Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Base Year For Estimation | 2025 |

| Forecast Data Period | 2026 - 2031 |

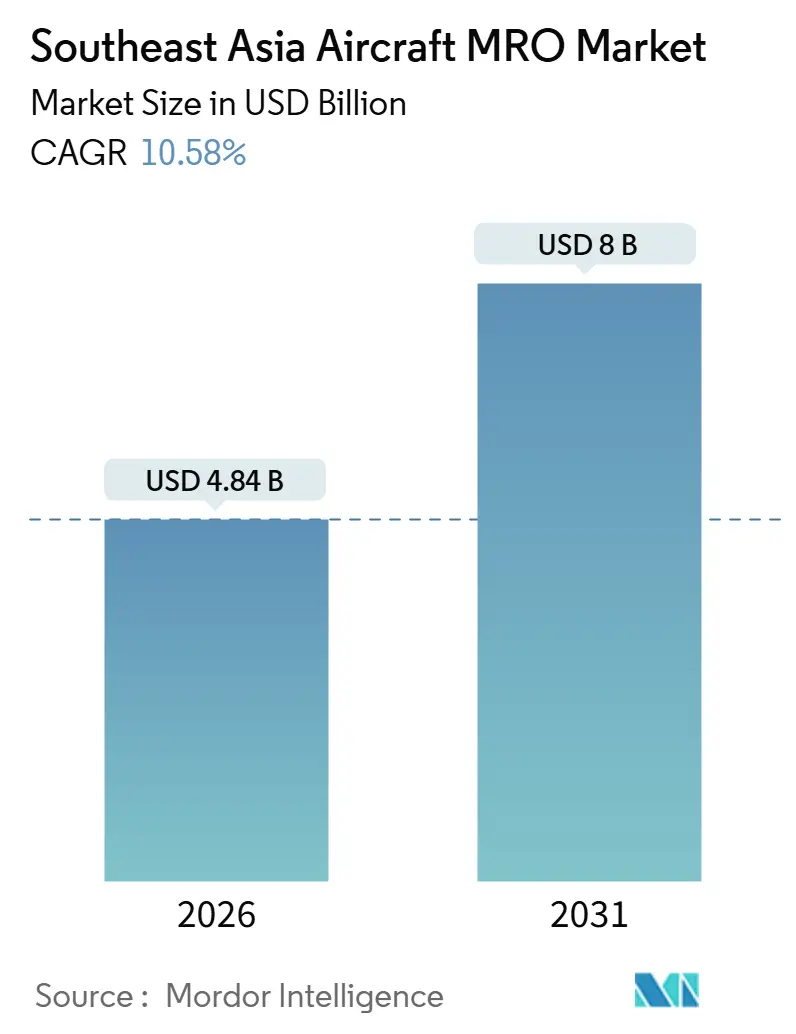

| Market Size (2026) | USD 4.84 Billion |

| Market Size (2031) | USD 8 Billion |

| Growth Rate (2026 - 2031) | 10.58% CAGR |

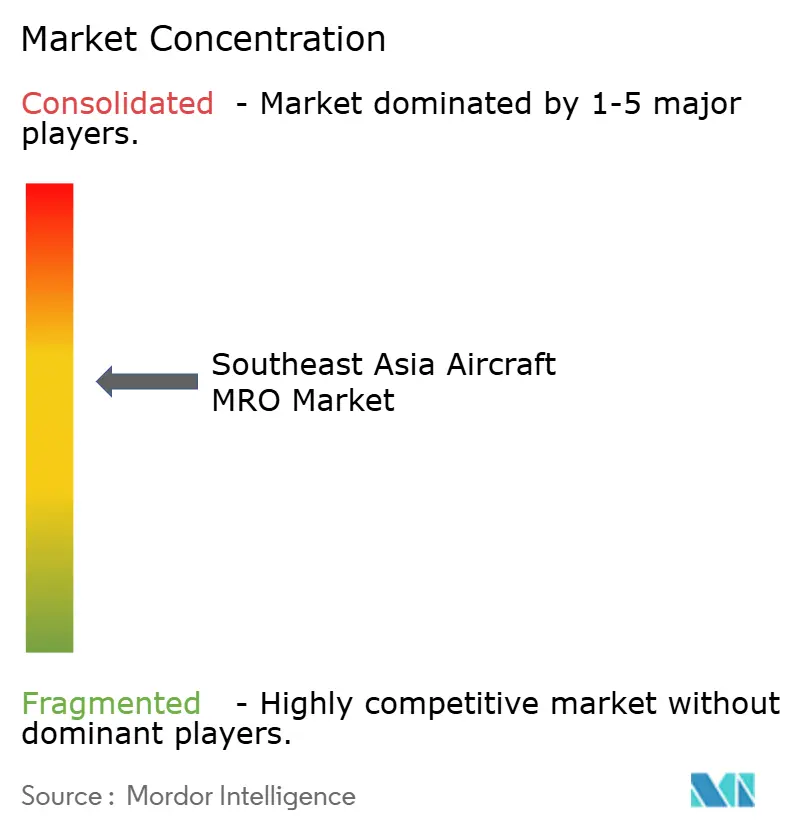

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Southeast Asia Aircraft MRO Market Analysis by Mordor Intelligence

The Southeast Asia aircraft MRO market size is USD 4.84 billion in 2026 and is expected to rise to USD 8.00 billion by 2031, representing a 10.58% CAGR. Fleet up-gauging toward LEAP-powered A320neo and B737 MAX families keeps engines in the spotlight; however, high-pressure turbine (HPT) blade shortages are forcing operators to lease spare engines for up to USD 1.2 million per month, while shop-visit turnaround times exceed 300 days. Airlines are responding by expanding in-house maintenance wings, and governments are competing with single-digit tax regimes to attract fresh hangar, test-cell, and component-repair investments. Predictive analytics is another accelerant, trimming unscheduled removals by almost one-fifth and freeing scarce bay capacity. Finally, freighter conversions are adding an extra 12–18 heavy-check events per airframe, a structural tailwind that supports double-digit growth through the decade.

Key Report Takeaways

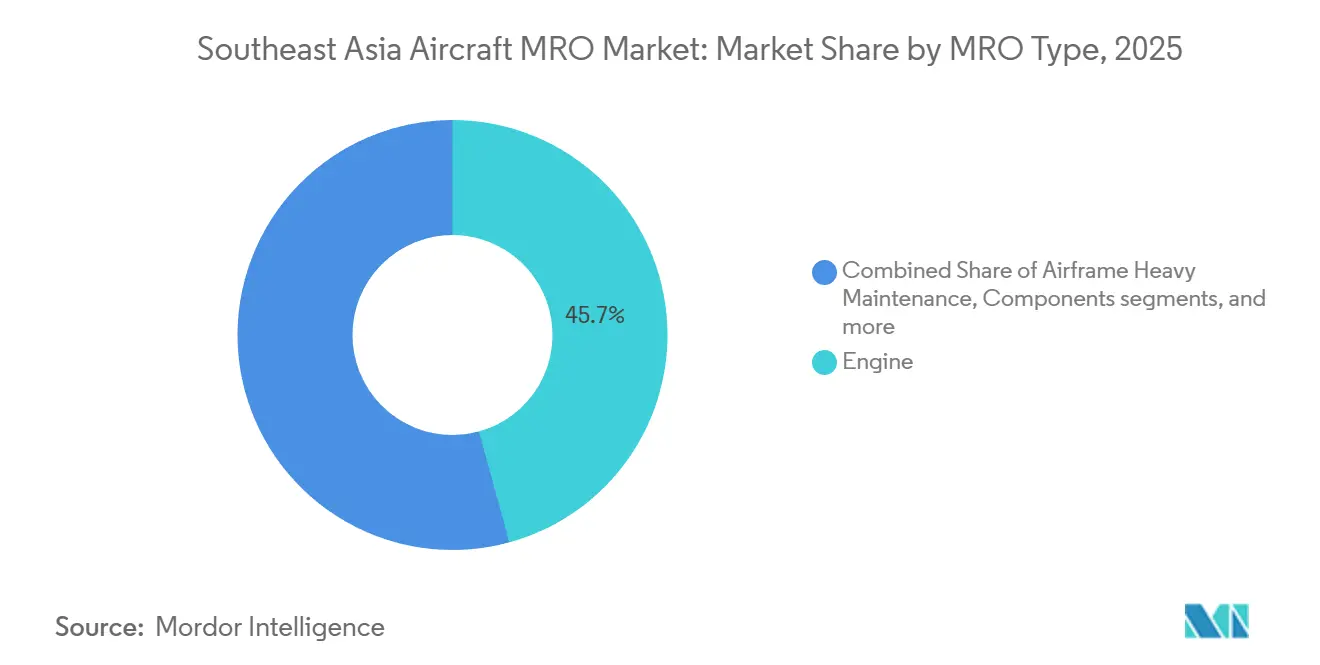

- By MRO type, engine work held 45.74% of the Southeast Asia aircraft MRO market share in 2025, while component repair is expected to advance at a 12.25% CAGR through 2031.

- By aircraft class, fixed-wing platforms accounted for 92.56% of the 2025 spend; rotary-wing work is the fastest-growing segment at an 11.87% CAGR to 2031.

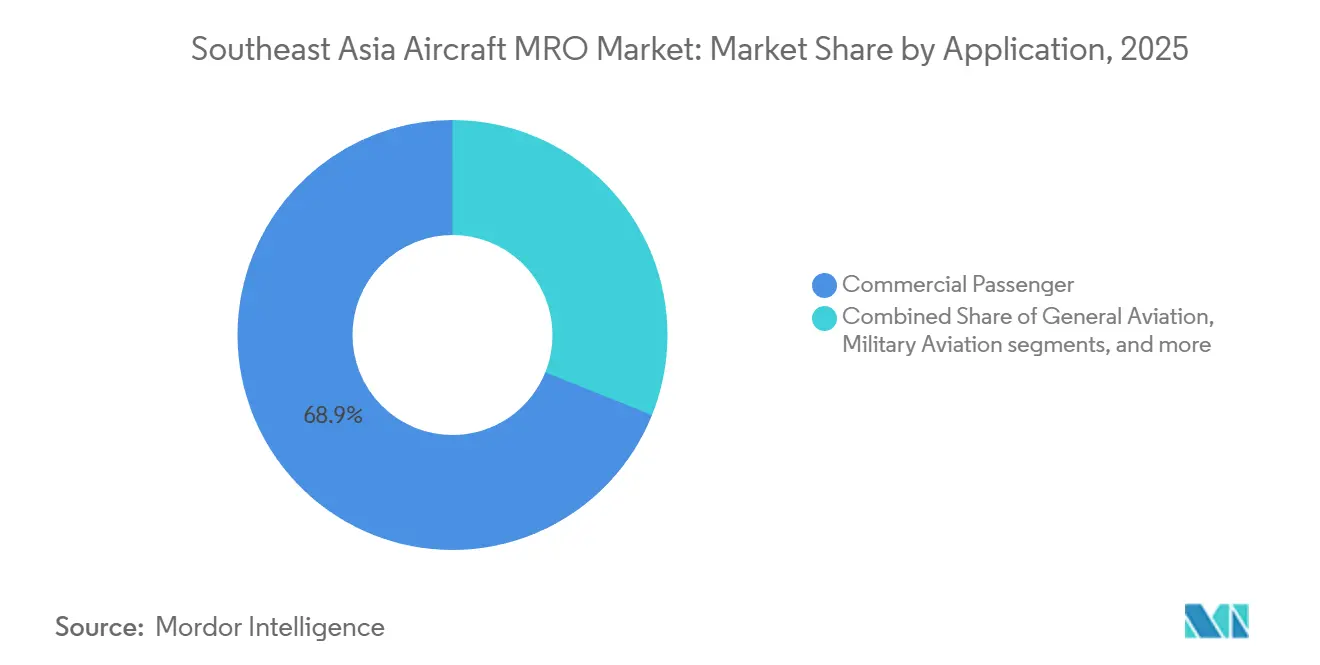

- By application, commercial passenger fleets generated 68.93% of the 2025 revenue; general aviation is growing at a 12.78% CAGR due to expanding business-jet fleets.

- By service provider, airline-affiliated shops controlled 53.67% of the 2025 revenue, while independents are growing at a 11.65% CAGR by focusing on component repairs and freighter conversions.

- By geography, Singapore led with 33.25% of 2025 revenue; Thailand is the fastest mover, with a 12.11% CAGR, driven by the USD 12 billion U-Tapao Aviation City scheme.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Southeast Asia Aircraft MRO Market Trends and Insights

Driver Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Passenger-fleet up-gauging to LEAP-powered narrowbody aircraft | +2.1% | Singapore, Malaysia, Thailand, Indonesia | Medium term (2–4 years) |

| Expansion of airline-affiliated “internal MRO” capacity to reduce third-party spend | +1.8% | Singapore, Indonesia, Thailand | Short term (≤ 2 years) |

| Digital-twin and predictive-maintenance ROI exceeding 15% on turnaround times | +1.5% | Early adoption in Singapore and Malaysia | Medium term (2–4 years) |

| Singapore-Malaysia cross-border tax incentives for engine-test-cell investment | +1.3% | Singapore, Malaysia | Long term (≥ 4 years) |

| OEM “open-ecosystem” programs (CFM, Pratt & Whitney) certifying new SEA independents | +1.2% | Thailand, Vietnam, Philippines | Medium term (2–4 years) |

| Up-cycle in freighter conversions driving heavy-check volumes | +1.4% | Singapore, Indonesia, Thailand | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Passenger-Fleet Up-Gauging to LEAP-Powered Narrow-Bodies

Carriers across the region are accelerating the switch from CFM56 and V2500 engines to LEAP-1A and LEAP-1B units, banking on 15% lower fuel burn and lower carbon intensity. GE Aerospace is spending USD 75 million to double LEAP maintenance throughput in Malaysia and Singapore and to install two new test cells by 2027.[1]GE Aerospace, “GE Aerospace Invests $75 Million to Expand LEAP Engine MRO Capacity,” geaviation.com ST Engineering obtained the first independent LEAP certification in Southeast Asia, positioning Seletar as a neutral hub for more than 500 annual shop visits. While the upgrade improves efficiency, the unique CMC liner, fine-mesh fuel nozzles, and additional borescope ports require specialised tooling and 18–24 months of technician retraining. CFM’s durability enhancement kit, certified in 2024, extends on-wing time by 2,000 cycles but obliges operators to adopt digital twins to monitor blade-cooling margins.

Expansion of Airline-Affiliated Internal MRO Capacity

Currency swings, particularly the IDR currency's 7% decline against the USD in 2025, prompted carriers to reclaim component and line maintenance to mitigate exposure. GMF AeroAsia's USD 1.50 billion plan will include the addition of four hangars at Soekarno-Hatta and a 24/7 component shop in Kertajati by 2030. Thai Airways is collaborating with Airbus to establish a widebody maintenance depot within U-Tapao Aviation City, aiming to capture one-fifth of regional revenue by 2028. SIA Engineering lifted quarterly revenue 12% year-on-year to SGD 325.5 million (USD 252.91 million) in FY2024/25 by shifting A350 and B787 checks in-house. The trend squeezes independents on narrow-body slots, yet frees up space in widebody and freighter conversions where airline shops lack the necessary tooling depth.

Digital-Twin and Predictive-Maintenance ROI

Predictive analytics trims unscheduled removals by roughly one-fifth and shortens shop visits. ST Engineering’s digital-twin platform handles 80,000 components annually and has reduced the turnaround time for landing-gear actuators and APUs by 15%. IATA projects that AI-driven planning could save the global sector USD 5 billion annually by 2030, with Southeast Asia capturing 12% of the savings, thanks to high daily utilization fleets.[2]International Air Transport Association, “MRO Market Outlook 2024-2030,” iata.org Rolls-Royce’s IntelligentEngine collates 12,000 flight-hour data points per Trent engine to predict blade erosion six months ahead, allowing pre-emptive parts ordering that reduces HPT-blade lead times by 25%. Widebody and freighter fleets reap the most significant benefit because each day of downtime can cost USD 150,000.

Singapore-Malaysia Cross-Border Tax Incentives

The Johor–Singapore Special Economic Zone, which opened in January 2025, offers a 5% corporate tax rate and a 15% personal income tax rate on aerospace investments exceeding SGD 100 million (USD 77.70 million). GE Aerospace is leveraging the framework to split labour-intensive LEAP test-cell work between low-cost Johor and high-velocity Singapore logistics. Pratt & Whitney added a GTF line at its Singapore Engine Centre in 2025, supported by SGD 50 million (USD 38.85 million) in grants tied to the zone’s workforce program. Lower landed costs for tooling down 8-10% make the corridor the world’s most cost-efficient LEAP and GTF maintenance location outside North America.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Long-cycle labor shortages for LEAP/GTF borescope-rated technicians | –1.6% | Thailand, Vietnam, Philippines; spill-over across the region | Medium term (2–4 years) |

| Supply-chain bottlenecks in HPT blades extending TAT for more than 300 days | –1.9% | Singapore and Malaysia engine shops | Short term (≤ 2 years) |

| Currency-linked cost pressure on imported spare parts | –0.9% | Indonesia, Thailand, Philippines, Vietnam | Short term (≤ 2 years) |

| Rising sustainability compliance costs for chromium-free strip and paint processes | –0.7% | Singapore, Malaysia, Thailand | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Long-Cycle Labor Shortages for LEAP/GTF Technicians

Borescope-rated technician rolls shrank 12% during the pandemic and have yet to recover. Training a fresh recruit to LEAP or GTF standard takes roughly two years, and certification queues at national regulators add another six to nine months. Pratt & Whitney’s powder-metal recall grounded an average of 350 aircraft during 2025-26, resulting in 1,200 unplanned shop visits and exhausting available talent. The Asian Development Bank warns that the region must add 15,000 technicians by 2030 to keep up with fleet growth. ST Engineering’s 2024 apprenticeship scheme aims to train 500 LEAP-certified staff by 2027, but attrition rates exceed 15% as experienced staff migrate to higher-paying Middle East jobs.

HPT-Blade Supply Bottlenecks

Just three global suppliers produce single-crystal HPT blades for the LEAP engine family, and capacity has not kept pace with 20% annual LEAP delivery growth. Airbus reduced A320neo production in May 2024 as a direct result, and MRO turnaround times increased to 300 days for carriers awaiting replacement modules. Safran released a life-extended blade in 2025; however, the upgraded casting sequence still requires 14 months from raw alloy to finished part.[3]Safran, “Safran Certifies Enhanced HPT Blade for LEAP-1B,” safran-group.com GE Aerospace is adding a reclamation line in Malaysia that will refurbish 30% of used LEAP blades by 2027, easing but not eliminating the crunch.

Segment Analysis

By MRO Type: Component Repairs Outpace Engine Work

Component services accounted for a 12.25% CAGR growth through 2031, outstripping engines, even though engines held 45.74% of the 2025 spend in the Southeast Asia aircraft MRO market. Digital twins trigger part replacements at the first sign of abnormal vibration or thermal stress, cutting AOG events by roughly one-quarter and shifting revenue toward avionics, landing-gear, and APU shops. ST Engineering now processes 80,000 parts across 23,500 part numbers annually and maintains a USD 300 million rotable inventory to uphold its 48-hour turnaround promise.

Predictive maintenance favors smaller work scopes performed more often, a pattern that keeps bays busy but with shorter dwell times. Asia Pacific Aircraft Component Services, a joint venture between SIA Engineering and SR Technics, became a Honeywell channel partner in 2024 and is scaling a 600-part-number facility in Malaysia. GMF AeroAsia entered the APU market in 2025 under a Honeywell agreement, targeting 150 visits per year by 2027. As a result, the Southeast Asia aircraft MRO market size for component work is projected to expand at a faster rate than any other service line through the forecast period.

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Aircraft Class: Rotary Wing Gains Altitude

Fixed-wing aircraft still dominated revenue, accounting for 92.56% in 2025; however, helicopter maintenance is growing at an annual rate of 11.87%, a clear outlier within the Southeast Asia aircraft MRO market. Weststar Aviation’s tie-up with Leonardo will create Malaysia’s first regional center capable of supporting 200 AW139, AW169, and AW189 heavy checks annually by 2028. Bell’s Asia Service Center in Singapore expanded to 15,500 square meters and completed 180 helicopter overhauls in 2025.[4]Bell Textron, “Bell Asia Service Center Expansion,” bellflight.com

Growth drivers include offshore energy demand, medical evacuation services, and a rising need for search-and-rescue (SAR) readiness. Safran Helicopter Engines processed 320 Arriel and Makila shop visits in 2025, up 14% year-on-year. Meanwhile, Sikorsky and its local partner, MyCopter, opened an S-76 support center in Malaysia in 2024, ensuring 72-hour engine-swap availability for offshore operators. The Southeast Asia aircraft MRO market size for rotary-wing assets is therefore expected to become material well before 2030.

By Application: General Aviation Climbs Fastest

Commercial passenger carriers generated 68.93% of 2025 revenue, but business-jet maintenance is the speed leader, with a 12.78% CAGR in the Southeast Asia aircraft MRO market. Jet Aviation Singapore became the only Airbus Corporate Jets service center between Dubai and Sydney in March 2025, aiming to perform 30 ACJ heavy checks annually. StandardAero’s facilities in Singapore and Indonesia handled 140 Honeywell and P&WC engine shop visits in 2025.

On the cargo side, freighter MRO is rising 11.4% annually on e-commerce momentum and Boeing’s forecast for 1,430 regional freighters by 2043. Military MRO represents 8% of 2025 spend and is growing at 10.9% CAGR as Singapore upgrades its F-16 fleet under a USD 1.09 billion package with Lockheed Martin. These mixed applications help cushion the Southeast Asia aircraft MRO market against airline-specific cycles.

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Service Provider: Independents Narrow the Gap

Airline-owned shops accounted for 53.67% of 2025 revenue, while independents are advancing at a 11.65% CAGR, significantly outpacing the overall Southeast Asia aircraft MRO market. GMF AeroAsia serves external operators such as Thai Vietjet and Cebu Pacific, while Thai Airways is building a joint venture with Airbus to secure wide-body work. Independents gain ground by offering flexible pricing and faster turnarounds. ST Engineering’s component network averages 15% shorter turn times, thanks to its deep parts pools.

AAR Corp’s 2024 deal with Thai Airways brings component distribution and landing-gear overhaul to Suvarnabhumi Airport, aiming for 250 shop visits a year by 2027. OEM-captive facilities, Safran’s LEAP and Rolls-Royce’s Trent centers, account for 18% of spend and are scaling to protect engine aftermarket margins. Military depots make up the balance, concentrated in Singapore and Indonesia.

Geography Analysis

Singapore remains the anchor of the Southeast Asia aircraft MRO market, with 33.25% of 2025 revenue. The island’s 190 MRO companies employ 19,500 people and benefit from a well-oiled logistics chain at Changi Airport.[5]Department of Statistics Singapore, “Singapore Aerospace Industry Statistics,” singstat.gov.sg ST Engineering’s SGD 1 billion (USD 0.78 billion) Seletar expansion added three hangars and the region’s first independent LEAP lines in 2024. Rolls-Royce expanded its Trent shop to handle 80 Trent 7000 and XWB visits per year, while Pratt & Whitney added a dedicated GTF line backed by SGD 50 million (approximately USD 38.85 million) in grants.

Thailand is the fastest riser, expanding at a 12.11% CAGR through 2031. The USD 12 billion U-Tapao Aviation City scheme offers an eight-year corporate tax holiday, plus duty-free spare part imports, attracting an Airbus-Thai Airways joint venture targeting one-fifth of the regional heavy-check volume by 2028. AAR Corp invested USD 18 million in a 12,000 m² component center at Suvarnabhumi, and Safran is scouting Rayong for a LEAP blade-repair plant.

Indonesia holds 22% of 2025 revenue thanks to GMF AeroAsia’s massive facilities near Jakarta and the nascent Kertajati Aerospace Park in West Java. Malaysia, the Philippines, and Vietnam together account for 18% of the spend. Weststar-Leonardo’s Melaka helicopter hub and GE Aerospace’s Johor test cells underscore Malaysia’s tilt toward rotary-wing and engine specialization. Lufthansa Technik’s Philippine arm added avionics and landing-gear work in 2024, while Vietnam is courting OEM licenses under an industrial park model.

Competitive Landscape

The Southeast Asia aircraft MRO market exhibits moderate concentration: the top five players, ST Engineering, SIA Engineering, GMF AeroAsia, Safran, and Rolls-Royce, command 58% of 2025 revenue. Airline-affiliated shops dominate narrow-body line checks, yet independents and OEMs are neck-and-neck in high-value engine and component niches. GE Aerospace’s USD 75 million outlay will double LEAP capacity across Malaysia and Singapore. At the same time, Pratt & Whitney’s GTF upgrade in Seletar preserves OEM control over an engine that already powers 170 aircraft in the region.

Technology is the chief differentiator. ST Engineering’s digital-twin system slashed average component turnaround by 15% and carved an early lead in predictive analytics. Rolls-Royce’s IntelligentEngine, which has been operational since 2024, predicts blade wear six months in advance, providing Trent operators with a scheduling advantage. Smaller challengers, such as Asia Digital Engineering and Subang MRO, and a growing cluster in Vietnam, target the turboprop, business-jet, and helicopter niches to avoid head-to-head battles with Singapore’s giants.

Regulatory hurdles are material. Dual FAA and EASA Part-145 approvals take up to two years, slowing market entry for Vietnam and Philippine shops. Conversely, Singapore and Malaysia attract investors with a five-percent corporate tax rate and accelerated permits within their special economic zones, reinforcing their hub status.

Southeast Asia Aircraft MRO Industry Leaders

Safran SA

SIA Engineering Company

Singapore Technologies Engineering Ltd.

Rolls-Royce Holdings plc

PT GMF AeroAsia Tbk (Garuda Indonesia)

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- September 2025: Honeywell International Inc. announced the expansion of its established collaboration with PT Garuda Maintenance Facility Aero Asia Tbk (GMF), Indonesia's leading provider of aircraft MRO services. The expanded partnership includes a three-year APU 131-9A/B and 331-350 part supply program, as well as a three-year flat-rate repair program for 331-350 APU line-replaceable units (LRUs), offered exclusively.

- May 2025: Weststar Aviation Services Sdn. Bhd. announced two significant developments for Malaysia's aviation industry. These include the launch of the country's largest government helicopter expansion and modernization program in collaboration with Leonardo, and the signing of an MoU with the Melaka State Government to establish an Aviation Centre of Excellence at Melaka International Airport.

- March 2025: Jet Aviation announced that its Singapore facility had been accredited to perform authorized maintenance, refurbishment, and warranty work as part of the Airbus Corporate Jets Service Center Network. This makes Singapore the third Jet Aviation maintenance site to join the network and the only member located in the Asia-Pacific region.

Southeast Asia Aircraft MRO Market Report Scope

Aircraft MRO refers to the overhaul, inspection, repair, or modification of an aircraft or any parts and components. The study includes the revenues sourced from the MRO activities of military, commercial, and general aviation aircraft fleets opting to undergo MRO operations in Southeast Asia.

The Southeast Asia aircraft MRO market is segmented based on MRO type, aircraft class, application, service provider, and geography. By MRO type, the market is segmented into airframe heavy maintenance, engine maintenance, component maintenance, line and routine checks, and modifications and upgrades. By aircraft class, the market is divided into fixed-wing and rotary-wing aircraft. By application, the market is segmented into commercial passenger, commercial cargo/freighter, military aviation, and general aviation. By service provider, the market is classified into airline-affiliated MRO, independent third-party MRO, OEM-captive MRO, and military depots. The report also offers the market size and forecasts for six countries across the region. For each segment, the market size is provided in terms of value (USD).

By MRO Type

| Airframe Heavy Maintenance |

| Engine Maintenance |

| Component Maintenance |

| Line and Routine Checks |

| Modifications and Upgrades |

By Aircraft Class

| Fixed-wing |

| Rotary-wing |

By Application

| Commercial Passenger |

| Commercial Cargo/Freighter |

| Military Aviation |

| General Aviation |

By Service Provider

| Airline-affiliated MRO |

| Independent Third-party MRO |

| OEM-Captive MRO |

| Military Depots |

By Geography

| Malaysia |

| Indonesia |

| Singapore |

| Thailand |

| Philippines |

| Vietnam |

| By MRO Type | Airframe Heavy Maintenance |

| Engine Maintenance | |

| Component Maintenance | |

| Line and Routine Checks | |

| Modifications and Upgrades | |

| By Aircraft Class | Fixed-wing |

| Rotary-wing | |

| By Application | Commercial Passenger |

| Commercial Cargo/Freighter | |

| Military Aviation | |

| General Aviation | |

| By Service Provider | Airline-affiliated MRO |

| Independent Third-party MRO | |

| OEM-Captive MRO | |

| Military Depots | |

| By Geography | Malaysia |

| Indonesia | |

| Singapore | |

| Thailand | |

| Philippines | |

| Vietnam |

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

How large will maintenance spending in Southeast Asia reach by 2031?

The Southeast Asia aircraft MRO market is projected to attain USD 8.00 billion by 2031, expanding at a 10.58% CAGR.

Which service line is growing fastest in regional maintenance budgets?

Component repair leads, advancing at 12.25% CAGR on the back of digital-twin diagnostics and expanded Honeywell and Honeywell-licensed shops.

Why are freighter conversions important to local MRO providers?

Each passenger-to-freighter conversion adds 12-18 heavy-check events, generating up to USD 5.50 million in incremental MRO revenue per aircraft and sustaining bay utilization.

Which country offers the most attractive fiscal terms for new engine facilities?

The Johor–Singapore Special Economic Zone (SEZ) sets a 5% corporate-tax rate and 15% personal-income tax for qualifying aerospace investments, attracting GE Aerospace and Pratt & Whitney.

How serious is the technician shortage for next-generation engines?

The region must add roughly 15,000 certified technicians by 2030 because LEAP and GTF shop-visit demand outstrips current manpower, extending turnaround times (TAT) beyond 300 days.