Subsea Fiber Backbone Network Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 8.21 Billion |

| Market Size (2031) | USD 12.30 Billion |

| Growth Rate (2026 - 2031) | 8.42% CAGR |

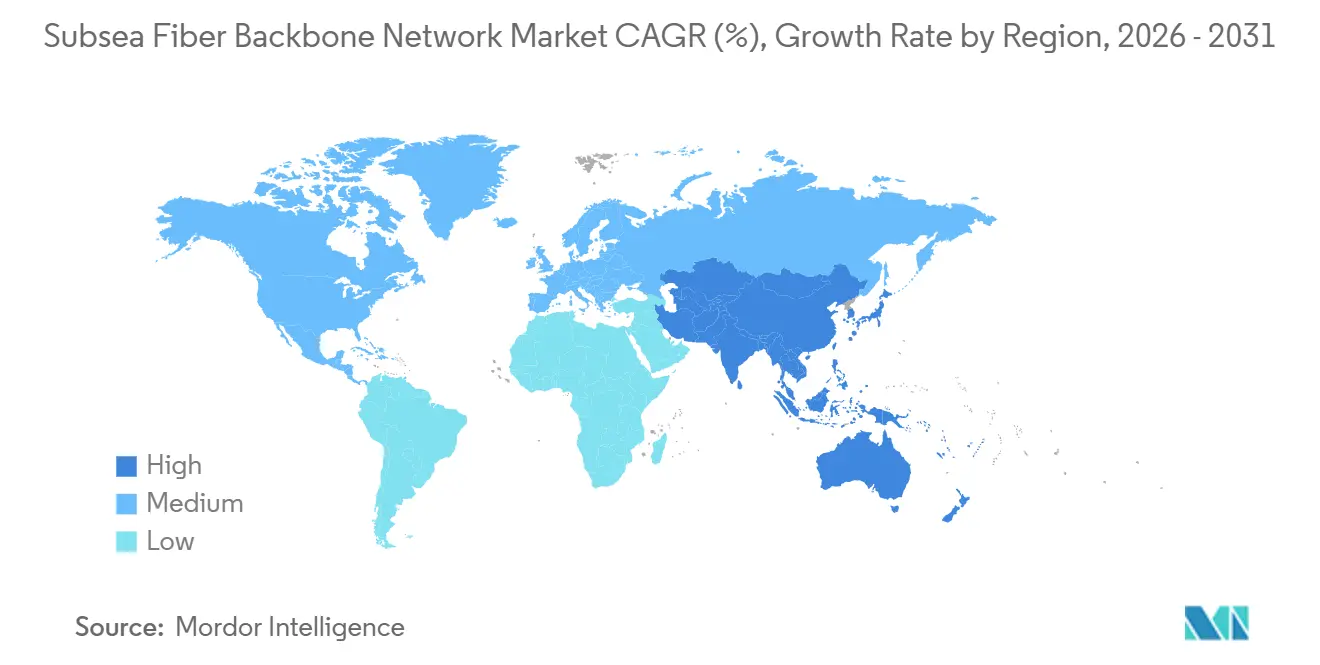

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

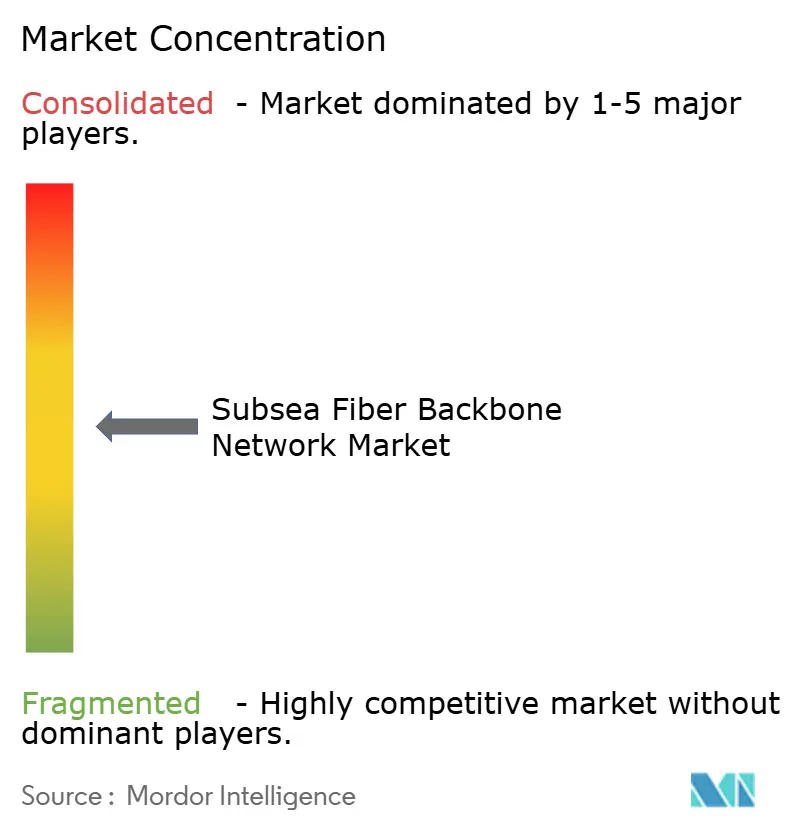

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Subsea Fiber Backbone Network Market Analysis by Mordor Intelligence

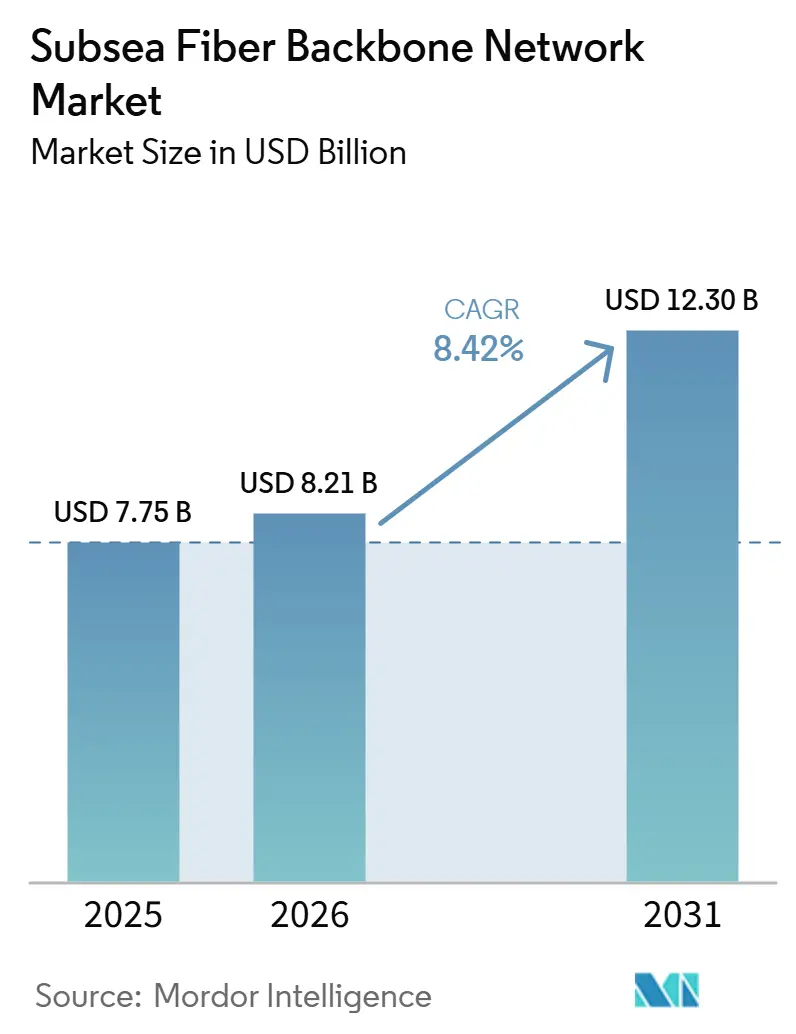

The Subsea Fiber Backbone Network Market size was valued at USD 7.75 billion in 2025 and estimated to grow from USD 8.21 billion in 2026 to reach USD 12.30 billion by 2031, at a CAGR of 8.42% during the forecast period (2026-2031). The subsea fiber backbone network market is being pushed by faster cross-border traffic growth from AI training, distributed inference, and multi-region cloud operations, which need low-latency capacity on long-haul routes. The subsea fiber backbone network market is also changing on the ownership side, because hyperscalers now fund more routes directly and use cables as performance assets rather than shared transport utilities. Security screening rules introduced across major Western markets in 2025 and 2026 are reshaping route planning, landing choices, and vendor qualification, which gives compliance-ready suppliers a clear advantage in the subsea fiber backbone network market. The subsea fiber backbone network market also faces tighter execution conditions because vessel availability, repair capacity, and permits now affect installation timing as much as cable demand does. This leaves the subsea fiber backbone network market with room to grow in sovereign connectivity, island links, and combined power-fiber projects, where private hyperscaler demand does not fully cover future requirements.

Key Report Takeaways

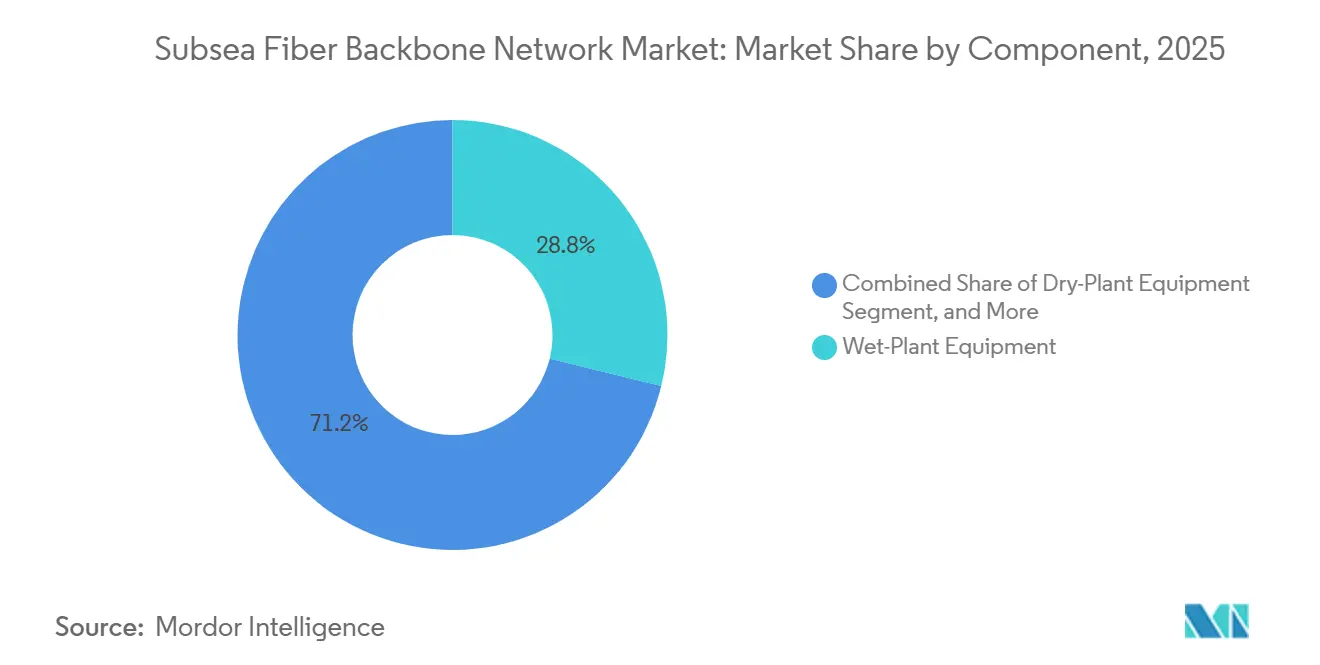

- By component, Wet-Plant Equipment held 28.82% share of the subsea fiber backbone network market size in 2025, while Auxiliary and Marine Services is projected to expand at a 9.41% CAGR through 2031.

- By cable type, Single-Mode Fiber accounted for 67.33% of the subsea fiber backbone network market size in 2025 and is also expected to record the highest CAGR at 8.78% through 2031.

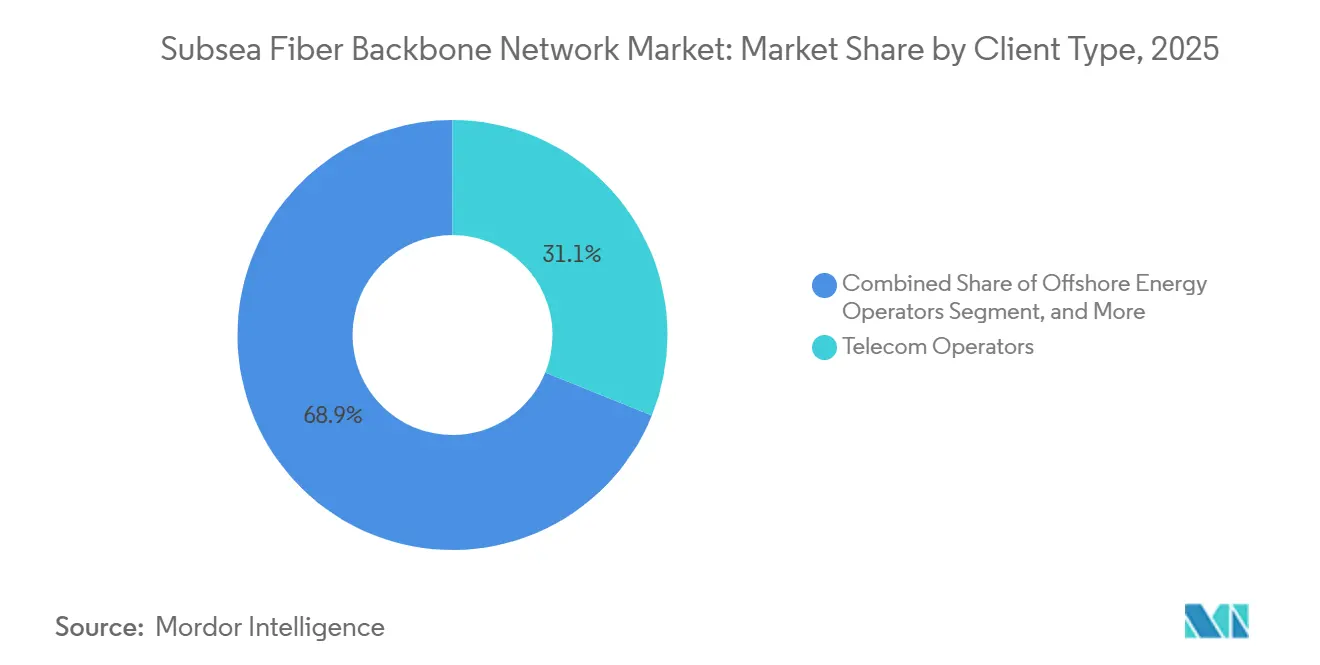

- By client type, Telecom Operators held 31.11% of the subsea fiber backbone network market share in 2025, while Content and Hyperscale Cloud Providers are projected to grow at a 10.10% CAGR through 2031.

- By ownership model, Consortium-Owned Networks held 25.12% of revenue in 2025, while Single-Owner Networks is expected to expand at a 10.42% CAGR through 2031.

- By geography, Asia-Pacific accounted for 30.12% of the subsea fiber backbone network market share in 2025 and is projected to advance at a 9.13% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Subsea Fiber Backbone Network Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Rising International Bandwidth Demand from Cloud and AI Traffic | +2.5% | Global | Short term (≤ 2 years) |

| Hyperscaler-Funded Route Ownership and Capacity Leasing | +1.8% | Global, concentrated in trans-Pacific and trans-Atlantic routes | Medium term (2-4 years) |

| Network Resilience Mandates and Redundancy Planning | +0.8% | North America and Europe | Medium term (2-4 years) |

| Offshore Energy and Remote-Island Connectivity Expansion | +0.6% | Europe (North Sea), Asia-Pacific core, spill-over to the Middle East and Africa | Long term (≥ 4 years) |

| Reuse of Retired Cable Infrastructure and Landing Assets | +0.4% | Global, with early gains in the Mediterranean and the North Atlantic | Short term (≤ 2 years) |

| Multi-Route Design to Reduce Geopolitical Single-Point Exposure | +0.5% | Asia-Pacific, with spill-over to the Middle East and Africa | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising International Bandwidth Demand from Cloud and AI Traffic

The subsea fiber backbone network market is seeing a different traffic pattern, as AI training and inference move large datasets between distant data centers rather than within a single region. According to the IEEE Communications Society, in January 2026, more than 570 in-service cables carried over 99% of international internet traffic, underscoring why changes in workload design now translate into material backbone demand.[1]IEEE Communications Society, “Fiber Optic Networks and Subsea Cable Systems as the Foundation for AI and Cloud Services,” IEEE Communications Society Technology Blog, techblog.comsoc.org This demand is not spreading evenly, because routes tied to fast digital adoption in Asia are absorbing more new traffic than mature corridors where installed capacity is already deeper. In the subsea fiber backbone network market, that uneven load is pushing capital toward undersupplied corridors and giving route diversity more value than another incremental upgrade on legacy lanes.

Hyperscaler-Funded Route Ownership and Capacity Leasing

The subsea fiber backbone network market is moving away from the older practice of shared ownership across many carriers and toward direct funding by cloud and content platforms. In June 2026, the IEEE Communications Society reported that hyperscalers held 75% of total international subsea bandwidth capacity by mid-2026 and were involved in over two-thirds of planned submarine cable deployments worldwide.[2]IEEE Communications Society, “Hyperscalers' Dominance of Subsea Cable Capacity to Increase in the AI Era,” IEEE Communications Society Technology Blog, techblog.comsoc.org Private ownership turns a cable into a performance asset because latency, routing control, and physical security become part of the service promise to enterprise and cloud users. That shift reduces the addressable wholesale opportunity for carrier-led consortium structures on the busiest ocean corridors. Within the subsea fiber backbone network market, suppliers that can deliver turnkey systems and satisfy security checks are gaining from longer contracts with a small group of very large buyers.

Network Resilience Mandates and Redundancy Planning

The subsea fiber backbone network market is also benefiting from resilience mandates that now treat submarine cables as critical infrastructure. The European Commission announced a EUR 347 million (USD 375 million) investment in submarine cable security in February 2026, paired with a Cable Security Toolbox and a list of Cable Projects of European Interest.[3]European Commission, “Commission Increases Submarine Cable Security with EUR 347 Million Investment and New Toolbox,” European Commission, ec.europa.eu The EU Critical Entities Resilience Directive requires member states to identify critical entities by July 2026 and explicitly covers submarine cable infrastructure within its risk and compliance framework. The Federal Communications Commission adopted a presumptive denial standard in August 2025 for foreign-adversary-linked cable applicants and restricted landings in designated foreign-adversary countries.[4]Federal Communications Commission, “FCC Fact Sheet, Review of Submarine Cable Landing License Rules,” Federal Communications Commission, docs.fcc.gov In the subsea fiber backbone network market, these measures are turning redundancy, vendor reviews, and route diversification into planned expenditures rather than optional safeguards.

Offshore Energy and Remote-Island Connectivity Expansion

The subsea fiber backbone network market is expanding beyond traditional telecom backbones, as offshore energy projects and island programs drive demand for integrated seabed infrastructure. Alcatel Submarine Networks received an Equinor contract in July 2025 for a DC/FO subsea control power and communications system for the Fram Sor field, indicating that power and fiber scopes are beginning to converge in a single project.[5]Alcatel Submarine Networks, “ASN Has Received the Contract Award for the Supply of a DC/FO Subsea Control Power and Communication Infrastructure for the Equinor Fram Sør Field,” Alcatel Submarine Networks, asn.com NEC completed the 2,250 km East Micronesia Cable System in May 2026, linking Micronesia, Kiribati, and Nauru with support from Australian and Japanese infrastructure programs. These island projects serve both broadband access and strategic presence, keeping them relevant even when commercial return profiles are weaker than on major cloud routes. In the subsea fiber backbone network market, this creates a new demand pool less exposed to hyperscaler concentration and broadens the types of buyers active in the supply chain.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| High Capital Intensity and Long Payback Cycles | -1.5% | Global | Long term (≥ 4 years) |

| Complex Cross-Border Permitting and Marine Survey Delays | -0.9% | Asia-Pacific core, the Middle East and Africa, with spill-over to Europe | Medium term (2-4 years) |

| Repair Vessel Scarcity and Prolonged Outage Risk | -0.7% | Global, with acute pressure in the Asia-Pacific | Short term (≤ 2 years) |

| Export Controls, Security Reviews, and Landing Restriction Risk | -0.5% | Asia-Pacific, North America routes | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Capital Intensity and Long Payback Cycles

The subsea fiber backbone network market still faces a financing barrier because intercontinental cable builds need very high upfront spending and long recovery periods. The input indicates that a single intercontinental route can require USD 200 million to USD 500 million in upfront investment and an 8-year to 15-year payback horizon, which narrows the field to large sponsors and consortia. This funding profile becomes more difficult when ship-day rates, survey costs, and armored cable requirements rise simultaneously. It also creates a timing problem, because optical technology continues to improve while capital is locked into assets that must recover value over many years. In the subsea fiber backbone network market, blended public-private financing is emerging, but it has not yet mitigated this restraint across the full project pipeline.

Complex Cross-Border Permitting and Marine Survey Delays

The subsea fiber backbone network market also slows when permits, marine surveys, and cross-border approvals lag engineering work. SMEC noted in 2026 that nearly all cable faults and a meaningful share of installation delays occur within territorial waters or exclusive economic zones where national permits are required before work can begin. Regulatory frameworks remain uneven across coastal states, and some jurisdictions still lack dedicated maintenance rules for submarine cable repairs. Even when a repair vessel is ready, permit delays can extend outages by weeks and raise the cost of redundancy planning. Across the subsea fiber backbone network market, that uncertainty makes timelines harder to manage in Asia-Pacific, the Middle East and Africa, and parts of Europe where multi-jurisdiction routes are common.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Marine Services Gain Ground on New-Build Dominance

Wet-Plant Equipment held the largest component share at 28.82% in 2025, reflecting the fact that submarine cables, repeaters, and branching units account for a large share of every new build budget. Dry-Plant Equipment ranked second because landing stations, submarine line terminal equipment, and power-feed systems need investment on both greenfield routes and upgrade programs. Open cable designs are making these upgrades more practical, since operators can refresh terminal equipment without replacing the full route. In the subsea fiber backbone network market, this spending is distributed across the cable itself and the shore-based systems that unlock its commercial value.

Auxiliary and Marine Services is projected to expand at a 9.41% CAGR from 2026 to 2031, which is faster than the overall subsea fiber backbone network market. Fewer than 70 repair vessels worldwide serve more than 600 cable systems, and around 65% of the maintenance fleet is projected to reach the end of life within 15 years. Suppliers are responding by expanding vessel access, survey capacity, and maintenance capabilities as cable commitments widen across regions. The subsea fiber backbone network market, therefore, depends on marine services not only for growth, but also for schedule control and outage recovery.

By Cable Type: Single-Mode Fiber Anchors High-Capacity Routes

Single-Mode Fiber commanded a 67.33% share of cable-type revenue in 2025 and is also projected to record the highest CAGR at 8.78% through 2031. It dominates because long-haul transoceanic transmission needs the range and capacity that multimode designs cannot match over thousands of kilometers. Google announced the Sol transatlantic cable in 2026 to connect the United States, Bermuda, the Azores, and Spain, underscoring that route owners are still investing in high-capacity long-haul systems built for future upgrades. In the subsea fiber backbone network market, single-mode design has become the default choice wherever owners want to scale traffic over the asset's life.

Multimode Fiber remains useful in short subsea spans near landing stations and shallow nearshore deployments. Its higher core diameter can support coupling efficiency in those localized settings, even though it is not suited to backbone routes. High-fiber-pair single-mode systems also provide owners with stranded capacity that can be activated later through coherent optical upgrades rather than physical redeployment. That design logic helps the subsea fiber backbone network market manage future demand without rebuilding whole corridors too early.

By Client Type: Hyperscalers Reshape Traditional Carrier Demand

Telecom Operators held the largest client share at 31.11% in 2025, maintaining their lead even as the buyer mix began to shift. They still support long-term capacity agreements and consortium systems that underpin many legacy routes in the subsea fiber backbone network market. IEEE Communications Society reported in June 2026 that annualized telecom capital expenditure fell 0.9% year over year to USD 295.7 billion in the fourth quarter of 2025 and stayed below USD 300 billion for the second straight year. That funding pressure limits how aggressively telecom carriers can match privately funded expansion from larger technology buyers.

Content and Hyperscale Cloud Providers are projected to grow at a 10.10% CAGR through 2031, making it the fastest-growing client category in the subsea fiber backbone network market. The IEEE Communications Society also stated in June 2026 that hyperscalers were involved in over two-thirds of all planned submarine cable deployments globally. This shift changes vendor relationships because systems integrators now contract directly with a small set of very large platform owners. The subsea fiber backbone network industry is therefore seeing demand migrate from shared carrier procurement toward direct platform-led infrastructure ownership.

By Ownership Model: Single Ownership Displaces Shared Network Structures

Consortium-Owned Networks held the largest ownership share at 25.12% in 2025, reflecting the long history of multi-party cost-sharing in cross-border cable projects. They remain relevant where several sovereign markets need a shared route, and no single anchor tenant can justify full ownership. Capacity-Leased Networks still serve buyers that want transoceanic reach without the capital burden or operational complexity of owning cable assets. That means the subsea fiber backbone network market continues to support multiple ownership forms even as private capital becomes more visible.

Single-Owner Networks is projected to expand at a 10.42% CAGR from 2026 to 2031, driven by hyperscaler-led private builds. The model gives one owner direct control over routing, latency management, and physical security across a route that supports its own traffic priorities. This movement is strongest on the highest-traffic trans-Pacific and trans-Atlantic corridors, reducing the role of consortia on routes that once delivered the richest wholesale economics. Across the subsea fiber backbone industry, public financing tools are becoming increasingly important, as governments seek strategic participation in routes that pure private ownership cannot support.

Geography Analysis

Asia-Pacific held the largest regional share at 30.12% in 2025 and is projected to record the fastest CAGR at 9.13% through 2031. IEEE Communications Society stated in June 2026 that India’s submarine cable landing capacity was projected to quadruple in 2025 as multiple new systems moved toward completion. The same source noted that Google’s America-India Connect initiative adds fiber connections linking India with Africa, Australia, and Southeast Asia. Japan is also pushing domestic participation in global cable programs, while South Korea is entering international telecom cable contracting through new regional routes. In the subsea fiber backbone network market, this combination of demand growth, policy support, and route density keeps Asia-Pacific at the center of new capacity planning.

North America remains a major traffic and supply hub in the subsea fiber backbone network market because the United States anchors both trans-Atlantic and trans-Pacific landings. SubCom announced in January 2026 that it was expanding its Newington, New Hampshire, manufacturing headquarters to raise the output of submarine cable systems and components. The MANTA system added new Gulf of Mexico connectivity with landing points in Veracruz and San Blas, Florida, extending links toward Mexico City, Bogotá, and Panama City. South America still depends heavily on externally funded systems, leaving Brazil as the main landing hub while other routes remain relatively underbuilt to meet digital demand.

Europe is shaping the subsea fiber backbone network market through public security funding, while the Middle East is gaining importance as a route-diversification hub, and Africa continues to scale from a low base. The European Commission said in February 2026 that CEF Digital had allocated EUR 533 million (USD 575 million) to submarine cable projects through 2027, with EUR 186 million already awarded to 25 projects by early 2026. ASN, Sparkle, and Elettra signed the GreenMed contract in February 2026, and SubCom secured the Arctic Way contract with Space Norway in May 2025, which shows that Europe is adding capacity from the Mediterranean to the high Arctic. For the subsea fiber backbone network market, the Middle East offers alternative landing options for Europe-Asia traffic, while Africa remains a long-run expansion zone where outside capital still plays a large role.

Competitive Landscape

The subsea fiber backbone network market is moderately concentrated at the systems-integrator level, with SubCom LLC, Alcatel Submarine Networks, NEC Corporation, HMN Tech Co., Ltd., and Prysmian S.p.A. as the main suppliers. Competition is centered on technical execution, installed base, manufacturing capacity, marine access, and compliance with stricter security review rules. SubCom announced a manufacturing expansion in Newington in January 2026 to lift output for rising hyperscaler-led demand. ASN signed the GreenMed contract in February 2026 and the I-AM cable contract in January 2026, which shows continued momentum in Mediterranean and intra-Asia supply programs. In the subsea fiber backbone network market, suppliers with delivery scale and regulatory credibility are better placed than firms that depend on limited route access or politically sensitive approvals.

NEC is trying to strengthen its position by pairing cable manufacturing and systems integration with stronger national backing and greater control over marine operations. NEC completed the East Micronesia Cable System in May 2026, which reinforced its role in grant-backed sovereign connectivity programs outside the largest commercial cloud corridors. The Candle project agreement, signed in September 2025, also kept NEC at the center of dense Asia-Pacific build activity alongside platform and carrier partners. This leaves the subsea fiber backbone network market with a competitive split between high-volume private corridor builds and strategically financed regional systems.

The competitive field is also being shaped by policy, because vendor screening and critical infrastructure rules are raising the qualification bar in Europe and North America. The EU resilience framework and new cable security tools are pushing buyers toward suppliers that can meet tougher physical and cybersecurity expectations. The FCC’s 2025 cable licensing order added similar pressure in the United States by tightening scrutiny of foreign adversary-linked participation. The subsea fiber backbone network market, therefore, remains open enough for rivalry, but not loose enough for easy entry, especially on strategic cross-border routes.

Subsea Fiber Backbone Network Industry Leaders

SubCom LLC

NEC Corporation

Prysmian S.p.A.

Alcatel Submarine Networks

HMN Tech Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: NEC Corporation completed construction of the East Micronesia Cable System (EMCS), a 2,250 km submarine cable connecting the Federated States of Micronesia, Kiribati, and Nauru, the first major international fiber cable to serve all 3 Pacific island nations simultaneously. The project received financial support from the Australian Infrastructure Financing Facility for the Pacific and Japan's infrastructure programs, demonstrating how grant-backed sovereign connectivity programs are driving incremental demand outside commercial hyperscaler corridors.

- May 2026: NEC announced a JPY 100 billion (USD 653 million) capital program for its submarine cable business over FY2026-FY2030, targeting investment in a dedicated cable-laying vessel, expanded manufacturing facilities, and research and development for higher-capacity cable designs. The program is framed explicitly as an economic security initiative with Japanese government backing, signaling that national industrial policy is now a structural driver of subsea cable research and development investment.

- February 2026: The European Commission announced a EUR 347 million (USD 375 million) investment in submarine cable security under the Connecting Europe Facility Digital Work Program, accompanied by the EU Cable Security Toolbox and a list of 13 Cable Projects of European Interest. The announcement included EUR 267 million earmarked across 2 calls for priority cable builds and EUR 60 million dedicated to repair infrastructure and SMART cable monitoring components.

- February 2026: : Alcatel Submarine Networks, Sparkle, and Elettra signed the contract for the GreenMed submarine cable system in the Mediterranean, with the first segments expected in service by late 2028. ASN is responsible for wet-plant design and manufacturing while Elettra leads marine operations, illustrating the division of scope that characterizes modern large-scale cable supply arrangements.

Global Subsea Fiber Backbone Network Market Report Scope

The Subsea Fiber Backbone Network Report is Segmented by Component (Wet-Plant, Dry-Plant, Marine Services, and Other Components), Cable Type (Single-Mode and Multimode Fiber), Client Type (Telecom Operators, Hyperscaler Cloud Providers, Offshore Energy operators, and Government and Defense Agencies), Ownership Model (Consortium-Owned, Single-Owner, and Capacity-Leased), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Wet-Plant Equipment |

| Dry-Plant Equipment |

| Auxiliary and Marine Services |

| Other Components |

| Single-Mode Fiber |

| Multimode Fiber |

| Telecom Operators |

| Content and Hyperscale Cloud Providers |

| Offshore Energy Operators |

| Government and Defense Agencies |

| Consortium-Owned Networks |

| Single-Owner Networks |

| Capacity-Leased Networks |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| By Component | Wet-Plant Equipment | ||

| Dry-Plant Equipment | |||

| Auxiliary and Marine Services | |||

| Other Components | |||

| By Cable Type | Single-Mode Fiber | ||

| Multimode Fiber | |||

| By Client Type | Telecom Operators | ||

| Content and Hyperscale Cloud Providers | |||

| Offshore Energy Operators | |||

| Government and Defense Agencies | |||

| By Ownership Model | Consortium-Owned Networks | ||

| Single-Owner Networks | |||

| Capacity-Leased Networks | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current size of the subsea fiber backbone network market?

The subsea fiber backbone network market was valued at USD 7.75 billion in 2025, stood at USD 8.21 billion in 2026, and is forecast to reach USD 12.30 billion by 2031 at an 8.42% CAGR.

Why are hyperscalers investing directly in submarine cable routes?

Large cloud and content platforms now treat cables as performance assets. This gives them more control over latency, routing, capacity, and physical security on high-traffic international corridors.

Which component category leads revenue and which one is growing fastest?

Wet-Plant Equipment led with a 28.82% share in 2025, while Auxiliary and Marine Services is projected to grow fastest at a 9.41% CAGR through 2031.

Why is Single-Mode Fiber dominant in long-haul backbone systems?

Single-Mode Fiber accounted for 67.33% of cable-type revenue in 2025 because it is better suited to terabit-class transmission over very long distances and can support future capacity upgrades.

Which client group is expanding the fastest?

Content and hyperscale cloud providers are projected to grow at a 10.10% CAGR through 2031, reflecting a shift from buying capacity to owning or anchoring cable systems directly.

Which region is leading growth in new subsea route development?

Asia-Pacific led with a 30.12% share in 2025 and is expected to grow at a 9.13% CAGR through 2031, supported by new landings, regional route density, and strong demand from India, Japan, South Korea, and Southeast Asia.

Page last updated on: