SRAM Near-Memory Cache Compute Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

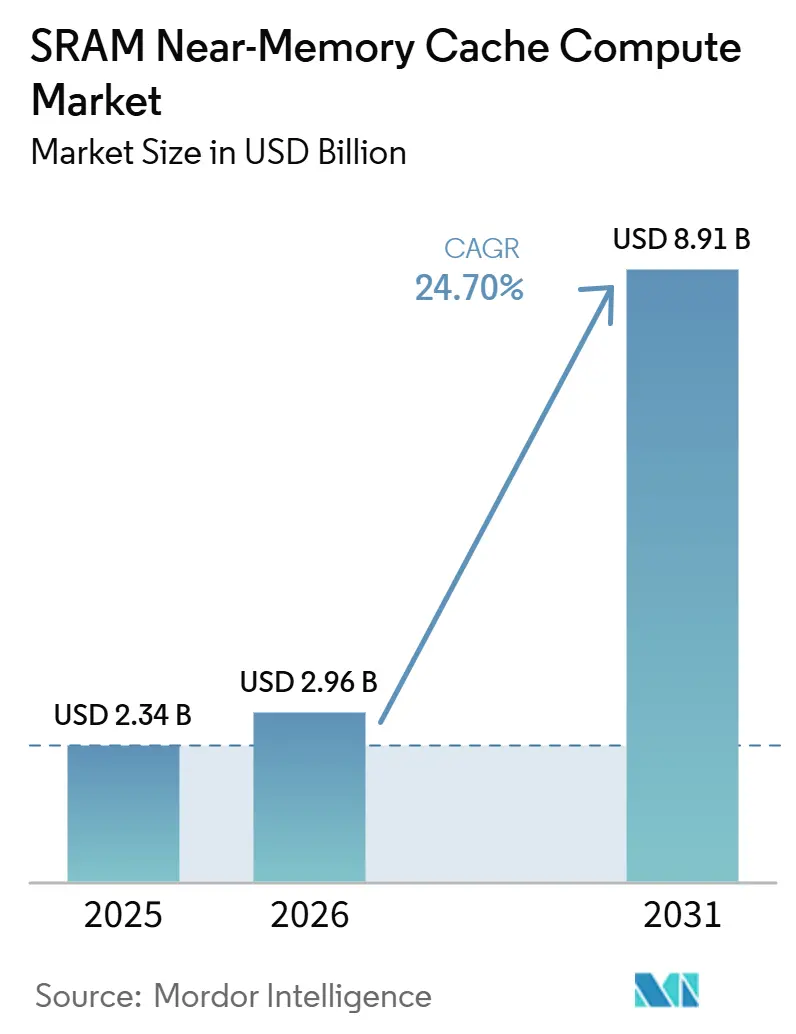

| Market Size (2026) | USD 2.96 Billion |

| Market Size (2031) | USD 8.91 Billion |

| Growth Rate (2026 - 2031) | 24.70% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

SRAM Near-Memory Cache Compute Market Analysis by Mordor Intelligence

The SRAM near-memory cache compute market size was valued at USD 2.34 billion in 2025 and is estimated to grow to USD 8.91 billion by 2031, at a CAGR of 24.70% during the forecast period from 2026 to 2031. Growth in the SRAM near-memory cache compute market is being shaped by the rising cost of moving data across chip boundaries, which makes local cache placement more valuable in AI systems that run continuously and at high utilization. The demand pattern is also shifting because deployed AI models now need sustained token throughput and low response delay, which favors architectures that keep memory physically close to compute blocks. Procurement across the SRAM near-memory cache compute market is being pulled by custom accelerators, advanced SoCs, and hyperscale infrastructure platforms that depend on larger on-chip cache footprints than prior processor generations. Competition is also tightening around dense custom SRAM design, packaging readiness, and node-level optimization, because those capabilities increasingly decide which suppliers win advanced AI silicon programs. Adoption is broadening beyond the largest cloud deployments, with automotive, networking, and edge inference creating additional room for the SRAM near-memory cache compute market to scale across different system classes.

Key Report Takeaways

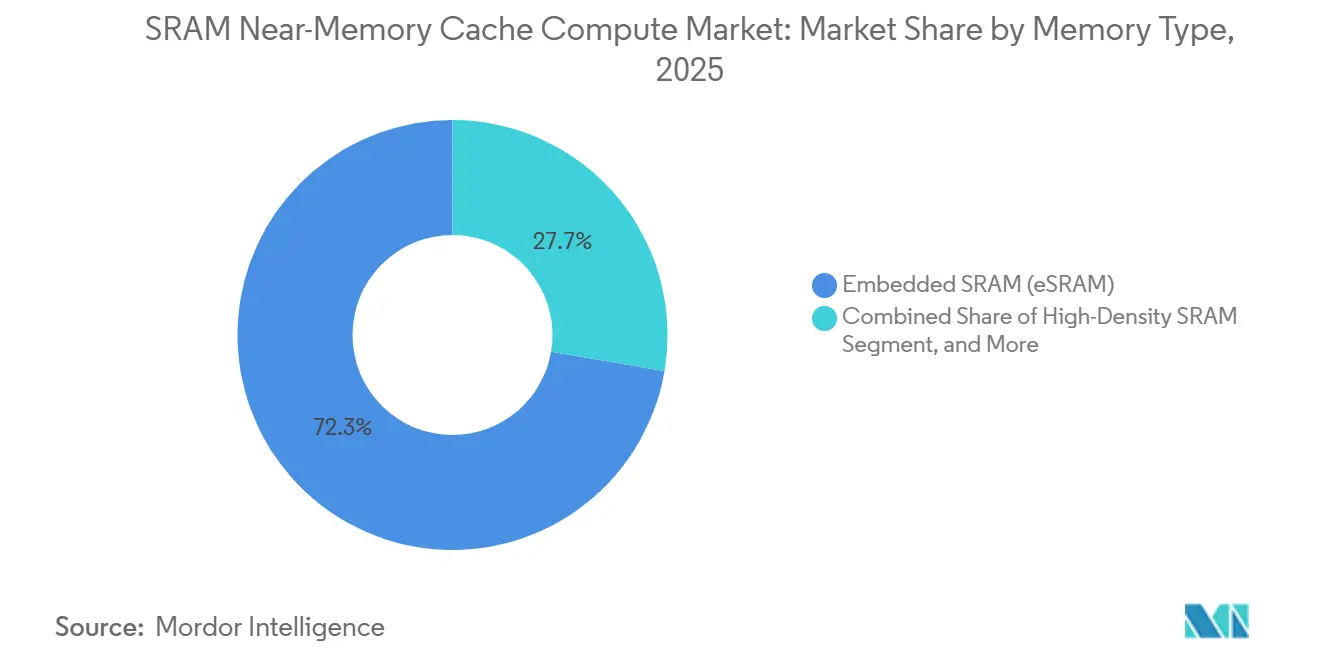

- By memory type, embedded SRAM held 73.84% of the revenue of the SRAM near-memory cache compute market in 2025, while high-density SRAM is projected to expand at 25.49% CAGR through 2031.

- By processor integration, AI accelerator cache integration held 43.17% of the SRAM near-memory cache compute market share in 2025 and is projected to advance at 25.43% CAGR through 2031.

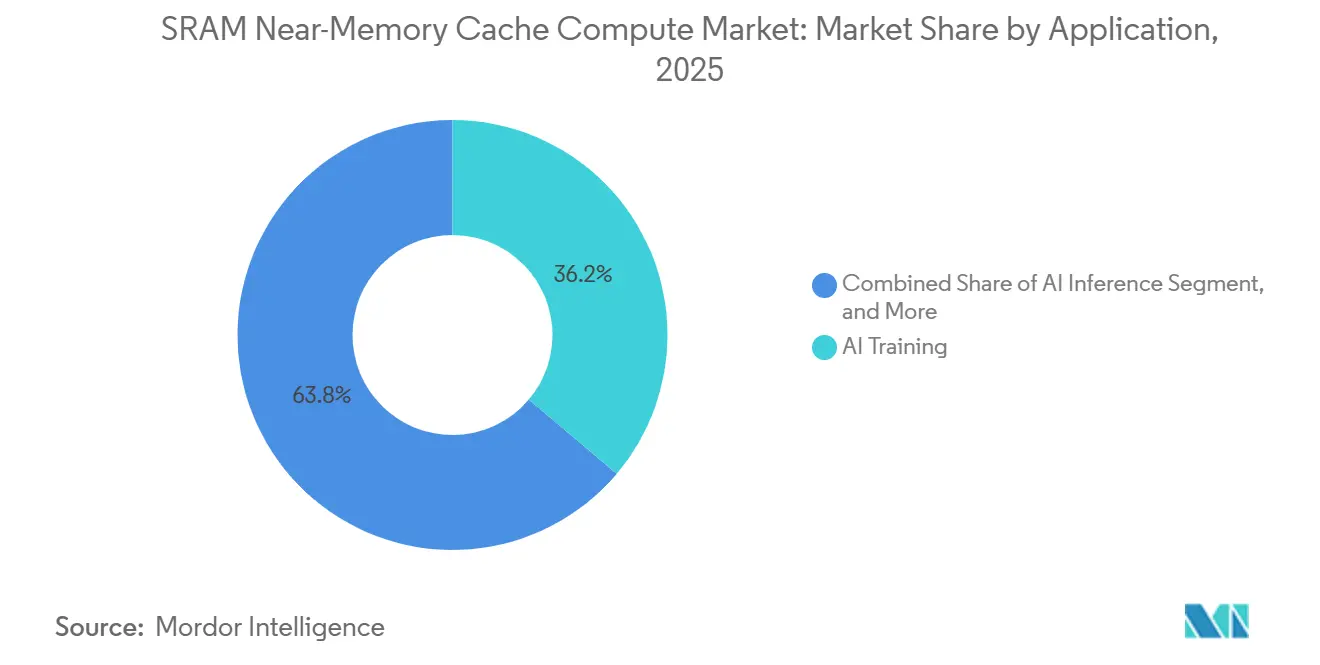

- By application, AI training accounted for 38.41% share of the SRAM near-memory cache compute market size in 2025 and is projected to grow at 25.88% CAGR through 2031.

- By end user, cloud and hyperscale providers held 59.09% of revenue in 2025 and are projected to expand at 25.67% CAGR through 2031.

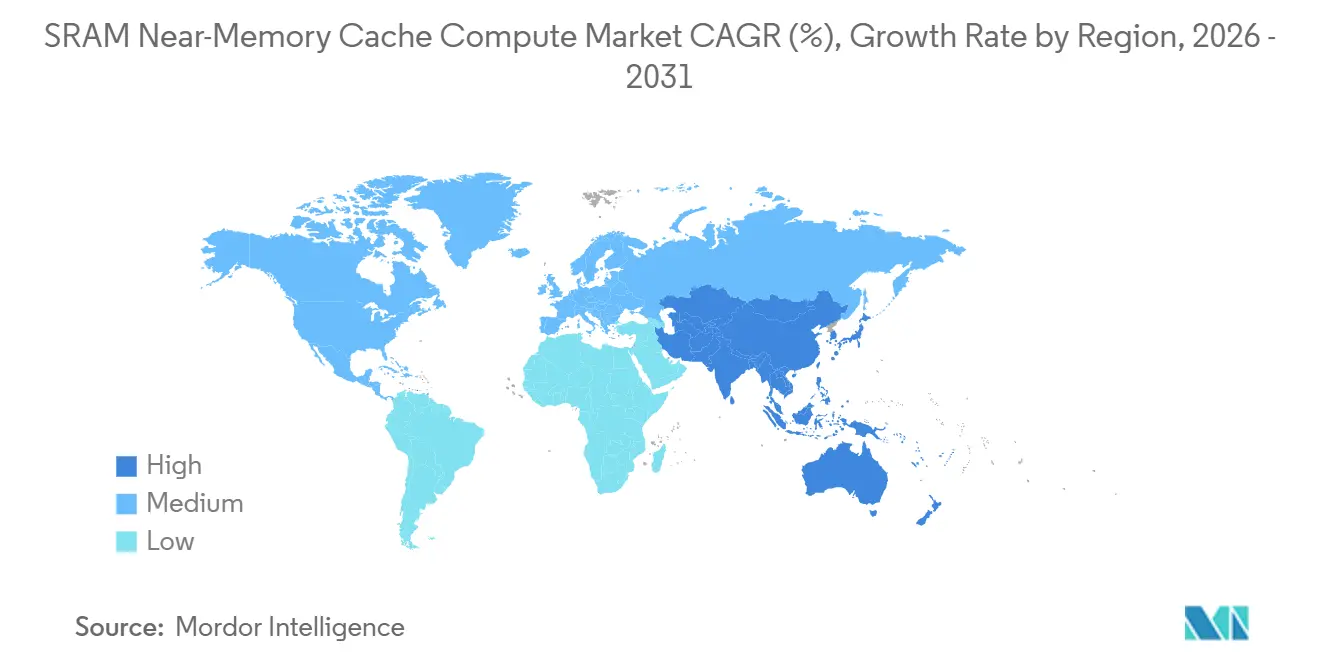

- By geography, North America held 42.77% of revenue in 2025, while Asia-Pacific is projected to record the fastest CAGR of 25.58% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global SRAM Near-Memory Cache Compute Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising AI Accelerator Demand for On-Chip Cache Proximity | +9.5% | Global | Short term (≤ 2 years) |

| Growth in High-Performance CPUs, GPUs, and NPUs | +6.5% | Global | Short term (≤ 2 years) |

| Shift Toward Energy-Efficient Data Movement Reduction | +4.8% | Global | Medium term (2-4 years) |

| Increasing Use of Embedded SRAM in Advanced SoCs | +3.2% | APAC core, spill-over to North America and EU | Medium term (2-4 years) |

| Expansion of Edge Compute and Real-Time Analytics Workloads | +2.1% | APAC and North America, with early gains in automotive manufacturing hubs | Medium term (2-4 years) |

| Foundry and IP Ecosystem Readiness for SRAM-Heavy Designs | +1.5% | Taiwan, South Korea, and North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising AI Accelerator Demand For On-Chip Cache Proximity

In the SRAM near-memory cache compute market, AI inference is pushing cache closer to the math engine because deployed models spend a large share of runtime waiting on memory access instead of raw compute. Peer-reviewed work showed that memory-access energy in modern neural networks can be heavily consumed by driving data across high-speed interconnects, which makes near-memory cache placement a direct efficiency lever rather than a secondary design choice.[1]Cognizance Journal, “Near-Data Computing: High Performance with Smart Data Processing for Data-Intensive Applications,” Cognizance Journal, doi.org That burden falls when SRAM sits beside the compute block and repeated token operations stay on die, which is why local bandwidth now matters as much as peak compute density in many AI accelerators. NVIDIA’s Hopper architecture already reflects this logic, with large on-die SRAM caches designed to reduce repeated trips to external memory in AI workloads.[2]“NVIDIA Hopper Architecture In-Depth,” NVIDIA Technical Blog, developer.nvidia.com Research on SRAM-accelerated LLM inference also showed that near-memory buffering can improve the decode stage, which is the stage most exposed to token-by-token delay in deployed language models. This is keeping the SRAM near-memory cache compute market centered on accelerator programs that can turn local memory proximity into measurable throughput gains.

Growth In High-Performance CPUs, GPUs, And NPUs

Growth in high-performance processors continues to lift the SRAM near-memory cache compute market because each additional compute block needs local cache to avoid stalls and repeated external memory calls. NVIDIA explained that each streaming multiprocessor carries SRAM-based L1 memory, so scaling the architecture raises on-die cache needs along with it. The H100 also uses a 50MB L2 cache in SRAM, which helps keep larger model and dataset fragments closer to the processor during AI execution. Arm’s 3nm pseudo-two-port SRAM macro work shows that IP suppliers are also tuning SRAM designs for higher bandwidth within fixed power and area budgets, which supports a wider set of advanced chip programs. This matters because the SRAM near-memory cache compute market is tied not only to data-center GPUs, but also to CPUs, NPUs, and edge processors that need persistent local model execution. As processor counts and core densities keep rising, local SRAM remains one of the few practical ways to preserve predictable response time.

Shift Toward Energy-Efficient Data Movement Reduction

In the SRAM near-memory cache compute market, energy savings from shorter data movement are becoming as important as peak bandwidth and raw clock speed. Marvell stated that its 2nm custom SRAM cut standby power by as much as 66% versus standard on-chip SRAM at similar density while operating at up to 3.75GHz. The same launch also pointed to 15% die area recovery, which gives designers room to reallocate silicon budget toward compute logic and interconnect resources. Research on SRAM-accelerated inference further showed that near-memory pipelining can improve LLM decode efficiency beyond simple cache placement alone.[3]“SAIL: SRAM-Accelerated LLM Inference System with Lookup-Table-Based GEMV,” arXiv, arxiv.org Peer-reviewed work on near-data computing supports the broader point that reducing data travel lowers energy overhead in data-intensive processing. That combination is making system power, heat load, and cooling cost part of the commercial case for SRAM-heavy architectures across the SRAM near-memory cache compute market.

Increasing Use Of Embedded SRAM In Advanced SoCs

The growing use of embedded SRAM in advanced SoCs is widening the addressable base of the SRAM near-memory cache compute market beyond the largest AI servers. IEEE work on 5nm digital SRAM in-memory computing macros reported a density of 5.67Mb/mm², which supports larger local model storage inside a constrained die area. NXP’s S32N7 processor series for software-defined vehicles combines AI and data acceleration with high-performance SRAM for real-time cache behavior in automotive domains. STMicroelectronics’ Stellar P3E automotive microcontroller also pairs AI acceleration with on-chip memory for neural network activations and graphics frame buffers. Renesas’ RA8P1 integrates 2MB of fully ECC-protected SRAM, which shows how reliability features are becoming part of near-memory design in safety-focused edge devices. This broadens demand for the SRAM near-memory cache compute market into automotive, industrial, and connected edge devices that need local AI response without high external memory dependence.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Design Complexity for Near-Memory Compute Integration | -1.4% | Global | Short term (≤ 2 years) |

| Limited Software Toolchain and Programmability Support | -0.9% | Global | Medium term (2-4 years) |

| SRAM Area Cost and Density Constraints Versus Alternative Memories | -0.7% | Global | Long term (≥ 4 years) |

| Thermal and Power Management Challenges in Dense Compute Dies | -0.5% | North America and APAC | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Design Complexity For Near-Memory Compute Integration

Near-memory compute integration remains difficult because SRAM arrays, logic blocks, physical layout, and package architecture have to be optimized together instead of in separate design stages. In the current SRAM near-memory cache compute market, that means advanced-node XPU programs often face longer validation cycles and higher engineering overhead before they reach acceptable yield and thermal behavior. A 2026 IEEE and JEDEC-linked analysis warned that high-duty SRAM activity from attention kernels can push local thermal stress beyond standard qualification assumptions in dense AI designs. The same analysis linked that stress to a higher risk of bias temperature instability and silent data corruption under sustained operating load. Foundry dependence also raises the barrier because the most advanced logic and dense SRAM nodes remain concentrated in a small number of fabrication ecosystems, including TSMC’s leading-edge roadmap. These constraints limit the number of teams that can scale new programs quickly inside the SRAM near-memory cache compute market.

Limited Software Toolchain And Programmability Support

Software support remains thinner than hardware ambition in the SRAM near-memory cache compute market, which slows adoption even when the underlying silicon is technically strong. ETH Zurich and EPFL showed that programmable near-memory control can deliver 53.9x lower execution time and 35.6x higher energy efficiency for targeted workloads, but it also requires compilers built for near-memory dataflows rather than standard processor flows. That creates a practical problem because enterprise deployment stacks are still built around familiar framework behavior and mature software ecosystems. The AccelCIM framework, published in 2026, also found that no single SRAM compute-in-memory dataflow dominates across both CNN and transformer workloads, which keeps standardization difficult. Toolchain fragmentation, therefore, remains a real brake on portability, developer productivity, and commercial adoption across the SRAM near-memory cache compute market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Memory Type: Embedded SRAM Holds The Core While High-Density Designs Gain Speed

Embedded SRAM held 73.84% of the SRAM near-memory cache compute market in 2025, which kept it as the clear anchor across memory type segmentation. Its lead comes from the fact that it is co-fabricated with logic in the same process flow, which removes package overhead and makes it the default option for advanced SoCs that need fast local memory. Marvell’s 2nm custom eSRAM shows how this segment is moving beyond basic cache utility, with up to 6Gb of high-speed on-chip memory, 66% lower standby power than standard SRAM at similar density, and 15% die area savings in a 2nm XPU design. That matters because eSRAM is already embedded across mobile NPUs, automotive processors, and data-center accelerators, so each design improvement scales across a very broad installed base. In practice, this gives embedded SRAM a durable position in the SRAM near-memory cache compute market, even as other memory variants improve.

High-density SRAM is projected to expand at 25.49% CAGR through 2031, making it the fastest-growing subsegment within memory type. IEEE research on 5nm digital SRAM in-memory computing macros reported a density of 5.67Mb/mm², which sets a meaningful benchmark for denser local model storage in future designs. Standalone SRAM remains relevant in L2 and last-level cache structures and in networking silicon, where repeated random access still rewards low-latency local memory. Multi-port SRAM is also becoming more important in processors that need simultaneous read and write access across parallel compute clusters without bottlenecking throughput. Taken together, these subsegments show that the SRAM near-memory cache compute industry is widening from standard cache blocks into more specialized memory forms that match different bandwidth and dataflow needs.

By Processor Integration: AI Accelerators Define The Fastest Design Priorities

AI accelerator cache integration held 43.17% share of the SRAM near-memory cache compute market size in 2025 and is projected to grow at 25.43% CAGR through 2031. This dual lead matters because dedicated training and inference chips allocate a larger portion of die area to SRAM than most general-purpose processors do. As a result, this segment now sets the pace for SRAM compilers, foundry tuning, and cache hierarchy design across much of the broader SRAM near-memory cache compute market. NVIDIA’s Hopper architecture illustrates the point, with a 50MB L2 cache in SRAM that is designed to reduce repeated trips to HBM during AI execution. When accelerator programs expand, they pull a wide range of upstream design choices with them, from cache density to power budgeting.

GPU cache integration remains a major volume contributor because each streaming multiprocessor depends on local SRAM-based L1 memory to maintain efficient data reuse. CPU cache integration provides a steadier volume base, especially in AI server platforms where host processors still manage orchestration, control, and memory coordination. Arm’s 3nm pseudo-two-port SRAM macro work shows that the IP ecosystem is still improving bandwidth within strict area and power limits, which supports continued optimization in this segment. Network and edge ASIC integration serves a different use case, with SRAM helping packet buffering, real-time inference, and low-latency control at the system edge. This leaves processor integration balanced between a fast-moving accelerator core and a stable supporting base across GPUs, CPUs, and specialized ASICs.

By Application: Training Leads The Base While Inference Broadens The Demand Mix

AI training accounted for 38.41% of application revenue in 2025 and is projected to expand at 25.88% CAGR through 2031. That position reflects procurement cycles that still prioritize frontier model development and large compute clusters. At the same time, inference is becoming more important because deployed language models depend on token throughput and low delay, which increases the value of local cache and near-memory buffering. Peer-reviewed work on near-data computing also supports the importance of reducing data travel in data-intensive AI tasks, which is a direct fit for inference-heavy workloads with repeated memory access. The application mix in the SRAM near-memory cache compute market is therefore becoming broader, even though training still defines the current revenue baseline.

HPC deployments are also a high-value application inside the SRAM near-memory cache compute market because science workloads need fast local memory for both simulation and AI processing. NVIDIA said Vera Rubin will power next-generation systems at Leibniz Supercomputing Center, NERSC, and Los Alamos National Laboratory, which shows that SRAM-rich cache hierarchies are relevant in production scientific computing environments. Edge AI adds another important layer, and IEEE work on the Maxwell near-SRAM architecture reported 250x inference speedup with only 0.6% area overhead for edge machine learning models. Networking and automotive applications contribute further breadth because packet handling, perception loops, and real-time control all benefit from low-latency local memory. This keeps the SRAM near-memory cache compute industry exposed to both frontier AI infrastructure and distributed embedded deployments.

By End User: Cloud Demand Dominates While Automotive Becomes A Meaningful Secondary Path

Cloud and hyperscale providers held 59.09% of end-user revenue in 2025 and are projected to expand at 25.67% CAGR through 2031. This concentration reflects their central role in training clusters, inference buildouts, and custom silicon programs that need large on-chip SRAM footprints. Their purchasing choices shape packaging demand, cache architecture, and node migration across the SRAM near-memory cache compute market more than any other buyer group. Enterprise data centers form a sizable secondary base, but they usually adopt merchant platforms rather than commissioning fully custom chips. The result is a demand pattern in which a small number of cloud buyers can move the direction of the whole market.

Automotive OEMs and tier-1 suppliers are the most notable emerging group in the SRAM near-memory cache compute market because vehicle platforms need local AI response, safety features, and predictable latency. NXP’s S32N7 brings AI and data acceleration together with high-performance SRAM for real-time vehicle domains, which makes it a clear example of near-memory logic moving into automotive processing. STMicroelectronics’ Stellar P3E and Renesas’ RA8P1 show the same direction, with automotive and edge systems adopting on-chip SRAM alongside reliability-focused memory protection. Industrial enterprises and telecommunications equipment providers make up the longer tail, with steady needs for embedded inference and low-latency networking. As this base widens, the SRAM near-memory cache compute industry gains a more diversified demand mix even though cloud remains the dominant customer class.

Geography Analysis

North America held 42.77% of the SRAM near-memory cache compute market share in 2025, making it the largest regional base for design and deployment. The region benefits from the concentration of leading chip designers, platform vendors, and hyperscale AI buyers that shape product priorities for the SRAM near-memory cache compute market. This gives North America strong influence over cache architecture, software requirements, and packaging choices, even when wafer fabrication happens elsewhere. Its main constraint is continued reliance on Asian foundries for the most advanced SRAM-heavy nodes, which keeps supply risk tied to offshore manufacturing capacity.

Asia-Pacific is projected to record the fastest 25.58% CAGR through 2031 in the SRAM near-memory cache compute market. The region combines foundry depth in Taiwan, memory manufacturing strength in South Korea, and expanding AI silicon design work across several national ecosystems. TSMC’s N2 process entered volume production in Q4 2025 and enabled SRAM density of around 0.019MB/mm², which supports denser cache integration at advanced nodes . That supply advantage matters because near-memory architectures depend on dense local SRAM without unacceptable die growth. As more advanced-node designs move from concept to volume, Asia-Pacific remains the main production base that turns architectural demand into shippable silicon for the SRAM near-memory cache compute market.

Europe’s role in the SRAM near-memory cache compute market is tied most closely to automotive and embedded processing, where memory reliability and local AI response matter. NXP, STMicroelectronics, and Renesas have each brought forward products that combine AI acceleration with on-chip SRAM for vehicle and edge use cases. South America and Middle East, and Africa remain earlier-stage adoption zones, with demand linked more to telecommunications, cloud rollout, and industrial modernization than to indigenous chip design. This creates a regional mix in which North America leads design demand, Asia-Pacific leads manufacturing momentum, and Europe adds automotive specialization, while South America and Middle East, and Africa build gradually.

Competitive Landscape

The SRAM near-memory cache compute market is moderately concentrated at the architectural layer, while remaining more fragmented across IP, design tools, and specialized integration services. A relatively small group of companies, including NVIDIA, TSMC, Marvell, Broadcom, Cerebras, NXP, STMicroelectronics, and Renesas, influences much of the visible product direction through platform design, foundry scale, and embedded system adoption. Companies that can combine advanced custom SRAM with packaging readiness and production access are in the strongest position to win the next wave of design programs. TSMC’s N2 volume production in Q4 2025 strengthened the supply position for leading-edge SRAM-heavy designs and reinforced the advantage of firms already aligned to advanced-node manufacturing.

Marvell made one of the clearest strategic moves in June 2025 when it launched the industry’s first 2nm custom SRAM, signaling that custom memory design had become a frontline competitive lever rather than a background feature. NVIDIA made another major move in June 2026 by placing the Vera Rubin platform into production deployment paths for science systems and cloud partners, which reinforced the link between advanced accelerators and large on-die cache hierarchies. NXP also widened the competitive field in January 2026 with the S32N7 processor series for software-defined vehicles, showing that high-performance SRAM design is becoming relevant in automotive compute as well as cloud infrastructure. STMicroelectronics added to that trend with Stellar P3E, which paired automotive AI acceleration with on-chip memory for edge intelligence workloads. Together, these moves show that competitive strength in the SRAM near-memory cache compute market comes from linking memory architecture to deployable systems and qualified end-use platforms.

Competition also depends on software readiness and qualification depth, not only on transistor density or peak cache performance. Research from ETH Zurich and EPFL showed that near-memory programmability can unlock strong performance, but it also highlighted the need for tailored compiler support and software mapping. The AccelCIM work published in 2026 further showed that dataflow optimization remains workload-specific, which leaves standardization incomplete for SRAM-centric compute paths. That leaves room for specialized IP vendors, but the overall SRAM near-memory cache compute market still favors companies that can combine design scale, manufacturing access, and customer reach.

SRAM Near-Memory Cache Compute Industry Leaders

NVIDIA Corporation

Intel Corporation

Advanced Micro Devices, Inc.

Samsung Electronics Co., Ltd.

Arm Holdings plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2026: Qualcomm introduced its High Bandwidth Compute (HBC) architecture, a near-memory computing platform that places SRAM-based compute close to HBM to reduce data movement, improve inference throughput, and overcome AI memory bottlenecks.

- June 2026: NVIDIA announced that the Vera Rubin platform, which entered full production on June 1, 2026, will power next-generation supercomputers at Leibniz Supercomputing Centre, the US Department of Energy’s NERSC, and Los Alamos National Laboratory. NVL4-based systems integrating SRAM-heavy Vera Rubin GPUs are expected from global OEMs in Q4 2026, with eight confirmed cloud partners including AWS, Google Cloud, and Microsoft Azure for commercial shipments.

- May 2026: NVIDIA launched the Vera CPU for AI agents at GTC Taipei, now in full production. The Vera CPU, purpose-built for agentic AI, reinforcement learning, and data processing, integrates with SRAM-heavy Vera Rubin GPU systems and enables 1.8x faster task completion versus x86 CPUs in agentic workloads.

- January 2026: NXP Semiconductors unveiled the S32N7 super-integration processor series at CES 2026, targeting software-defined vehicles on a 5nm SoC foundation. The S32N7 integrates AI and data acceleration, high-performance SRAM for real-time cache, and domain consolidation across 32 compatible variants, addressing ADAS and vehicle gateway functions under ISO 26262 automotive safety requirements.

Global SRAM Near-Memory Cache Compute Market Report Scope

The SRAM Near-Memory Cache Compute Market refers to architectures and solutions that place computation close to SRAM-based cache or memory layers to reduce data movement and accelerate processing. It is designed to improve latency, bandwidth efficiency, and energy use in data-heavy workloads.

The SRAM Near-Memory Cache Compute Market Report is Segmented by Memory Type (Embedded SRAM (eSRAM), Standalone SRAM, Multi-Port SRAM, and High-Density SRAM), Processor Integration (CPU Cache Integration, GPU Cache Integration, AI Accelerator Cache Integration, and Network And Edge ASIC Integration), Application (AI Training, Inference, HPC, Networking, Edge AI, and Automotive), End User (Cloud and Hyperscale Providers, Enterprise Data Centers, Automotive OEMs and Tier-1 Suppliers, Industrial Enterprises, and Telecommunications Equipment Providers), and Geography (North America, Europe, Asia-Pacific, South America, MEA). The Market Forecasts are Provided in Terms of Value (USD).

| Embedded SRAM (eSRAM) |

| Standalone SRAM |

| Multi-Port SRAM |

| High-Density SRAM |

| CPU Cache Integration |

| GPU Cache Integration |

| AI Accelerator Cache Integration |

| Network And Edge ASIC Integration |

| AI Training |

| AI Inference |

| HPC |

| Networking |

| Edge AI |

| Automotive |

| Cloud and Hyperscale Providers |

| Enterprise Data Centers |

| Automotive OEMs and Tier-1 Suppliers |

| Industrial Enterprises |

| Telecommunications Equipment Providers |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| South Korea | |

| Taiwan | |

| India | |

| Rest of Asia-Pacific | |

| South America | |

| Middle East and Africa |

| By Memory Type | Embedded SRAM (eSRAM) | |

| Standalone SRAM | ||

| Multi-Port SRAM | ||

| High-Density SRAM | ||

| By Processor Integration | CPU Cache Integration | |

| GPU Cache Integration | ||

| AI Accelerator Cache Integration | ||

| Network And Edge ASIC Integration | ||

| By Application | AI Training | |

| AI Inference | ||

| HPC | ||

| Networking | ||

| Edge AI | ||

| Automotive | ||

| By End User | Cloud and Hyperscale Providers | |

| Enterprise Data Centers | ||

| Automotive OEMs and Tier-1 Suppliers | ||

| Industrial Enterprises | ||

| Telecommunications Equipment Providers | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| Taiwan | ||

| India | ||

| Rest of Asia-Pacific | ||

| South America | ||

| Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size and growth outlook for the SRAM near-memory cache compute market?

The SRAM near-memory cache compute market was valued at USD 2.34 billion in 2025 and is projected to reach USD 8.91 billion by 2031, growing at a 24.70% CAGR over 2026-2031.

Why is SRAM becoming more important in AI compute systems?

SRAM is becoming more important because AI training and inference both need fast local memory to reduce repeated trips to external memory, which helps improve throughput, latency, and system power efficiency.

Which memory type leads this space today?

Embedded SRAM led with 73.84% of revenue in 2025 because it is integrated with logic, avoids packaging overhead, and remains the default local memory option in advanced SoCs and accelerators.

Which processor integration segment is expanding the fastest?

AI accelerator cache integration is both the largest and the fastest-growing processor integration segment, with 43.17% share in 2025 and a projected 25.43% CAGR through 2031.

Which end users are driving the highest demand?

Cloud and hyperscale providers are the main demand center, holding 59.09% of end-user revenue in 2025 and posting a projected 25.67% CAGR through 2031.

Which region offers the strongest growth potential through 2031?

Asia-Pacific offers the strongest growth outlook, with a projected 25.58% CAGR, supported by advanced foundry capacity, dense SRAM scaling, and broad semiconductor ecosystem depth.

Page last updated on: