Spain Alfalfa Hay Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2020 - 2023 |

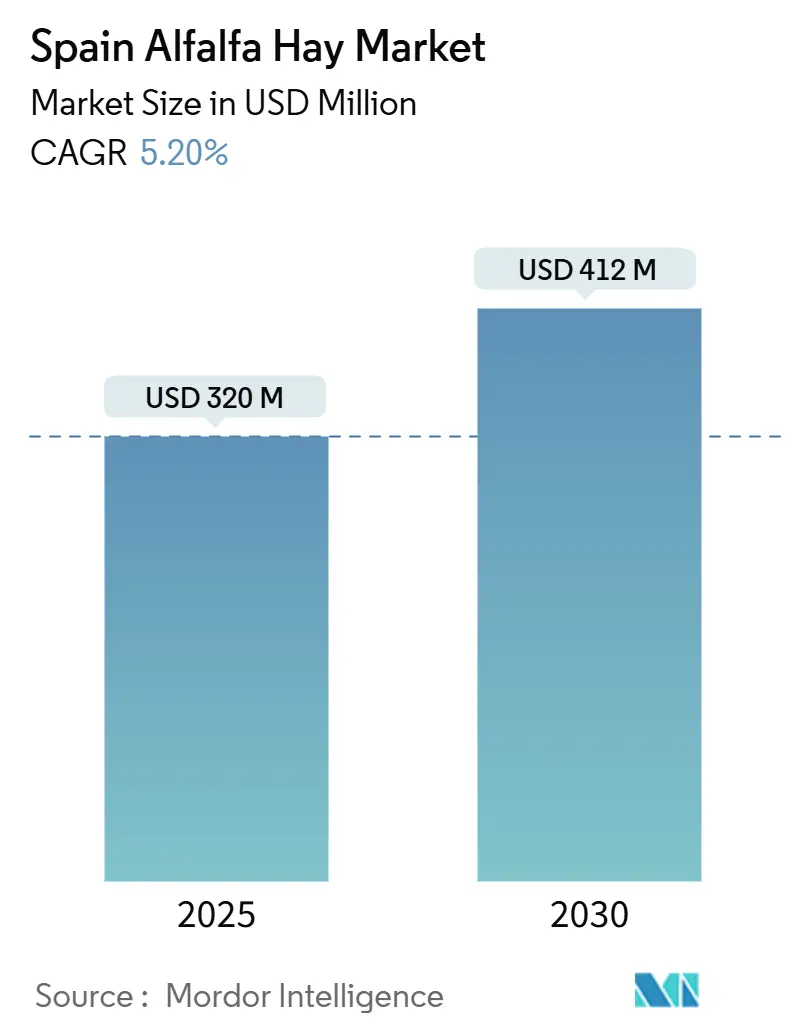

| Market Size (2025) | USD 320 Million |

| Market Size (2030) | USD 412 Million |

| Growth Rate (2025 - 2030) | 5.20% CAGR |

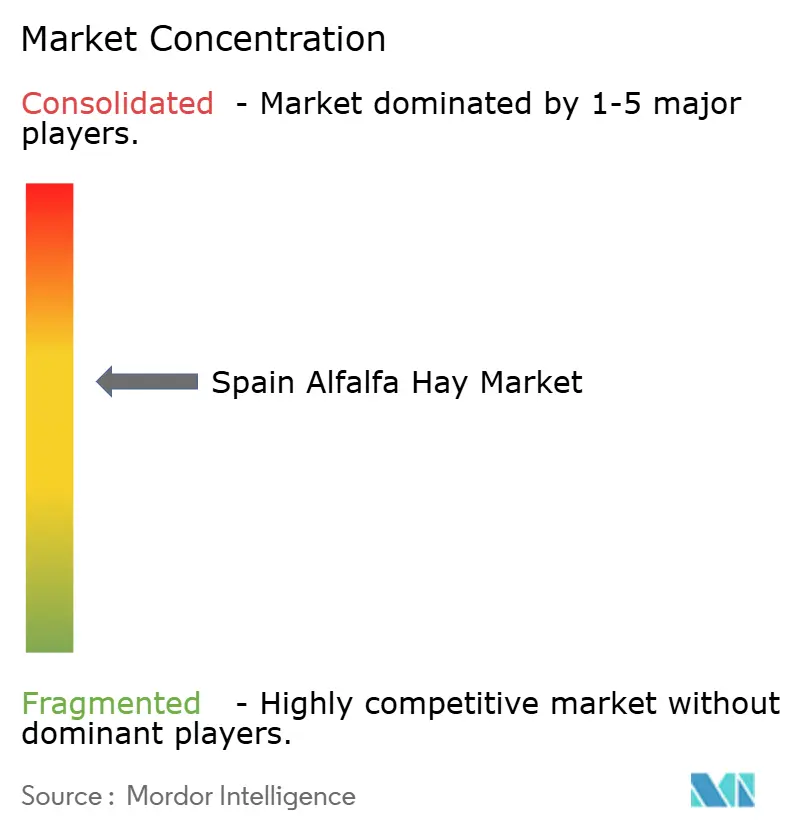

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Spain Alfalfa Hay Market Analysis by Mordor Intelligence

The Spain alfalfa hay market size reached USD 320 million in 2025 and is projected to climb to USD 412 million by 2030 at a 5.20% CAGR, underscoring the resilience of the sector after the 2023 drought episode. Strong local protein demand, European Union Common Agricultural Policy (CAP) eco-scheme incentives, and rapid roll-out of drip irrigation have restored grower confidence. Spain now ranks as Europe’s top alfalfa producer and the world’s third-largest exporter; pellets alone surpassed around 250,000 metric tons in 2024, the highest global share [1]Source: USDA Foreign Agricultural Service, “Grain and Feed Annual: Spain,” FAS.USDA.GOV . Domestic feed integrators increasingly favor dehydrated alfalfa to improve rumen health, poultry pigmentation, and pet-food fiber content. Meanwhile, CAP payments for nitrogen-fixing rotations and soil-carbon pilots are turning environmental services into a secondary revenue stream. Energy costs and water scarcity remain structural headwinds, yet strategic investments in biomass boilers and precision irrigation are narrowing the risk gap.

Key Report Takeaways

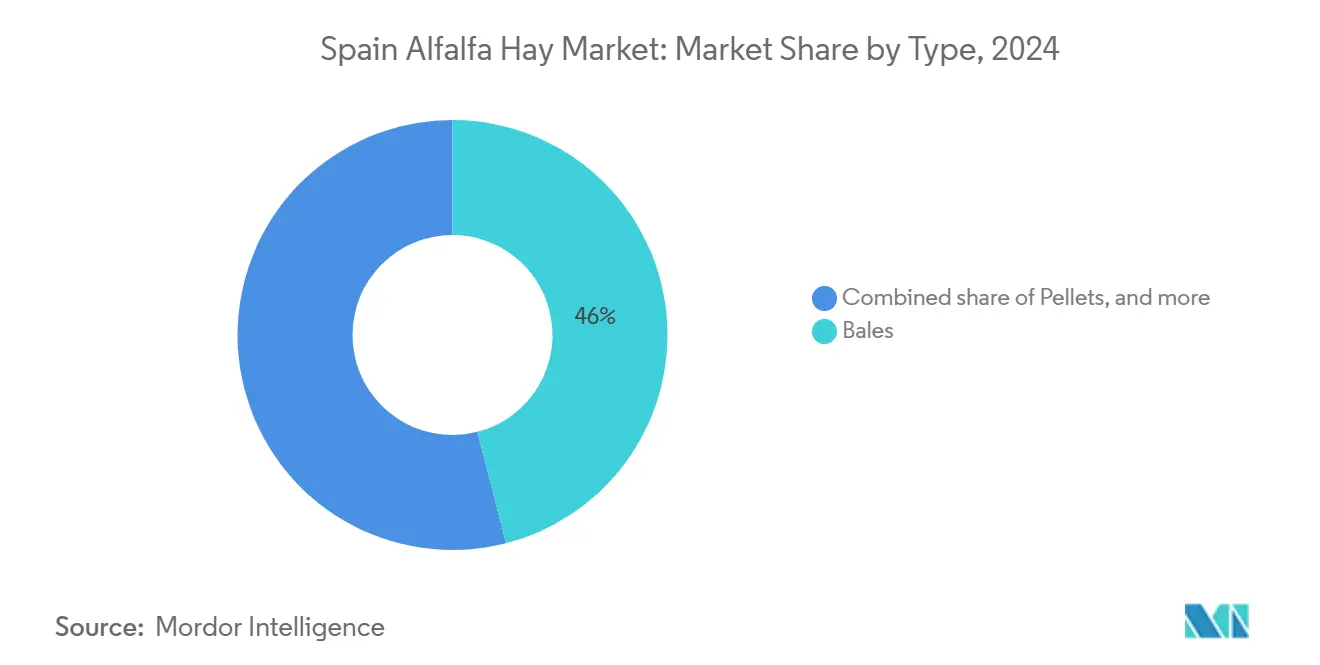

- By type, bales held 46% of the Span Alfalfa Hay Market in 2024, while pellets are forecast to expand at a 6.7% CAGR through 2030.

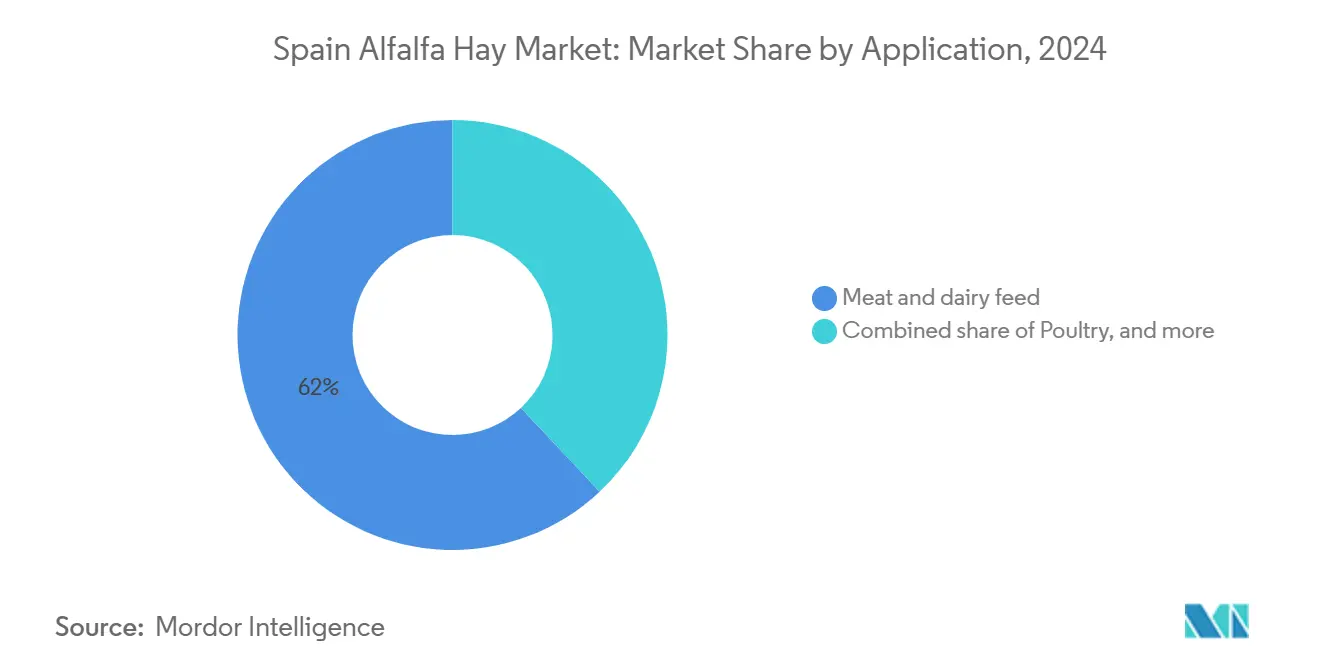

- By application, meat and dairy feed accounted for 62% of the 2024 volume, while poultry feed is advancing at a 7.3% CAGR.

Spain Alfalfa Hay Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising domestic demand for high-protein dairy and cheese products | +1.2% | Castile-and-Leon, Galicia, Asturias | Medium term (2–4 years) |

| Growing live-cattle exports to North Africa | +0.9% | Andalusia, Murcia, Catalonia | Short term (≤ 2 years) |

| EU Common Agricultural Policy (CAP) greening payments favoring forage crops | +0.8% | Aragon, Castile-La Mancha, Navarre | Long term (≥ 4 years) |

| Expansion of water-efficient drip irrigation in semi-arid regions | +0.7% | Andalusia, Castile-La Mancha, Aragon | Medium term (2–4 years) |

| Emerging alfalfa-based functional pet-food market | +0.4% | Madrid, Barcelona, Valencia | Long term (≥ 4 years) |

| Pilot carbon-credit schemes rewarding alfalfa's soil-carbon sequestration | +0.3% | Navarre, Aragon | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Domestic Demand for High-Protein Dairy and Cheese Products

Spain’s specialty cheese and yogurt makers continue to command shelf premiums, so dairy cooperatives are chasing higher milk-protein scores to capture that added value. Nutritionists report that farms in Castile-and-Leon and Galicia have raised per-cow alfalfa inclusion rates by about 9% since 2024 to support those protein targets. Alfalfa offers a 15%–18% crude protein range, plus a strong calcium density, which enhances butterfat yields without increasing concentrate costs. Forward contracts now feature protein-based bonuses, tying farm price directly to feed-quality analytics and further anchoring alfalfa in ration formulations.

Growing Live-Cattle Exports to North Africa

Spanish exporters loaded 5% more cattle and small ruminants through Cadiz, Cartagena and Almeria in the first four months of 2025 than in the same period a year earlier. Each voyage requires fiber-rich rations to keep rumen fill stable and minimize weight loss during the 24- to 48-hour crossing. The trade complies with European Union animal-welfare rules that discourage concentrate-heavy diets while animals are in transit, giving alfalfa a regulatory advantage. Exporters also value alfalfa’s low dust content, which reduces respiratory stress when loading livestock at port facilities.

EU Common Agricultural Policy (CAP) Greening Payments Favoring Forage Crops

Under the 2023-2027 Common Agricultural Policy, Spain earmarked EUR 180 million (USD 195 million) for protein crops, and certified alfalfa hectares rose 9% in Aragon and 8% in Castile-La Mancha during 2024 [2]Source: European Commission, “CAP at a Glance,” EUROPA.EU. Many growers now keep stands in place for five years instead of three to lock in the annual eco-scheme payment, spreading establishment costs across additional harvests. Longer rotations also suppress weed pressure and cut herbicide use, supporting the European Union Farm-to-Fork pesticide-reduction target. Dehydration plants benefit as well, because older stands tend to deliver more uniform stem-leaf ratios that improve pellet quality grades. The policy therefore aligns economic and environmental incentives, reinforcing alfalfa’s position in crop plans even when cereal prices spike.

Expansion of Water-Efficient Drip Irrigation in Semi-Arid Regions

Irrigated alfalfa area reached 90,755 hectares in 2024, a 9% year-on-year gain, with drip systems accounting for 42% of new installations. Public subsidies cover up to 60% of hardware costs, trimming payback to fewer than four seasons at current hay prices. Drip lines cut water use by 30%–40% versus flood methods yet still support yields of 12–14 metric tons of dry matter per hectare. Andalusian growers now achieve three reliable cuts even in below-average rainfall years, which has attracted procurement contracts from dehydration plants seeking stable throughput. The technology lowers weed incidence because foliage stays dry, making late-season harvests cleaner and reducing foreign-matter penalties.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile electricity and natural-gas prices for dehydration plants | −0.8% | Aragon, Castile-La Mancha | Short term (≤ 2 years) |

| Recurrent droughts in Ebro and Guadalquivir basins | −1.1% | Aragon, Andalusia, Catalonia | Medium term (2–4 years) |

| Rising competition from soybean meal imports | −0.5% | National poultry and pig sectors | Medium term (2–4 years) |

| Fragmented farm structure limiting economies of scale | −0.4% | Castile-and-Leon, Extremadura | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatile Electricity and Natural-Gas Prices for Dehydration Plants

Spain’s 33 dehydration facilities require up to 1.5 MWh of energy to turn one tonne of fresh forage into export-grade pellets, so power and gas swings immediately squeeze margins. Iberian spot electricity averaged EUR 85 (USD 92) per MWh in early 2025, still 40% above pre-2021 norms despite recent easing, while industrial natural-gas held near EUR 35 (USD 38) per MWh. Large processors are installing biomass boilers that burn almond shells and olive pits, cutting fossil-gas use by as much as 60% and unlocking renewable-energy subsidies, yet the EUR 800,000–EUR 1.2 million (USD 865,000–USD 1.3 million) capital cost sidelines many mid-tier plants [3]Source: Asociación Española de Fabricantes de Alfalfa Deshidratada, “Production Statistics,” AEFA.ES . Until energy hedging tools or on-site renewables become widespread, profit volatility will continue to constrain expansion plans and discourage speculative capacity additions.

Recurrent Droughts in Ebro and Guadalquivir Basins

Reservoir storage fell to 58% of capacity in the Ebro basin and 42% in the Guadalquivir basin during spring 2025, forcing a 15% cut in irrigation water and triggering yield losses of up to 30% in some districts. The 2023 drought pushed national production down to 980,000 tonnes, the weakest level in a decade, and underscored the sector’s climate exposure. Growers are trialing drought-tolerant cultivars and deficit-irrigation schedules, but these methods need multi-year validation before they can offset extreme rainfall deficits. Persistent hydrological stress raises financing costs for new dehydration lines, because lenders now scrutinize water-security metrics alongside traditional credit ratios.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Bales Dominate, Pellets Accelerate

Bales held 46% of 2024 revenue in the Spain alfalfa hay market, supported by long-standing dairy usage. Pellets are set for a 6.7% CAGR, the fastest among formats, thanks to poultry reformulation and Middle Eastern demand; pellet exports hit 252,000 metric tons in 2024. The Spain alfalfa hay market size for pellets could capture 38% of total value by 2030 if current trajectories hold. Pellets deliver bulk densities near 700 kg per m³ versus 150 kg for bales, cutting freight cost per metric tons by roughly two-thirds. Nafosa specifies 15%–18% protein and under 12% moisture for export-grade 6 mm pellets, enabling substitution for soybean meal in poultry rations.

Technological gains in dehydration efficiency and particle-size control have lowered processing energy by 15% since 2022, improving pellet margins even amid volatile electricity tariffs. Bales, while still dominant, face logistic disadvantages on long export hauls. Cubes represent a premium niche aimed at equine nutrition, whereas chopped alfalfa finds modest uptake in organic dairy systems. Overall, dehydrated formats accounted for 76.1% of 2024 production, underscoring Spain’s energy-intensive comparative advantage.

By Application: Dairy Leads, Poultry Surges

Meat and dairy feed accounted for 62% of 2024 consumption. The Spain alfalfa hay market size tied to poultry feed is forecast to expand at a 7.3% CAGR through 2030, outpacing all other segments. Poultry integrators leverage alfalfa’s xanthophylls to deepen yolk color and improve broiler skin tone. Horse feed maintains a steady 8%–10% share, buoyed by Andalusia’s equestrian cluster and Catalonia’s recreational market, where low-dust cubes trade at EUR 300–EUR 350 (USD 325–USD 379) per tonne.

Dairy growth hinges on per-cow intake rather than herd expansion, given the plateau at 850,000 cows. Integrators blending alfalfa with corn silage report fewer cases of ruminal acidosis, supporting feed stability premiums. Functional pet-food recipes absorb only single-digit volumes but return high margins, validating the development of micro-pellets.

Geography Analysis

Aragon achieved a modest production share in 2024 thanks to 60,000 irrigated hectares and a dense processor network that ships pellets from Zaragoza to Barcelona for export within 24 hours. Four cuts per season yield up to 14 metric tons of dry matter per hectare, although rising energy costs prompted EUR 90 million (USD 97 million) in electricity expenditure in 2024, accelerating biomass boiler retrofits.

Castile-La Mancha and Castile-and-Leon held nearly half of the national output but face water shortages from the Tagus and Duero rivers. Contract-farming pilots guarantee minimum prices if growers adopt drip irrigation, aiming to add 3,000 hectares by 2028. Land costs of EUR 8,000–EUR 10,000 (USD 8,650–USD 10,800) per hectare draw new entrants despite irrigation uncertainty.

Andalusia’s growing season supports five cuts, and its proximity to Cadiz and Almeria reduces lead times to North Africa. Guadalquivir storage level at 42% in spring 2025 highlights a hydrological risk. Navarre leverages precision-irrigation controllers that match water delivery to real-time soil-moisture data, boosting yields in carbon-credit pilot zones. Catalonia, Extremadura, and Murcia collectively supply roughly 8% but show latent upside as processors scout new plant sites.

Competitive Landscape

Spain’s alfalfa hay sector remains moderately concentrated, with the five largest suppliers accounting for almost half of the total revenue, a level that translates to a concentration score of 6 on a 10-point scale. Nafosa retains its edge as the country’s largest dehydrated alfalfa processor within the Sanlucar Group. Anderson Hay and Grain follows, channeling imports through Valencia port and maintaining long-standing ties with dairy cooperatives in Castile-and-Leon. Al Dahra Agriculture secures a major share by running 17 processing lines nationwide and piloting drip-irrigation programs that deliver uniform forage quality. Alfalfa Monegros and Cubeit Hay Company round out the leading tier, both specializing in compressed formats that maximize container payloads for Middle Eastern buyers.

Competitive focus is shifting toward vertical integration and energy resilience. Smaller cooperatives are installing biomass boilers fueled by almond shells and olive pits that can displace up to 60% of fossil-gas demand while unlocking renewable-energy subsidies. Rising power prices have accelerated these retrofits, positioning energy-efficient plants to widen margin gaps over older dehydration lines. Al Dahra’s network approach reduces transportation miles between fields and plants, while Anderson Hay and Grain experiments with forward contracts that guarantee growers stable returns over multi-year cycles. Nafosa invests in near-infrared spectroscopy to analyze protein and fiber in real time, a move that cuts batch variability and supports price premiums in export markets.

Several white-space segments are opening. Dehydrated alfalfa for functional pet food fetches a 15% to 20% premium over standard livestock pellets because buyers demand stricter microbial limits. Voluntary carbon-credit schemes in Navarre and Aragon pay growers EUR 18 (USD 19.50) per verified metric ton of carbon dioxide equivalent, adding a fresh revenue layer that favors early adopters. Digital platforms are starting to aggregate smallholder volumes and record blockchain traceability, a feature valued by Gulf importers that insist on verifiable sustainability data. Fragmented farm ownership still leaves plenty of room for consolidation, and international traders are testing contract-farming models in Aragon and Castile-La Mancha that bundle agronomic advice with minimum-price guarantees. The players that marry low-carbon processing, traceable supply chains and grower support services are poised to gain share over the next five years.

Spain Alfalfa Hay Industry Leaders

Nafosa S.A.

Anderson Hay and Grain Co., Inc.

Al Dahra Agriculture LLC

Alfalfa Monegros S.L.

Cubeit Hay Company LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Cibus and S and W Seed Company obtained United States Food and Drug Administration clearance for their altered-lignin gene-edited alfalfa trait, paving the way for commercial launch of two new varieties that promise improved digestibility and greater harvest-timing flexibility.

- October 2024: Nafosa confirmed it will showcase its forage portfolio at the Saudi Agriculture Exhibition in Riyadh, set for 21–24 October 2024, and invited clients to schedule meetings through its online platform.

Spain Alfalfa Hay Market Report Scope

| Bales |

| Pellets |

| Cubes |

| Chopped Alfalfa |

| Pelleted-Timothy Mix |

| Dehydrated Alfalfa |

| Meat and Dairy Animal Feed |

| Poultry |

| Horse Feed |

| Other Animal Types (Rabbits, Goats, etc.) |

| By Type | Bales |

| Pellets | |

| Cubes | |

| Chopped Alfalfa | |

| Pelleted-Timothy Mix | |

| Dehydrated Alfalfa | |

| By Application | Meat and Dairy Animal Feed |

| Poultry | |

| Horse Feed | |

| Other Animal Types (Rabbits, Goats, etc.) |

Key Questions Answered in the Report

How large is the Spain alfalfa market in 2025?

It is valued at USD 320 million and projected to grow to USD 412 million by 2030 at a 5.20% CAGR.

Which product type is expanding fastest?

Pellets are advancing at a 6.7% CAGR through 2030 due to demand from poultry integrators and Middle Eastern importers.

How are energy prices affecting processors?

High power and natural-gas costs spur biomass boiler investments that can lower fossil-fuel use by up to 60%.

Who leads the Spain alfalfa market?

Nafosa holds maximum share, followed by Anderson Hay and Grain, Grupo Oses, Al Dahra Agriculture and Alfalfa Monegros.

Page last updated on: