Speech-to-Text API Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 2.87 Billion |

| Market Size (2031) | USD 7.21 Billion |

| Growth Rate (2026 - 2031) | 20.23% CAGR |

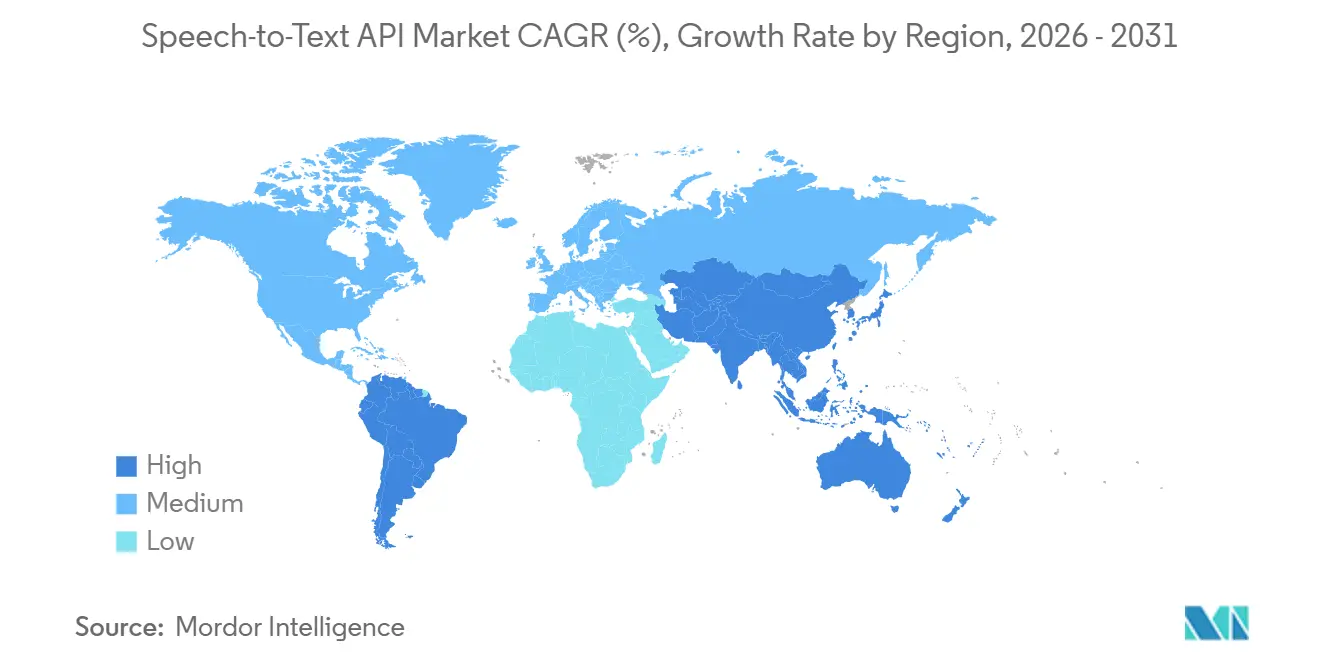

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

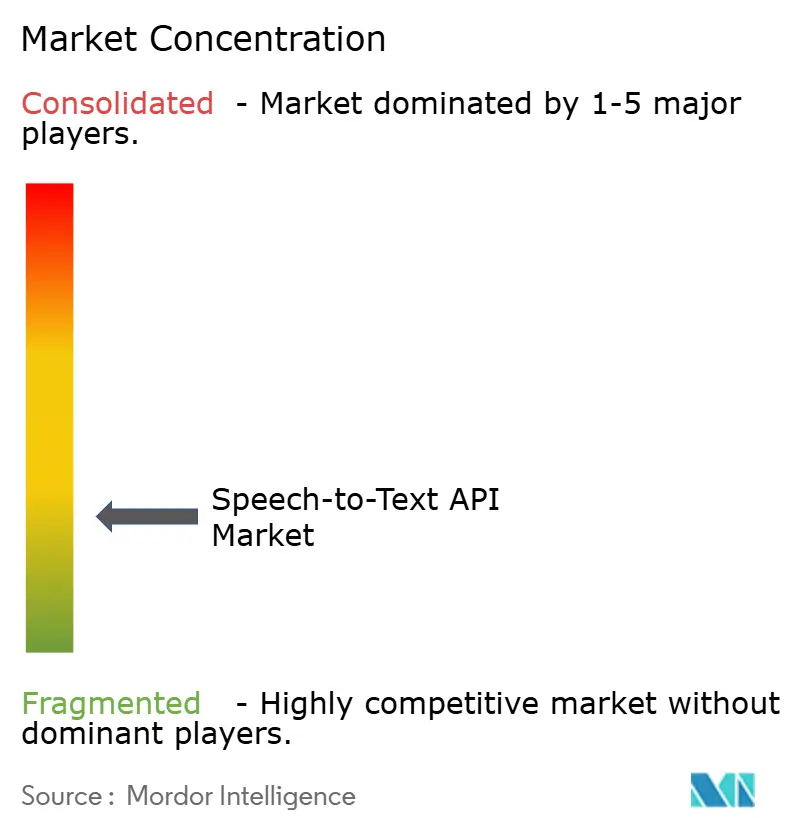

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Speech-to-Text API Market Analysis by Mordor Intelligence

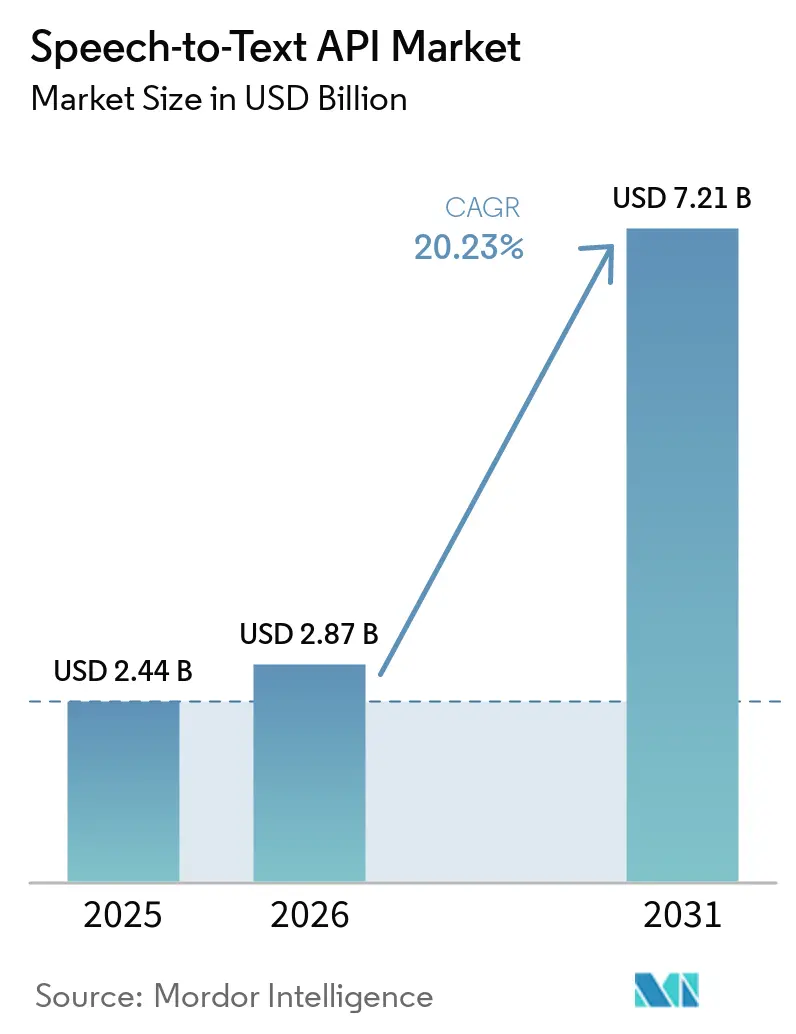

The speech-to-text API market size was valued at USD 2.44 billion in 2025 and estimated to grow from USD 2.87 billion in 2026 to reach USD 7.21 billion by 2031, at a CAGR of 20.23% during the forecast period (2026-2031). The core shift behind this expansion is the role of speech-to-text APIs as the input layer for agentic AI systems, where downstream reasoning, automation, and response quality depend on fast and accurate audio capture. The speech-to-text API market is also benefiting from stronger enterprise spending on conversational AI, broader production use of voice agents, and rising demand for real-time transcription in meetings, service workflows, and customer interactions. Competitive pressure is moving beyond standalone transcription because vendors are increasingly packaging speech recognition, reasoning, and text-to-speech into unified voice stacks that can reshape pricing and contract structure in the speech-to-text API market. At the same time, buyers are placing greater weight on latency, multilingual support, deployment control, and compliance readiness, which is changing vendor selection criteria across the speech-to-text API market. These conditions continue to create room for growth, but they also raise the bar for providers that need to prove reliability in regulated settings, noisy environments, and large-scale enterprise deployments.

Key Report Takeaways

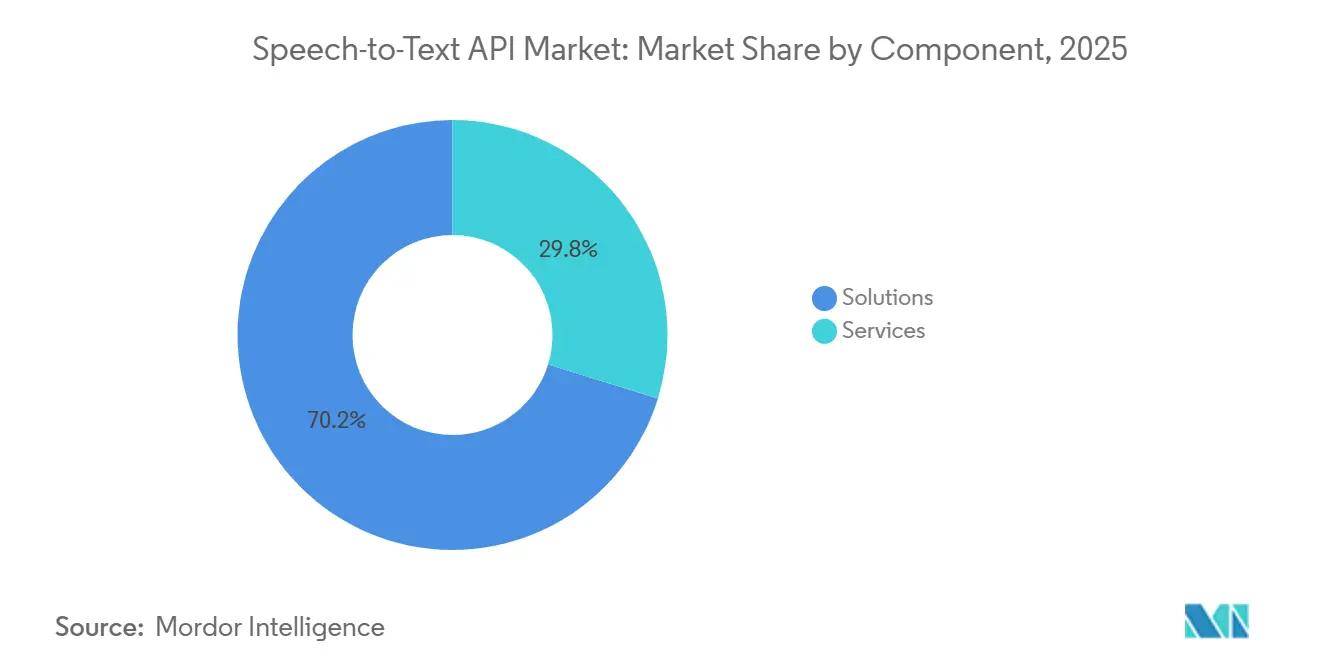

- By component, solutions held 70.23% of the revenue of the speech-to-text API market in 2025, while services are projected to expand at a 21.78% CAGR through 2031.

- By deployment model, cloud-based deployment captured 59.11% of revenue of the speech-to-text API market in 2025, while hybrid and sovereign cloud are projected to advance at a 22.43% CAGR through 2031.

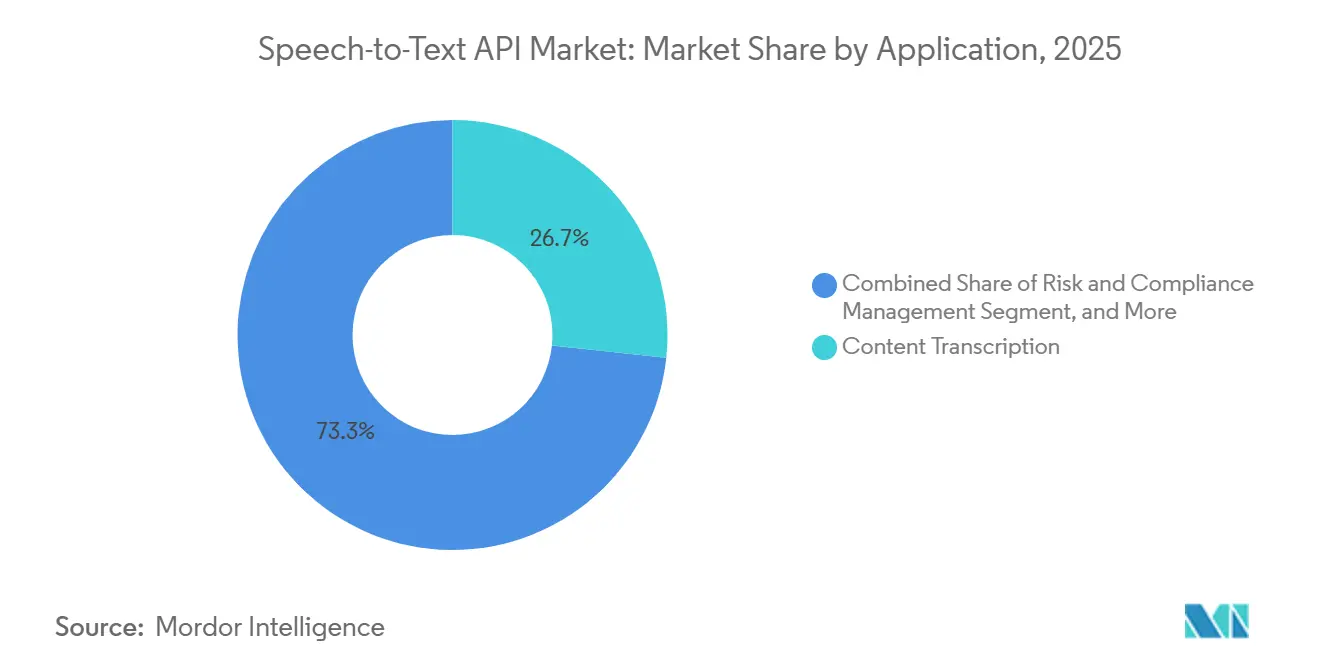

- By application, content transcription accounted for 26.68% share of the speech-to-text API market size in 2025, while voice-enabled workflow automation and note generation are projected to expand at a 22.78% CAGR through 2031.

- By end-user industry, IT and telecommunications held 18.88% of revenue in 2025, while healthcare and life sciences are projected to record the highest CAGR at 23.71% through 2031.

- By organization size, large enterprises held 51.91% of the revenue of the speech-to-text API market in 2025, while small and medium-sized enterprises are projected to grow at a 21.98% CAGR through 2031.

- By geography, North America held 32.44% of the speech-to-text API market share in 2025, while Asia-Pacific is projected to expand at a 22.66% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Speech-to-Text API Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Enterprise Adoption Of Conversational AI And Voice Agents | +4.8% | Global, strongest pull in North America and Western Europe | Short term (≤ 2 years) |

| Growing Need For Real-Time Transcription In Contact Centers And Meetings | +3.9% | Global, concentrated in North America, EU, APAC core, India, Australia, Japan | Short term (≤ 2 years) |

| Sub-300 Millisecond Latency Requirements For Production Voice Agents | +3.2% | Global, early-adopter concentration in North America and EU | Medium term (2-4 years) |

| Expansion Of Multilingual And Domain-Tuned Speech Models | +2.8% | APAC core, Middle East and Africa, South America, with spillover to EU multilingual deployments | Medium term (2-4 years) |

| Accessibility And Captioning Compliance Across Digital Media | +2% | North America and EU, with early-stage adoption in APAC | Short term (≤ 2 years) |

| Sovereign Cloud And Regional Data Residency Options Unlocking Regulated Demand | +1.6% | EU, Middle East and Africa, India, Australia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Enterprise Adoption Of Conversational AI And Voice Agents

Enterprise spending has moved beyond experimentation, and that change is directly supporting the speech-to-text API market. A February 2026 survey by Rasa found that 67% of enterprise decision-makers were actively expanding or scaling conversational AI programs across sectors such as finance, healthcare, retail, government, and telecom, which points to faster production rollout cycles for voice-enabled systems.[1]Rasa, “2026 State of Conversational AI Report,” Rasa, rasa.com The same report also cited McKinsey data showing that 88% of enterprises regularly used generative AI for at least 1 business function, up 10 percentage points year over year, which supports a broader software budget shift toward AI-enabled workflows. Within that transition, voice agents are becoming a standard deployment pattern because speech recognition is the starting point for routing, summarization, and action-taking systems in the speech-to-text API market. This also increases switching costs because an enterprise that standardizes on a single speech layer often extends that choice across orchestration, monitoring, and compliance workflows in the speech-to-text API market. The Deepgram and IBM partnership announced in February 2026 shows how providers are seeking durable distribution by embedding speech capabilities directly inside enterprise agent platforms rather than selling transcription as a separate utility.

Growing Need For Real-Time Transcription In Contact Centers And Meetings

The speech-to-text API market is also growing because real-time transcription is becoming a core operating tool in contact centers and enterprise meetings. Buyers are no longer focused only on retrospective call review, because live transcription supports agent guidance, automated quality checks, compliance monitoring, and post-call summarization while the interaction is still active. This shift matters because real-time processing changes the commercial value of transcription from a back-office record to a live workflow control layer within the speech-to-text API market. Meeting workflows are evolving in the same direction, where transcription is being used to build searchable organizational memory rather than simple meeting notes. Otter.ai’s April 2026 launch of its Conversational Knowledge Engine shows how speech data is being turned into a structured enterprise context that can connect with other workplace tools and expand the value of each recorded interaction. As a result, vendors that lack real-time streaming performance are losing ground in the speech-to-text API market because enterprise request processes increasingly treat low-latency transcription as a baseline requirement rather than an advanced feature.

Sub-300 Millisecond Latency Requirements For Production Voice Agents

Latency has become one of the clearest technical filters in the speech-to-text API market because voice systems need near-instant response to feel usable in real conversations. If transcription arrives too slowly, the rest of the voice stack also slows down, which makes customer service, call routing, and automated assistance feel unnatural. This is why the speech-to-text API market is shifting toward models and infrastructure that can deliver streaming output with very low delay, even when accuracy remains high in difficult conditions. AssemblyAI’s Universal-3 Pro Streaming, launched in May 2026, was positioned around sub-200-millisecond end-to-end latency with an 8.14% word error rate across English, which shows how vendors are competing on speed and recognition quality at the same time. Microsoft also highlighted model efficiency and multilingual accuracy in its April 2026 introduction of MAI-Transcribe-1, showing that major platforms are improving both performance and throughput as deployment scale rises.[2]Microsoft AI, “State-of-the-Art Speech Recognition With MAI-Transcribe-1,” Microsoft AI, microsoft.ai The result is a speech-to-text API market where vendors without purpose-built streaming architectures face limits on their ability to win real-time production contracts.

Expansion Of Multilingual And Domain-Tuned Speech Models

Multilingual coverage is moving from a premium feature to a baseline buying criterion in the speech-to-text API market. Global enterprises need speech systems that can handle multiple languages, accents, and mixed-language speech across customer service, government, and internal communication workflows. Deepgram’s April 2026 launch of Flux Multilingual, with automatic language detection and real-time code-switching across 10 languages, reflects how commercial vendors are responding to that demand in the speech-to-text API market. On the research side, NVIDIA’s Canary-1B-v2 showed that efficient multilingual speech recognition across 25 languages can also support edge and private deployment scenarios, which broadens the addressable set of workloads beyond public cloud inference.[3]arXiv, “Canary-1B-v2 and Parakeet-TDT-0.6B-v3, Efficient and High-Performance Models for Multilingual ASR and AST,” arXiv, arxiv.org Domain-specific tuning is developing in parallel because general models still struggle with medical, regulatory, or region-specific vocabulary, and that opens room for specialized providers in the speech-to-text API market. This is especially relevant in Arabic and other less-standardized commercial environments, where local players can still compete effectively by offering language coverage and deployment choices that global providers do not consistently match.

Restraint Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accuracy Degradation Across Accents, Code-Switching, Noise, And Cross-Talk | -2.0% | Global, most severe in Africa, South Asia, Middle East, Southeast Asia | Long term (≥ 4 years) |

| Voice Data Privacy, Security, And Compliance Burdens | -1.7% | EU, US, and global regulated sectors | Medium term (2-4 years) |

| EU AI Act Limits On Emotion Inference Reducing Speech Analytics Upside | -1.1% | EU, with precedent effects for the UK and APAC regulated markets | Long term (≥ 4 years) |

| GPU And AI Infrastructure Cost Volatility Pressuring API Pricing | -0.8% | Global, most acute for pure-play API providers without captive compute | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Accuracy Degradation Across Accents, Code-Switching, Noise, And Cross-Talk

Accuracy gaps remain a real limit on the speech-to-text API market, especially outside clean English audio conditions. Research presented in the 2026 EACL proceedings through the AfriVox benchmark showed that word error rates rose sharply on accent-diverse evaluation sets, including Indian and African accented English, which confirms that production performance can diverge meaningfully from vendor benchmark claims. Code-switching adds another layer of difficulty, and arXiv research on Mandarin-English mixed speech showed that Whisper-family models could still post mixed error rates above 60% on benchmark tasks even when they performed well on monolingual audio. For enterprises in India, Southeast Asia, the Middle East, and Africa, this means the speech-to-text API market still carries execution risk whenever real traffic contains non-standard accents, overlapping speakers, or mid-sentence language changes. These gaps often force buyers to add human review, post-processing layers, or narrower deployment scopes, which weakens the cost-efficiency case for large-scale rollout in the speech-to-text API market. Until multilingual and accent-robust performance improves more consistently, this restraint will continue to shape vendor evaluation and buyer confidence.

Voice Data Privacy, Security, And Compliance Burdens

Compliance remains a major friction point in the speech-to-text API market because voice data often contains personal, sensitive, or regulated information. Procurement teams in healthcare, financial services, government, and enterprise collaboration environments need clarity on processing location, retention, deletion, subcontractors, and audit controls before deployment can move forward. That requirement slows onboarding because the speech-to-text API market is not only selling model accuracy, it is also selling trust, documentation, and operating discipline. This is one reason sovereign and private deployment options are gaining importance, as large cloud providers have continued expanding region-controlled infrastructure for regulated workloads in Europe and other sensitive jurisdictions. Healthcare use cases face an additional hurdle because buyers expect formal contractual protection around patient information, which raises the bar for vendors seeking to scale in that part of the speech-to-text API market. As compliance expectations tighten, providers without strong audit credentials, deployment flexibility, and transparent data handling processes are likely to face longer sales cycles and narrower contract access.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Solutions Lead Revenue While Services Scale With Complexity

Solutions held 70.23% of revenue in 2025, which shows that model inference APIs, SDK licensing, and platform subscriptions remained the primary commercial engine of the speech-to-text API market. This dominance reflects where most buyer budgets still sit, because enterprises first purchase access to recognition models, streaming endpoints, and core platform features before they expand into deeper implementation work. The solutions layer also benefits from repeat usage because every production workload, whether in meetings, contact centers, or workflow automation, generates recurring API consumption inside the speech-to-text API market. Microsoft’s April 2026 launch of MAI-Transcribe-1 reinforced that point by highlighting lower average word error rates across 25 languages, lower hourly pricing, and faster batch speed than the earlier Azure Fast approach, which improves the economics of high-volume transcription workloads. As model efficiency improves, providers can push lower unit pricing while expanding the number of use cases that remain commercially attractive in the speech-to-text API market.

Services are projected to expand at a 21.78% CAGR through 2031, which indicates that enterprise complexity is increasing even as core APIs become easier to access. The growth is tied to regulated deployments, domain tuning, uptime commitments, compliance documentation, and architecture support, all of which extend beyond basic API provisioning. In practice, many buyers need a service wrapper around the technology because production deployment often includes vocabulary adaptation, security configuration, workflow integration, and governance design. Speechmatics’ January 2026 partnership with Sully.ai for healthcare-focused autonomous scribing illustrates how managed services can sit on top of a speech engine to deliver clinical workflows with different deployment modes, including on-premises and private cloud options. This means the speech-to-text API industry is not shifting away from solutions, but it is attaching more service value to deployments where the cost of failure is high.

By Deployment Model: Cloud Leads While Hybrid And Sovereign Options Gain Ground

Cloud-based deployment captured 59.11% of revenue in 2025, and that lead reflects the ease of integration, usage-based billing, and developer accessibility that helped scale the speech-to-text API market. Public cloud remains the simplest entry point for buyers who want fast deployment without building their own speech infrastructure. It also supports experimentation at lower commitment levels, which has been important for product teams and digital businesses entering the speech-to-text API market. Even so, hybrid and sovereign cloud is projected to grow at a faster 22.43% CAGR through 2031, which shows that deployment preference is shifting as production use expands. Rasa’s 2026 enterprise survey found that 63% of AI leaders preferred hybrid architectures, while only 17% preferred fully cloud-based deployment, which aligns with stronger buyer demand for control over sensitive workloads.

On-premises and private cloud remain strategically important wherever data localization, internal security policy, or sector regulation limits the use of shared infrastructure. In those settings, the deployment model becomes part of the buying decision rather than a post-sale technical detail in the speech-to-text API market. Microsoft’s sovereign cloud expansion in Europe and AWS’s European Sovereign Cloud initiative show that infrastructure providers are investing to unlock demand from government and critical sectors that could not easily adopt public cloud speech services before. That trend supports a broader shift in the speech-to-text API market, where cloud scale still matters, but ownership of deployment flexibility is becoming a stronger competitive differentiator. As compliance scrutiny increases, vendors that can serve public cloud, hybrid, and private environments are likely to stay better positioned across regulated verticals.

By Organization Size: Enterprises Supply Revenue Depth While SMEs Lift Usage Growth

Large enterprises held 51.91% of revenue in 2025, which shows that multi-seat contracts, large call volumes, and formal service requirements still anchor the speech-to-text API market. These buyers often need speaker diarization, multi-channel audio handling, custom vocabulary, audit logs, and guaranteed support, which pushes spending toward vendors with mature platforms and delivery teams. The size of these deployments also makes enterprises important for revenue visibility because usage is tied to ongoing business processes rather than short-term experimentation. Rasa’s 2026 report, which referenced McKinsey data showing regular enterprise use of generative AI across business functions, supports the view that large organizations are continuing to move AI tools into day-to-day operations. In the speech-to-text API market, that usually translates into deeper integration with service desks, meeting systems, analytics layers, and compliance workflows.

Small and medium-sized enterprises are projected to expand at a 21.98% CAGR through 2031, and that growth reflects a lower barrier to entry in the speech-to-text API market. Consumption-based pricing, self-serve onboarding, and developer-friendly documentation have made it easier for smaller firms to test and deploy speech features without large upfront commitments. AssemblyAI’s developer-oriented access model, including credits highlighted in its 2026 recap, supports this wider pool of experimentation and early production work. Even so, SME growth is not purely a demand story because open-source options are improving and can cap long-term hosted API spending at certain volumes. This creates a mixed picture for the speech-to-text API market, where smaller customers increase usage breadth, but providers still need to prove enough performance, convenience, and governance value to keep those customers from self-hosting as workloads scale.

By Application: Content Transcription Holds The Lead While Workflow Automation Gains Strategic Weight

Content transcription held 26.68% of application revenue in 2025, which keeps it as the largest use case in the speech-to-text API market. The category remains large because it is already embedded in media production, legal discovery, podcast workflows, archived communications, and captioning processes that require dependable conversion from speech to text. Its scale comes from workflow depth and steady usage volume rather than premium pricing, which means it is important but also more exposed to commoditization pressure inside the speech-to-text API market. Google Cloud’s November 2025 general availability release for Chirp 3, with speaker diarization, automatic language detection, speech adaptation, and denoising, shows how platform vendors continue to strengthen the core transcription stack for multilingual and production-grade workloads. Accessibility requirements also support this segment because captioning demand extends beyond media companies into public, education, and enterprise communication settings.

Voice-enabled workflow automation and note generation is projected to expand at a 22.78% CAGR through 2031, making it the fastest-growing application area in the speech-to-text API market. This segment matters because transcription is no longer treated as the end product, and instead becomes the trigger for summaries, CRM updates, compliance flags, scheduling actions, and structured note creation. In that model, the value of speech recognition rises because it feeds operational systems rather than producing a static transcript. Otter.ai’s April 2026 launch of its Conversational Knowledge Engine illustrates how vendors are trying to turn spoken interactions into searchable organizational knowledge and connected work outputs. The speech-to-text API market is therefore moving toward applications where language capture, context extraction, and next-step automation sit in the same workflow, which raises the strategic importance of real-time performance and integration quality.

By End-User Industry: IT And Telecom Leads While Healthcare Builds The Fastest Momentum

IT and telecommunications held 18.88% of revenue in 2025, which reflects the sector’s role as both a direct buyer and an infrastructure enabler for the speech-to-text API market. Technology vendors, service providers, communications platforms, and telecom operators all deploy speech recognition in customer service, internal tools, and product development. This creates concentrated spending because the same organizations that build or resell digital services also consume speech APIs across their own operations. Their requirements often center on scale, uptime, integration depth, and multilingual handling, which makes them important reference buyers in the speech-to-text API market. The segment’s position also matters strategically because these buyers influence downstream adoption through the products and platforms they expose to enterprise users.

Healthcare and life sciences is projected to expand at a 23.71% CAGR through 2031, making it the fastest-growing end-user segment in the speech-to-text API market. Growth is being driven by ambient scribing, clinical documentation automation, and patient intake workflows, where voice capture directly reduces administrative burden and helps structure records. Speechmatics and Sully.ai highlighted this direction in January 2026 through a healthcare-focused partnership built around autonomous agents and clinical scribing workflows. The same announcement noted strong medical-model performance on accuracy and medical keyword recall, which reinforces that clinical use depends more on domain precision than on generic benchmark scores. BFSI, government, education, media, retail, and travel remain relevant parts of the speech-to-text API industry, but healthcare is where compliance, workflow value, and measurable productivity gains are currently combining most clearly.

Geography Analysis

North America held 32.44% of global revenue in 2025, giving it the largest regional position in the speech-to-text API market. The region benefits from a dense concentration of API providers, enterprise software buyers, healthcare technology adoption, and early production deployment of AI-enabled communication tools. Pricing competition is especially visible here because major vendors launched new voice models and streaming products in quick succession, which increased buyer choice and margin pressure at the same time. OpenAI’s May 2026 release of GPT-Realtime-Whisper at USD 0.017 per minute added to that pricing pressure and showed how bundled voice offerings are influencing buyer expectations in the speech-to-text API market. North America also remains a major demand anchor for clinical ambient scribing and enterprise meeting intelligence, which helps sustain both usage volume and premium feature demand.

Asia-Pacific is projected to grow at a 22.66% CAGR through 2031, making it the fastest-growing regional block in the speech-to-text API market. Demand is being shaped by linguistic diversity, government digitization programs, and the large-scale contact center outsourcing in countries such as India, the Philippines, and Malaysia. The region also places stronger emphasis on localized languages, mixed-language speech, and deployment flexibility, which gives regional vendors room to compete with larger global providers in the speech-to-text API market. iFLYTEK’s 2026 expansion in Southeast Asia, including stronger Singapore capacity and localized sovereign AI positioning, reflects that demand for region-aligned deployments and language support continues to rise.

Europe holds an important but more complex role in the speech-to-text API market because demand remains solid while compliance expectations continue to rise. Sovereign and region-controlled infrastructure options from Microsoft and AWS are helping vendors address enterprise concerns over data handling, residency, and procurement control. Middle East and Africa shows emerging opportunity in Saudi Arabia and the UAE, where Arabic-language AI demand and sovereign deployment priorities are strengthening regional use cases in the speech-to-text API market. South America is also gaining traction, especially in contact center automation and financial service workflows, as localized offerings and regional partnerships make speech deployment easier for enterprise buyers.

Competitive Landscape

The speech-to-text API market has a three-layer competitive structure made up of hyperscalers, established enterprise AI vendors, and speech-native specialists. Hyperscalers such as Alphabet, Amazon, and Microsoft benefit from captive infrastructure, broad developer ecosystems, and the ability to bundle speech functions with adjacent AI services. Established vendors such as IBM, Baidu, and iFLYTEK bring enterprise reach, regional familiarity, or language-specific strengths that still matter in procurement-heavy environments. Specialists such as Deepgram, AssemblyAI, Speechmatics, and Soniox compete more directly on latency, recognition quality, developer experience, and workflow-specific performance. Across the speech-to-text API market, the main competitive shift is toward bundled voice stacks where transcription, reasoning, and speech output are offered together, which can reduce the pricing power of standalone transcription services.

OpenAI reinforced that shift in May 2026 when it launched GPT-Realtime-Whisper, GPT-Realtime-2, and GPT-Realtime-Translate, placing real-time speech recognition inside a broader voice agent offering rather than selling it only as a separate utility. AssemblyAI responded with Universal-3 Pro Streaming, Medical Mode, and a flat-rate Voice Agent API, showing that specialist vendors are defending their position through lower latency, vertical tuning, and simpler pricing models. Microsoft added MAI-Transcribe-1 into its broader AI stack and tied the model to products such as Copilot Voice and Teams, which shows how platform integration has become a major distribution advantage in the speech-to-text API market. IBM also expanded voice capabilities in watsonx Orchestrate through partner integrations, which underscores that orchestration platforms are becoming important gateways for speech adoption.

Even with stronger bundling pressure, the speech-to-text API market still has opportunity areas in regulated deployments, medical documentation, sovereign cloud environments, and low-resource language coverage. Vendors that can combine auditability, private deployment support, and strong streaming performance can still command differentiated pricing when buyers need more than low-cost transcription. Nuance no longer operates as a standalone competitive force because its speech assets have already been absorbed into Microsoft, which means separate vendor profiling would overstate the number of independent players. That shift makes independent comparison more relevant among newer providers such as Cohere and other specialist platforms that target enterprise use cases where deployment control and model flexibility remain important.

Speech-to-Text API Industry Leaders

Alphabet Inc.

Amazon.com, Inc.

Microsoft Corporation

International Business Machines Corporation

Deepgram, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: OpenAI launched GPT-Realtime-Whisper on May 7, 2026, a streaming speech-to-text model priced at USD 0.017 per minute, alongside GPT-Realtime-2, GPT-5-class reasoning, USD 32 per 1M audio input tokens, and GPT-Realtime-Translate supporting 70-plus input languages, entering direct competition with Deepgram and AssemblyAI for real-time voice agent pipelines, Deutsche Telekom and Zillow are among early production partners.

- May 2026: AssemblyAI launched Universal-3 Pro Streaming on May 1, 2026, achieving 8.14% WER across English, lowest among major streaming providers, with sub-200-millisecond end-to-end latency, the company simultaneously launched a Medical Mode, reducing missed medical entities by over 20%, and a Voice Agent API at USD 4.50 per hour flat, approximately 4x cheaper than OpenAI's Realtime API.

- April 2026: Deepgram raised USD 130 million in Series C funding at a USD 1.3 billion valuation and simultaneously launched Flux Multilingual, the first multilingual conversational speech recognition model with real-time code-switching across 10 languages.

- April 2026: Otter.ai launched its Conversational Knowledge Engine on April 28, 2026, incorporating MCP client functionality enabling enterprise search across external tools, AI Chat, and Otter for Desktop. The company had crossed USD 100 million in annual recurring revenue in 2025.

Global Speech-to-Text API Market Report Scope

The Speech-to-Text API Market includes cloud-based and on-premises APIs that convert spoken audio into written text for applications such as transcription, captioning, voice commands, and call-center automation. It covers both real-time and batch transcription solutions used by developers and enterprises to embed speech recognition into apps, workflows, and digital platforms.

The Speech-to-Text API Market Report is Segmented by Component (Software and Services), Deployment Model (Cloud-based, On-Premises, Hybrid), Organization Size (Large Enterprises, and Small and Medium-sized Enterprises), Application (Content transcription, Contact center and customer management, Subtitle and caption generation, Fraud detection and prevention, Risk and compliance management, Voice-enabled workflow automation and note generation), End-User Industry (IT and Telecommunications, BFSI, Healthcare and Life Sciences, Media and Entertainment, Retail and E-commerce, Government and Defense, Education, Travel and Hospitality), and Geography (North America, South America, Europe, Asia-Pacific and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Software | |

| Services | Professional Services |

| Managed Services |

| Cloud-based |

| On-premises and Private cloud |

| Hybrid and Sovereign Cloud |

| Large Enterprises |

| Small and Medium-sized Enterprises |

| Content Transcription |

| Contact Center and Customer Management |

| Subtitle and Caption Generation |

| Fraud Detection and Prevention |

| Risk and Compliance Management |

| Voice-enabled Workflow Automation and Note Generation |

| IT and Telecommunications |

| BFSI |

| Healthcare and Life Sciences |

| Media and Entertainment |

| Retail and E-commerce |

| Government and Defense |

| Education |

| Travel and Hospitality |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia and New Zealand | |

| Rest of Asia-Pacific | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| South Africa | |

| Egypt | |

| Rest of Middle East and Africa |

| By Component | Software | |

| Services | Professional Services | |

| Managed Services | ||

| By Deployment Model | Cloud-based | |

| On-premises and Private cloud | ||

| Hybrid and Sovereign Cloud | ||

| By Organization Size | Large Enterprises | |

| Small and Medium-sized Enterprises | ||

| By Application | Content Transcription | |

| Contact Center and Customer Management | ||

| Subtitle and Caption Generation | ||

| Fraud Detection and Prevention | ||

| Risk and Compliance Management | ||

| Voice-enabled Workflow Automation and Note Generation | ||

| By End-User Industry | IT and Telecommunications | |

| BFSI | ||

| Healthcare and Life Sciences | ||

| Media and Entertainment | ||

| Retail and E-commerce | ||

| Government and Defense | ||

| Education | ||

| Travel and Hospitality | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| South Africa | ||

| Egypt | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size and outlook for the speech-to-text API market?

The speech-to-text API market was valued at USD 2.44 billion in 2025, reached USD 2.87 billion in 2026, and is projected to reach USD 7.21 billion by 2031 at a CAGR of 20.23%.

Which deployment model is growing the fastest in speech-to-text APIs?

Hybrid and sovereign cloud is the fastest-growing deployment model, with a projected CAGR of 22.43% through 2031 as enterprises seek more control over data and compliance.

Why is healthcare becoming a major growth area for speech recognition APIs?

Healthcare and life sciences is projected to grow at 23.71% through 2031 because providers are using voice tools for clinical documentation, ambient scribing, and patient intake workflows.

Which application area is expanding the fastest?

Voice-enabled workflow automation and note generation is expected to post the fastest growth at a 22.78% CAGR, reflecting the shift from simple transcription to action-oriented voice workflows.

Which region offers the strongest growth opportunity?

Asia-Pacific is projected to grow the fastest at 22.66% through 2031, supported by multilingual demand, digital government programs, and large contact center outsourcing activity.

What are the main risks buyers should watch when selecting a vendor?

The main risks are accuracy loss in accented or noisy speech, code-switching errors, data privacy obligations, and the need for compliant deployment options in regulated environments.

Page last updated on: