Sovereign Fiber Backbone Infrastructure Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 34.20 Billion |

| Market Size (2031) | USD 64.10 Billion |

| Growth Rate (2026 - 2031) | 13.39% CAGR |

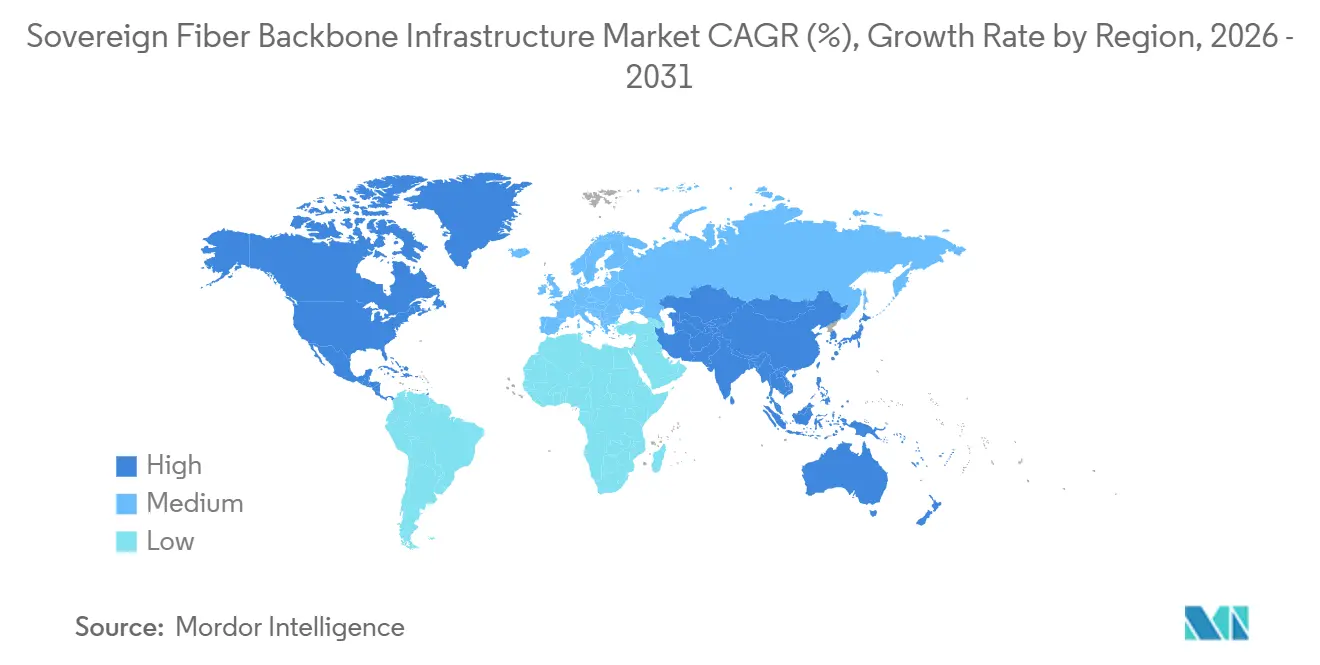

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Sovereign Fiber Backbone Infrastructure Market Analysis by Mordor Intelligence

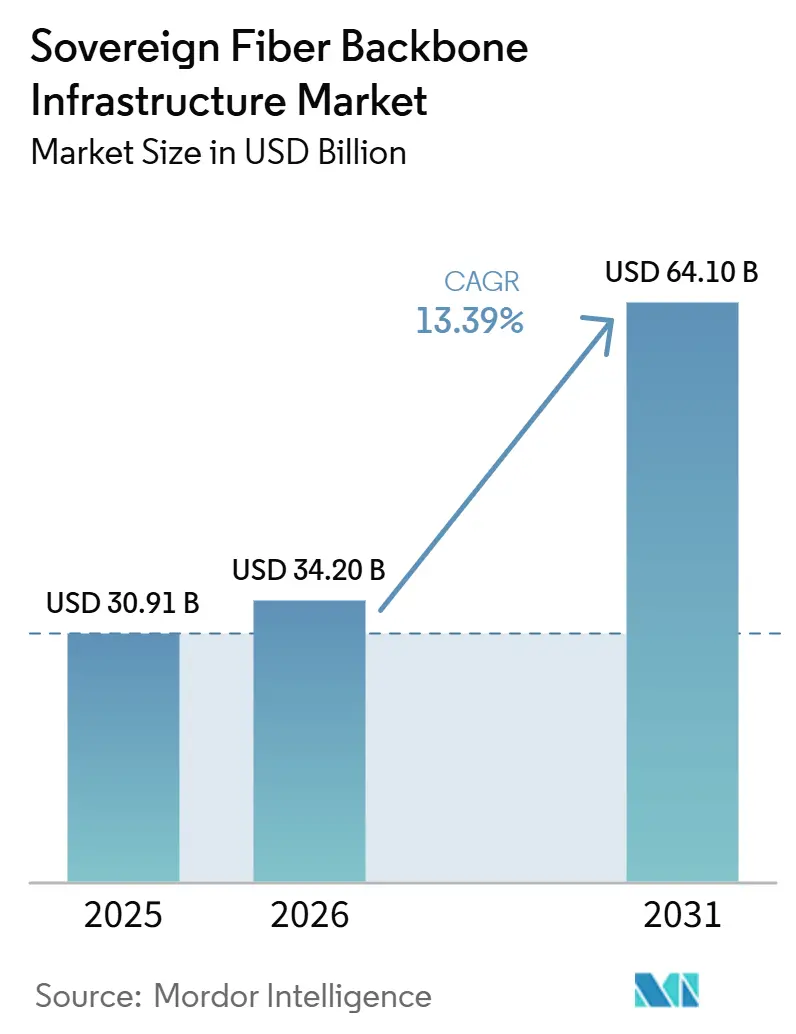

The sovereign fiber backbone infrastructure market size was valued at USD 30.91 billion in 2025 and is expected to reach USD 34.20 billion by 2028, and USD 64.10 billion by 2031, registering a CAGR of 13.39% over 2026-2031. The sovereign fiber backbone infrastructure market is expanding as governments shift data sovereignty from policy to network procurement, driving demand for domestic long-haul routes, secure landing points, and controlled optical capacity. The same sovereign fiber backbone infrastructure market is also being boosted by AI corridor development, as hyperscale data center growth increases demand for dense, low-latency backbone links between compute clusters, metro nodes, and intercity routes. International traffic rerouting is adding another layer of demand, as repeated disruptions around exposed maritime chokepoints are pushing buyers to favor route diversity, alternate overland paths, and new subsea alignments. Capital deployment in the sovereign fiber backbone infrastructure market is becoming more concentrated as state and commercial cloud demand converge in the same investment window, benefiting operators and suppliers that can scale quickly. Competitive positioning is therefore shifting toward vendors with security clearances, installation capacity, and proven delivery records, while opportunities remain strongest where governments want local control and hyperscalers need new capacity on routes that legacy networks did not build for current workloads.

Key Report Takeaways

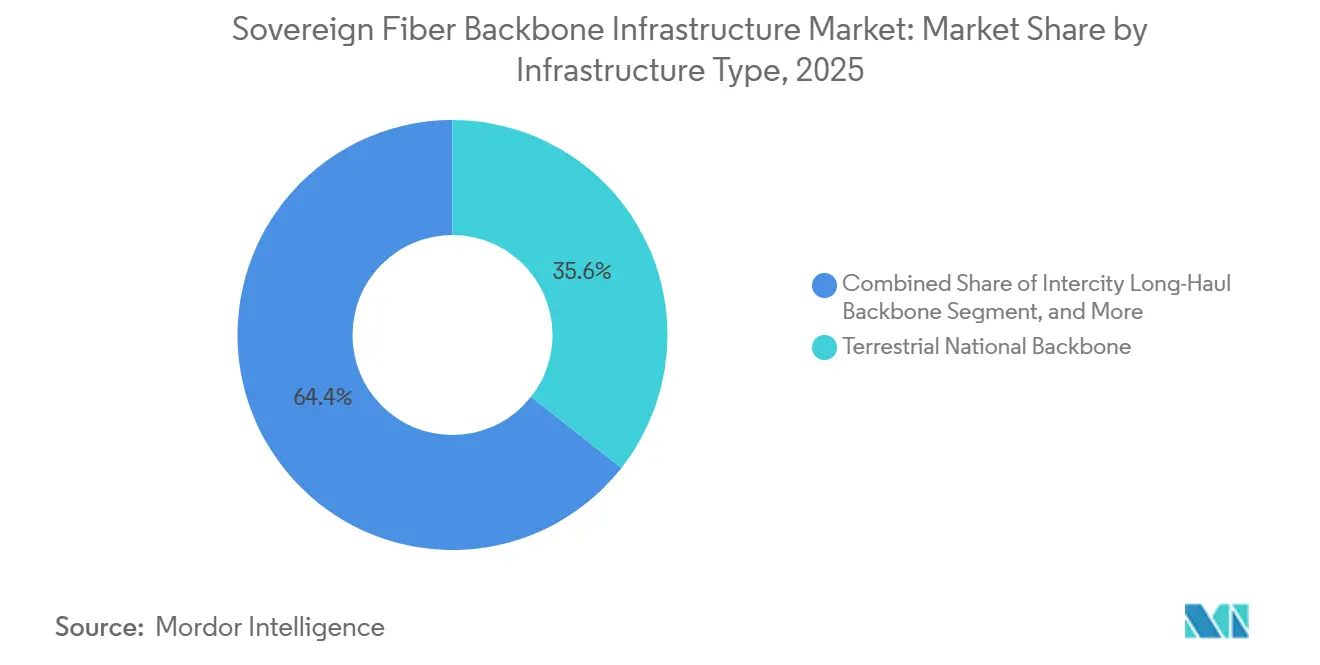

- By infrastructure type, terrestrial national backbone accounted for 35.61% share of the sovereign fiber backbone infrastructure market size in 2025, while subsea and cross-border backbone routes are projected to expand at a 14.76% CAGR through 2031.

- By deployment architecture, dark fiber held 41.21% of the sovereign fiber backbone infrastructure market share in 2025, while hybrid fiber and wave services are projected to expand at a 15.31% CAGR through 2031.

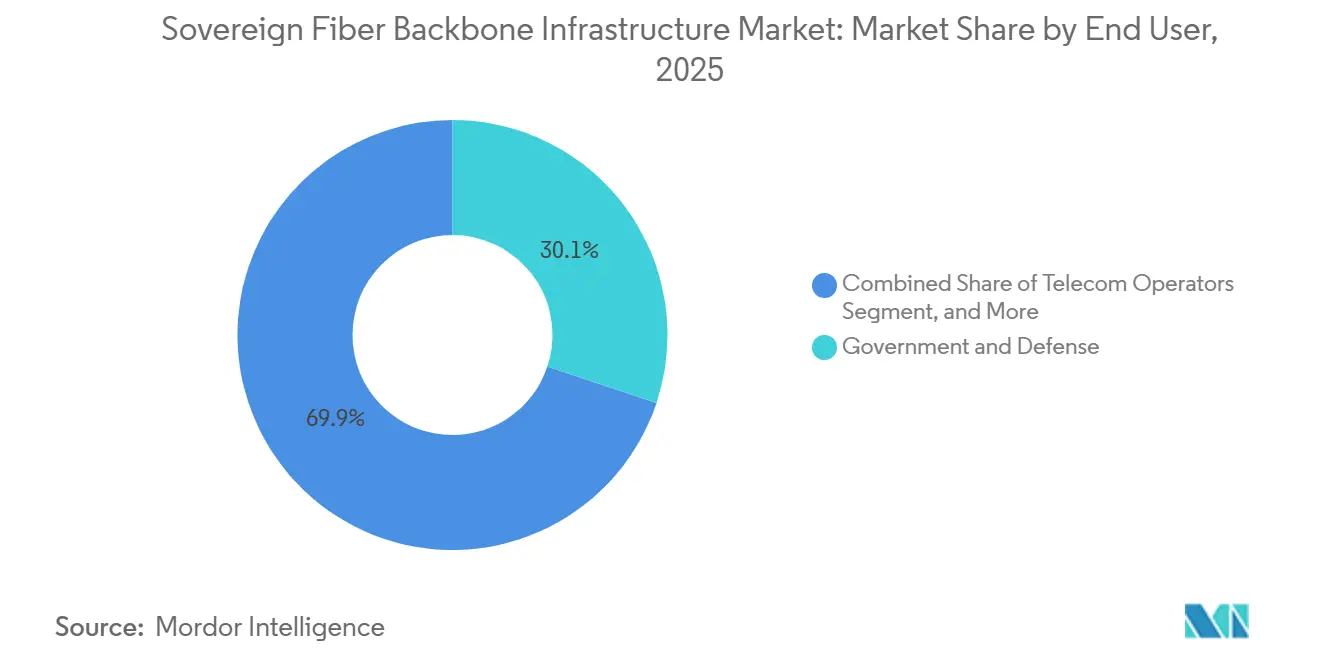

- By end user, government and defense accounted for 30.12% share of the sovereign fiber backbone infrastructure market size in 2025, while cloud and hyperscale data centers are projected to advance at a 14.66% CAGR through 2031.

- By geography, North America held 22.31% of the sovereign fiber backbone infrastructure market share in 2025, while Asia-Pacific is projected to grow at a 15.11% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Sovereign Fiber Backbone Infrastructure Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| National Data Sovereignty Laws Accelerate Domestic Backbone Buildouts | +3.2% | Global, with early concentration in Europe, India, Southeast Asia, and the Gulf states | Medium term (2-4 years) |

| AI And Data Center Corridor Growth Raise Demand For Low-Latency Fiber Backbones | +3.0% | North America is primary, with spillover to the Asia Pacific and Europe | Short term (≤ 2 years) |

| Hyperscaler And Cloud Interconnect Needs Push Long-Haul Capacity Expansion | +2.5% | North America and Europe core, expanding to the Asia Pacific and the Middle East | Short term (≤ 2 years) |

| Defense, Critical Infrastructure, And Public Sector Segmentation Increase Demand For Controlled Fiber Routes | +1.7% | North America, Europe, and select Asia Pacific defense markets | Medium term (2-4 years) |

| Geopolitical Route Diversification Away From Chokepoints Reduces Reliance On Foreign Transit | +1.3% | Middle East and Africa, South Asia, and East Africa corridor | Medium term (2-4 years) |

| Open-Access Backbone Policies Improve Asset Utilization And Anchor Tenant Economics | +0.8% | EU, APAC national broadband markets, select South American states | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

National Data Sovereignty Laws Accelerate Domestic Backbone Buildouts

The sovereign fiber backbone infrastructure market is seeing a direct shift from broad localization rules to procurement-led network buildouts, especially where governments want more control over where sensitive traffic lands and how it is routed. This is increasing demand for nationally controlled backbone assets rather than reliance on transit arrangements that pass through third-party jurisdictions. In the sovereign fiber backbone infrastructure market, this changes route planning because public buyers increasingly favor domestically landed fiber and controlled backbone segments for sensitive workloads. It also creates scarcity in high-security dark fiber and exclusive route capacity, which supports stronger lease pricing and favors operators that already hold local permits, rights-of-way, and trust with state buyers. At the same time, international coordination on cable resilience and permit processing has risen on the policy agenda, which supports a more formal regulatory backdrop for sovereign network planning.[1]International Telecommunication Union, “International Advisory Body For Submarine Cable Resilience,” ITU, itu.int

AI And Data Center Corridor Growth Raise Demand For Low-Latency Fiber Backbones

The sovereign fiber backbone infrastructure market is being reshaped by AI workload growth, as distributed compute clusters require lower-latency links across metro and intercity corridors than older enterprise traffic patterns demanded. Corning reported 36% year-over-year growth in the Optical Communications segment revenue in Q1 2026, underscoring how quickly fiber demand has risen with AI infrastructure deployment.[2]Corning Incorporated, “Optical Communications Results And AI Fiber Supply Agreement Updates,” Corning, corning.comCorning also signed a USD 6 billion supply agreement with Meta in January 2026 for AI-grade optical fiber, which reflects the scale of backbone and interconnect requirements now attached to large AI programs. In the sovereign fiber backbone infrastructure market, power constraints are also spreading AI capacity across more regional campuses, which increases the number of interconnect paths needed per deployment rather than reducing them. That pattern supports sustained demand for low-latency long-haul routes, metro rings, and optical upgrades across the routes that link high-density compute clusters.

Hyperscaler And Cloud Interconnect Needs Push Long-Haul Capacity Expansion

The sovereign fiber backbone infrastructure market is also benefiting from a clear shift in hyperscaler buying behavior, as large cloud operators are no longer relying solely on third-party wavelength capacity and are increasingly backing dedicated route expansion. Zayo announced a major AI-focused build program in April 2026 with an anchor customer commitment across 8,000 route miles of new construction, marking the largest such commitment in the company’s history.[3]Zayo Group, “AI Route Expansion And Anchor Customer Commitment,” Zayo, zayo.comLumen said it was targeting 47 million intercity fiber miles by 2028, up from 16.6 million at the end of 2025, after adding more than 5.9 Pbps of network capacity during 2025.[4]Lumen Technologies, “Intercity Fiber Expansion And Network Capacity Growth,” Lumen, lumen.com In the sovereign fiber backbone infrastructure market, these anchor commitments matter because routes backed early by hyperscaler demand attract capital faster and support longer contract terms than routes that remain uncommitted. This is creating a pricing split between preferred AI corridors and standard long-haul routes, strengthening the position of operators that secured demand before competing builds entered those corridors.

Defense, Critical Infrastructure, And Public Sector Segmentation Increase Demand For Controlled Fiber Routes

The sovereign fiber backbone infrastructure market is gaining support from defense and public-sector modernization, as mission-critical networks are moving away from older copper and mixed transport stacks toward more controlled optical architectures. The US Air Force’s 2025 Network of the Future strategy identified dark fiber and 5G as key transport modes for future connectivity upgrades, underscoring the centrality of secure fiber to defense network planning.[5]United States Air Force, “Network Of The Future Strategy,” U.S. Air Force, af.mil In the sovereign fiber backbone infrastructure market, this preference supports dark fiber and encrypted wavelength models, enabling end users to maintain tighter control over traffic handling, route diversity, and security policy. The same pattern is spreading into utilities and other critical infrastructure operators as operational networks and IT systems become more closely linked and require higher-capacity, lower-latency transport. That broadens the demand base beyond defense alone and helps keep backbone investment active across public networks, utility corridors, and state-controlled infrastructure systems.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| High Upfront Civil Works and Permitting Complexity Slow Time to Revenue | -2.9% | North America, Europe, with spillover to the Asia Pacific urban corridors | Short term (≤ 2 years) |

| Cross-Border Coordination and Landing Rights Delays Increase Project Risk | -1.6% | Global, acute in the Middle East, Africa, and South Asia | Medium term (2-4 years) |

| Fiber Cut Exposure, Right-Of-Way Theft, And Physical Security Risks Raise Operating Cost | -1.0% | Middle East and Africa, South and Southeast Asia, and Eastern Europe | Medium term (2-4 years) |

| Sovereign Procurement Rules Can Limit Vendor Flexibility and Raise Lifecycle Cost | -0.7% | Global, most acute in Europe, and high-security government markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Upfront Civil Works and Permitting Complexity Slow Time To Revenue

The sovereign fiber backbone infrastructure market continues to face pressure from the intensity of civil works, as trenching, crossings, attachments, and route approvals still account for a large share of project costs and schedule risk. When multiple national and regional programs move simultaneously, contractor availability and agency review capacity become bottlenecks even before physical construction reaches peak activity. The FCC proposed a 120-day deadline for processing right-of-way authorization requests in June 2026, indicating that regulatory bodies are treating approval delays as a structural issue. In the sovereign fiber backbone infrastructure market, the effect of slow approvals is a longer wait between capital commitment and revenue generation, which raises financing pressure on multi-jurisdiction backbone builds. That challenge is strongest on long-haul routes, where a single unresolved permit can delay entire segments and force changes to network sequencing, contractor deployment, and customer activation.

Cross-Border Coordination and Landing Rights Delays Increase Project Risk

The sovereign fiber backbone infrastructure market also faces a distinct cross-border risk, as international backbone projects require layered approvals that do not proceed on a single schedule. Subsea and cross-border systems can depend on landing permits, national security reviews, treaty-level coordination, and later-stage repair permissions, all of which create timing risk for investors and operators. The ITU’s International Advisory Body for Submarine Cable Resilience was formed in 2024 and, in early 2026, moved toward recommendations encouraging governments to streamline repair and coordination processes. In the sovereign fiber backbone infrastructure market, this matters because the regions that need route diversification most often have the most complex approval requirements for new overland and maritime routes. As a result, projects designed to reduce dependence on exposed chokepoints can still be delayed by the political and administrative burdens associated with the alternative routes themselves.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Infrastructure Type: Subsea Expansion Adds New Weight To National Backbone Networks

Terrestrial national backbone accounted for 35.61% of revenue in 2025, making it the largest infrastructure type in the sovereign fiber backbone market. This leading position reflects state-funded broadband programs, national carrier upgrades, and the continued use of railway and public utility corridors as cost-efficient backbone deployment rights-of-way. The sovereign fiber backbone infrastructure market still depends heavily on terrestrial assets because they provide the domestic control that governments want for public services, defense communications, and high-priority digital traffic. NEC Corporation and Nokia were selected in February 2026 to expand Eletronet’s optical backbone across Brazil by 8,000 kilometers, taking the system to 25,000 kilometers across 23 states with up to 1.2 Tb/s per optical channel.

The subsea and cross-border backbone segment is projected to grow at a 14.76% CAGR through 2031, making it the fastest-growing infrastructure type in the sovereign fiber backbone market. This growth reflects the need for route diversity as governments and operators try to reduce exposure to congested or geopolitically sensitive transit paths. In the sovereign fiber backbone infrastructure industry, this shift is important because route design is no longer only a resilience question and is increasingly treated as a matter of strategic control over traffic movement and landing jurisdiction. That is why sovereign buyers are accepting higher complexity and cost when new cable paths help them avoid specific bottlenecks or reliance on politically exposed corridors. The result is a more durable investment case for subsea and cross-border routes than traditional commercial return models alone would suggest.

By Deployment Architecture: Dark Fiber Stays In Front While Hybrid Models Gain Speed

Dark fiber accounted for 41.21% of the deployment architecture segment in 2025, making it the largest architecture in the sovereign fiber backbone infrastructure market. This position reflects the strong preference of governments, defense agencies, and hyperscalers for exclusive fiber strands where they can control encryption, monitoring, and operating policy themselves. The sovereign fiber backbone infrastructure market continues to favor dark fiber where route control matters more than managed service convenience, especially for classified, regulated, or strategically sensitive traffic. That preference is reinforced by defense modernization priorities that place more value on physically separated transport and stronger control of optical assets. Lit fiber services remain important because they offer a practical option for enterprises and telecom operators that need capacity but do not require full-strand ownership.

Hybrid fiber and wave services are forecast to expand at a 15.31% CAGR through 2031, which makes them the fastest-growing architecture in the sovereign fiber backbone infrastructure market. This rise reflects growing demand from buyers who want high-performance wavelengths and strong service levels without assuming the full maintenance burden of dark fiber operations. Ciena said in January 2026 that its WaveLogic 6 Extreme technology was being deployed with Trans Pacific Networks on the Echo and Tabua submarine systems at 1 Tb/s per wavelength. In the sovereign fiber backbone infrastructure market, that improvement matters because wavelength performance is moving closer to what many customers once expected only from fully controlled dark fiber. As these optical platforms spread across backbone routes, hybrid models should remain attractive to sovereign operators that want control and performance while also needing faster deployment and lower upfront capital commitments.

By End User: Government Demand Holds The Base While Hyperscalers Set The Pace

Government and defense accounted for 30.12% of revenue in 2025, making them the largest end-user segment in the sovereign fiber backbone infrastructure market. This position comes from national backbone contracts, classified network modernization, and the continued use of state-controlled assets in transport, utility, and public communications systems. The sovereign fiber backbone infrastructure market remains anchored by this segment because government-led demand is long-cycle, security-driven, and tied to essential infrastructure rather than short-term traffic trends. Public agencies also continue to favor dark fiber or tightly controlled wavelength models where traffic sensitivity limits the use of shared commercial networks. Telecom operators and enterprise buyers remain important, but their procurement logic is more commercial and does not shape route ownership in the same way as public sector mandates.

Cloud and hyperscale data centers are projected to grow at a 14.66% CAGR through 2031, making them the fastest-growing end-user segment in the sovereign fiber backbone infrastructure market. Their expansion reflects a shift from isolated point-to-point connectivity to denser interconnect meshes among compute clusters, storage nodes, and metro access points. Verizon announced in 2025 an agreement with Amazon Web Services to deploy long-haul, high-capacity fiber routes between AWS data center locations, demonstrating how hyperscaler commitments are now directly influencing backbone investment decisions. In the sovereign fiber backbone infrastructure market, utilities and other critical infrastructure operators are also becoming more relevant as grid digitalization increases the need for high-capacity backbone links at transmission and operations sites. That broadens the customer mix and supports continued investment across routes that combine public utility demand, enterprise-grade resilience, and hyperscaler-scale bandwidth needs

Geography Analysis

North America accounted for 22.31% of revenue in 2025, making it the largest regional segment in the sovereign fiber backbone infrastructure market. This position reflects the region’s concentration of hyperscaler capital spending, AI corridor development, and a stronger policy focus on secure domestic routing for strategic digital infrastructure. Zayo completed 100% 400G enablement of its North American core network in July 2025 and also advanced new long-haul AI routes, including a 385-mile Chicago-to-Columbus build. The sovereign fiber backbone infrastructure market in North America also benefits from Canada’s digital sovereignty efforts and Mexico’s role as a transboundary corridor for nearshoring, data center growth, and cross-border traffic demand.

South America is entering a new investment phase in the sovereign fiber backbone infrastructure market, as the focus shifts from simple connectivity expansion toward AI, data center interconnect, and high-capacity optical upgrades. Brazil stands out in this transition as Eletronet’s network expansion with NEC Corporation and Nokia adds scale, reach, and higher channel performance to a backbone platform aimed at hyperscaler and data center demand. Europe is also building momentum in the sovereign fiber backbone infrastructure market through coordinated backbone and submarine connectivity programs backed at the regional level. This matters because pan-European funding and policy coordination favor larger platforms over isolated national deployments. The result is a stronger foundation for sovereign connectivity, enabling regional interoperability and route resilience to be improved simultaneously.

Asia-Pacific is projected to expand at a 15.11% CAGR through 2031, which makes it the fastest-growing regional segment in the sovereign fiber backbone infrastructure market. Growth in this region reflects the overlap of India’s digital infrastructure push, China’s cable system scale, and rising hyperscale demand across Southeast Asia. Tata Communications announced a USD 152 million commitment in June 2026 to 2 India-Singapore subsea cable projects, including the MIST system and Project CS, adding major capacity between Mumbai, Chennai, and Singapore. The Asia Link Cable also landed in Hong Kong in May 2026 through a China Telecom-led consortium, strengthening the Hong Kong-to-Singapore international corridor. The Middle East and Africa are also becoming more important in the sovereign fiber backbone infrastructure market as Gulf states invest in overland alternatives to Red Sea exposure and African markets continue to scale national backbone systems and cross-border links.

Competitive Landscape

The sovereign fiber backbone infrastructure market remains moderately fragmented because the value chain spans fiber and cable manufacturing, optical transport equipment, submarine system construction, and backbone network operations. No single company has full leadership across all of these layers without depending on partners, which keeps the sovereign fiber backbone infrastructure market open to both integrated suppliers and specialist operators. Nokia completed its USD 2.3 billion acquisition of Infinera in February 2025, and its optical networks segment later posted a 20% revenue increase in Q1 2026, showing how equipment consolidation can improve scale and customer access. Corning, Prysmian, and Furukawa continue to compete on the supply side, each with strengths in manufacturing footprint, fiber performance, and proximity to strategic procurement regions. This means buyer decisions in the sovereign fiber backbone infrastructure market often depend on execution capacity and security alignment as much as on price.

Strategic moves are increasingly centered on vertical reach and route readiness in the sovereign fiber backbone infrastructure market. Prysmian’s 2026 acquisition of ACSM for EUR 169 million (USD 191.12 million) extended its position from cable supply into submarine survey and installation services. Nokia’s selection by Orange Belgium in July 2026 for an optical upgrade with quantum-resilient security features showed how security requirements are becoming a stronger differentiator in backbone awards. Ciena’s 2026 AI networking launches also show how optical performance upgrades are being timed directly to hyperscaler and large-capacity backbone demand.

White-space opportunities in the sovereign fiber backbone infrastructure market are most visible in AI-specific routes that legacy carrier networks did not build to meet current latency and throughput needs. Utility and rail corridor monetization is another opening, especially in emerging markets where rights-of-way are already controlled but the optical layer is not yet fully commercialized. Smaller regional operators and state-backed platforms are gaining more attention in the sovereign fiber backbone infrastructure market when they can offer ownership structures that better align with national sovereignty priorities. Compliance is becoming a meaningful filter as well, because buyers increasingly favor vendors that can meet formal security expectations and move quickly under public procurement rules. The ITU’s work on submarine cable resilience adds to this direction by supporting more structured coordination on repair and operational continuity, which could strengthen incumbents that prepare early for stricter qualification standards.

Sovereign Fiber Backbone Infrastructure Industry Leaders

Nokia Corporation

Ciena Corporation

Cisco Systems, Inc.

Corning Incorporated

Prysmian S.p.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2026: Nokia was selected by Orange Belgium for an optical network upgrade incorporating quantum-resilient security and AI-scale computing support, positioning Orange Belgium's backbone among the first in the Benelux region to advance post-quantum cryptography readiness.

- July 2026: Lightstorm announced a new subsea cable connecting India's east coast with Singapore and Malaysia, adding a geographically distinct east-coast corridor to complement its existing west-coast Mumbai-to-Singapore route and strengthening India's position as a multi-path submarine cable hub.

- June 2026: Tata Communications announced a USD 152 million investment in 2 India-Singapore subsea cable projects, USD 63 million in the MIST system, targeted Q4 FY2027, adding 20 Tbps, and USD 89 million in Project CS, expected Q3 FY2031, adding 78 Tbps, integrating with more than 100 data centers across India.

- May 2026: Asia Link Cable, ALC, a China Telecom-led consortium of 13 telecom operators, landed at the newly built Chung Hom Kok cable landing station in Hong Kong, set to become the highest-capacity international submarine cable on the Hong Kong-to-Singapore route, with commercial service targeting later in 2026.

Global Sovereign Fiber Backbone Infrastructure Market Report Scope

The Sovereign Fiber Backbone Infrastructure Market Report is Segmented by Infrastructure Type (Terrestrial, Intercity, Metro, Subsea and Cross-Border, and Utility and Rail), Deployment Architecture (Dark Fiber, Lit Fiber, and Hybrid Wave), End User (Government, Telecom, Cloud and Hyperscale, Enterprises, and Utilities), and Geography (North America, South America, Europe, Asia-Pacific, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Terrestrial National Backbone |

| Intercity Long-Haul Backbone |

| Metro Backbone Rings |

| Subsea and Cross-Border Backbone |

| Utility and Rail Corridor Fiber Backbone |

| Dark Fiber |

| Lit Fiber Services |

| Hybrid Fiber and Wave Services |

| Government and Defense |

| Telecom Operators |

| Cloud and Hyperscale Data Centers |

| Enterprises and Financial Institutions |

| Utilities and Critical Infrastructure Operators |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Turkey |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Qatar | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Kenya | ||

| Nigeria | ||

| Rest of Africa | ||

| By Infrastructure Type | Terrestrial National Backbone | ||

| Intercity Long-Haul Backbone | |||

| Metro Backbone Rings | |||

| Subsea and Cross-Border Backbone | |||

| Utility and Rail Corridor Fiber Backbone | |||

| By Deployment Architecture | Dark Fiber | ||

| Lit Fiber Services | |||

| Hybrid Fiber and Wave Services | |||

| By End User | Government and Defense | ||

| Telecom Operators | |||

| Cloud and Hyperscale Data Centers | |||

| Enterprises and Financial Institutions | |||

| Utilities and Critical Infrastructure Operators | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Turkey | |

| Saudi Arabia | |||

| United Arab Emirates | |||

| Qatar | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Kenya | |||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the sovereign fiber backbone infrastructure market size in 2025, and what is its projected growth by 2031?

The sovereign fiber backbone infrastructure market size was USD 30.91 billion in 2025, is expected to reach USD 34.20 billion by 2028, and is projected to reach USD 64.10 billion by 2031 at a 13.39% CAGR over 2026-2031.

Which infrastructure type is leading sovereign fiber backbone deployments today?

Terrestrial national backbone led in 2025 with a 35.61% revenue share, supported by state-funded broadband programs, railway corridor assets, and national carrier upgrades.

Which deployment model is growing the fastest across sovereign fiber networks?

Hybrid fiber and wave services are the fastest-growing deployment architecture, with a projected 15.31% CAGR through 2031, as buyers seek performance without full dark fiber maintenance responsibility.

Why are governments investing more heavily in sovereign fiber routes?

Governments are tying data sovereignty, public network control, and security requirements more closely to backbone procurement, which raises demand for domestic landing points, controlled routing, and exclusive optical capacity.

Which end-user group is growing the fastest in this space?

Cloud and hyperscale data centers are growing the fastest, with a 14.66% CAGR through 2031, because AI workloads need dense, low-latency links between compute clusters and data center nodes.

Which region is expected to grow the fastest over the forecast period?

Asia-Pacific is projected to post the highest growth at 15.11% through 2031, supported by India's subsea investments, China's scale in cable systems, and stronger hyperscale demand across Southeast Asia.

Page last updated on: