Sports Medicine Biologics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.88 Billion |

| Market Size (2031) | USD 2.43 Billion |

| Growth Rate (2026 - 2031) | 5.25% CAGR |

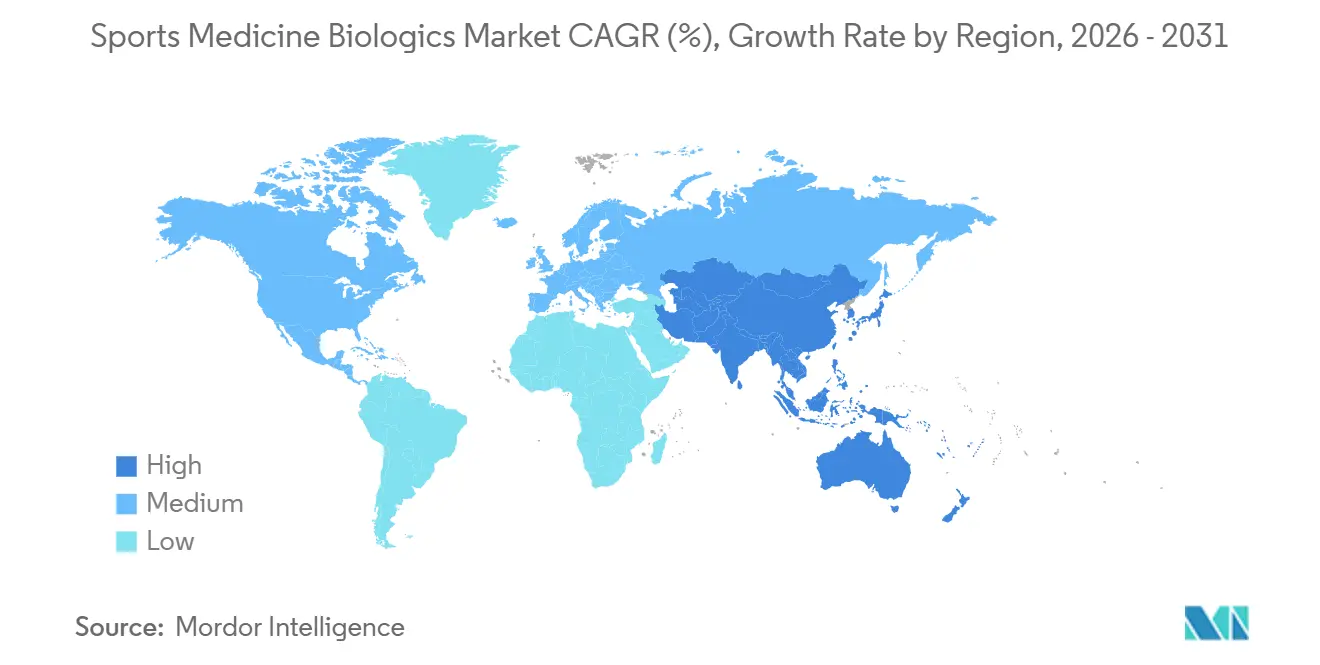

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

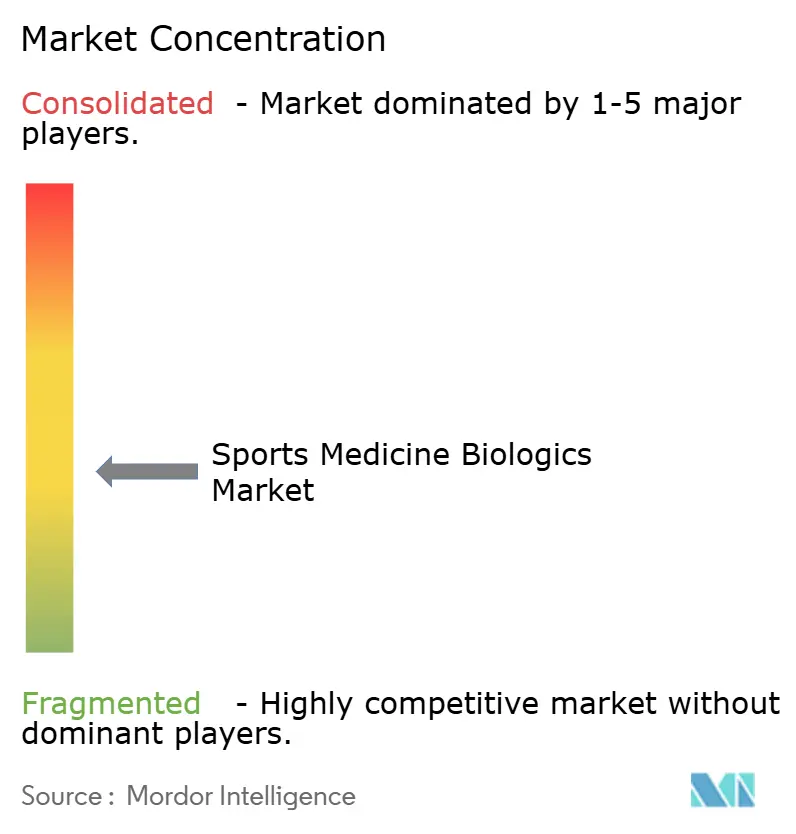

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Sports Medicine Biologics Market Analysis by Mordor Intelligence

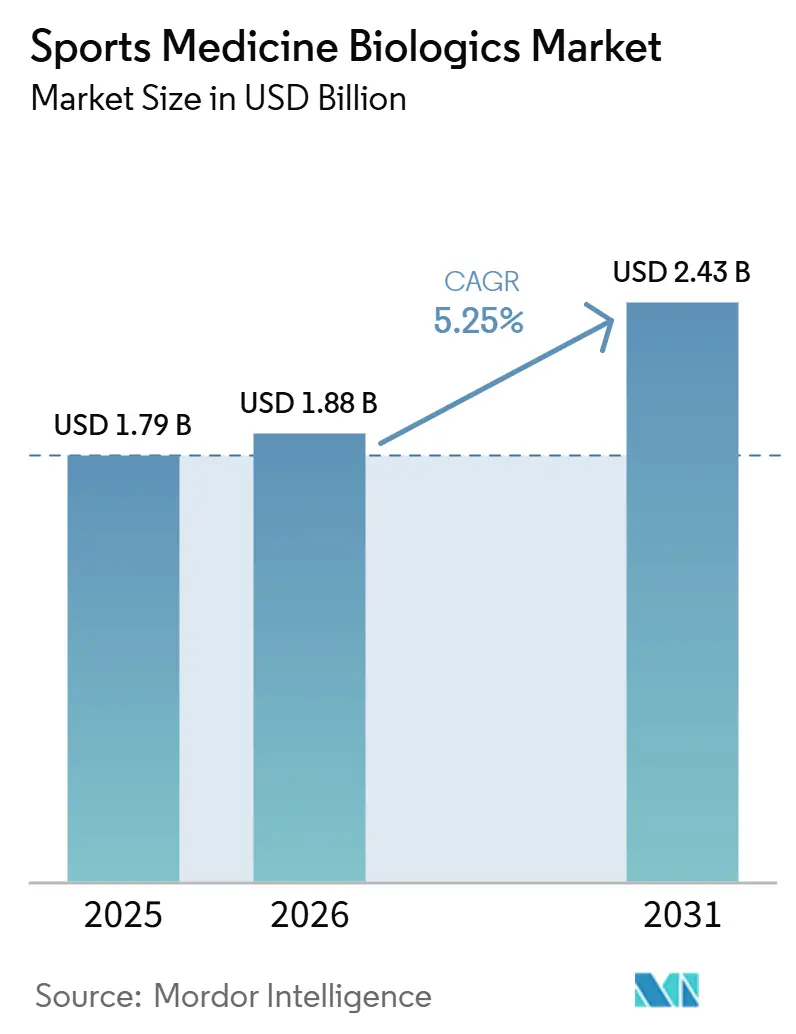

The Sports Medicine Biologics Market size was valued at USD 1.79 billion in 2025 and is estimated to grow from USD 1.88 billion in 2026 to reach USD 2.43 billion by 2031, at a CAGR of 5.25% during the forecast period (2026-2031).

Participation-led musculoskeletal injuries, the expanding base of active adults over 50, and sustained demand for tissue-preserving treatments continue to support the sports medicine biologics market. Strategic interest has also increased as the demand for biologics is growing, indicating stronger buyer focus on this space. Clinical uptake is improving as products demonstrate repeat surgeon use and durable outcomes. Payer coverage and approval pathways now influence commercial success as much as product design, as reimbursement gaps and tighter cell-therapy oversight can delay adoption despite strong clinical interest. Companies that combine clinical evidence, outpatient workflow fit, and clearer payer access are well-positioned to capture near-term opportunities in the sports medicine biologics market.

Key Report Takeaways

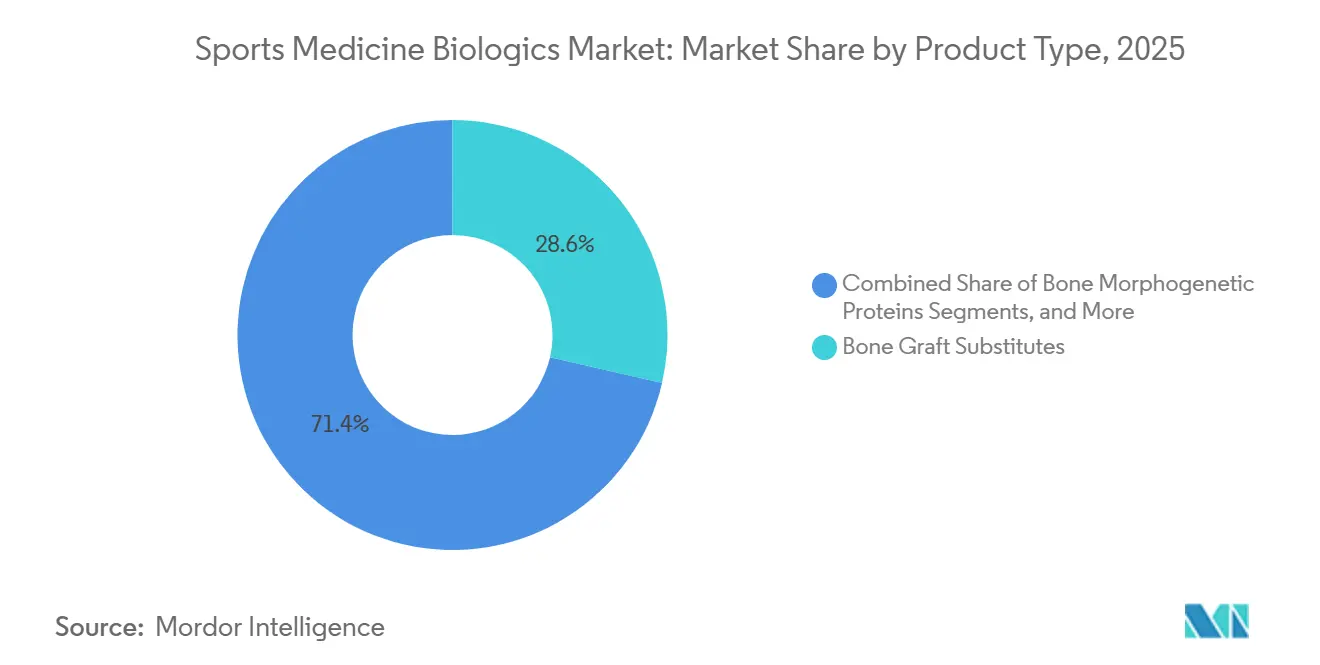

- By product type, bone graft substitutes held 28.58% of the sports medicine biologics market share in 2025, while stem cell-based products are projected to expand at 6.20% CAGR through 2031.

- By application, knee accounted for 37.45% share of the sports medicine biologics market size in 2025, while foot and ankle are forecast to advance at 6.57% CAGR through 2031.

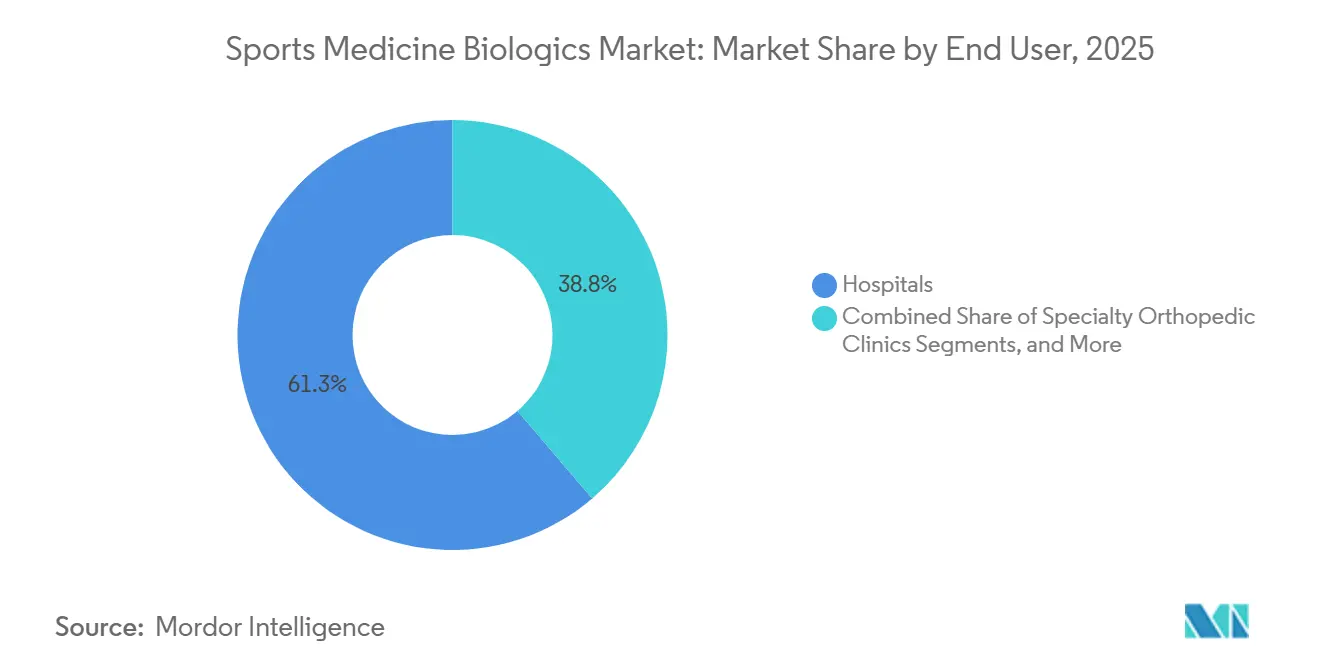

- By end user, hospitals represented 61.25% of revenue in 2025, while specialty orthopedic clinics are set to grow at 7.10% CAGR through 2031.

- By geography, North America held 40.30% of revenue in 2025, while Asia-Pacific is projected to record the fastest CAGR of 7.45% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Sports Medicine Biologics Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Rising sports injury burden and repeat procedure demand | +1.4% | Global, with demand concentrated in North America and Asia-Pacific | Medium term (2-4 years) |

| Shift toward faster recovery and reduced downtime | +1.1% | North America and Europe, spill-over to APAC core | Short term (≤ 2 years) |

| Expansion of arthroscopy-linked biologic adjacent procedures | +0.8% | North America, Western Europe | Medium term (2-4 years) |

| Surge in outpatient and ASC-based orthopedic care | +0.7% | North America, emerging in APAC core | Short term (≤ 2 years) |

| Growth in surgeon-preferred point-of-care biologic preparation systems | +0.6% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Sports Injury Burden and Repeat Procedure Demand

The global prevalence of musculoskeletal disorders rose by 71% between 1990 and 2024, and osteoarthritis is expected to remain the largest contributor through 2050, supporting a strong long-term addressable pool for the sports medicine biologics market. In the United States, sports-related injuries among adults over 65 are projected to reach 111,225 annually by 2040, up 119% from 2024, while the supply of sports medicine physicians is expected to rise by only 19.7% over the same period.[1]Sports Health, “Projected Growth in Sports-Related Injuries Among Older Adults and Sports Medicine Workforce Gaps,” SAGE Journals, doi.org This supply-demand gap supports office-based biologic treatment, as physicians can manage more patients in clinical settings than through surgery-intensive care pathways. The CDC burden cited in the source material places the annual cost of osteoarthritis in the United States at USD 137 billion and notes that 32.5 million adults are affected, reinforcing interest in biologic care before joint replacement.[2]NFL Player Health and Safety, “2025 Season Key Takeaways,” NFL, nfl.comQuality and tissue-handling requirements under FDA 21 CFR Part 1271 also raise operating standards, helping established suppliers defend their share in the sports medicine biologics market.

Shift Toward Faster Recovery and Reduced Downtime

Elite sports teams and organized rehabilitation programs are increasingly using autologous biologics, as faster return to activity now carries measurable competitive and financial value. NFL data cited for the 2025 regular season indicate a 25% decline in ACL tears, but cartilage repair demand remained firm as the injury mix shifted toward chronic degenerative and osteochondral conditions that still require intervention. A 2025 network meta-analysis of 23 randomized controlled trials found that leukocyte-poor PRP with high platelet concentration delivered the strongest WOMAC function and stiffness outcomes at 12 to 18 months, supporting more standardized treatment protocols.[3]Frontiers in Public Health, “Global, Regional, and National Burden of Musculoskeletal Disorders, 1990-2021,” Frontiers in Public Health, frontiersin.org Source: Sports Health, “Projected Growth in Sports-Related Injuries Among Older Adults and Sports Medicine Workforce Gaps,” SAGE Journals, doi.org

Expansion of Arthroscopy-Linked Biologic Adjacent Procedures

Arthroscopy is increasingly becoming a biologic-supported procedure as surgeons add PRP, scaffold systems, and graft support during repair. German clinical data published in Arthroskopie supported the use of autologous matrix-induced chondrogenesis and matrix-associated autologous chondrocyte transplantation for large chondral defects above 2 to 3 cm² in weight-bearing knee surfaces, expanding the need for dedicated biologic materials. This trend increases revenue per case without relying on a major rise in total arthroscopy volumes, which is especially relevant in mature procedure markets. Arthrex develops more than 1,000 new products and procedures each year and generated USD 158.9 million in orthobiologics revenue in 2025, showing how platform companies are embedding biologics into broader surgical workflows. As this attachment model deepens, the sports medicine biologics market benefits from higher procedure intensity and stronger system-level placement within orthopedic practices.

Surge in Outpatient and ASC-Based Orthopedic Care

The shift toward outpatient care is changing the growth pattern of the sports medicine biologics market, as many injection-based and minor implant procedures can be performed outside inpatient hospital settings. Ambulatory surgical centers offer a clear cost advantage over hospitals for several orthopedic interventions, making them a strong fit for biologic workflows that do not require a full inpatient setup. Bioventus reported 7.5% organic growth in 2025, supported by above-market Durolane demand in outpatient orthopedic settings, showing how closely product momentum is tied to non-hospital channels. Faster patient throughput and shorter authorization cycles also make outpatient settings commercially attractive when reimbursement is available. At the same time, ISO 13485 compliance and facility accreditation requirements continue to favor suppliers with stronger quality systems and broader channel support.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Payer reluctance toward nonstandardized biologic therapies | -1.1% | North America, spill-over to EU private insurance markets | Short term (≤ 2 years) |

| Regulatory scrutiny on cell-based and human tissue products | -0.9% | Global, most acute in North America and EU | Medium term (2-4 years) |

| Inconsistent clinical evidence across product classes | -0.6% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Payer Reluctance Toward Nonstandardized Biologic Therapies

Insurance coverage remains the most immediate volume constraint for the sports medicine biologics market, particularly for PRP-based procedures. The Federal Employee Program Blue and other major payers classify PRP as investigational across orthopedic applications, including knee osteoarthritis, Achilles tendinopathy, lateral epicondylitis, and rotator cuff repair augmentation, limiting access for a large insured patient base. The key challenge is the absence of a standardized PRP product definition, as platelet concentration, leukocyte content, injection volume, and activation method vary across studies and clinical practices. A 2025 network meta-analysis is expected to confirm that these protocol differences produce materially different outcomes, reinforcing the payer view that PRP is not one consistent therapy. When reimbursement remains uncertain, practices find it harder to sustain repeat low-cost procedures, even as clinical interest remains high.[4]Journal of Orthopaedic Surgery and Research, “Network Meta-Analysis of PRP Formulations in Knee Osteoarthritis,” Journal of Orthopaedic Surgery and Research, springer.com

Regulatory Scrutiny On Cell-Based And Human Tissue Products

Regulatory oversight is tightening in the sports medicine biologics market, particularly for products positioned near the boundary between minimally manipulated tissue and full biologic therapy. The FDA’s distinction between Section 361 HCT/P exemptions and Section 351 biologics approval continues to determine which products can remain commercialized at scale and which require a longer approval pathway. As of 2024, no stem cell therapy has received FDA Section 351 approval for an orthopedic joint indication, keeping commercial timelines long for many advanced programs positioned as high-growth opportunities in the sports medicine biologics market. Organogenesis is expected to complete its rolling BLA submission for ReNu in April 2026 after receiving RMAT designation in 2021, highlighting the progress possible for strong programs and the time and capital required to reach that stage. In Europe, ATMP review requirements add another layer of compliance, while unresolved classification issues can result in access limits, enforcement risk, or delayed revenue realization.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Bone Graft Substitutes Lead, Stem Cell Therapies Set the Growth Pace

Bone graft substitutes captured 28.58% of the sports medicine biologics market share in 2025, making them the largest product category in the sports medicine biologics industry. Their leadership is supported by broad use in osteochondral lesion repair, bone void filling after ligament reconstruction, and reinforcement at tendon-to-bone fixation sites. Kuros Biosciences demonstrated scalability in this category, with its MagnetOs platform reaching 100,000 cumulative surgeries globally and generating USD 146.1 million in 2025 revenue, up 71.7% year over year. Stem cell-based products are forecast to grow at a CAGR of 6.20% through 2031, making them the fastest-growing product group in the sports medicine biologics market. This growth is supported by late-stage regulatory progress, as developers move closer to commercial decisions in major knee repair and osteoarthritis programs. MEDIPOST secured FDA agreement in June 2026 for a single pivotal Phase 3 study for CARTISTEM in the United States and Canada and is backing the strategy with USD 140 million for cGMP scale-up.

By Application: Knee Anchors Revenue, Foot And Ankle Outpaces the Field

Knee accounted for 37.45% of the sports medicine biologics market size in 2025, maintaining its position as the largest application area across the sports medicine biologics market. Demand spans viscosupplementation for knee osteoarthritis, autologous chondrocyte repair for osteochondral defects, PRP support in ACL and meniscal repair, and amniotic tissue injections for chronic joint symptoms. A 2025 systematic review and meta-analysis of 12 randomized controlled trials found that intra-articular leukocyte-poor PRP delivered better WOMAC total scores and VAS pain scores than hyaluronic acid at 6 and 12 months in knee osteoarthritis. Foot and ankle is projected to expand at a CAGR of 6.57% through 2031, making it the fastest-growing application in the sports medicine biologics market. Rising intervention volumes for Achilles tendon disorders, talar osteochondral lesions, and plantar fasciitis support this growth, as tissue healing in these conditions is often slower and revision risk remains a key concern.

By End User: Hospital Dominance Persists, Specialty Clinics Expand Fastest

Hospitals held 61.25% of end-user revenue in 2025, maintaining their position as the leading care setting across the sports medicine biologics market. Their dominance is supported by a higher concentration of complex multi-ligament cases, operative bone graft procedures, and autologous chondrocyte implantation surgeries that require strong sterile support and coordinated surgical teams. Large institutions also manage product handling, storage, and reporting requirements more efficiently under tissue and biologic quality rules. Specialty orthopedic clinics are projected to grow at a CAGR of 7.10% through 2031, the fastest rate among end-user categories in the sports medicine biologics market. These clinics are well positioned for PRP, viscosupplementation, and amniotic injections because the procedures are repeatable, physician-delivered, and do not require anesthesia-heavy support.

Geography Analysis

North America is expected to account for 40.30% of global revenue in 2025, maintaining its position as the largest regional block in the sports medicine biologics market. Extensive ambulatory surgical infrastructure, high sports participation, and an established device pathway support the commercialization of preparation systems and adjacent biologic tools. Reimbursement progress can materially improve market access, with Smith & Nephew’s expected 2025 Category 1 CPT code for CartiHeal AGILI-C showing how payment clarity can support procedure uptake. However, payer resistance remains the primary constraint, as major coverage policies continue to classify PRP as investigational for many orthopedic uses. Canada and Mexico remain smaller contributors, but both markets can expand as outpatient orthopedic infrastructure and reimbursement pathways develop further.

In Europe, Germany, the United Kingdom, and France anchor demand, while Germany remains a key clinical adoption center for cartilage biologics used in larger chondral defects. EU MDR requirements and the EMA ATMP framework increase entry costs for manufacturers, slowing some launches while protecting companies with compliant systems already in place. The United Kingdom adds further complexity, as separate MHRA oversight increases compliance requirements for pan-European strategies.

Asia-Pacific is projected to grow at a CAGR of 7.45% through 2031, making it the fastest-growing regional segment in the sports medicine biologics market. Growth is supported by expanding private sports clinics, rising orthopedic procedure volumes, and Japan’s relatively open regulatory environment for regenerative medicine pathways compared to many Western markets. MEDIPOST is expected to complete Phase 3 work for CARTISTEM in Japan in 2025 and plans to file for approval in Japan in H2 2026, with approval targeted for 2027. South Korea also remains important as a development and export base for advanced point-of-care systems, with Miracell expected to receive FDA 510(k) clearance in April 2026 for SMART M-CELL after earlier deployment across 40 countries. The Middle East and Africa, and South America, remain smaller markets today, but private hospital investment and broader orthopedic build-out keep them relevant to the long-term expansion of the sports medicine biologics market.

Competitive Landscape

The sports medicine biologics market remains moderately fragmented, with no single company accounting for more than 9.6% of orthobiologics revenue and more than 20 companies generating at least USD 50 million in annual sales. Companies compete across three broad groups: platform-led surgical companies, focused biologics specialists, and diversified medtech players that use biologics as one of several growth levers. Heraeus’s expected 2025 acquisition of bone void filler assets further highlights specialty materials companies’ interest in this adjacent growth opportunity. Even the largest sports medicine franchises have not achieved the same dominance in biologics that they hold in broader sports medicine hardware, creating opportunities for focused players to compete on evidence and access.

Regulatory progress, reimbursement recognition, and point-of-care efficiency are becoming stronger differentiators than product novelty alone in the sports medicine biologics market. Smith & Nephew’s Category 1 CPT code for AGILI-C demonstrated how payment recognition can support adoption beyond clinical evidence. Organogenesis strengthened its position by completing the ReNu BLA after receiving earlier RMAT designation, giving it a clearer regulatory path in amniotic-based therapy. Anika Therapeutics is also expected to advance its cartilage repair position in November 2025 by filing the final PMA module for Hyalofast, after the product had already built a large installed clinical base globally.

Point-of-care autologous cell concentration systems are adding another competitive layer across the sports medicine biologics market. Miracell’s expected FDA 510(k) clearance for SMART M-CELL in April 2026 would expand the US opportunity for same-session autologous preparation workflows. Established suppliers are also expanding their procedural reach, with Arthrex expected to launch the TightRope SB all-suture implant in February 2026 and MTF Biologics, with Kolosis BIO, expected to launch Summit Matrix in January 2026. Companies that do not invest in real-world evidence, registries, and payer-facing data packages may face increasing pressure as orthopedic purchasing becomes more value-driven.

Sports Medicine Biologics Industry Leaders

Stryker Corporation

Zimmer Biomet Holdings, Inc.

Medtronic plc

Arthrex, Inc.

Smith & Nephew plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: MEDIPOST secured FDA alignment for a pivotal Phase 3 CARTISTEM study in the United States and Canada, supported by South Korea and Japan Phase 3 data and real-world evidence from 550 patients.

- April 2026: Organogenesis Holdings completed a rolling Biologics License Application submission for ReNu, supported by two Phase 3 trials, including a larger 515-patient study that met its primary pain-reduction endpoint.

- April 2026: Miracell received U.S. FDA 510(k) clearance for its SMART M-CELL PRP and Bone Marrow Concentration Systems, expanding access to the U.S. market after commercialization in 40 countries.

- February 2026: Arthrex launched the TightRope SB all-suture implant for single-bundle ACL reconstruction, following use of nearly 2,000 implants in U.S. procedures before commercialization.

- January 2026: MTF Biologics and Kolosis BIO launched Summit Matrix, a synthetic bone graft for orthopedic and spinal surgeries using NanoLift nanoscale surface technology to improve osseointegration.

Global Sports Medicine Biologics Market Report Scope

As per the scope of the report, in sports medicine, biologics (or orthobiologics) are natural, non-surgical treatments that use substances harvested from the body, like concentrated blood platelets or stem cells, to accelerate the healing of injured muscles, tendons, ligaments, and cartilage.

The sports medicine biologics market is segmented by product type, application, end user, and geography. By product type, the market includes platelet-rich plasma products, bone graft substitutes, bone morphogenetic proteins, stem cell-based products, viscosupplementation products, amniotic and placental tissue products, hyaluronic acid injections, and others. By application, the market is segmented into knee, shoulder, foot and ankle, hip and groin, elbow and wrist, and others. By end user, the market is segmented into hospitals, ambulatory surgical centers, specialty orthopedic clinics, sports medicine centers, and others. By geography, the market is analyzed across North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the market sizes and forecasts in terms of value (USD) for the above segments.

| Platelet-Rich Plasma Products |

| Bone Graft Substitutes |

| Bone Morphogenetic Proteins |

| Stem Cell-Based Products |

| Viscosupplementation Products |

| Amniotic And Placental Tissue Products |

| Hyaluronic Acid Injections |

| Others |

| Knee |

| Shoulder |

| Foot And Ankle |

| Hip And Groin |

| Elbow And Wrist |

| Others |

| Hospitals |

| Ambulatory Surgical Centers |

| Specialty Orthopedic Clinics |

| Sports Medicine Centers |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Platelet-Rich Plasma Products | |

| Bone Graft Substitutes | ||

| Bone Morphogenetic Proteins | ||

| Stem Cell-Based Products | ||

| Viscosupplementation Products | ||

| Amniotic And Placental Tissue Products | ||

| Hyaluronic Acid Injections | ||

| Others | ||

| By Application | Knee | |

| Shoulder | ||

| Foot And Ankle | ||

| Hip And Groin | ||

| Elbow And Wrist | ||

| Others | ||

| By End User | Hospitals | |

| Ambulatory Surgical Centers | ||

| Specialty Orthopedic Clinics | ||

| Sports Medicine Centers | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the sports medicine biologics space?

The sports medicine biologics market is valued at USD 1.88 billion in 2026 and is projected to reach USD 2.43 billion by 2031 at a 5.25% CAGR.

Which product category leads revenue generation?

Bone Graft Substitutes led in 2025 with 28.58% share, supported by broad use across repair, reconstruction, and fixation support procedures.

Which application area is growing the fastest?

Foot And Ankle is the fastest-growing application with a projected 6.57% CAGR through 2031, helped by rising use in Achilles, talar, and plantar cases.

Why does North America remain the largest regional contributor?

North America held 40.30% of revenue in 2025 because it combines strong outpatient infrastructure, high sports participation, and more established reimbursement pathways.

What is the biggest challenge to wider adoption?

Payer reluctance toward nonstandardized biologic therapies remains the main barrier, especially for PRP, where large insurers still classify many uses as investigational.

How competitive is the sports medicine biologics field?

The field is moderately fragmented, with no player above 9.6% share and more than 20 companies generating at least USD 50 million in annual sales.

Page last updated on: