Spain CRM Marketing Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

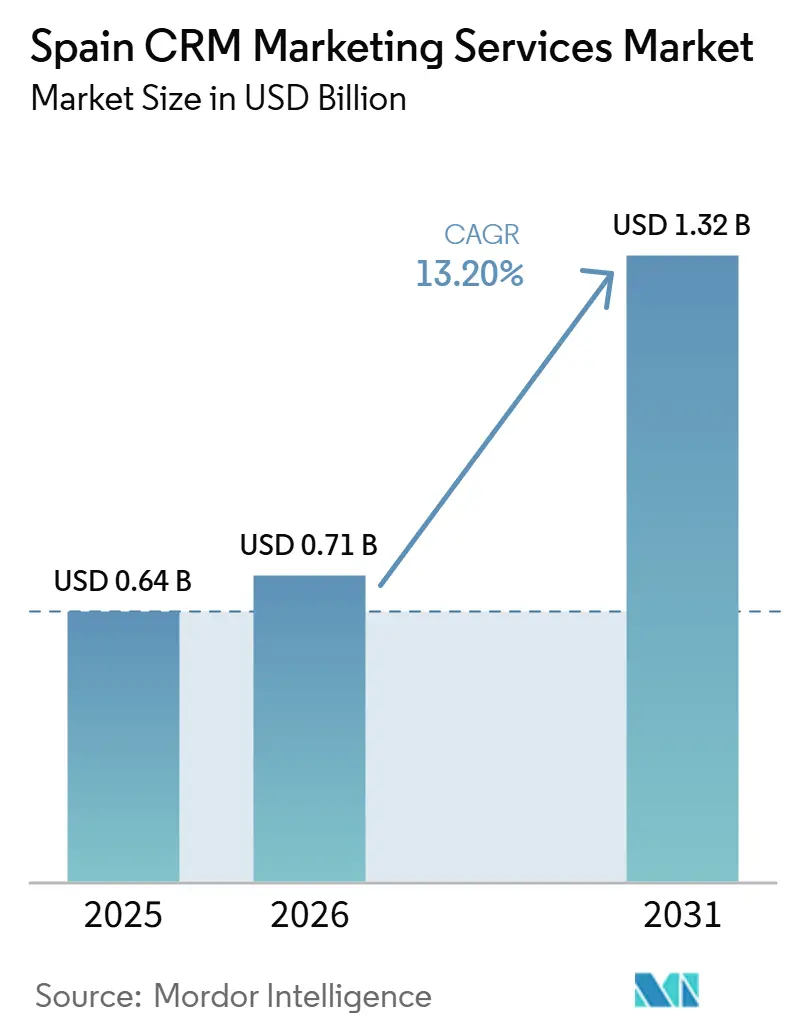

| Base Year Market Size (2025) | USD 0.64 Billion |

| Market Size (2026) | USD 0.71 Billion |

| Market Size (2031) | USD 1.32 Billion |

| Growth Rate (2026 - 2031) | 13.20% CAGR |

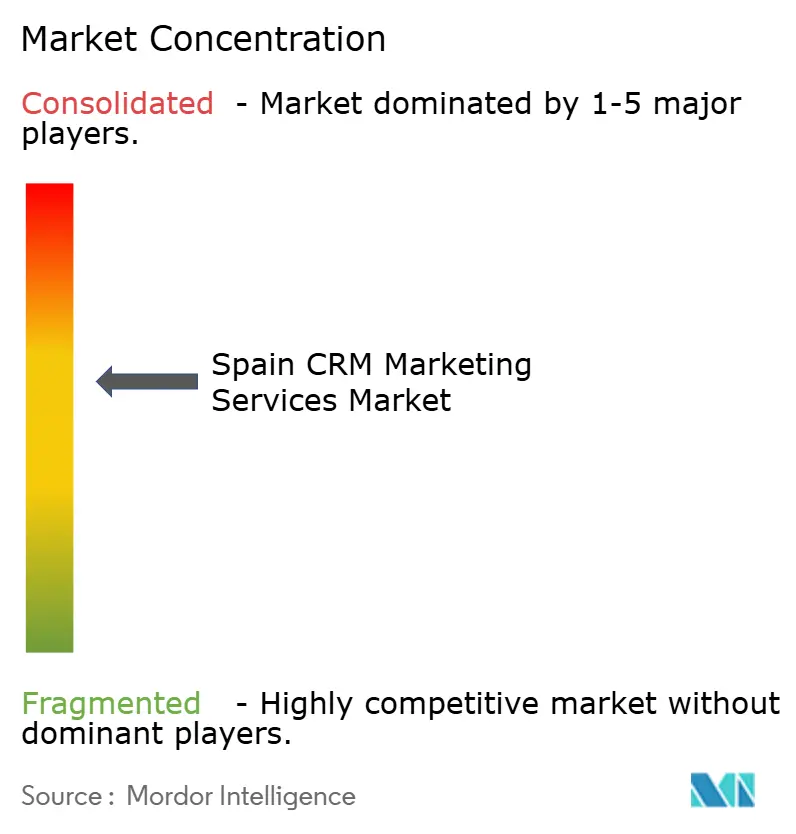

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Spain CRM Marketing Services Market Analysis by Mordor Intelligence

The Spain CRM marketing services market size was valued at USD 0.64 billion in 2025 and estimated to grow from USD 0.71 billion in 2026 to reach USD 1.32 billion by 2031, at a CAGR of 13.20% during the forecast period (2026-2031). The Spain CRM marketing services market is expanding as enterprises replace disconnected campaign tools with more unified customer management and activation systems. Spain’s strong digital usage patterns support broader adoption of cloud-based CRM workflows across both enterprise and mid-market buyers. Public digitization programs, rising demand for coordinated customer journeys, and wider use of AI-led personalization are all pushing the Spain CRM marketing services market forward. Competition remains active as global software vendors defend enterprise accounts while European and local providers compete on price, language support, and compliance readiness. Complexity in deployment and tighter privacy expectations are slowing some projects, but they are also creating room for vendors that can deliver simpler implementation and stronger governance.

Key Report Takeaways

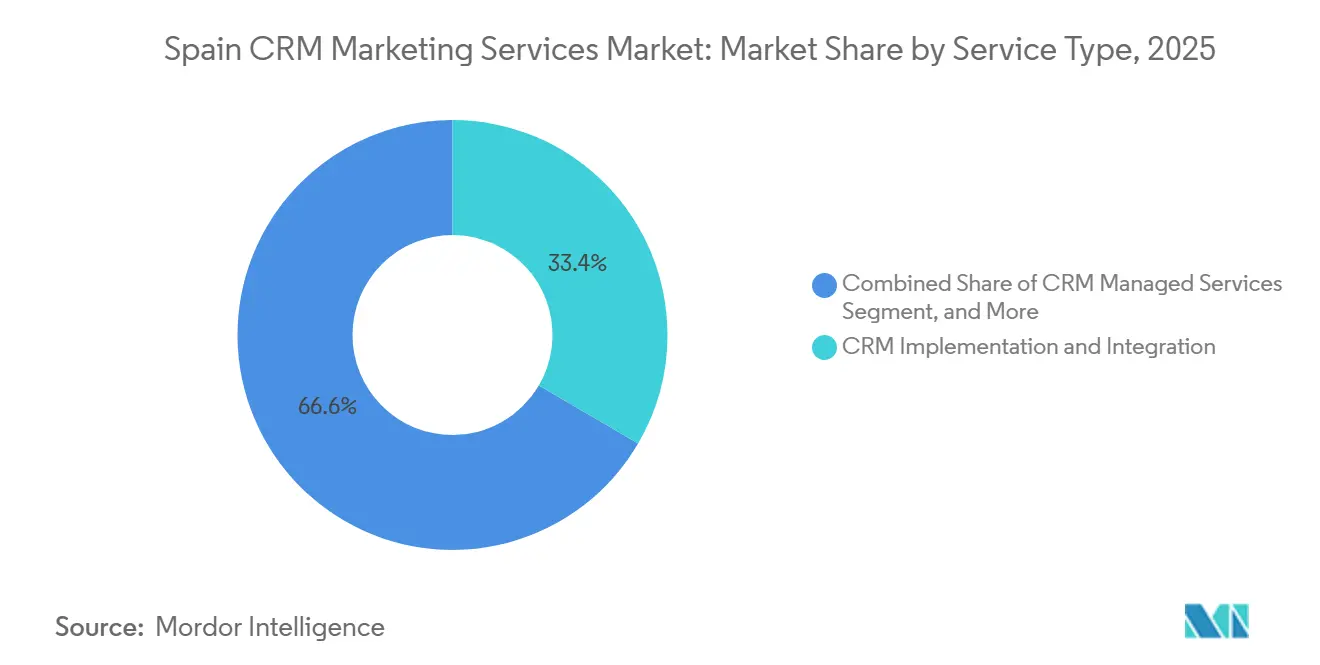

- By service type, CRM implementation and integration held 33.42% of the Spain CRM marketing services market share in 2025, while CRM managed services is projected to expand at 13.84% CAGR through 2031.

- By enterprise size, large enterprises accounted for 66.81% of demand in 2025, while small and medium enterprises are projected to expand at a 13.69% CAGR through 2031.

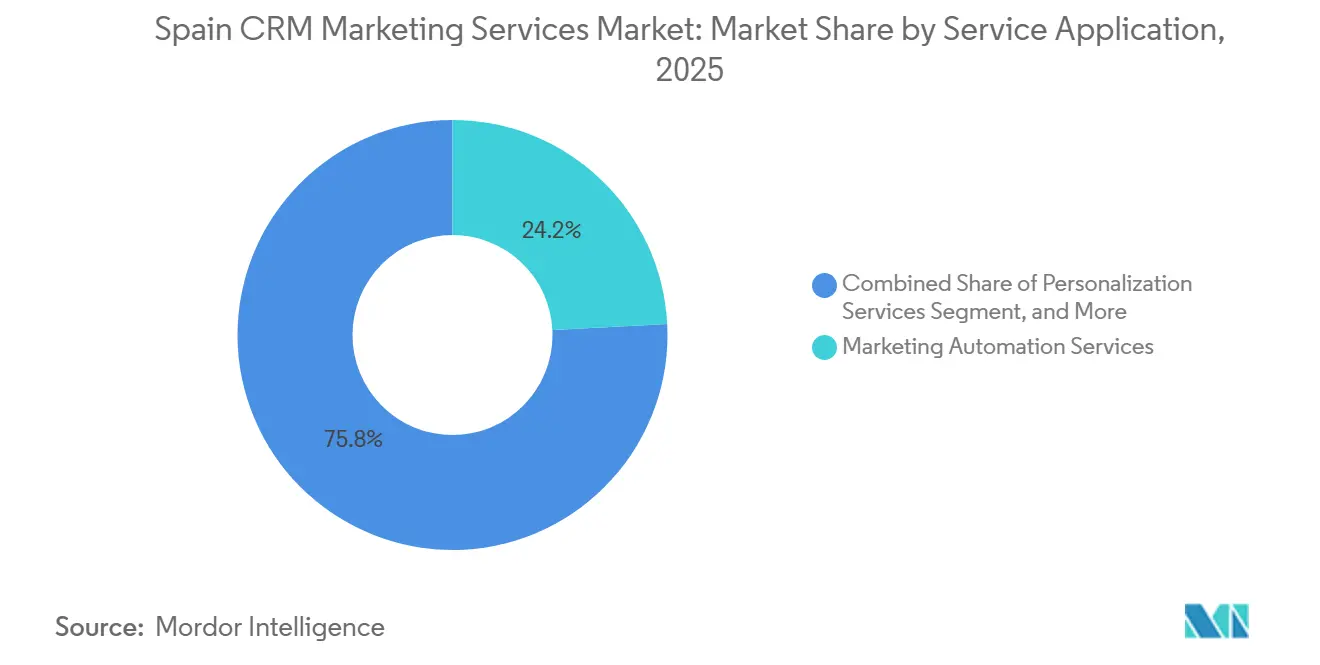

- By service application, marketing automation services led in 2025, while personalization services are projected to expand at a 14.83% CAGR through 2031.

- By end-user industry, BFSI held a 28.74% share in 2025, while retail and e-commerce are projected to expand at a 14.83% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Spain CRM Marketing Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerating SME Digitization and CRM Adoption | +3.2% | National, with concentrated gains in Madrid, Barcelona, Valencia, and Bilbao SME clusters | Short term (≤ 2 years) |

| Rising Demand for Omnichannel Customer Orchestration | +2.8% | National, cross-sector with strongest pull from retail, BFSI, and IT and telecom verticals | Medium term (2-4 years) |

| AI-Driven Personalization and Lead Scoring Use Cases | +2.5% | National, with early gains concentrated in large enterprise and mid-market demand centers | Medium term (2-4 years) |

| Shift Toward First-Party Data and Consent-Ready Marketing | +2.1% | EU-wide, particularly acute in Spain under tightening data protection expectations | Short term (≤ 2 years) |

| Expansion of Cloud-Based Marketing Automation Budgets | +1.9% | National, with spillover into healthcare and government demand | Medium term (2-4 years) |

| WhatsApp and Mobile-First Engagement in Spain | +1.5% | National, with stronger uptake among retail and consumer-facing SMEs | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Accelerating SME Digitization and CRM Adoption

SME digitization remains the strongest demand catalyst for the Spain CRM marketing services market. Programs such as Kit Digital have lowered the first barrier to CRM adoption and made software, setup, and training more accessible to smaller firms. That first installation often creates follow-on demand because businesses then need integration support, user onboarding, and workflow redesign to make the system useful in daily operations. The same pattern matters for the Spain CRM marketing services market because many smaller firms are still early in their digital transition and tend to expand usage after the first deployment proves value. Electronic invoicing rules and broader process digitization are also pushing customer, billing, and communication data closer together, which makes CRM integration more relevant. This is why SME demand is not just a one-time subsidy effect, but a multi-stage service opportunity that can extend from setup into optimization and managed support.

Rising Demand for Omnichannel Customer Orchestration

The Spain CRM marketing services market is also benefiting from a clear shift toward coordinated customer journeys across channels. Buyers no longer view email, messaging, mobile notifications, web activity, and in-store engagement as separate programs, because customers move between them in a single purchase cycle. That change increases the value of CRM service work because orchestration requires data unification, rule setting, and stronger integration between systems. Spain’s active digital and social environment supports this pattern, keeping mobile and social touchpoints at the center of customer engagement plans.[1]IAB Spain, “Estudio De Redes Sociales 2025,” IAB Spain, iabspain.es Retail behavior also reinforces the need for connected campaigns, as online buyers in Spain are already using AI tools during the purchase research stage, underscoring the need for better timing and message consistency across channels. Vendors that can connect these touchpoints into one operating model are likely to win more durable contracts in the Spain CRM marketing services market.[2]IAB Spain, “Estudio Ecommerce 2025,” IAB Spain, iabspain.es

AI-Driven Personalization and Lead Scoring Use Cases

AI is changing what buyers expect from the Spain CRM marketing services market. Enterprises now want CRM systems that can support lead prioritization, tailored messaging, and faster campaign decisions without forcing teams to rebuild their full stack each time. This creates direct demand for service partners because personalization only works well when data models, consent records, and customer identifiers remain clean across platforms. A peer-reviewed European study found that AI personalization programs often fail when consent records or legacy identifiers do not validate properly, underscoring the critical importance of implementation quality in live environments. A bank project highlighted by Capgemini Spain showed that AI-based offer management delivered 3x greater personalization density while reducing operating costs by EUR 750,000 (USD 810,000), which helps explain why buyers continue to invest despite the complexity. As a result, the Spain CRM marketing services market is moving beyond basic automation toward more advanced services tied to AI readiness and data quality.[3]MDPI Administrative Sciences, “AI-Driven Personalization in Marketing Administration, Qualitative Insights From European Professionals,” Administrative Sciences, mdpi.com

Shift Toward First-Party Data and Consent-Ready Marketing

The move toward first-party data is becoming a structural support for the Spain CRM marketing services market. As privacy rules tighten and third-party tracking becomes less reliable, companies are placing greater value on customer information collected directly through owned channels. That change lifts demand for consent capture, preference management, segmentation logic, and data governance inside CRM programs. It also favors service providers that can build compliant workflows into implementation rather than treat compliance as an afterthought. The Spain CRM marketing services market is therefore gaining support from a shift that is both defensive and commercial, because better consent design lowers risk while also improving the quality of audience targeting. Buyers who once relied on broad external lists are now being pushed toward more durable, auditable data practices.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented SME Buying Behavior and Long Sales Cycles | -1.5% | National, most acute in micro-enterprise segments and smaller municipalities | Short term (≤ 2 years) |

| Implementation Talent Gaps In CRM Integration and MarTech Operations | -1.2% | National, with particular severity in Madrid and Barcelona’s competitive technology labor markets | Medium term (2-4 years) |

| Data Privacy, Cookie Loss, and Consent Management Complexity | -0.8% | EU-wide, with heightened importance in Spain | Short term (≤ 2 years) |

| Vendor Lock-In Concerns and Integration Debt | -0.7% | National, most visible in mid-market firms with legacy CRM deployments | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Fragmented SME Buying Behavior and Long Sales Cycles

Fragmented SME buying behavior remains a practical brake on the Spain CRM marketing services market. Smaller firms often enter the category with limited internal ownership, narrow budgets, and an urgent need for fast results, which makes procurement irregular and renewal behavior less predictable. Many projects begin when a grant window opens or a short-term sales issue arises, rather than through a long-planning cycle tied to measurable digital targets. This creates high selling costs for providers because education, configuration, and change management must happen before the customer sees clear value. The Spain CRM marketing services market therefore grows from SME participation, but it also absorbs higher acquisition friction in that same customer group. Providers that depend too heavily on small accounts can see attractive top-line demand but weaker margins and slower contract expansion.

Implementation Talent Gaps in CRM Integration and MarTech Operations

Talent gaps in integration and marketing operations are also slowing execution in the Spain CRM marketing services market. Modern CRM programs now involve customer data layers, AI workflows, compliance controls, campaign logic, and cross-channel activation, which makes delivery far more demanding than a basic software installation. Recent enterprise deployments show how broad these environments have become, especially when customer engagement, analytics, and process integration need to work together from the start. SAP’s April 2026 work with Haleon also showed that enterprises are still building larger, integrated data environments, which increases the level of technical and operational skills required from service partners. When those skills are scarce, timelines stretch, post-deployment adoption weakens, and buyer confidence falls. This means the Spain CRM marketing services market is not only a software opportunity, but also a labor and delivery capability challenge.[4]Salesforce, “Adamed Laboratorios Selects Salesforce Life Sciences For Healthcare Engagement,” Salesforce, salesforce.com

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Integration Work Anchors Revenue While Managed Services Build Recurring Demand

CRM implementation and integration accounted for 33.42% of the Spain CRM marketing services market share in 2025, indicating that current spending remains concentrated in initial deployments, system integration, and platform setup. This pattern fits a market in which many companies are still modernizing their customer engagement infrastructure rather than fine-tuning mature programs. Implementation work remains central because enterprises need CRM platforms to connect with analytics, automation, ecommerce, billing, and service environments before campaign value becomes visible. The Spain CRM marketing services industry is therefore still anchored by technical delivery, even as buyer expectations move toward more strategic outcomes.

Managed services are the fastest-growing service type through 2031, with a CAGR of 13.84%, as organizations that have already deployed the core platform now seek outside help to run, improve, and scale it. That shift is important for the Spain CRM marketing services market because recurring support contracts tend to be more stable than one-time deployment projects. Strategy and consulting remain relevant at the front end, especially when buyers need vendor selection, use-case planning, or operating model design before committing to a larger rollout. Migration and modernization work is also gaining relevance as older on-premise or lightly customized systems struggle to support AI features and cross-channel data activation. Training and support have a smaller revenue base, but they matter more over time because weak user adoption can reduce the return on even well-built CRM programs.

By Enterprise Size: Large Enterprises Lead In Volume While SMEs Set The Growth Pace

Large enterprises commanded 66.81% of the market in 2025, reflecting stronger budgets, deeper CRM maturity, and greater willingness to run multi-layer deployments across major software ecosystems. In practical terms, these buyers are more likely to fund integrations that connect marketing, sales, service, analytics, and compliance functions within a single environment. That keeps them at the center of current revenue for the Spain CRM marketing services market and supports larger average contract values. It also means enterprise reference accounts often shape the buying expectations of the broader Spain CRM marketing services industry.

Small and medium enterprises are the fastest-growing demand pool through 2031, with a CAGR of 13.69%, because entry costs are falling and digitalization support has widened exposure to CRM tools. Affordable SaaS offers have made first-time adoption easier, especially for firms that previously relied on spreadsheets, basic email platforms, or disconnected point solutions. The next step after adoption often involves outside help with campaign setup, segmentation, and reporting, which expands the service opportunity beyond the initial software decision. That is why SME growth matters so much to the Spain CRM marketing services market, even though the customer base can be harder to convert and retain. The same firms that begin with low-cost tools often return later for cleaner integration, better automation, or stronger personalization. This creates a layered growth pattern where small accounts can mature into higher-value service relationships over time.

By Service Application: Automation Leads Today While Personalization Expands The Fastest

Marketing automation services held the largest share in 2025, making it the most established application area in current spending. The strongest demand comes from workflows that are easy to measure, such as welcome journeys, cart recovery, post-purchase communication, and re-engagement campaigns. That makes automation the easiest budget line to defend because finance teams can usually connect it to conversion or efficiency goals more quickly than they can for broader transformation projects. In the Spain CRM marketing services market, automation therefore acts as the most practical entry point for many buyers.

Personalization services are projected to grow at a 14.83% CAGR through 2031, making it the fastest-growing application in the market. This reflects a shift toward real-time content selection, behavioral scoring, and message timing that depends on cleaner customer data and stronger orchestration logic. Capgemini Spain showed how a bank used AI-powered offer management to raise personalization density by 3x while cutting operating costs by EUR 750,000 (USD 810,000), which helps explain why this use case is gaining budget support. At the same time, European evidence shows that personalization can break down when consent and identity records are weak, so execution quality remains a major part of the value proposition. Customer acquisition, retention, and loyalty; campaign management; analytics and insights; and omnichannel engagement remain important because they cover the broader customer lifecycle around which automation and personalization operate.

By End-User Industry: BFSI Holds The Lead While Retail And E-Commerce Gains Speed

BFSI accounted for 28.74% of the market in 2025, making it the largest end-user vertical in terms of current demand. The sector benefits from large stores of first-party customer data, frequent communication needs, and heavier pressure to make outreach traceable and consistent. Those conditions make banks and financial institutions natural buyers of more advanced CRM implementation, governance, and optimization services. The Spain CRM marketing services market therefore continues to draw a large share of its current value from BFSI-led programs, while healthcare and life sciences, IT and telecom, industrial manufacturing, government and public administration, and other industries complete the addressable base.

Retail and e-commerce are the fastest-growing verticals through 2031, with a CAGR of 14.81%, as merchants need faster activation across web, mobile, loyalty, and service touchpoints. Tendam posted record revenue of EUR 1.47 billion (USD 1.59 billion) in the financial year 2025, and that performance supports the case for continued investment in omnichannel customer management and analytics. Spain’s online buyers are also already using AI tools during purchase research, which raises the value of coordinated customer data and timing across channels. Healthcare is also becoming increasingly relevant as specialized deployments move into production, as evidenced by Adamed Laboratorios selecting Salesforce Agentforce Life Sciences in January 2026 to unify commercial processes and healthcare engagement workflows. This mix shows that BFSI still sets the spending baseline, while retail, ecommerce, and specialized regulated sectors are expanding the next wave of demand.

Geography Analysis

The Spain CRM marketing services market size stood at USD 0.64 billion in 2025 and is forecast to reach USD 1.32 billion by 2031, because geography in this study is measured at the country level and all demand is captured within Spain. Even within a single-country scope, demand conditions vary meaningfully by enterprise density, digital maturity, and sector mix. Spain’s digital usage profile supports cloud-led CRM activity because social, mobile, and ecommerce behavior keeps digital customer interaction high across industries. The country also benefits from a wide base of firms still building formal CRM workflows, leaving room for both first-time implementation and second-stage optimization. That combination gives the Spain CRM marketing services market a broad national base rather than a narrow opportunity tied only to top-tier enterprises.

Madrid and Barcelona remain the two main demand centers for the Spain CRM marketing services market. Madrid concentrates a large share of enterprise buying because financial institutions, major service businesses, and national commercial teams continue to operate there at scale. Barcelona is the country’s strongest digital commerce and technology cluster, supporting greater demand for automation, personalization, and integration work. Bilbao and the wider Basque region form an emerging pocket of opportunity where industrial and B2B customer engagement needs are becoming more structured.

Andalusia and Valencia are also important to the Spain CRM marketing services market because they widen the SME opportunity outside the two largest metropolitan hubs. These areas are relevant for lighter implementation, packaged consulting, and training-led projects that fit the needs of smaller firms with earlier CRM maturity. Spain’s mobile and social behavior continues to support these regional opportunities because customer journeys often move through messaging, content, and digital discovery before conversion. Geography, therefore, matters less as a barrier to access than as a signal of which service model, enterprise-grade or SME-focused, is most likely to fit local demand.

Competitive Landscape

The Spain CRM marketing services market remains moderatley consolidated, with global software vendors strong in enterprise platforms and a broad field of regional service providers active in deployment, customization, and support. Salesforce, Microsoft, SAP, Adobe, and HubSpot continue to anchor large-account competition because they offer deep ecosystem integration and recognizable enterprise standards. At the same time, European-origin challengers such as Brevo, Pipedrive, and Odoo appeal to buyers who want leaner pricing, simpler deployment, or a more local operating fit. This mix keeps the Spain CRM marketing services market competitive not only at the software layer, but also in the service layer where implementation quality often shapes renewal value. Buyers frequently choose one platform and a separate integration or managed service partner, which keeps competitive pressure spread across several vendor types.

Strategic moves in 2025 and 2026 show how vendors are trying to strengthen their position in the Spain CRM marketing services market. Salesforce signed a definitive agreement in May 2025 to acquire Informatica for approximately USD 8 billion, a step aimed at improving data management and real-time orchestration capabilities across enterprise CRM environments. Salesforce also made Agentforce 360 generally available in October 2025, which pushed agentic AI capabilities closer to production use across CRM, marketing, service, and commerce workflows. Brevo raised EUR 500 million (USD 583 million) in December 2025 and reported more than EUR 200 million (USD 216 million) in annual recurring revenue, giving it greater scale to challenge larger rivals across Europe. These moves show that platform competition is now centered on data depth, AI readiness, and the ability to support broader activation use cases.

Customer-side deployments also shape how competition plays out in the Spain CRM marketing services market. Adamed Laboratorios selected Salesforce Agentforce Life Sciences in January 2026 to unify commercial processes and customer engagement in a regulated setting, which highlights the growing importance of sector-specific CRM capability. Haleon selected SAP Business Suite in April 2026 to modernize its digital infrastructure, indicating continued demand for integrated data environments rather than isolated campaign tools. White space remains strongest in healthcare, public-sector modernization, and SME-grade personalization services, where buyers need simpler delivery and stronger compliance controls. Providers that can combine implementation discipline, local support, and AI-enabled workflow design are likely to gain more ground as the market expands.

Spain CRM Marketing Services Industry Leaders

Salesforce, Inc.

Adobe Inc.

HubSpot, Inc.

Zoho Corporation Pvt. Ltd.

Oracle Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Haleon, an international consumer healthcare company, selected SAP Business Suite, including SAP Cloud ERP with embedded AI and SAP Business Data Cloud, to modernize its digital infrastructure. Implementation begins in late 2026 and will establish an integrated CRM-marketing data layer for consumer relationship management.

- March 2026: Salesforce launched Headless 360 at its TDX developer event, introducing a headless architecture that allows agentic AI to operate natively across Slack, WhatsApp, and voice interfaces. For Spanish enterprises where WhatsApp is a primary customer engagement channel, Headless 360 meaningfully closes the gap between CRM system-of-record and conversational customer-facing channels.

- January 2026: Salesforce deployed Agentforce Life Sciences for Customer Engagement at Adamed Laboratorios, a Spanish pharmaceutical company. The implementation, led by Salesforce partner Izertis, unifies commercial processes, e-detailing, and healthcare professional relationship management within a single CRM platform.

- December 2025: Brevo SAS raised EUR 500 million (USD 583 million) in equity funding, achieving unicorn status at a valuation exceeding USD 1 billion. The round, backed by eBay, H&M, and Louis Vuitton as key enterprise partners, will fund AI development, US market entry, and acquisitions. Brevo reported surpassing EUR 200 million (USD 216 million) in annual recurring revenue in 2025, with a target of EUR 1 billion (USD 1.08 billion) in annual recurring revenue by 2030.

Spain CRM Marketing Services Market Report Scope

The Spanish CRM (Customer Relationship Management) marketing services market encompasses the range of professional, managed, and support services provided to organizations in Spain to help them strategize, implement, optimize, and maintain CRM systems specifically for marketing functions. This market excludes the actual CRM software licenses or platform subscriptions (SaaS/on-premise), focusing entirely on the human expertise, consulting, and outsourced operations required to leverage these technologies effectively. The services covered include initial CRM strategy and consulting, system implementation and integration with existing marketing stacks, data migration and platform modernization, ongoing managed services, and user training and support. These services are used by businesses of varying sizes across multiple industries to execute specific marketing applications, including customer acquisition, retention, and loyalty programs; campaign management; marketing automation; customer analytics; omnichannel engagement; and hyper-personalization. The market value represents the revenue generated by service providers and agencies operating within Spain for these specific CRM-related marketing engagements.

The Spain CRM Marketing Services Market Report is Segmented by Service Type (CRM Strategy and Consulting, CRM Implementation and Integration, CRM Migration and Modernization, CRM Managed Services, and CRM Training and Support), Enterprise Size (Large Enterprises, and Small and Medium Enterprises), Service Application (Customer Acquisition, Customer Retention and Loyalty, Campaign Management Services, Marketing Automation Services, Customer Analytics and Insights, Omnichannel Customer Engagement, and Personalization Services), and End-user Industry (Banking, Financial Services, and Insurance (BFSI), Healthcare and Life Sciences, Information Technology and Telecom, Retail and E-commerce, Industrial Manufacturing, Government and Public Administration, and Other End-user Industries). The Market Forecasts are Provided in Terms of Value (USD).

| CRM Strategy and Consulting |

| CRM Implementation and Integration |

| CRM Migration and Modernization |

| CRM Managed Services |

| CRM Training and Support |

| Large Enterprises |

| Small and Medium Enterprises |

| Customer Acquisition |

| Customer Retention and Loyalty |

| Campaign Management Services |

| Marketing Automation Services |

| Customer Analytics and Insights |

| Omnichannel Customer Engagement |

| Personalization Services |

| Banking, Financial Services, and Insurance (BFSI) |

| Healthcare and Life Sciences |

| Information Technology and Telecom |

| Retail and E-commerce |

| Industrial Manufacturing |

| Government and Public Administration |

| Other End-user Industries |

| By Service Type | CRM Strategy and Consulting |

| CRM Implementation and Integration | |

| CRM Migration and Modernization | |

| CRM Managed Services | |

| CRM Training and Support | |

| By Enterprise Size | Large Enterprises |

| Small and Medium Enterprises | |

| By Service Application | Customer Acquisition |

| Customer Retention and Loyalty | |

| Campaign Management Services | |

| Marketing Automation Services | |

| Customer Analytics and Insights | |

| Omnichannel Customer Engagement | |

| Personalization Services | |

| By End-user Industry | Banking, Financial Services, and Insurance (BFSI) |

| Healthcare and Life Sciences | |

| Information Technology and Telecom | |

| Retail and E-commerce | |

| Industrial Manufacturing | |

| Government and Public Administration | |

| Other End-user Industries |

Key Questions Answered in the Report

What is the size of the Spain CRM marketing services market?

The Spain CRM marketing services market was valued at USD 0.64 billion in 2025, is estimated at USD 0.71 billion in 2026, and is forecast to reach USD 1.32 billion by 2031 at a 13.20% CAGR.

Which service type leads spending in Spain CRM marketing services?

CRM implementation and integration led spending with a 33.42% share in 2025, showing that deployment, migration, and system connection work still account for a large part of current demand.

Which customer group is driving the fastest expansion in Spain?

Small and medium enterprises are the fastest-growing demand pool through 2031 with CAGR of 13.69%, even though large enterprises still accounted for 66.81% of the market in 2025.

Which application area is growing the fastest?

Personalization services is projected to expand at a 14.83% CAGR through 2031, supported by growing demand for AI-led content, scoring, and real-time message decisions.

Which end-user vertical currently leads demand?

BFSI held the largest end-user share at 28.74% in 2025 because financial institutions have large customer data sets, frequent communication needs, and tighter governance requirements.

What is shaping competition among vendors in Spain?

Competition is centered on data integration, AI readiness, and service execution, with strategic moves such as Salesforces Informatica deal, Agentforce 360 rollout, and Brevos EUR 500 million funding round highlighting where vendors are placing their bets.

Page last updated on: