Southeast Asia Printed Circuit Board Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

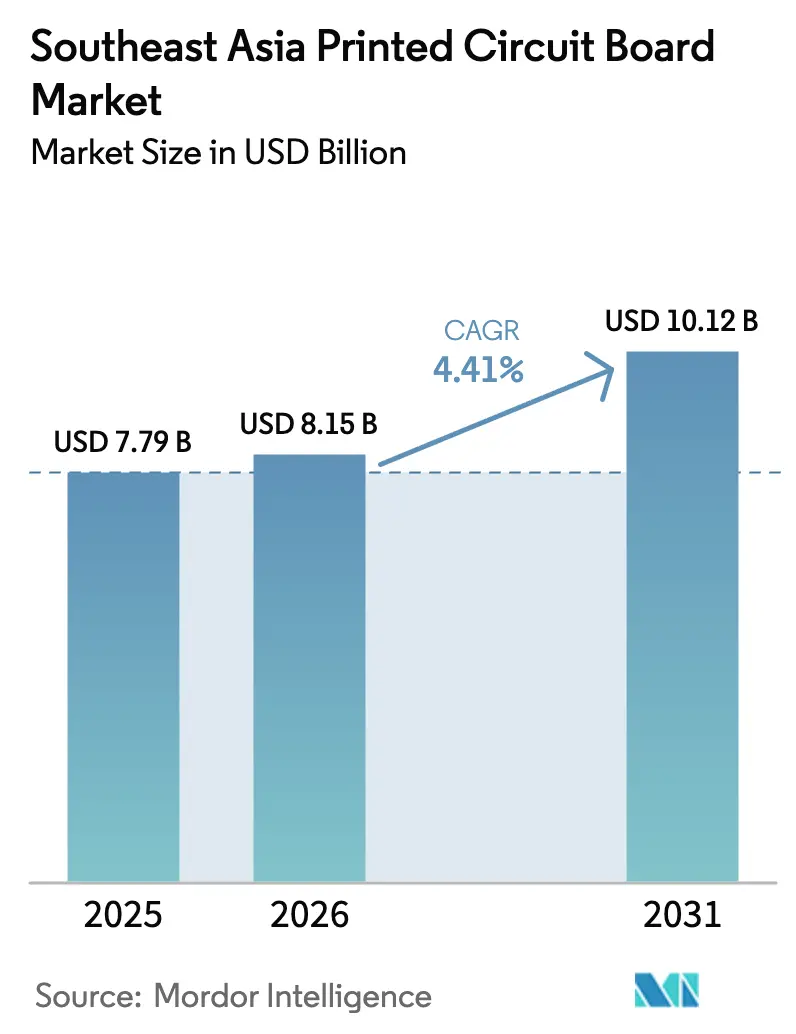

| Base Year Market Size (2025) | USD 7.79 Billion |

| Market Size (2026) | USD 8.15 Billion |

| Market Size (2031) | USD 10.12 Billion |

| Growth Rate (2026 - 2031) | 4.41% CAGR |

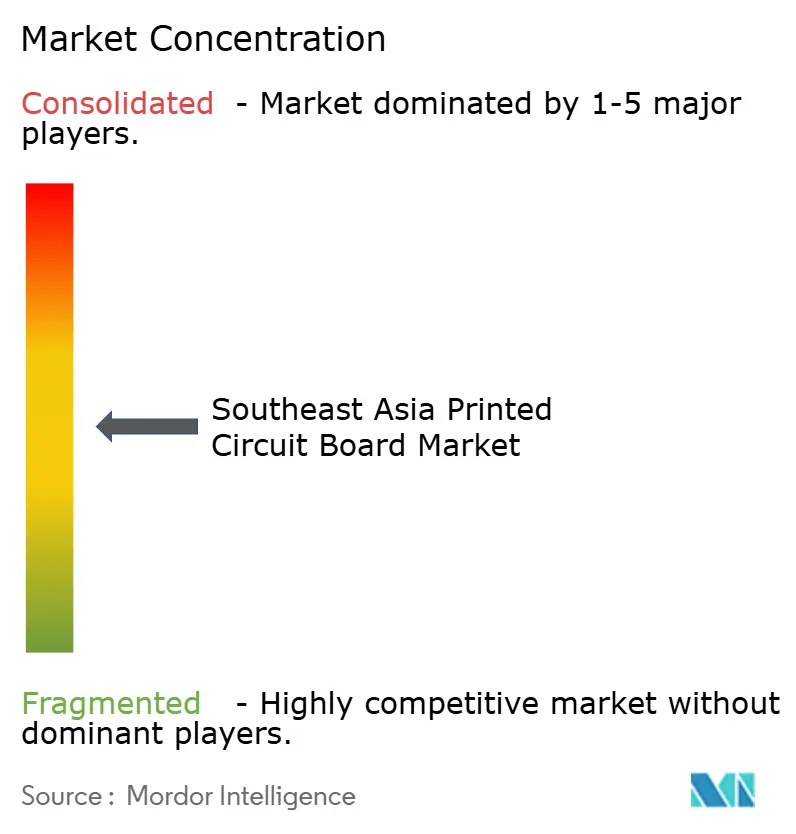

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Southeast Asia Printed Circuit Board Market Analysis by Mordor Intelligence

The Southeast Asia Printed Circuit Board Market was valued at USD 7.79 billion in 2025 and expected to grow from USD 8.15 billion in 2026 to reach USD 10.12 billion by 2031, at a CAGR of 4.41% during the forecast period (2026-2031). Thailand dominates current output because more than 60 Taiwanese and mainland Chinese board houses moved high-layer and HDI capacity into the country between 2023 and 2025, while Vietnam is set to post the briskest expansion as global electronics brands build flexible-circuit and substrate lines inside its northern industrial clusters. Relocation of server and AI motherboard fabrication from mainland China, accelerated roll-out of standalone 5G networks that require low-loss RF laminates, and mounting automotive electrification programs that push heavy-copper boards into two-wheeler drive trains. Competitive behavior is shifting as Taiwanese substrate leaders race Japanese incumbents for AI-server contracts, local champions adopt modified semi-additive processes to meet 15 µm trace widths, and western suppliers leverage quality credentials to defend radar and ADAS niches. Taken together, these trends position the Southeast Asia PCB market as a strategic alternative to East Asian supply chains rather than merely a cost-arbitrage assembly hub.

Key Report Takeaways

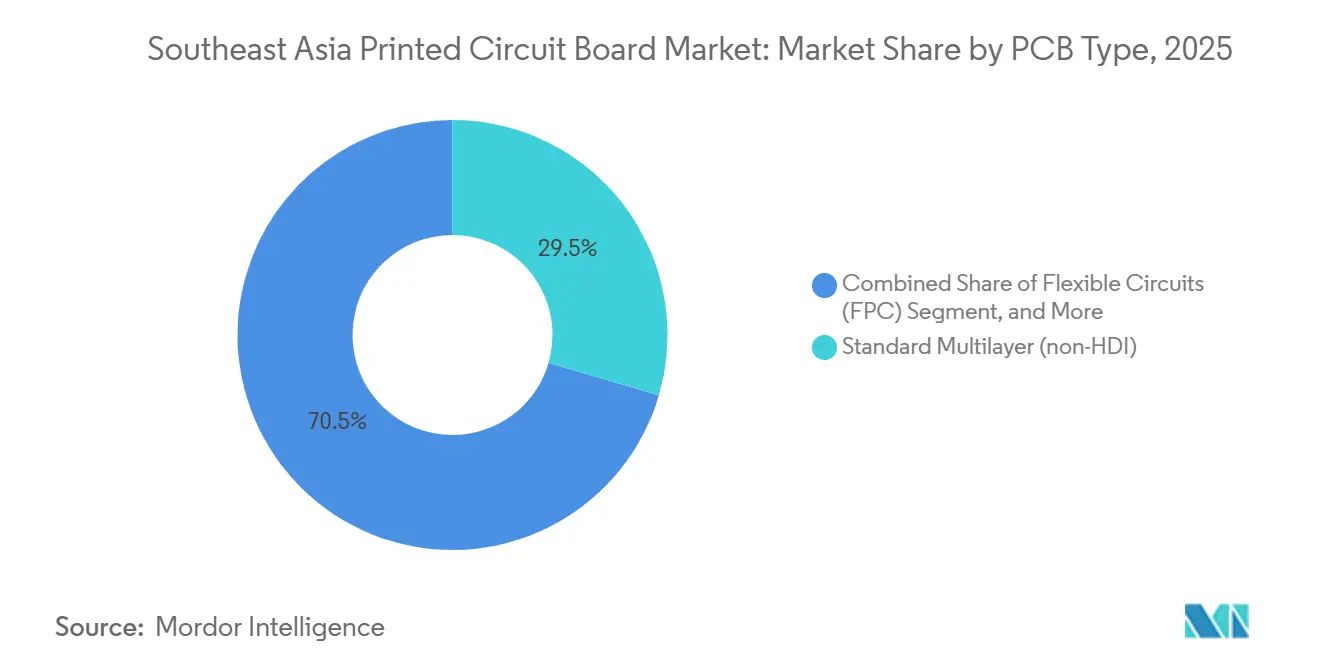

- By PCB type, standard multilayer non-HDI boards captured 29.53% revenue share in 2025; flexible circuits are projected to expand at a 5.23% CAGR through 2031.

- By substrate material, glass-epoxy FR-4 accounted for 43.19% of the Southeast Asia PCB market share in 2025, while high-speed low-loss laminates are forecast to post the fastest 5.46% CAGR to 2031.

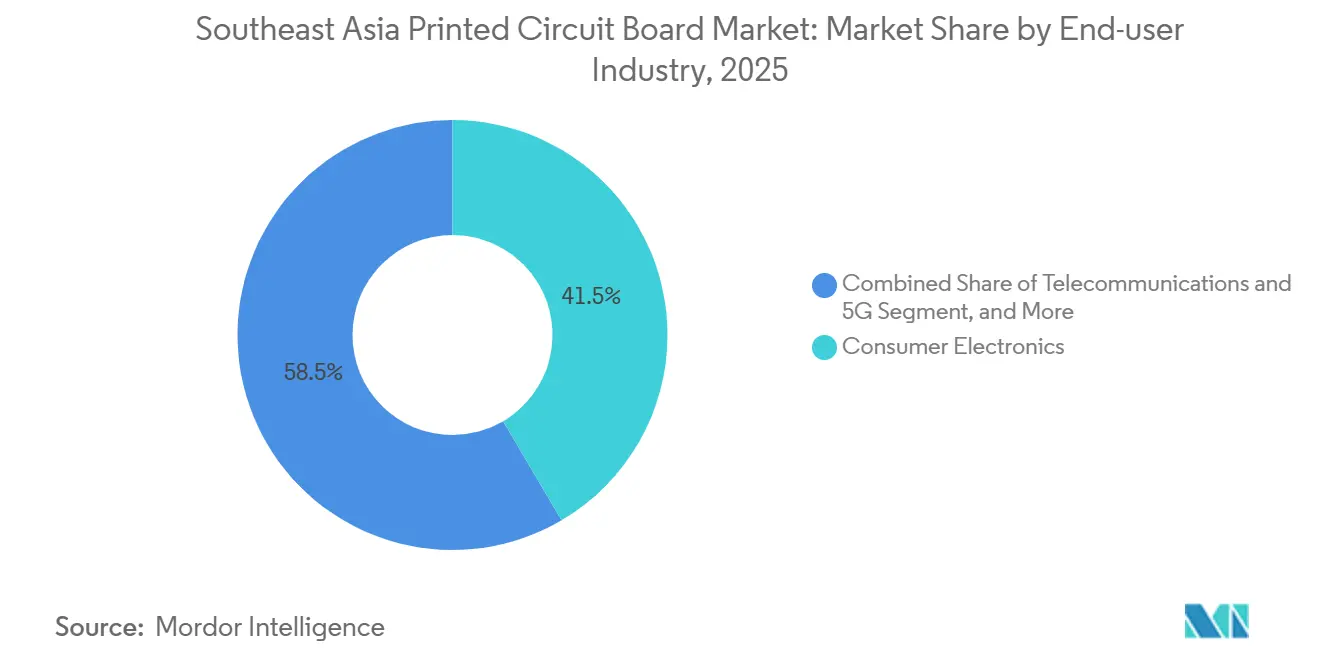

- By end-user industry, consumer electronics led demand with 41.53% share in 2025; telecommunications and 5G infrastructure are expected to record the highest 5.72% CAGR through 2031.

- By country, Thailand accounted for 33.32% of market share in 2025, whereas Vietnam is projected to grow at a 5.58% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Southeast Asia Printed Circuit Board Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Proliferation of Consumer Electronics and Smartphone Assembly Hubs | +1.2% | Thailand, Vietnam, Malaysia, spillover to Indonesia and Philippines | Medium term (2-4 years) |

| Expansion of 5G Infrastructure and Telecom Equipment Manufacturing | +1.4% | Thailand, Vietnam, Singapore, Malaysia | Medium term (2-4 years) |

| Electrification of Automotive Sector Including Two-Wheelers | +0.9% | Indonesia, Thailand, Vietnam, emerging demand in Malaysia and Philippines | Long term (≥ 4 years) |

| Adoption of High-Density Interconnect and Advanced Packaging Technologies | +1.1% | Thailand, Vietnam, Singapore, Malaysia | Medium term (2-4 years) |

| Relocation of Advanced Server and AI PCB Lines from China | +1.3% | Thailand and Vietnam core, secondary benefits to Malaysia | Short term (≤ 2 years) |

| OEM Sustainability Audits Driving Low-Carbon PCB Processes | +0.7% | Thailand, Vietnam, Malaysia, multinational supply chains | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Proliferation of Consumer Electronics and Smartphone Assembly Hubs

Southeast Asia accounted for 41.53% of PCB demand for consumer electronics in 2025, and the shift from final assembly to local component fabrication is accelerating. Malaysia secured more than USD 100 billion in semiconductor pledges, led by Micron’s USD 7 billion high-bandwidth-memory plant, creating captive substrate demand. Vietnam hosts Qualcomm’s AI R&D center and Samsung Display’s USD 3 billion OLED line, compressing flexible-circuit lead times to below 2 weeks. The Philippines reoriented from test-and-pack to substrate-capable operations after landing USD 1.1 billion in 2024 commitments. Indonesia joined with Infineon’s IDR 5.4 trillion (USD 337 million) Batam plant, signaling a broad regional climb up the value chain. The result is a 5.23% annual advance for flexible circuits that outpaces overall market growth.

Expansion of 5G Infrastructure and Telecom Equipment Manufacturing

Telecom PCBs are on track for a 5.72% CAGR through 2031, driven by standalone cores and Open RAN radios that require RF laminates with dissipation factors below 0.003. Singapore reached nationwide 5G by 2025, with each small-cell radio consuming up to six decimeters of high-frequency laminate. Thailand’s 2024 spectrum auction prompted ISO 9001 and IATF 16949 dual-certified board houses to add base-station lines. Vietnam’s millimeter-wave rollout drives Meiko’s USD 340 million factory to 24-hour shifts. Rogers RO4350B and Panasonic Megtron 6, priced at 3.5-3.8 times FR-4, grew 5.46% because hyperscale switches cannot accept 0.5-1 dB insertion loss. Multi-year laminate supply contracts now lock in price and allocation ahead of demand peaks.

Electrification of Automotive Sector Including Two-Wheelers

Indonesia’s roadmap targets 3.1 million electric motorcycles annually by 2035, requiring battery-management and motor-controller PCBs rated for 125 °C junction temperatures and 50,000 hours of operation. Thailand’s high-efficiency standards require metal-core boards, prompting tie-ups with Japanese suppliers. Vietnam’s VinFast is installing 40,000 DC chargers that use heavy-copper boards rated at 150 A continuous. Malaysia’s Fieldman EV and EP Manufacturing committed MYR 1.1 billion (USD 256 million) to EV components, expanding its IATF 16949-certified production capacity. These projects add 0.9 percentage points to regional CAGR and drive investments in rigid-flex and heavy-copper capacity.

Adoption of High-Density Interconnect and Advanced Packaging Technologies

AI servers require organic interposers with via densities above 10,000 cm-². Zhen Ding Technology’s USD 2 billion Rayong complex focuses on 18-layer-plus any-layer HDI, making Thailand a regional advanced-packaging node. Ajinomoto’s ABF shortage pushed OEMs to qualify BT-resin substitutes, accelerating substrate localization. Samsung Electro-Mechanics, Ibiden, and Shinko are scaling FC-BGA lines in Malaysia and Singapore for co-located module plants. Unimicron and Nan Ya PCB deploy modified semi-additive processes that cut copper waste by 40% and achieve 15 µm lines. This evolution contributes 1.1 percentage points to growth and blurs the line between packaging and PCB fabrication.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in Copper and Epoxy Resin Prices | -0.8% | Thailand, Vietnam, Malaysia, Indonesia | Short term (≤ 2 years) |

| Shortage of Skilled HDI Fabrication Workforce | -0.6% | Thailand, Vietnam, Malaysia, Philippines | Medium term (2-4 years) |

| Intermittent Power and Water Supply Constraints in Emerging Industrial Parks | -0.4% | Indonesia, Philippines, secondary zones in Vietnam | Short term (≤ 2 years) |

| OEM-Imposed Scope 3 Carbon Targets Raising Compliance Costs for SMEs | -0.5% | Indonesia, Philippines, smaller Thai fabricators | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatility in Copper and Epoxy Resin Prices

Copper rose 21% between 4Q 2024 and 4Q 2025, lifting PCB material costs by 3-5 percentage points because contracts fix prices for only 90-180 days. Epoxy resin climbed 8-12% in 1H 2025 amid bisphenol-A shortages, and low-chlorine grades cost another 15-20% premium. SMEs rarely hedge futures, so margins compress or customer prices renegotiate mid-term, undermining trust. Larger firms salvage higher-grade scrap, but most producers pass on surcharges, dampening capital-spending plans. This restraint subtracts 0.8 percentage points from near-term growth until commodity markets stabilize.

Shortage of Skilled HDI Fabrication Workforce

Thailand’s Eastern Economic Corridor counts fewer than 2,000 certified engineers for HDI tasks, pushing wages up 12-18% per year and triggering poaching battles. Vietnam’s partnership with Meiko trains only 500 students annually, while a 4,000-technician need is expected by 2028. Malaysia’s Penang Skills Development Centre offers IPC courses but lacks HDI modules, stretching onboarding from three to nine months. Philippine vocational standards for PCB fabrication remain undeveloped, delaying its move beyond assembly. Automation investments will help, but capability gaps clip 0.6 percentage points off the medium-term CAGR.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By PCB Type: Flexible Circuits Lead A Structural Shift

Flexible circuits advanced at a 5.23% annual clip and are set to outpace the wider Southeast Asia printed circuit board market through 2031. Wearable devices, foldable smartphones, and in-vehicle displays depend on polyimide boards rated for more than 100,000 bending cycles, reinforcing demand despite a 2.5-times cost premium. In contrast, standard multilayer non-HDI boards retained 29.53% of 2025 revenue, anchored by cost-sensitive set-top boxes and LED drivers, yet their share is slipping as OEMs adopt system-in-package modules that shrink board area by up to 40%. The Southeast Asia printed circuit board market size for flexible circuits is therefore projected to stretch faster than commodity rigid boards, a trajectory underpinned by rapid consumer electronics refresh cycles and proximity to assembly hubs.

High-density interconnect boards keep pace with overall expansion, as every new 3 nm smartphone processor requires escape routing at a 40 µm pitch. IC substrates, though counted separately in some industry statistics, are spilling into PCB fabs as AI servers standardize on any-layer HDI backplanes paired with flip-chip BGAs. Ajinomoto’s ABF film shortage, however, caps near-term supply, forcing hyperscalers to pre-qualify BT-resin alternatives. Rigid-flex boards continue to penetrate automotive dashboards and medical probes because they replace connectors and reduce assembly labor. Meanwhile, heavy-copper and metal-core boards serve industrial inverters and LED lighting, illustrating how niche requirements sustain multiproduct portfolios inside the Southeast Asia PCB market.

By Substrate Material: High-Speed Laminates Gain Ground

Glass-epoxy FR-4 accounted for 43.19% of 2025 consumption, the largest share of the Southeast Asia printed circuit board market, thanks to decades of familiarity with the process and a competitive supplier pool. Yet high-speed, low-loss laminates such as Rogers RO4350B and Panasonic Megtron 6 are expected to grow 5.46% annually, as 800 Gbps switches and millimeter-wave radios require dissipation factors below 0.003. These materials cost 3.5-3.8 times the price of standard FR-4, but their electrical benefits outweigh the price premium in premium data-center and telecom hardware. The Southeast Asia PCB market share for high-speed substrates will therefore expand even as FR-4 maintains volume leadership in commodity devices.

Polyimide remains indispensable for flexible and rigid-flex builds, while packaging resins BT and ABF face capacity bottlenecks that echo upstream chemical constraints. To maintain margins, fabricators deploy modified semi-additive processes and low-roughness copper foils to offset scrap generated by tighter press cycles. Concurrently, OEMs require halogen-free laminates to comply with RoHS and REACH rules, lifting material premiums by another 8-12% while lowering downstream disposal risks. Metal-core and ceramic substrates fill thermal niches in power electronics and RF front-ends, adding necessary diversity to material portfolios as the Southeast Asia printed circuit board market matures.

By End-User Industry: Telecommunications Outpaces Consumer Electronics

Consumer electronics still consumed 41.53% of market share in 2025, but telecommunications infrastructure is on track for a 5.72% CAGR and will narrow the gap by 2031. Every Open RAN radio features up to six decimeters of high-frequency laminate with impedance held within ±5%, a specification that pushes adoption of low-loss materials far beyond smartphone volumes. At the same time, data-center operators are installing NVIDIA H100 and AMD MI300 accelerators, each requiring any-layer HDI carriers and multiple flip-chip substrates, intensifying pressure on ABF film supply. The Southeast Asia PCB market serving telecom racks is therefore growing faster than the handheld devices market, and this shift in mix underpins plant upgrades across Thailand and Malaysia.

Automotive electrification is driving new demand for rigid-flex and heavy-copper materials as Indonesia targets 3.1 million electric motorcycles per year by 2035. Battery-management boards must withstand 125 °C junction temperatures and 50,000-hour duty cycles, driving tighter quality control and incentivizing IATF 16949 certification. Industrial power, healthcare imaging, and aerospace systems together occupy a manageable but profitable slice because they demand AS9100 traceability and long-term supply agreements. As a result, suppliers diversify across verticals to buffer cyclical swings in the Southeast Asia printed circuit board market while capturing higher-margin specialty orders.

Geography Analysis

Thailand captured 33.32% of the market share in 2025 on the back of Zhen Ding Technology’s USD 2 billion Rayong complex, Victory Giant Technology’s USD 650 million expansion, and a wave of 60 Taiwanese and mainland Chinese factories seeking tariff relief. The Board of Investment’s eight-year tax holiday compresses payback on sequential lamination and laser direct-imaging equipment, anchoring multilayer and HDI leadership. Nevertheless, the talent pool numbers fewer than 2,000 certified engineers, prompting a 12-18% wage escalation and accelerating capital outlays for automation. [1]Eastern Economic Corridor, “Labor Market Analysis,” eeco.or.th

Vietnam is forecast to post a 5.58% CAGR through 2031, the fastest in Southeast Asia, thanks to Meiko Electronics adding USD 540 million in greenfield plants and the EU-Vietnam Free Trade Agreement eliminating 2.5-4% tariffs on Chinese boards. [2]European Commission, “EU-Vietnam Free Trade Agreement,” ec.europa.eu Samsung Display’s USD 3 billion OLED line and Qualcomm’s AI R&D hub are drawing flexible-circuit suppliers to Bac Ninh, compressing logistics cycles and lowering working capital. Yet the country still lacks enough HDI-skilled technicians, so onboarding stretches to nine months and restrains near-term capacity ramps.

Malaysia attracted more than USD 100 billion in semiconductor promises, led by Micron’s USD 7 billion high-bandwidth-memory back-end, Texas Instruments’ MYR 5 billion (USD 1.17 billion) assembly expansion, and X-Fab’s RM 3 billion (USD 700 million) wafer fab. [3]Infocomm Media Development Authority, “5G Network Deployment Statistics,” imda.gov.sg Penang’s Skills Development Centre certifies IPC courses, but HDI-specific modules remain absent, prolonging ramp-up. Singapore focuses on niche advanced-packaging lines supported by nationwide 5G coverage, whereas Indonesia and the Philippines remain in earlier stages of substrate localization due to infrastructure and skills gaps. Collectively, these dynamics ensure that the Southeast Asia printed circuit board market benefits from geographic specialization while diversifying supply risk away from reliance on a single country.

Competitive Landscape

Competition is moderately fragmented. Taiwanese giants Unimicron, Zhen Ding Technology, and Nan Ya PCB share advanced-substrate orders with Japanese rivals Meiko Electronics and Ibiden, largely because Ajinomoto’s ABF film bottleneck forces OEMs to dual-source with a handful of qualified suppliers. Local players such as Thailand’s KCE Electronics and Malaysia’s Vitrox install automated optical inspection and LDI systems to meet sub-75 µm design rules demanded by hyperscale data-center customers. South Korean groups Samsung Electro-Mechanics and LG Innotek expanded FC-BGA capacity in Malaysia and Vietnam to support smartphone and automotive assembly production.

Western fabricator TTM Technologies reported USD 579.5 million revenue in 3Q 2024, up 12.7% year over year, and leveraged its Malaysian site to service automotive radar and ADAS orders. [4]TTM Technologies, “Third-Quarter 2024 Results,” ttm.com AT&S clocked EUR 1.32 billion (USD 1.41 billion) in revenue in the first half of fiscal-year 2024-2025, anchored by mobile and automotive substrates, which carry higher margins. Smaller contenders chase niche plays, Kingboard integrates backward into copper-clad laminates, Flexium runs roll-to-roll flexible lines for infotainment modules, and Suntak offers hybrid rigid-flex solutions.

Since 2023, the relocation of 60 Chinese and Taiwanese board houses has slashed lead times for standard multilayer and HDI orders in Thailand from 4 weeks to 2, forcing incumbents to match response times or cede share. Leaders are doubling down on modified semi-additive technology that cuts copper waste 40%, whereas laggards cling to subtractive etching, sustaining 30-40% scrap on dense builds. The compressed cycle also enables Thai facilities to quote inventory buffers 3-5% below regional norms, a saving that translates directly into lower working-capital needs for ODM customers. Distributors have responded by repositioning hub warehouses near Rayong and Chonburi so same-day prototype deliveries can be executed within a 150-kilometer radius of the main fabrication clusters.

Southeast Asia Printed Circuit Board Industry Leaders

Unimicron Technology Corporation

Zhen Ding Technology Holding Limited

TTM Technologies Inc.

AT&S Austria Technologie & Systemtechnik Aktiengesellschaft

Compeq Manufacturing Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Zhen Ding Technology began trial production at its USD 2 billion Rayong plant in Thailand, adding 1.2 million m² of any-layer HDI capacity aimed at AI-server modules.

- December 2025: Meiko Electronics completed its USD 200 million multilayer-board factory in Vietnam, bringing 600 000 m² of annual capacity online with dual ISO 9001 and IATF 16949 certification.

- November 2025: Samsung Display confirmed a USD 3 billion OLED expansion in Vietnam that will require 400 000 m² of flexible circuits annually by 2028.

- October 2025: Micron Technology ramped high-volume output at its USD 7 billion high-bandwidth-memory packaging plant in Malaysia, spurring local substrate qualification.

Southeast Asia Printed Circuit Board Market Report Scope

Printed Circuit Boards (PCBs) are essential components used to mechanically support and electrically connect electronic components through conductive pathways, tracks, or signal traces. They are widely utilized across various industries, including consumer electronics, automotive, telecommunications, and healthcare, among others.

The Southeast Asia Printed Circuit Board (PCB) Market Report is Segmented by PCB Type (Standard Multilayer, Rigid 1-2 Sided, High-Density Interconnect, Flexible Circuits, IC Substrates, Rigid-Flex, and Other PCB Types), Substrate Material (Glass Epoxy, High-Speed Low-Loss, Polyimide, Packaging Resins, and Other Substrate Materials), End-user Industry (Consumer Electronics, Computing and Data Centers, Telecommunications and 5G, Automotive and EV, Industrial and Power, Healthcare and Medical, Aerospace and Defense, and Other End-user Industries), and Country (Indonesia, Malaysia, Philippines, Singapore, Thailand, Vietnam, Rest of Southeast Asia). The Market Forecasts are Provided in Terms of Value (USD).

| Standard Multilayer (non-HDI) |

| Rigid 1-2 Sided |

| High-Density Interconnect (HDI) |

| Flexible Circuits (FPC) |

| IC Substrates (Package Substrates) |

| Rigid-Flex |

| Other PCB Types |

| Glass Epoxy (FR-4) |

| High-Speed / Low-Loss |

| Polyimide (PI) |

| Packaging Resins (BT / ABF) |

| Other Substrate Materials |

| Consumer Electronics |

| Computing and Data Centers |

| Telecommunications and 5G |

| Automotive and EV |

| Industrial and Power |

| Healthcare / Medical |

| Aerospace and Defense |

| Other End-user Industries |

| Indonesia |

| Malaysia |

| Philippines |

| Singapore |

| Thailand |

| Vietnam |

| Rest of Southeast Asia |

| By PCB Type | Standard Multilayer (non-HDI) |

| Rigid 1-2 Sided | |

| High-Density Interconnect (HDI) | |

| Flexible Circuits (FPC) | |

| IC Substrates (Package Substrates) | |

| Rigid-Flex | |

| Other PCB Types | |

| By Substrate Material | Glass Epoxy (FR-4) |

| High-Speed / Low-Loss | |

| Polyimide (PI) | |

| Packaging Resins (BT / ABF) | |

| Other Substrate Materials | |

| By End-user Industry | Consumer Electronics |

| Computing and Data Centers | |

| Telecommunications and 5G | |

| Automotive and EV | |

| Industrial and Power | |

| Healthcare / Medical | |

| Aerospace and Defense | |

| Other End-user Industries | |

| By Country | Indonesia |

| Malaysia | |

| Philippines | |

| Singapore | |

| Thailand | |

| Vietnam | |

| Rest of Southeast Asia |

Key Questions Answered in the Report

How big will Southeast Asia’s printed circuit board market demand be by 2031?

The Southeast Asia printed circuit board (PCB) market is forecast to reach USD 10.12 billion by 2031, growing at a 4.41% CAGR from 2026.

Which board type is expanding the quickest?

Flexible circuits lead growth at a 5.23% CAGR, buoyed by wearables, foldable phones and vehicle-display adoption.

Why are low-loss laminates gaining share?

5G radios and 800 Gbps switches need dissipation factors below 0.003, so high-speed materials such as Rogers RO4350B are replacing FR-4 in telecom gear.

What makes Vietnam the fastest-growing location?

Large greenfield projects from Meiko Electronics, Samsung Display and duty-free EU access underpin Vietnams 5.58% geographic CAGR.

How are suppliers coping with copper price spikes?

Larger fabricators hedge futures and optimize scrap, whereas SMEs renegotiate contracts or absorb lower margins, dampening growth by 0.8 percentage points.

What technologies are leaders investing in?

Modified semi-additive processes that create 15 µm traces, automated optical inspection and laser DI are the main focus areas for capacity upgrades.

Page last updated on: