Sphygmomanometer Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 2.93 Billion |

| Market Size (2031) | USD 4.26 Billion |

| Growth Rate (2026 - 2031) | 7.76% CAGR |

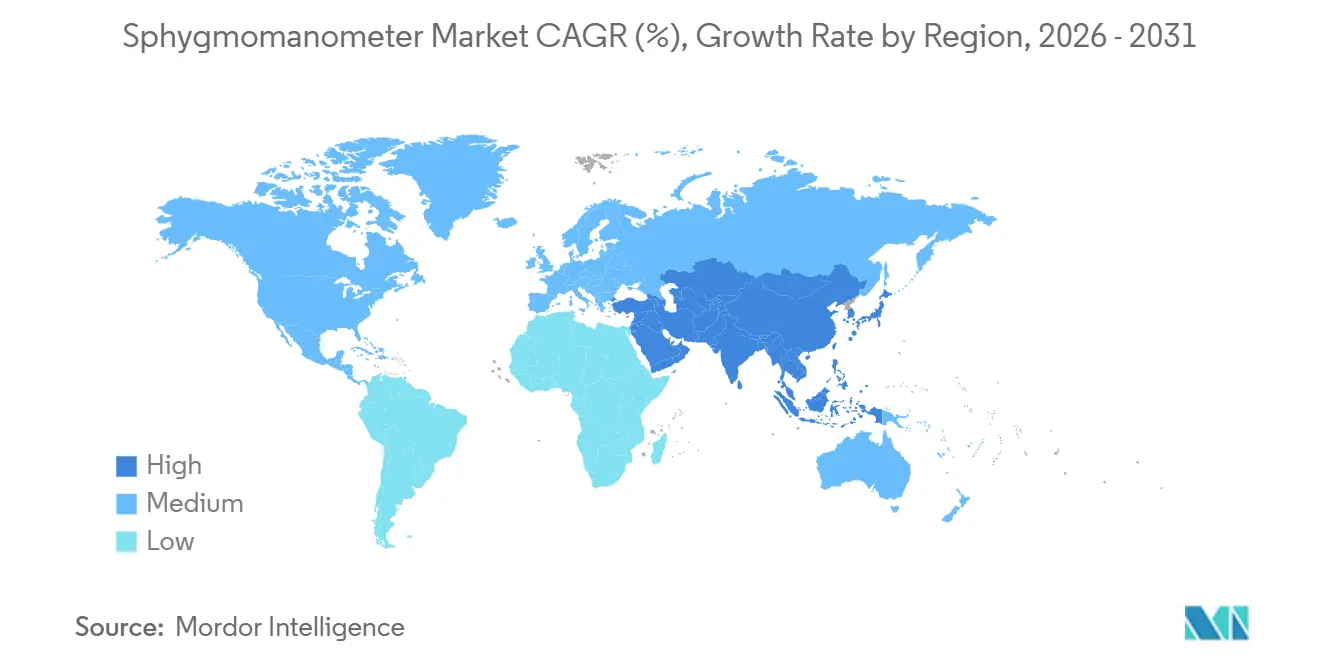

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

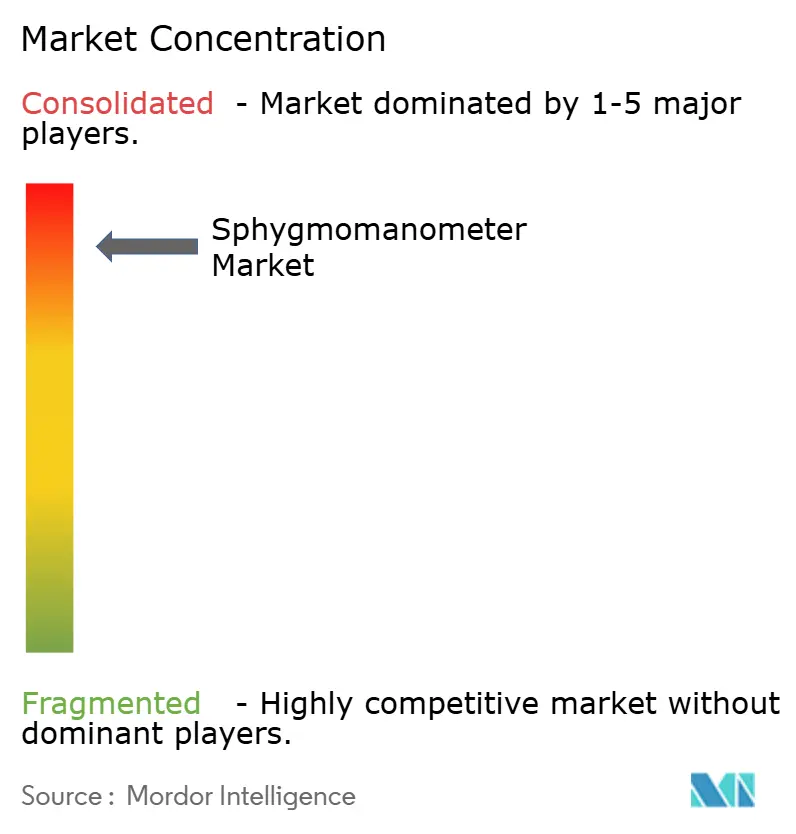

| Market Concentration | High |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Sphygmomanometer Market Analysis by Mordor Intelligence

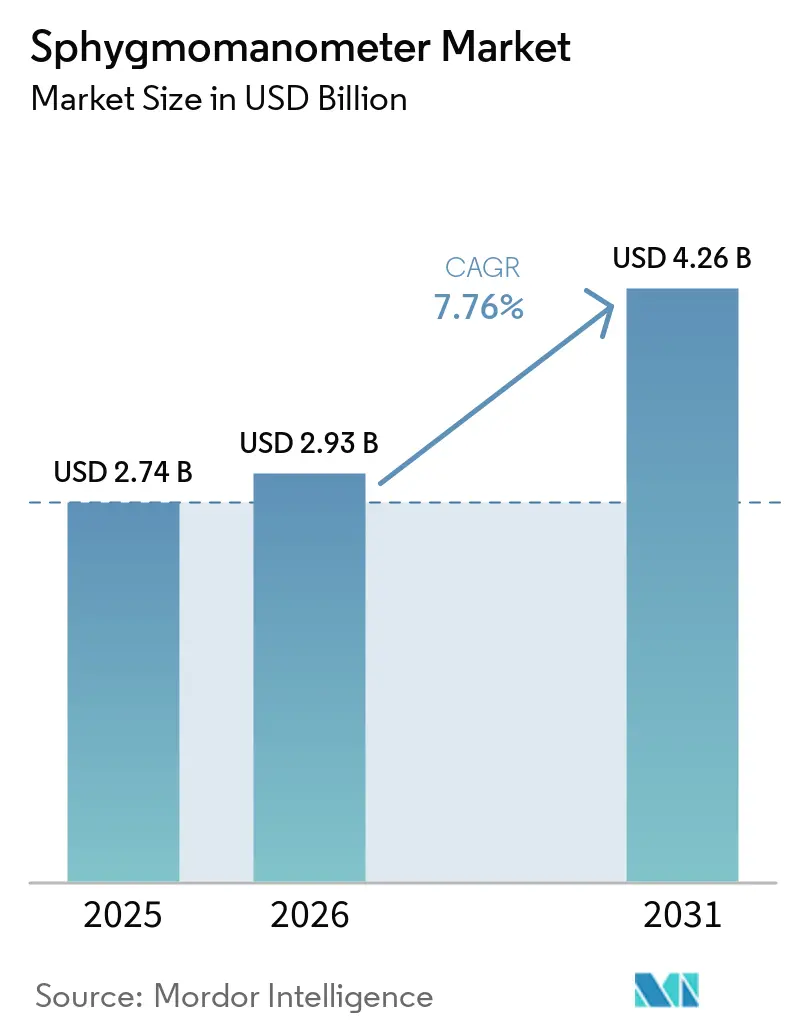

The Sphygmomanometer Market size is expected to increase from USD 2.74 billion in 2025 to USD 2.93 billion in 2026 and reach USD 4.26 billion by 2031, growing at a CAGR of 7.76% over 2026-2031.

Continuous, AI-enabled home monitoring is replacing occasional clinic-based measurements as hypertension prevalence rises, telehealth reimbursement widens, and the first Food and Drug Administration (FDA)-cleared cuffless wearables enter United States retail channels. North America dominates the market, but Asia Pacific leads in growth as payers confront cardiovascular costs and high regional hypertension prevalence. Incumbents defend share with AI upgrades and consumables bundles even as digital-native wearables such as Aktiia’s G0 attract funding and regulatory momentum.

Key Report Takeaways

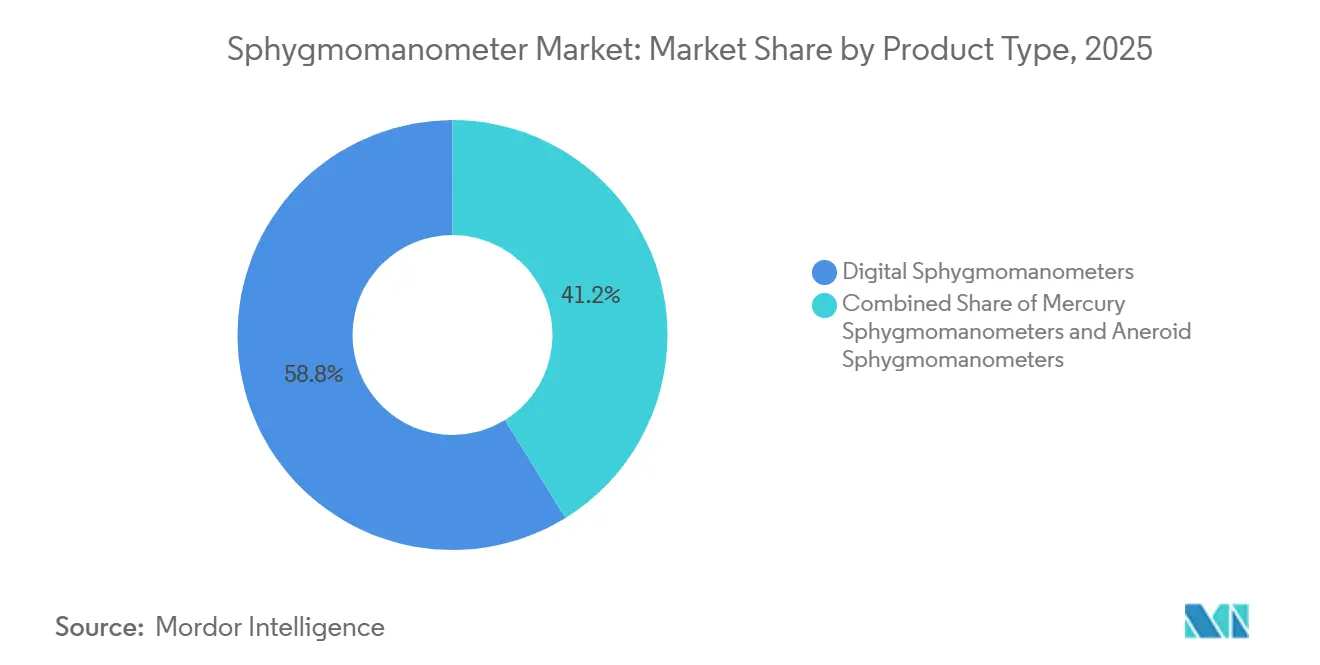

product type, digital devices led with 58.8% of the sphygmomanometer market share in 2025; wearable and cuffless formats are projected to expand at an 8.3% CAGR through 2031.

By operation, automatic monitors captured 53.45% share of the sphygmomanometer market size in 2025 and are advancing at a 7.96% CAGR through 2031.

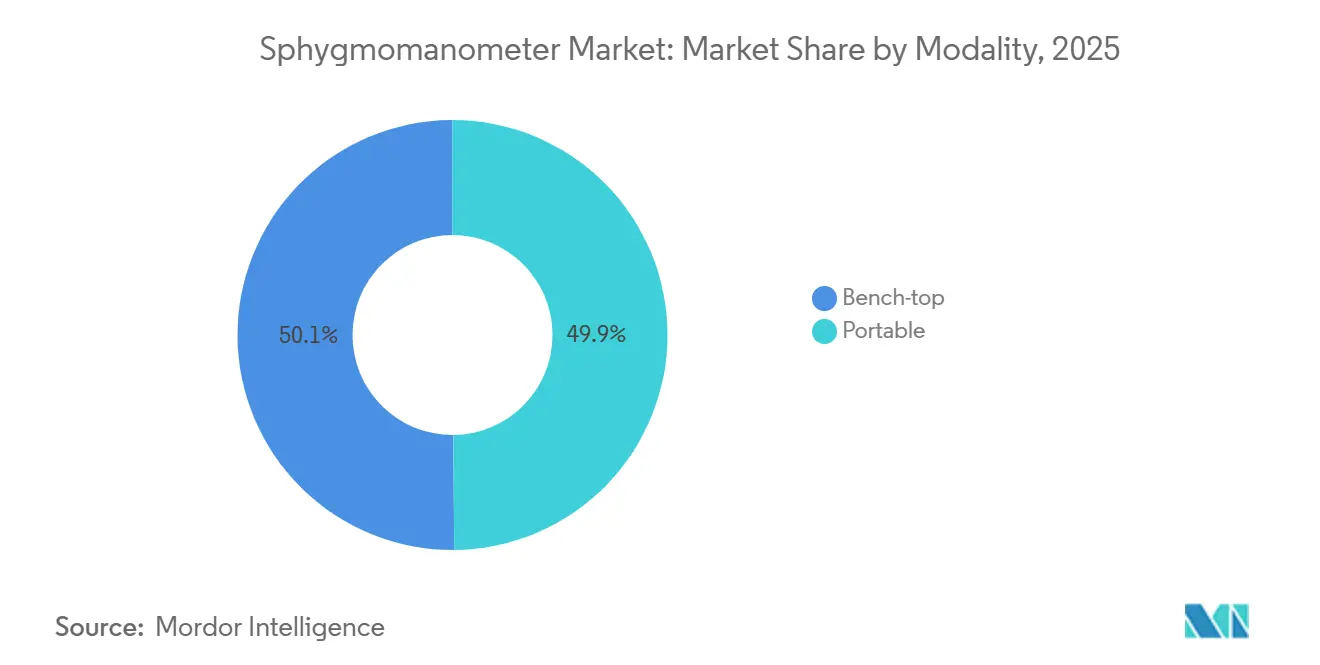

By modality, portable units accounted for 49.87% of 2025 revenue and will grow at an 8.12% CAGR, outpacing bench-top systems.

By end user, hospitals and clinics held 56.32% share in 2025, while homecare settings posted the highest projected CAGR at 8.06% to 2031.

By geography, North America dominated with 45.29% share in 2025, whereas Asia-Pacific is on track for the highest 8.24% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Sphygmomanometer Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of hypertension and cardiovascular diseases | 1.8% | Global, with peak burden in Asia Pacific (Japan 48.3%, Singapore 35.5%) and North America (~48% adults) | Long term (≥ 4 years) |

| Rapid adoption of home-based blood-pressure monitoring devices | 1.5% | North America & Europe (Medicare/telehealth reimbursement), Asia Pacific (cost-driven shift) | Medium term (2-4 years) |

| Aging global population & chronic-disease burden | 1.2% | Global, concentrated in Japan, Europe, North America | Long term (≥ 4 years) |

| Expansion of telehealth reimbursement for remote BP monitoring | 1.0% | North America (Medicare CPT 99473/99474), Europe (emerging), Asia Pacific (pilot programs) | Medium term (2-4 years) |

| AI-enabled predictive analytics in digital sphygmomanometers | 0.9% | North America, Europe, Asia Pacific (technology hubs) | Medium term (2-4 years) |

| Corporate wellness & insurance programs mandating BP tracking | 0.6% | North America, Europe, Asia Pacific (multinational employers) | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Hypertension and Cardiovascular Diseases

The World Health Organization reported that 1.4 billion adults were living with hypertension globally in 2024, while the Centers for Disease Control and Prevention documented that approximately 48% of United States adults meet diagnostic thresholds for elevated blood pressure, a prevalence that translates directly into demand for home monitoring devices as clinical guidelines shift toward frequent measurement for diagnosis confirmation and treatment titration. As per the data reported by American College of Cardiology[1]American College of Cardiology Foundation, "NHANES Data: Nearly 80% of US Adults Have HTN Above BP Goals" in February 2026, nearly 80% of United States Adults Have HTN Above BP Goals. This epidemiological trend is structural in nature rather than cyclical, supporting consistent unit demand even as average selling prices decline due to the commoditization of aneroid and entry-level digital devices.

Aging Global Population & Chronic-Disease Burden

The global population aged 65 and older is expanding at 3.1% annually, with Japan, Italy, and Germany exhibiting median ages above 45 years, demographics that correlate with hypertension incidence, which rises from approximately 30% in the 40-49 age cohort to over 70% in those aged 70 and above. This aging cohort also presents higher rates of comorbidities such as diabetes, chronic kidney disease, and atrial fibrillation, conditions that complicate blood pressure management and necessitate frequent monitoring to avoid hypotensive episodes during medication titration. The burden of chronic diseases acts as both a volume driver, bringing more patients into need of monitoring, and a driver of feature complexity, increasing demand within the sphygmomanometer market.

Rapid Adoption of Home-Based Blood-Pressure Monitoring Devices

Telehealth platforms integrated CPT 99473/99474 billing codes during 2025, trimming consumer cost-sharing that once curbed uptake by 59% in the United States studies. FDA clearance of Aktiia’s cuffless G0 system demonstrates regulatory confidence in continuous optical sensing, and wearable comfort drives weekly readings far beyond clinic frequency. Independent validation sites list an expanding roster of upper-arm models, increasing physician trust. Together, reimbursement certainty, patient convenience, and clinical endorsement shift measurement decisively into the home.

Expansion of Telehealth Reimbursement for Remote BP Monitoring

The expansion of telehealth reimbursement is a key driver in the sphygmomanometer market, as it encourages wider adoption of remote blood pressure (BP) monitoring devices. When insurers and government programs cover virtual care and home-based monitoring, patients are more likely to use digital or connected sphygmomanometers. For example, in the United States, Centers for Medicare & Medicaid Services expanded reimbursement for remote patient monitoring (RPM) services, enabling providers to bill for at-home BP tracking. This policy shift has accelerated demand for clinically validated, Bluetooth-enabled BP monitors. As a result, manufacturers are increasingly innovating to meet the growing need for telehealth-compatible devices.

Restraints Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accuracy concerns & lack of device validation standards | -0.8% | Global, with heightened scrutiny in Europe (MDR), North America (FDA 510(k)), Asia Pacific (NMPA, PMDA) | Medium term (2-4 years) |

| Stringent multi-region regulatory approval timelines | -0.6% | Global, with longest timelines in Europe (MDR transition), China (NMPA), Japan (PMDA) | Medium term (2-4 years) |

| Data-privacy & cybersecurity risks in connected devices | -0.5% | North America & Europe (GDPR, FDA Section 524B), Asia Pacific (emerging frameworks) | Short term (≤ 2 years) |

| Supply-chain disruptions for critical electronic components | -0.4% | Global, with acute impact in Asia Pacific (semiconductor sourcing), Europe, North America | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Accuracy Concerns & Lack of Device Validation Standards

Accuracy concerns and lack of standardized validation protocols remain a significant restraint in the sphygmomanometer market. As per the data published in Digital Health[2]Long-term accuracy and stability of blood pressure measurements from a smartwatch: Prospective validation study in January 2026, a study conducted by the Ethics Committee of the Faculty of Biomedical Engineering of the Czech Technical University in Prague on May 15, 2023, shows that many commercially available devices lack proper clinical validation, with over 500 cuffless devices reported without standardized accuracy verification. As per the article published in Hypertension[3]Abstract P317: Are Home Blood Pressure Devices Accurate? A Systematic Review of the Evidence in October 2024, a literature search of MEDLINE and EMBASE from 1946 and 1947, respectively, through April 2023, stated that discrepancies of 10%–72% in systolic readings have been observed between home monitors and mercury sphygmomanometers, the clinical gold standard. These inconsistencies, coupled with limited adherence to global validation standards, continue to hinder device reliability and market adoption.

Stringent Multi-Region Regulatory Approval Timelines

European Union Medical Device Regulation recertification backlogs delay launches 12-24 months; Microlife certified 222 SKUs by 2023, diverting research and development resources. China’s 2024 guidance adds clinical-trial demands, and Japan’s Pharmaceuticals and Medical Devices Agency took 24 months to clear Tanita’s BP-225. Meanwhile, FDA Section 524B cybersecurity rules require Software Bills of Materials, raising compliance overhead for connected devices. Staggered rules fragment global rollouts and slow revenue recognition.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Digital Devices Extend Leadership

Digital models dominated in 2025, accounting for 58.8% of the sphygmomanometer market share as mercury options receded under environmental bans. Manufacturers such as Omron are expanding digital sphygmomanometer ecosystems by integrating connected BP monitors, mobile applications, and remote patient monitoring services, enabling improved hypertension management and real-time clinician oversight. At the same time, AI-enabled hypertension management is gaining momentum, with devices increasingly incorporating algorithms for AFib detection and cardiovascular risk assessment during routine blood pressure measurements. This shift toward predictive and preventive care is enhancing the clinical value of home BP monitoring devices beyond traditional readings. For instance, in October 2025, Omron Healthcare was recognized by the Digital Health Hub Foundation’s 2025 Digital Health Awards as Best in Class in Home Health Diagnostics & Monitoring for its AI-powered AFib-detecting BP monitors.

By Operation: Automatic Monitors Prevail

Automatic units held 53.45% share in 2025, due to automated cuff inflation during measurement cycles that shorten procedure time and reduce discomfort. The sphygmomanometer market size for automatic devices is forecast to expand at 7.96% CAGR to 2031. Beurer’s BM 48 checks cuff position before inflation, aborting errors that once generated false alarms. Semi-automatic monitors survive mainly in price-sensitive markets but now claim below 10% unit share, while manual auscultatory kits remain niche for arrhythmia or pediatric use.

By Modality: Portable Gains Momentum

Portable formats secured 49.87% revenue in 2025 and are growing at 8.12% CAGR as hoseless, battery-powered units replace cart-mounted monitors. NFC and Bluetooth pairings simplify data transfer to cloud dashboards, pivotal to reimbursement workflows. Bench-top models remain embedded in high-acuity wards where continuous vital-sign integration matters, yet ASCs and community clinics increasingly choose portable kits to save space and cost. Wearable devices enhance portability by enabling continuous, passive monitoring, enabling 24-hour capture without user action. Consequently, variability analytics emerge as a service layer, opening subscription income for manufacturers.

By End User: Homecare Outpaces Institutional Buyers

Hospitals and clinics still account for 56.32% of 2025 demand, but budget priorities are shifting toward consumables. Nihon Kohden[4]Nihon Koden Corporation, "Consolidated Financial Highlights for the First Quarter of FY2025" expects consumables to reach 50% of business by 2026, reducing reliance on episodic capital sales. Homecare devices are projected to grow at an 8.06% CAGR, driven by reimbursement support through remote patient monitoring (RPM) billing codes and employer-sponsored wellness programs that subsidize monitors for insured populations. Meanwhile, ambulatory surgical centers (ASCs) and community health centers are increasingly adopting portable, low-maintenance solutions. This shift is further reinforced by Medicare’s site-neutral payment policies, which incentivize the migration of procedures from hospital settings to lower-cost outpatient and community-based care environments.

Geography Analysis

The increasing prevalence of cardiovascular and lifestyle-related diseases across major regions is emerging as a key public health concern, significantly influencing the demand for diagnostic and monitoring devices such as sphygmomanometers. Heart disease and stroke are affecting a significantly larger population than previously estimated, with about 6 million people living with these conditions in Canada alone, according to Heart & Stroke’s latest Heart Month report. This reflects a growing cardiovascular burden across North America, driven by aging populations and lifestyle risk factors such as hypertension and obesity. The rising prevalence is increasing the demand for regular blood pressure monitoring and preventive care.

A recent nationwide survey by the National Statistics Office reported in The India Practitioner[5]Lifestyle Diseases Surge in India as Cardiometabolic Burden Nearly Doubles in April 2026 in India highlights a sharp increase in lifestyle-related diseases, with nearly half the population now reporting cardiovascular and metabolic conditions such as hypertension, heart disease, and diabetes. Cardiovascular ailments rose from 16.7% in 2017–18 to 25.6% in 2025, while metabolic and endocrine disorders also showed a marked increase. This rapid escalation across the Asia Pacific region underscores a strong need for improved screening and monitoring of blood pressure and related health conditions.

Overall, the rising burden of cardiovascular and metabolic disorders in both North America and Asia Pacific is expected to drive sustained growth in the sphygmomanometer market, as early diagnosis and regular blood pressure monitoring become increasingly critical for disease management and prevention.

Competitive Landscape

The global sphygmomanometer market is moderately consolidated and highly competitive, with a few dominant multinational players shaping innovation and pricing dynamics. Companies such as Omron Healthcare and A&D Company collectively hold a significant share of the market, leveraging strong brand recognition, wide distribution networks, and leadership in digital blood pressure monitoring technologies. Other major competitors, including Welch Allyn, Philips Healthcare, GE Healthcare, Microlife Corporation, and SunTech Medical, compete through product accuracy, clinical-grade reliability, and expanding portfolios of connected and automated devices.

The competitive landscape is further intensified by strong regional manufacturers such as Yuwell and Andon in Asia-Pacific, which focus on cost-effective solutions for price-sensitive markets. Overall, competition is driven by rapid digitalization, integration with remote health platforms, and continuous innovation in connectivity, accuracy, and user-friendly designs, as companies seek to capture growing demand across both clinical and home-care segments.

Sphygmomanometer Industry Leaders

-

A&D Company, Limited

-

Hillrom / Welch Allyn

-

Mindray Bio-Medical Electronics Co., Ltd.

-

Nihon Kohden Corporation

-

Omron Healthcare Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Omron integrated its monitors with Tricog Health’s CardioCheck, streaming readings from 3,000+ Indian sites

- November 2025: Omron deepened investment in Tricog Health to cement corporate-wellness partnerships across Asia.

Global Sphygmomanometer Market Report Scope

As per the scope of the report, a sphygmomanometer is a medical instrument used to measure blood pressure, typically consisting of an inflatable cuff, a measuring gauge (aneroid or mercury), and a bulb for inflation.

The sphygmomanometer market is segmented by product type, operation, modality, end user, and geography. Based on product type, the market is segmented into mercury sphygmomanometers, aneroid sphygmomanometers, and digital sphygmomanometers. Digital sphygmomanometers are further bifurcated into standard upper-arm digital, wrist digital, wearable / cuff-less. By operation, the market is segmented into manual, automatic, and semi-automatic. By modality, the market is segmented into portable and bench-top. By end user, the market is segmented into hospitals & clinics, homecare settings, ambulatory surgical centers, community health centers & others. Geographically, the market is segmented into North America, Europe, Asia-Pacific, the Middle East & Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. For each segment, the market size and forecast are provided in terms of value (USD).

| Mercury Sphygmomanometers | |

| Aneroid Sphygmomanometers | |

| Digital Sphygmomanometers | Standard Upper-Arm Digital |

| Wrist Digital | |

| Wearable / Cuff-less |

| Manual |

| Automatic |

| Semi-automatic |

| Portable |

| Bench-top |

| Hospitals & Clinics |

| Homecare Settings |

| Ambulatory Surgical Centers |

| Community Health Centers & Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Mercury Sphygmomanometers | |

| Aneroid Sphygmomanometers | ||

| Digital Sphygmomanometers | Standard Upper-Arm Digital | |

| Wrist Digital | ||

| Wearable / Cuff-less | ||

| By Operation | Manual | |

| Automatic | ||

| Semi-automatic | ||

| By Modality | Portable | |

| Bench-top | ||

| By End User | Hospitals & Clinics | |

| Homecare Settings | ||

| Ambulatory Surgical Centers | ||

| Community Health Centers & Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the sphygmomanometer market?

The sphygmomanometer market size stands at USD 2.93 billion in 2026 and is projected to reach USD 4.26 billion by 2031, reflecting a 7.8% CAGR.

Which product category leads sales?

Digital sphygmomanometers command 58.8% of revenue, driven by oscillometric accuracy and AI features that outpace aneroid and mercury options.

Which region offers the highest growth potential?

Asia Pacific posts the fastest CAGR at 8.24% through 2031 because of hypertension prevalence up to 48.3% and payer incentives for preventive monitoring

What technologies are disrupting traditional cuffs?

Cuffless wearables using photoplethysmography, such as Aktiia’s G0, received FDA clearance in 2025 and exemplify the shift toward continuous optical sensing.

Page last updated on: