Stainless Steel Kirschner Wires Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

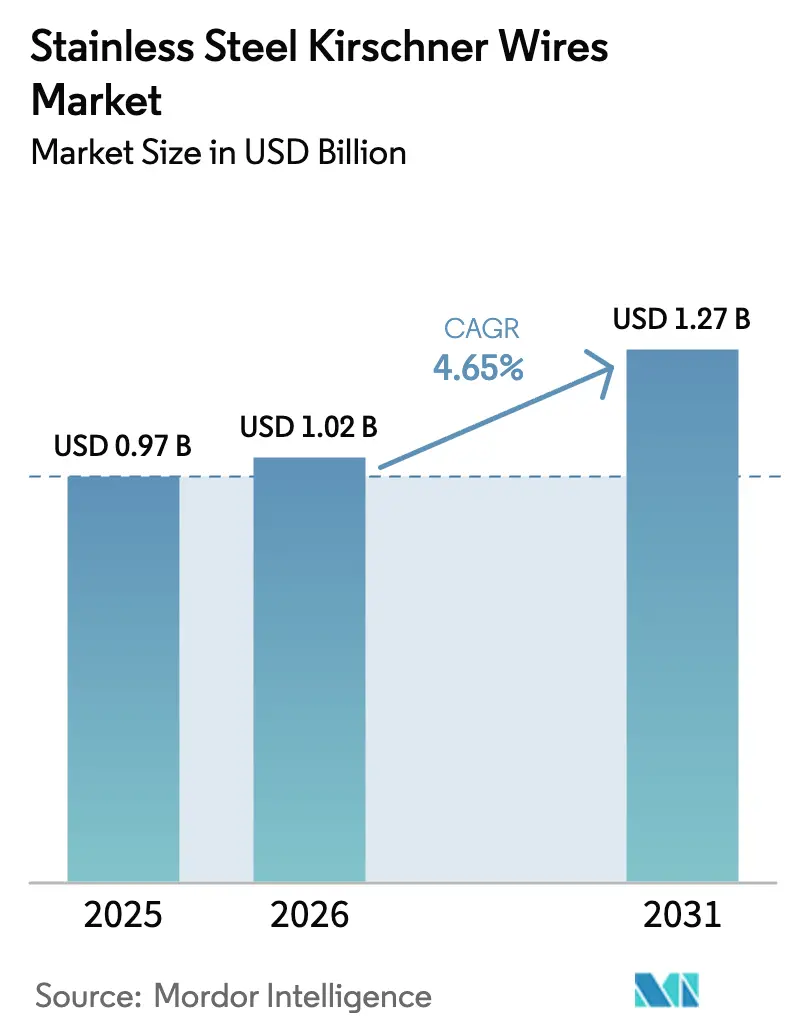

| Market Size (2026) | USD 1.02 Billion |

| Market Size (2031) | USD 1.27 Billion |

| Growth Rate (2026 - 2031) | 4.65% CAGR |

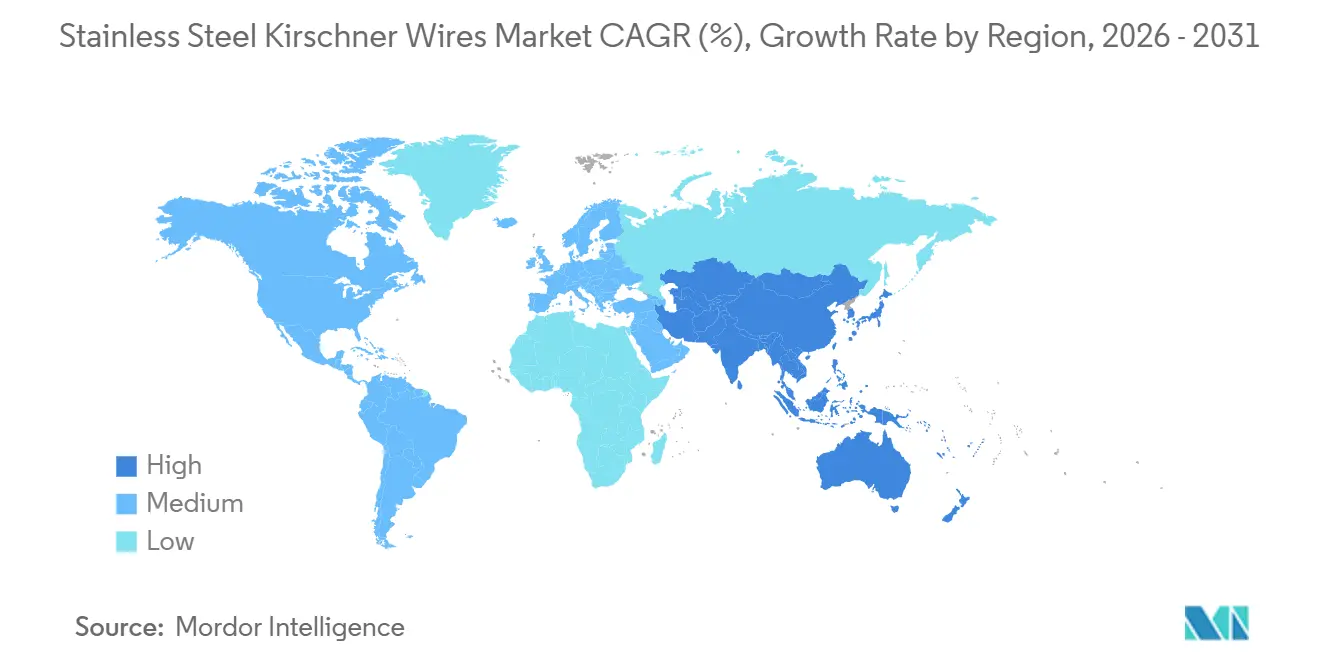

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Stainless Steel Kirschner Wires Market Analysis by Mordor Intelligence

The Stainless Steel Kirschner Wires Market size is expected to increase from USD 0.97 billion in 2025 to USD 1.02 billion in 2026 and reach USD 1.27 billion by 2031, growing at a CAGR of 4.65% over 2026-2031.

Current growth reflects rising fracture volumes in aging populations, wider acceptance of minimally invasive pinning, and the shift of routine trauma care to ambulatory surgical centers[1]National Center for Biotechnology Information, “The Global Burden of Fractures,” ncbi.nlm.nih.gov. Superior biomechanical performance of larger-diameter wires, combined with reimbursement incentives for outpatient hand and foot procedures, is steering product mix toward premium, single-use sterile kits[2]Centers for Medicare & Medicaid Services, “Ambulatory Surgical Center Payment,” cms.gov . Manufacturers that balance cost control with improvements in MRI compatibility and infection mitigation are positioned to capture unmet needs. Competitive focus is moving away from commodity K-wires toward value-added coatings and threaded designs that reduce migration in weight-bearing bones. Regionally, North America retains the largest share, yet Asia-Pacific delivers the fastest incremental demand due to policy-led import substitution and expanding local device capacity.

Key Report Takeaways

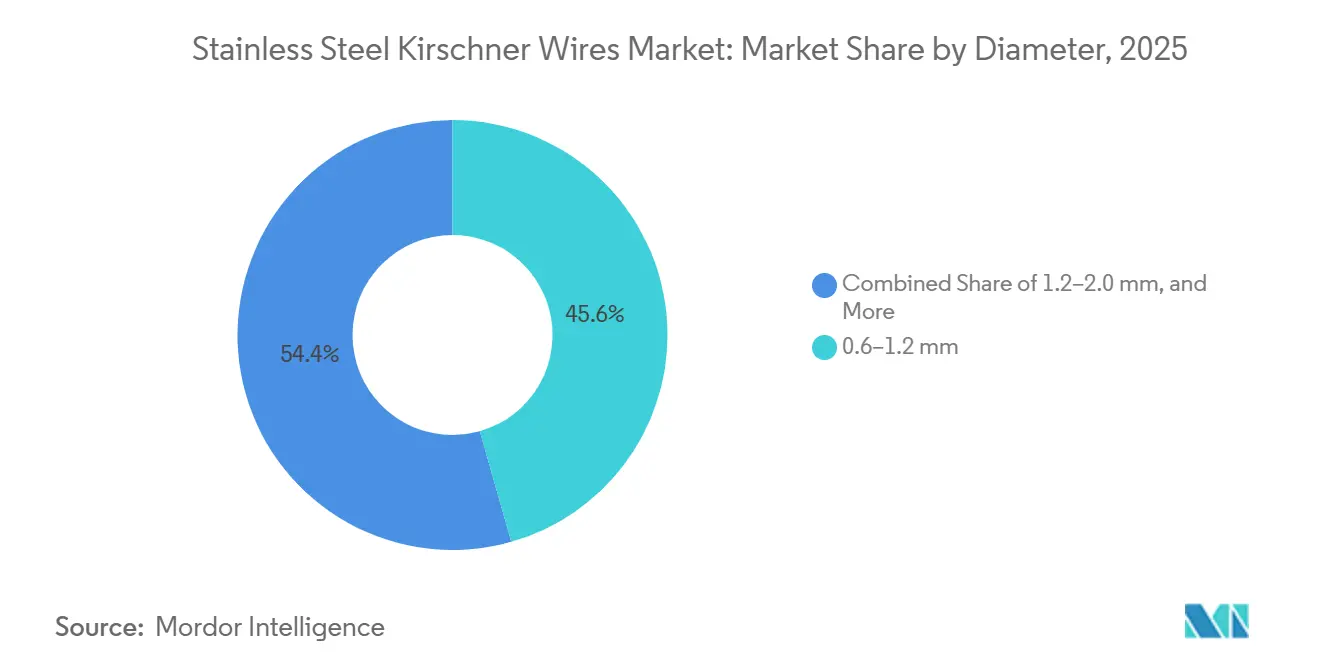

- By diameter, the 1.2–2.0 mm segment led with 45.55% market share for stainless steel Kirschner wires in 2025, whereas the >2.0 mm segment is set to advance at an 8.25% CAGR through 2031.

- By tip type, smooth wires accounted for 61.23% of 2025 revenue; threaded variants are forecast to grow at a 9.15% CAGR through 2031.

- By application, trauma and fracture fixation commanded 48.15% of 2025 revenue, while pediatric orthopedics is projected to expand at an 8.51% CAGR over the same horizon.

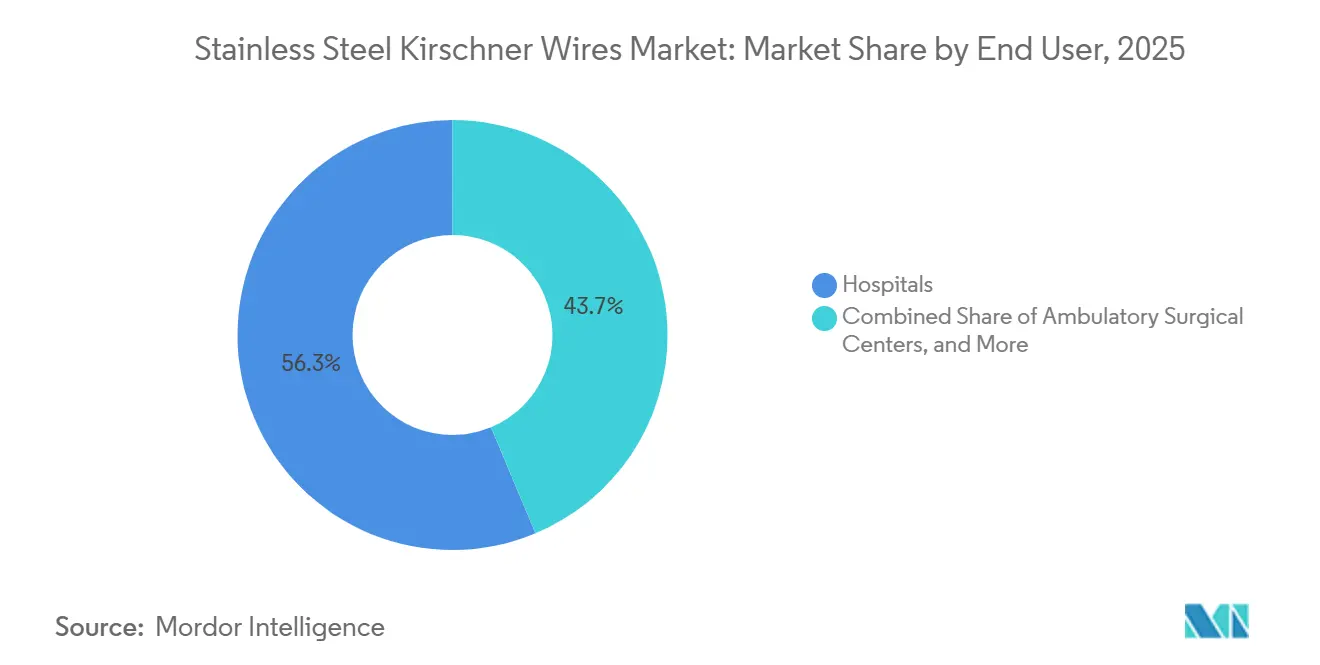

- By end user, hospitals accounted for 56.35% of sales in 2025; ambulatory surgical centers are expected to post a 9.11% CAGR through 2031.

- North America accounted for 35.25% of 2025 revenue, yet Asia-Pacific is on track for an 8.02% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Stainless Steel Kirschner Wires Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Incidence of Orthopedic Fractures among Aging Population | +1.2% | North America, Europe, Japan, South Korea | Long term (≥ 4 years) |

| Growing Adoption of Minimally Invasive Percutaneous Pinning Techniques | +1.0% | North America, Europe, urban Asia-Pacific | Medium term (2-4 years) |

| Surge In Sports-Related Injuries in Emerging Economies | +0.8% | China, India, Southeast Asia, Latin America | Medium term (2-4 years) |

| Increasing Use of MRI-Compatible Carbon-Fiber Reinforced Stainless-Steel K-Wires | +0.6% | North America, Europe | Long term (≥ 4 years) |

| Shift Toward Outpatient Surgeries and Single-Use Sterile Wires | +0.9% | North America, Europe, selected Asia-Pacific markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Incidence of Orthopedic Fractures Among Aging Population

Global life-expectancy gains are driving higher fracture volumes, particularly at distal radius, metacarpal, and metatarsal sites that lend themselves to K-wire fixation. United States emergency rooms handled 3.85 million geriatric fractures between 2019 and 2023, over half of which required hospitalization. Same-day percutaneous pinning in ambulatory centers now shortens stays and increases the number of wire units per case. Japan and South Korea, both with median ages above 48 years, show parallel demand patterns, while China’s population aged 60 and older is projected to exceed 400 million by 2035, reinforcing long-run growth.

Growing Adoption of Minimally Invasive Percutaneous Pinning Techniques

Percutaneous K-wires reduce operative time, soft-tissue disruption, and equipment costs compared with open plating. Contemporary studies report pin-tract infection rates ranging from 0% to 30%, depending on care protocols and retention duration [3].Radiopaedia Editors, “Kirschner Wire,” radiopaedia.org Hand and wrist surgeons favor fluoroscopy-guided pinning because slim wires preserve tendon glide, and pediatric data show 85-97% excellent or good outcomes despite infection risk. Migration toward outpatient settings amplifies the value proposition for this technique.

Surge in Sports-Related Injuries in Emerging Economies

Higher urban incomes and increased participation in organized sports are associated with higher fracture incidence among adolescents and young adults in the Asia-Pacific and Latin America. Hospital surveys in India and China reveal a higher prevalence of metacarpal and metatarsal fractures requiring percutaneous fixation. Domestic manufacturers in both nations now offer ASTM F138-compliant wires at price points aligned with public procurement, meeting rising procedure volumes while limiting reliance on imports.

Increasing Use of MRI-Compatible Carbon-Fiber Reinforced Stainless-Steel K-Wires

Conventional stainless steel distorts MRI images, whereas carbon-fiber-reinforced hybrids reduce artifacts by up to 80%, improving postoperative assessment of surrounding soft tissue. Early adopters in North American and European tertiary centers accept a 30-40% price premium for clearer scans that reduce repeat imaging. Regulatory clarity and ASTM adoption will dictate the eventual scale of this niche.

Restraints Impact Analysis*

| Restraint | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Pin-Tract Infection Risk and Need For Removal Surgery | -0.7% | Global, more pronounced in low-resource settings | Medium term (2-4 years) |

| Substitution by Cannulated Screws and Bio-Absorbable Pins | -0.5% | North America, Europe | Long term (≥ 4 years) |

| Specialty-Grade 316L Stainless-Steel Supply Volatility | -0.3% | Global | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Pin-Tract Infection Risk and Need for Removal Surgery

Infections remain the most common complication, reported in up to 30% of K-wire cases depending on hygiene and duration. Superficial cases respond to antibiotics, but deep infections may demand wire removal, risking loss of fixation and extra surgery. Diabetes, immunosuppression, and retention beyond eight weeks raise odds. Buried-wire techniques reduce exposure but compromise bedside extraction, limiting their universal uptake.

Substitution by Cannulated Screws and Bio-Absorbable Pins

Cannulated screws deliver superior rotational stability for slipped capital femoral epiphysis and scaphoid fractures, though they cost two to three times more and require larger incisions. Bio-absorbable magnesium or poly-L-lactic acid pins remove the need for hardware removal, but remain expensive and mechanically less robust. Where payer budgets allow, these options siphon share from the stainless steel Kirschner wires market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Diameter: Larger Wires Gain Traction on Mechanical Grounds

The 1.2–2.0 mm category accounted for 45.55% of revenue in 2025, reflecting its adaptability across wrist, forearm, and foot procedures. A 2024 biomechanical study reported that 2.0 mm wires showed greater axial and flexion stiffness than 1.6 mm alternatives in distal radius models. Consequently, the >2.0 mm group is expected to achieve an 8.25% CAGR through 2031 as surgeons select sturdier wires for osteoporotic bone. Smaller diameters of 0.6–1.2 mm continue to serve pediatric hand fractures where growth-plate safety is critical. The stainless steel Kirschner wire market size in the >2.0 mm segment is projected to expand as complex trauma volumes rise.

Demand patterns diverge by specialty. Foot surgeons increasingly choose 1.6–2.0 mm wires after evidence linked 1.2 mm constructs to higher breakage in metatarsophalangeal joints. Hand surgeons still favor 1.0–1.6 mm options for their slim profile, yet threaded versions within this range are advancing, even though migration risk is elevated. Cannulated formats in diameters over 2.0 mm blur lines with screws, offering guidewire precision and attracting adopters in obese and geriatric cohorts seeking robust fixation.

By Tip Type: Threads Curb Migration in Load-Bearing Sites

Smooth tips secured 61.23% of 2025 sales thanks to quick insertion and easy removal in pediatric and hand cases. Threaded tips, however, are anticipated to expand at a 9.15% CAGR, as studies show a 40-60% reduction in wire migration during weight-bearing periods of the foot and ankle. Surgeons accept a modest rise in drilling time to gain this stability, particularly in outpatient arthrodesis, where early mobilization is desired. The stainless steel Kirschner wire market size, driven by threaded designs, will increase in parallel.

Adoption of threaded wires is accelerating as ambulatory centers emphasize same-day weight-bearing. Manufacturers differentiate through fine-pitch threads for metaphyseal bone and coarse-pitch threads for diaphyseal zones. Smooth wires remain the standard in supracondylar humerus repairs, where retention lasts only 4 to 6 weeks, and migration risk is minor.

By Application: Pediatric Orthopedics Delivers Outsize Growth

Trauma and fracture fixation accounts for the largest revenue share at 48.15%, yet growth aligns with the overall market CAGR. Pediatric orthopedics, in contrast, is slated for an 8.51% CAGR through 2031 as clinical data confirm up to 97% good outcomes in forearm and elbow fractures managed with K-wires. The stainless steel Kirschner wires market share derived from pediatric cases will rise as day-surgery protocols favor simple, removable hardware.

Hand and wrist indications remain steady, anchored by scaphoid and Bennett fractures that benefit from low-profile pins. Foot and ankle volumes expand alongside outpatient arthrodesis, where threaded 1.6–2.0 mm wires resist migration during rehabilitation. Temporary joint stabilization during ligament repairs and provisional fixation during plating account for the residual segment, paced by the broader adoption of minimally invasive techniques.

By End User: Ambulatory Centers Erode Hospital Dominance

Hospitals accounted for 56.35% of 2025 purchases, but ambulatory surgical centers are projected to have a 9.11% CAGR as Medicare and private payers encourage outpatient care. Single-use sterile kits suit ASC workflows, eliminating sterilization costs and lowering infection liability. The stainless steel Kirschner wires market size attached to ASCs will therefore rise faster than the inpatient share.

Specialty orthopedic clinics in emerging regions are also rising, sourcing cost-effective wires from domestic manufacturers that comply with ASTM F138. Hospitals will sustain share in polytrauma and open fractures requiring intensive resources, but low-complexity cases will increasingly migrate to outpatient settings

Geography Analysis

North America contributed 35.25% of 2025 revenue, supported by high procedure rates, mature trauma networks, and reimbursement that rewards outpatient pinning. Medicare Advantage penetration reached 54% in 2024, reinforcing the cost pressure that favors K-wires over pricier screws. Canada and Mexico mirror the U.S. in adopting single-use kits, with Mexico’s medical-tourism clinics performing hand and foot surgeries at 40–60% lower fees for U.S. patients.

Asia-Pacific is forecast to have an 8.02% CAGR to 2031. China cleared 79 Class III orthopedic devices in the first nine months of 2024, accelerating domestic substitution and trimming multinational prices by up to 30%. India’s Production Linked Incentive scheme incentivizes local implant manufacturing, reducing import dependence and expanding access to ASTM-grade wires. Japan’s aging population sustains steady demand, while South Korea and Australia post above-average growth, driven by sports trauma volumes and private clinic expansion.

Europe holds a mid-teens share. The region’s Medical Device Regulation has slowed new launches, giving incumbents with grandfathered approvals a temporary edge. Long National Health Service waiting lists in the United Kingdom steer patients toward private centers that favor same-day pinning. Middle East, Africa, and South America make up a low-teens collective share, with growth concentrated in urban hubs like Dubai and São Paulo where private pay clients seek rapid fracture care.

Competitive Landscape

Market concentration is moderate. Stryker, DePuy Synthes, Zimmer Biomet, Smith & Nephew, and Medtronic together command a meaningful but not dominant slice, leaving space for regional specialists. Stryker booked USD 2.2 billion in orthopedics revenue in Q3 2024 and purchased Vertos Medical for USD 850 million to deepen its spine offering rather than expand commodity pins. Zimmer Biomet’s USD 1.9 billion Q3 2024 sales included the Embody acquisition to enhance biologics. Smith & Nephew’s orthopedics revenue grew 6.1% to USD 1.1 billion in H1 2024, aided by connected instruments that anchor implant pull-through.

Multinationals regard K-wires as consumables that complete trauma trays, dedicating R&D toward robotics and patient-specific implants with margins above 70%. Innovation opportunities persist in MRI-friendly hybrids, threaded foot-and-ankle designs, and single-use ASC kits, but ASTM standards for carbon-fiber composites remain pending. Domestic players in China, India, and Brazil leverage cost advantage and policy support to undercut global brands by up to 40%, targeting public tenders and export to neighboring regions.

Stainless Steel Kirschner Wires Industry Leaders

DePuy Synthes (Johnson & Johnson)

Medtronic plc

Smith & Nephew plc

Stryker Corporation

Zimmer Biomet

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2024: Stryker completed the USD 850 million acquisition of Vertos Medical to add minimally invasive spine solutions.

- July 2024: ConMed received a U.S. patent for sterile K-wire packaging that integrates caps and removal guides, streamlining ASC workflows.

Global Stainless Steel Kirschner Wires Market Report Scope

As per the report's scope, stainless steel Kirschner wires (K‑wires) are slender, rigid surgical wires commonly used in orthopedic and trauma procedures. They serve as fixation devices to stabilize bone fragments, guide implants, or provide temporary skeletal support during healing. Their biocompatibility, strength, and ease of insertion make them essential tools for minimally invasive fracture management and small-bone surgeries.

The stainless steel Kirschner wires market segmentation includes diameter, tip type, application, end user, and geography. By diameter, the market is segmented into 0.6–1.2 mm, 1.2–2.0 mm, and > 2.0 mm. By tip type, the market is segmented into smooth tip and threaded tip. By application, the market is segmented into trauma & fracture fixation, foot & ankle surgery, hand & wrist surgery, pediatric orthopedics, and other applications. By end user, the market is segmented into hospitals, ambulatory surgical centers, and specialty orthopedic clinics. By geography, the market is segmented into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The market report also covers estimated market sizes and market trends for 17 countries across major regions worldwide. The report offers market value (in USD) for the above segments.

| 0.6–1.2 mm |

| 1.2–2.0 mm |

| 2.0 mm |

| Smooth Tip |

| Threaded Tip |

| Trauma & Fracture Fixation |

| Foot & Ankle Surgery |

| Hand & Wrist Surgery |

| Pediatric Orthopedics |

| Other Applications |

| Hospitals |

| Ambulatory Surgical Centers |

| Specialty Orthopedic Clinics |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Diameter | 0.6–1.2 mm | |

| 1.2–2.0 mm | ||

| 2.0 mm | ||

| By Tip Type | Smooth Tip | |

| Threaded Tip | ||

| By Application | Trauma & Fracture Fixation | |

| Foot & Ankle Surgery | ||

| Hand & Wrist Surgery | ||

| Pediatric Orthopedics | ||

| Other Applications | ||

| By End User | Hospitals | |

| Ambulatory Surgical Centers | ||

| Specialty Orthopedic Clinics | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How fast is the stainless steel Kirschner wires market expected to grow through 2031?

Revenue is forecast to rise from USD 0.97 billion in 2026 to USD 1.27 billion by 2031, corresponding to a 4.65% CAGR.

Which diameter segment is gaining momentum?

Wires larger than 2.0 mm are projected to post an 8.25% CAGR, outpacing smaller sizes due to superior mechanical stability.

Why are ambulatory surgical centers significant for future demand?

Reimbursement favors outpatient hand and foot trauma, and single-use sterile wire kits match ASC workflows that lack central sterilization.

What is the main clinical drawback of K-wire fixation?

Pin-tract infections can affect up to 30% of cases, sometimes forcing early hardware removal and additional treatment.

Which region will add the most incremental revenue?

Asia-Pacific, driven by local manufacturing in China and India and a projected 8.02% CAGR through 2031.

How are manufacturers differentiating their K-wire offerings?

Firms add threaded tips to curb migration, explore carbon-fiber reinforcement to improve MRI imaging, and supply procedure-specific sterile kits for outpatient centers.

Page last updated on: