Sunflower Seed (Seed For Sowing) Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 1.22 Billion |

| Market Size (2031) | USD 1.60 Billion |

| Growth Rate (2026 - 2031) | 5.63% CAGR |

| Fastest Growing Market | Europe |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Sunflower Seed (Seed For Sowing) Market Analysis by Mordor Intelligence

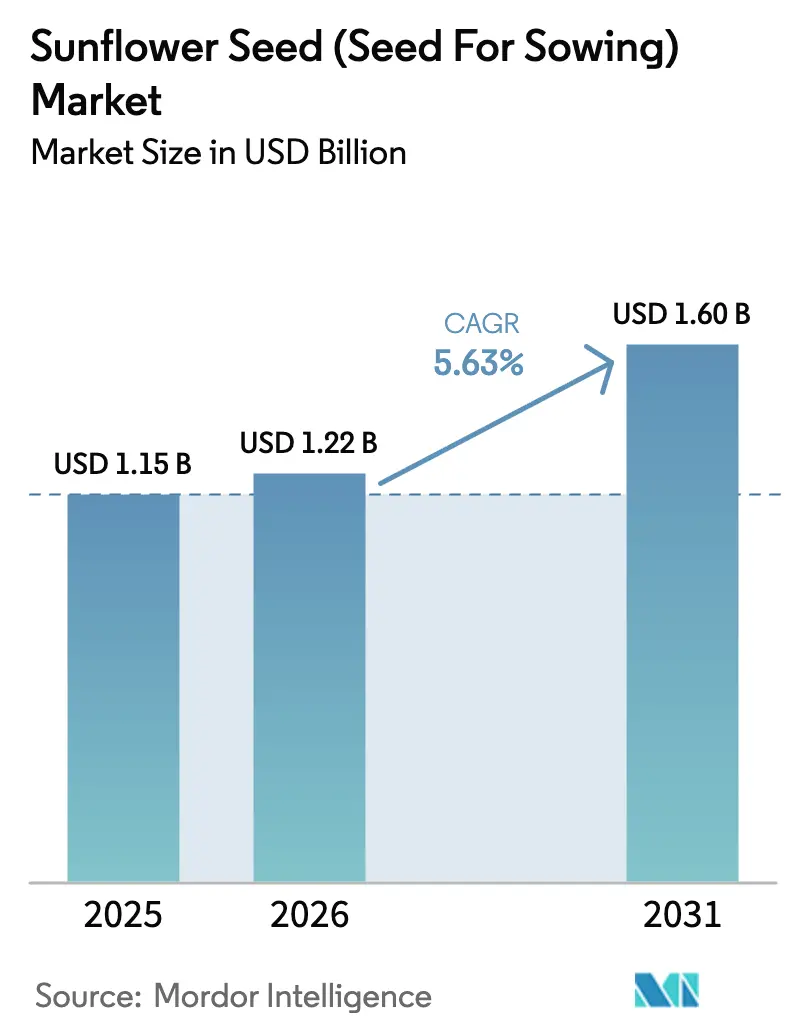

The sunflower seed (seed for sowing) market size is projected to expand from USD 1.15 billion in 2025 and USD 1.22 billion in 2026 to USD 1.60 billion by 2031, registering a CAGR of 5.63% between 2026 and 2031. Growth is anchored in Europe, where the Common Agricultural Policy eco-schemes reward certified seed use, while refiners across France, Spain, and Germany lock in long-term contracts for high-oleic sunflower oil that meets Renewable Energy Directive II thresholds. Drought-prone regions in Africa, the Middle East, and South Asia are also pivoting acreage toward sunflowers because the crop requires less irrigation than soybeans, shortens crop cycles by 2 to 3 weeks, and fits into double-cropping rotations. Multinational breeders answer that pull with non-transgenic hybrids stacking resistance to Sclerotinia head rot, Orobanche parasitism, and imidazolinone herbicide, giving growers a yield premium and access to premium biodiesel markets. At the same time, digital-traceability platforms link each seed lot to verified low-carbon field data, allowing producers to sell greenhouse-gas credits alongside commodity output and thus de-risk the switch from farm-saved to certified hybrid seed.

Key Report Takeaways

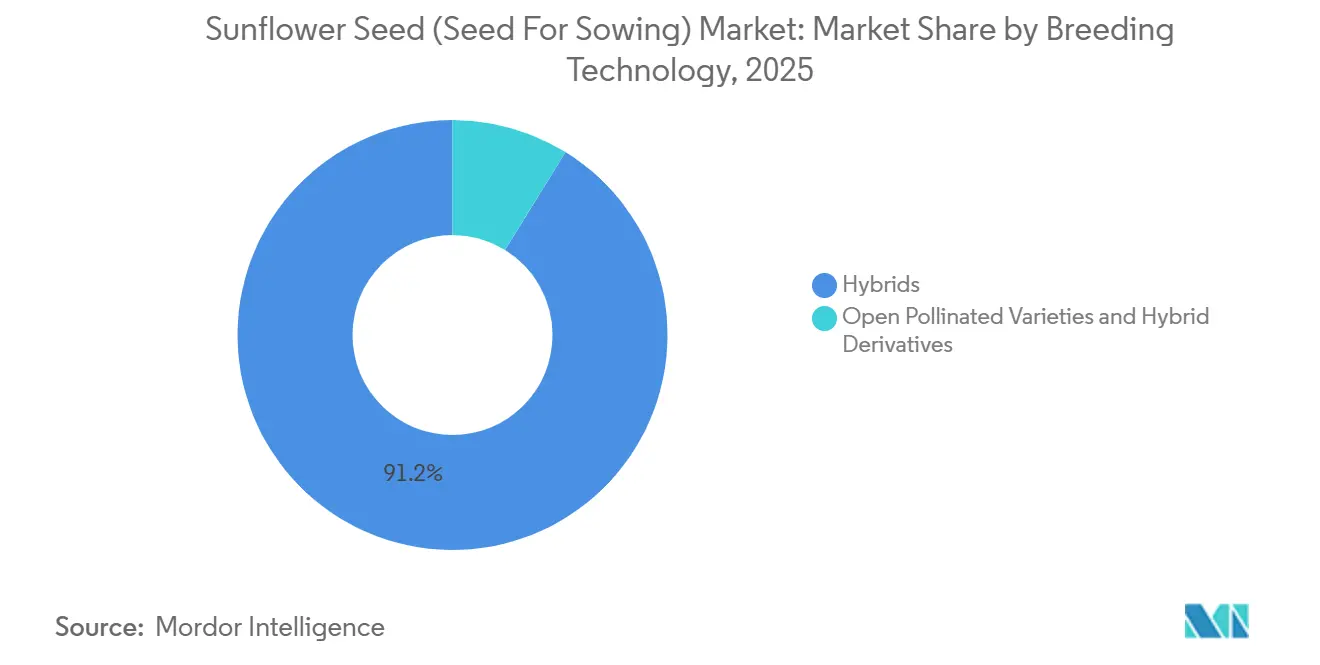

- By breeding technology, hybrids led with 91.2% of the sunflower seed (seed for sowing) market share in 2025 and are advancing at a 5.7% CAGR through 2031.

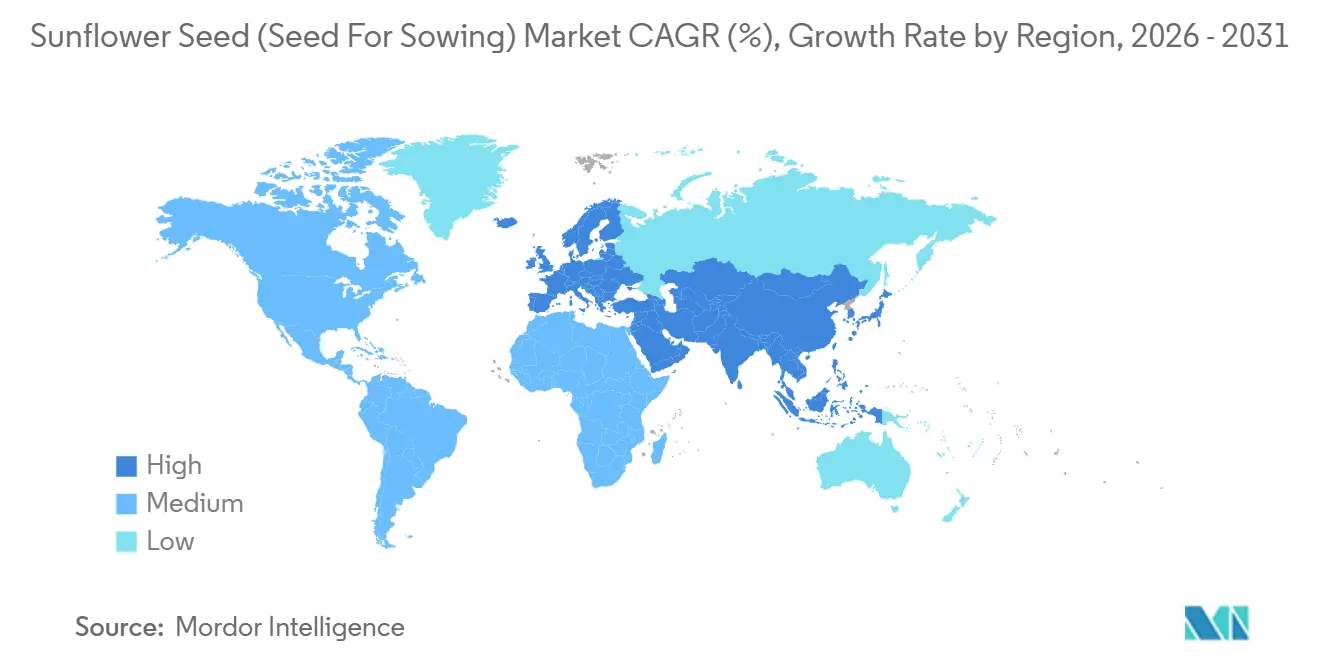

- By geography, Europe accounted for 48.6% of the sunflower seed (seed for sowing) market size in 2025 and is projected to post the fastest regional CAGR of 6.3% to 2031.

- Nufarm Limited (Nuseed), Euralis Semences S.A.S. (Euralis Group), Corteva Agriscience, Land O'Lakes, Inc., and KWS SAAT SE & Co. KGaA (KWS Group) accounted for significant revenue in the market in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Sunflower Seed (Seed For Sowing) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising adoption of hybrid sunflower seed in commercial farming | +1.0% | Europe, North America, and Argentina | Medium term (2-4 years) |

| Expansion of acreage in drought-prone regions favoring sunflower | +0.9% | Sub-Saharan Africa, Middle East, and South Asia | Long term (≥ 4 years) |

| Growth of contract farming models with input financing for certified seed | +0.8% | India, Pakistan, Kenya, and Tanzania | Medium term (2-4 years) |

| Surge in regenerative-agriculture certifications demanding hybrids | +0.9% | European Union, Brazil, and Argentina | Short term (≤ 2 years) |

| Digitally traceable seed lot identifiers enabling carbon-credit stacking | +0.6% | United States, European Union, and Australia | Long term (≥ 4 years) |

| Government mandates boost demand for high-oleic sunflower oil | +0.4% | France, Germany, and Canada | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Adoption of Hybrid Sunflower Seed in Commercial Farming

Growers in Romania, France, and the United States are transitioning from open-pollinated lines to hybrids that enhance oil yield and reduce fungicide applications by two sprays. These hybrids offer improved agronomic performance, making them a preferred choice for farmers aiming to optimize productivity. Breeders utilize marker-assisted selection and gamma-ray mutagenesis to combine disease resistance with imidazolinone tolerance, improving weed control and reducing input costs. Hybrid adoption in Romania is projected to increase by 2025, supported by Common Agricultural Policy payments for certified seed usage, which incentivize the use of advanced seed technologies. As this technology expands eastward into Ukraine and westward into Spain, manufacturers are accelerating product release cycles to every 18 months, fostering grower loyalty and ensuring recurring royalty revenues. This rapid innovation cycle allows manufacturers to address evolving grower needs and maintain a competitive edge in the market.

Expansion of Acreage in Drought-Prone Regions Favoring Sunflower

Sunflower cultivation is an important agricultural industry worldwide, with the European Union (EU) among the leading producers. In the United States, in 2025, the planted area reached 1.29 million acres, a 79% increase from the previous year. The harvested area also rose by 82% from 2024, reaching 1.25 million acres. North Dakota, the top sunflower-producing state in 2025, harvested 1.09 billion pounds, marking a 111% increase from 2024. In the same period, North Dakota's planted area grew by 89%, and yield improved by 206 pounds to 1,958 pounds per acre[1]Source: National Sunflower Association, "USDA Releases Report on Big 2025 Sunflower Crop,'' sunflowernsa.com. This significant growth in North Dakota's sunflower production can be attributed to favorable weather conditions, advancements in farming techniques, and increased adoption of high-yield seed varieties. Government subsidies for hybrid seed costs are planned to be implemented by 2027. These policy measures are projected to support long-term growth, particularly as climate models forecast increasing rainfall variability across the Sahel and the Indian subcontinent. The subsidies aim to enhance farmers' access to improved seed varieties, which are more resilient to changing climatic conditions, thereby boosting productivity and ensuring food security in the region.

Growth of Contract Farming Models with Input Financing for Certified Seed

Seed companies and crushers combine hybrid seeds, micro-loans, and guaranteed off-take agreements, reducing smallholder working capital requirements. These initiatives aim to address financial constraints faced by smallholders, enabling them to access better-quality seeds and improve productivity. In Punjab, Pakistan, Advanta Seeds provides credit seed packs through village agents and deducts repayments at harvest, minimizing defaults and ensuring financial sustainability. This model not only supports smallholders in managing their financial risks but also promotes the adoption of advanced agricultural practices. Similarly, Kenya’s East African Grain Council has adopted this tripartite model, connecting growers with two regional crushers. This approach has significantly enhanced hybrid seed adoption, doubling within three seasons, thereby improving agricultural output, farmer incomes, and the overall efficiency of the agricultural value chain.

Digitally Traceable Seed Iot Identifiers Premium Carbon-Credit Stacking

Bayer AG is implementing blockchain tags on individual seed bags in Germany, connecting planting data to satellite-verified emissions. This initiative enables the generation of soil-carbon credits, providing farmers with an opportunity to monetize sustainable practices. By linking planting data with verified emissions, Bayer AG aims to enhance transparency and traceability in agricultural operations. This approach not only supports farmers in adopting environmentally friendly practices but also aligns with global efforts to reduce agricultural carbon footprints. With the European Union's Carbon Border Adjustment Mechanism set to impose penalties on unverified imports starting in 2028, this traceability offers a potential safeguard against future tariffs while promoting accountability and sustainability in agricultural supply chains[2]Source: Directorate-General for Energy, “Renewable Energy Directive Targets and Rules,” energy.ec.europa.eu Drivers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Price volatility of competing oilseed crops reducing seed budgets | −0.9% | Global | Short term (≤ 2 years) |

| Challenges in phytosanitary rules for seed imports and field isolation | −0.6% | Europe, Asia, and Africa | Medium term (2-4 years) |

| Farm-saved seeds limiting commercial seed adoption | −0.7% | Africa, and South Asia | Long term (≥ 4 years) |

| Stricter rules on micro-plastic seed coatings | −0.3% | Europe and prospective adoption in North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Price Volatility of Competing Oilseed Crops Reducing Seed Budgets

Soybean futures fluctuated due to drought in Brazil and logistical disruptions in the Black Sea region. These factors pressured sunflower profit margins and led to acreage adjustments in North Dakota and Buenos Aires. The drought in Brazil significantly impacted soybean yields, reducing supply and driving price volatility in the global market. Simultaneously, the Black Sea logistics issues disrupted the transportation of agricultural commodities, further intensifying market instability. As a result, growers delayed hybrid-seed purchases, forcing distributors to offer late-season discounts, which eroded profit margins and added financial strain to the supply chain.

Stricter Rules on Micro-Plastic Seed Coatings

The European Chemicals Agency mandates that coatings biodegrade within 5 years, prompting BASF SE and Corteva Agriscience to adopt starch- or chitosan-based matrices. This transition increases the per-unit seed price and reduces shelf life from 18 months to 12 months[3]Source: European Chemicals Agency, "Microplastics Restriction Proposal," echa. europa.eu. The regulatory requirement has significant implications for the seed treatment market, as companies must balance compliance with maintaining product affordability and effectiveness. Additionally, the shift to biodegradable coatings requires further research and development to ensure these new materials meet performance standards while adhering to environmental regulations. Similarly, consultations initiated in Canada in 2025 introduce regulatory uncertainty, hindering investment in next-generation treatments and creating challenges for market participants aiming to innovate while adhering to evolving standards.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Breeding Technology: Hybrids Dominate Commercial Adoption

Hybrids were the largest breeding technology, capturing 91.2% of the sunflower seed (seed for sowing) market in 2025, advancing fastest at a 5.7% CAGR through 2031. Their dominance is attributed to higher yields, broad disease resistance, and high-oleic oil content, which qualifies for biodiesel premiums. This transition was driven by the development of reliable cytoplasmic male-sterility (CMS) systems and restorer genes, enabling large-scale commercial hybrid production. Modern hybrids are specifically bred for genetic resistance to major threats such as downy mildew, sunflower rust, and the parasitic weed broomrape. Annually, numerous hybrids are released by public and private institutions, with over 45 introduced in India alone. The shift from open-pollinated varieties to hybrids has significantly contributed to the global increase in sunflower productivity. Additionally, hybrids have been instrumental in meeting the growing demand for sunflower oil, which is widely used in food processing, cosmetics, and biodiesel production. Their adaptability to diverse agro-climatic conditions has further strengthened their market position.

Open-pollinated varieties and hybrid derivatives, including farmer-saved F2 seeds and landraces, are primarily used in smallholder systems in sub-Saharan Africa and South Asia, where seed replacement rates remain low. According to the International Crops Research Institute for the Semi-Arid Tropics, open-pollinated sunflower varieties are preferred in countries like Tanzania and Kenya because they enable seed saving, reducing input costs compared to hybrids. These varieties are also valued for their resilience in low-input farming systems, making them a practical choice for resource-constrained farmers in these regions.

Geography Analysis

Europe is the largest geography, accounting for 48.6% of the sunflower seed (seed for sowing) market value in 2025 and is forecast to accelerate at a 6.3% CAGR through 2031, supported by the Common Agricultural Policy eco-payments, which help reduce certified seed costs. Spain, France, and Romania collectively account for a significant share of sunflower cultivation, as refiners secure high-oleic feedstock through long-term take-or-pay agreements. According to the United States Department of Agriculture, Russia has the highest sunflower seed production globally in the 2024/2025 crop year, with an estimated output of approximately 6.7 million metric tons. Ukraine is also a significant producer, with a projected production volume of around 5.6 million metric tons during the 2024/2025 period.

North and South America collectively contributed significantly to market demand. According to the United States Department of Agriculture, Argentina’s sunflower market is undergoing notable expansion, with expectations for continued growth into marketing year 2025/26. The sunflower planted area has been revised to 2.65 million hectares in 2025, an increase of 600,000 hectares from the previous forecast and 450,000 hectares above the previous year. This growth is driven by strong farmer interest and favorable market conditions, with part of the new planting area replacing soybean cultivation[4]Source: Foreign Agriculture Service, "Argentina: Oilseeds and Products Update," fas.usda.gov. In Brazil, an increase in the biodiesel blend has prompted growers in Mato Grosso and Goiás to incorporate sunflower into their soybean-corn rotations.

Asia-Pacific, the Middle East, and Africa collectively account for the remaining market share. Government subsidies in India and Iran have reduced hybrid seed prices, making them more accessible to farmers and encouraging their adoption. These subsidies have played a crucial role in promoting the use of hybrid seeds, thereby supporting agricultural development. Furthermore, contract farming models in Kenya and Tanzania have significantly improved certified seed penetration, doubling it over three seasons. This development has contributed to increased agricultural productivity, enhanced the overall efficiency of farming practices, and strengthened the supply chain in these regions.

Competitive Landscape

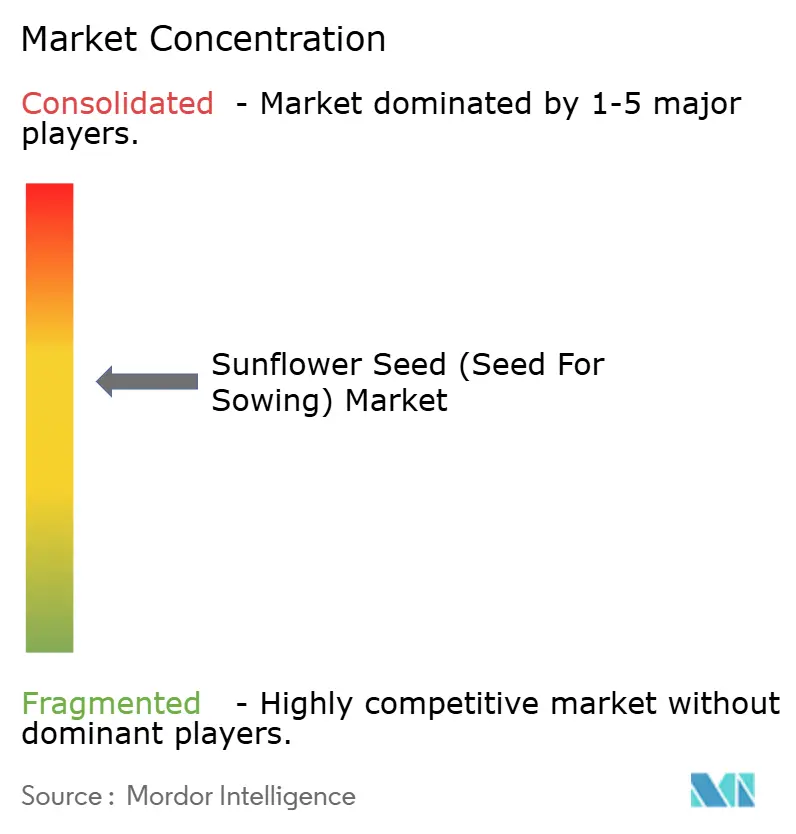

The market is moderately consolidated, with the top five players, Nufarm Limited (Nuseed), Euralis Semences S.A.S. (Euralis Group), Corteva Agriscience, Land O'Lakes, Inc., and KWS SAAT SE & Co. KGaA (KWS Group), accounting for significant revenue in the market in 2025. The companies leveraging multi-location breeding hubs and digital agronomy services that lock in farm-gate loyalty. Each launches new hybrids every 18 months, compressing trait life cycles and raising research and development barriers for smaller firms.

Mid-tier specialists such as KWS SAAT SE & Co. KGaA (KWS Group), Groupe Limagrain Holding S.A., and Euralis Semences S.A.S. (Euralis Group) exploit local germplasm libraries to tailor hybrids for Mediterranean and Danube Basin microclimates, often releasing varieties one season ahead of multinational rivals. Joint ventures with public institutes in Spain and Romania speed resistance-gene introgression and cut time-to-market.

Emerging disruptors in Africa and South Asia use contract farming and sachet-pack strategies to reach smallholders who are otherwise priced out of hybrids. Seed Co International Limited pilot blockchain traceability and carbon-credit stacking to create premium channels that bypass spot markets and buffer price risk for growers.

Sunflower Seed (Seed For Sowing) Industry Leaders

-

Euralis Semences S.A.S. (Euralis Group)

-

Corteva Agriscience

-

Land O'Lakes, Inc.

-

KWS SAAT SE & Co. KGaA (KWS Group)

-

Nufarm Limited (Nuseed)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Rusagro Group has announced the formation of a new joint venture, Solrost, in collaboration with Turkish businessman Sarikurt Bedirhan. The venture will focus on seed production, including sunflower seeds. By producing seeds internally, Rusagro seeks to reduce its dependence on external suppliers for key crops such as sunflowers, which are vital to its fat-and-oil business, its largest revenue-generating division.

- November 2025: Syngenta Group and LNZ Group have formed a strategic partnership for the long-term local production and exclusive distribution of sunflower and corn hybrids in Ukraine. Under this agreement, LNZ Group has obtained exclusive rights for the production and distribution of Syngenta Group’s NK Kondi sunflower hybrid.

- September 2025: KWS SAAT SE & Co. KGaA and Groupe Limagrain Holding S.A. finalized the sale of 100% ownership of AgReliant Genetics to GDM. AgReliant Genetics, a joint venture between KWS and Limagrain, specializes in the research, production, and sale of seeds, including sunflower seeds. This transaction marks a significant development in the seed industry, as GDM aims to strengthen its position in the North American market through this acquisition.

Global Sunflower Seed (Seed For Sowing) Market Report Scope

Sunflower seeds for sowing are the dried, mature fruits (achenes) of the sunflower plant (Helianthus annuus L.), chosen for their high germination rates, purity, and seedling vigor. These seeds feature a hard pericarp (hull) that encloses the kernel and are often treated to enhance resistance to soil-borne fungi, ensuring a robust field stand. The Sunflower Seed (Seed for Sowing) Market Report is Segmented by Breeding Technology (Hybrids and Open-Pollinated Varieties and Hybrid Derivatives), and by Geography (North America, Europe, Asia-Pacific, South America, the Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Metric Tons).

| Hybrids | Non-Transgenic Hybrids |

| Open-Pollinated Varieties and Hybrid Derivatives |

| North America | Canada |

| Mexico | |

| United States | |

| Rest of North America | |

| Europe | France |

| Germany | |

| Italy | |

| Netherlands | |

| Poland | |

| Romania | |

| Russia | |

| Spain | |

| Ukraine | |

| United Kingdom | |

| Rest of Europe | |

| Asia-Pacific | Australia |

| Bangladesh | |

| China | |

| India | |

| Indonesia | |

| Myanmar | |

| Pakistan | |

| Thailand | |

| Rest of Asia-Pacific | |

| South America | Argentina |

| Brazil | |

| Rest of South America | |

| Middle East | Iran |

| Turkey | |

| Rest of Middle East | |

| Africa | Egypt |

| Ethiopia | |

| Ghana | |

| Kenya | |

| Nigeria | |

| South Africa | |

| Tanzania | |

| Rest of Africa |

| By Breeding Technology | Hybrids | Non-Transgenic Hybrids |

| Open-Pollinated Varieties and Hybrid Derivatives | ||

| By Geography | North America | Canada |

| Mexico | ||

| United States | ||

| Rest of North America | ||

| Europe | France | |

| Germany | ||

| Italy | ||

| Netherlands | ||

| Poland | ||

| Romania | ||

| Russia | ||

| Spain | ||

| Ukraine | ||

| United Kingdom | ||

| Rest of Europe | ||

| Asia-Pacific | Australia | |

| Bangladesh | ||

| China | ||

| India | ||

| Indonesia | ||

| Myanmar | ||

| Pakistan | ||

| Thailand | ||

| Rest of Asia-Pacific | ||

| South America | Argentina | |

| Brazil | ||

| Rest of South America | ||

| Middle East | Iran | |

| Turkey | ||

| Rest of Middle East | ||

| Africa | Egypt | |

| Ethiopia | ||

| Ghana | ||

| Kenya | ||

| Nigeria | ||

| South Africa | ||

| Tanzania | ||

| Rest of Africa | ||

Market Definition

- Commercial Seed - For the purpose of this study, only commercial seeds have been included as part of the scope. Farm-saved Seeds, which are not commercially labeled are excluded from scope, even though a minor percentage of farm-saved seeds are exchanged commercially among farmers. The scope also excludes vegetatively reproduced crops and plant parts, which may be commercially sold in the market.

- Crop Acreage - While calculating the acreage under different crops, the Gross Cropped Area has been considered. Also known as Area Harvested, according to the Food & Agricultural Organization (FAO), this includes the total area cultivated under a particular crop across seasons.

- Seed Replacement Rate - Seed Replacement Rate is the percentage of area sown out of the total area of crop planted in the season by using certified/quality seeds other than the farm-saved seed.

- Protected Cultivation - The report defines protected cultivation as the process of growing crops in a controlled environment. This includes greenhouses, glasshouses, hydroponics, aeroponics, or any other cultivation system that protects the crop against any abiotic stress. However, cultivation in an open field using plastic mulch is excluded from this definition and is included under open field.

| Keyword | Definition |

|---|---|

| Row Crops | These are usually the field crops which include the different crop categories like grains & cereals, oilseeds, fiber crops like cotton, pulses, and forage crops. |

| Solanaceae | These are the family of flowering plants which includes tomato, chili, eggplants, and other crops. |

| Cucurbits | It represents a gourd family consisting of about 965 species in around 95 genera. The major crops considered for this study include Cucumber & Gherkin, Pumpkin and squash, and other crops. |

| Brassicas | It is a genus of plants in the cabbage and mustard family. It includes crops such as carrots, cabbage, cauliflower & broccoli. |

| Roots & Bulbs | The roots and bulbs segment includes onion, garlic, potato, and other crops. |

| Unclassified Vegetables | This segment in the report includes the crops which don’t belong to any of the above-mentioned categories. These include crops such as okra, asparagus, lettuce, peas, spinach, and others. |

| Hybrid Seed | It is the first generation of the seed produced by controlling cross-pollination and by combining two or more varieties, or species. |

| Transgenic Seed | It is a seed that is genetically modified to contain certain desirable input and/or output traits. |

| Non-Transgenic Seed | The seed produced through cross-pollination without any genetic modification. |

| Open-Pollinated Varieties & Hybrid Derivatives | Open-pollinated varieties produce seeds true to type as they cross-pollinate only with other plants of the same variety. |

| Other Solanaceae | The crops considered under other Solanaceae include bell peppers and other different peppers based on the locality of the respective countries. |

| Other Brassicaceae | The crops considered under other brassicas include radishes, turnips, Brussels sprouts, and kale. |

| Other Roots & Bulbs | The crops considered under other roots & bulbs include Sweet Potatoes and cassava. |

| Other Cucurbits | The crops considered under other cucurbits include gourds (bottle gourd, bitter gourd, ridge gourd, Snake gourd, and others). |

| Other Grains & Cereals | The crops considered under other grains & cereals include Barley, Buck Wheat, Canary Seed, Triticale, Oats, Millets, and Rye. |

| Other Fibre Crops | The crops considered under other fibers include Hemp, Jute, Agave fibers, Flax, Kenaf, Ramie, Abaca, Sisal, and Kapok. |

| Other Oilseeds | The crops considered under other oilseeds include Ground nut, Hempseed, Mustard seed, Castor seeds, safflower seeds, Sesame seeds, and Linseeds. |

| Other Forage Crops | The crops considered under other forages include Napier grass, Oat grass, White clover, Ryegrass, and Timothy. Other forage crops were considered based on the locality of the respective countries. |

| Pulses | Pigeon peas, Lentils, Broad and horse beans, Vetches, Chickpeas, Cowpeas, Lupins, and Bambara beans are the crops considered under pulses. |

| Other Unclassified Vegetables | The crops considered under other unclassified vegetables include Artichokes, Cassava Leaves, Leeks, Chicory, and String beans. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: IDENTIFY KEY VARIABLES: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the forecast years are in nominal terms. Inflation is not a part of the pricing, and the average selling price (ASP) is kept constant throughout the forecast period.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases, and Subscription Platforms