Sterilization Pouches Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 41.84 Billion |

| Market Size (2031) | USD 56.01 Billion |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Sterilization Pouches Market Analysis by Mordor Intelligence

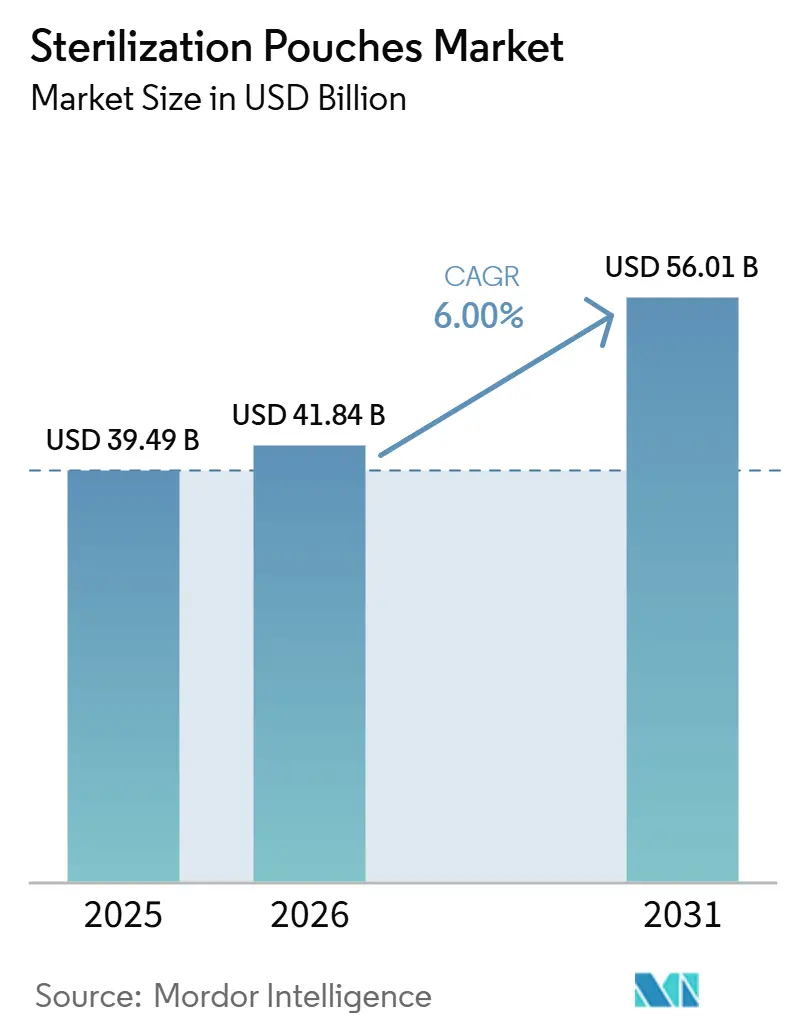

The Sterilization Pouches Market size was valued at USD 39.49 billion in 2025 and is estimated to grow from USD 41.84 billion in 2026 to reach USD 56.01 billion by 2031, at a CAGR of 6% during the forecast period (2026-2031).

The sterilization pouches market is expanding on the back of sustained procedural demand, because more than 300 million surgical procedures are performed globally each year and each procedure depends on a validated sterile barrier before use. A second force in the sterilization pouches market is tighter packaging validation expectations, as amended ISO 11607 standards are now embedded more clearly in regulatory practice across major medical device jurisdictions. That combination is changing procurement behavior, because buyers are no longer focused only on unit volume and are increasingly screening products for validation support, seal consistency, traceability readiness, and compatibility with multiple sterilization methods. The sterilization pouches market also faces clear pressure from price-led hospital tenders, especially where public procurement systems still reward the lowest bid even when compliance expectations are rising. At the same time, the sterilization pouches market is opening room for suppliers that can meet low-temperature sterilization needs, support digital labeling, and adapt multi-layer structures to future recycling rules without weakening sterile barrier performance.

Key Report Takeaways

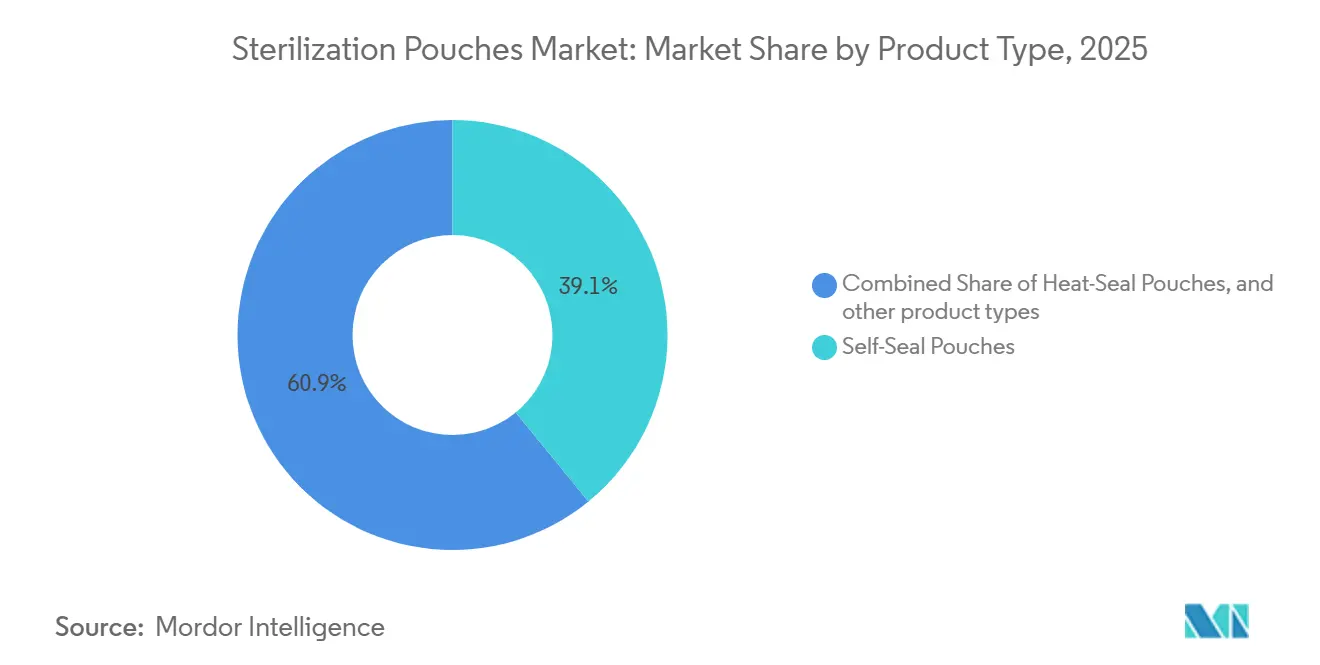

- By product type, self-seal pouches held 39.11% revenue share in 2025, while heat-seal pouches are forecast to expand at an 8.11% CAGR through 2031.

- By material type, the paper and plastic segment accounted for 54.30% of revenue in 2025, while Tyvek is projected to grow at an 8.16% CAGR through 2031.

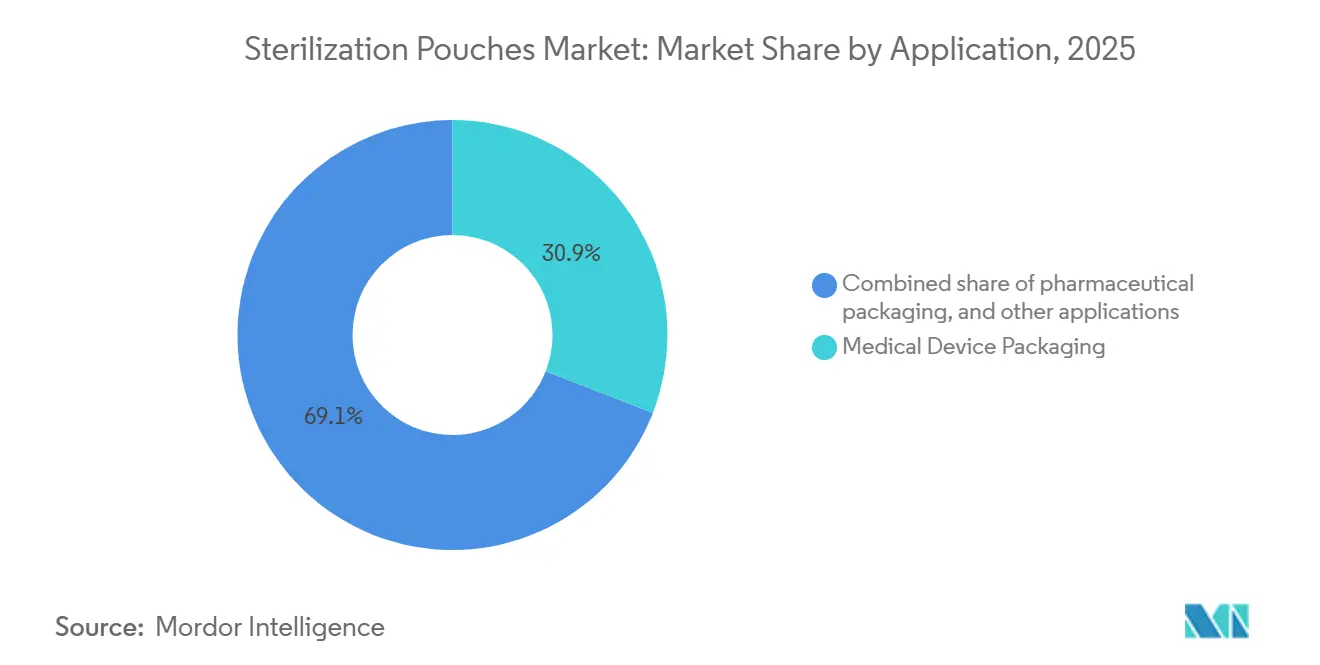

- By application, medical device packaging held 30.87% of revenue in 2025, while pharmaceutical packaging is forecast to grow at a 9.87% CAGR through 2031.

- By end-user, hospitals held 40.77% of revenue in 2025, while dental clinics and practices are projected to expand at an 8.38% CAGR through 2031.

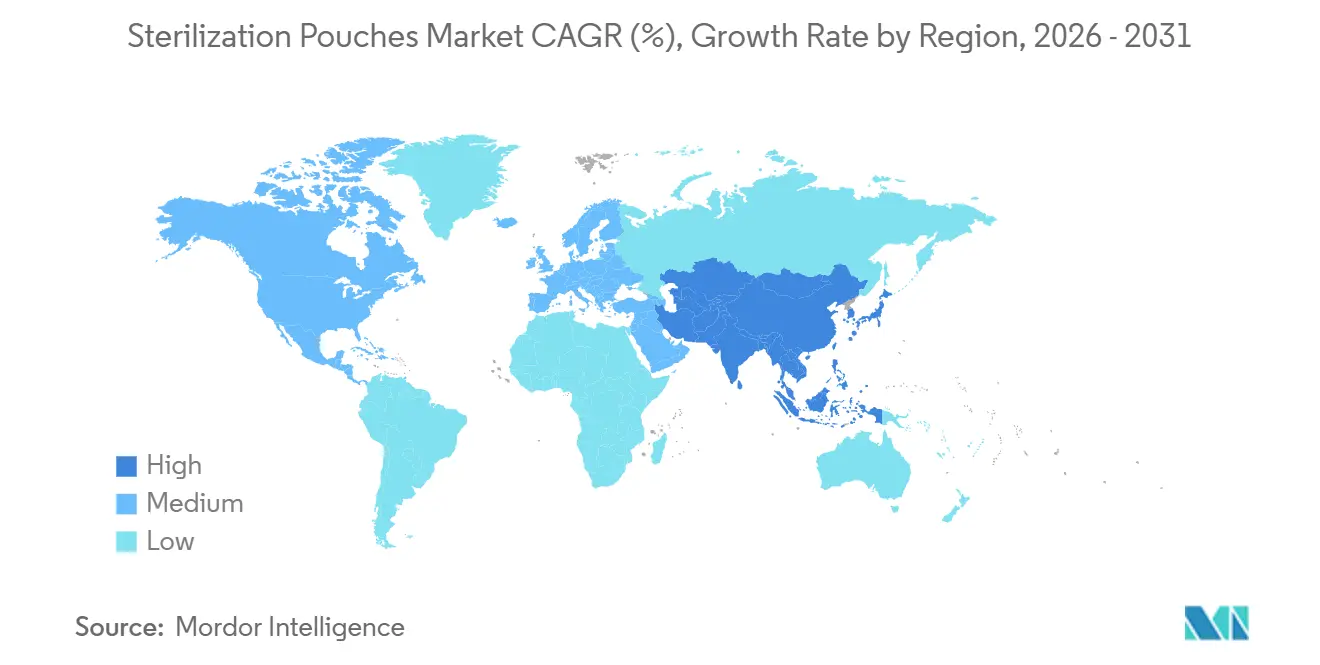

- By geography, North America held 38.80% of revenue in 2025, while Asia-Pacific is expected to grow at the fastest 8.06% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Sterilization Pouches Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Surgical Volumes and Outpatient Procedure Growth | +1.5% | Global, with concentrated gains in North America, Europe, and APAC core | Short term (≤ 2 years) |

| Regulatory Push for Sterile Barrier Validation | +1.0% | North America and EU, with APAC spillover from MDR harmonization | Medium term (2-4 years) |

| Expansion of Medical Device Manufacturing And Contract Sterilization | +0.8% | North America, APAC, and Eastern Europe | Medium term (2-4 years) |

| Shift Toward Single-Use, Traceable Sterile Packaging | +0.6% | Global, with early gains in the United States, Germany, and Japan | Medium term (2-4 years) |

| Increased Adoption of Low-Temperature Sterilization Compatible Pouches | +0.4% | North America and EU, with spillover to APAC and MEA | Long term (≥ 4 years) |

| Digitized Lot Traceability and Recall Readiness Requirements | +0.3% | North America and EU primary, APAC secondary in hospital systems | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Surgical Volumes and Outpatient Procedure Growth

The sterilization pouches market continues to benefit from the basic fact that every surgical procedure needs a sterile barrier before an instrument or kit reaches the point of use. The World Health Organization places annual global surgical volume above 300 million procedures, which gives the sterilization pouches market a large and recurring procedural base[1]World Health Organization, “Global Initiative for Emergency and Essential Surgical Care,” World Health Organization, who.int. Demand is also shifting in format, because outpatient and ambulatory settings often prefer smaller and faster pouch configurations over bulkier options used in large hospital departments. That shift matters commercially because ambulatory centers tend to buy for per-procedure use, which supports distributor-led channels and stronger unit economics. Medical tourism in countries such as Thailand, India, and Turkey adds another layer of geographically concentrated demand for sterile consumables, which gives the sterilization pouches market new distribution opportunities in high-growth treatment corridors.

Regulatory Push for Sterile Barrier Validation

The sterilization pouches market is also being shaped by a stronger regulatory focus on validated sterile barrier systems rather than basic packaging supply alone. ISO 11607-1 now gives more explicit weight to risk management within packaging system design, which raises the documentation burden for device companies and their packaging partners.

In Europe, amended EN ISO 11607 standards were added to the harmonized framework under the EU MDR, which means manufacturers selling into the region must align packaging qualification with the updated versions. This is compressing validation timelines across product portfolios and bringing packaging review forward in commercial planning. The sterilization pouches market, therefore, favors suppliers that can provide faster test support, stronger technical files, and better guidance during requalification cycles.

Expansion of Medical Device Manufacturing and Contract Sterilization

The sterilization pouches market rises with sterilization capacity because every device entering a commercial sterilization cycle must already be packed in a validated sterile barrier. STERIS announced construction of a USD 60 million sterility assurance manufacturing plant in Mentor, Ohio, which will consolidate 3 existing facilities into one center of excellence and run through 2027. In Europe, Medistri commissioned a second ethylene oxide sterilization line at its Hungary site after the facility’s January 2025 launch and earlier investment program, adding more compliant processing capacity for regional customers.

BGS US also opened an electron-beam sterilization facility in Imperial, Pennsylvania, in July 2025 to serve medical device, pharmaceutical, and biotech customers. These additions expand sterilizable throughput across North America and Europe, which directly supports pouch consumption. They also raise technical expectations in the sterilization pouches market because suppliers increasingly need products qualified across ethylene oxide, radiation, steam, and low-temperature processes.

Shift Toward Single-Use, Traceable Sterile Packaging

The sterilization pouches market is moving beyond basic containment and toward packaging that supports traceability, process control, and recall readiness. The FDA’s Unique Device Identification framework requires machine-readable UDI marking on regulated device labels and packages, which turns the package into a tracking point across sterilization, storage, and use. That shift increases the value of pouch labels and indicators that remain readable after chemical or thermal exposure.

Solventum’s March 2025 launch of the Attest eBowie-Dick Test System shows how sterility assurance is becoming more digitized inside central sterile departments, with electronic documentation replacing visual interpretation in some workflows. As hospitals and device makers modernize traceability practices, the sterilization pouches market is likely to reward suppliers that can pair barrier performance with clearer labeling, smarter indicators, and documentation support.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Price Sensitivity in Cost-Constrained Healthcare Procurement | -0.6% | South Asia, Southeast Asia, MEA, South America, with secondary impact in Eastern Europe | Short term (≤ 2 years) |

| Compliance Burden Across Multi-Jurisdiction Medical Packaging Standards | -0.4% | Global, acute in companies exporting across FDA, EU MDR, NMPA, and CDSCO jurisdictions | Medium term (2-4 years) |

| Material Substitution Pressure from Recyclability and Waste-Reduction Mandates | -0.5% | EU primary, North America secondary, APAC emerging | Long term (≥ 4 years) |

| Compatibility Constraints with Emerging Sterilization Modalities | -0.3% | Global, concentrated in facilities moving from ethylene oxide to VHP or other alternatives | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Price Sensitivity in Cost-Constrained Healthcare Procurement

The sterilization pouches market still runs into price ceilings in public healthcare systems that rely on lowest-bid tendering. This is especially visible across South Asia, Southeast Asia, the Middle East, Africa, and parts of South America, where hospitals may need compliant packaging but still award contracts mainly on cost. That creates a two-tier structure inside the same country, with premium validated pouches serving private hospitals and multinational device manufacturers, while lower-cost products compete for public tenders.

The result is margin pressure for suppliers that serve both ends of the market, because cheap public-sector pricing becomes a reference point in wider negotiations. Until procurement scoring gives more weight to ISO 11607 documentation and validation quality, the sterilization pouches market will continue to face uneven pricing discipline across emerging healthcare systems.

Compliance Burden Across Multi-Jurisdiction Medical Packaging Standards

The sterilization pouches market is also slowed by the cost of meeting different packaging rules across the United States, Europe, China, and India. Europe now references amended EN ISO 11607 standards under the EU MDR, while U.S. regulatory practice is tied to its own recognized standard framework and submission expectations. China applies packaging requirements under YY/T 0698, and companies cannot always directly use U.S. or EU submission files without adapting them to meet China-specific requirements. For global suppliers, this means parallel validation work, repeated aging studies, seal testing, and barrier documentation across jurisdictions. That burden raises the minimum scale needed to compete effectively and gradually shifts the sterilization pouches market toward companies with deeper regulatory, quality, and documentation resources.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Self-Seal Formats Hold Share As Heat-Seal Momentum Builds

Self-seal pouches held 39.11% of revenue in 2025, which made them the largest product category in the sterilization pouches market. Their position rested on clear workflow advantages because they do not require separate heat-sealing equipment, and they support fast instrument turnaround in hospitals, clinics, and sterile processing departments. Flat pouches continued to serve the broad base of routine packaging demand and remained the standard option for common instruments and kits. Gusseted pouches filled a different role by supporting bulkier sets and multi-component packs where flat structures may not seal or present well.

Heat-seal pouches are projected to grow at an 8.11% CAGR through 2031, which makes them the fastest-rising format in the sterilization pouches market size by product type. Their growth reflects stronger and more repeatable seal integrity, which appeals to hospital systems that are adopting monitored sealing workflows and to device manufacturers that rely on automated packaging lines. Foil pouches stayed limited to a narrower niche, but they remained important where moisture-sensitive products need a zero-permeability barrier that paper-based formats cannot provide. Reels and rolls kept steady demand from dental clinics and small healthcare facilities that need flexibility in pouch length without managing a large inventory of pre-made sizes. Together, these patterns show that the sterilization pouches market is balancing convenience-led demand in clinical settings with validation-led adoption of more controlled sealing formats in larger institutions and OEM environments.

By Material Type: Paper-Plastic Composite Dominates, Tyvek Accelerates On Low-Temperature Compatibility

Paper and plastic composites accounted for 54.30% of revenue in 2025 and led the sterilization pouches market share at the material level. Their leadership came from broad modality compatibility across steam, ethylene oxide, and gamma sterilization, along with pricing that still fits public procurement budgets in many countries. This material mix remains the workhorse of the sterilization pouches market because it supports high-volume use cases without pushing users into premium cost bands. Non-woven materials continued to serve selected applications where different microbial barrier properties are preferred, while foil and laminated materials kept a specialized role in moisture- and light-sensitive packaging.

Tyvek is forecast to grow at an 8.16% CAGR through 2031, which makes it the fastest-rising material in the sterilization pouches market size by material segment. The main reason is structural compatibility with low-temperature sterilization processes, especially where cellulosic paper is not suitable for vaporized hydrogen peroxide systems. DuPont’s investment of more than USD 30 million in its Tyvek Medical Packaging Transition Project underlined the company’s confidence in long-term demand for this substrate[2]DuPont, “Tyvek Medical Packaging Transition Project,” DuPont, dupont.com. Olympus also began incorporating DuPont Tyvek with Renewable Attribution into sterile packaging for more than 100 device categories at facilities in Japan and Vietnam in 2026, linking barrier performance with lower CO2 intensity in procurement decisions. That move suggests the sterilization pouches market is starting to judge material choice on both sterilization compatibility and sustainability credentials, especially in OEM device packaging programs.

By Application: Medical Device Packaging Anchors Volume, Pharmaceutical Packaging Drives The Fastest Growth

Medical device packaging held 30.87% of 2025 revenue and remained the largest application area in the sterilization pouches market. That lead reflects the basic design purpose of sterile barrier systems, which is to maintain device sterility during transport, storage, and use across regulated healthcare environments. Medical device demand also tends to be broad and recurring, which gives this segment a stable base even when individual end markets move at different speeds. Surgical instrument packaging and dental instrument packaging stayed meaningful mid-sized categories, supported by ongoing infection control needs and steady reprocessing volumes.

Pharmaceutical packaging is projected to grow at a 9.87% CAGR through 2031, which makes it the fastest-growing application in the sterilization pouches market. This growth is driven by biologics manufacturing scale-up and stricter sterile manufacturing expectations in regulated pharmaceutical settings. That creates a more demanding specification environment, because suppliers must satisfy both sterile barrier requirements and pharmaceutical quality documentation expectations. Laboratory supplies and veterinary instruments packaging remained smaller in absolute terms, but both were structurally advancing as testing activity and veterinary surgical care expanded. The sterilization pouches industry is therefore seeing a wider spread of demand beyond its device packaging base, but the sterilization pouches market still depends on device volumes for scale, while pharmaceutical applications lift the growth curve and quality threshold.

By End-User: Hospitals Hold The Base While Dental Clinics Expand Faster

Hospitals accounted for 40.77% of revenue in 2025 and led the sterilization pouches market share by end-user. Their dominance reflected the concentration of sterilization infrastructure inside hospital central sterile services departments, where high-volume instrument sets are processed through standardized and validated workflows. Hospitals also influence the wider sterilization pouches market because central purchasing teams often standardize pouch formats across multiple departments and procedure lines. Central sterile services departments act as aggregation points for demand, which gives hospital procurement decisions outsized influence on product mix and supplier selection.

Dental clinics and practices are forecast to grow at an 8.38% CAGR through 2031, making them the fastest-growing end-user group in the sterilization pouches market size by end-use. Growth in this segment is supported by wider access to dental care in India and Southeast Asia and by tighter infection-control enforcement in smaller practice settings. Ambulatory surgical centers also stand out because they combine high procedure throughput with lean staffing, which favors simple and validated pouch formats that reduce preparation time. Medical device manufacturers remain an important end-user because they consume pouches as part of finished device packaging and are closely tied to OEM production growth. Larger hospital groups are also using more single-use procedure trays and prepacked kits, which can consolidate sterile packaging demand into fewer but higher-value supplier relationships across the sterilization pouches market.

Geography Analysis

North America held 38.80% of global revenue in 2025, which gave it the largest regional position in the sterilization pouches market. The region benefits from dense surgical infrastructure, mature regulatory enforcement, and purchasing practices that place a high value on validated packaging systems. The United States drives most of that demand, supported by strict device labeling rules and established infection-control expectations that leave little room for non-validated formats in institutional purchasing. Canada remained a smaller but stable contributor through provincial procurement systems, while Mexico added support as a medical device manufacturing hub. North America also continues to benefit from an expanding ambulatory surgical center base, which adds new procedural sites that need reliable sterile packaging in high-throughput settings.

Asia-Pacific is forecast to grow at an 8.06% CAGR through 2031, making it the fastest-growing regional segment in the sterilization pouches market. Growth is being supported by hospital investment in China, India, Japan, South Korea, and Southeast Asia, along with rising medical device output across the region. India is also moving higher in importance as hospital capacity grows and sterile medical device packaging requirements tighten in local procurement. Amcor’s April 2026 opening of a USD 35 million healthcare packaging coating facility in Malaysia, supported by the Malaysian Investment Development Authority, and its June 2026 investment in India both show how suppliers are building closer to regional device manufacturing clusters.

Europe remained a structurally important part of the sterilization pouches market because the EU MDR ties sterile device packaging to amended EN ISO 11607 compliance. Germany and the United Kingdom stood out as major national markets due to procedure volumes and concentrated medical device manufacturing activity. The EU Packaging and Packaging Waste Regulation is also shaping long-run material choices by pushing packaging design toward recyclability and closer material scrutiny, even though healthcare-specific application realities remain important. Middle East and Africa and South America remained smaller but meaningful, with GCC hospital investment supporting premium demand while Brazil and Argentina continued to grow despite persistent procurement price sensitivity.

Competitive Landscape

The sterilization pouches market is moderately concentrated, with a core group of specialized healthcare packaging suppliers competing across regulated hospital, dental, pharmaceutical, and device packaging applications. Companies such as Amcor, Oliver Healthcare Packaging, Wipak Group under Steriking, and STERIS are important competitors, while DuPont remains highly influential because Tyvek is a key substrate across a large installed base of sterile barrier systems. In this setting, competition is not based on product supply alone. Validation support, technical files, material data, and the ability to guide customers through qualification work are becoming central selling points in the sterilization pouches market. That shift helps larger suppliers because they can support global customers across more sites, more sterilization methods, and more documentation needs.

Several company moves in 2025 and 2026 show how this competitive pattern is taking shape inside the sterilization pouches market. Amcor opened a healthcare packaging coating facility in Malaysia in April 2026, expanded healthcare packaging production in India in June 2026, and achieved cleanroom certification at its Carolina, Puerto Rico thermoforming site in June 2026. These moves point to a strategy built around proximity to OEM clusters, stronger compliance coverage, and better service continuity across regions. Amcor’s Winterbourne site in the United Kingdom also achieved ISO 13485:2016 certification in March 2026, which reinforces the same emphasis on regulated manufacturing readiness.

Material and solution providers are also using innovation to strengthen their position in the sterilization pouches market. DuPont highlighted a sterile barrier redesign through its Sustainable Healthcare Packaging Awards program that removed 64 metric tons of plastic and 4,400 pounds of paper annually, showing how sustainability is becoming part of product differentiation. Wipak’s Steriking business published its HORIZON 2030 strategy in 2026, signaling a stronger focus on innovation, sustainability, and customer value in sterile barrier systems. Solventum’s digital sterility assurance launches also add a systems layer around pouch use rather than pouch supply alone, which can influence purchasing standards over time. The remaining opening is strongest in low-temperature compatible products for smaller clinics and dental settings, where premium products still face affordability limits, and not every tier-one supplier is fully optimized for that price-performance range.

Sterilization Pouches Industry Leaders

Solventum Corporation

STERIS

Amcor

Oliver Healthcare Packaging

Wipak Group (Steriking)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Amcor expanded its healthcare packaging production capabilities at its manufacturing facility in Sira, Karnataka, India, through a multi-million-dollar investment designed to strengthen high-performance packaging and patient-centric drug-delivery solutions for India and South Asia. The site joins three other dedicated Amcor healthcare packaging plants in India, reinforcing the company's regional footprint for sterile medical packaging supply.

- June 2026: Amcor achieved cleanroom certification at its thermoforming facility in Carolina, Puerto Rico, expanding its global cleanroom thermoforming network and strengthening its ability to deliver globally compliant sterile packaging solutions to medical and pharmaceutical customers in the Americas.

- August 2025: BGS US officially opened an electron-beam sterilization facility in Imperial, Pennsylvania, near Pittsburgh International Airport, bringing certified E-Beam radiation sterilization capabilities to the U.S. and serving medical device, pharmaceutical, and biotech manufacturers requiring scalable, sustainable sterilization solutions.

Global Sterilization Pouches Market Report Scope

As per the report’s scope, sterilization pouches are medical-grade packaging solutions designed to protect reusable instruments throughout the sterilization process. They facilitate the penetration of sterilizing agents, such as steam or gas, to eliminate microorganisms. Following sterilization, the pouches serve as sealed sterile barriers, maintaining instrument sterility until the point of use.

The sterilization pouches market is segmented by product type, material type, application, end-user, and geography. By product type, the market is categorized into self-seal pouches, heat-seal pouches, flat pouches, gusseted pouches, foil pouches, sterilization reels and rolls, and other product types. By material type, the market is categorized into paper and plastic, tyvek, non-woven materials, foil and laminated materials, and other material types.

By application, the market is segmented into medical device packaging, surgical instruments packaging, dental instruments packaging, laboratory supplies packaging, pharmaceutical packaging, veterinary instruments packaging, and other applications. By end-user, the market is categorized into hospitals, central sterile services departments, ambulatory surgical centers, dental clinics and practices, medical device manufacturers, and other end-users. Geographically, the market is segmented across North America, Europe, the Asia-Pacific region, the Middle East and Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. For each segment, the market size and forecast are provided in terms of value (USD).

| Self-Seal Pouches |

| Heat-Seal Pouches |

| Flat Pouches |

| Gusseted Pouches |

| Foil Pouches |

| Sterilization Reels and Rolls |

| Other Product Types |

| Paper and Plastic |

| Tyvek |

| Non-Woven Materials |

| Foil and Laminated Materials |

| Other Material Types |

| Medical Device Packaging |

| Surgical Instruments Packaging |

| Dental Instruments Packaging |

| Laboratory Supplies Packaging |

| Pharmaceutical Packaging |

| Veterinary Instruments Packaging |

| Other Applications |

| Hospitals |

| Central Sterile Services Departments |

| Ambulatory Surgical Centers |

| Dental Clinics and Practices |

| Medical Device Manufacturers |

| Other End-Users |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Self-Seal Pouches | |

| Heat-Seal Pouches | ||

| Flat Pouches | ||

| Gusseted Pouches | ||

| Foil Pouches | ||

| Sterilization Reels and Rolls | ||

| Other Product Types | ||

| By Material Type | Paper and Plastic | |

| Tyvek | ||

| Non-Woven Materials | ||

| Foil and Laminated Materials | ||

| Other Material Types | ||

| By Application | Medical Device Packaging | |

| Surgical Instruments Packaging | ||

| Dental Instruments Packaging | ||

| Laboratory Supplies Packaging | ||

| Pharmaceutical Packaging | ||

| Veterinary Instruments Packaging | ||

| Other Applications | ||

| By End-User | Hospitals | |

| Central Sterile Services Departments | ||

| Ambulatory Surgical Centers | ||

| Dental Clinics and Practices | ||

| Medical Device Manufacturers | ||

| Other End-Users | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

Which product format leads current revenue?

Self-seal pouches led product revenue with a 39.10% share in 2025, supported by simple operation and fast use in clinical settings.

Which material is growing fastest in sterile medical packaging?

Tyvek is the fastest-growing material segment, with an 8.16% CAGR through 2031, mainly because it suits low-temperature sterilization methods better than paper-based options.

Why are regulations becoming more important in sterile barrier packaging?

Updated ISO 11607 expectations and EU MDR alignment are raising documentation and validation requirements, which makes technical support and regulatory readiness more important in supplier selection.

Which end-user group is expanding the fastest?

Dental clinics and practices are forecast to grow at an 8.38% CAGR through 2031, driven by wider care access and stronger infection-control enforcement.

Which region offers the strongest growth opportunity through 2031?

Asia-Pacific is the fastest-growing region, with an 8.06% CAGR through 2031, supported by hospital expansion, manufacturing investment, and rising demand across major healthcare systems.

Page last updated on: