Spinal Stenosis Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

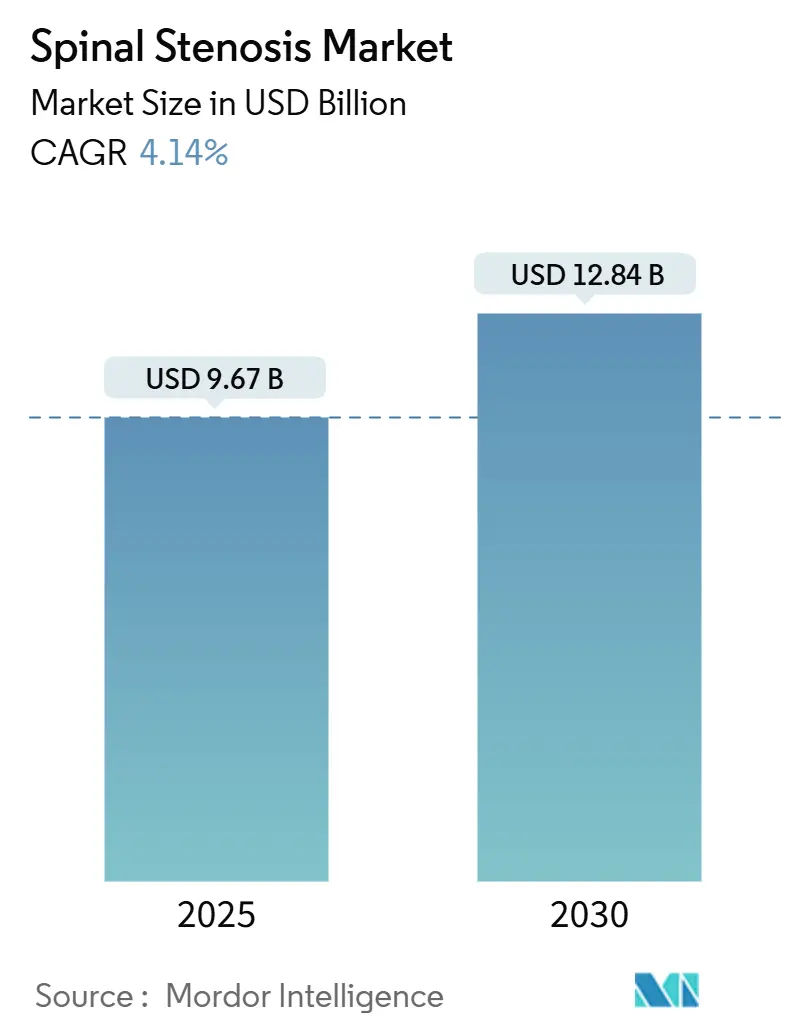

| Market Size (2025) | USD 9.67 Billion |

| Market Size (2030) | USD 12.84 Billion |

| Growth Rate (2025 - 2030) | 4.14% CAGR |

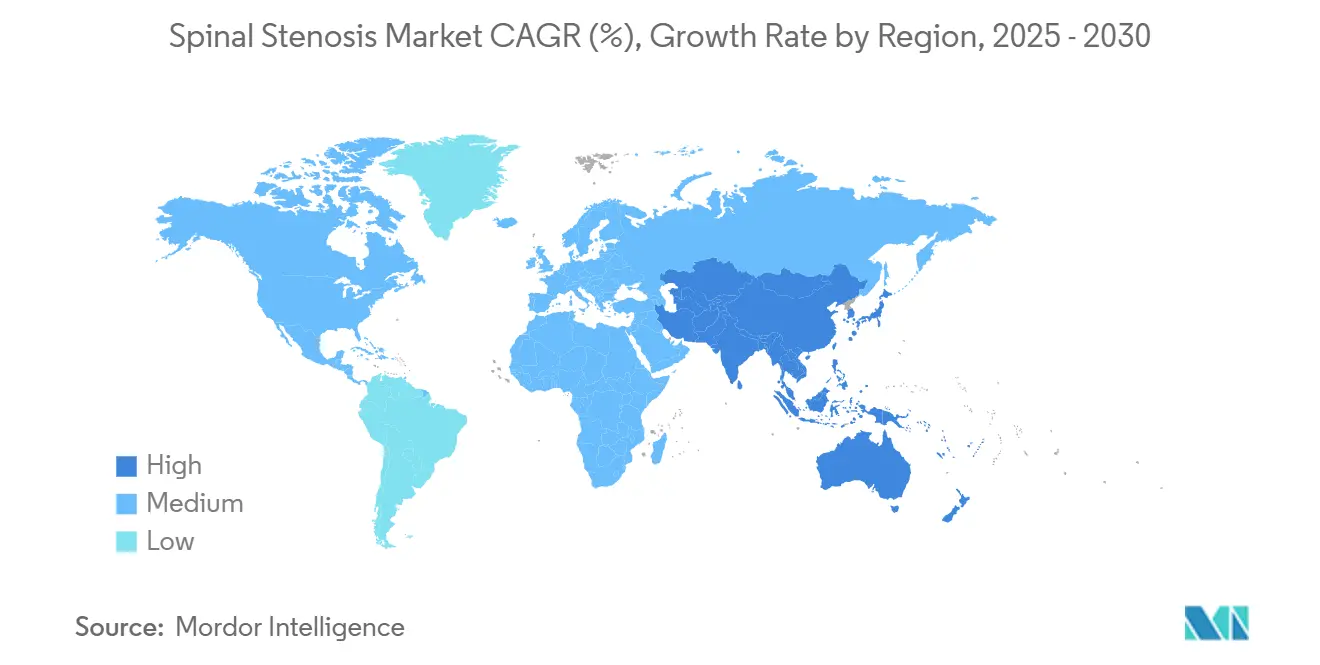

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

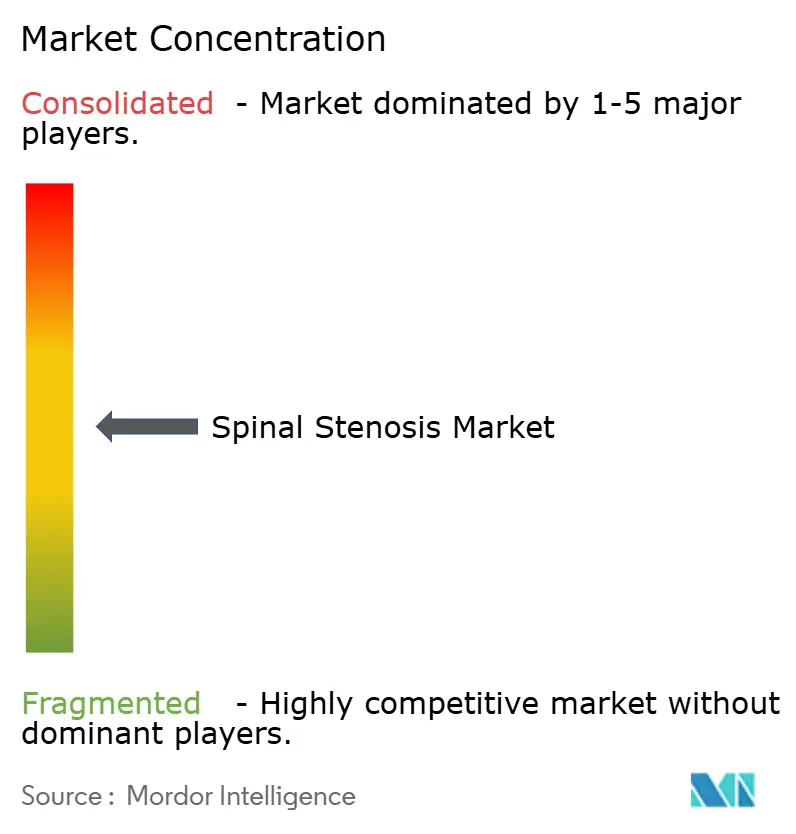

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Spinal Stenosis Market Analysis by Mordor Intelligence

The Spinal Stenosis Market size is estimated at USD 9.67 billion in 2025, and is expected to reach USD 12.84 billion by 2030, at a CAGR of 4.14% during the forecast period (2025-2030).

Aging populations, outpatient–friendly payment rules, and rapid implant refresh cycles anchor near-term demand, while motion-preservation platforms steadily erode the fusion stronghold. Ambulatory surgical centers (ASCs) now absorb a growing share of decompression and single-level fusion cases, compelling vendors to release implants that minimize anesthesia time and enable same-day discharge. Device makers widen portfolios with AI navigation, 3D-printed cages, and endoscopic instrumentation to satisfy surgeons who prioritize precision and speed. Competitive intensity centers on ecosystem scale rather than price, and regulatory tailwinds in Asia-Pacific invite domestic entrants that challenge Western incumbents.

Key Report Takeaways

- By product type, fusion implants held 55.32% of spinal stenosis market share in 2024, while motion-preservation devices are advancing at a 9.1% CAGR through 2030.

- By anatomical region, lumbar procedures commanded 57.43% of the spinal stenosis market in 2024; cervical interventions exhibit the fastest growth at a 7.9% CAGR to 2030.

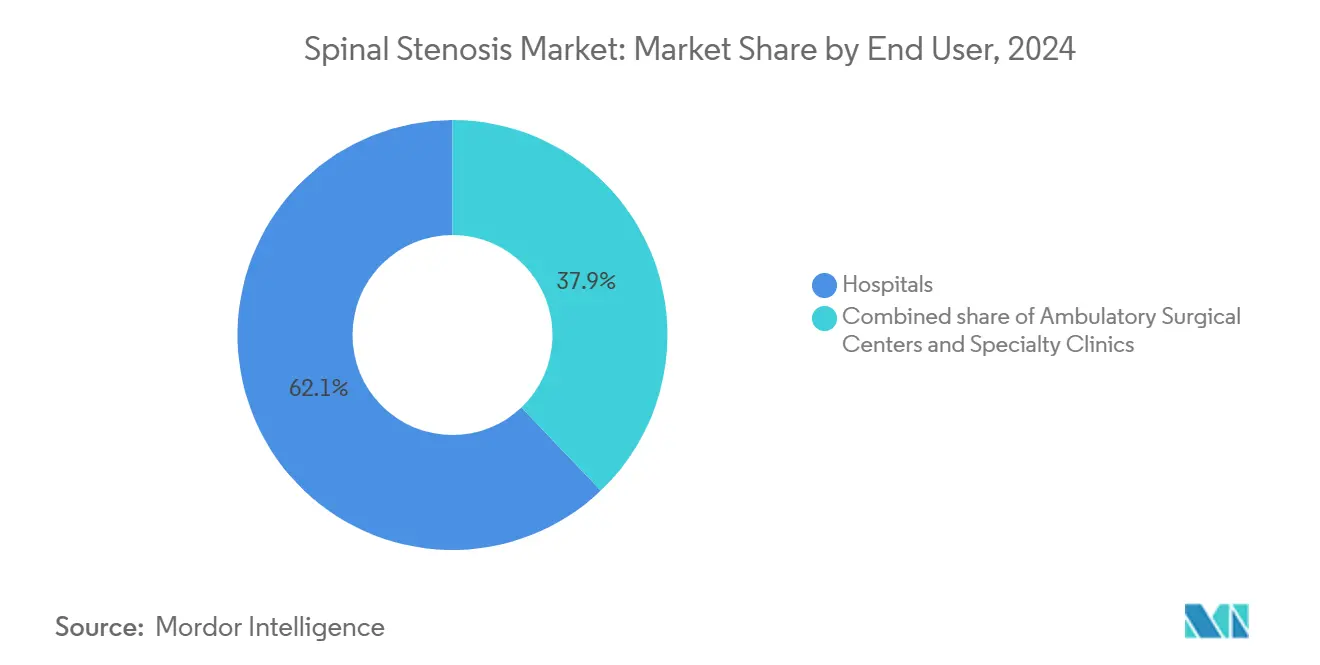

- By end user, hospitals retained 62.12% share in 2024, but ASCs are growing at an 8.4% CAGR on the back of the 2025 U.S. OPPS rule that expanded outpatient spine coverage.

- By geography, North America represented 42% revenue in 2024; Asia-Pacific is set to expand at a 7.2% CAGR through 2030, spurred by India’s USD 50 billion device industrial policy and accelerated Chinese approvals.

Global Spinal Stenosis Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Aging Population & Disease Prevalence Surge | +1.2% | Global, led by U.S., EU, Japan | Long term (≥ 4 years) |

| Adoption of Minimally Invasive & Endoscopic Procedures | +0.9% | North America, EU, rising in Asia-Pacific | Medium term (2-4 years) |

| Implant Technology Upgrades (3D-Printing, Biomaterials) | +0.7% | North America, Europe, early Asia-Pacific | Medium term (2-4 years) |

| Shift to Ambulatory Surgical Centers Boosts Device Refresh | +0.8% | U.S., Australia, UK | Short term (≤ 2 years) |

| Payer-Led Outpatient Incentives for Decompression Devices | +0.5% | U.S., Canada, Germany | Short term (≤ 2 years) |

| AI-Guided Navigation Widens Surgeon Adoption Base | +0.6% | U.S., Western Europe, China, India | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Aging Population & Disease Prevalence Surge

Lumbar stenosis affects 11% of U.S. adults aged 50 plus, and prevalence rises sharply beyond age 60[1]National Institutes of Health, “Spinal Stenosis,” . Older patients prefer shorter anesthesia time, pushing cases into ASCs that demand rapid-deploy implants and streamlined workflows. Cervical stenosis, though rarer, afflicts working-age adults who favor motion-preservation to avoid adjacent-segment degeneration. The demographic swell increases baseline procedure volume regardless of technology shifts and keeps the spinal stenosis market on a steady upward trajectory.

Adoption of Minimally Invasive & Endoscopic Procedures

Endoscopic decompression techniques such as biportal endoscopic spine surgery cut muscle trauma and enable same-day discharge for lumbar cases [2]Journal of Spine Surgery, “Endoscopic Techniques,” . Vertos Medical’s percutaneous system removes hypertrophied ligamentum flavum in under 30 minutes, reinforcing ASC economics. Academic hospitals invest in robotics to draw complex referrals, while community centers rely on manual endoscopic tools that replicate most clinical gains at lower capital cost.

Implant Technology Upgrades (3D-Printing, Biomaterials)

Patient-matched 3D-printed titanium cages align precisely with endplate contours and reduce subsidence in osteoporotic bone. Trabecular lattice structures promote osseointegration and improve postoperative imaging clarity. Surgeon preference has shifted from PEEK to porous titanium and calcium phosphate graft extenders that deliver biologic fixation and minimize donor-site morbidity. Recombinant bone morphogenetic proteins plateaued after safety warnings, steering research toward novel osteobiologics.

Shift to Ambulatory Surgical Centers Boosts Device Refresh

The 2025 OPPS final rule lifted ASC spine payment rates by 2.9% and added single-level fusion and cervical artificial disc replacement to the covered list. ASCs operate at 40-60% lower cost than hospital outpatient departments, creating a fertile channel for implants designed with pre-assembled screw-rod systems, single-use kits, and fluoroscopy-friendly geometry. Boston Scientific’s Superion spacer demonstrates that ASC-optimized devices can move patients from incision to discharge in two hours.

Restraints Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Implant Costs & Reimbursement Gaps | -0.7% | Global, acute in U.S. and emerging Asia | Short term (≤ 2 years) |

| Stringent Global Regulatory Timelines | -0.4% | EU, China, India | Medium term (2-4 years) |

| Payer Push-Back on Fusion Add-Ons | -0.5% | U.S., Germany, Canada | Short term (≤ 2 years) |

| High Early-Revision Rate of Some Interspinous Devices | -0.3% | North America, Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Implant Costs & Reimbursement Gaps

Single-level lumbar fusion implants cost USD 8,000–12,000 while Medicare bundles average USD 18,000, squeezing hospital margins. Private insurers tighten approvals for expensive grafts and navigation fees, prodding surgeons toward lower-priced motion-preservation options. India’s 80% import reliance inflates prices, but its USD 50 billion domestic device policy aims to localize production and narrow affordability gaps.

Stringent Global Regulatory Timelines & High Early-Revision Rate of Interspinous Devices

EU MDR lengthens certification to 24 months and obliges costly post-market surveillance, pressuring small innovators[3]European Commission, “Medical Device Regulation,”. Early-generation interspinous spacers faced 15-20% reoperation within two years, prompting FDA post-market studies and surgeon hesitancy. The burden consolidates share toward large vendors with robust regulatory budgets.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Fusion Dominates While Motion-Preservation Accelerates

Fusion implants captured 55.32% of spinal stenosis market share in 2024, supported by multi-level PLIF and TLIF procedures that demand robust biomechanical stability. The spinal stenosis market size for fusion implants was USD 5.35 billion and is forecast to reach USD 6.67 billion by 2030 at a 3.7% CAGR. Additive manufacturing allows vendors to supply patient-specific cages on-demand, trimming operating time and inventory holding costs. Hospitals adopt expandable cages that restore disc height without extensive bone removal, reducing neurologic risk.

Motion-preservation devices are forecast to grow at 9.1% CAGR, twice as fast as the overall spinal stenosis market. Cervical disc replacements such as ProDisc-C and Mobi-C preserve range of motion and lower adjacent-segment degeneration risk, making them popular among younger patients. Interspinous spacers like Superion facilitate percutaneous lumbar decompression in less than 45 minutes and allow ASC discharge within hours. Payer pressure against fusion add-ons and a cultural shift toward tissue-sparing care underpin adoption.

By Anatomical Area: Lumbar Leads While Cervical Gains Momentum

Lumbar procedures accounted for 57.43% of spinal stenosis market size in 2024, equal to USD 5.56 billion, with stable mid-single-digit growth expected through 2030. Endoscopic lumbar decompressions cut hospital stays from three days to outpatient status, integrating seamlessly with ASC economics. Multilevel lumbar disease in older adults still necessitates fusion, ensuring fusion revenue remains substantial.

Cervical interventions are projected to expand at a 7.9% CAGR as total disc replacement mitigates the long-term complication profile of anterior cervical fusion. Younger, working-age patients value preserved mobility, and insurers see lower revision costs. FDA clearances for new cervical discs tripled from three in 2015 to eight in 2024, increasing surgeon choice and fostering price competition.

By End User: ASC Migration Reshapes Device Design

Hospitals maintained 62.12% of spinal stenosis market revenue in 2024, driven by complex deformity corrections and high-risk patients requiring overnight monitoring. Academic centers lean on navigation and robotics to boost referral flow and justify million-dollar capital spend.

ASCs are growing at an 8.4% CAGR, fueled by CMS reimbursement hikes and payer mandates for outpatient pathways. Facility operators favor pre-packaged, single-use kits that cut turnaround time and minimize sterilization overhead. Vendors now design screw-rod constructs that can be implanted in under 90 minutes, satisfying same-day discharge criteria. Specialty clinics focus on nonsurgical pain management and neuromodulation, occupying a peripheral yet stable niche in the spinal stenosis industry.

Geography Analysis

North America commanded 42% of global demand in 2024 as mature reimbursement, high elective surgery rates, and rapid technology uptake underpin demand. The spinal stenosis market size in the region will climb with continued ASC migration and subscription-based AI navigation that lowers adoption barriers for mid-volume surgeons. Payer scrutiny on fusion add-ons, however, propels a shift toward motion-preservation.

Asia-Pacific is projected to post the fastest growth at 7.2% CAGR. India’s localization push promises a USD 50 billion domestic output by 2030 and encourages price-competitive implants. China’s real-world evidence pilot in Hainan compresses approval to one year for qualified devices, accelerating Western vendor market entry while motivating local innovators. Japan’s aging population and robust national insurance add further procedural momentum.

Europe, the Middle East, and Africa exhibit mixed potential. EU MDR heightens compliance cost and slows pipeline flow, narrowing small-cap participation. Gulf Cooperation Council states invest in medical tourism, luring international patients with 40–50% lower surgery costs. Africa remains nascent, constrained by limited surgical capacity and cash-pay models, although urban centers in South Africa and Egypt present modest pockets of growth.

Competitive Landscape

The spinal stenosis market features a top-heavy profile. Medtronic, Globus Medical and Stryker emerged as major players in the industry. Stryker’s 2024 purchase of Vertos Medical added percutaneous decompression to capture ASC flow, while Orthofix–SeaSpine pooled biologics and motion-preservation expertise.

Mid-caps target niches that larger competitors under-serve. Carlsmed and EIT emerging implants exploit 3D-printing agility to supply customized cages with minimal inventory. Joimax and Richard Wolf focus on endoscopic tools that offer 80% of robotic precision at a fraction of the price. SpineGuard’s real-time haptic feedback drill democratizes safe pedicle screw placement without expensive cameras. Regulatory hurdles and ASC-centric design requirements drive consolidation as scale provides compliance leverage and R&D funding.

Start-ups with AI navigation software benefit from China’s SaMD rule that classifies algorithms as standalone products, enabling fast commercialization. Established vendors may respond through tuck-in acquisitions or licensing deals to secure data-driven features and defend platform stickiness in the spinal stenosis market.

Spinal Stenosis Industry Leaders

Medtronic plc

Johnson & Johnson

Stryker Corporation

Globus Medical, Inc.

ZimVie

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2024: Carlsmed secured FDA clearance for Aprevo Cervical ACDF Interbody System. It is a patient-specific 3D-printed titanium interbody cage platform.

- July 2024: Stryker completed the acquisition of Vertos Medical, adding percutaneous lumbar decompression tools for ASC deployment.

Global Spinal Stenosis Market Report Scope

As per the scope of the report, spinal stenosis is the narrowing of the spinal canal that puts pressure on the spinal cord and nerves, causing symptoms like pain, numbness, or weakness in the back, legs, neck, or arms. Spinal stenosis surgery aims to create more space for the spinal cord and nerves by removing bone or tissue that is causing pressure. If the spine is unstable, a spinal fusion may be combined with decompression surgery to stabilize the vertebrae.

The spinal stenosis market is segmented by product type, anatomical region, end user, and geography. By product type, the market is categorized into fusion implants, interspinous spacers, motion-preservation devices and spinal stimulators and bone growth devices. By anatomical area, it is segmented into cervical, lumbar, and thoracic. By end user, the segmentation includes hospitals, ambulatory surgical centers, and specialty clinics. Geographically, the market is segmented across North America, Europe, the Asia-Pacific region, the Middle East & Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. For each segment, the market size and forecast are provided in terms of value (USD).

| Fusion Implants |

| Interspinous Spacers |

| Motion-Preservation Devices |

| Spinal Stimulators & Bone Growth Devices |

| Cervical |

| Lumbar |

| Thoracic |

| Hospitals |

| Ambulatory Surgical Centers |

| Specialty Clinics |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Fusion Implants | |

| Interspinous Spacers | ||

| Motion-Preservation Devices | ||

| Spinal Stimulators & Bone Growth Devices | ||

| By Anatomical Area | Cervical | |

| Lumbar | ||

| Thoracic | ||

| By End User | Hospitals | |

| Ambulatory Surgical Centers | ||

| Specialty Clinics | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the spinal stenosis market in 2025?

The spinal stenosis market size stands at USD 9.67 billion in 2025.

What is the expected growth rate through 2030?

The market is forecast to expand at a 4.14% CAGR, reaching USD 12.84 billion by 2030.

Which product category is growing the fastest?

Motion-preservation devices, including cervical disc replacements and interspinous spacers, are advancing at a 9.1% CAGR.

Why are ASCs gaining share in spinal procedures?

Outpatient payment incentives, lower facility costs, and minimally invasive techniques enable same-day discharge and drive case migration.

Page last updated on: