Spain Customer Data Platform Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

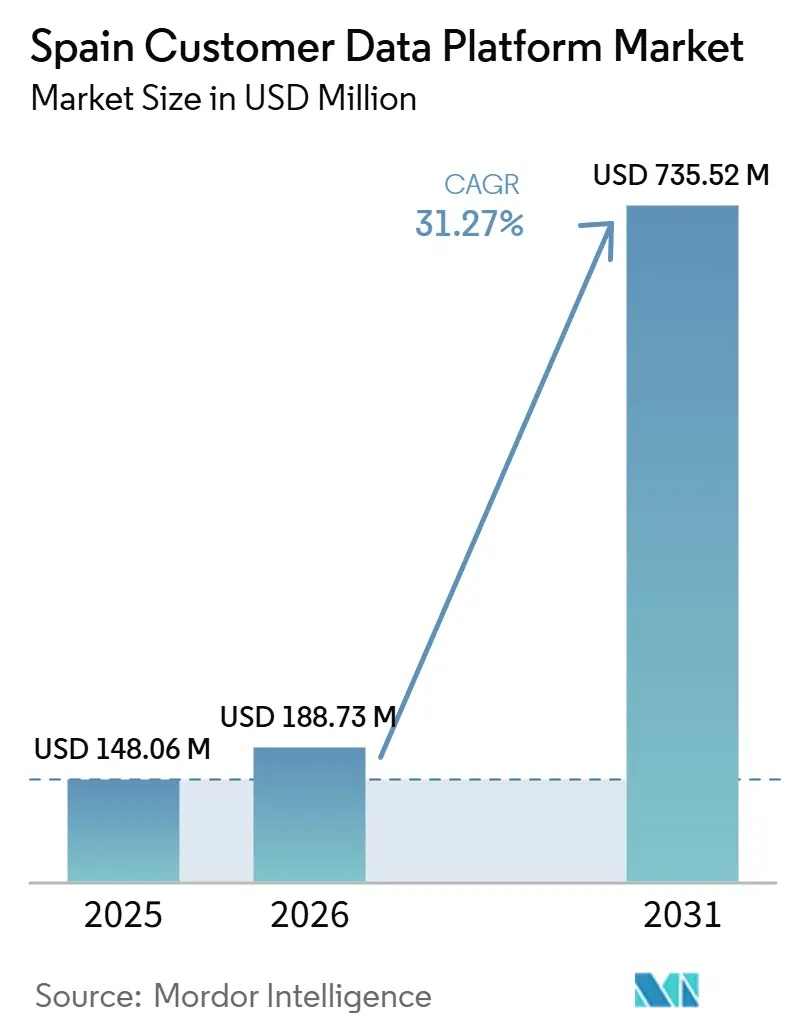

| Base Year Market Size (2025) | USD 148.06 Million |

| Market Size (2026) | USD 188.73 Million |

| Market Size (2031) | USD 735.52 Million |

| Growth Rate (2026 - 2031) | 31.27% CAGR |

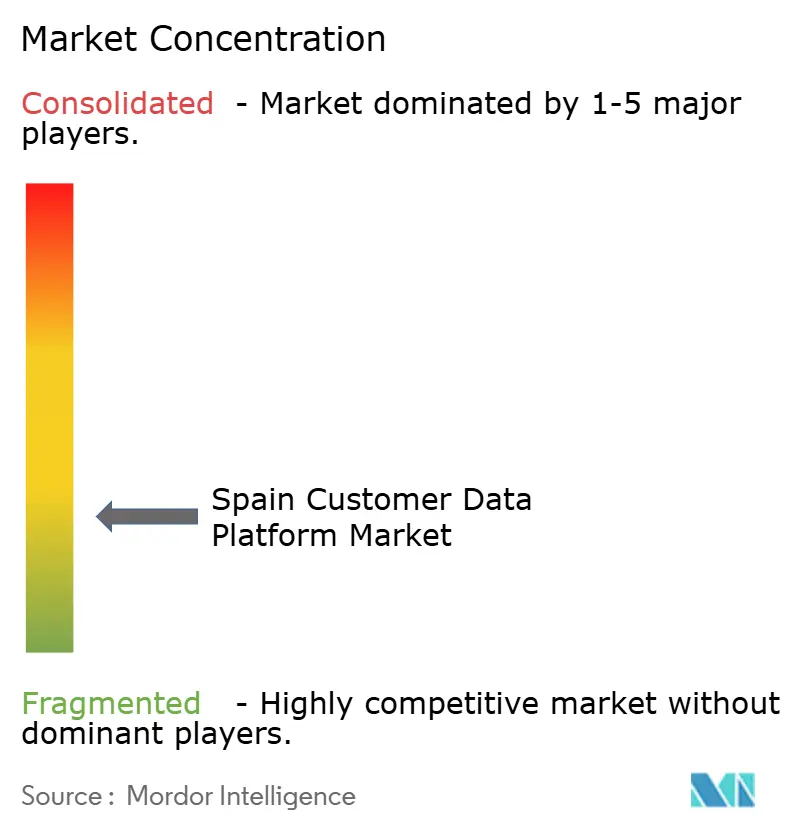

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Spain Customer Data Platform Market Analysis by Mordor Intelligence

The Spain customer data platform market size was valued at USD 148.06 million in 2025 and estimated to grow from USD 188.73 million in 2026 to reach USD 735.52 million by 2031, at a CAGR of 31.27% during the forecast period 2026-2031. The Spain customer data platform market is moving quickly because Spanish companies now need a cleaner way to collect, unify, and activate first-party customer data across websites, apps, stores, and service channels. Consent enforcement under GDPR and Spain’s LOPDGDD has turned customer identity management into a business priority rather than a marketing upgrade, so CDP adoption now sits closer to compliance and operating decisions than before. Strong digital advertising growth and rapid expansion in connected TV have also raised the value of real-time audience activation, making unified customer profiles more useful in daily execution. E-commerce growth in Spain has increased the volume of customer interactions brands need to connect with, pushing more firms toward cloud-based, activation-ready data environments. Competition remains active between large suite vendors and pure-play providers, while implementation friction, fragmented internal systems, and slower legal review cycles continue to shape how quickly the Spain customer data platform market moves from interest to full deployment.

Key Report Takeaways

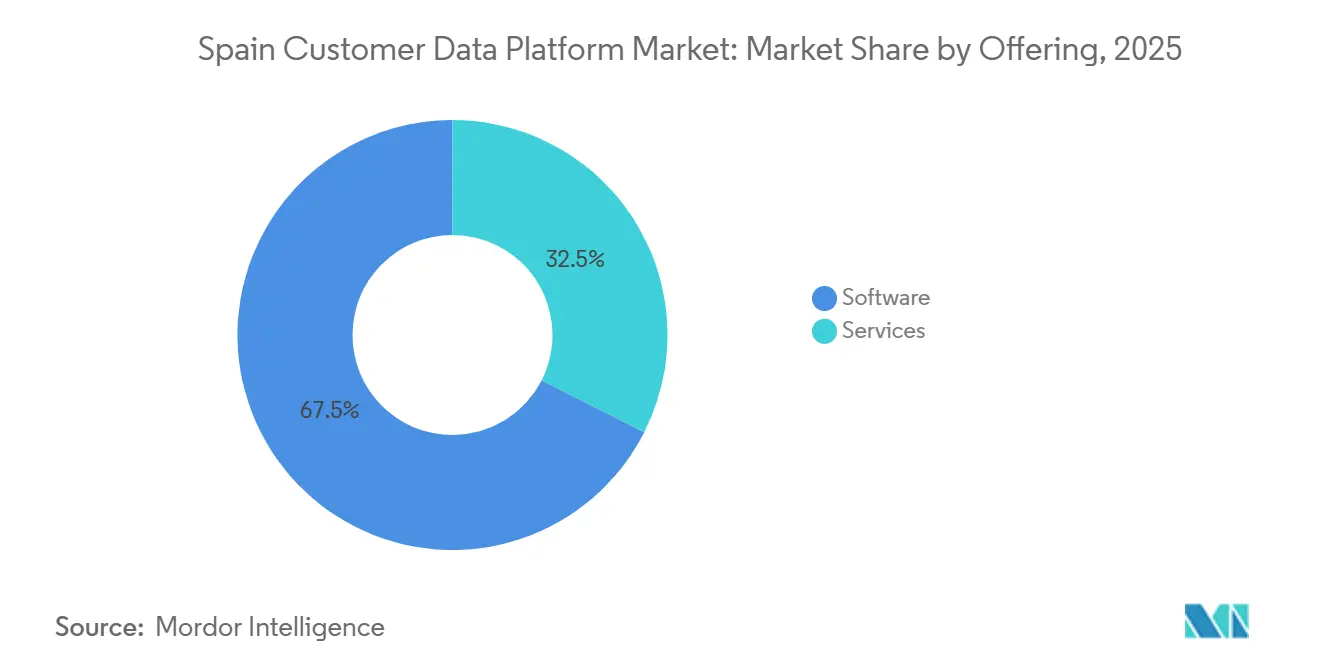

- By offering, software led the market with a 67.54% of the Spain customer data platform market revenue share in 2025, while services is projected to expand at a 33.92% CAGR through 2031.

- By deployment mode, cloud held the largest share at 61.49% in 2025, and cloud is also expected to record the fastest growth at a 33.18% CAGR through 2031.

- By organization size, large enterprises accounted for 71.23% of revenue share in 2025, while SMEs are projected to expand at a 33.51% CAGR through 2031 in the Spain customer data platform market.

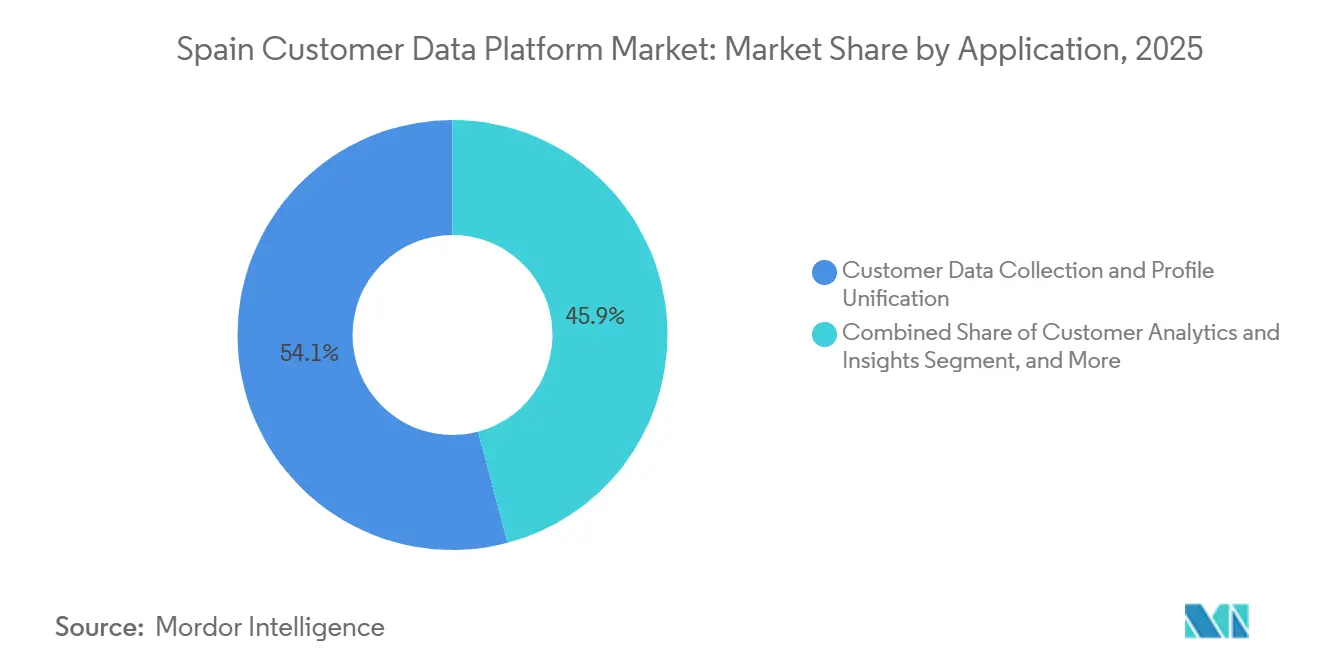

- By application, customer data collection and profile unification captured a 54.12% of the Spain customer data platform market revenue share in 2025, while audience segmentation and personalization are expected to grow at a 32.89% CAGR through 2031.

- By end-user industry, retail and e-commerce held the largest share at 30.11% in 2025, while media and entertainment is projected to advance at a 32.44% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Spain Customer Data Platform Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising First-Party Data Investment by Spanish Brands | +5.2% | National, with concentration in Madrid, Catalonia, and Basque Country | Medium term (2-4 years) |

| Cookie Deprecation Accelerating Identity Resolution | +4.3% | National | Short term (≤ 2 years) |

| Real-Time Personalization Across Omnichannel Journeys | +3.9% | National, led by Madrid and Barcelona retail corridors | Medium term (2-4 years) |

| Retail and E-Commerce CDP Modernization | +3.4% | National, concentrated in Catalonia and Madrid | Short term (≤ 2 years) |

| Tourism, Hospitality, and Travel Data Unification Demand | +2.8% | Canary Islands, Andalusia, Balearic Islands, and Valencia | Medium term (2-4 years) |

| AI-Driven Next-Best-Action Orchestration | +2.5% | National, with early gains in BFSI and telecom sectors | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising First-Party Data Investment by Spanish Brands

The Spain customer data platform market is gaining support from a clear shift toward first-party data strategies in consumer-facing sectors. Spanish brands now face weaker returns from older tracking approaches, so owned customer data has become more valuable in both acquisition and retention work. Spain’s digital advertising market gives brands a strong reason to invest in systems that can turn their own customer data into addressable audiences at speed. Connected TV grew 48.4% in the same year, underscoring the value of real-time audience matching and making profile quality more important in campaign delivery. As a result, the Spain customer data platform market is being shaped less by software replacement alone and more by the need to build a durable first-party data layer across paid, owned, and service channels. This also explains why CDP spending is increasingly tied to revenue activation, not only to better reporting or basic customer record management.

Cookie Deprecation Accelerating Identity Resolution

The Spain customer data platform market is also benefiting from the practical limits of cookie-based targeting in a privacy-first setting. Spain’s cookie enforcement standards have remained active under the AEPD's guide, which has been in effect since January 2024, and continue to put pressure on firms to use more reliable, consent-based identity signals.[1]Agencia Española de Protección de Datos, “Guide on the Use of Cookies,” AEPD, aepd.es IAB Europe noted that signal loss and cross-platform data access remain key challenges in the post-third-party cookie environment, which supports demand for identity systems that can work across channels with stronger control. In this setting, deterministic identity resolution based on email, phone number, loyalty credentials, and consented logins is becoming more useful than older probabilistic approaches. That shift directly favors the Spain customer data platform market because CDPs are one of the few systems built to unify those signals into a persistent profile. It also lifts the value of consent management and governance features, which many buyers now view as core platform requirements rather than add-on functions.

Real-Time Personalization Across Omnichannel Journeys

The Spain customer data platform market is being driven by the need to respond to customer behavior while a shopping or service session is still active. Spain-to-Spain e-commerce transactions show how quickly digital customer interactions are expanding inside the country. Higher transaction intensity makes it harder for brands to rely on delayed batch systems when offers, service prompts, and journey decisions need to reflect current intent. Connected TV growth adds another real-time activation layer because audience segments now need to be refreshed across video, web, app, and CRM channels in a more coordinated way. This is why the Spain customer data platform market is seeing stronger demand for low-latency profile access, event-based orchestration, and integrations that can support personalization at the moment of interaction. It also increases the cost of poor data unification, as customers now expect greater consistency across channels than many legacy stacks can deliver.

Retail and E-Commerce CDP Modernization

Retail and e-commerce modernization remains one of the clearest demand engines for the Spain customer data platform market. Domestic online transactions continued to scale quickly in 2025, and that growth is increasing the need to connect product discovery, browsing, purchase, loyalty, and service data in a single model. Spanish retailers are now treating the CDP less as an extension of CRM and more as the canonical layer for customer identity across online and offline touchpoints. A documented Mercadona case showed that unified behavioral analytics across digital and physical retail environments improved the company's understanding of product discovery and conversion behavior. That pattern fits the wider Spain customer data platform market, where retail buyers are increasingly linking platform investments to measurable commercial outcomes rather than only to back-end efficiency. Consent mapping for loyalty and transaction data adds a governance dimension, so modernization plans now tend to combine activation goals with stronger data control.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Legacy CRM and Martech Fragmentation in Mid-Market Firms | -3.8% | National, most acute in mid-market enterprises outside major cities | Short term (≤ 2 years) |

| GDPR Consent Governance and Legal Review Delays | -3.2% | National, with AEPD jurisdiction across all sectors | Medium term (2-4 years) |

| Shortage of Customer Data Engineering Talent | -2.5% | National | Medium term (2-4 years) |

| ROI Pressure from Long Implementation Cycles | -2.1% | National, most pronounced in B2B and industrial sectors | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Legacy CRM and Martech Fragmentation in Mid-Market Firms

A major brake on the Spain customer data platform market is the fragmented state of customer data systems in many mid-market firms. Customer information often sits in separate CRM, e-commerce, email, analytics, and service tools that were never designed to share one identity framework. That makes CDP deployment harder because firms must fix data structure, permissions, and process ownership before they can activate unified profiles at scale. The issue is especially evident outside Spain’s largest corporate centers, where technology resources and support for integration are usually thinner. Compliance needs add another layer, as legacy records often require consent review and governance checks before they can be brought into a unified environment. This means the Spain customer data platform market can face slow adoption even when business demand is clear, simply because the work needed before implementation is larger than many buyers first expect.

GDPR Consent Governance and Legal Review Delays

Consent governance and legal review delays continue to slow parts of the Spain customer data platform market even as privacy rules also create long-term demand for compliant systems. The AEPD said it received 30,931 complaints in 2025, up 64% from the prior year, which shows how visible data protection issues have become in Spain. When a CDP project includes behavioral profiling, cross-channel activation, or new consent flows, legal review can stretch procurement and delay implementation. The AEPD strategic plan for 2025-2030 also points to more proactive and technology-aware supervision, so companies are less willing to move quickly without a documented governance design. This adds friction for firms that want fast activation but do not yet have clear rules for lawful processing, preference capture, and audit trails. As a result, the Spain customer data platform market often advances through staged deployments, where data unification begins first and broader activation follows after governance controls are established.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering: Software Anchors Revenue as Services Define the Growth Arc

Software accounted for 67.54% of revenue in 2025, indicating that the Spain customer data platform market still derives most of its current value from core platform subscriptions and enterprise software commitments. Large organizations usually buy software first because they need a central environment for profile unification, audience building, and activation across multiple business units. In many deployments, the platform becomes the operating layer that connects campaign tools, analytics, service systems, and customer identity logic. This keeps software at the center of current spending because the buyer cannot unlock the rest of the use case without that foundation. It also reflects the fact that the Spain customer data platform market has already moved beyond early experimentation in larger accounts and into more structured platform adoption.

Services, however, are projected to grow at a 33.92% CAGR through 2031, which indicates that execution capacity is becoming just as important as platform selection in the Spain customer data platform market. Implementation, integration, managed services, and data engineering work now shape how fast a buyer reaches value after signing a contract. Many firms want composable deployments that fit around existing tools, and that raises the role of outside specialists who can connect systems without forcing a full rebuild. This is one reason the service layer is expanding faster than software, even though software still generates the larger revenue base. Partners with local governance knowledge and change management support are well placed to benefit, as many Spanish buyers need both technical delivery and internal adoption support. Over time, that should narrow the gap between the software base and service expansion inside the Spain customer data platform industry.

By Deployment Mode: Cloud Consolidates Lead as Hybrid Gains Enterprise Traction

Cloud captured a 61.49% revenue share in 2025 and recorded the fastest growth at a 33.18% CAGR through 2031, indicating it already accounts for a leading share of the Spain customer data platform market in current deployments. This lead reflects the need for scalable processing, faster updates, and easier integration with marketing, commerce, and analytics tools that already run in cloud environments. Real-time profile use cases are harder to support when data must move slowly between isolated systems, so cloud deployment naturally aligns with the operational needs of modern CDP programs. The cloud model also helps vendors deliver new features faster and lets customers expand workloads without rebuilding the core environment. These practical advantages explain why cloud remains the default path for much of the Spain customer data platform market.

On-premises deployment still has relevance in regulated sectors such as BFSI and healthcare, where data-handling rules, internal controls, and legacy architecture can slow a full migration. Hybrid models are gaining ground because they let firms keep sensitive records in tightly governed environments while extending activation into cloud-based engagement systems. This balance matters for enterprise buyers who need auditability and processing traceability but still want faster personalization and orchestration capabilities. In practice, hybrid adoption shows that buyers are not choosing between speed and control in absolute terms. They are instead building staged architectures that preserve critical data safeguards while expanding activation reach over time. That makes deployment mode one of the clearest examples of how the Spain customer data platform market is adapting to local compliance and operating realities rather than following a single global template.

By Organization Size: Large Enterprises Lead While SMEs Accelerate Adoption

Large enterprises held a 71.23% revenue share in 2025, meaning they accounted for 71.23% of Spain customer data platform market share in the current revenue base. This concentration reflects the high cost, deep integration, and organizational readiness required to deploy CDPs across many channels, brands, and internal teams. Larger firms usually have more customer data, more activation use cases, and stronger budgets for implementation, which makes them the first group to adopt advanced profile unification at scale. They also face more pressure to standardize data governance across business units, so the business case for centralized platforms tends to be stronger. For these reasons, the large-enterprise segment remains the anchor of present-day demand in the Spain customer data platform market.

SMEs are the fastest-growing segment, with a 33.51% CAGR through 2031, which signals an important broadening of the buyer base in the Spain customer data platform market. Smaller firms are entering through lighter deployments, vertical SaaS pathways, and composable models that focus on practical activation rather than large infrastructure projects. Digital support programs and wider adoption of CRM, analytics, and marketing tools have lowered the barrier for many SMEs to consider unified customer data as a commercial asset. These firms usually care most about faster time-to-value, easier onboarding, and simpler day-to-day use for sales and marketing teams. As SME digital maturity improves, vendors that package CDP functionality in more accessible ways should gain traction. This shift also shows that the Spain customer data platform industry is moving from a large-enterprise core toward a broader and more layered demand structure.

By Application: Profile Unification Leads While Personalization Scales Faster

Customer data collection and profile unification accounted for 54.12% of revenue in 2025, representing 54.12% of the Spain customer data platform market size in the largest application group. That result is logical because every subsequent use case depends on having a persistent, usable customer profile first. Spanish buyers often start with identity stitching, consented data collection, and customer record standardization before they expand into more visible activation scenarios. This keeps profile unification at the center of current spending, even when marketing teams are primarily focused on personalization or journey automation. The structure of the Spain customer data platform market therefore still reflects a build-first pattern where firms secure data foundations before widening commercial use.

Audience segmentation and personalization are projected to grow at a 32.89% CAGR through 2031, which shows where the next layer of budget is moving once data foundations are in place. After unification, companies want to use those profiles for campaign triggers, offer selection, customer journey coordination, and channel-level decisioning. Marketing orchestration and analytics follow naturally because unified data becomes more valuable when it supports measurable engagement and conversion gains. Consent and preference management is also gaining a larger application role because activation at scale is difficult without clear permissions and governance controls. This progression from collection to activation captures the current maturity path of the Spain customer data platform market. It also explains why the fastest growth is happening in applications that turn unified data into direct customer-facing actions.

By End-User Industry: Retail Leads While Media and Entertainment Expands Fastest

Retail and e-commerce accounted for 30.11% of the Spain customer data platform market share in 2025, making it the largest vertical. Retailers generate rich streams of transactional, behavioral, loyalty, and service data, so they often have the clearest need for profile unification across channels. Spain-to-Spain e-commerce transactions grew 30.1% year over year in the second quarter of 2025, underscoring the need for retailers to connect customer actions across web, app, store, and support channels. This makes retail the most natural revenue anchor for the Spain customer data platform market at the current stage of adoption. It also helps explain why many of the most practical deployment cases in Spain center on omnichannel commerce and loyalty activation.

Media and entertainment is projected to grow at a 32.44% CAGR through 2031, placing it ahead of other verticals in forward expansion within the Spain customer data platform market. Connected TV advertising rose 48.4% in 2025, driving stronger demand for audience resolution and cross-channel activation built on first-party data. BFSI remains an important contributor because banks and insurers need unified profiles to optimize service, retention, and offers across digital and branch channels. Healthcare and life sciences are also moving forward as firms build fuller accounts and professional views for commercial engagement, a pattern reflected in Salesforce’s life sciences deployment activity in Spain.[2]Salesforce, “Adamed Selects Salesforce Life Sciences for Healthcare Engagement,” Salesforce, salesforce.com Manufacturing and telecom contribute in more selective ways, often tied to service journeys, account management, or channel partner coordination. Taken together, these verticals show that the Spain customer data platform industry is expanding beyond retail, even though commerce still accounts for the largest share today.

Geography Analysis

Madrid remains the largest center of demand in the Spain customer data platform market because it houses financial services, insurance, telecom, energy, and national decision-making functions. Many of the most visible enterprise deployments have been tied to organizations operating from Madrid, including Vodafone España’s use of Salesforce Data Cloud and related activation tools across its B2B environment. The city also hosts a dense ecosystem of implementation partners, enterprise technology teams, and vendor relationships that support larger and more complex projects. Regulatory awareness is especially strong there, which increases interest in platforms that can combine customer activation with clearer consent and governance controls.

Catalonia, led by Barcelona, forms the second-largest demand cluster in the Spain customer data platform market due to its concentration in retail, FMCG, direct-to-consumer brands, pharmaceuticals, and digital commerce. The region’s strong e-commerce orientation supports demand for tools that can connect browsing, transactions, loyalty, and campaign activation with fewer delays. Barcelona’s technology base also supports earlier adoption of composable and integration-heavy deployments, especially among firms that want to preserve existing data investments. The Basque Country and Valencia add important demand through industrial, logistics, trade, and B2B operating models where customer data is spread across many systems and touchpoints.

Tourism gives the Spain customer data platform market a wider regional footprint than many other enterprise software categories. National tourism data initiatives and smart destination programs are helping hospitality operators take unified customer data across hotels, destinations, and visitor services more seriously.[3]Ministerio de Industria y Turismo, “La Secretaria de Estado de Turismo Anuncia la Puesta en Marcha Desde Hoy de la Plataforma Inteligente de Destinos,” Ministry of Industry and Tourism, mintur.gob.es The first 30 hotels joined the initial phase of Smart Data Canarias in early 2026, indicating that structured data activation is beginning to spread across regional hospitality networks. Andalusia, the Canary Islands, the Balearic Islands, and Valencia stand out because they combine heavy visitor flows with fragmented customer data environments that have historically been harder to unify. As those regional systems mature, geography in the Spain customer data platform market should become less concentrated in corporate headquarters alone and more distributed across tourism-driven operating zones.

Competitive Landscape

The Spain customer data platform market is moderately fragmented, with global suite vendors competing against pure-play providers and composable specialists. Salesforce has built visible momentum through customer data and activation deployments in sectors such as telecom, publishing, and life sciences, supported by both direct product offerings and partner-led execution.[4]NTT DATA, “Transforming Vodafone España’s B2B Marketing,” NTT DATA, nttdata.com This gives suite vendors an advantage when buyers want CDP capability closely tied to CRM, marketing automation, and service workflows. At the same time, vendors such as Tealium, Amperity, Bloomreach, and Zeotap stay relevant by emphasizing composability, faster implementation, privacy-oriented architecture, and lower disruption to existing stacks.

Competition in the Spain customer data platform market is also shifting toward the activation and AI layer rather than staying focused only on ingestion and profile unification. Databricks entered the CDP space in June 2026 with CustomerLake, an agentic CDP embedded in its lakehouse platform, and launched with a 21-partner ecosystem that included Bloomreach, Twilio, Adobe, and The Trade Desk. That move matters because it brings together customer data, identity resolution, audience construction, automation, and AI agents into a single, governed environment. For standalone CDP vendors, this raises the pressure to show why a separate platform still adds value when data and activation functions can sit closer together. It also strengthens the role of European compliance and governance expertise, as Spanish buyers increasingly want privacy controls built into the operating model rather than added after deployment. As a result, the competitive edge in the Spanish customer data platform market is shifting toward usable orchestration, faster deployment, and clearer governance.

Local execution will remain an important differentiator even as large global platforms expand their product reach. Buyers in Spain often need partner support for integration, consent design, organizational adoption, and phased rollout planning, especially when existing systems are fragmented. This means that vendors that combine strong core functionality with dependable implementation networks are likely to perform better than those that rely solely on product depth. The next competitive openings appear strongest in hospitality, tourism, and mid-market deployments, where data is abundant but tailored activation models are still underdeveloped.

Spain Customer Data Platform Industry Leaders

Oracle Corporation

Salesforce, Inc.

SAP SE

Adobe Inc.

Twilio Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Databricks announced CustomerLake, an agentic CDP natively embedded in its Lakehouse platform, at its Data and AI Summit. The product unifies customer data, identity resolution, audience building, campaign automation, and AI agents in a single environment, with a 21-partner launch ecosystem that includes Bloomreach, Twilio, and The Trade Desk. Early adopters include Getnet by Santander, signaling direct relevance for Spain’s BFSI sector.

- June 2026: Spain’s Ministry of Industry and Tourism launched LINX, the Espacio de Datos de Turismo, a national federated data space enabling tourism operators, hotel chains, and destination managers to securely exchange and activate customer data in line with European governance standards. The platform integrates sandbox environments and a solution marketplace for advanced analytics and AI-driven tourism use cases, addressing the long-standing fragmentation of visitor data across Spain’s tourism economy.

- March 2026: Smart Data Canarias onboarded its first 30 hotels to its tourism data intelligence platform, funded with EUR 600,000 (USD 671,000) from the Canarian Government and Next Generation EU funds. The platform integrates hotel PMS systems, IoT devices, and external databases for real-time sustainability and competitive intelligence.

- January 2026: Adamed Laboratorios, a leading Spanish pharmaceutical company, selected Salesforce Agentforce Life Sciences for Customer Engagement to unify commercial operations and build a 360-degree view of hospital, pharmacy, and healthcare professional accounts. The implementation, led by Izertis, is designed as the foundation for scalable international expansion.

Spain Customer Data Platform Market Report Scope

The Spain Customer Data Platform Market comprises platforms designed to centralize, unify, and activate customer data from multiple sources to support personalized marketing, customer analytics, and customer journey management initiatives. These solutions enable organizations to improve customer understanding, campaign effectiveness, audience segmentation, and consent management. Rising investments in digital customer engagement, the increasing adoption of advanced marketing technologies, and the growing demand for personalized customer experiences are fueling the market. CDPs help enterprises optimize customer interactions and improve marketing outcomes through data-driven decision-making.

The Spain Customer Data Platform Market Report is Segmented by Offering (Software, and Services), Deployment Mode (Cloud, On-Premises, and Hybrid), Organization Size (Large Enterprises, and Small and Medium Enterprises), Application (Customer Data Collection and Profile Unification, Audience Segmentation and Personalization, Marketing Campaign and Customer Journey Orchestration, Customer Analytics and Insights, Consent and Preference Management, and Other Applications), and End-User Industry (Retail and E-Commerce, Banking, Financial Services, and Insurance (BFSI), Healthcare and Life Sciences, Information Technology and Telecom, Media and Entertainment, Industrial Manufacturing, Government and Public Administration, and Other End-User Industries). The Market Forecasts are Provided in Terms of Value (USD).

| Software |

| Services |

| Cloud |

| On-Premises |

| Hybrid |

| Large Enterprises |

| Small and Medium Enterprises |

| Customer Data Collection and Profile Unification |

| Audience Segmentation and Personalization |

| Marketing Campaign and Customer Journey Orchestration |

| Customer Analytics and Insights |

| Consent and Preference Management |

| Other Applications |

| Retail and E-Commerce |

| Banking, Financial Services, and Insurance (BFSI) |

| Healthcare and Life Sciences |

| Information Technology and Telecom |

| Media and Entertainment |

| Industrial Manufacturing |

| Government and Public Administration |

| Other End-User Industries |

| By Offering | Software |

| Services | |

| By Deployment Mode | Cloud |

| On-Premises | |

| Hybrid | |

| By Organization Size | Large Enterprises |

| Small and Medium Enterprises | |

| By Application | Customer Data Collection and Profile Unification |

| Audience Segmentation and Personalization | |

| Marketing Campaign and Customer Journey Orchestration | |

| Customer Analytics and Insights | |

| Consent and Preference Management | |

| Other Applications | |

| By End-User Industry | Retail and E-Commerce |

| Banking, Financial Services, and Insurance (BFSI) | |

| Healthcare and Life Sciences | |

| Information Technology and Telecom | |

| Media and Entertainment | |

| Industrial Manufacturing | |

| Government and Public Administration | |

| Other End-User Industries |

Key Questions Answered in the Report

What is the current and forecast size of the Spain customer data platform sector?

The Spain customer data platform market size was USD 148.06 million in 2025, stood at USD 188.73 million in 2026, and is forecast to reach USD 735.52 million by 2031 at a 31.27% CAGR.

What is driving demand for customer data platforms in Spain?

The main demand drivers are first-party data investment, tighter privacy enforcement, stronger omnichannel commerce activity, and the need for real-time personalization across customer touchpoints.

Which deployment model is leading adoption in Spain?

Cloud leads adoption with a 61.49% revenue share in 2025 and is also the fastest-growing deployment model with a 33.18% CAGR through 2031.

Which application is growing fastest in Spain?

Audience segmentation and personalization is the fastest-growing application area, with a projected 32.89% CAGR through 2031, as more firms move from data collection into commercial activation.

Which end-user vertical contributes the most revenue?

Retail and e-commerce led with a 30.11% revenue share in 2025 because this segment creates large volumes of transactional and behavioral data across online and offline channels.

Are SMEs becoming important buyers of CDP solutions in Spain?

Yes. Large enterprises still held 71.23% of revenue in 2025, but SMEs are projected to grow faster at a 33.51% CAGR, showing that adoption is broadening beyond the enterprise base.

Page last updated on: