Southeast Asia Social Commerce Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

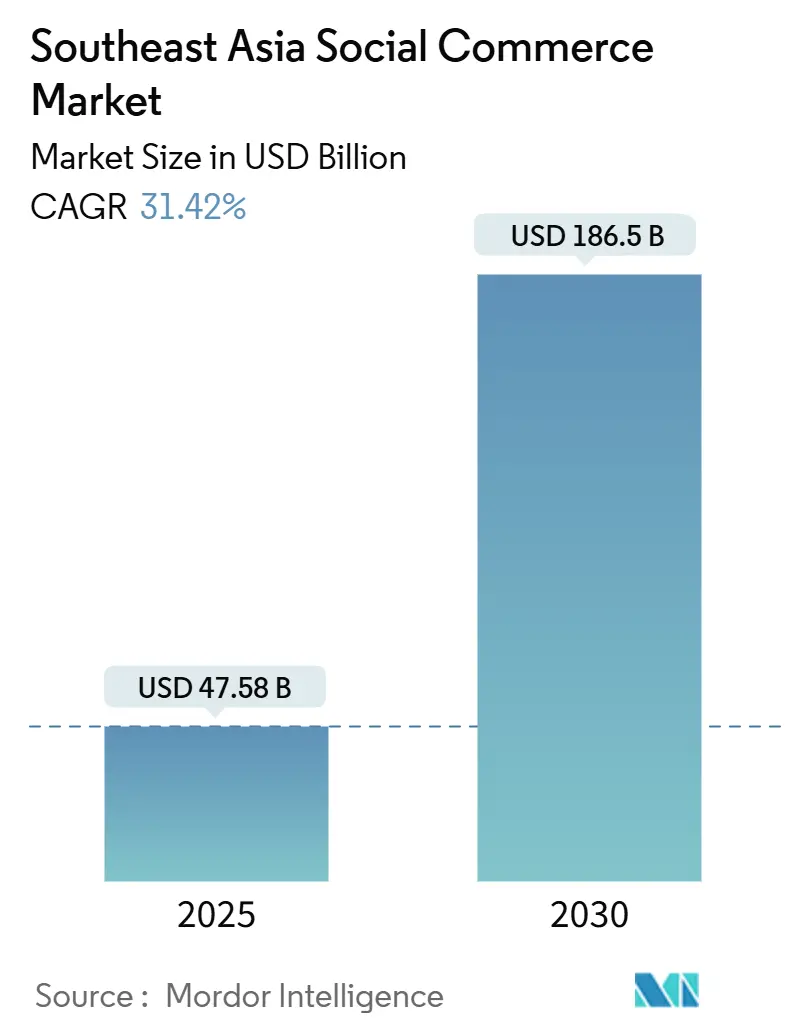

| Market Size (2025) | USD 47.58 Billion |

| Market Size (2030) | USD 186.5 Billion |

| Growth Rate (2025 - 2030) | 31.42% CAGR |

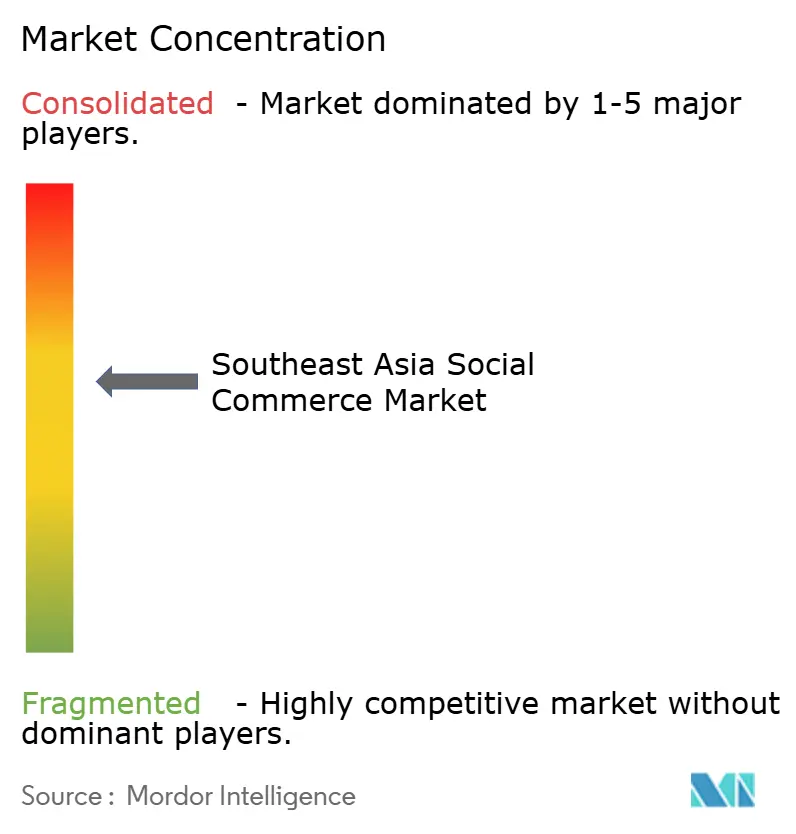

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Southeast Asia Social Commerce Market Analysis by Mordor Intelligence

The Southeast Asia social commerce market reached USD 47.58 billion in 2025 and is forecast to hit USD 186.50 billion by 2030, translating into a 31.42% CAGR; this trajectory underscores the market’s broadening addressable base and the growing preference for mobile-first shopping journeys that merge entertainment and transactions. Robust live-stream engagement, secure in-app payments, and expanding 5G coverage continue to pull new shoppers into the ecosystem, while community group-buying, influencer-led discovery, and cross-border fulfillment hubs lift average order values across categories. Smartphone dominance, supported by falling device prices, keeps customer acquisition costs comparatively low for platforms able to personalize feeds at scale. Intensifying regulatory scrutiny is prompting larger platforms to invest in localized compliance and dispute-resolution infrastructure, a move that raises entry barriers for new entrants but improves consumer trust. Competitive intensity remains high as incumbents step up live-commerce features and logistics investments to match TikTok Shop’s rapid traction.

Key Report Takeaways

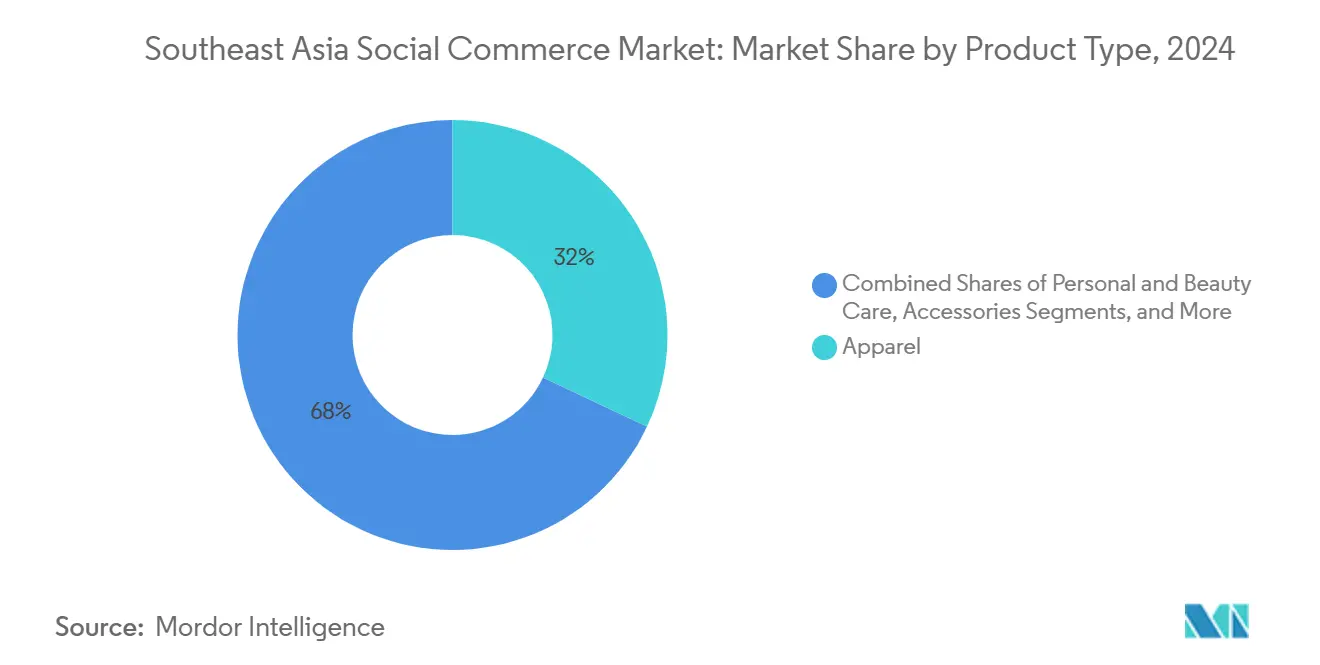

- By product type, Apparel held 31.71% revenue share in 2024; Personal and Beauty Care are projected to expand at 32.11% CAGR through 2030

- By device, smartphones commanded 92.22% of the Southeast Asia social commerce market share in 2024 and is projected to expand at a 31.66%CAGR through 2030

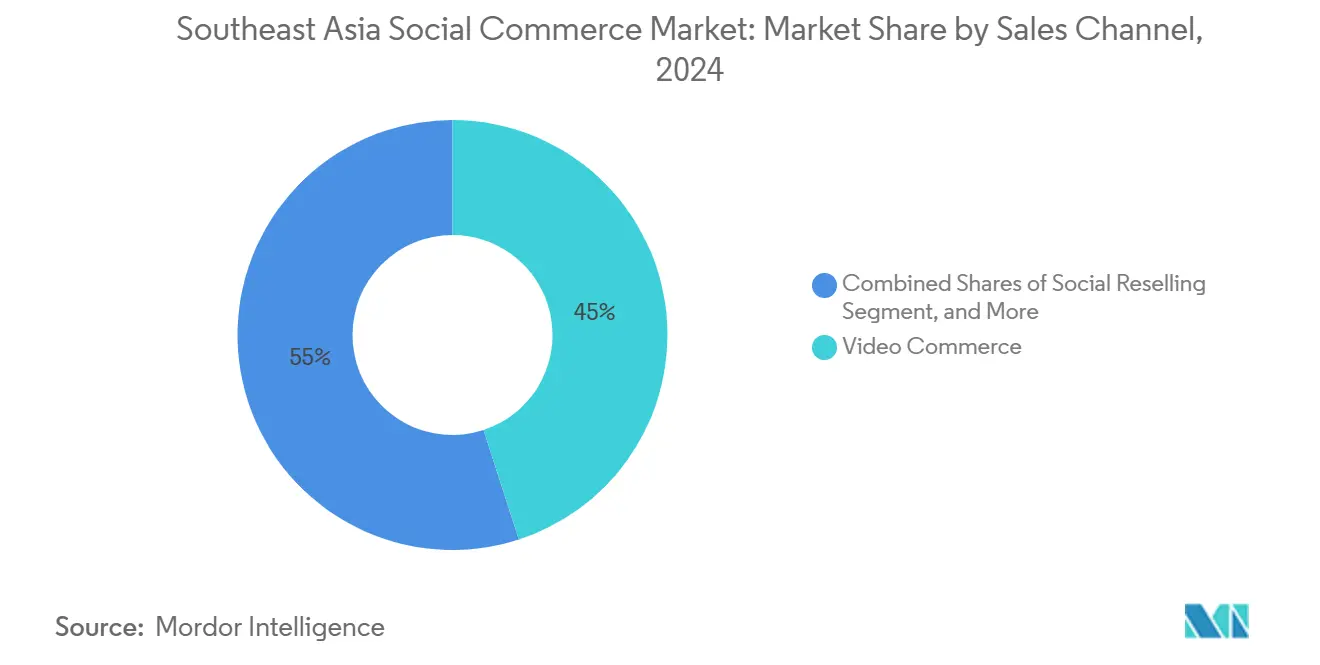

- By sales channel, Video Commerce captured 44.81% of 2024 revenues; Social Reselling is forecast to grow at a 33.12% CAGR to 2030

- By geography, Indonesia led with 39.29% of the Southeast Asia social commerce market share in 2024, whereas Vietnam is projected to post the fastest 32.47% CAGR between 2025-2030

Southeast Asia Social Commerce Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising smartphone and mobile-data penetration | +8.2% | Indonesia, Vietnam, Philippines | Medium term (2-4 years) |

| Integration of in-app checkout and secure payment rails | +7.1% | Singapore, Thailand, Malaysia; rollouts in Indonesia, Philippines | Short term (≤ 2 years) |

| Growth of live-stream and short-video commerce | +6.8% | Thailand, Vietnam, Indonesia | Short term (≤ 2 years) |

| High Gen-Z social-media engagement | +5.9% | Vietnam, Philippines, Thailand | Long term (≥ 4 years) |

| Community group-buying tailored to rural SEA | +4.3% | Indonesia, Philippines; scaling in Thailand, Vietnam | Medium term (2-4 years) |

| Cross-border micro-fulfillment hubs enabling 48-hour delivery | +3.2% | Singapore hub serving Malaysia, Thailand; expansion to Vietnam | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising smartphone and mobile-data penetration

Indonesia’s smartphone penetration climbed to 89% in 2024 as data prices fell 35%, widening rural reach and letting micro-sellers tap national demand through livestreams and short-form videos. Affordable 5G devices in Vietnam and Thailand boost adoption of data-heavy features such as AR try-ons that convert browsers to buyers in seconds. MSMEs leverage this infrastructure leap to bypass costly physical storefronts, pushing the Southeast Asia social commerce market deeper into tier-two cities and remote islands while cementing mobile-first behavior across income segments.[1]Cube, “Rising Influence of Social Commerce in Southeast Asia: Trends Shaping the Future”, cube.asia

Integration of in-app checkout and secure payment rails

TikTok Shop’s tie-ups with local wallets in all six core markets trimmed cart abandonment by 40% versus off-platform redirects, proving that frictionless payments unlock impulse spending in beauty, fashion, and electronics. Shopee’s bank partnerships and buy-now-pay-later options raise ticket sizes among first-time shoppers who previously hesitated at upfront costs. Seamless cross-border settlement now let’s Vietnamese consumers pay in local currency for Thai skincare during livestreams, accelerating regional GMV convergence.

Growth of live-stream and short-video commerce

Live sessions convert at more than triple the rate of static listings, as shoppers pose real-time questions and watch demos before clicking “buy.” Beauty and apparel dominate airtime, but electronics brands pilot tech unboxings that entice Gen-Z audiences. In 2024, Skintific, a Vietnamese label, achieved notable sales growth by conducting daily streams with bilingual hosts. This strategy demonstrates how AI translation tools can enhance market accessibility without requiring additional staffing.[2]tmo group, “How Skintific dominates Southeast Asia's Beauty and Skincare eCommerce”, .tmogroup.asia

High Gen-Z social-media engagement

Seventy-three percent of Gen-Z users in Vietnam and the Philippines finalize purchases without leaving the social platform, valuing peer validation and short-form reviews over traditional ads. This comfort with sharing hauls drives viral loops that slash customer-acquisition budgets for brands able to seed authentic content. Their expectations for gamified, personalized feeds push platforms to deploy AI that recommend bundles based on viewing history, thus lengthening session times and boosting lifetime value.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented last-mile logistics in archipelagic regions | -4.7% | Indonesia, Philippines archipelagic areas; Malaysia East Coast | Medium term (2-4 years) |

| Tightening data-privacy and consumer-protection laws | -3.1% | Singapore, Thailand leading; Indonesia, Vietnam implementing | Short term (≤ 2 years) |

| Escalating CAC from algorithm changes on social platforms | -2.8% | Global impact, particularly affecting TikTok Shop, Meta platforms | Short term (≤ 2 years) |

| Real-money-game feature bans dampening engagement monetisation | -1.9% | Malaysia, Philippines, Thailand with gaming restrictions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Fragmented last-mile logistics in archipelagic regions

Serving 17,000 Indonesian islands or 7,600 Philippine islands pushes delivery costs to 15% of order value versus 5% in cities, eroding margins on low-priced social commerce orders. Weak address systems and limited ferry schedules extend lead times to 7-10 days, dampening repeat purchases for perishables and fashion. LOCAD’s micro-fulfillment model shortens routes but covers only major metros, leaving vast rural pockets underserved until infrastructure catches up.[3] LOCAD Team, “LOCAD Expands Micro-Fulfillment Across SEA,” LOCAD, locad.io

Tightening data-privacy and consumer-protection laws

Indonesia’s Regulation No. 31/2023 forces platforms to verify sellers and run local dispute centers, hiking compliance spend for midsize players.[4]Herbert Smith Freehills Kramer, “New e-commerce regulation introduces new requirements for social commerce platforms and imported products in Indonesia”, hsfkramer.comSingapore’s 2024 data-transfer rules compel encrypted cross-border flows, complicating centralized analytics that power AI recommendations. Extra content-moderation mandates in local languages demand scalable moderation tech, and the burden risks nudging smaller firms toward M&A exits, accelerating market consolidation.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Beauty’s Rapid Ascent Amid Apparel Leadership

Personal and Beauty Care is forecast to record a 32.11% CAGR, reflecting halal cosmetics demand and influencer-driven tutorials that thrive on visual feeds. Apparel nevertheless retained the largest 31.71% slice of the Southeast Asia social commerce market size in 2024, thanks to fast-fashion drops streamed nightly from Indonesian and Thai warehouses. Beauty sellers exploit AR shade-matching and live Q&A to raise conversion and basket sizes, while accessories and home décor gain momentum through lifestyle content. Health supplements pick up wellness-conscious consumers, yet perishability and customs hurdle slow Food and Beverages traction. Category winners deploy bespoke tech, such as virtual try-ons for lipstick or size-prediction algorithms for denim, proving that one-size-fits-all storefronts are losing relevance inside the Southeast Asia social commerce market.

The pivot toward self-expression categories echoes rising disposable incomes and a shift from necessities toward aspirational spending. Sociolla’s 250% revenue jump after launching livestreams shows how niche, category-led platforms can outmaneuver broader marketplaces. Food sellers must cope with cold-chain deficits and border rules, while electronics balance high ASPs against lengthier decision cycles. Segment diversification compels platforms to curate category-specific experiences rather than merely listing SKUs, deepening user engagement and boosting retention metrics.

By Device: Smartphones Cement Unrivaled Dominance

Smartphones generated 92.22% of revenue and advanced at 31.66% CAGR, confirming the mobile-centric DNA of the Southeast Asia social commerce market. Falling handset costs and expanding 5G allow HD streams and instant checkout, neutralizing historic desktop advantages. Desktop and laptop usage lingers for B2B ordering and high-value electronics where spec sheets matter, yet their share shrinks as mobile UX innovations accelerate.

In-app wallets, push-alert campaigns, and camera-enabled visual search synergize with smartphone portability, letting users shop during commutes or in cafés. Camera-first interactions—scanning QR codes on live videos or uploading outfits for style matches—keep purchase loops inside apps. This always-on access positions smartphones as both point-of-inspiration and point-of-sale, closing the gap that once required switching to desktop for final payment.

By Sales Channel: Video Commerce Leads as Social Reselling Surges

Video Commerce owned 44.81% of 2024 revenue by merging entertainment with immediacy; timed vouchers and on-screen product links convert engagement to GMV in seconds. Social Reselling, however, races ahead with a 33.12% CAGR, riding trust-based recommendations in WhatsApp or Line groups where friends batch orders for discounts. Social Network-Led Commerce on Facebook and Instagram sustains growth by leveraging existing user graphs, while Group Buying scales rural savings for price-sensitive shoppers.

The rise of Social Reselling signals decentralization: individuals become micro-entrepreneurs, and platforms shift to enablement—offering payment links, drop-shipping APIs, and coaching on content creation. Product Review and Discovery sites slot into earlier funnel stages, feeding traffic to livestreams and resell chats. To hedge channel risk, leading platforms now orchestrate omnichannel programs where a single SKU circulates through video, group-buy, and influencer storefronts.

Geography Analysis

Indonesia contributed 39.29% of regional value in 2024, powered by 270 million residents and government-backed MSME digitalization grants. Jakarta hubs anchor same-day delivery pilots that replicate offline spontaneity while national regulation pushes verified-seller policies improving trust. TikTok Shop Indonesia became its second-largest global market in 2024, forcing local rivals to add live-commerce widgets and Bahasa content. Logistics upgrades, including toll-road extensions and container-port expansions, widen reach to secondary islands, sustaining the country’s leadership in the Southeast Asia social commerce market.

Vietnam posted the fastest 32.47% CAGR outlook, reflecting 65% youth population and 85% smartphone adoption. State digital-economy programs and improved express-parcel networks shorten delivery times, enhancing conversions on trend-driven beauty and fashion streams. International investors such as AnyMind Group’s 2025 Vibula acquisition underscore confidence in Vietnam’s live-commerce talent pool and creator economy depth.

Thailand, Philippines, Malaysia, and Singapore offer diverse advantages. Thailand attracts USD 8.8 billion in TikTok commitments that will establish fulfillment centers and creator academies. The Philippines leverages high English proficiency, producing regionally exported content while experimenting with cross-border affiliate payouts. Malaysia serves as a cross-border shipping hub into mainland Southeast Asia, and Singapore’s advanced fintech ecosystem enables instant settlement across currencies. Lesser-penetrated markets—Cambodia, Laos, Myanmar, Brunei, Timor-Leste—enter the strategic horizon as handset prices fall and 4G coverage widens, representing the next frontier for the Southeast Asia social commerce market.

Competitive Landscape

Competition sits at a moderate concentration level where two or three giants hold commanding positions, yet specialist challengers thrive in niches. Shopee leans on integrated logistics and embedded financing to defend GMV share, while TikTok Shop prioritizes AI-driven content recommendations that amplify conversion during real-time streams. Meta deploys Instagram Shops and Facebook Marketplace upgrades to keep its extensive user base transacting in-feed.

High capital commitments define the arms race: TikTok’s multibillion-dollar Thai investment funds regional studios and fulfillment nodes, and Grab acquires grocery chains to mesh offline inventory with online demand. Category-focused players such as Sociolla demonstrate that deep vertical expertise and curated communities can fend off broader platforms. M&A consolidates service enablers: OnPoint’s purchase of Thailand’s CREA integrates marketing, technology, and 3PL services under one roof, bolstering full-stack capabilities for global brands targeting the Southeast Asia social commerce market.

Regulation is now a competitive lever; scalable compliance systems around seller vetting and data residency favor larger, well-funded incumbents. Smaller apps turn to white-label technology or align under bigger umbrellas, compressing the long-tail vendor set. Platforms able to marry content, payments, and last-mile control under a single login are positioned to guard margins against rising customer-acquisition costs.

Southeast Asia Social Commerce Industry Leaders

Sea Limited (Shopee)

ByteDance Ltd.

Meta Platforms Inc.

Lazada Group SA

PT GoTo Gojek Tokopedia Tbk

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: AnyMind Group has finalized the acquisition of Vibula, a live commerce agency based in Vietnam. This acquisition facilitates strategic collaboration by combining Vibula's expertise in live commerce operations with AnyMind's proprietary technology platforms. Additionally, Vibula's creator and affiliate network in Vietnam will be integrated into AnyMind's ecosystem, creating opportunities for monetization through platforms such as AnyCreator and the YouTube Shopping Affiliate program.

- August 2025: AnyMind Group has introduced AnyLive for Creators, designed to provide new opportunities for creators and brands expanding its hybrid human-AI live-commerce suite across Southeast Asia. This platform enables influencers and content creators in Southeast and East Asia to develop customized AI avatars and generate revenue through avatar-related sales. Malaysian creator Bella Khan has been announced as the company’s first signed creator under this initiative.

- May 2025: Grab completed the acquisition of Malaysian supermarket chain Everrise, adding 19 stores to reinforce grocery delivery links with its super-app ecosystem.

- January 2025: Grab finalized the purchase of Cambodian food-delivery and e-commerce platform Nham24, consolidating its presence in Cambodia’s social commerce scene

Southeast Asia Social Commerce Market Report Scope

The Southeast AsiaSocial Commerce Market Report is Segmented by Product Type (Apparel, Personal and Beauty Care, Accessories, Home Products, Health Supplements, Food and Beverages, Other Product Types), Device (Laptops and Desktops, Smartphone), Sales Channel (Video Commerce, Social Network-Led Commerce, Social Reselling, Group Buying/Team Purchase, Product Review and Discovery Platforms), and Geography (Indonesia, Thailand, Vietnam, Philippines, Malaysia, Singapore, Rest of Southeast Asia). The Market Forecasts are Provided in Terms of Value (USD).

| Apparel |

| Personal and Beauty Care |

| Accessories |

| Home Products |

| Health Supplements |

| Food and Beverages |

| Other Product Types |

| Laptops and Desktops |

| Smartphone |

| Video Commerce |

| Social Network-Led Commerce |

| Social Reselling |

| Group Buying / Team Purchase |

| Product Review and Discovery Platforms |

| Indonesia |

| Thailand |

| Vietnam |

| Philippines |

| Malaysia |

| Singapore |

| Rest of Southeast Asia (Cambodia, Laos, Myanmar, Brunei, Timor-Leste) |

| By Product Type | Apparel |

| Personal and Beauty Care | |

| Accessories | |

| Home Products | |

| Health Supplements | |

| Food and Beverages | |

| Other Product Types | |

| By Device | Laptops and Desktops |

| Smartphone | |

| By Sales Channel | Video Commerce |

| Social Network-Led Commerce | |

| Social Reselling | |

| Group Buying / Team Purchase | |

| Product Review and Discovery Platforms | |

| By Geography | Indonesia |

| Thailand | |

| Vietnam | |

| Philippines | |

| Malaysia | |

| Singapore | |

| Rest of Southeast Asia (Cambodia, Laos, Myanmar, Brunei, Timor-Leste) |

Key Questions Answered in the Report

How large is the Southeast Asia social commerce market in 2025?

The market reached USD 47.58 billion in 2025 and is projected to keep expanding at a 31.42% CAGR.

Which country leads regional revenue?

Indonesia contributed 39.29% of 2024 value, supported by a large population and rapid digitalization.

What segment is growing fastest?

Personal and Beauty Care posts the highest 32.11% CAGR to 2030, buoyed by influencer-driven demand.

Why is Social Reselling gaining momentum?

Peer-to-peer trust and group discounts fuel a 33.12% CAGR, especially in rural and price-sensitive communities.

How do tightening regulations affect platforms?

New data-privacy and consumer-protection rules raise compliance costs, favoring well-funded incumbents that can scale verification and dispute processes.

What role do smartphones play?

Smartphones account for 92.22% of sales, anchoring live-stream engagement and frictionless in-app payments.

Page last updated on: