Sponsorship Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 177.44 Billion |

| Market Size (2031) | USD 234.46 Billion |

| Growth Rate (2026 - 2031) | 5.73% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Sponsorship Market Analysis by Mordor Intelligence

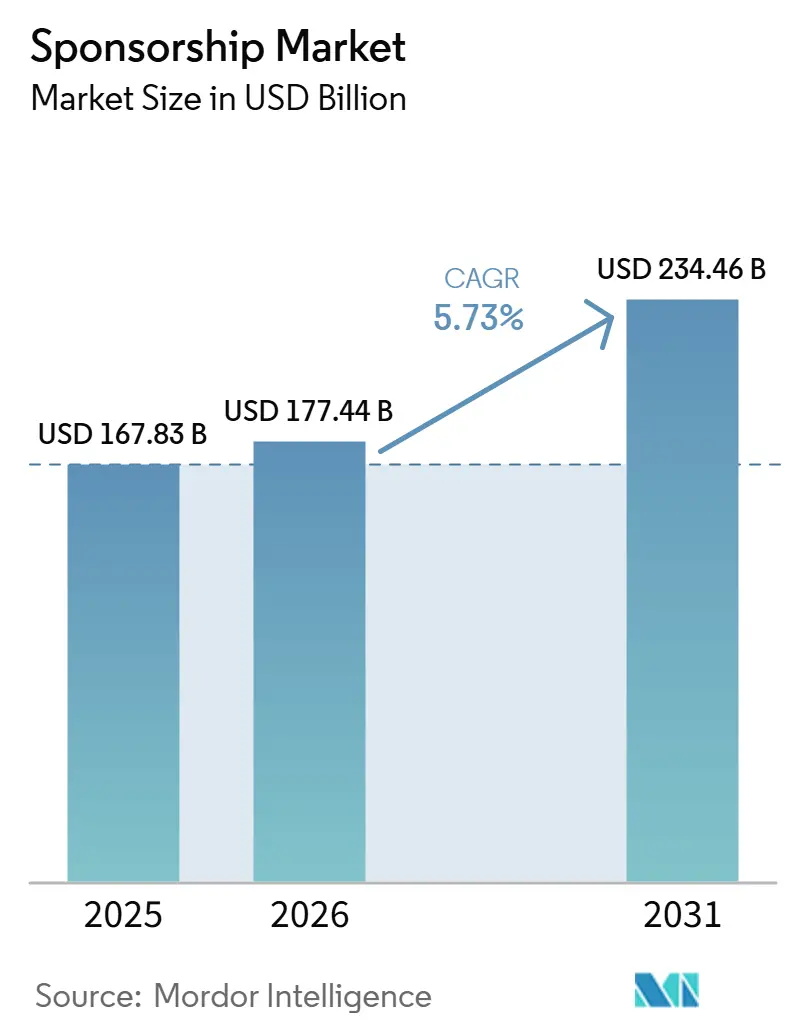

The Sponsorship market size was valued at USD 167.83 billion in 2025 and estimated to grow from USD 177.44 billion in 2026 to reach USD 234.46 billion by 2031, at a CAGR of 5.73% during the forecast period (2026-2031). The sponsorship market is expanding as brands and rights holders move away from broad exposure deals and toward activation models tied to measurable business outcomes. Live entertainment, digital streaming, and social media now work together as one commercial environment, which gives sponsors a longer and more active presence with audiences than venue signage alone. Brand owners are concentrating budgets around properties that can support shared data, clearer performance tracking, and stronger renewal cases, while rights holders are investing more in digital inventory, reporting capability, and packaged multi-channel assets. Competitive strategy is also shifting toward scale in data, measurement, and execution, as large holding companies, specialist agencies, and platform providers build more integrated sponsorship capabilities. At the same time, the sponsorship market still faces pressure from uneven attribution across channels and changing privacy rules, which continue to influence deal design, valuation, and renewal confidence.

Key Report Takeaways

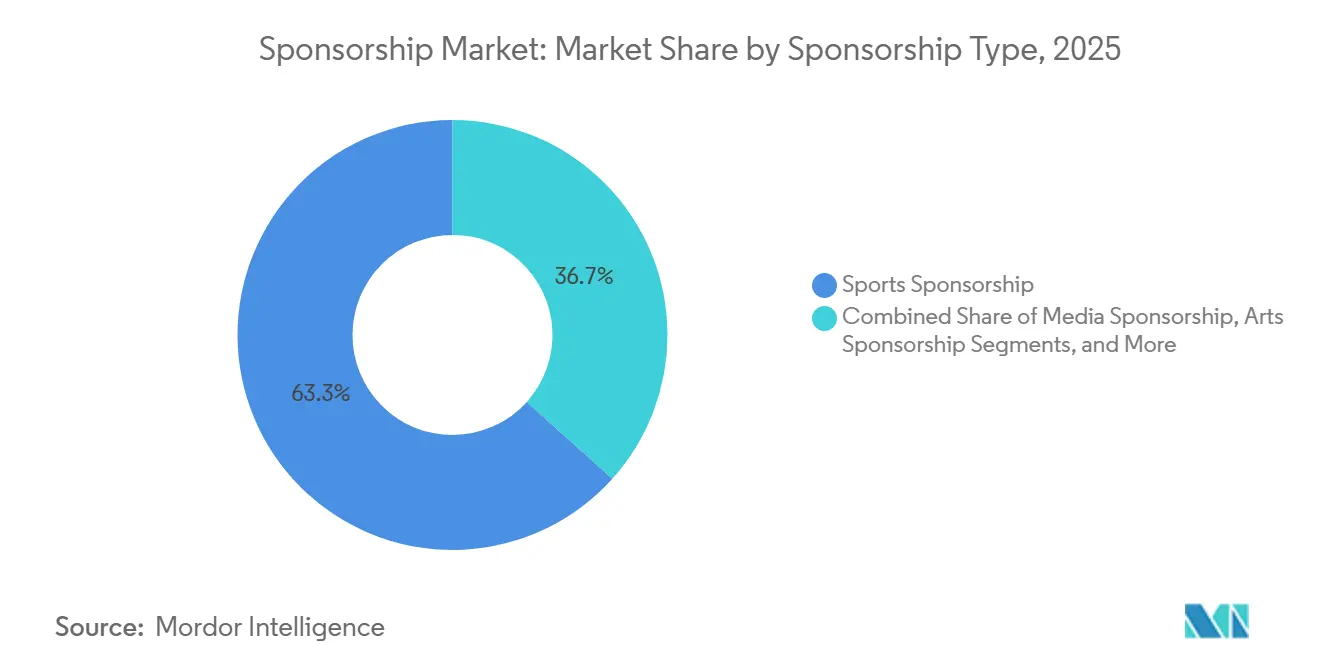

- By Sponsorship Type, Sports led with 63.34% revenue share in 2025, while Media is projected to expand at a 6.61% CAGR through 2031.

- By Sponsorship Rights, Endorsement Rights held 39.72% of the Sponsorship Market size in 2025, while Licensing Rights are projected to advance at a 9.17% CAGR through 2031.

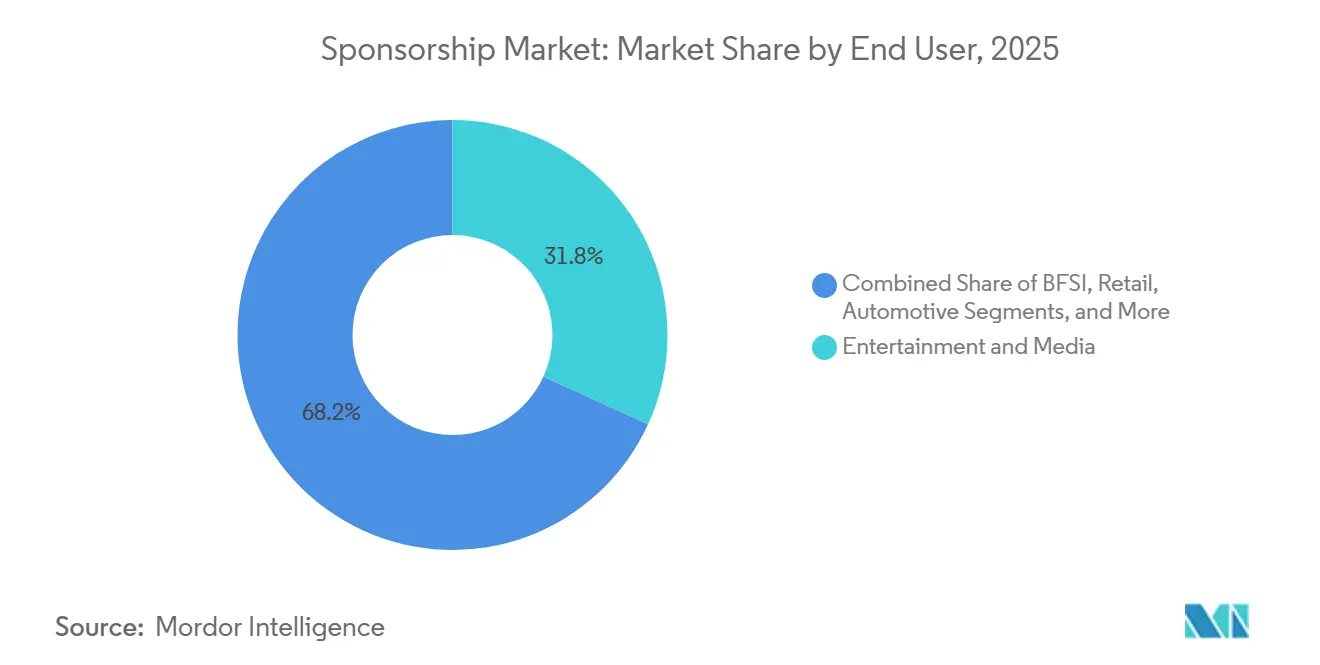

- By End User, Entertainment and Media accounted for 31.82% share in 2025, while BFSI is projected to grow at a 9.42% CAGR through 2031.

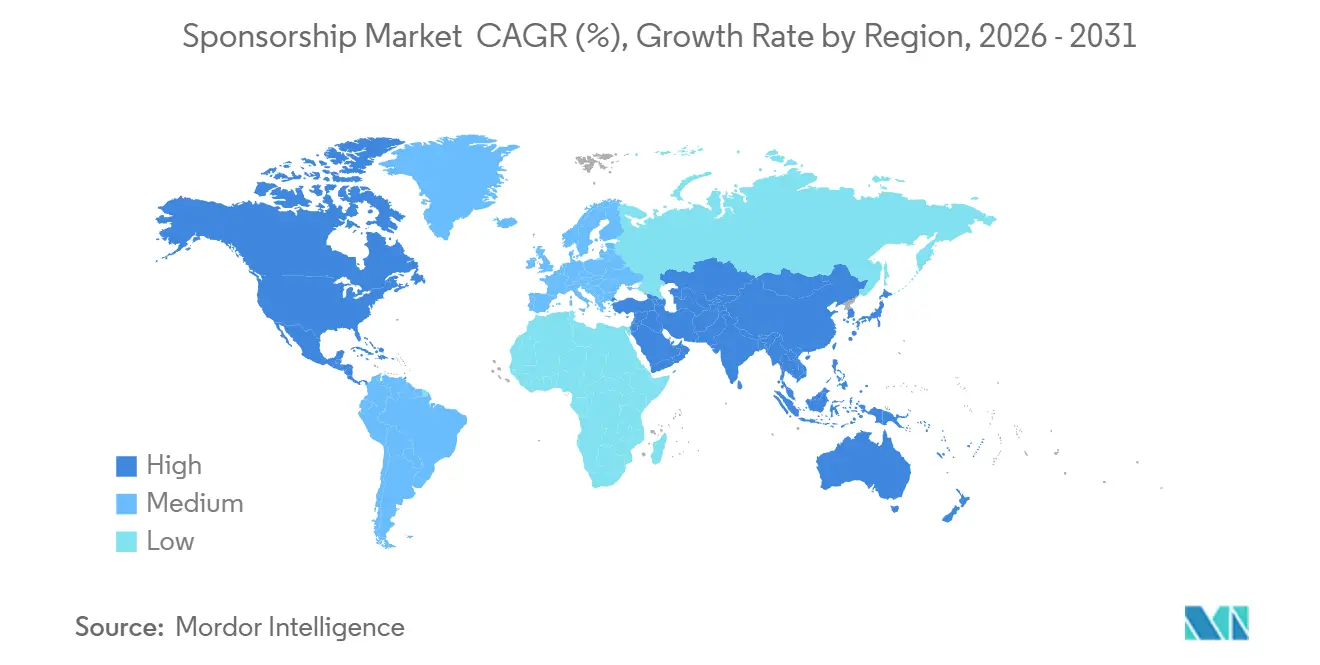

- By Geography, North America held 38.11% of the Sponsorship Market share in 2025, while Asia-Pacific is projected to expand at a 10.92% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Sponsorship Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Brand Demand for Measurable Return on Sponsorship Spend | +1.4% | Global | Short term (≤ 2 years) |

| Expansion of Data-Driven Sponsorship Valuation Platforms | +1.2% | Global, with early-mover advantage in North America and Europe | Medium term (2-4 years) |

| Growth of Creator-Led and Influencer-Led Property Inventories | +1.1% | Global, concentrated in North America and Asia-Pacific | Short term (≤ 2 years) |

| Multi-Channel Activation Across Live, Digital, and Social Media | +0.9% | Global | Medium term (2-4 years) |

| Rights Holders Packaging More Tiered and Modular Inventory | +0.7% | North America and Europe, spillover to APAC | Medium term (2-4 years) |

| Automation of Contracting, Approvals, and Reporting Workflows | +0.6% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Brand Demand For Measurable Return On Sponsorship Spend

Brands are moving away from sponsorship programs that cannot show business outcomes, and that shift is concentrating spend around properties with stronger data systems. Deals are increasingly built around shared data layers, pre-agreed KPIs, and clearer reporting routines, which makes performance review part of the core commercial package rather than an afterthought. Live Nation reported sponsorship and advertising revenue of USD 258.6 million in Q1 2026, up 20% year over year, which shows that properties with broad and trackable fan engagement continue to draw higher brand demand.[1]Live Nation Entertainment, “Live Nation Entertainment Reports First Quarter 2026 Results,” Live Nation Entertainment TKO also reported growth in partnerships and marketing revenue across UFC and WWE in full year 2025, reinforcing that premium live properties with repeatable commercial inventory can grow faster than the wider sponsorship market.[2]TKO Group Holdings, “TKO Reports Fourth Quarter and Full Year 2025 Results,” TKO Group Holdings This is pushing the sponsorship market toward fewer but larger partnerships that are easier for brand teams to defend during budget review and renewal discussions.

Expansion Of Data-Driven Sponsorship Valuation Platforms

Data-driven valuation platforms are changing sponsorship economics because they reduce the information gap that once favored sellers with opaque pricing and broad media-value claims. SponsorUnited introduced its 4.0 platform in February 2026 with AI-enabled intelligence built across 2.2 million deals and 21.1 million data points, which signals that benchmarked pricing and partner intelligence are becoming more accessible across the market. Two Circles also deployed its KORE Sponsorship and Partner Engagement platform for the German Football Association in February 2026, bringing structured asset value analysis, deal efficiency tracking, and data-led commercial planning into federation-level operations. As more rights holders adopt similar systems, buyers can compare inventory quality more consistently, which puts downward pressure on sellers that still lack asset-level evidence. The sponsorship market is therefore rewarding properties and agencies that can pair relationship management with live commercial intelligence and measurable reporting.

Growth Of Creator-Led and Influencer-Led Property Inventories

Creator-led inventory is gaining importance because it gives brands targeted reach, persistent audience access, and native digital distribution inside sponsorship programs. Lowe’s launched its Home Improvement Creator Network in June 2025 with MrBeast among the first creators, showing that brands are moving creator relationships into structured and scalable commercial programs rather than one-off promotional deals. The model turned creators into repeatable inventory that could support storefronts, funded projects, and branded content across several digital touchpoints, which reflects the broader commercial value of creator-led sponsorship packaging. Rights holders in sports and entertainment are under pressure to add creator programming as a first-party asset so that audience attention stays inside the sponsorship package instead of moving to outside platforms with no shared upside. This is widening the sponsorship market beyond venue signage and broadcast placements into creator communities, commerce links, and year-round social engagement.

Multi-Channel Activation Across Live, Digital, and Social Media

Multi-channel activation is expanding the amount of inventory that can be sold within a single sponsorship agreement. Live Nation’s Q1 2026 results showed that brands continue to pay for venue, digital, and promotional exposure in one package, with sponsorship and advertising revenue rising 20% to USD 258.6 million. Kraft Heinz also entered a multi-year partnership with Live Nation across 80 venues in the United States in July 2025, linking menu integration, fan experience, and event presence inside one commercial structure. When sponsors can connect physical presence, social engagement, and post-event interaction, they gain a clearer view of performance across the full fan journey. That feedback loop strengthens renewal cases and rewards rights holders that invest in integrated inventory design across live, digital, and social media touchpoints.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented Attribution Across Offline and Digital Touchpoints | -1.3% | Global | Medium term (2-4 years) |

| Budget Scrutiny From CFO-Led Marketing Governance | -1.0% | Global, most acute in North America and Europe | Short term (≤ 2 years) |

| Short Deal Cycles and Renewal Volatility | -0.6% | Global | Short term (≤ 2 years) |

| Privacy Constraints on Audience-Level Measurement | -0.5% | Europe, with Asia-Pacific and North America spillover | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Fragmented Attribution Across Offline and Digital Touchpoints

Fragmented attribution remains one of the biggest constraints on growth because sponsors still struggle to connect live events, broadcast exposure, out-of-home presence, and digital engagement into one comparable performance view. This makes it harder to build repeatable business cases for renewal, especially when different markets and channels use different standards for audience and activation reporting. The German Football Association’s rollout of Two Circles’ KORE platform highlights why rights holders are investing in systems that can unify asset value analysis, sales operations, and deal efficiency tracking inside one workflow.[3]Two Circles, “DFB Rolls Out an Intelligent Sponsorship Platform, Deploying KORE Sponsorship and Partner Engagement,” Two Circles Properties that can share cleaner and more connected data with brand partners are better positioned to defend premium pricing and longer commitments. The sponsorship market still loses some momentum when advertisers cannot compare contribution across channels with enough confidence to support portfolio-wide renewal decisions.

Budget Scrutiny From CFO-Led Marketing Governance

Budget scrutiny is increasing the burden of proof for sponsorship spending, which means narrative-led selling is becoming less effective than structured commercial reporting. This pressure is favoring partners that can combine data, audience intelligence, media execution, and activation support inside one operating model. Omnicom’s completed acquisition of IPG in November 2025 and Publicis Groupe’s April 2026 acquisition of 160over90 show that large service groups see measurement scale and execution breadth as necessary to win and protect client budgets. Smaller agencies and properties that still rely on broad awareness narratives face a harder selling environment when procurement and finance teams want clearer proof of value. As a result, budget discipline is shortening deal cycles and shifting more spend toward partners with stronger commercial systems and renewal visibility.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Sponsorship Type: Sports Dominance Accelerates Property Diversification

Sports sponsorship held 63.34% of the Sponsorship market share in 2025, which confirms that live sports still offer the deepest pool of premium inventory and the widest scale of emotionally engaged audience attention. That lead continues to rest on the ability of major sports properties to deliver repeated visibility, sponsorship layers across events and venues, and stronger commercial renewal logic than most other formats. TKO’s 2025 results showed continued growth in partnerships and marketing revenue across UFC and WWE, which supports the view that premium sports and sports-adjacent properties remain central to sponsor allocation. Sports dominance also creates a harder environment for smaller arts, educational, and niche entertainment properties, because brand budgets that flow heavily into flagship sports deals leave less room for secondary categories unless they offer a distinct audience or activation angle. Media is projected to expand at a 6.61% CAGR through 2031, which reflects growing demand for branded content integrations, podcast sponsorships, and streaming partnerships that place brands inside content rather than around it.

Arts and entertainment sponsorship are becoming more strategically useful when brands want cultural differentiation beyond crowded sports inventory. Hyundai Motor Group’s June 2026 support for cultural and artistic exchanges between Korea and France, including the Festival d’Avignon, shows how arts sponsorship can serve cross-market positioning goals while still supporting visibility and engagement. Educational sponsorship continues to build gradually because STEM and talent pipeline partnerships give companies both brand exposure and workforce relevance in the same program. The others category remains important because it absorbs esports integrations, sustainability-linked sponsorships, and community programs that do not fit neatly into legacy type classifications. Creator-centered initiatives such as Lowe’s creator network also show how nontraditional media inventory is becoming more formalized, which supports broader diversification inside the sponsorship market.

By Sponsorship Rights: Licensing Rights Lead as IP Monetization Scales

Endorsement rights retained 39.72% of the segment in 2025, which shows that brands still value athlete and celebrity association when those relationships can transfer trust, relevance, and cultural visibility. Endorsement remains strong because it can work across sport, entertainment, retail, and financial services, and it often gives sponsors a faster path to audience connection than property-only branding. At the same time, brands are placing more pressure on endorsers to support measurable commerce, social engagement, and conversion activity rather than awareness alone. Licensing rights are projected to grow at a 9.17% CAGR through 2031, the fastest pace in this Sponsorship market size mix, because IP-led product extensions and digital integrations can keep generating revenue after the initial sponsorship moment. Spin Master’s April 2026 renewal of its worldwide master toy licensing agreement with Feld Motor Sports for Monster Jam, with more than 75 million toy units distributed since 2019, shows how licensing can turn sponsorship-linked IP into durable commercial output.

Naming rights still represent a smaller share by deal count, but they attract high value per contract because they combine long duration, repeated public visibility, and strong place-based brand association. TKO’s September 2025 extension of its exclusive partnership with T-Mobile Arena through 2030 shows how long-duration venue-linked rights can preserve premium visibility across recurring live events. Merchandising rights are also gaining importance as rights holders connect brand affinity with direct-to-fan product sales at events and through digital storefronts. Overall, the rights mix is shifting away from one-time placement value and toward repeatable IP monetization that can travel across products, venues, and media channels.

By End User: BFSI Pursues Mass Trust at Sponsorship Scale

Entertainment and Media accounted for 31.82% of demand in 2025, which reflects the close fit between content-rich environments and the sponsorship formats that depend on live audience attention, recurring events, and branded experiences. This segment benefits from the fact that entertainment companies already operate inside the same venue, ticketing, fan, and content systems that now drive sponsorship packaging. Retail and automotive end users continue to use sponsorship to maintain visibility in fragmented media environments where traditional broadcast reach is less dependable than before. Ram’s multi-year strategic partnership with TKO across WWE, UFC, and PBR from January 2026 shows how automotive brands are using multi-property platforms to stay present across several fan communities at once. BFSI is projected to expand at a 9.42% CAGR through 2031, which makes it the fastest-growing end-user category as financial brands use sponsorship to build trust, familiarity, and long-cycle customer consideration.

The BFSI growth pattern is especially important because it shows that sponsorship is not being treated as discretionary awareness spending in every case, but as a recurring brand infrastructure tool in markets where trust strongly influences purchase behavior. Financial services advertisers tend to favor large fan communities, high-frequency visibility, and rights structures that can support both compliance discipline and broad consumer relevance. These priorities fit well with long-duration partnerships, venue-linked assets, and premium live properties that can support repeated exposure without relying on a single campaign window. Healthcare and education also continue to participate where institutional reputation and public engagement matter, while the others category captures growing technology and sustainability demand that has not yet reached standalone scale. Across end users, the sponsorship market is seeing stronger allocation toward sectors that can use partnerships for both long-term brand building and clearer commercial conversion paths.

Geography Analysis

North America held 38.11% of the Sponsorship market share in 2025, which keeps the region in the lead because it combines dense professional sports leagues, mature naming-rights inventory, strong agency infrastructure, and high commercial pricing power. The United States remains the main revenue center because brands can access large-scale live sports, music, and entertainment platforms with established sponsor packaging and frequent activation windows. Live Nation’s Q1 2026 sponsorship and advertising revenue rose 20% year over year to USD 258.6 million, which reflects the monetization depth available in North American live entertainment. TKO’s full year 2025 partnerships and marketing growth, along with its 2025 extension with T-Mobile Arena through 2030, also shows that premium North American live properties continue to deepen sponsor relationships and preserve long-duration value. Europe is also moving up the value chain as agency consolidation, data-led activation, and higher-value premium rights continue to reshape how pan-European brands structure sponsorship execution.

Asia-Pacific is projected to grow at a 10.92% CAGR through 2031, the fastest pace within the Sponsorship market size, supported by rising sports consumption, broader digital media infrastructure, and the growing commercial weight of cricket, football, esports, and fan-driven entertainment. The region benefits from a mix of mobile-first engagement and strong live fandom, which gives sponsors more room to connect digital discovery with in-person activation. Infront renewed its partnership with the Badminton World Federation through 2034, which points to long-horizon confidence in rights monetization and sponsor demand across Asia-Pacific sports ecosystems. South Korea’s cultural export model is also shaping commercial behavior, and Hyundai Motor Group’s June 2026 support for cultural and artistic exchanges between Korea and France shows how Asia-based brands are using sponsorship to build international narratives beyond domestic media spend. This combination of sports rights, creator ecosystems, and cross-border brand ambition keeps Asia-Pacific well positioned for above-market expansion.

South America is becoming a more mature commercial arena, while the Middle East and Africa are building broader sponsor ecosystems around sports, music, and destination branding. SPORTFIVE’s 2026 commercial partnership with the International Hockey Federation across the Middle East, South Asia, Europe, and the United Kingdom shows how rights bodies are using global agency support to widen sponsor access beyond traditional geographies. The Middle East continues to move from state-backed visibility programs toward a more diversified commercial structure, and national advertising frameworks still influence which categories can scale. Africa remains earlier in development, but diaspora-led entertainment properties and cross-border streaming ties are creating a wider base for future sponsorship demand.

Competitive Landscape

The sponsorship market remains moderately fragmented, with competition led by a handful of established players. SponsorUnited, Inc. emerged as the leading participant in the input ranking, supported by its strong pure-play position in sponsorship intelligence and analytics across sports and entertainment partnerships. Two Circles Limited is recognized for its data-led commercial growth model and advisory role across major sports properties and leagues. SPORTFIVE GmbH & Co. KG is supported by its broad global footprint in rights sales, sponsorship activation, and commercial partnerships across multiple sports verticals. Infront Sports & Media AG and Omnicom Group Inc. also rank among the leading participants, reflecting a competitive landscape that includes both specialist sports marketing firms and diversified agency networks.

SponsorUnited has strengthened its position by expanding its intelligence-led platform offering, including the February 2026 launch of SponsorUnited 4.0, which added AI-powered capabilities across a large deal and brand database. That move reinforced its role in helping brands, rights holders, and agencies benchmark partnerships, evaluate asset values, and improve planning accuracy. Two Circles has also advanced its competitive position through platform-led commercialization, including the February 2026 deployment of its KORE Sponsorship and Partner Engagement platform for the German Football Association. This gave the company deeper visibility in federation-level sales operations, asset analysis, and structured commercial decision-making. Omnicom’s position in the sponsorship market was strengthened by its completed acquisition of IPG in November 2025, which expanded its scale in integrated marketing, data, and sponsorship activation services.

SPORTFIVE continues to compete through its wide rights and activation network, with recent moves including its July 2026 LED and virtual advertising partnership with Villarreal CF and its commercial partnership with the International Hockey Federation. Infront Sports and Media remains important in the sponsorship market because of its strong presence in sports rights commercialization and its long-term renewal with the Badminton World Federation, which extends through 2034. The competitive pattern shows that specialist firms are leading in sponsorship data, rights packaging, and commercial execution, while larger agency groups compete through broader brand relationships and cross-channel delivery. Overall, the sponsorship market is being shaped by players that can combine analytics, sales capability, rights access, and measurable activation at scale.

Sponsorship Industry Leaders

SponsorUnited, Inc.

Two Circles Limited

SPORTFIVE GmbH & Co. KG

Omnicom Group Inc.

Infront Sports & Media AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2026: SPORTFIVE and Villarreal CF announced a new LED and virtual advertising partnership, extending SPORTFIVE's digital inventory activation to one of Spain's top LaLiga clubs and enabling dynamic in-stadium brand placements accessible to international sponsors without physical presence, a model that is becoming a standard mechanism for extending rights holder commercial reach across digital broadcast windows.

- April 2026: Publicis Groupe announced a definitive agreement to acquire 160over90, the premier global sports and culture-first agency, creating the industry's leading data-driven sport and culture platform with reach across the United States, the United Kingdom, EMEA, and Asia-Pacific, and integrating with Epsilon identity data for end-to-end planning, personalization, and measurement across media, experiential, content, and sponsorship activation.

- February 2026: Two Circles deployed its KORE Sponsorship and Partner Engagement platform for the German Football Association, enabling data-led decision-making across commercial sales operations, asset value analysis, deal efficiency tracking, and structured offer development, signaling the accelerating adoption of intelligent sponsorship infrastructure at national federation level in European football.

Global Sponsorship Market Report Scope

The Sponsorship Market Report is Segmented by Sponsorship Type (Sports Sponsorship, Arts Sponsorship, Entertainment Sponsorship, Educational Sponsorship, Media Sponsorship, and Other Sponsorship Types), Sponsorship Rights (Naming Rights, Endorsement Rights, Licensing Rights, Merchandising Rights, and Other Sponsorship Rights), End User (Retail, Automotive, Healthcare, BFSI, Entertainment and Media, Education, and Other End Users), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Sports Sponsorship |

| Arts Sponsorship |

| Entertainment Sponsorship |

| Educational Sponsorship |

| Media Sponsorship |

| Other Sponsorship Types |

| Naming Rights |

| Endorsement Rights |

| Licensing Rights |

| Merchandising Rights |

| Other Sponsorship Rights |

| Retail |

| Automotive |

| Healthcare |

| BFSI |

| Entertainment and Media |

| Education |

| Other End Users |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Qatar | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Nigeria | |

| Rest of Africa |

| By Sponsorship Type | Sports Sponsorship | |

| Arts Sponsorship | ||

| Entertainment Sponsorship | ||

| Educational Sponsorship | ||

| Media Sponsorship | ||

| Other Sponsorship Types | ||

| By Sponsorship Rights | Naming Rights | |

| Endorsement Rights | ||

| Licensing Rights | ||

| Merchandising Rights | ||

| Other Sponsorship Rights | ||

| By End User | Retail | |

| Automotive | ||

| Healthcare | ||

| BFSI | ||

| Entertainment and Media | ||

| Education | ||

| Other End Users | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Qatar | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the 2026 value of the sponsorship market?

The sponsorship market stands at USD 177.44 billion in 2026 and is forecast to reach USD 234.46 billion by 2031 at a CAGR of 5.73%.

Which sponsorship type leads global demand?

Sports is the largest sponsorship type, with 63.34% share in 2025, supported by the scale and repeatable inventory of live sports properties.

Which sponsorship rights category is growing the fastest?

Licensing rights is the fastest-growing rights category and is projected to expand at a 9.17% CAGR through 2031 as IP monetization becomes more important.

Which end-user group is expanding the fastest?

BFSI is projected to grow at a 9.42% CAGR through 2031 because sponsorship helps financial brands build trust, familiarity, and broad consumer reach.

Which region is growing the fastest in sponsorship?

Asia-Pacific is the fastest-growing region, with a projected CAGR of 10.92% through 2031, supported by strong sports consumption and expanding digital media infrastructure.

What is changing competition in sponsorship services?

Competition is shifting toward firms that can combine data, measurement, activation, and operational scale, as shown by Omnicoms IPG acquisition and Publicis Groupes acquisition of 160over90.

Page last updated on: