Southeast Asia Customer Data Platform Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 0.25 Billion |

| Market Size (2026) | USD 0.34 Billion |

| Market Size (2031) | USD 1.48 Billion |

| Growth Rate (2026 - 2031) | 34.20% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Southeast Asia Customer Data Platform Market Analysis by Mordor Intelligence

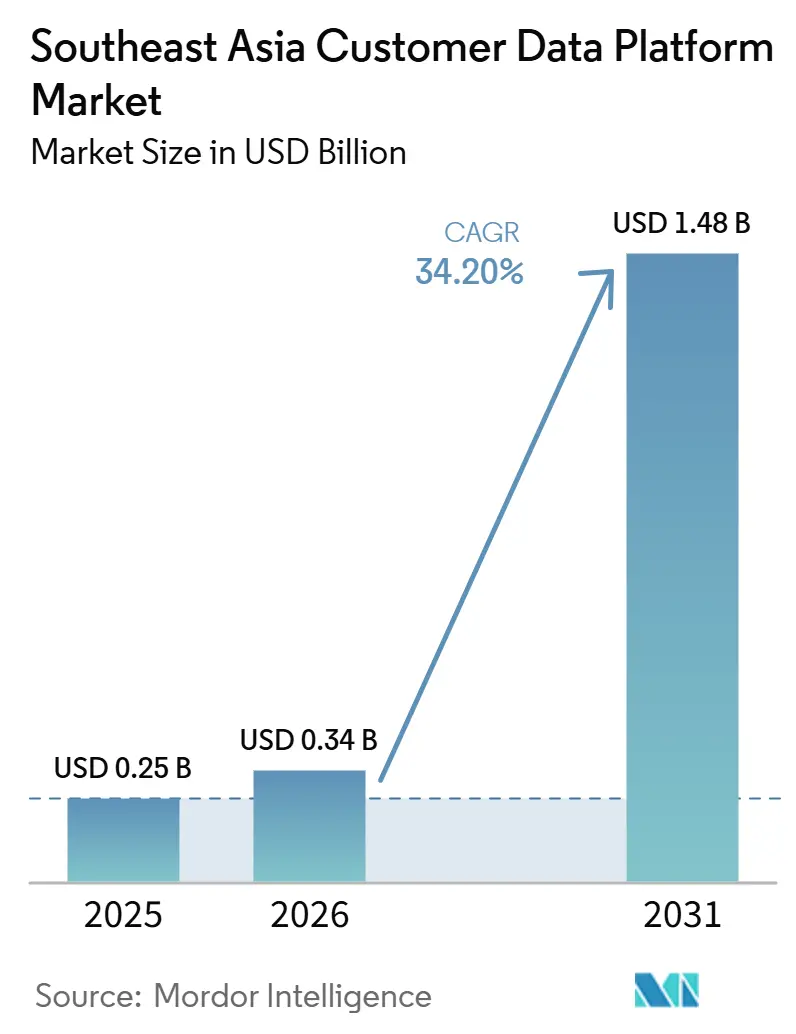

The Southeast Asia customer data platform market size was valued at USD 0.25 billion in 2025 and estimated to grow from USD 0.34 billion in 2026 to reach USD 1.48 billion by 2031, at a CAGR of 34.20% during the forecast period 2026-2031. The growth path is tied to structural changes in how enterprises collect, organize, and use customer information, because regional businesses now face stricter privacy duties at the same time that digital commerce generates far more customer interactions than older CRM systems were built to handle. The Southeast Asia customer data platform market is also benefiting from the steady shift toward first-party data strategies, since brands can no longer rely on older third-party targeting methods and now need a unified record of customer behavior, consent, and preferences across channels. Demand is rising further as retail, financial services, healthcare, and telecom companies move from simple data collection to real-time activation, where the value of a platform depends on how quickly it can turn a customer signal into a message, recommendation, or service action. The competitive field is widening because global vendors are expanding local data residency and cloud delivery, while regional providers are using faster implementation cycles and local channel integrations to win buyers that were not well served by older enterprise-heavy offerings. The Southeast Asia customer data platform market is therefore moving into a phase where compliance readiness, ease of deployment, and AI-based automation matter as much as core data unification features.

Key Report Takeaways

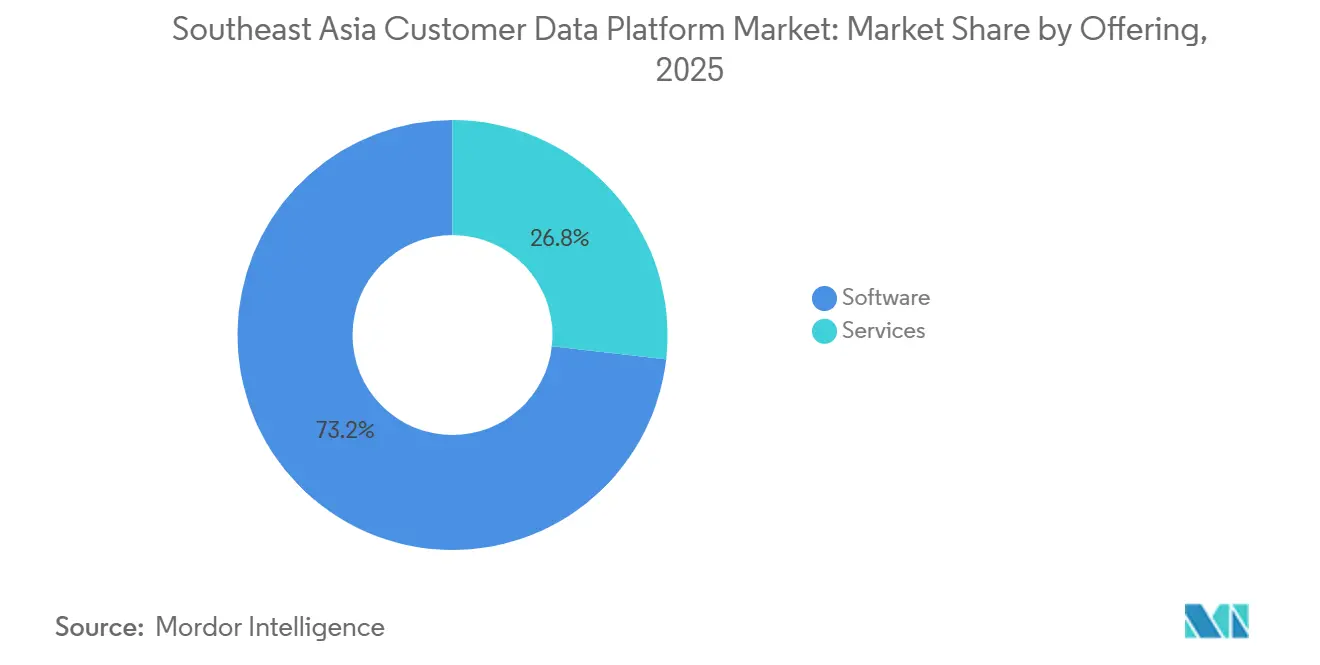

- By offering, software held a 73.21% share of the Southeast Asia customer data platform market in 2025, while services are projected to expand at a 35.87% CAGR through 2031.

- By deployment mode, cloud held 71.42% of the Southeast Asia customer data platform market share in 2025 and is expected to remain the fastest-growing deployment model at a 36.28% CAGR through 2031.

- By organization size, large enterprises accounted for 63.47% share in 2025, while small and medium enterprises are projected to grow at a 36.39% CAGR through 2031.

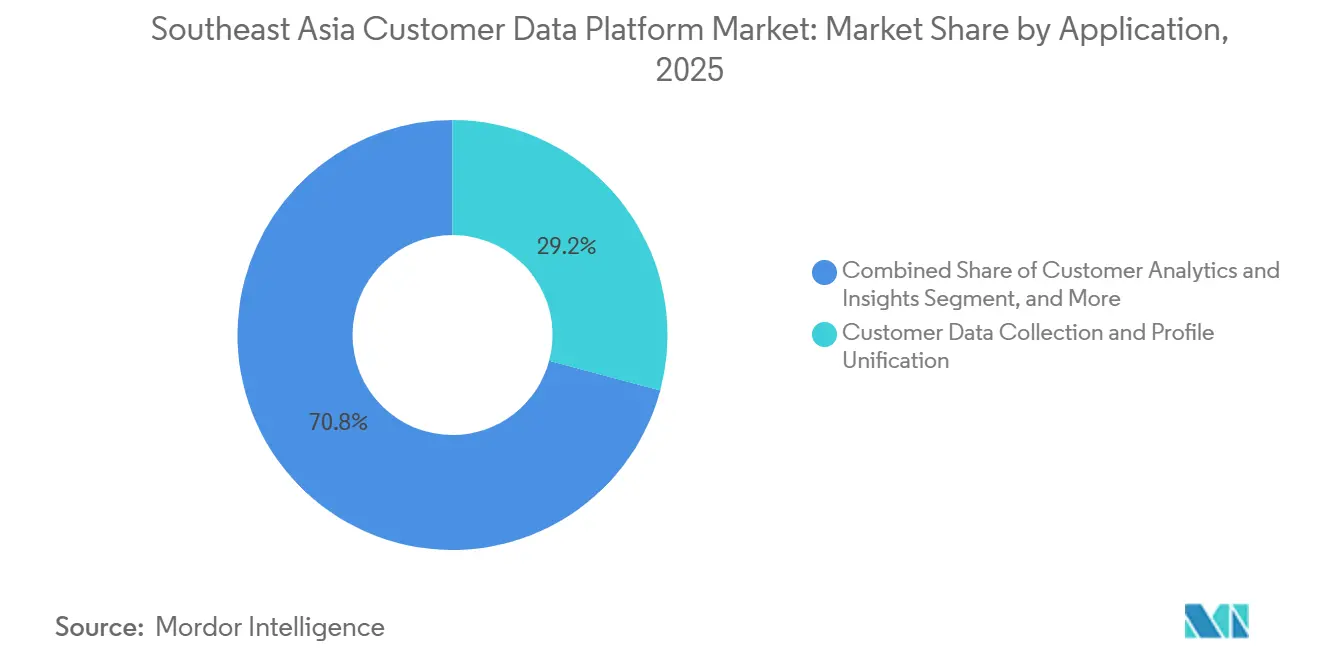

- By application, customer data collection and profile unification accounted for 29.16% share in 2025, while audience segmentation and personalization are projected to expand at a 37.54% CAGR through 2031.

- By end-user industry, retail and e-commerce held 27.83% share in 2025, while healthcare and life sciences are projected to grow at a 36.81% CAGR through 2031.

- By geography, Singapore accounted for 29.57% of the Southeast Asia customer data platform market in 2025, while Indonesia is projected to expand at a 36.12% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Southeast Asia Customer Data Platform Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Rising First-Party Data Prioritization Across Digital Businesses | +4.2% | Global, with ASEAN core concentration in Singapore, Indonesia, and Thailand | Short term (≤ 2 years) |

| Real-Time Personalization Demand in Retail and E-Commerce | +3.8% | ASEAN core, Indonesia, Vietnam, Thailand, Philippines | Short term (≤ 2 years) |

| Privacy-Driven Replacement of Cookie-Based Targeting | +3.5% | Global, spillover to all Southeast Asian markets by 2026 | Short term (≤ 2 years) |

| Expansion of Omnichannel Customer Engagement Stacks | +3.1% | APAC core, expanding into Malaysia, Vietnam, Philippines | Medium term (2-4 years) |

| Growth of Cloud-Native MarTech and AdTech Integration | +2.7% | APAC core, spillover to rest of Southeast Asia | Medium term (2-4 years) |

| Cross-Border Digital Commerce Expansion in Southeast Asia | +2.4% | ASEAN regional, with early concentration in Singapore and Indonesia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising First-Party Data Prioritization Across Digital Businesses

The phaseout of older third-party targeting tools has made first-party data a core operating need rather than a marketing option. In Southeast Asia, the issue is sharper because many customer interactions happen inside closed digital environments, which limit how much behavior brands can observe unless they collect it directly. A customer data platform helps solve this problem by bringing consented customer signals into one record that can be used across sales, service, analytics, and campaign channels. The Southeast Asia customer data platform market is gaining from this shift because firms that organize direct customer data early can build stronger identity records and more reliable audience models over time. That creates a practical advantage in retention, personalization, and compliance, especially for brands that operate across several local platforms and messaging channels. The need for portable and usable customer profiles is therefore becoming a lasting demand driver for new deployments and platform upgrades.

Real-Time Personalization Demand in Retail And E-Commerce

Retailers and online sellers across the region are moving from broad campaign targeting to real-time response based on customer intent. That change matters because the Southeast Asia customer data platform market now serves buyers who want to react to browsing, messaging, cart, and payment signals as they happen rather than hours later. Video commerce, marketplace selling, and mobile-led shopping have made customer journeys less predictable, so brands need a system that connects events quickly and turns them into the next best action. Platforms that can stream data into decision engines are becoming more relevant than older systems built around delayed batch processing. PT Erajaya Swasembada used Salesforce Data 360 to build a centralized customer view for more personalized campaigns across its brand portfolio. The commercial value now comes less from storing data and more from acting on it before the customer shifts to another seller or channel.

Privacy-Driven Replacement of Cookie-Based Targeting

Privacy regulation is pushing enterprises toward platforms that can manage consent, preferences, and data use rules in a documented way. Singapore put its Personal Data Protection Amendment Regulations 2026 into operation on March 2, 2026, which strengthened several compliance obligations tied to cross-border handling and processor responsibilities.[1]Singapore Statutes Online, “Personal Data Protection (Amendment) Regulations 2026,” Singapore Statutes Online, sso.agc.gov.sg Vietnam enacted Law No. 91/2025/QH15 on Personal Data Protection on June 26, 2025, and the law took effect on January 1, 2026.[2]Vietnam National Assembly, “Law No. 91/2025/QH15 On Personal Data Protection,” Vietnam Government Gazette, congbao.chinhphu.vn Indonesia’s Personal Data Protection Law also remained a central compliance driver after its full enforcement began in October 2024, which raised the need for auditable data handling across enterprise systems. The Southeast Asia customer data platform market is benefiting because these legal changes make consent capture and governed activation part of normal operations, not an optional feature. A platform that records why data was collected and how it is used helps companies lower compliance risk while improving the quality of the customer data they keep.

Expansion of Omnichannel Customer Engagement Stacks

Customer journeys in Southeast Asia move across marketplaces, chat apps, payments, retail sites, and service channels, so enterprises increasingly need one operating layer that can connect those touchpoints. The Southeast Asia customer data platform market is expanding on this requirement because the platform often becomes the coordination point between data collection, customer identity, and activation. Vendors are also adding AI-based workflow automation, which allows campaign triggers and audience actions to run with less manual setup. Tealium launched its full suite on the AWS Singapore Region in March 2026, which gave regional users local data residency and low-latency processing support for broader engagement workflows. Salesforce also expanded Data Cloud and Agentforce investment in Singapore, which reinforced the push toward integrated customer data and engagement environments. As these stacks deepen, buyers are placing more value on platforms that reduce the gap between signal capture and customer action.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Fragmented Customer Identity and Data Silos | -2.8% | All Southeast Asian markets, acute in Indonesia, Thailand, Vietnam | Short term (≤ 2 years) |

| Talent Shortage in Data Engineering and Activation Workflows | -2.1% | Regional, most severe in Philippines, Vietnam, Indonesia | Medium term (2-4 years) |

| Integration Complexity With Legacy CRM and CDW Environments | -1.7% | ASEAN enterprise sector, concentrated in BFSI and large retail | Medium term (2-4 years) |

| Budget Sensitivity Among Mid-Market Buyers | -1.3% | Mid-market segments across all Southeast Asian economies | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Fragmented Customer Identity and Data Silos

Many enterprises still hold customer records in separate systems, including online storefronts, point-of-sale tools, loyalty databases, service desks, and finance applications. This makes identity resolution difficult because the same customer may appear with different attributes, names, or identifiers across systems that were never designed to work together. The Southeast Asia customer data platform market faces friction here because the value of the platform depends on how well these disconnected records can be stitched into one trusted profile. The issue becomes more severe in regional digital environments where key behavioral data sits inside closed apps and marketplace ecosystems. Companies that try to handle this through manual data preparation often add technical debt instead of solving the root data architecture problem. The result is slower deployment, weaker activation quality, and a longer time before buyers see a clear return from the platform.

Talent Shortage in Data Engineering and Activation Workflows

Customer data platforms still require skilled people to define data models, create ingestion pipelines, set identity rules, and connect data to usable campaign logic. That talent is unevenly distributed across Southeast Asia, with stronger pools in Singapore and selected urban hubs than in the rest of the region. The Southeast Asia customer data platform market is, therefore, constrained by the fact that many buyers can purchase software faster than they can build internal capability around it. This gap can delay implementation, limit the number of use cases launched, and raise churn risk when business teams do not see value quickly enough. Salesforce launched a startup program in Malaysia and the Philippines in January 2026 to widen access to Data Cloud and AI tools, which also reflects the need for simpler onboarding and partner-led support models. Vendors that reduce the skill burden through templates, guided setup, and easier audience building are likely to perform better with small and mid-sized buyers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering: Services Erode Software’s Revenue Lead

Software held 73.21% of Southeast Asia's customer data platform market share in 2025, which shows that licensing and subscription revenue still formed the base of most enterprise purchases. That position reflected the strength of established platform vendors that had already built recognized products, broad integration ecosystems, and regional data handling capabilities. In the Southeast Asia customer data platform market, software remained the first spending category because enterprises still needed a core platform before they could widen use cases across analytics, personalization, and compliance. The leading software role was especially clear in large organizations that preferred proven enterprise tools with strong governance controls and multi-country deployment options. This kept software at the center of buyer budgets even as implementation needs grew more complex.

Services are projected to expand at a 35.87% CAGR between 2026 and 2031, which is faster than the broader market and signals a change in how buyers want value delivered. Many organizations now care less about feature lists and more about how quickly they can move from purchase to their first usable audience, customer journey, or compliance workflow. That is why managed services, implementation consulting, and integration support are taking a larger role in contract design. The Southeast Asia customer data platform market is seeing this pattern most clearly in regulated fields such as BFSI and healthcare, where data governance work can slow deployment if the vendor leaves too much of the setup burden with the buyer. This shift does not weaken software demand, but it does show that platform adoption increasingly depends on service depth, partner support, and the ability to shorten time to value.

By Deployment Mode: Cloud Becomes the Default Architecture

Cloud accounted for 71.42% of the Southeast Asia customer data platform market size in 2026, which confirmed that hosted delivery had become the default architecture for most new projects. The main reason was practical rather than theoretical, since regional buyers needed infrastructure that could handle high event volumes, rapid scaling, and faster deployment across multiple business units. The Southeast Asia customer data platform market has leaned toward cloud because customer interactions now come from mobile commerce, messaging, marketplaces, apps, and service channels that create a large and continuous stream of data. Cloud environments are better suited to process this activity in near real time without the cost and maintenance burden of expanding local hardware for each new use case. This architecture also made it easier for vendors to add AI tools, security controls, and new integrations without long upgrade cycles.

On-premises deployment still mattered in selected public sector and regulated enterprise settings, where physical control over customer records remained an important governance preference. Even so, that position was under pressure as major cloud providers expanded local regions and vendors aligned their offerings with regional compliance needs. Tealium’s March 2026 launch on the AWS Singapore Region showed how data residency support could remove a long-standing objection to hosted deployment for regional users. Hybrid models also retained a role for companies that wanted to keep sensitive attributes on local systems while using the cloud for behavioral event processing and activation. The balance of demand still favored cloud strongly, which suggests that future competition will center on performance, data residency, and ease of integration rather than on the basic delivery model itself.

By Organization Size: SME Momentum Challenges Enterprise Primacy

Large enterprises held 63.47% share of spending in 2025, which reflected the bigger contract values typical of banks, telecom groups, multinational retailers, and other complex organizations. These buyers often run multiple brands, channels, and countries, so they need stronger data governance, deeper integration support, and more advanced identity management than smaller firms. In the Southeast Asia customer data platform market, large enterprises also moved earlier because they had both the budget and the internal teams required to justify broader data platform investments. That early lead helped them shape vendor road maps, reference projects, and local partner ecosystems. It also meant that many of the largest software wins in the region were tied to enterprise-wide data modernization rather than to a single campaign use case.

Small and medium enterprises are projected to expand at a 36.39% CAGR between 2026 and 2031, and the Southeast Asia customer data platform market size for SMEs is therefore rising faster than for any other organization group. This signals that the buyer base is widening beyond early enterprise adopters into firms that need simpler and more modular tools. Usage-based pricing, SaaS delivery, and faster setup have lowered entry barriers for businesses that manage customers across marketplaces, messaging apps, and direct storefronts. Salesforce’s startup program for Malaysia and the Philippines showed how major vendors are already adjusting their go-to-market approach to capture this emerging demand pool.[3]Salesforce, “Salesforce Launches Startup Program in Malaysia and the Philippines Strengthening Innovation Ecosystem in ASEAN,” Salesforce, salesforce.com As SME adoption grows, vendors that support quicker onboarding and lower technical overhead are likely to gain ground against heavier enterprise-first offerings.

By Application: Personalization Outpaces Profile Aggregation

Customer data collection and profile unification accounted for 29.16% of the Southeast Asia customer data platform market size in 2025, which is consistent with a market still building its identity foundation. Before companies can personalize or automate outreach well, they need one trusted customer profile that brings together transactions, preferences, behavior, and consent history. That is why basic profile building remained the largest application area, even while more advanced use cases were growing faster. In the Southeast Asia customer data platform market, many buyers were still formalizing this foundation as they replaced disconnected CRM and campaign data environments with a more usable record structure. The first phase of adoption, therefore, remained tied to unification, data quality, and a single customer view.

Audience segmentation and personalization is projected to grow at a 37.54% CAGR between 2026 and 2031, which shows that the market is shifting from collection toward activation. Buyers increasingly judge platform value by whether the system can help them decide who to target, what to offer, and when to act. Twilio released Segment AI for general availability in June 2025, including Generative Audiences and recommendation tools that reduced the skill barrier for audience creation.[4]Twilio, “Twilio Segment AI Releases General Availability,” Twilio, twilio.com Consent and preference management is also becoming more central because Singapore, Vietnam, and Indonesia now require stronger control and documentation around how customer data is used. The practical result is that platform road maps are moving toward real-time activation and governed personalization, not just toward bigger data stores.

By End-User Industry: Healthcare Challenges Retail’s First-Mover Lead

Retail and e-commerce held 27.83% share in 2025, which kept the sector in the lead due to its strong digital acquisition activity and direct need for real-time customer engagement. Sellers in this segment handle frequent browsing, cart activity, repeat purchase signals, and campaign response data, so they were among the earliest buyers of customer data platforms. The Southeast Asia customer data platform market has a natural fit with retail because the commercial payoff from better targeting and faster response can be seen quickly in conversion, retention, and basket outcomes. Retail teams also tend to work across many channels, which makes unified profiles and cross-channel activation especially useful. That first-mover advantage helped the segment establish the largest end-user position by 2025.

Healthcare and life sciences is projected to expand at a 36.81% CAGR between 2026 and 2031, making it the fastest-growing end-user vertical in the draft. Growth here is linked to private hospital expansion, digital patient engagement, and the need for more structured management of healthcare professional relationships. DKSH Healthcare and Euris launched ConnectPlus in November 2024, and the Thailand rollout began in January 2025 as one of the clearer examples of a regional healthcare-focused engagement platform with a 360-degree view of professionals. BFSI remained another important demand center because banks and insurers are under steady pressure to improve customer data governance, consent handling, and service personalization. This means the Southeast Asia customer data platform market is broadening beyond retail into verticals where trust, regulation, and lifecycle management are just as important as marketing efficiency.

Geography Analysis

Singapore held 29.57% of Southeast Asia customer data platform market share in 2025, which kept it as the largest country market in the region. That position reflected its role as the regional base for many global software vendors and multinational enterprise buyers. The Southeast Asia customer data platform market in Singapore also benefited from stronger local partner capability, enterprise budgets, and a more mature compliance culture than most neighboring markets. The Personal Data Protection framework continued to shape buying decisions, and penalties under the amended regime can scale to 10% of annual Singapore turnover in certain cases. Salesforce announced a USD 1 billion investment in Singapore in March 2025, including further work around Data Cloud and local data residency, which reinforced the country’s role as a lead deployment hub. As a result, new capabilities introduced in Singapore often shape vendor and buyer expectations across the wider region.

Indonesia is projected to expand at a 36.12% CAGR between 2026 and 2031, making it the fastest-growing geography in the Southeast Asia customer data platform market. The country combines a large digital economy, broad online commerce activity, and a growing need for governed customer data infrastructure. New Zealand’s Ministry of Foreign Affairs and Trade estimated Indonesia’s digital economy at USD 146 billion in 2025, which supports the scale argument behind higher technology demand.[5]New Zealand Ministry of Foreign Affairs and Trade, “Indonesia’s Digital Economy - November 2025,” New Zealand Ministry of Foreign Affairs and Trade, mfat.govt.nz Salesforce expanded local data residency in Indonesia in July 2025 across Data Cloud and related products, which showed direct vendor alignment with local compliance and enterprise demand. Indonesia’s growth path is therefore supported by both demand-side digital expansion and supply-side vendor investment in local infrastructure.

Malaysia, Thailand, Vietnam, and the Philippines formed the next tier of opportunity in the Southeast Asia customer data platform market, though each country had a different trigger for demand. Malaysia’s appeal came from a mix of retail digitization and a relatively mature banking base that supported broader enterprise data projects. Thailand’s relevance increased as privacy enforcement moved from awareness to action, which pushed delayed consent and customer data architecture projects closer to purchase decisions. Vietnam became more important after Law No. 91/2025/QH15 took effect on January 1, 2026, giving enterprises a clearer statutory framework around personal data handling. The Philippines remained smaller in absolute terms, but rising digital activity in banking, telecom, and online commerce continued to build a stronger base for future enterprise CDP adoption.

Competitive Landscape

The Southeast Asia customer data platform market is moderately fragmented, and the draft does not show any single company with category-defining control. Competition is spread across global CRM vendors, data platform specialists, and a growing set of ASEAN-focused providers with local implementation models. In this market, buyers are not choosing on core profile storage alone, because most serious vendors can now claim strong data unification capability. The main comparison points have shifted toward local data residency, AI-led activation, integration breadth, and how quickly a customer can move from setup to measurable use. That is why the Southeast Asia customer data platform market has become more competitive, even without a dominant share leader.

Large vendors are strengthening their position by tying customer data platforms more closely to wider cloud, analytics, and automation portfolios. Salesforce’s investment in Singapore and its data residency expansion in Indonesia are examples of how major vendors are using infrastructure and compliance alignment to deepen regional trust. Twilio’s 2025 release of Segment AI and later real-time journey and data residency capabilities showed a similar push toward easier activation and governed use of customer data. Zeta Global’s March 2026 general availability launch of Athena and its June 2026 strategic partnership with Palantir highlighted how AI decisioning and enterprise data governance are being tied more tightly together. These moves show that major participants are trying to own more of the workflow around data, insight, and action instead of competing on a narrow CDP definition.

Regional opportunity remains meaningful for providers that build around local channel behavior, local compliance, and faster deployment support. The Southeast Asia customer data platform market still has space for vendors that understand how customer signals flow through super apps, local messaging channels, and marketplace-heavy selling models. That is one reason the field remains open to ASEAN-native competitors and vertical specialists, especially in SME and sector-specific use cases. Amplitude’s January 2026 acquisition of InfiniGrow and its February 2026 launch of Agentic AI Analytics also showed that the competitive line is moving toward clearer measurement of business outcomes, not just data visibility. Over time, vendors that combine regional fit with lower implementation friction are likely to be the hardest challengers for global platforms that were originally designed for more open Western data environments.

Southeast Asia Customer Data Platform Industry Leaders

Twilio Segment Inc.

Adobe Inc.

Salesforce, Inc.

SAP SE

Oracle Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Zeta Global and Palantir Technologies announced a 7-year strategic partnership aimed at generating USD 100 million in annual combined revenue, integrating Palantir Foundry's operational data governance with Zeta's AI decisioning layer, Athena by Zeta, to create an enterprise-grade agentic marketing infrastructure.

- March 2026: Zeta Global launched Athena by Zeta for general availability, an AI agent for enterprise marketing teams that compresses multi-day segmentation analyses to minutes and multi-week campaign workflows to hours.

- February 2026: Amplitude introduced a suite of Agentic AI Analytics agents that continuously analyze product usage patterns, identify behavioral anomalies, and recommend real-time actions. The release included Agent Analytics for tracking AI-agent performance and integration with Claude from Anthropic.

- January 2026: Salesforce launched its Startup Program in Malaysia and the Philippines, providing early-stage companies with access to Data Cloud, Agentforce, and the broader Salesforce partner ecosystem to accelerate AI-native product development in both markets.

Southeast Asia Customer Data Platform Market Report Scope

The Southeast Asia Customer Data Platform Market covers platforms and services across countries such as Singapore, Indonesia, Malaysia, Thailand, Vietnam, and the Philippines that consolidate customer data into unified, centralized profiles. These platforms support identity resolution, real-time integration, segmentation, personalization, and analytics, enabling enterprises to deliver consistent omnichannel customer experiences. Rapid e-commerce growth, mobile-first consumer behavior, and the strong adoption of AI-powered personalization drive the market, while evolving data privacy regulations and the need for scalable martech solutions across diverse digital economies continue to shape market dynamics.

The Southeast Asia Customer Data Platform Market Report is Segmented by Offering (Software, and Services), Deployment Mode (Cloud, On-Premises, and Hybrid) Organization Size (Large Enterprises, and Small and Medium Enterprises), Application (Customer Data Collection and Profile Unification, Audience Segmentation and Personalization, Marketing Campaign and Customer Journey Orchestration, Customer Analytics and Insights, Consent and Preference Management, and Other Applications), End-User Industry (Retail and E-Commerce, Banking, Financial Services, and Insurance (BFSI), Healthcare and Life Sciences, IT and Telecom, Media and Entertainment, Industrial Manufacturing, Government and Public Administrationm and Other End-User Industries). and Country (Singapore, Indonesia, Malaysia, Thailand, Vietnam, Philippines, and the Rest of Southeast Asia). The Market Forecasts are Provided in Terms of Value (USD).

| Software |

| Services |

| Cloud |

| On-Premises |

| Hybrid |

| Large Enterprises |

| Small and Medium Enterprises |

| Customer Data Collection and Profile Unification |

| Audience Segmentation and Personalization |

| Marketing Campaign and Customer Journey Orchestration |

| Customer Analytics and Insights |

| Consent and Preference Management |

| Other Applications |

| Retail and E-Commerce |

| Banking, Financial Services, and Insurance (BFSI) |

| Healthcare and Life Sciences |

| IT and Telecom |

| Media and Entertainment |

| Industrial Manufacturing |

| Government and Public Administration |

| Other End-User Industries |

| Singapore |

| Indonesia |

| Malaysia |

| Thailand |

| Vietnam |

| Philippines |

| Rest of Southeast Asia |

| By Offering | Software |

| Services | |

| By Deployment Mode | Cloud |

| On-Premises | |

| Hybrid | |

| By Organization Size | Large Enterprises |

| Small and Medium Enterprises | |

| By Application | Customer Data Collection and Profile Unification |

| Audience Segmentation and Personalization | |

| Marketing Campaign and Customer Journey Orchestration | |

| Customer Analytics and Insights | |

| Consent and Preference Management | |

| Other Applications | |

| By End-User Industry | Retail and E-Commerce |

| Banking, Financial Services, and Insurance (BFSI) | |

| Healthcare and Life Sciences | |

| IT and Telecom | |

| Media and Entertainment | |

| Industrial Manufacturing | |

| Government and Public Administration | |

| Other End-User Industries | |

| By Country | Singapore |

| Indonesia | |

| Malaysia | |

| Thailand | |

| Vietnam | |

| Philippines | |

| Rest of Southeast Asia |

Key Questions Answered in the Report

How large is the Southeast Asia customer data platform space in 2026?

The Southeast Asia customer data platform market size stood at USD 0.25 billion in 2025, reached USD 0.34 billion in 2026 and is projected to reach USD 1.48 billion by 2031 at a 34.20% CAGR.

What is driving adoption of customer data platforms across Southeast Asia?

The main factors are stricter privacy rules, rising first-party data needs, growth in real-time personalization, and the expansion of omnichannel customer engagement across marketplaces, apps, and messaging channels.

Which application area is growing the fastest in Southeast Asia?

Audience segmentation and personalization is the fastest-growing application, with a projected 37.54% CAGR through 2031, while customer data collection and profile unification remained the largest application segment in 2025.

Which country leads regional demand and which one is growing the fastest?

Singapore held the largest share at 29.57% in 2025, while Indonesia is projected to record the fastest growth at a 36.12% CAGR through 2031.

Which end-user sector creates the strongest current demand?

Retail and e-commerce led with a 27.83% share in 2025 because the sector needs fast customer insight, strong profile unification, and real-time activation across digital channels.

What is the biggest challenge for buyers implementing these platforms?

The main barriers are fragmented customer records across systems and a shortage of staff who can manage data engineering, identity rules, and activation workflows at scale.

Page last updated on: