Southeast Asia Electronics Manufacturing Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

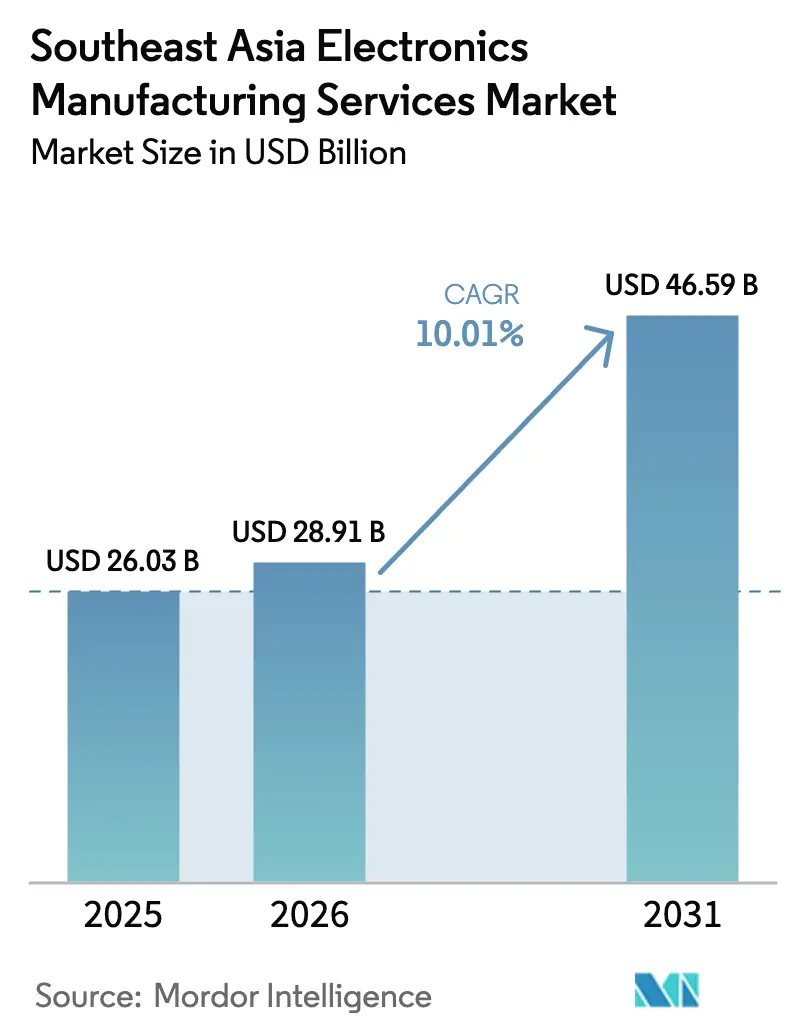

| Base Year Market Size (2025) | USD 26.03 Billion |

| Market Size (2026) | USD 28.91 Billion |

| Market Size (2031) | USD 46.59 Billion |

| Growth Rate (2026 - 2031) | 10.01% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Southeast Asia Electronics Manufacturing Services Market Analysis by Mordor Intelligence

Southeast Asia electronics manufacturing services market size in 2026 is estimated at USD 28.91 billion, growing from 2025 value of USD 26.03 billion with projections showing USD 46.59 billion, growing at 10.01% CAGR over 2026-2031. Expanding foreign direct investment, government incentive packages, and the China+1 diversification push are combining to elevate ASEAN as a preferred production base. Sustained spending on consumer electronics, rapid growth in electric-vehicle platforms, and hyperscaler demand for AI hardware are keeping factory utilization high. Large contract manufacturers are deepening regional automation to improve yield, while regional specialists are winning design-centric programs that favor shorter product life cycles. Rising ESG compliance costs and lingering component supply risks temper the otherwise upbeat outlook.

Key Report Takeaways

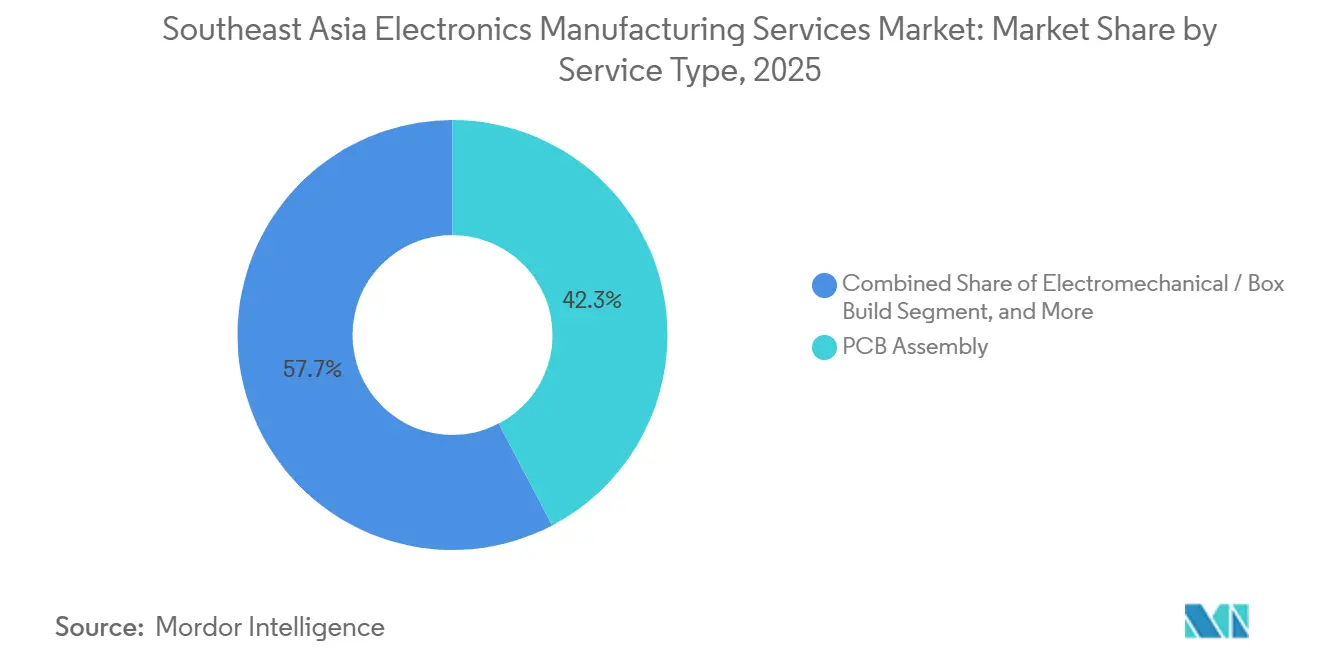

- By service type, PCB assembly accounted for 42.33% of the Southeast Asia electronics manufacturing services market share in 2025, while electromechanical assembly and box build are forecast to expand at a 11.12% CAGR through 2031.

- By business model, contract manufacturing accounted for 63.19% of the Southeast Asia electronics manufacturing services market share in 2025, and hybrid and turnkey models are advancing at a 10.66% CAGR through 2031.

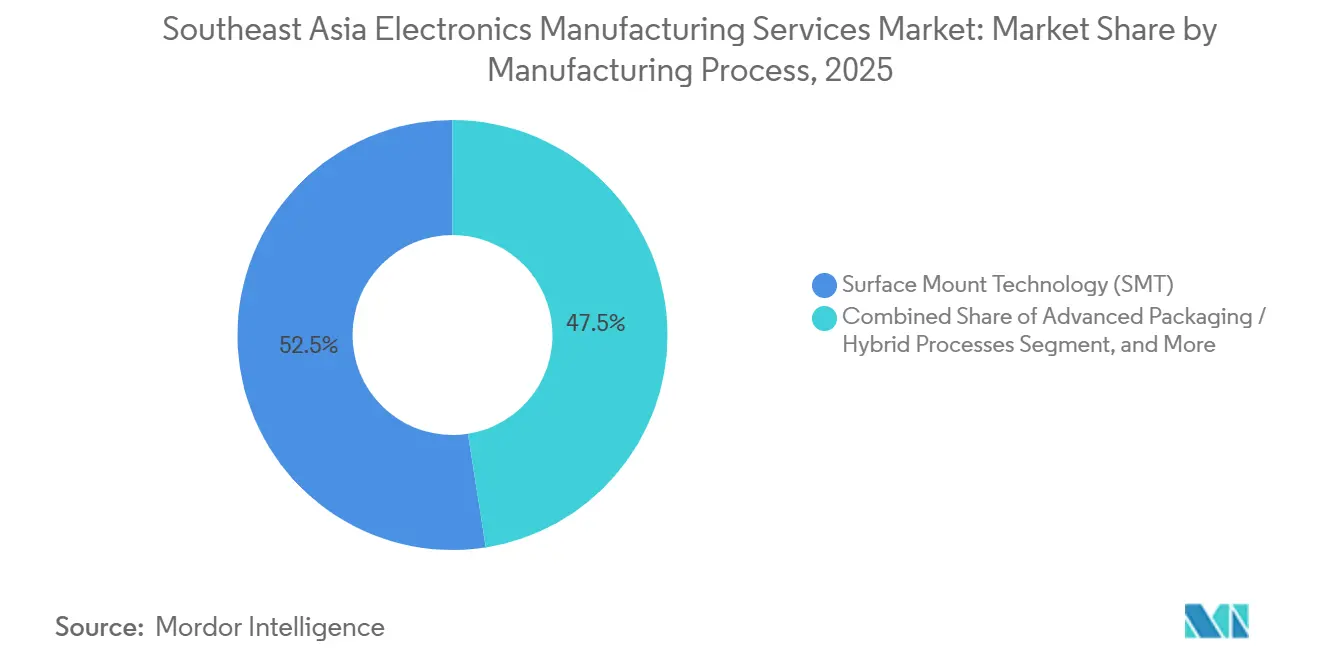

- By manufacturing process, surface-mount technology accounted for 52.47% of the Southeast Asia electronics manufacturing services market in 2025, whereas advanced packaging and hybrid processes are set to grow at a 10.71% CAGR through 2031.

- By end-user, automotive electronics is expected to expand at an 11.93% CAGR between 2026 and 2031, outpacing consumer electronics, which led with 33.67% of the Southeast Asia EMS market share in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Southeast Asia Electronics Manufacturing Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing Outsourcing of Electronics Production by OEMs | +2.3% | Global, with concentration in Vietnam, Thailand, Malaysia | Medium term (2-4 years) |

| Booming Consumer Electronics Demand in ASEAN Middle-Class | +1.8% | Indonesia, Philippines, Vietnam, Thailand | Short term (≤ 2 years) |

| Government Incentives and Free-Trade Zones in Southeast Asian Countries | +1.5% | Vietnam, Thailand, Malaysia, Indonesia, Philippines | Long term (≥ 4 years) |

| China+1 Supply-Chain Diversification Strategy | +1.4% | Vietnam, Thailand, Malaysia, with spillover to Indonesia | Medium term (2-4 years) |

| Adoption of Advanced Packaging in Emerging EMS Hubs such as Vietnam | +1.2% | Vietnam, Malaysia, Singapore | Long term (≥ 4 years) |

| Rise of Local Design Houses Collaborating with EMS Providers | +0.9% | Malaysia, Singapore, Vietnam, Philippines | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increasing Outsourcing of Electronics Production by OEMs

Brand-name OEMs are allocating a growing share of final assembly and test work to regional EMS partners, enabling internal capital to focus on R&D. Apple’s February 2025 agreement with Indonesia includes a USD 150 million AirTag plant and a semiconductor R&D center, reinforcing a shift toward localized accessory manufacturing. Samsung Electro-Mechanics committed PHP 50.7 billion to an automotive MLCC line in the Philippines, scheduled to be operational by 2027.[1]Alexis Romero, “Samsung investing P50 billion more in Philippines,” philstar.com Similar moves in power IC assembly for electric vehicles illustrate how outsourcing now spans consumer, automotive, and industrial products. This trend is shortening product cycles and pushing EMS firms to invest in rapid prototyping and new-product-introduction lines.

Booming Consumer Electronics Demand in the ASEAN Middle Class

Higher disposable income and smartphone adoption are expanding local demand for appliances, wearables, and smart-home devices. Panasonic earmarked PHP 3 billion to convert part of its Laguna, Philippines, campus to domestic production beginning in 2026. Vietnam-based PISEN Tech scaled power-bank output for regional brands, underlining a pivot to higher-mix, lower-volume runs. As local brands strive for cost competitiveness, EMS providers must maintain flexible lines and quick changeovers.

Government Incentives and Free-Trade Zones in Southeast Asian Countries

Tax holidays, duty-free capital imports, and infrastructure co-investment underpin the region’s FDI boom. Samsung’s Philippine expansion benefited from the first Presidential Incentives package under the CREATE MORE Act, covering a five-year income-tax holiday and duty exemptions.[2]Bam Natividad, “Samsung to inject PHP 50.7 billion for Philippine expansion,” gizguide.com Thailand’s Board of Investment extended similar breaks in its Eastern Economic Corridor, saving Celestica roughly USD 44 million in 2024 taxes. Time-bound incentives are creating urgency for EMS investors to lock in capacity while requirements for local sourcing and job creation grow stricter.

China+1 Supply-Chain Diversification Strategy

Multinationals are rebalancing global footprints to mitigate geopolitical and tariff risks. LG added USD 1.7 billion to its Indonesian EV battery facility in April 2025. Celestica shrank China’s share of revenue to 5% in 2024 while scaling Thai and Malaysian sites for AI networking hardware.[3]Celestica Inc., “Annual Report on Form 10-K for fiscal year ended December 31 2024,” celestica.com These moves preserve China's domestic sales operations but redirect export-oriented production toward tariff-advantaged ASEAN locations under the Regional Comprehensive Economic Partnership.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Supply-Chain Disruptions and Component Shortages | -0.8% | Global, acute in Vietnam, Thailand, Indonesia | Short term (≤ 2 years) |

| Infrastructure Constraints in Emerging ASEAN Countries | -0.7% | Indonesia, Philippines, Vietnam (secondary cities) | Medium term (2-4 years) |

| Talent Shortages in High-Skill Manufacturing | -0.5% | Vietnam, Indonesia, Philippines | Medium term (2-4 years) |

| Rising ESG Compliance Costs for EMS Exporters | -0.4% | Global, with higher burden on smaller regional players | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Supply-Chain Disruptions and Component Shortages

Tight supplies of automotive-grade semiconductors and MLCCs persisted into early 2025. Celestica reported elevated inventory and continued supplier-managed programs to buffer single-source risks, yet margins came under pressure when demand signals shifted. Smaller EMS firms without scale purchasing or customer cash deposits faced canceled orders, highlighting the importance of diversified sourcing and resilient logistics.

Infrastructure Constraints in Emerging ASEAN Countries

Power reliability and port congestion limit scalability in Indonesia and the Philippines. Manufacturers in Batangas industrial zones still allocate capital to backup generators, and road congestion adds to lead-time variability for imported components. Secondary Vietnamese cities promise lower wages but lack dense supplier clusters, compelling EMS providers to invest in on-site warehousing and workforce training until public infrastructure catches up.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Box Build Gains as OEMs Seek Turnkey Integration

Electromechanical assembly and box-build services are on track for an 11.12% CAGR to 2031, steadily eroding PCB assembly’s 42.33% share recorded in 2025. The Southeast Asia EMS market size for integrated box-build work is expanding as OEMs request enclosure integration and direct-ship logistics in a single contract. Jabil’s Thai partnership with Inno on a 15,000 m² metal-enclosure plant underscores the vertical integration race. PCB assembly remains the entry point for many providers, yet commoditization drives a pivot toward engineering-heavy niches.

Complementary services such as design-for-manufacturability consulting, firmware coding, and validation testing have grown, providing EMS firms with sticky revenue as demand for higher-mix production increases. Logistics services, ranging from reverse logistics to IT asset disposition, bolster lifecycle support. Larger companies are internalizing precision machining and injection molding, following Keiteq Direct’s integrated aluminum die-casting plus PCB model in Malaysia.

By Business Model: Hybrid and Turnkey Models Capture Design-to-Delivery Demand

Contract manufacturing still led with 63.19% of the Southeast Asia EMS market share in 2025, but customers increasingly favor risk-sharing hybrids that fuse design, sourcing, and fulfillment. Hybrid and turnkey arrangements are forecast to post a 10.66% CAGR through 2031, reflecting pressure to compress launch timelines. PISEN Tech’s dual OEM and ODM lines in Thailand illustrate how EMS firms now handle concept, R&D, and full build for clients lacking internal design bandwidth.

Original design manufacturing is concentrated in consumer electronics accessories and industrial IoT devices, where customization drives value. Valuetronics’ cross-functional campus near Hanoi brings together marketing, engineering, and quality teams to deliver cost-down and feature-improvement programs that accelerate time-to-market. These full-stack services demand sizable R&D budgets and robust IP controls, favoring well-capitalized players.

By Manufacturing Process: Advanced Packaging Emerges Alongside SMT Maturity

Surface-mount technology retained 52.47% of revenue in 2025, but demand for chiplet integration and fan-out wafer-level packaging is pushing advanced packaging toward a 10.71% CAGR through 2031. The Southeast Asia EMS market size for advanced packaging is growing fastest in Malaysia and Vietnam, where state support is strongest. ASE Malaysia’s module and wafer-level chip-scale services anchor Penang’s backend cluster.

Through-hole technology persists in power electronics and harsh-environment controls, yet the share is drifting downward. Hybrid lines that blend SMT, through-hole, and advanced packaging are appearing for automotive domain controllers and medical modules. PCBCart’s March 2025 move into HDI and rigid-flex boards in Thailand exemplifies the region’s shift to higher-frequency, high-density interconnects.

By End-User: Automotive Surges as EVs Drive Electronics Intensity

Automotive electronics is projected to grow at an 11.93% CAGR and narrow the gap with consumer electronics, which commanded 33.67% of the Southeast Asia electronics manufacturing services market share in 2025. Samsung Electro-Mechanics’ planned automotive-grade MLCC output in the Philippines underscores the pivot toward EV platforms. EMS Group’s power-IC ramp in Laguna, with volume transfer to Batangas by 2026, highlights local momentum.

The computer and mobile device segments continue to anchor PCB volume demand, particularly in Vietnam and Thailand's assembly hubs. Industrial equipment is benefiting from Industry 4.0 rollouts that require rugged edge gateways. Communication infrastructure, covering 5G radios and datacenter switches, remains a strategic vertical for Celestica’s enlarged Thai and Malaysian plants. The medical module assembly market is enjoying steady growth, supported by ASEAN efforts to harmonize device regulations.

Geography Analysis

Vietnam leads regional growth, propelled by Foxconn, Pegatron, and Luxshare, all of which scaled northern and southern campuses post-2024 to serve smartphone and accessory lines. The government’s emphasis on advanced packaging and semiconductor backend work is widening the country’s value-add, as evidenced by Valuetronics’ multi-functional Hanoi campus, which began phased operations in 2020. Logistics gaps in secondary cities and acute talent shortages in advanced process engineering remain hurdles, yet overall momentum points to continued share gains.

Thailand’s Eastern Economic Corridor remains indispensable for automotive electronics and HDD subassemblies. Jabil’s Rayong enclosure plant for energy-storage systems and Celestica’s AI-hardware expansions typify Thailand’s diversification beyond legacy storage into energy transition and datacenter hardware. PCBCart’s HDI and rigid-flex project underscores 5G and radar demand. Incentive schemes run through 2029, giving investors a medium-term tax window. Malaysia continues to anchor advanced packaging in Penang. ASE Malaysia’s IC substrate expertise dovetails with the March 2025 Arm-Malaysia chip-design center that will feed custom silicon into local assembly lines. Jabil’s greenfield Perlis site brings EMS investment to less developed northern states, broadening economic impact.

Indonesia and the Philippines are positioning for large-format assembly and EV supply-chain niches. LG’s USD 1.7 billion battery investment signals Indonesia’s pull for cell and pack production. Apple’s planned Batam AirTag facility and semiconductor R&D center further elevate Indonesia’s profile. The Philippines secured Samsung’s PHP 50.7 billion MLCC expansion and Panasonic’s domestic appliance line, solidifying its dual export and local-market role. Singapore retains a high-tech orientation, hosting planned NXP and VIS 12-inch wafer fabs for automotive and industrial chips. Its precision-engineering base continues to serve high-mix, low-volume contracts in medical and industrial instrumentation.

Competitive Landscape

The regional market is moderately concentrated. Foxconn, Flex, Jabil, Pegatron, and Wistron together accounted for over half of billings in 2025, leveraging automation, global sourcing muscle, and multi-site redundancy. Celestica produced roughly 70% of its 2024 revenue in Asia and plowed fresh capital into Thai and Malaysian lines for AI networking hardware. Regional champions such as Venture Corporation, SVI Public Company, and Hana Microelectronics bank on proximity to customers and flexible, engineering-heavy models.

Collaborations between local design houses and EMS players are a budding differentiator. Malaysia-based SMD Semiconductor provides RISC-V and mixed-signal design services, delivering turnkey solutions for automotive, energy, and smart health devices. Synopsys’ EDA tool adoption by Philippine layout firms is elevating local analog-IC capabilities. Technology upgrades include AI-assisted visual inspection and digital twins to trim downtime.

Cost headwinds, increasingly stringent ESG mandates, and the ongoing trend of customer consolidation are intensifying competition across the market. In response, scale providers are placing a stronger emphasis on vertical integration to enhance their competitive positioning and operational efficiency. At the same time, mid-tier specialists are actively pursuing strategic design partnerships as a means to differentiate themselves and avoid being drawn into purely price-driven competition.

Southeast Asia Electronics Manufacturing Services Industry Leaders

Foxconn Technology Group

Flex Ltd

Jabil Inc

Pegatron Corporation

Sanmina Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Panasonic Manufacturing Philippines registered a new PEZA project in Laguna Technopark to begin domestic production of fans, refrigerators, and washing machines in 2026.

- November 2025: Samsung Electro-Mechanics secured a PHP 50.7 billion incentive-backed expansion in Laguna to build automotive-grade MLCCs, targeting July 2027 operations.

- April 2025: Pegatron opened a 5G-enabled smart factory in Batam, Indonesia, marking the region’s most advanced manufacturing base.

- April 2025: LG committed an additional USD 1.7 billion to its Indonesian EV battery complex, slated for completion in 2025.

Southeast Asia Electronics Manufacturing Services Market Report Scope

The Southeast Asia Electronics Manufacturing Services Market Report is Segmented by Service Type (Electronics Manufacturing Services, Engineering Services, Test and Development Implementation Services, Logistics Services, Other Service Types), Business Model (Contract Manufacturing (CM), Original Design Manufacturing (ODM), Hybrid / Turnkey / Other Business Models), Manufacturing Process (Surface Mount Technology (SMT), Through-Hole Technology (THT), Advanced Packaging / Hybrid Processes), End-user (Mobile Devices, Consumer Electronics, Computer, Industrial, Automotive, Communication, Lighting, Medical, Other End-users). The Market Forecasts are Provided in Terms of Value (USD).

| Electronics Manufacturing Services | PCB Assembly |

| Electromechanical Assembly/Box Build | |

| Prototyping | |

| Other Electronics Manufacturing Services | |

| Engineering Services | |

| Test and Development Implementation Services | |

| Logistics Services | |

| Other Service Types |

| Contract Manufacturing (CM) |

| Original Design Manufacturing (ODM) |

| Hybrid / Turnkey / Other Business Models |

| Surface Mount Technology (SMT) |

| Through-Hole Technology (THT) |

| Advanced Packaging / Hybrid Processes |

| Mobile Devices (Smartphones and Tablets) |

| Consumer Electronics |

| Computer (PCs/Desktop/Laptops) |

| Industrial |

| Automotive |

| Communication |

| Lighting |

| Medical |

| Other End-users |

| By Service Type | Electronics Manufacturing Services | PCB Assembly |

| Electromechanical Assembly/Box Build | ||

| Prototyping | ||

| Other Electronics Manufacturing Services | ||

| Engineering Services | ||

| Test and Development Implementation Services | ||

| Logistics Services | ||

| Other Service Types | ||

| By Business Model | Contract Manufacturing (CM) | |

| Original Design Manufacturing (ODM) | ||

| Hybrid / Turnkey / Other Business Models | ||

| By Manufacturing Process | Surface Mount Technology (SMT) | |

| Through-Hole Technology (THT) | ||

| Advanced Packaging / Hybrid Processes | ||

| By End-user | Mobile Devices (Smartphones and Tablets) | |

| Consumer Electronics | ||

| Computer (PCs/Desktop/Laptops) | ||

| Industrial | ||

| Automotive | ||

| Communication | ||

| Lighting | ||

| Medical | ||

| Other End-users |

Key Questions Answered in the Report

How large will Southeast Asia’s EMS demand be by 2031?

The Southeast Asia electronics manufacturing services market size is projected to reach USD 46.59 billion by 2031.

Which service category is growing fastest?

Electromechanical assembly and box-build work are forecast to grow at an 11.12% CAGR, the quickest among service types.

Why are OEMs shifting production to ASEAN?

Diversification away from China, generous government incentives, and proximity to expanding local consumer markets are drawing OEMs toward Vietnam, Thailand, Malaysia, Indonesia, and the Philippines.

Which end-user vertical offers the highest growth?

Automotive electronics is expected to expand at an 11.93% CAGR through 2031, buoyed by electric-vehicle and ADAS adoption.

What is the main operational risk in the region?

Ongoing component shortages and infrastructure gaps, especially in power and port logistics, pose near-term constraints.

Who are the key EMS players in Southeast Asia?

Foxconn, Jabil, Flex, Pegatron, Wistron, and Celestica lead on regional scale, while Venture Corporation, SVI, and Hana Microelectronics specialize in flexible, value-added programs.

Page last updated on: