Standard Multilayer Printed Circuit Board Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 41.82 Billion |

| Market Size (2031) | USD 52.15 Billion |

| Growth Rate (2026 - 2031) | 4.51% CAGR |

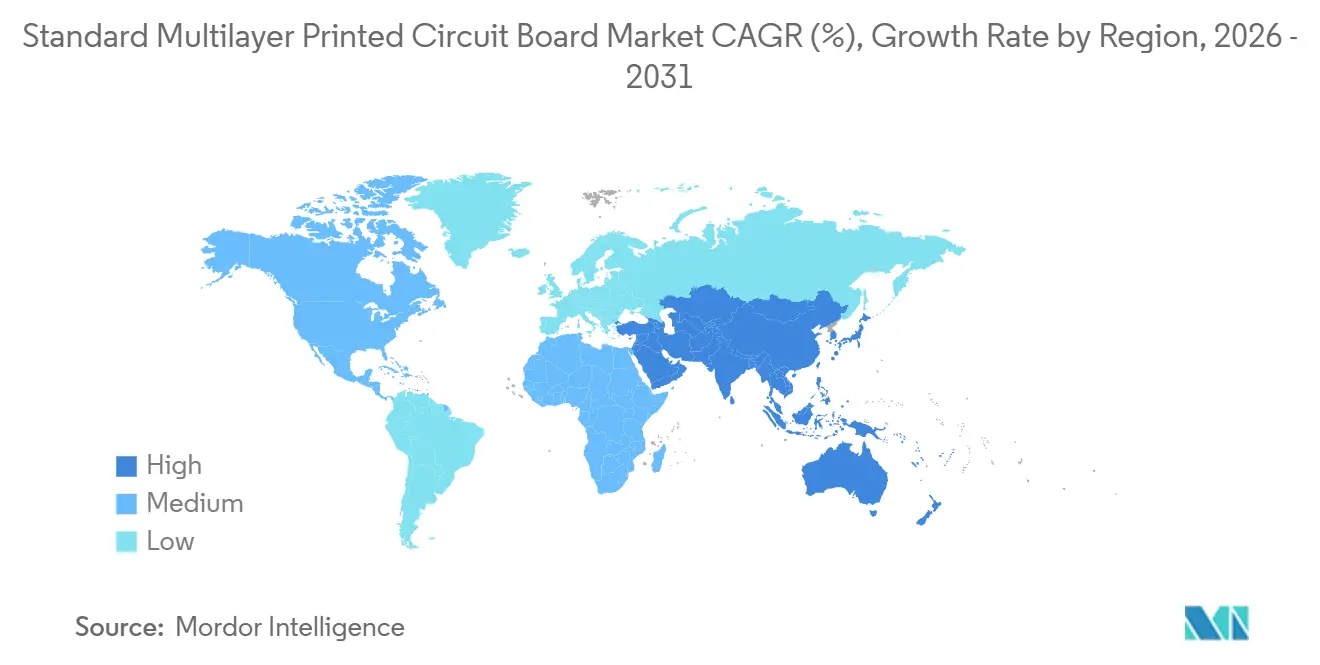

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

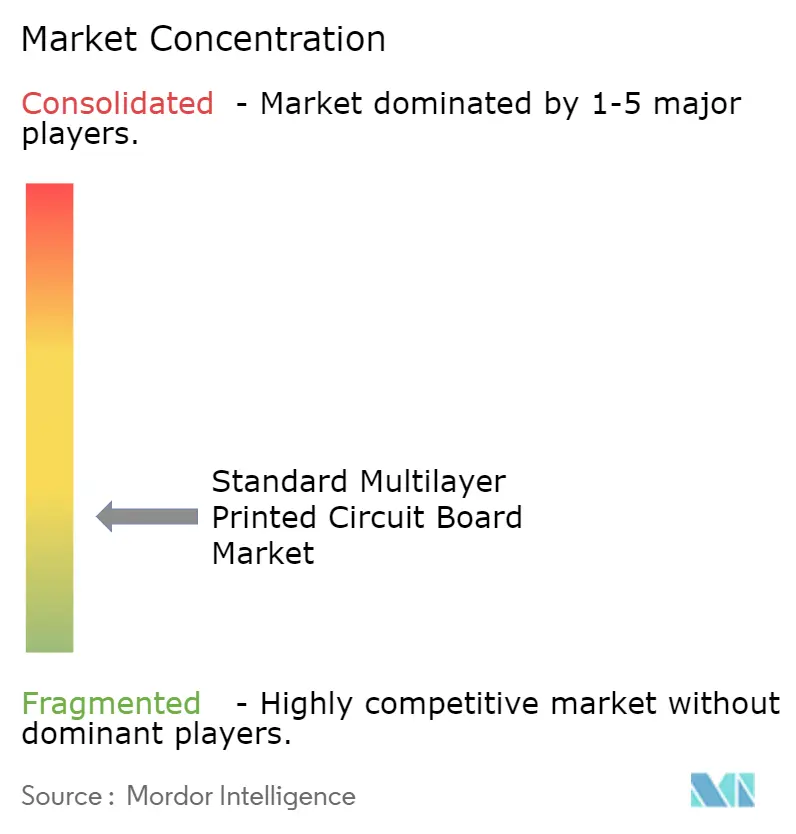

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Standard Multilayer Printed Circuit Board Market Analysis by Mordor Intelligence

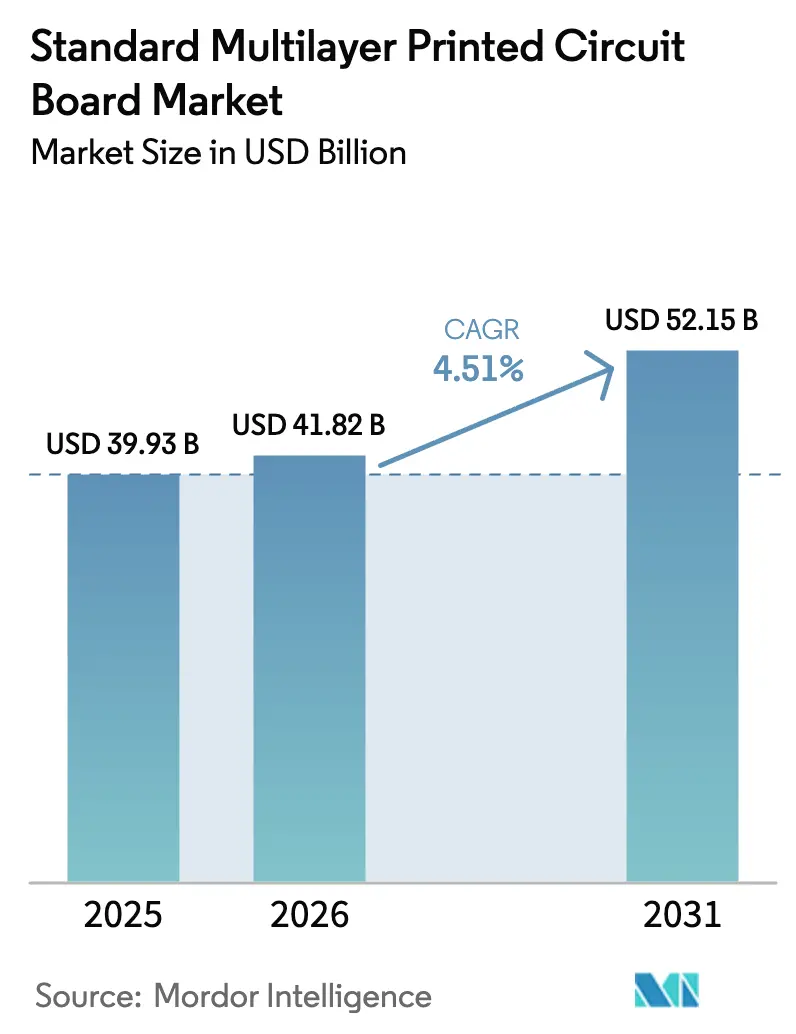

The Standard Multilayer Printed Circuit Board Market was valued at USD 39.93 billion in 2025 and expected to grow from USD 41.82 billion in 2026 to reach USD 52.15 billion by 2031, at a CAGR of 4.51% during the forecast period (2026-2031). Demand is broadening from smartphones and laptops to artificial-intelligence servers, 5G macro-cell radios and advanced driver-assistance vehicles, all of which rely on 10-layer to 24-layer stack-ups that push beyond the electrical and thermal limits of commodity glass-epoxy. Hyperscalers are already re-architecting data-center fabrics around 112 G and 224 G SerDes channels that lose signal integrity on legacy FR-4, forcing a pivot toward ultra-low-loss laminates and reverse-treated copper foils. Automakers are following with zone-controller boards that mirror aerospace tolerances, while satellite primes such as SpaceX bring production in-house to secure supply for constellations that now run into tens of thousands of nodes. Together, these shifts are raising the average layer count, material complexity, and gross value per panel far faster than headline revenue growth implies, repositioning the standard multilayer PCB market as a linchpin of next-generation compute, mobility, and connectivity ecosystems.

Key Report Takeaways

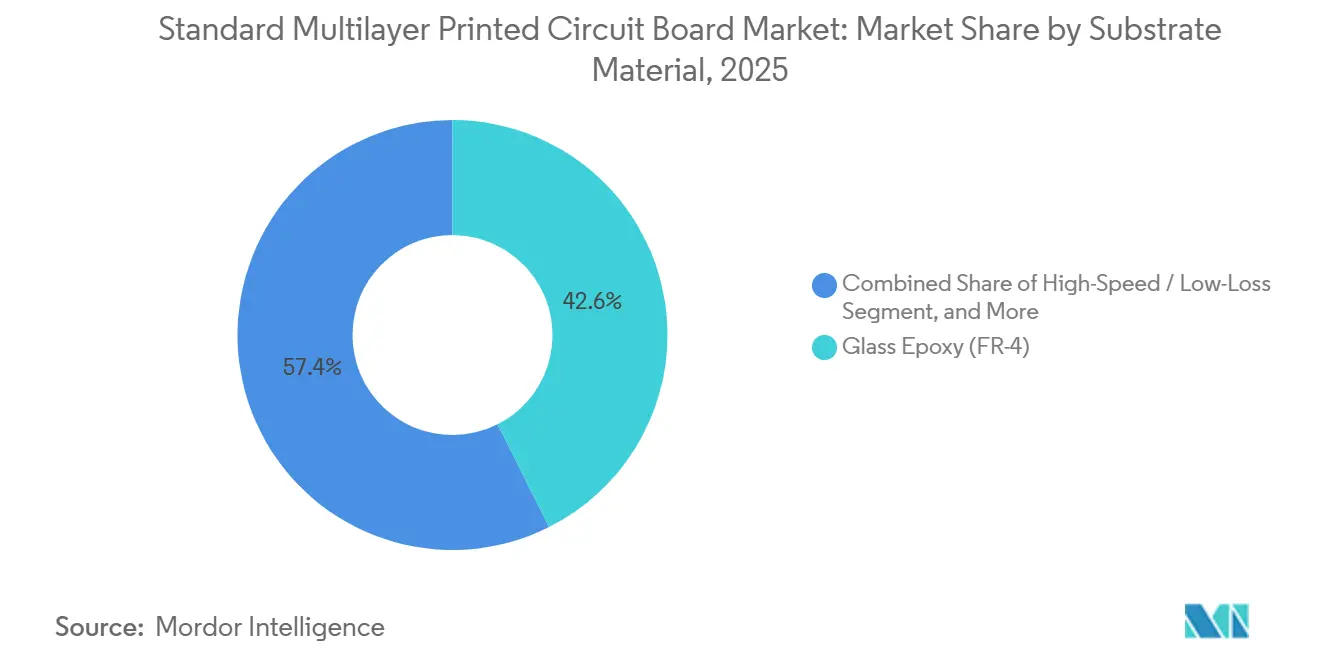

- By substrate material, glass-epoxy (FR-4) led with a 42.59% share of the standard multilayer Printed Circuit Board Market in 2025, while high-speed low-loss laminates are advancing at a 5.63% CAGR through 2031.

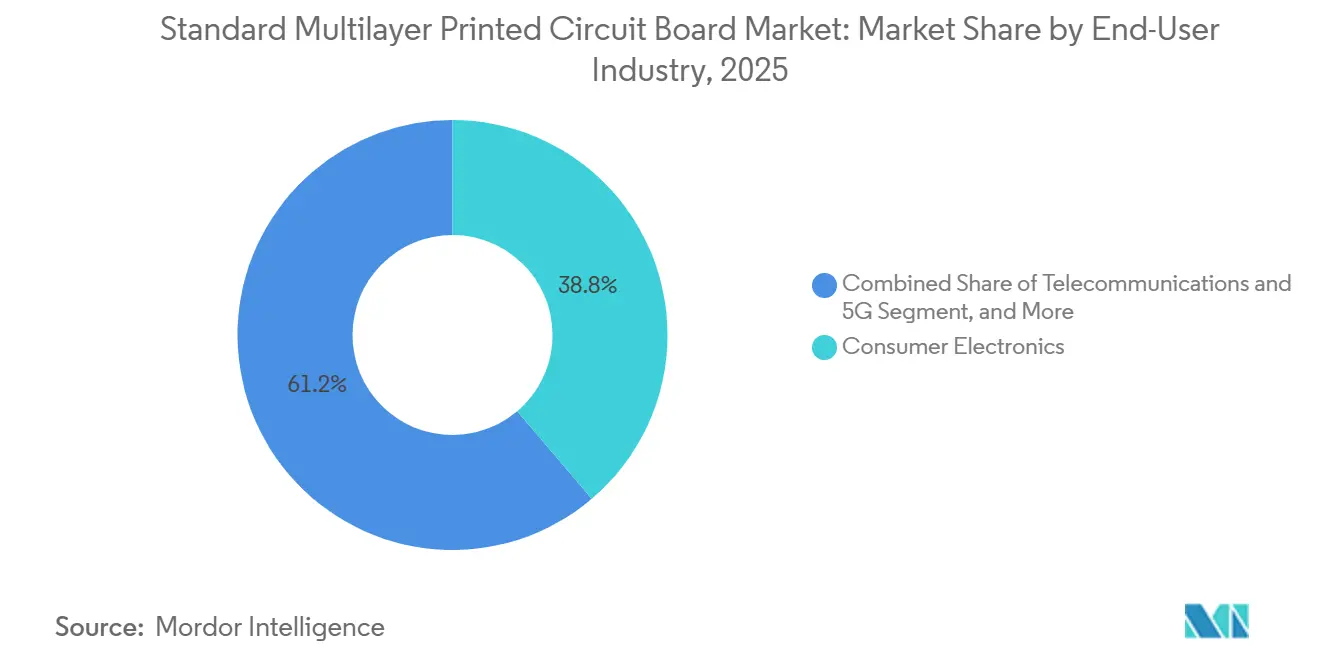

- By end-user industry, consumer electronics accounted for 38.79% of the standard multilayer Printed Circuit Board Market size in 2025, whereas telecommunications and 5G are expanding at the fastest 5.79% CAGR to 2031.

- By geography, Asia-Pacific captured 82.54% revenue in 2025 and is forecast to grow at a 5.25% CAGR, reinforcing its role as the production and demand fulcrum for the standard multilayer Printed Circuit Board Market.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Standard Multilayer Printed Circuit Board Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging Demand for High-Density Interconnects in Smartphones | +0.90% | Global, with concentration in China, Taiwan, South Korea, and India | Medium term (2-4 years) |

| Rapid 5G Base-Station Rollouts Accelerating PCB Upgrades | +1.20% | Global, led by Asia-Pacific (China, India, Southeast Asia), North America, and Europe | Short term (≤ 2 years) |

| Automotive ADAS Penetration Driving Board Layer Counts | +0.80% | Global, with early adoption in Europe, North America, China, and Japan | Long term (≥ 4 years) |

| Data-Center Adoption of 112G/224G SerDes Necessitating Low-Loss Laminates | +1.00% | North America and Europe (hyperscaler hubs), Asia-Pacific (manufacturing and deployment) | Medium term (2-4 years) |

| Government Incentives for Local PCB Fabrication in India and Vietnam | +0.50% | India and Vietnam, with spillover to Southeast Asia | Medium term (2-4 years) |

| Renewed Satellite Constellation Investments Requiring Radiation-Resistant Boards | +0.30% | North America (SpaceX, Amazon), Europe (OneWeb), Asia-Pacific (manufacturing) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surging Demand for High-Density Interconnect Smartphones

Smartphone brands are shifting from 8-layer to 10-layer and 12-layer any-layer HDI to squeeze multi-camera arrays, under-display sensors and high-band 5G antennas into slimmer handsets. Samsung and LG Display accelerated Korea’s any-layer adoption in 2025 by standardizing stacked micro-vias that cut board thickness 20% and lift routing density 35%.[1]Korea Printed Circuit Association, “Technical Bulletin 2025,” KPCA.OR.KR Apple’s requirement that every iPhone logic board use recycled tin forced contract fabricators to validate lead-free profiles across six or more laser-via layers, driving metrology and reflow-oven upgrades. Beyond phones, Starlink user terminals absorb billions of HDI panels per year, underscoring how satellite broadband is emerging as a parallel mass-volume driver. With 2 µm lines now creeping into fan-out wafer-level packages, the boundary between substrate and board is blurring, boosting crossover know-how among HDI shops. Collectively, these trends keep the standard multilayer PCB market on a relentless technology treadmill, shortening equipment depreciation cycles and elevating capital intensity.

Rapid 5G Base-Station Upgrades

GSMA forecasts 5.7 billion 5G connections by 2030, equal to 60% of global mobile subscriptions.[2]GSMA Intelligence, “Mobile Economy 2025,” GSMAINTELLIGENCE.COM Every dense-urban macro cell now integrates 12-layer to 24-layer boards that mix FR-4 power planes with Rogers or Astra MT77 antenna feeds, a hybrid that costs 40% more than legacy LTE designs but halves insertion loss at 28–39 GHz. Ericsson expects a second replacement wave as first-generation radios from 2020-2022 hit obsolescence, lifting outdoor unit demand through 2028. Fabricators must hit copper-foil roughness below 3 µm RMS and contain resin-rich zones to less than 5% of laminate volume to suppress passive intermodulation. Compliance with IPC-6012 Class 3 is now contractual for tier-1 telecom suppliers, adding 15%-20% inspection overhead but rewarding qualified shops with multiyear volume lock-ins. These conditions cement telecommunications as the fastest-growing slice of the standard multilayer PCB market.

Automotive ADAS Penetration

Industry estimate projects 84 million ADAS-equipped vehicles by 2035, versus 53.5 million units in 2023. Each domain controller consolidates radar, lidar and camera fusion onto 16-layer to 20-layer boards that endure −40 °C to +105 °C cycling under AEC-Q100 Grade 2. NVIDIA’s Drive Orin platforms require 75 µm trace-space plus blind-via terminations to curb skew on 12 Gbps camera links. Toyota’s dual-sourcing push into Southeast Asia and India widens regional demand footprints and shortens logistics loops. Centralized zone architectures reduce the number of boards per car but raise value per board up to 80%, enriching the Standard Multilayer PCB market long term as electrification and autonomy converge.

Adoption of 112 G-224 G SerDes in Data Centers

Intel’s 800 Gbps switches allocate just 18 dB of the 30 dB channel budget to PCB traces, ruling out standard FR-4 and mandating laminates with dissipation factors below 0.004.[3]Intel Corp., “Ethernet 800 Series Product Brief 2024,” INTEL.COM Panasonic Megtron 7 and Isola Astra MT77 cost three to four times FR-4 yet guarantee eye openings at 28 GHz Nyquist. Synopsys warns that 224 G lanes at 56 GHz slash loss budgets further, pushing fabricators toward ultra-smooth copper and 180 °C Tg resins. The Optical Internetworking Forum’s co-packaged optics spec shortens reach but dumps 800 W of heat onto a 60 mm × 60 mm substrate, forcing embedded copper blocks and vapor-chamber inlays. Hyperscale’s respond by qualifying captive laminate stacks, driving vertical integration and locking in long-term demand for the standard multilayer Printed Circuit Board Market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile Copper Pricing Squeezing Fabricator Margins | -0.60% | Global, with acute impact on Asia-Pacific fabricators operating on thin margins | Short term (≤ 2 years) |

| Stringent EU RoHS and REACH Updates Increasing Compliance Costs | -0.40% | Europe (direct), global suppliers to EU market (indirect) | Medium term (2-4 years) |

| Supply-Chain Bottlenecks in Ajinomoto Build-up Film (ABF) | -0.30% | Global, concentrated in Taiwan, Japan, and South Korea IC-substrate producers | Medium term (2-4 years) |

| Rising In-house PCB Making by Tier-1 EMS Players | -0.20% | North America and Asia-Pacific, affecting merchant PCB fabricators | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatile Copper Pricing Squeezing Margins

Goldman Sachs pegs average copper at USD 10,710 per tonne for 1H-2026, while J.P. Morgan foresees a 330,000-tonne deficit by year-end due to Zambian outages and Indonesian export curbs. Copper forms up to 30% of a multilayer board’s bill of materials, and a 15% spot swing can wipe 300-400 basis points of gross margin at plants that quote on 60-day cycles. Although giants such as Unimicron hedge on the London Metal Exchange, roughly 40% of Asia-Pacific capacity sits in small and medium enterprises that lack treasury desks. Rapid price spikes can therefore stall production or force line shutdowns, tempering the growth trajectory of the standard multilayer Printed Circuit Board Market in the near term.

Stringent EU RoHS and REACH Updates

The European Commission will withdraw remaining lead-solder exemptions for industrial and medical gear by 2027, while the European Chemicals Agency extended exemption reviews from 18 to 24 months. Compliance compels thermal-cycle testing to IPC-9701, adds two to three weeks to new-product introduction and costs EUR 50,000-100,000 (USD 56,000-112,000) per product family for mid-tier shops. The concurrent Ecodesign Regulation and Stockholm POPs bans pressure fabricators to adopt halogen-free resins and verify recyclability, lifting documentation overhead. Well-capitalized groups fold the expense into premium pricing, but smaller exporters face up to 100 basis-point margin erosion, diluting returns across the standard multilayer Printed Circuit Board Market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Substrate Material: High-Speed Laminates Secure Premium Value

High-speed low-loss laminates are growing at a 5.63% CAGR between 2026 and 2031, outpacing overall sector growth and siphoning revenue from glass-epoxy. In absolute terms, glass-epoxy retained 42.59% of the standard multilayer Printed Circuit Board Market share in 2025, reflecting its USD 8-12 per square-meter price advantage. Yet migration to 10 GHz-plus applications means every deployed rack of AI servers or millimeter-wave radios contains at least two panels built on Megtron 7 or Astra MT77, each priced at USD 30-50 per square meter, expanding the premium layer of the standard multilayer printed circuit board market.

The differential is widening. Elite Material’s NTD 2.78 billion investment (USD 88.5 million) in Taoyuan launches in 2H-2026, while Shengyi expands high-frequency CCL by 30% to chase 5G and radar orders. Polyimide remains essential for -55 °C to +200 °C military avionics, but its cost five to eight times FR-4 caps share growth. As volume tilts toward low-loss CCL, commodity FR-4 plants risk utilization gaps unless they retrofit press lines, a strategic fork that could reshape capacity allocation in the standard multilayer Printed Circuit Board Market.

By End-User Industry: Telecommunications and 5G Outpace Legacy Segments

Telecommunications and 5G logged the highest 5.79% CAGR forecast, propelled by 5.7 billion projected 5G connections by 2030. Consumer electronics still dominated revenue in 2025, but handset shipments flattened as brands extended replacement cycles for sustainability ratings. Hyperscale computing and data-center buyers co-invest with board suppliers to lock down 16-layer to 20-layer panels that sustain 112 G links, adding stickiness to this sub-segment.

Automotive and EV growth accelerates as centralized zone architectures proliferate; each controller commands USD 60-80 of PCB content, more than double a legacy ECU. Industrial and power gear favour 3-oz to 6-oz heavy-copper builds for 20-year field life, creating a stable, if slower, baseline for the standard multilayer PCB industry. Healthcare, aerospace and defense remain niche but margin-rich, leveraging controlled outgassing polyimide or halogen-free FR-4 to meet strict regulatory frameworks. Overall, vertical diversification cushions cyclical swings and lifts blended ASPs across the standard multilayer Printed Circuit Board Market.

Geography Analysis

Asia-Pacific anchored 82.54% of global revenue in 2025 and is forecast to grow at 5.25% through 2031, underscoring its centrality to the standard multilayer Printed Circuit Board Market. China and Taiwan together supplied 65% of worldwide output, with Taiwan’s TWD 735 billion production (USD 23.5 billion) equal to 30% of global value. Mainland China contributed about CNY 350 billion (USD 48.3 billion) the same year, fuelled by aggressive HDI capacity additions in Guangdong and Jiangsu provinces. Government stimulus stacks on top: India’s Electronics Component Manufacturing Scheme allocates INR 22,919 crore (USD 2.75 billion) and reimburses up to 10% of capital outlay, while Vietnam’s Circular 33/2025 pegs corporate tax breaks to 30% local-supplier content, nudging multinationals into regional joint ventures.

North America represents a small share yet punches above its weight in high-reliability boards for aerospace, defense and data centers. TTM Technologies booked USD 579 million in Q3-2024, with 44% from defense, protecting the firm from consumer downturns. SpaceX’s Bastrop plant, claimed to be the continent’s largest by volume, will funnel thousands of satellite antenna panels per day into captive channels, demonstrating how strategic vertical integration can reshape local supply chains.

Europe sits between the cost efficiency of Asia and the national-security imperatives of North America. Austria-based AT&S is pouring EUR 300 million (USD 336 million) into Leoben for automotive and industrial substrates, and Germany’s tier-1 carmakers routinely dual-source from European fabs to meet stringent RoHS and REACH audit trails. The rest of world block Latin America, Middle East and Africa remains nascent but is courting foreign direct investment: Mexico’s shelter manufacturing model and Morocco’s Tanger Med free zone both promote nearshoring strategies that could capture spillover demand from the standard multilayer printed circuit board market as geopolitical risks drive supply-chain diversification.

Competitive Landscape

The standard multilayer Printed Circuit Board Market exhibits a K-shaped structure. Hundreds of small and medium Chinese and Taiwanese plants fight over commodity FR-4, while a dozen oligopolists capture more than half the profits in advanced substrates. AT&S integrates laminate, board and substrate lines under one roof, enabling 40-50% higher blended gross margin than peers that must source copper-clad laminate externally. Unimicron pulled 49.2% of 2024 revenue from Ajinomoto build-up film substrates, a lucrative but capacity-constrained niche that also exposes the company to supply risk as ABF expansions lag demand.

White-space opportunities emerge in the 10-layer to 16-layer band, where ADAS cars, industrial robots and medical scanners need Class-3 process control but not the extreme line-width tolerances of IC substrates. Players that upgrade press lines and laser drills without overinvesting in substrate plating can secure 15-20% EBITDA margins, above the commodity average yet below elite substrate specialists. Technology gaps widen as 30-40% of Asia-Pacific capacity still uses photographic film rather than direct imaging, limiting yield on 75 µm trace-space designs and pushing OEMs toward vetted partners.

Backward integration is the disruptor to watch. SpaceX already makes its own antenna boards, and Amazon is rumoured to invest in Kuiper substrates. Such moves remove merchant volume and tighten supply for smaller brands, potentially triggering further consolidation. Standards escalation compounds this trend: IPC-6012 Class 3, IPC-A-600 Class 3 and incoming ISO 17 121 traceability norms raise capex thresholds, compelling sub-scale fabs either to merge or exit, thereby reshaping the competitive topology of the standard multilayer printed circuit board market.

Standard Multilayer Printed Circuit Board Industry Leaders

Zhen Ding Technology Holding Limited

Nippon Mektron, Ltd.

Unimicron Technology Corporation

TTM Technologies Inc.

AT&S AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Vietnam’s Ministry of Science and Technology activated Circular 33/2025, linking corporate tax incentives for electronics projects to 30% domestic supplier content and verifiable PCB layout ownership.

- December 2025: AT&S confirmed that its Kulim, Malaysia campus, a EUR 2.3 billion (USD 2.6 billion) project, entered ramp-up for AI and high-performance computing substrates, targeting volume output by 2H-2026.

- November 2025: Unimicron allocated TWD 35 billion (USD 1.1 billion) for additional ABF substrate lines in Taoyuan and Shanying, with first capacity slated for 1H-2026.

- October 2025: Samsung Electro-Mechanics reported KRW 10.8 trillion (USD 8.1 billion) 2024 revenue and detailed plans to double flip-chip BGA capacity in Vietnam to serve hyperscale AI demand.

Global Standard Multilayer Printed Circuit Board Market Report Scope

The Standard Multilayer Printed Circuit Board Market Report is Segmented by Substrate Material (Glass Epoxy (FR-4), High-Speed/Low-Loss, Polyimide (PI)), End-User Industry (Consumer Electronics, Computing and Data Centers, Telecommunications and 5G, Automotive and EV, Industrial and Power, Healthcare/Medical, Aerospace and Defense, Other End-user Industries), and Geography (North America, Europe, Asia-Pacific, Rest of World). The Market Forecasts are Provided in Terms of Value (USD).

| Glass Epoxy (FR-4) |

| High-Speed / Low-Loss |

| Polyimide (PI) |

| Packaging Resins (BT / ABF) |

| Other Substrate Materials |

| Consumer Electronics |

| Computing and Data Centers |

| Telecommunications and 5G |

| Automotive and EV |

| Industrial and Power |

| Healthcare / Medical |

| Aerospace and Defense |

| Other End-user Industries |

| North America | United States |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Netherlands | |

| Rest of Europe | |

| Asia-Pacific | China |

| Taiwan | |

| Japan | |

| India | |

| South Korea | |

| Southeast Asia | |

| Rest of Asia-Pacific | |

| Rest of World |

| By Substrate Material | Glass Epoxy (FR-4) | |

| High-Speed / Low-Loss | ||

| Polyimide (PI) | ||

| Packaging Resins (BT / ABF) | ||

| Other Substrate Materials | ||

| By End-User Industry | Consumer Electronics | |

| Computing and Data Centers | ||

| Telecommunications and 5G | ||

| Automotive and EV | ||

| Industrial and Power | ||

| Healthcare / Medical | ||

| Aerospace and Defense | ||

| Other End-user Industries | ||

| By Geography | North America | United States |

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Taiwan | ||

| Japan | ||

| India | ||

| South Korea | ||

| Southeast Asia | ||

| Rest of Asia-Pacific | ||

| Rest of World | ||

Key Questions Answered in the Report

What is the current value of the standard multilayer Printed Circuit Board Market?

The standard multilayer Printed Circuit Board Market size stood at USD 41.82 billion in 2026 and is set to rise to USD 52.15 billion by 2031.

Which end-user vertical is growing the fastest?

Telecommunications and 5G leads with a projected 5.79% CAGR through 2031, driven by dense 5G macro-cell upgrades.

Why are low-loss laminates gaining share?

112 G and 224 G SerDes channels in AI servers and 5G radios exceed FR-4 loss budgets, pushing demand toward Megtron 7, Astra MT77 and similar materials.

How will EU RoHS changes affect suppliers?

The 2027 lead-solder phase-out will extend product-qualification cycles by up to three weeks and raise compliance costs, squeezing smaller fabricators.

Which region dominates production?

Asia-Pacific accounts for more than 80% of revenue, with China and Taiwan together supplying 65% of global output.

What is the biggest near-term risk to margins?

Copper price volatility could remove 300-400 basis points of gross margin for shops that cannot hedge or rapidly reprice.

Page last updated on: