Sports OTT Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

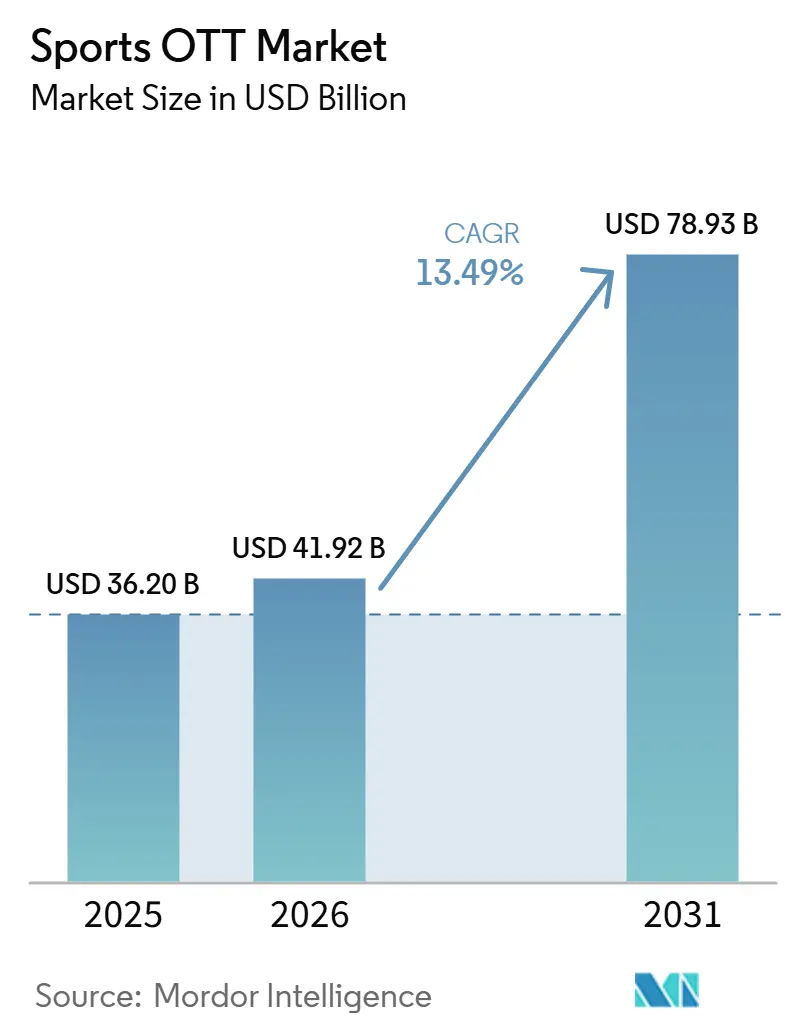

| Market Size (2026) | USD 41.92 Billion |

| Market Size (2031) | USD 78.93 Billion |

| Growth Rate (2026 - 2031) | 13.49% CAGR |

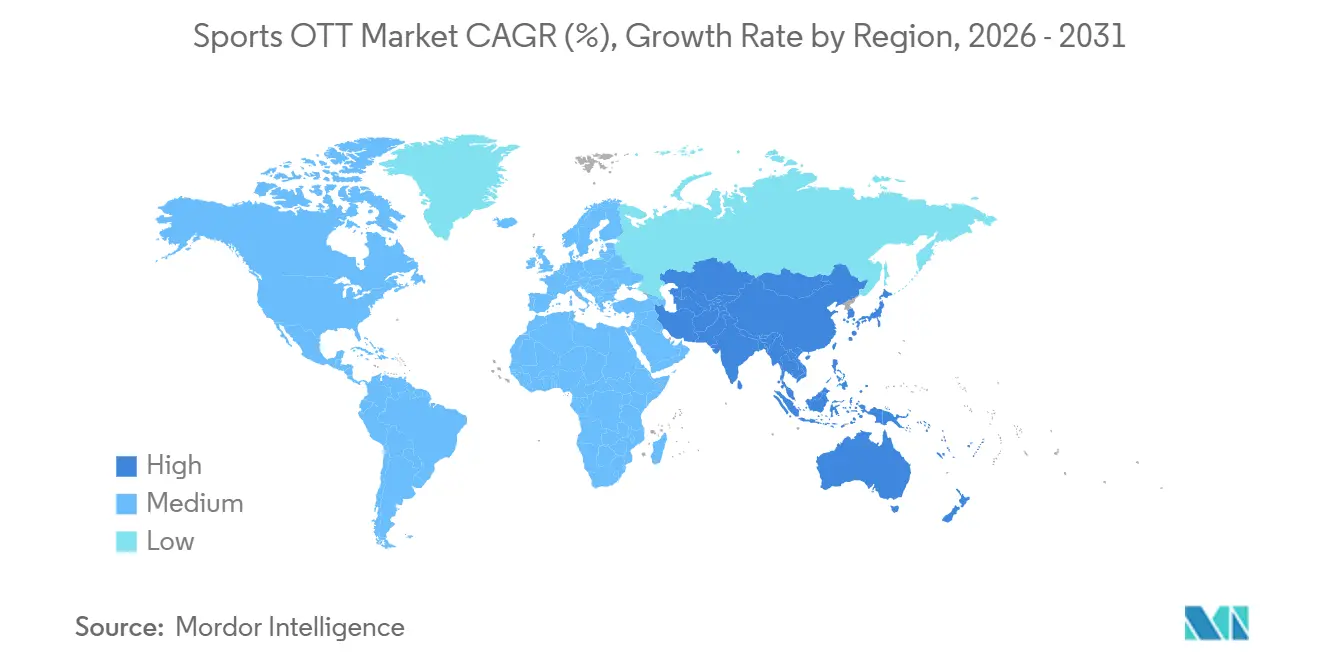

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Sports OTT Market Analysis by Mordor Intelligence

The sports OTT market size was valued at USD 36.20 billion in 2025 and estimated to grow from USD 41.92 billion in 2026 to reach USD 78.93 billion by 2031, at a CAGR of 13.49% during the forecast period (2026-2031). The sports OTT market is expanding because live sports audiences continue to move away from linear television and toward app-based viewing that offers more control, wider device access, and stronger personalization. Exclusive rights have become the main competitive tool, which means platforms are investing more heavily in premium leagues and combat sports to secure recurring viewers rather than casual traffic. The sports OTT market is also widening through ad-supported access, mobile-first viewing, and better streaming delivery, which together make live sports easier to reach in both mature and price-sensitive markets. Competition is becoming sharper as technology companies, broadcasters, and sports-focused streaming services chase the same premium event windows, which is raising platform standards and increasing the importance of scale. At the same time, higher rights costs and persistent piracy remain real constraints, which means the strongest opportunities are shifting toward operators that can combine premium rights, flexible monetization, and reliable live delivery.

Key Report Takeaways

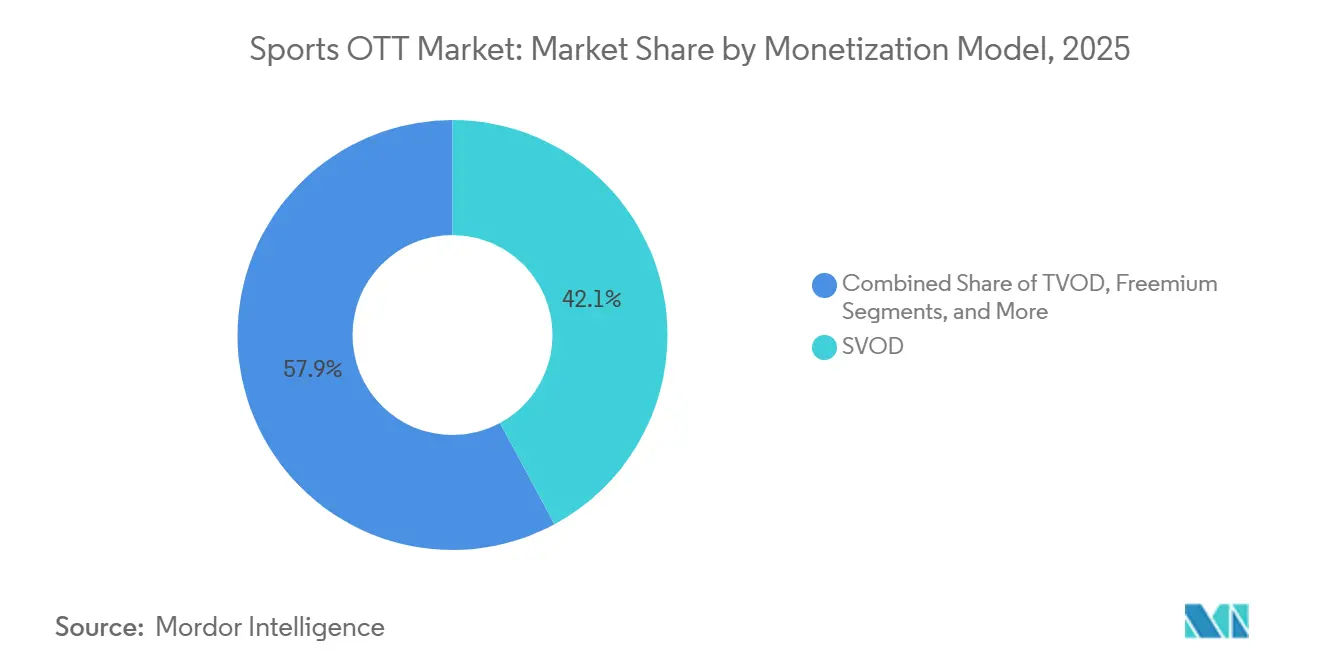

- By monetization model, SVOD held 42.13% of the sports OTT market share in 2025, while AVOD is projected to expand at a 14.18% CAGR through 2031.

- By device type, Smart TVs accounted for 40.62% share in 2025, while Smartphones and Tablets are projected to grow at a 14.42% CAGR through 2031.

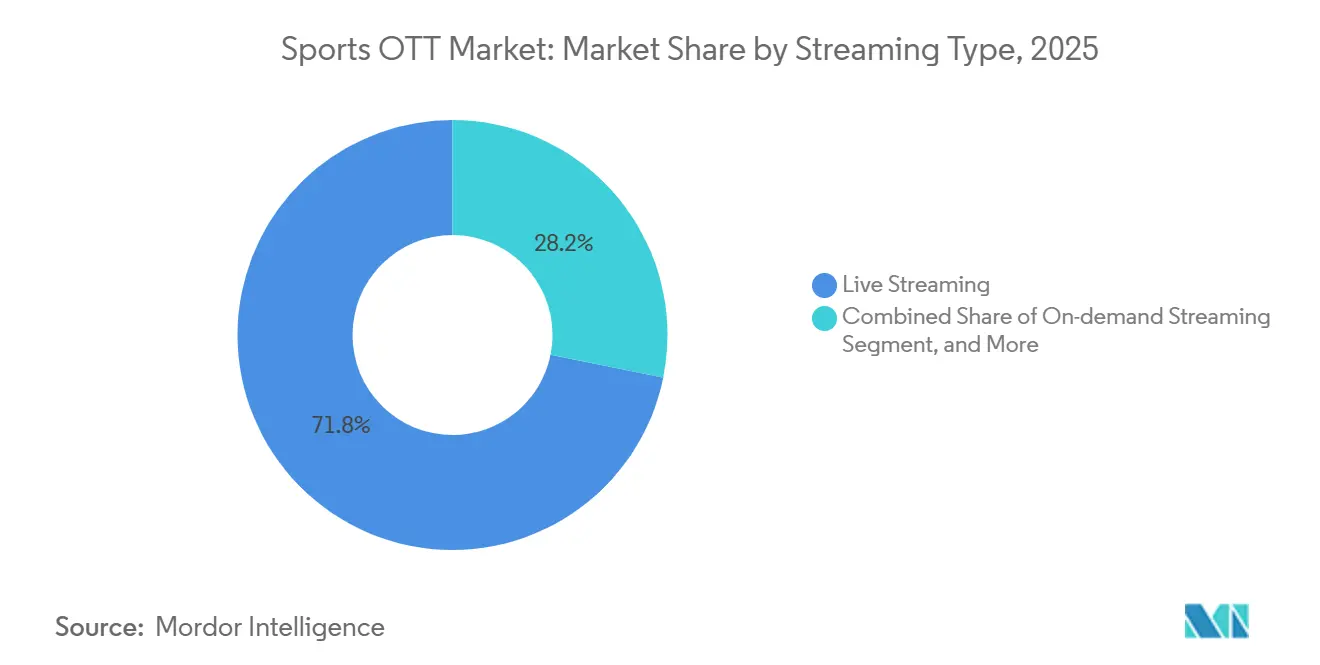

- By streaming type, live streaming accounted for 71.83% of the sports OTT market size in 2025, while on-demand streaming is projected to expand at a 14.08% CAGR through 2031.

- By sport type, football and soccer accounted for 33.58% in 2025, while cricket is projected to grow at a 15.39% CAGR through 2031.

- By geography, North America held 34.21% share in 2025, while Asia-Pacific is projected to expand at a 15.73% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Sports OTT Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Exclusive Sports Rights Acquisitions by OTT Platforms | +4.2% | Global | Short term (≤ 2 years) |

| Growth of Hybrid Monetization Across Subscription and Advertising Models | +2.8% | North America and Europe, spill-over to APAC | Medium term (2-4 years) |

| Increasing Mobile-First Sports Consumption and Second-Screen Viewing | +2.1% | APAC core, spill-over to South America and MEA | Short term (≤ 2 years) |

| Expansion of Low-Latency and Interactive Streaming Capabilities | +1.5% | Global | Medium term (2-4 years) |

| Rising Integration of Personalized Highlights and AI-Driven Discovery | +1.2% | Global | Medium term (2-4 years) |

| Growth of Direct-to-Consumer League and Team-Owned Platforms | +0.9% | North America, early gains in select European leagues | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Exclusive Sports Rights Acquisitions by OTT Platforms

Exclusive rights are now central to subscriber acquisition in the sports OTT market because premium live windows remain the clearest reason for fans to pay every month. Amazon Prime Video launched its first season under the 11-year NBA agreement in October 2025, adding 66 regular-season games to its streaming lineup and materially deepening its basketball offering. Paramount Skydance and TKO Group then set a new benchmark with a 7-year, USD 7.7 billion UFC rights agreement, under which Paramount+ became the exclusive US digital home for all UFC numbered events and Fight Nights from 2026. ESPN platforms also became the exclusive US domestic home for all WWE Premium Live Events, including WrestleMania, beginning in 2026 under the August 2025 agreement. Taken together, these moves show that the sports OTT market rewards platforms that secure access to must-watch events rather than those that simply add more nonexclusive sports content.

Growth of Hybrid Monetization Across Subscription and Advertising Models

Hybrid monetization is gaining ground in the sports OTT market because operators increasingly need both recurring subscription income and broad advertising reach. Paramount+ folded all UFC numbered events and Fight Nights into the subscription offer rather than preserving a separate pay-per-view layer, thereby widening access to premium combat sports. The World Boxing Council also announced in May 2025 that DAZN and Premier Boxing Champions had reached a landmark agreement that kept marquee fight nights on DAZN while leaving premium pay-per-view events available through Prime Video.[1]World Boxing Council, “DAZN and PBC Announce Landmark Agreement,” World Boxing Council, wbcboxing.com Disney added another version of this approach when it launched ESPN's direct-to-consumer service in August 2025 with a broad monthly package built around live sports networks and enhanced digital access. This mix of recurring fees, event upsell, and wider audience reach is helping the sports OTT market serve both premium households and viewers who are more price-sensitive.

Increasing Mobile-First Sports Consumption and Second Screen Viewing

Mobile viewing is becoming more central to the sports OTT market because fans increasingly follow live games, highlights, and updates away from the living room. In the Spring 2026 Sports Video Group survey, mobile and tablet devices moved into the second-most-used viewing category among US sports fans, and 54% of respondents said they were interested in vertical live sports streams built for phones. ESPN's August 2025 direct-to-consumer launch also came with an enhanced app, which showed that major operators are pairing rights expansion with smoother multiscreen access and easier mobile discovery. The NBA also reworked its app in October 2025 to combine live games with 24-hour programming, which made handheld discovery and repeat engagement more important to the basketball streaming experience. As these patterns deepen, the sports OTT market is likely to keep widening through device-specific presentation, lower entry pricing, and stronger second-screen behavior around live events.

Expansion of Low-Latency and Interactive Streaming Capabilities

Lower delay is becoming a core feature in the sports OTT market because live sports lose value when the digital stream lags far behind the event itself. OTT Engine reported that LL-HLS and LL-DASH can now deliver 2-5-second end-to-end latency for large-scale sports streaming, while Tencent RTC described WebRTC architectures that support sub-300-millisecond delay for interactive sports use cases. Stats Perform said its Realtime Streaming platform has already demonstrated sub-second delivery at more than 500,000 concurrent viewers, which shows that this capability is moving beyond limited trials. This matters because premium live services are no longer judged solely by picture quality; they are also judged by how closely the stream feels to the actual moment of play. Platforms that can maintain low-delay performance at scale are better placed to support synchronized fan engagement, interactive layers, and higher-value live experiences in the sports OTT market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High and Rising Costs of Premium Sports Rights | -2.3% | Global | Short term (≤ 2 years) |

| Piracy and Unauthorized Restreaming of Live Sports Events | -1.1% | Global, concentrated in MEA, South Asia, and Western Europe | Short term (≤ 2 years) |

| Churn Pressure from Fragmented Rights Across Multiple Platforms | -0.8% | North America and Europe | Medium term (2-4 years) |

| Latency, QoE, and Peak-Load Reliability Challenges During Live Events | -0.6% | APAC and MEA, emerging infrastructure markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High and Rising Costs of Premium Sports Rights

Premium rights costs are rising fast enough to tighten the economics of the sports OTT market and to narrow the field of platforms that can compete consistently. Paramount Skydance's 7-year, USD 7.7 billion UFC agreement and Amazon's 11-year NBA deal show how large the financial commitments for top-tier sports have become. These deals favor companies that can spread sports spending across broader media, commerce, or ecosystem revenues, while smaller services have much less room to absorb losses or overpay for renewals. The pressure is even greater when rights holders want wider digital reach, stronger production quality, and more flexible distribution from the same contract cycle. As a result, the sports OTT market is increasingly rewarding scale, balance-sheet strength, and cross-platform monetization rather than pure appetite for sports content alone.

Piracy and Unauthorized Restreaming of Live Sports Events

Piracy continues to divert value away from licensed platforms and remains a direct commercial drag on the sports OTT market. In September 2025, authorities shut down Streameast, which the BBC identified as the largest illegal live sports streaming site, after the network drew 1.6 billion visits in the prior year. The case also showed how quickly illegal distribution can return after enforcement, as mirror sites and alternative domains can quickly rebuild audience access. That pattern weakens the full benefit of exclusive rights deals, especially when platforms are paying more for premium content and trying to convert casual users into paying subscribers. Until enforcement, payment controls, and platform-level protection improve together, piracy will remain a persistent brake on growth and retention across the sports OTT market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Monetization Model: SVOD Leads While AVOD Expands Faster

SVOD held 42.13% share of the sports OTT market in 2025, while AVOD is projected to grow at a 14.18% CAGR through 2031. The lead came from the strong pull of exclusive live rights, which still gives subscription platforms the clearest way to lock in committed viewers across full seasons and major tournaments. Amazon, ESPN, and Paramount+ each reinforced this logic by tying headline rights packages to broader digital subscriptions instead of limiting access to stand-alone event purchases. The sports OTT market also benefits from the fact that sports subscribers tend to remain active through key matches and playoffs, which gives premium rights a more durable retention role than most general entertainment libraries.

AVOD is rising faster because it lowers the entry barrier and allows the sports OTT market to reach viewers who may not commit to premium monthly fees from the start. Paramount+ moved UFC numbered events into the base subscription offer, while DAZN and Premier Boxing Champions maintained a mixed structure combining subscription access with selective premium-event sales through Prime Video. That blend gives operators more room to balance audience growth, advertising sales, and event-level monetization across a broader user base in the sports OTT market. Stats Perform's 2026 survey also showed wider AI adoption by sports media executives, which supports better discovery and retention across subscription, advertising, and mixed monetization structures.

By Device Type: Smart TVs Anchor Premium Viewing While Mobile Gains Pace

Smart TVs accounted for 40.62% share of the sports OTT market in 2025, while Smartphones and Tablets are projected to advance at a 14.42% CAGR through 2031. That lead shows that the largest screen still carries the premium viewing role for full matches, tentpole events, and longer sessions shared across households. Disney linked rights expansion with easier connected-TV access when it launched ESPN's direct-to-consumer service and enhanced app in August 2025. The sports OTT market continues to build around the living-room screen because premium sports still benefits from better picture quality, fuller sound, and a more stable shared viewing experience.

Smartphones and tablets are moving faster because fans now expect live access, short clips, and score-driven viewing throughout the day rather than only during planned television sessions. Sports Video Group said in Spring 2026 that mobile and tablet devices had become the second-most-used viewing category among US sports fans, while 54% of respondents showed interest in vertical live streams on phones. The NBA's reworked app also points to a wider pattern in which leagues and platforms are shaping discovery, highlights, and repeat engagement across handheld devices as much as on television. Laptops, desktops, consoles, and set-top boxes still matter, but the sports OTT market is steadily centering product design on the connected-TV screen and the smartphone screen.

By Streaming Type: Live Coverage Dominates While On-Demand Builds Value

Live streaming accounted for 71.83% of the sports OTT market size in 2025, while on-demand streaming is projected to grow at a 14.08% CAGR through 2031. Live content kept this lead because sports lose much of their appeal once the result is widely known, making real-time access very difficult to replicate. Amazon's NBA package, ESPN's expanded baseball rights, and the WWE arrangement on ESPN all reinforce the central role of live event access in platform competition. This makes the sports OTT market structurally different from many other streaming categories, as the live window still drives urgency, retention, and willingness to pay.

On-demand viewing is growing faster as platforms extend the life of each match through replays, clips, condensed games, and personalized highlights. Stats Perform launched Opta Pulse in May 2026, and the company said the tool can produce broadcast-quality sports highlights up to 80% faster than traditional workflows.[2]Stats Perform, “Opta Pulse Launch,” Stats Perform, statsperform.com Spiideo also launched AI Highlights in May 2026 to turn live event footage into story-driven content at scale for broadcasters and OTT platforms. As these workflows improve, the sports OTT market can monetize more viewing moments after the final whistle without weakening the core value of the live stream itself.

By Sport Type: Football And Soccer Lead Revenue While Cricket Moves Faster

Football and soccer accounted for 33.58% of the sports OTT market in 2025, while cricket is projected to grow at a 15.39% CAGR through 2031. Football and soccer continue to anchor revenue because they combine global fandom, strong club loyalty, and premium rights cycles across several high-value countries simultaneously. This structure fits the sports OTT market well because globally recognized sports can support both multinational rights strategies and local subscription bundles without losing their audience pull. Amazon's long-term NBA commitment does not displace football and soccer, but it confirms that leading platforms are still concentrating investment around sports with a durable, cross-border audience appeal.

Basketball, American football, baseball, tennis, motorsport, and esports each add different seasonality patterns and engagement behavior to the sports OTT market. The NBA refreshed its direct-to-consumer app in October 2025 with live games and 24-hour programming, while ESPN secured MLB.TV rights for 2026-2028 and in-market streaming for 6 clubs inside its app. These examples show how leagues and platforms are expanding digital access beyond one-off live windows into year-round, full-viewing relationships. The result is a sports OTT market where tentpole sports still lead revenue, but secondary sports remain important for smoothing churn, broadening audience choice, and filling the calendar.

Geography Analysis

North America held 34.21% of the sports OTT market share in 2025. The region stayed ahead because households were already accustomed to paying for premium sports access, and major operators shifted that spending into digital bundles. Disney launched ESPN's new direct-to-consumer service in August 2025 at USD 29.99 per month with 12 ESPN linear networks, and the same move broadened ESPN's role as a digital sports destination.[3]ESPN Press Room US, “ESPN Launches New Direct-to-Consumer Service, Enhanced ESPN App,” ESPN Press Room US, us.espnpressroom.com Amazon also launched its first exclusive NBA season in October 2025, sharpening competition for premium basketball viewers in the United States. The sports OTT market in North America is therefore moving toward fewer operators with broader rights portfolios, stronger bundles, and deeper financial capacity.

Asia-Pacific is projected to expand at a 15.73% CAGR through 2031, making it the fastest-growing regional market for sports OTT. India remains the main growth engine because cricket, mobile broadband, and mass digital distribution are scaling simultaneously. This regional pattern also fits the stronger shift toward mobile viewing, lower entry price points, and flexible monetization models that can reach large audiences beyond mature subscription households. As a result, the sports OTT market in Asia-Pacific is increasingly shaping global thinking on how to combine premium live rights with very large digital reach.

Europe remained a high-value part of the sports OTT market in 2025, although rights structures and platform strength continued to vary by country. DAZN said in August 2025 that it had added the Bundesliga Konferenz Saturday afternoon rights in Germany alongside its Sunday match portfolio, which confirmed the stronger role of streaming platforms in national football negotiations. South America and the Middle East and Africa are also moving deeper into streaming, but adoption patterns are shaped more clearly by major football rights, connected-TV growth, and the strength of mobile access than by a single region-wide model. Taken together, these regions show that the sports OTT market is expanding through different routes, with mature countries leaning on premium bundling and emerging markets leaning on access, device reach, and ad-supported viewing.

Competitive Landscape

The sports OTT market is moderately concentrated, with a small group of global platforms holding the strongest rights portfolios and the broadest subscriber reach. Amazon, The Walt Disney Company, DAZN, and Alphabet compete with different business models, but each uses sports to deepen engagement inside a wider digital ecosystem. Amazon began its exclusive NBA era in October 2025, while Disney launched ESPN's new direct-to-consumer service in August 2025 and expanded it to include major live sports. Paramount+ also raised the stakes in August 2025 by securing all UFC numbered events and Fight Nights for the US market from 2026. These moves show that scale in the sports OTT market now depends on both the depth of premium rights and the ability to spread those rights across large existing user bases.

Pure-play services are responding by building sharper sport and territory positions instead of trying to match every global rights bid. DAZN widened that approach through its CFL agreement for 2027-2032, which added another structured North American rights position to its portfolio.[4]DAZN Group, “DAZN Kicks Off a New Era for Canadian Football with Domestic and Global CFL Rights Beginning 2027,” DAZN Group, dazngroup.com The World Boxing Council also said in May 2025 that DAZN and Premier Boxing Champions had reached a landmark agreement that kept marquee fight nights on DAZN's global subscription platform. Smaller operators still have room when they focus on underserved sports, local language depth, or event windows that larger platforms do not prioritize.

Technology is becoming another competitive divider inside the sports OTT market because highlight speed, personalization, and streaming performance now shape user value after rights are secured. Stats Perform launched Opta Pulse in May 2026, and Spiideo launched AI Highlights in the same month, showing how quickly automated content production is moving into mainstream sports workflows. Platforms that pair exclusive rights with faster highlight creation, better search, and lower-latency delivery can keep viewers active before, during, and after live matches. That is why the next phase of the sports OTT market is likely to reward companies that combine premium rights, flexible monetization, and product execution rather than rights ownership alone.

Sports OTT Industry Leaders

Amazon.com, Inc.

The Walt Disney Company

DAZN Group Limited

Warner Bros. Discovery, Inc.

Paramount Skydance Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: DAZN Group Limited acquired domestic and global media rights to the Canadian Football League (CFL) for the 2027-2032 cycle, covering all regular season games, playoff games, and the Grey Cup, according to DAZN's official press release. The deal marks the CFL's first worldwide media rights agreement and extends DAZN's North American sports portfolio beyond soccer and combat sports.

- May 2026: Stats Perform launched Opta Pulse, an AI-assisted video creation and distribution platform that generates broadcast-quality sports highlights up to 80% faster than traditional workflows, per the company's official announcement.

- May 2026: Spiideo launched its AI Highlights product covering soccer, ice hockey, basketball, and handball, transforming live event footage into story-driven content at scale for broadcasters and OTT platforms, per the company's official release.

- August 2025: ESPN and WWE signed a landmark exclusive deal, making ESPN DTC the sole US home for all WWE Premium Live Events beginning in 2026, including WrestleMania, per WWE's official corporate announcement. The deal moved WrestleMania and 9 other annual marquee events from Peacock to ESPN's streaming ecosystem.

Global Sports OTT Market Report Scope

The Sports OTT Market refers to the delivery of live and on-demand sports content via over-the-top (OTT) streaming platforms that distribute video directly to viewers over the Internet, without traditional cable, satellite, or broadcast television providers. The market includes subscription-, advertising-, transactional-, and hybrid streaming models across various sports categories, including football, basketball, cricket, tennis, motorsports, and other professional and amateur sports events.

The Sports OTT Market Report is Segmented by Monetization Model (SVOD, AVOD, TVOD, Hybrid, and Freemium), Device Type (Smartphones and Tablets, Smart TVs, Laptops and Desktops, and Other Device Types), Streaming Type (Live Streaming, On-demand Streaming, and Other Streaming Types), Sport Type (Football and Soccer, Cricket, Basketball, Baseball, Tennis, Motorsport, Esports, and Other Sports Types), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| SVOD |

| AVOD |

| TVOD |

| Hybrid |

| Freemium |

| Smartphones and Tablets |

| Smart TVs |

| Laptops and Desktops |

| Other Device Types |

| Live Streaming |

| On-demand Streaming |

| Other Streaming Types |

| Football and Soccer |

| Cricket |

| Basketball |

| Baseball |

| Tennis |

| Motorsport |

| Esports |

| Other Sports Types |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Qatar | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Nigeria | |

| Rest of Africa |

| By Monetization Model | SVOD | |

| AVOD | ||

| TVOD | ||

| Hybrid | ||

| Freemium | ||

| By Device Type | Smartphones and Tablets | |

| Smart TVs | ||

| Laptops and Desktops | ||

| Other Device Types | ||

| By Streaming Type | Live Streaming | |

| On-demand Streaming | ||

| Other Streaming Types | ||

| By Sport Type | Football and Soccer | |

| Cricket | ||

| Basketball | ||

| Baseball | ||

| Tennis | ||

| Motorsport | ||

| Esports | ||

| Other Sports Types | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Qatar | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current and forecast size of the sports OTT market?

The sports OTT market was valued at USD 36.20 billion in 2025, reached USD 41.92 billion in 2026, and is forecast to reach USD 78.93 billion by 2031 at a 13.49% CAGR.

Which monetization model leads sports streaming platforms today?

SVOD led with 42.13% share in 2025 because exclusive live rights still convert committed sports fans into recurring subscribers more effectively than other models.

Which viewing device is growing fastest for sports streaming?

Smartphones and tablets are projected to grow at 14.42% CAGR through 2031, even though Smart TVs remained the largest device category with 40.62% share in 2025.

Why does live streaming still dominate sports viewing?

Live streaming held 71.83% share in 2025 because real-time access remains critical for sports, where delayed viewing loses much of its appeal once outcomes are known.

Which sport categories are shaping future platform growth?

Football and soccer remained the largest sport segment with 33.58% share in 2025, while cricket is projected to grow fastest at a 15.39% CAGR through 2031.

Which region offers the strongest near-term growth opportunity?

Asia-Pacific is the fastest-growing region with a projected 15.73% CAGR through 2031, while North America remained the largest region with 34.21% share in 2025.

Page last updated on: