Subscription Video-on-Demand (SVOD) Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

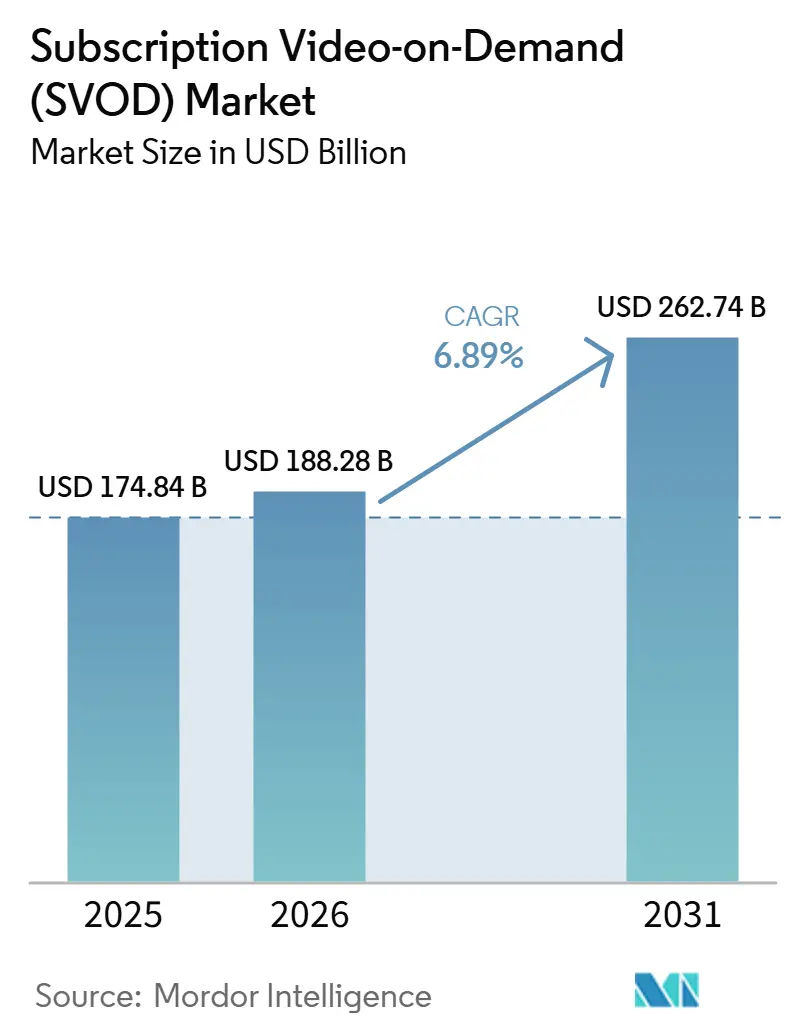

| Market Size (2026) | USD 188.28 Billion |

| Market Size (2031) | USD 262.74 Billion |

| Growth Rate (2026 - 2031) | 6.89% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Subscription Video-on-Demand (SVOD) Market Analysis by Mordor Intelligence

The subscription video-on-demand market size was valued at USD 174.84 billion in 2025 and estimated to grow from USD 188.28 billion in 2026 to reach USD 262.74 billion by 2031, at a CAGR of 6.89% during the forecast period (2026-2031). Growth in the subscription video-on-demand market is being shaped less by headline subscriber gains and more by pricing mix, retention, and average revenue per user discipline. Lower-priced plans, broader household bundling, and deeper integration with connected-TV interfaces are widening access while giving platforms more ways to manage revenue quality. Local-language originals and region-specific catalogs are also becoming more central, because expansion now depends on relevance in multilingual and mobile-first countries as much as on a global scale. At the same time, consolidation is raising the value of owned intellectual property, distribution control, and platform ecosystems that can keep users engaged across multiple services. Higher rights costs, compliance obligations, and subscriber fatigue in mature regions are therefore keeping the subscription video-on-demand market focused on efficiency, monetization, and growth.

Key Report Takeaways

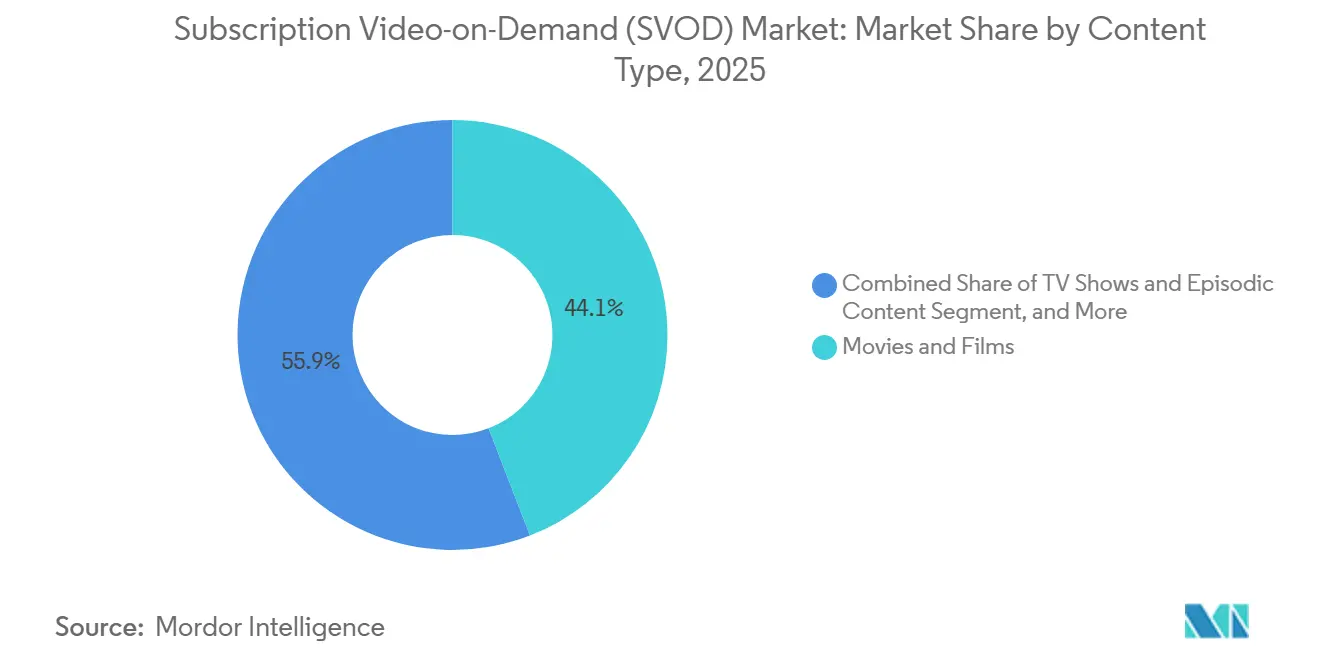

- By content type, Movies and Films held 44.13% of the subscription video-on-demand market in 2025, while Other content types is projected to expand at a 7.32% CAGR through 2031.

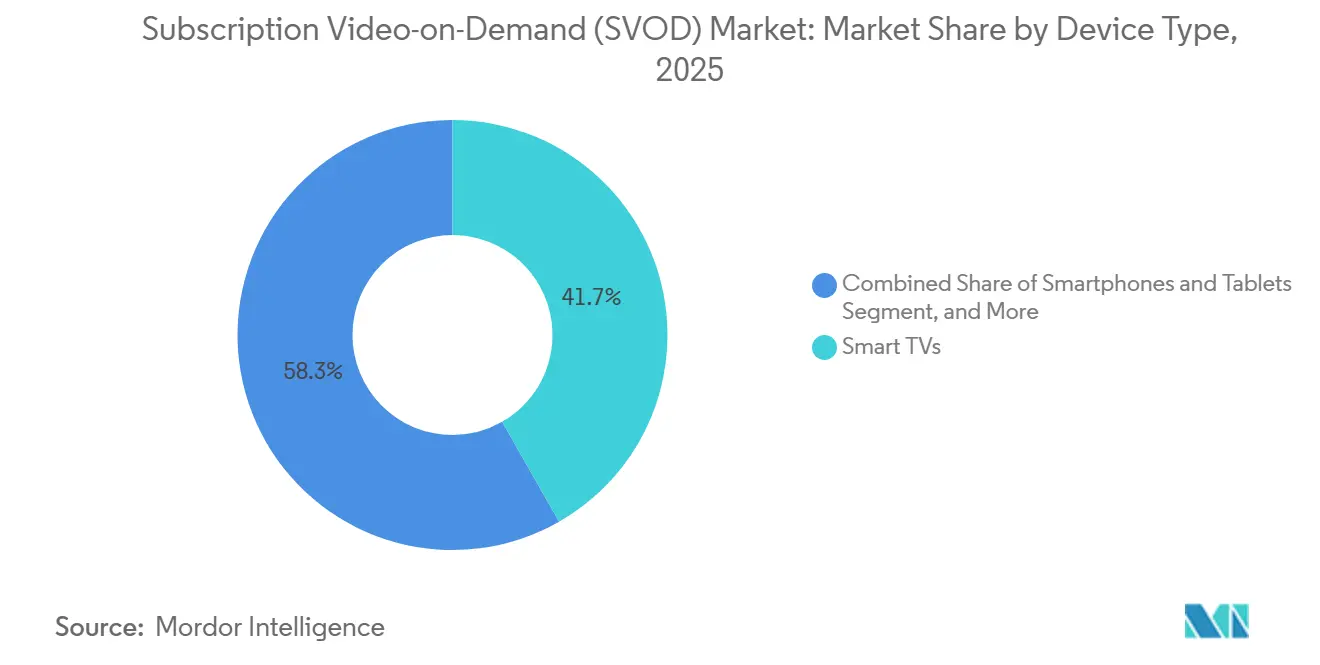

- By device type, Smart TVs accounted for 41.74% of the market share in 2025, while Smartphones and Tablets are projected to record the highest CAGR of 7.48% through 2031.

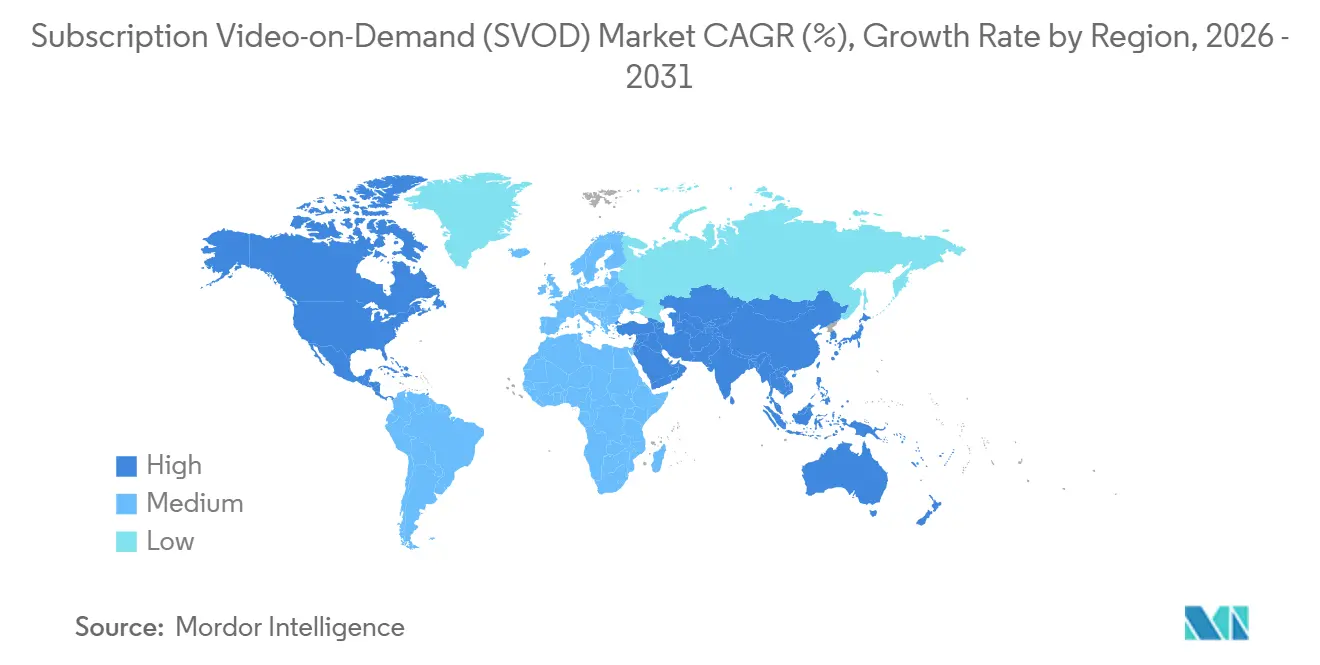

- By geography, North America captured 39.61% of the SVOD market in 2025, while Asia-Pacific is projected to grow fastest at a 7.86% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Subscription Video-on-Demand (SVOD) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Demand for Premium Original Content | +1.8% | Global | Medium term (2-4 years) |

| Smart TV and Connected Device Ecosystem Expansion | +1.4% | North America, Europe, Asia-Pacific | Short term (≤ 2 years) |

| Bundling With Telecom and Pay-TV Offers | +1.2% | Europe, North America | Short term (≤ 2 years) |

| Ad-Supported Tier Expansion in Mature Markets | +1.0% | North America, Europe | Short term (≤ 2 years) |

| AI-Personalized Discovery and Retention Tools | +0.7% | Global | Medium term (2-4 years) |

| Local-Language Library Expansion in High-Growth Markets | +0.6% | Asia-Pacific, Middle East, Africa, South America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Premium Original Content

Premium original programming remains a core growth lever in the subscription video-on-demand market because exclusive titles help platforms justify recurring payments. The strongest commercial value still sits in reusable intellectual property, where films and series can support sequels, spin-offs, merchandising, and deeper audience loyalty. Netflix’s planned all-cash acquisition of Warner Bros. Discovery’s streaming and studios assets showed how aggressively major players now value owned libraries and long-life franchises.[1]Netflix Investor Relations, “Netflix and Warner Bros. Discovery Amend Agreement to All-Cash Transaction,” Netflix Investor Relations, ir.netflix.net European content rules reinforce this logic, because platforms that already invest in broad production pipelines are better placed to meet local catalog obligations without weakening release quality. This is pushing investment toward titles that can travel across regions while still being adapted for local audiences. As a result, the subscription video-on-demand market is rewarding platforms that can spread content spending across global franchises, local originals, and multi-year release slates.

Smart TV and Connected Device Ecosystem Expansion

Connected devices are reshaping the subscription video-on-demand market, because distribution is now built into the screens people use every day. Smart-TV operating systems matter more than before, since placement on home screens and recommendation rows can influence what households open first. Fox’s agreement to acquire Roku showed that control of the device layer has become strategically important in its own right, not just as a route to third-party services. The same logic is visible in app pre-installation and interface partnerships, where platforms move closer to the household entry point before a user even chooses a service. This reduces sign-up friction, shortens the viewing path, and helps both premium and ad-supported services stay visible in crowded homes. For the subscription video-on-demand market, device expansion is no longer just a hardware trend; it is part of the customer acquisition and retention strategy.

Bundling With Telecom and Pay-TV Offers

Bundling with telecom and pay-TV offers is supporting the subscription video-on-demand market by lowering the effort required to start and maintain paid services. When streaming access is folded into a broader household bill, the service becomes easier to keep and harder to cancel on impulse. The model also helps platforms reach users who may hesitate to manage separate subscriptions or payment relationships. In practice, bundling is shifting competition away from one-off sign-ups and toward long-term distribution partnerships. It is also giving operators a stronger role in merchandising, billing, and service discovery inside the home. That leaves the subscription video-on-demand market better positioned when it is present inside large partner ecosystems, and at a disadvantage when it relies only on standalone acquisition.

Ad-Supported Tier Expansion in Mature Markets

Ad-supported tiers have become an increasingly important part of the subscription video-on-demand market as mature regions seek growth without relying solely on full-price plans. These lower-priced offers widen the funnel for price-sensitive users and create a second revenue stream from advertisers. They also provide platforms with richer viewing data that can support better content promotion, ad placement, and retention efforts. The model is not costless, because advertising-driven services need stronger data governance and clearer controls over profiling practices. Recent privacy enforcement in Europe showed that streaming platforms face tighter scrutiny over transparency and data handling. Even so, the subscription video-on-demand market is likely to keep expanding ad-supported options, as they better balance affordability, reach, and monetization than a one-price model.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Subscription Fatigue and Churn in Mature Households | -1.6% | North America, Europe | Short term (≤ 2 years) |

| Escalating Content Licensing and Sports Rights Costs | -1.2% | Global | Long term (≥ 4 years) |

| Fragmented Rights Windows Across Platforms | -0.7% | North America, Europe | Medium term (2-4 years) |

| Privacy and Algorithm Transparency Compliance Burden | -0.5% | Europe, with spillover to Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Subscription Fatigue and Churn In Mature Households

Subscription fatigue is limiting the subscription video-on-demand market among mature households, where many users already pay for multiple services simultaneously. That makes cancellations easier to justify when a platform finishes a tentpole release cycle or loses a must-watch title. The problem is not a collapse in demand, but a more tactical pattern of joining, pausing, and returning. This behavior weakens revenue visibility and forces providers to spend more on programming and promotion just to hold the same household. It also raises the importance of release timing, pricing discipline, and bundled distribution inside the subscription video-on-demand market. Platforms with thinner catalogs or weaker local relevance are therefore more exposed to short-duration usage and inconsistent subscriber loyalty.

Escalating Content Licensing and Sports Rights Costs

Escalating licensing and sports rights costs are putting steady pressure on margins across the subscription video-on-demand market. Live sports can support engagement and brand visibility, but the cost of securing premium rights keeps rising faster than many services can comfortably absorb. The same pressure extends to film and television libraries, where scale players can outbid smaller rivals for widely recognized content. When a platform loses a marquee rights package, it can also lose part of the audience that joined for that property in the first place. This cost dynamic helps explain why consolidation has become more appealing, including the planned combination of Netflix with Warner Bros. Discovery’s streaming and studio assets. In effect, the subscription video-on-demand market is becoming harder for mid-scale services that lack either premium rights depth or a strong local niche.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Content Type: Franchise Films Lead As Live Formats Expand

Movies and Films held 44.13% of the subscription video-on-demand market share in 2025, making filmed entertainment the leading content anchor for paid streaming platforms. Their strength comes from repeatable franchise value, exclusive windows, and broad appeal across age groups and regions. In the subscription video-on-demand market, film libraries also help services maintain a visible pipeline of recognizable titles between major series launches. TV Shows and Episodic Content remained the second-largest segment because serial viewing supports habitual use and keeps subscribers returning across several weeks or months. European catalog rules reinforce the need for depth across both films and episodic content, since platforms must maintain a minimum 30% share of European works in their catalogs.

The other content types segment is the fastest-growing, projected to expand at a 7.32% CAGR through 2031 as platforms broaden their mix beyond scripted entertainment. Live sports, special events, and interactive formats create appointment viewing, which makes this part of the subscription video-on-demand industry especially useful for retention and differentiation. Documentaries remain smaller in scale, but they add credibility, subject variety, and catalog breadth at a lower production intensity than high-end scripted releases. In Europe, viewing of EU films retained a meaningful place in subscription catalog consumption, which supports the case for sustained investment in diverse local and regional libraries.[2]Council of Europe, “SVOD Usage in the EU, 2024 Data,” Council of Europe, rm.coe.int

By Device Type: Smart TVs Lead Revenue As Mobile Viewing Broadens Access

Smart TVs accounted for 41.74% share of the subscription video-on-demand market size in 2025, confirming the living room as the largest revenue setting for streamed video. Larger screens support longer sessions, shared household viewing, and stronger merchandising of premium titles and bundled offers. Device operating systems have also become strategic gatekeepers, because interface placement can influence which apps viewers open first. Fox’s move to buy Roku illustrated how seriously media groups now view control over the connected-TV layer. For the subscription video-on-demand market, smart-TV access is now part of a monetization strategy rather than only a distribution endpoint.

Smartphones and Tablets are the fastest-growing device type, and they are projected to record a 7.48% CAGR through 2031 as mobile-first viewing expands in price-sensitive and multilingual countries. JioHotstar’s launch of conversational voice discovery in 12 Indian languages showed how mobile and voice-led access are being adapted to large, diverse user bases. Laptops and Desktops continue to serve workday and individual viewing needs, while streaming sticks, gaming consoles, and set-top boxes extend services to older screens and secondary rooms. This leaves the SVOD market industry with a two-layer device pattern, where Smart TVs lead premium household consumption, and mobile devices broaden reach, discovery, and daily usage.

Geography Analysis

North America held 39.61% of the subscription video-on-demand market share in 2025, maintaining its position as the largest regional revenue base. The region still benefits from a strong willingness to pay, broad service availability, and a mature ad-supported offering mix. Growth there is becoming more dependent on retention, bundling, and price realization than on first-time household adoption. South America remains a smaller base, but it offers meaningful headroom for unlocking wider paid use through local-language content and flexible pricing. For the subscription video-on-demand market, the region’s opportunity lies in turning mobile and broadband adoption into longer-lasting paid relationships.

Asia-Pacific is the fastest-growing region in the subscription video-on-demand market, with a 7.86% CAGR projected through 2031. Demand in this region is being shaped by younger digital audiences, growing connected-device access, and strong acceptance of local-language storytelling. India stands out because scale depends on serving many languages and usage patterns rather than relying on a single national content formula. JioHotstar’s rollout of voice-led discovery across 12 Indian languages reflected how product design is being tailored to this reality.[3]JioStar, “JioHotstar Launches ChatGPT-Branded Conversational Streaming in India,” JioStar, jiostar.com Europe follows a different path, where growth is closely tied to content localization and regulatory compliance under the Audiovisual Media Services Directive.

The Middle East and Africa are growing from a smaller base in the SVOD market, with expansion shaped by youth demographics, mobile use, and distribution partnerships. In the Gulf states, paid streaming growth is supported by affluent digital consumers and a strong role for operator-led service packaging. Across Africa, infrastructure and currency volatility continue to slow wider adoption, keeping affordability and device access central to strategy. Canal+’s control of MultiChoice highlighted how scale in Africa is increasingly being built through regional platforms, local rights, and broader digital distribution.

Competitive Landscape

The subscription video-on-demand market is moderately concentrated globally, but it remains fragmented when regional, language, and genre specialists are included. Netflix, Amazon, and Disney still shape much of the premium global conversation, yet their scale does not remove the need for local content, local billing, and regional brand strength. The clearest strategic theme in 2026 was consolidation, particularly Netflix’s planned USD 82.7 billion all-cash acquisition of Warner Bros. Discovery’s streaming and studios assets. Fox’s USD 22 billion agreement to acquire Roku showed that distribution control is now being valued alongside content ownership.[4]Roku Newsroom, “Fox Corporation to Acquire Roku, Inc.,” Roku Newsroom, newsroom.roku.com In the subscription video-on-demand market, competitive advantage is therefore moving toward companies that can combine strong libraries, broad reach, and direct visibility on consumer screens.

Regional specialists continue to challenge global entrants by offering language depth, local sports, and pricing structures that match local purchasing power. JioHotstar’s conversational discovery launch across 12 Indian languages illustrated how product localization can serve as a competitive moat rather than just a usability feature. Canal+’s effective control of MultiChoice created a broader African platform with established brands, sports rights, and regional distribution that global services cannot replicate quickly. This keeps the subscription video-on-demand industry open to both global scale players and regionally dominant firms that understand local viewing behavior better.

Compliance is also becoming a competitive variable, because content quotas, privacy expectations, and platform transparency rules raise the cost of operating across multiple jurisdictions. The AVMSD in Europe has already made local catalog composition a strategic requirement rather than an optional market-entry tactic. No irrelevant companies were identified among the 21 profiled participants, since each one operates a subscription streaming service directly or controls one through a broader media portfolio. The SVOD market, therefore, remains open, but it increasingly rewards firms that can pair scale with local execution and regulatory readiness.

Subscription Video-on-Demand (SVOD) Industry Leaders

Netflix, Inc.

Amazon.com, Inc.

The Walt Disney Company,

Apple Inc.

Warner Bros. Discovery, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2026: Sky agreed to acquire ITV's Media and Entertainment business for total consideration of up to GBP 1.6 billion (USD 2.14 billion). The deal is expected to close in the second half of 2027, subject to regulatory approval. The acquisition gives Sky control of ITVX, which grew monthly active users nearly 60% over four years to 16.5 million, and separates ITV Studios as a standalone global content entity.

- June 2026: Fox Corporation and Roku announced a definitive agreement for Fox to acquire Roku at USD 160.00 per share in a combination of cash and stock, valuing Roku at USD 22 billion in enterprise value. The transaction is expected to close in the first half of 2027. The combined company would become the third-largest television business in the United States by viewership.

- June 2026: Canal+ and Samsung announced the pre-installation of the DStv Stream app on all new Samsung Smart TVs across 18 African countries, including South Africa, Nigeria, Kenya, Angola, and Zimbabwe. This marked the first pre-installation rollout of a MultiChoice Group streaming application and strengthened Canal+’s digital distribution footprint following its 2025 acquisition of MultiChoice.

- May 2026: Canal+ announced it expects to deliver EUR 250 million (USD 290 million) in synergies from its MultiChoice integration in 2026, accelerating the target following its exit from the Showmax streaming venture. Canal+ also confirmed partnerships with Google Cloud, OpenAI, and Sky to advance content technology development across its 40 million-subscriber, 70-country platform.

Global Subscription Video-on-Demand (SVOD) Market Report Scope

The Subscription Video-on-Demand (SVOD) market comprises digital streaming services that provide subscribers with unlimited on-demand access to a library of video content in exchange for a recurring subscription fee, typically billed monthly or annually. SVOD platforms deliver content over the internet across multiple connected devices, enabling users to stream movies, television series, documentaries, and other video programming without requiring traditional broadcast, cable, or satellite television subscriptions.

The Subscription Video-on-Demand (SVOD) Market Report is Segmented by Content Type (Movies and Films, TV Shows and Episodic Content, Documentaries, Other Content Types), Device Type (Smartphones and Tablets, Smart TVs, Laptops and Desktops, Other Device Types), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Movies and Films |

| TV Shows and Episodic Content |

| Documentaries |

| Other Content Types |

| Smartphones and Tablets |

| Smart TVs |

| Laptops and Desktops |

| Other Device Types |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Qatar | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Nigeria | |

| Rest of Africa |

| By Content Type | Movies and Films | |

| TV Shows and Episodic Content | ||

| Documentaries | ||

| Other Content Types | ||

| By Device Type | Smartphones and Tablets | |

| Smart TVs | ||

| Laptops and Desktops | ||

| Other Device Types | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Qatar | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

How large is the subscription video-on-demand (SVOD) market in 2026?

The subscription video-on-demand market size stood at USD 188.28 billion in 2026 and is forecast to reach USD 262.74 billion by 2031 at a 6.89% CAGR.

Which region is growing fastest for subscription video-on-demand services?

Asia-Pacific is the fastest-growing region, with the subscription video-on-demand market projected to expand at a 7.86% CAGR through 2031.

Which content type leads global paid streaming revenue?

Movies and Films led with 44.13% share in 2025, reflecting the commercial strength of franchises, exclusives, and broad audience appeal.

Why are Smart TVs so important for SVOD platforms?

Smart TVs held 41.74% share in 2025 and remain critical because they support household viewing, stronger title promotion, and better monetization on larger screens.

What is driving growth in mobile viewing for streamed video subscriptions?

Smartphones and Tablets are projected to grow at a 7.48% CAGR through 2031, supported by mobile-first usage, multilingual audiences, and easier access in price-sensitive countries.

What are the main risks facing SVOD providers through 2031?

The main risks are subscription fatigue in mature households, higher content and sports rights costs, and tighter compliance requirements across privacy and local content regulation.

Page last updated on: