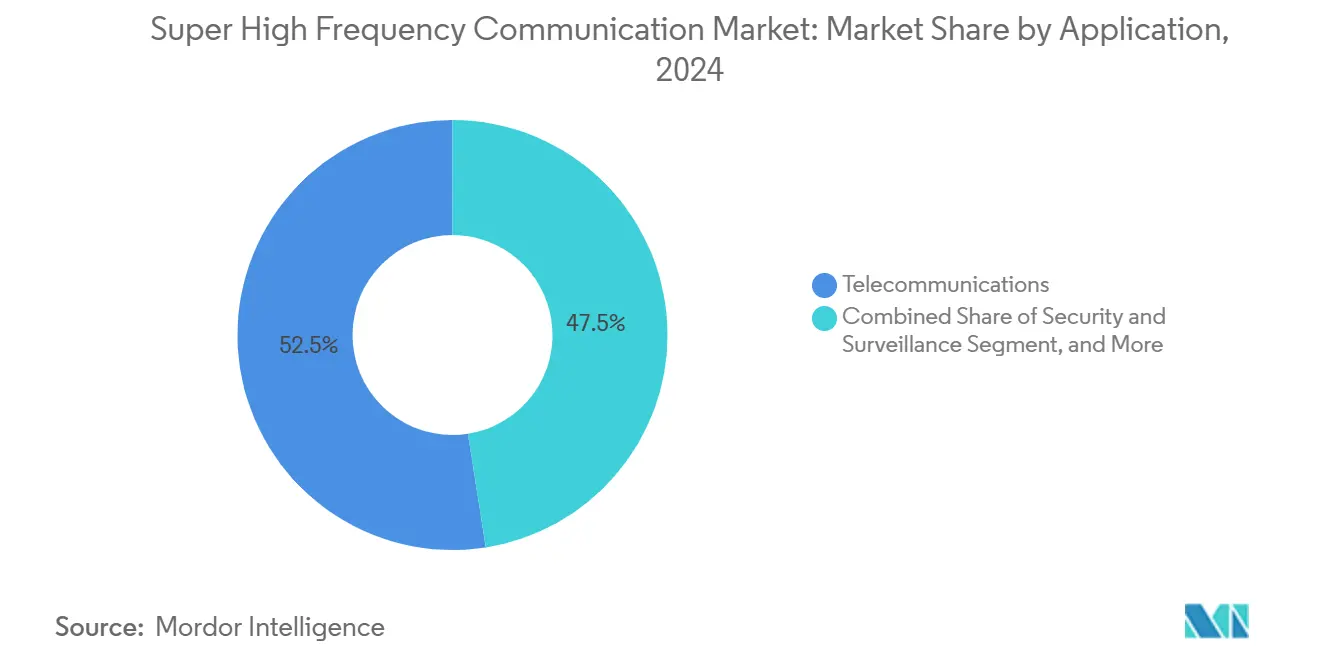

- By application, telecommunications dominated with a 52.47% share of the Super High Frequency Communication market size in 2024, whereas security and surveillance use cases are poised to expand at a 17.57% CAGR between 2025 and 2030.

- By end-user industry, aerospace and defense held a 49.82% share of the Super High Frequency Communication market size in 2024, while automotive and transportation exhibit the highest forecast growth at a 17.49% CAGR through 2030.

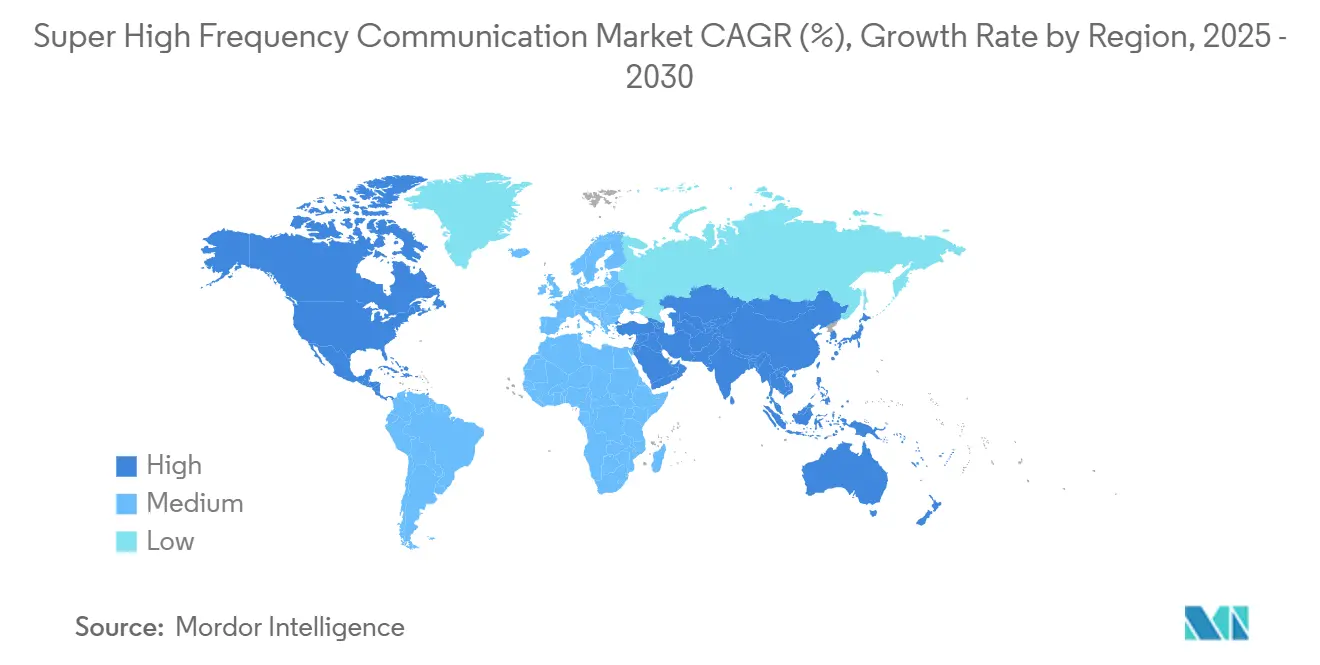

- By geography, North America captured a 35.71% share of the Super High Frequency Communication market size in 2024; the Asia Pacific is projected to grow at a 17.78% CAGR through 2030.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Super High Frequency Communication Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| 24 GHz – 57 GHz Spectrum Commercialization | +3.2% | North America, Asia Pacific | Medium term (2-4 years) |

| Defense-Grade Ka-Band Radar Modernization | +2.8% | North America, Europe | Long term (≥ 4 years) |

| Low-Earth-Orbit Constellation Roll-outs | +4.1% | Global | Medium term (2-4 years) |

| AI-Optimized Beamforming Chipsets | +2.9% | Asia Pacific manufacturing hubs | Short term (≤ 2 years) |

| Private 5G Backhaul for Smart Factories | +1.8% | Asia Pacific, Europe, North America | Medium term (2-4 years) |

| Regulatory Fast-Tracking of 7 GHz – 24 GHz Bands | +2.3% | Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

24 GHz – 57 GHz Spectrum Commercialization

Mobile operators accelerated their procurement after regulators in South Korea, Australia, and Hong Kong released contiguous 26 GHz – 28 GHz blocks that support peak data rates of 10 Gbps.[1]Ministry of Science and ICT, “28 GHz Spectrum Policies for 5G,” msit.go.kr These commercial allocations shorten payback periods for small-cell densification and create a globally harmonized ecosystem that lowers unit costs. Device makers align their radio front-end roadmaps with these bands, allowing for faster time-to-market of enhanced mobile broadband and fixed-wireless access services.

Defense-Grade Ka-Band Radar Modernization

The U.S. Army commissioned the AN/TPY-4 radar in 2024, marking a shift to Ka-band sensors that provide finer target discrimination and reduced susceptibility to jamming.[2]U.S. Army, “AN/TPY-4 Radar Deployment,” army.mil NATO programs and Indo-Pacific defense alliances mirror this trend, sparking multi-year procurement cycles for GaN-based transmit-receive modules, agile beam steering algorithms, and ruggedized processing units.

Low-Earth-Orbit Constellation Roll-outs

SpaceX surpassed 5,000 active Starlink satellites in 2024, driving a surge in demand for Ka-band ground terminals and V-band inter-satellite links.[3]SpaceX, “Starlink Satellite Constellation Status,” spacex.com OneWeb, Kuiper, and regional operators are increasing their capacity needs, prompting phased-array antenna suppliers to scale up production. The constellation model requires continuous replenishment, providing recurring hardware and service revenue over the forecast period.

AI-Optimized Beamforming Chipsets

Qualcomm’s Snapdragon X80 integrates machine-learning routines that adapt beam patterns in real-time, cutting power draw by 30% while increasing link reliability in dense urban deployments. Vendors embed similar intelligence into small-cell radios and satellite modems, unlocking efficiency gains that translate directly into opex savings for network operators.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Atmospheric and Rain Fade Above 20 GHz | -2.1% | Tropical and high-precipitation regions | Long term (≥ 4 years) |

| Acute RF Engineering Talent Shortage | -1.4% | North America, Europe | Medium term (2-4 years) |

| Short Product Life-Cycles and Rapid Obsolescence | -1.8% | Global | Short term (≤ 2 years) |

| High Initial CAPEX for Dense Small-Cell Networks | -1.9% | Urban markets in developed economies | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Atmospheric and Rain Fade Above 20 GHz

Studies by the IEEE Communications Society found 60 GHz links can lose 15-25 dB/km during tropical downpours. Operators install adaptive modulation and redundant routing, but these measures escalate capital and operational costs. The challenge remains acute for fixed backhaul and high-throughput satellite links where path diversity options are limited.

Acute RF Engineering Talent Shortage

An IEEE MTT-S survey reported that 78% of firms struggled to hire senior millimeter-wave designers in 2024, with vacancies remaining open for an average of eight months. The scarcity slows prototype cycles and inflates salary baselines, pushing smaller vendors to outsource design or form academic partnerships that lengthen product roadmaps.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Frequency Band: Higher Bands Drive Innovation

The 24 GHz – 57 GHz segment accounted for the largest share, accounting for 43.78% of the Super High Frequency Communication market size in 2024. Established allocations, proven propagation models, and volume handset demand keep this tier commercially dominant. In contrast, 57 GHz – 95 GHz platforms, fueled by unlicensed spectrum, are expected to record the fastest expansion at a 17.16% CAGR through 2030. Automotive radar, high-density backhaul, and short-range fiber-substitution links are driving this growth, with vendors utilizing wide 7 GHz contiguous channels to achieve multi-gigabit throughput. Above 95 GHz, nascent opportunities in terahertz scanning and secure point-to-point links emerge, but restrictive device physics and fragmented regulation temper near-term uptake. The evolutionary ladder thus progresses methodically, with ecosystem maturity cascading from lower to higher bands.

The Super High Frequency Communication market benefits from advances in frequency-agnostic semiconductor technology, notably in GaN-on-SiC power amplifiers, which increase efficiency across multiple frequency bands. Licensing frameworks such as the FCC’s 2024 experimental rules encourage early-stage terahertz trials. Coupled with the growth of university consortia, these policies seed a pipeline of innovation that should crystallize into commercial offerings beyond the forecast horizon.

By Component: Communication Systems Lead Growth

Antennas and transceiver blocks retained 39.73% of revenue in 2024, reflecting their ubiquity across every deployment scenario. Yet, communication and networking subsystems, layered with software-defined features, outpace other categories at a 17.36% CAGR, as network operators demand flexible radios that pivot across three to four separate millimeter-wave bands. Ericsson’s 2024 Massive-MIMO millimeter-wave platform highlights the convergence of beamforming, MIMO, and AI-driven link adaptation within a single enclosure.

Frequency sources, including low-phase-noise oscillators, gain relevance as higher-order QAM schemes tighten error budgets. Imaging components, although niche, are rising steadily with the growth of airport body scanners and industrial non-destructive testing. Integrated design shrinks bill-of-materials counts, and foundries transition to 90 nm and 45 nm SiGe nodes for volume RFIC production, further compressing cost curves.

By Application: Security Applications Accelerate

Telecommunications still account for 52.47% of 2024 revenue; however, security and surveillance installations are forecast to grow at a 17.57% CAGR, reflecting heightened protection of critical infrastructure. The U.S. Department of Homeland Security certified next-generation body scanners in 2024, demonstrating the superiority of millimeter-wave imaging over conventional X-ray alternatives. Radar and satellite communications continue to absorb defense budgets, while imaging and scanning migrate from laboratories to production lines, enabling sub-millimeter fault detection.

Multi-application convergence becomes pronounced as base-station vendors bundle perimeter-security functions into cellular hardware, and airports deploy shared antenna arrays for both passenger screening and narrowband telemetry. These synergies broaden addressable use cases, driving incremental hardware demand without proportional site-acquisition costs.

By End-User Industry: Automotive Transformation Accelerates

Aerospace and defense comprised a 49.82% share in 2024; nonetheless, automotive and transportation are growing at a 17.49% CAGR as safety regulators mandate 77 GHz collision-avoidance radar. The European Commission’s automatic emergency braking rule, effective from 2024, transformed millimeter-wave sensors from premium options to baseline equipment. Japanese automakers push 79 GHz imaging radar to refine lane-level navigation in autonomous prototypes.

Industrial plants utilize 60 GHz position sensors for robotic guidance, while healthcare providers are exploring terahertz spectroscopy for non-invasive diagnostics. Cross-industry technology transfer accelerates when automotive volume drives down component pricing, benefiting defense and industrial segments. Conversely, ruggedized military innovations in phased arrays trickle into civilian vehicular platforms, reinforcing continuous improvement loops.

Geography Analysis

North America maintained leadership with 35.71% of 2024 revenue, propelled by USD 2.8 billion U.S. Department of Defense allocations for next-generation Ka-band radar. Aggressive private-sector investment in LEO ground infrastructure complements defense demand, creating a diversified revenue base. Canada’s NORAD modernization and Mexico’s fixed-wireless programs provide incremental tailwinds, even as spectrum-sharing rules expedite commercial rollouts.

Europe trails in growth yet exhibits robust vertical depth driven by ESA-funded Ka-band upgrades for Galileo satellites and Germany’s 77 GHz automotive radar clusters. Fragmented national regulations previously hindered adoption, but the 2025 ETSI harmonization is expected to streamline licensing. Scandinavian vendors leverage long-standing microwave heritage to export to Middle Eastern defense clients and Latin American telecom operators.

Asia Pacific is forecast to post the highest 17.78% CAGR, fueled by China’s deployment of more than one million millimeter-wave base stations by late 2024. South Korea’s USD 1.2 billion 6G test-bed sponsorship and Japan’s automotive radar mandates position the region as both a demand center and manufacturing powerhouse. India’s Ka-band rural-connectivity ground stations extend addressable markets beyond megacities, while Australia ties defense-grade 26 GHz systems into naval modernization, diversifying regional revenue streams.

Competitive Landscape

The Super High Frequency Communication market is moderately fragmented, with the top five suppliers accounting for approximately 55% of the global revenue. Telecommunications stalwarts such as Ericsson and Nokia capitalize on 5G millimeter-wave experience to penetrate adjacent security and industrial niches. Qualcomm dominates device chipsets, embedding tight RF-baseband integration that sets performance benchmarks.

Defense specialists L3Harris and Thales anchor high-margin radar and electronic-warfare segments, leveraging classified IP and long procurement cycles for durable returns. In 2024, L3Harris acquired an advanced phased-array antenna firm to solidify vertical integration, exemplifying a broader M&A trend targeting scarce RF talent and proprietary design libraries. In the test-and-measurement corner, Keysight, Rohde & Schwarz, and Anritsu are investing heavily in 110 GHz instrumentation to secure early 6G research customers.

Strategically, vendors pursue ecosystem partnerships: base-station makers bundle satellite backhaul, semiconductor fabless houses pair with OSATs for antenna-in-package manufacturing, and constellation operators co-design ground terminals with chipset suppliers. These alliances compress the time-to-revenue, optimize the bill of materials, and share risk across the value chain.

Super High Frequency Communication Industry Leaders

Anritsu Corporation

Aviat Networks Inc.

BridgeWave Communications Inc.

Ceragon Networks Ltd.

E-Band Communications LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: South Korea’s Ministry of Science and ICT finalized allocation of the 140 GHz band for nationwide 6G pilot networks, authorizing three carriers to build 500 experimental sites ahead of commercial spectrum auctions slated for 2027.

- July 2025: Qualcomm completed the USD 320 million acquisition of WaveCore Semiconductor, a U.S. developer of gallium-nitride power-amplifier dies optimized for 57 GHz-95 GHz backhaul radios, accelerating its roadmap for integrated millimeter-wave chipsets.

- April 2025: SpaceX initiated on-orbit validation of V-band inter-satellite laser links across 50 Starlink satellites, confirming sub-10 millisecond round-trip latency between ground terminals on separate continents.

- February 2025: Nokia introduced a 110 GHz small-cell prototype for pre-6G field trials, integrating a dual-band phased-array module that demonstrated 20 Gbps peak data rates during tests with two European mobile operators.

Global Super High Frequency Communication Market Report Scope

| 24 – 57 GHz |

| 57 – 95 GHz |

| 95 – 300 GHz |

| Antennas and Transceiver Components |

| Communication and Networking Components |

| Frequency Sources and Related Components |

| Imaging Components |

| Telecommunications |

| Radar and Satellite Communication Systems |

| Imaging and Scanning Systems |

| Security and Surveillance |

| Aerospace and Defence |

| Automotive and Transportation |

| Industrial and Manufacturing |

| Healthcare |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| By Frequency Band | 24 – 57 GHz | ||

| 57 – 95 GHz | |||

| 95 – 300 GHz | |||

| By Component | Antennas and Transceiver Components | ||

| Communication and Networking Components | |||

| Frequency Sources and Related Components | |||

| Imaging Components | |||

| By Application | Telecommunications | ||

| Radar and Satellite Communication Systems | |||

| Imaging and Scanning Systems | |||

| Security and Surveillance | |||

| By End-User Industry | Aerospace and Defence | ||

| Automotive and Transportation | |||

| Industrial and Manufacturing | |||

| Healthcare | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Key Questions Answered in the Report

How large is the Super High Frequency Communication market in 2025?

The market stands at USD 3.46 billion in 2025 with a 16.87% CAGR through 2030.

Which frequency band holds the greatest revenue share?

The 24 GHz – 57 GHz tier commands 43.78% of 2024 revenue thanks to mature 5G ecosystems.

What is the fastest-growing application area?

Security and surveillance use cases, expanding at a 17.57% CAGR as critical-infrastructure protection intensifies.

Which region is expected to grow the quickest?

Asia Pacific leads with a forecast 17.78% CAGR, buoyed by large-scale 5G and automotive radar deployments.

Who are the leading companies?

Ericsson, Nokia, Qualcomm, L3Harris, and Thales rank among top suppliers, together holding about 55% of global revenue.

What limits millimeter-wave adoption?

Atmospheric rain fade and a shortage of experienced RF engineers remain the primary technical and resource barriers.

Page last updated on: