Southern African Development Community (SADC) Water Treatment Chemicals Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

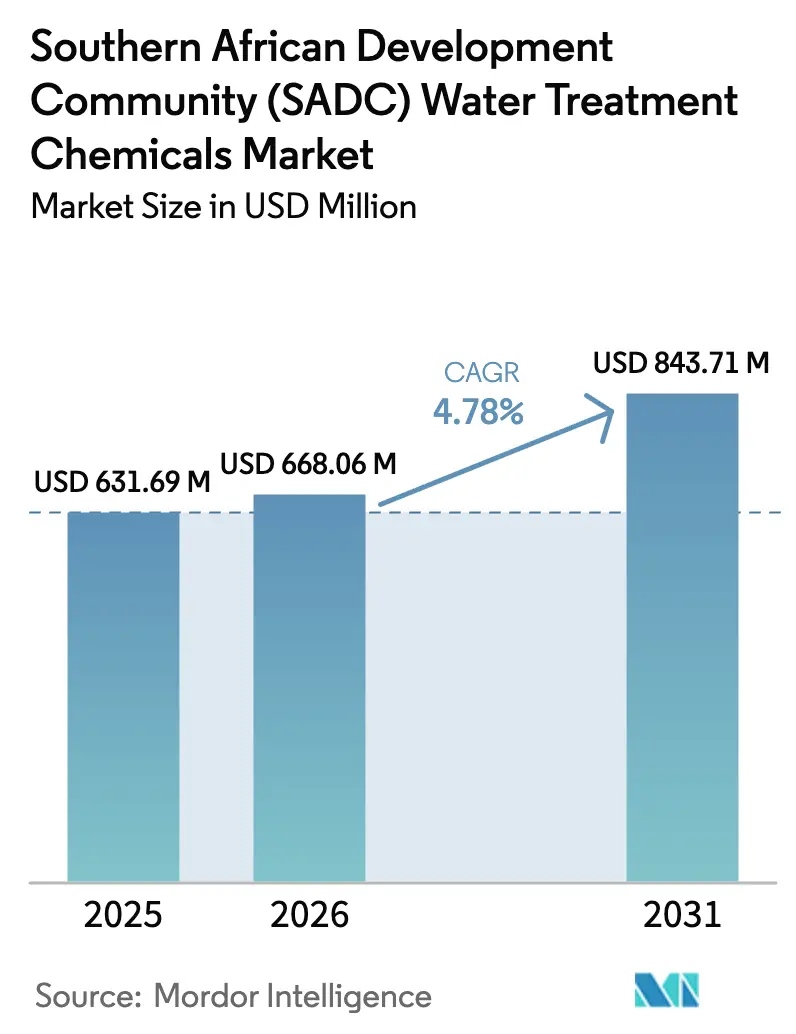

| Base Year Market Size (2025) | USD 631.69 Million |

| Market Size (2026) | USD 668.06 Million |

| Market Size (2031) | USD 843.71 Million |

| Growth Rate (2026 - 2031) | 4.78% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Southern African Development Community (SADC) Water Treatment Chemicals Market Analysis by Mordor Intelligence

The Southern African Development Community Water Treatment Chemicals Market size is projected to be USD 631.69 million in 2025, USD 668.06 million in 2026, and reach USD 843.71 million by 2031, growing at a CAGR of 4.78% from 2026 to 2031. Severe drought in 2024, mounting municipal debt, and tighter effluent limits are simultaneously squeezing budgets and lifting chemical‐dosing intensity as operators grapple with degraded raw-water quality. South Africa’s utilities are ring-fencing procurement to retain Blue Drop compliance, while mining-led demand in Zambia and the DRC is opening secondary growth corridors. Rising adoption of desalination, brackish-groundwater blending, and industrial reuse is creating specification pressure for coagulants, biocides, and corrosion inhibitors that can perform under higher salinity and variable pH. Competitive responses range from bolt-on acquisitions for distribution reach to digital dosing platforms that shave off chemical consumption yet preserve residual safety margins.

Key Report Takeaways

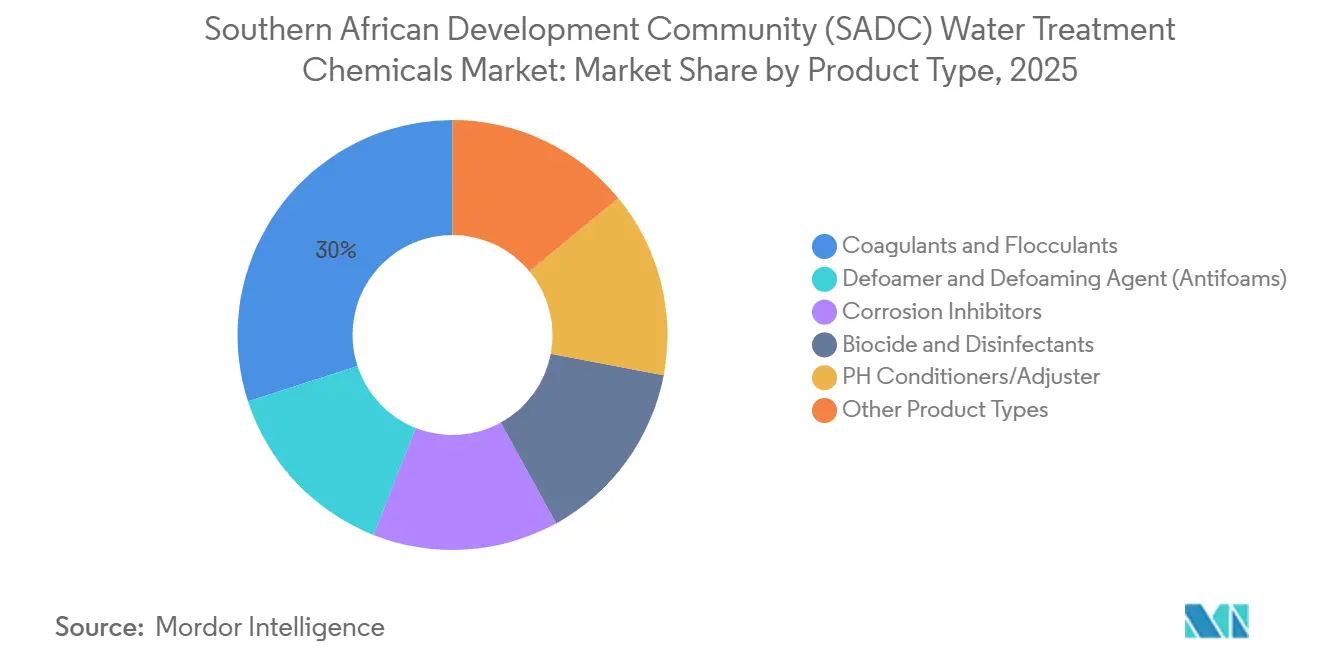

- By product type, coagulants and flocculants captured 30.01% of the SADC water treatment chemicals market share in 2025, while the same category is forecast to expand at a 5.82% CAGR through 2031.

- By geography, South Africa held 71.26% revenue share of the SADC water treatment chemicals market in 2025, and is projected to record the highest country-level CAGR at 5.06% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Southern African Development Community (SADC) Water Treatment Chemicals Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Chronic water scarcity intensifying treatment demand | +1.4% | SADC-wide, acute in Namibia, Zimbabwe, South Africa | Medium term (2-4 years) |

| Urban population growth and rising municipal demand | +1.2% | South Africa metros, Luanda, Dar es Salaam, Maputo | Long term (≥ 4 years) |

| Tightening potable and effluent regulations | +1.0% | South Africa, Namibia, Mauritius | Short term (≤ 2 years) |

| Mining and industrial capacity expansion | +1.1% | Zambia, DRC, Zimbabwe, Mozambique LNG corridor | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Chronic Water Scarcity Intensifying Treatment Demand

In 2024, the El Niño season led to a year-on-year drop in dam levels in Namibia. This pushed utilities to adopt multi-barrier treatment trains, integrating coagulation, filtration, and residual disinfection. In Zimbabwe, with millions of people grappling with acute water insecurity, emergency chemical stockpiles are being planned[1]UNICEF, “Zimbabwe WASH Budget 2025,” unicef.org. The blending of brackish groundwater now mandates precise pH adjustments and anti-scalant dosing—chemistries that were rarely included in tenders just five years prior. While the total volume of treated water remains stagnant, scarcity has driven up per-capita consumption. This is because utilities are working harder to elevate poor-quality feedwater to potable standards. As a result, the SADC water treatment chemicals market is witnessing higher unit margins on these specialized formulations, compensating for the softness in volume.

Urban Population Growth and Rising Municipal Demand

Dar es Salaam, Luanda, and Maputo add new residents annually, yet treatment expansions trail by almost two years. South African metros suffer from non-revenue water, forcing overdosing to replace lost supply without comparable revenue recovery. Luanda’s peri-urban plants adopt modular skids that can scale chemical feed as new neighborhoods connect. Maputo’s LNG-fueled labor influx drives demand for mobile package plants reliant on liquid coagulants. Collectively, these dynamics enlarge the SADC water treatment chemicals market footprint in fast-growing cities while exposing suppliers to credit risk from tariff-strapped utilities.

Tightening Potable and Effluent Regulations

South Africa’s revised Blue Drop and Green Drop audits penalize exceedances in turbidity and coliform counts with grant claw-backs, accelerating continuous clarification and chlorination adoption. Eskom’s Medupi retrofit will yield acidic wastewater that must be neutralized with lime slurry and polymer clarification before discharge. Namibia’s coastal towns now mandate ferric-based phosphorus removal to safeguard marine ecosystems, spurring a niche market for high-purity ferric chloride. Mauritius pilots reverse-osmosis desalination in hotels, each requiring anti-scalants and membrane cleaners under the 2015 Technology Action Plan. Specification creep into PFAS and trace-contaminant removal uplifts demand for activated carbon and specialty coagulants, reinforcing value growth across the SADC water treatment chemicals market.

Mining and Industrial Capacity Expansion

Zambia aims to produce refined copper, necessitating larger tailings thickeners and flotation circuits that depend on polyacrylamide flocculants. The DRC’s cobalt belt attracts hydrometallurgical flowsheets demanding pH control, anti-foaming agents, and selective precipitants. Zimbabwe’s lithium concentrators use flocculants and corrosion inhibitors to manage acidic streams. Mozambique’s Coral Sul FLNG doses biocides and scale inhibitors to protect seawater cooling towers. These industrial cornerstones underpin a resilient, high-margin slice of the SADC water treatment chemicals industry.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Competition from non-chemical technologies | -0.6% | South Africa metros, Namibia desalination hubs | Short term (≤ 2 years) |

| Financial stress and under-investment in utilities | -0.9% | SADC-wide, acute in Zimbabwe, Zambia municipalities | Long term (≥ 4 years) |

| Import-dependent raw-material costs and forex volatility | -0.5% | Angola, Mozambique, Zimbabwe, Zambia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Competition from Non-Chemical Technologies

In 2024, South Africa allocated a portion of its municipal capital expenditure to membrane filtration, UV, and ozone technologies, gradually reducing its reliance on chlorine[2]Ecolab, “Water Treatment Solutions,” ecolab.com. Meanwhile, Namibia's reverse-osmosis plant is pushing back the demand for coagulants by opting for membrane-based primary clarification. Rural water schemes, facing grid reliability issues with UV, continue to lean on chlorine products. Ozone, while effective, comes at a premium, limiting its adoption primarily to beverage bottlers seeking a chlorine-free flavor. Activated carbon, especially after Kemira's 2024 acquisition of Norit's UK unit, is being positioned as a complementary agent to coagulants rather than a direct replacement. While these dynamics may temper the growth in demand, they don't alter the long-term positive outlook for the SADC water treatment chemicals market.

Financial Stress and Under-Investment in Utilities

South African water boards grapple with municipal arrears, straining their operating cash and curtailing chemical orders. In Zimbabwe, hyperinflation leads to sporadic chlorination, resulting in higher coliform counts during the dry season. Instead of purchasing coagulants, Lusaka Water and Sewerage Company in Zambia opts to extend clarifier retention times, leading to increased turbidity in distribution. Angola's EPAL faces a currency mismatch between the kwanza and USD, leading to inventory hoarding when oil prices are stable and rationing during currency depreciation. While donor loans frequently fund infrastructure projects, they often overlook consumables. This oversight means that newly commissioned plants in Mozambique face underdosing issues within just a year. Such recurring challenges are dampening the short-term growth of the SADC water treatment chemicals market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Coagulants Lead on Sludge-Volume Economics

Coagulants and flocculants accounted for 30.01% of the SADC water treatment chemicals market size in 2025 and are projected to expand at a 5.82% CAGR to 2031. Polyaluminum chloride is winning share because it produces less sludge than aluminum sulfate, trimming landfill fees in capacity-constrained cities. Ferric chloride secures coastal phosphorus-removal projects by achieving 90% precipitation at a lower dosage than alum. Mining expansions in Zambia and the DRC pull high-molecular-weight polyacrylamide volumes that minimize tailings ponds and water loss.

Chlorine gas, hypochlorite, and calcium hypochlorite, the leading biocides, dominate the total disinfection tonnage. However, in major metropolitan areas, projects focused on membranes are reducing this volume. Corrosion inhibitors enjoy niche demand in Angola and Mozambique, where hybrid alloys in LNG and aging pipelines coexist. pH conditioners serve both distribution stabilization and membrane-cleaning roles, with lime and caustic soda bookending the product family. Defoamers remain small but critical for biological aeration systems. Scale inhibitors, oxygen scavengers, and chelants are rising in desalination and industrial reuse schemes, notably Namibia’s forthcoming reverse-osmosis plant.

Geography Analysis

South Africa dominates the SADC water treatment chemicals market, holding 71.26% revenue share in 2025 and growing at 5.06% CAGR to 2031. Eskom’s Medupi retrofit will require large volumes of pH adjusters, anti-scalants, and polymers as it ramps toward full operation. Metros such as Johannesburg and Cape Town continue full-spec dosing despite high non-revenue water, while smaller towns ration chemicals due to arrears, creating a bifurcated procurement landscape.

Zambia and the DRC form the fastest-growing axis of the SADC water treatment chemicals market as copper and cobalt expansions mandate flotation reagents, tailings flocculants, and process-water biocides. Suppliers maintain only 30-45 days of inventory amid forex constraints, heightening supply-chain risk. Zimbabwe’s lithium boom adds demand for acidic-service corrosion inhibitors and high-performance flocculants. Mozambique’s Coral Sul FLNG facility doses proprietary inhibitor packages to protect seawater cooling systems, while Angola’s offshore fields pivot to oxygen scavengers to meet new discharge norms.

Namibia’s new desalination capacity will boost anti-scalant and membrane-cleaning volumes even as RO reduces primary coagulant need. Tanzania’s Dar es Salaam expands modular plants with flexible dosing skids to accommodate urban migration. Mauritius pilots hotel-scale RO, importing anti-scalants on a just-in-time basis under its Technology Action Plan. Smaller SADC states rely on donor-funded kits that bundle coagulant and chlorine tablets, adding steady though limited tonnage to the regional total.

Competitive Landscape

The SADC water treatment chemicals market is moderately consolidated. White-space opportunities cluster around Namibia’s desalination pre- and post-treatment chemistry, mining-specific flocculants in Zambia and Zimbabwe, and closed-loop reuse packages for Mozambique’s LNG and Angola’s offshore platforms. Digital dosing systems promise double-digit chemical savings, a selling point for cash-strapped utilities. Regulatory gaps remain around brine disposal in Mauritius, delaying anti-scalant and neutralization tenders until a monitoring framework appears.

Southern African Development Community (SADC) Water Treatment Chemicals Industry Leaders

AECI

SNF Group

Kemira

Solenis

Ecolab Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Ecolab completed the acquisition of Ovivo’s Electronics Ultrapure Water business, expanding advanced chemistry and service capabilities for South African high-tech users.

- November 2024: BASF divested its Magnafloc and related flocculant brands to Solenis to focus on solvent-extraction and leaching reagents for mining applications.

Southern African Development Community (SADC) Water Treatment Chemicals Market Report Scope

Water treatment chemicals are substances used to purify water by removing contaminants, disinfecting, and preventing scaling or corrosion in industrial, municipal, and residential water systems. These chemicals are categorized based on their specific roles in the water treatment process.

The water treatment chemicals market is segmented by product type and geography. By product type, the market is segmented into coagulants and flocculants, defoamers and defoaming agents (antifoams), corrosion inhibitors, biocides and disinfectants, pH conditioners/adjusters, and other product types. By geography, the market is segmented into Angola, the Democratic Republic of Congo (DRC), Mauritius, Mozambique, Namibia, South Africa, the United Republic of Tanzania, Zambia, Zimbabwe, and other SADC countries. For each segment, the market sizing and forecasts have been done on the basis of revenue (USD).

| Coagulants and Flocculants |

| Defoamer and Defoaming Agent (Antifoams) |

| Corrosion Inhibitors |

| Biocide and Disinfectants |

| PH Conditioners/Adjuster |

| Other Product Types |

| Angola |

| Democratic Republic of Congo (DRC) |

| Mauritius |

| Mozambique |

| Namibia |

| South Africa |

| United Republic of Tanzania |

| Zambia |

| Zimbabwe |

| Rest of SADC Countries |

| By Product Type | Coagulants and Flocculants |

| Defoamer and Defoaming Agent (Antifoams) | |

| Corrosion Inhibitors | |

| Biocide and Disinfectants | |

| PH Conditioners/Adjuster | |

| Other Product Types | |

| By Geography | Angola |

| Democratic Republic of Congo (DRC) | |

| Mauritius | |

| Mozambique | |

| Namibia | |

| South Africa | |

| United Republic of Tanzania | |

| Zambia | |

| Zimbabwe | |

| Rest of SADC Countries |

Key Questions Answered in the Report

How large is the SADC water treatment chemicals market in 2026?

It is valued at USD 668.06 million and projected to reach USD 843.71 million by 2031, registering a 4.78% CAGR.

Which product category leads sales?

Coagulants and flocculants account for the largest 30.01% share of 2025 revenue and post the fastest 5.82% CAGR to 2031.

Why does South Africa dominate regional demand?

Blue Drop enforcement, mining effluent rules, and high non-revenue water push continuous dosing, giving South Africa 71.26% of 2025 revenue.

What is the main growth driver outside South Africa?

Mining expansions in Zambia and the DRC are boosting demand for flocculants, pH controllers, and biocides.

Page last updated on: