South Korea Turning Machine and Equipment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

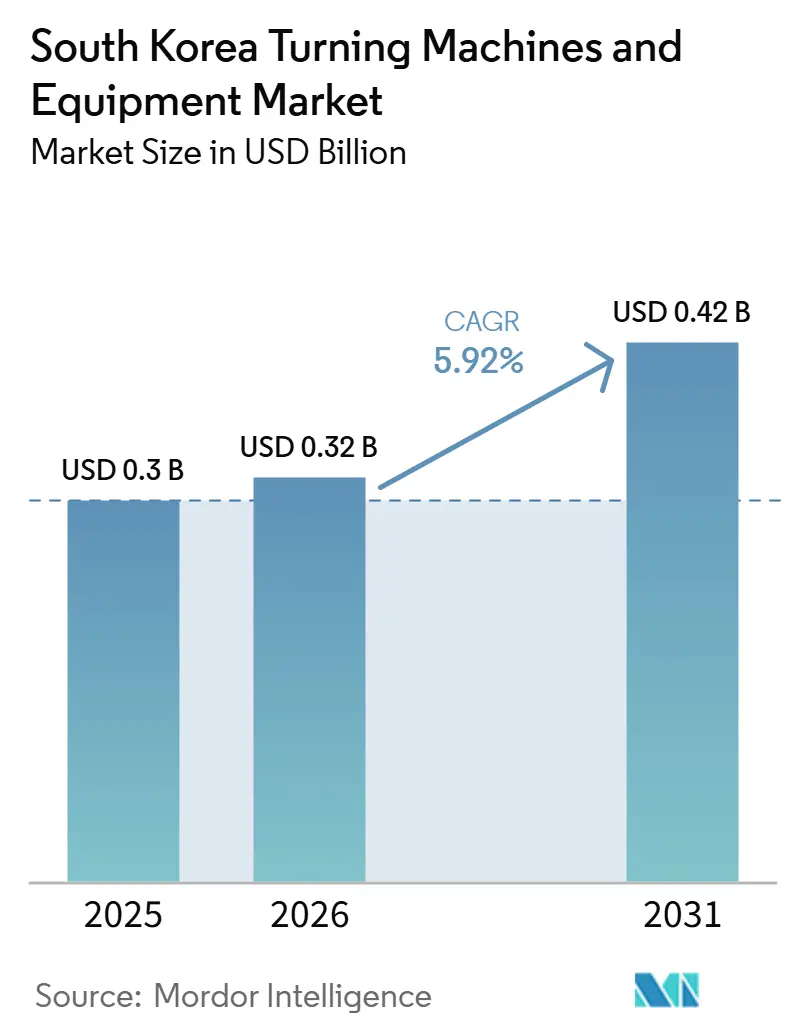

| Base Year Market Size (2025) | USD 0.3 Billion |

| Historical Data Period | 2020 - 2024 |

| Market Size (2026) | USD 0.32 Billion |

| Market Size (2031) | USD 0.42 Billion |

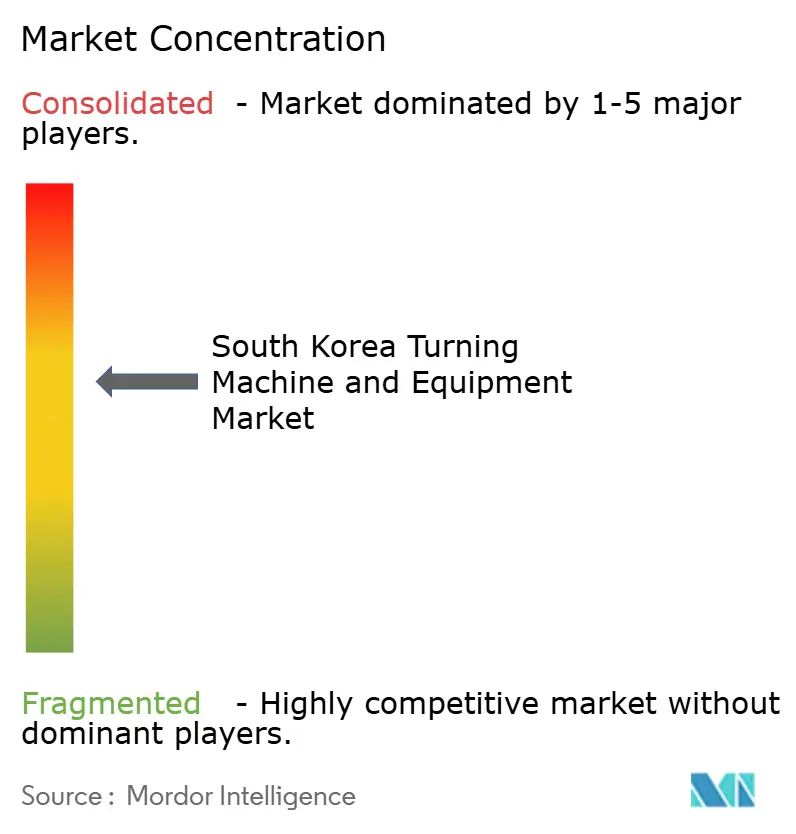

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South Korea Turning Machine and Equipment Market Analysis by Mordor Intelligence

The South Korea Turning Machine and Equipment Market size is expected to grow from USD 0.3 billion in 2025 to USD 0.32 billion in 2026 and is forecast to reach USD 0.42 billion by 2031 at 5.92% CAGR over 2026-2031.

South Korea remains one of the world’s largest manufacturing economies, and its broad industrial base keeps it at the forefront of the equipment market, tied to steady demand for precision metal-cutting systems across export-oriented production lines. General machinery exports reached USD 51.2 billion in 2024, underscoring the importance of machining equipment to the country’s industrial supply chain. The South Korea turning machine and equipment market has a durable base in automotive, electronics, and capital goods production. Demand is also moving toward higher precision because semiconductor, electric vehicle, defense, and aerospace manufacturers need tighter tolerances and more stable machining performance than older production programs required. The South Korea turning machine and equipment market also benefits from smart factory funding, which is pushing buyers toward connected CNC platforms that can support real-time data flow, predictive maintenance, and closer process control. At the same time, high equipment cost, labor shortages, and slower replacement cycles keep the South Korea turning machine and equipment market from expanding faster, even as demand from semiconductors, mobility, and defense creates a stable floor for growth.

Key Report Takeaways

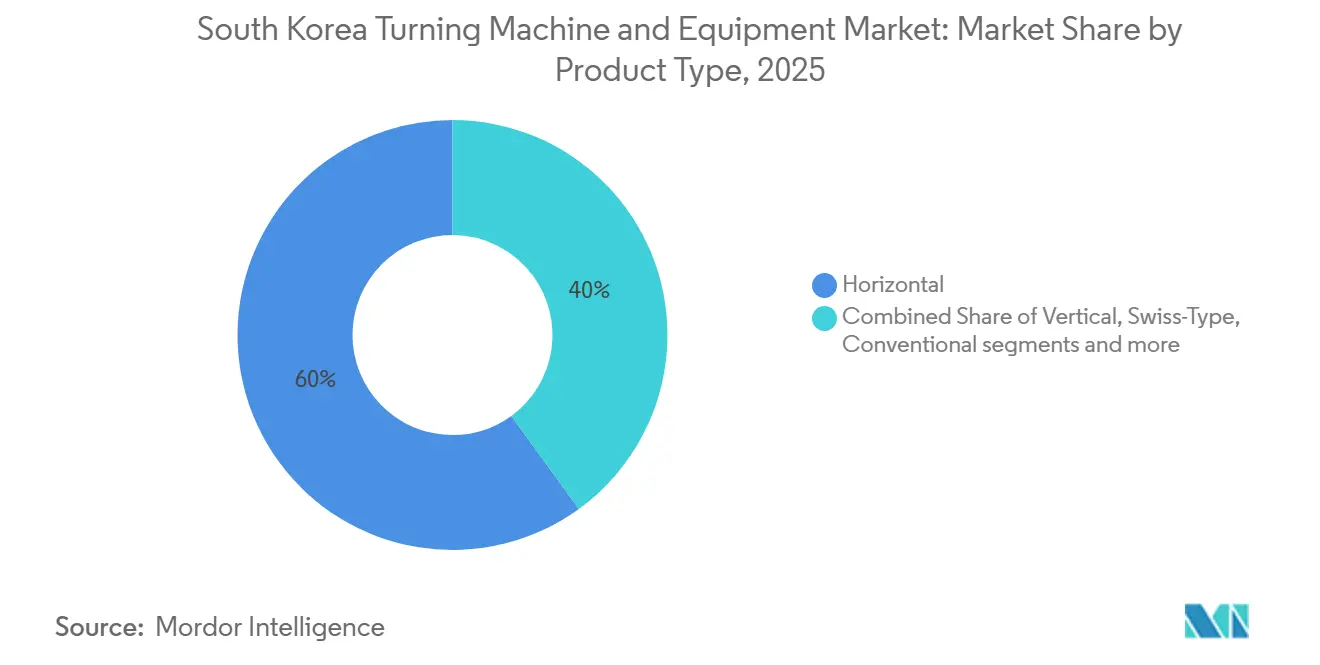

- By product type, the horizontal segment accounted for 60% of the South Korea turning machine and equipment market share in 2025, while the multi-tasking turning machine and equipment segment is projected to expand at a 7.2% CAGR through 2031.

- By automation type, fully automatic CNC segment accounted for 86% of the South Korea turning machine and equipment market size in 2025 and recorded the highest projected CAGR of 7% through 2031.

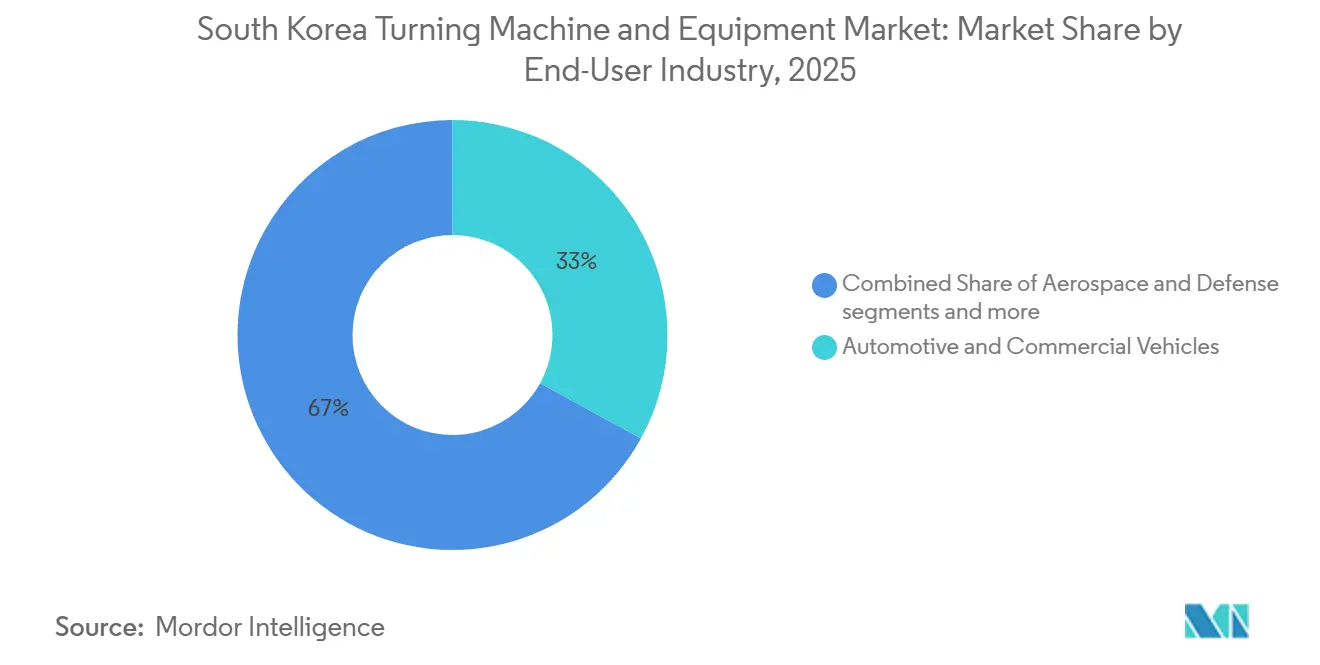

- By end-user industry, automotive and commercial vehicles accounted for 33% share in 2025, while aerospace and defense are forecast to advance at a 7.4% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

South Korea Turning Machine and Equipment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion of Semiconductor Equipment Manufacturing Driving Precision Machining Requirements | +1.8% | Gyeonggi, including Pyeongtaek, Yongin, and Hwaseong, and Chungnam, including Cheongju | Long term (≥ 4 years) |

| Rising Factory Automation Investments | +1.3% | National, with early gains in Changwon, Ulsan, and Daegu industrial complexes | Medium term (2-4 years) |

| Manufacturing Modernization by Industrial Conglomerates | +1.0% | National, concentrated in the Seoul Metropolitan Area and Gyeonggi Province | Medium term (2-4 years) |

| Growth in EV and Advanced Mobility Production | +0.8% | Ulsan, Asan, and Gwangmyeong | Medium term (2-4 years) |

| Export-Driven Manufacturing Competitiveness | +0.5% | National, with export clusters in Changwon and Busan | Long term (≥ 4 years) |

| Localization of Precision Component Production | +0.4% | Gumi, Busan, Changwon, Daejeon, and Gwangju | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Expansion of Semiconductor Equipment Manufacturing Driving Precision Machining Requirements

South Korea’s plan to build KRW 700 trillion (USD 485.8 billion) of semiconductor fabrication capacity through 2047 is reshaping the supply chain that supports precision-machining demand. The government’s December 2025 semiconductor roadmap places materials, components, and equipment at the center of this effort, and private commitments in these areas reached a record KRW 850.1 billion (USD 589.9 million) in 2025. New fabrication plants require a wide range of precision turned parts for wafer handling systems, deposition tools, and utility equipment, driving demand for high-precision horizontal and swiss-type turning machine and equipment in the South Korea turning machine and equipment market. The Semiconductor Special Act, passed in January 2026, prioritizes power, water, and transport links for designated clusters in Pyeongtaek and Yongin, removing a major delay point in plant installation schedules. That shift matters because faster cluster development pulls equipment orders forward and supports a more visible procurement cycle for machine builders serving the South Korea turning machine and equipment market. The plan to foster 150 domestic and foreign materials, components, and equipment firms within the semiconductor belt also supports longer demand visibility beyond a single memory cycle.

Rising Factory Automation Investments

Government-backed automation spending is the clearest near-term driver of CNC upgrades across small- and mid-sized manufacturers in the South Korea turning machine and equipment market.[1]Organisation for Economic Co-operation and Development, “Korea’s Smart Manufacturing Innovation Initiative,” OECD, oecd.org MOTIE allocated KRW 478.7 billion (USD 332.2 million) to 445 industrial AI projects in 2025, with AI factory development and autonomous manufacturing among the main budget uses. The M.AX Alliance launched in 2025, and the government provided KRW 53 billion (USD 36.8 million) in 2026 for AI factory infrastructure projects, which has kept automation demand active. OECD records show that the 2025 budget for the smart manufacturing initiative totaled KRW 247.9 billion (USD 172.0 million), of which 95% was allocated to smart factory adoption. The Ministry of SMEs and Startups also launched a 2026 program that covers 450 projects, including 30 autonomous factory projects and 400 AI-specialized smart factory deployments. These programs shift buyer preference in South Korea turning machine and equipment market toward fully automatic CNC turning centers that can connect to factory software and provide real-time maintenance and process data.[2]Ministry of SMEs and Startups, “Smart Manufacturing Innovation Support Program 2026,” Ministry of SMEs and Startups, mss.go.kr

Manufacturing Modernization by Industrial Conglomerates

Large domestic industrial groups continue to set the pace for technology upgrades in the South Korea turning machine and equipment market. In November 2025, Samsung Electronics, Hyundai Motor Group, LG Group, and other major firms pledged to invest close to KRW 700 trillion (USD 485.8 billion) in domestic projects over 5 years. Samsung committed KRW 450 trillion, (USD 312.3 billion), for domestic investment and linked that plan to a fifth semiconductor plant at Pyeongtaek and a new AI Mega factory developed with NVIDIA. LG Group pledged KRW 100 trillion (USD 69.4 billion) and directed 60% of that spending to materials, components, and equipment areas with a direct link to machine tool demand. SK Group also partnered with NVIDIA to build a manufacturing AI cloud and AI factory with more than 50,000 GPUs, demonstrating how digital infrastructure and production equipment decisions are converging. Because these companies act as buyers, their specifications often shape what suppliers across the South Korea turning machine and equipment market are expected to install and support.

Growth in EV And Advanced Mobility Production

Electric vehicle growth is adding a new layer of demand to the South Korea turning machine and equipment market, and the technical requirements differ from older combustion-focused machining programs. New EV registrations rose 50.1% in 2025 to 220,177 units, which ended a 2-year decline and improved the production outlook for vehicle parts suppliers. Total automobile production reached 4.1 million units in 2025, and automobile exports hit a record USD 72 billion, keeping the broader manufacturing base active. The government committed KRW 1.5 trillion (USD 1.04 billion) to EV purchase incentives in 2025, which supports the production pipeline that machine shops are working against. EV motor housings, battery casing parts, and powertrain assemblies need tighter thermal control and more stable turning performance than many legacy automotive lathes can deliver. The K-Mobility strategy also targets a 90% eco-friendly vehicle share of new car sales by 2035. It includes plans to train 70,000 future mobility specialists and support 200 specialized companies, giving the South Korea turning machine and equipment market a longer runway in this end use.[3]Ministry of Trade, Industry and Energy, “Strategy For Nurturing High-Tech Industries By Sector,” Invest Korea, investkorea.org

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Cost of Advanced Turning Machine and Equipment | -1.2% | National, with the sharpest effect on SMEs outside major industrial clusters | Long term (≥ 4 years) |

| Shortage of Skilled Workforce | -0.6% | National, with the strongest pressure in the Changwon and Daegu industrial clusters | Medium term (2-4 years) |

| Competition from Chinese Machine Tool Suppliers | -0.9% | National, with the highest concentration in standard CNC categories | Medium term (2-4 years) |

| Long Machine Replacement Cycles | -0.4% | National | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Cost of Advanced Turning Machine and Equipment

High capital costs remain a structural limit on replacement demand in the South Korea turning machine and equipment market, especially among small- and mid-sized manufacturers. Advanced 5-axis CNC turning centers and multi-tasking machines can cost hundreds of millions of KRW per unit, and installation lead times can stretch from 6 to 12 months, which creates a financing and scheduling burden for smaller firms. MOTIE’s 2025 investment-linked technology program attracted only 183 companies from the machinery and automation sector, suggesting that capital constraints remain a significant barrier to adoption. The Smart Manufacturing Innovation 3.0 framework helps offset some of this pressure by subsidizing 50% to 80% of participating SMEs' smart factory construction costs. Even so, the 2026 cycle covers only 450 projects, which is small compared to a manufacturing SME base of over 10,000 companies. That gap keeps upgrade rates uneven across the South Korea turning machine and equipment market and leaves many buyers on longer replacement schedules than demand conditions alone would suggest.

Shortage of Skilled Workforce

Labor availability is another limitation on the South Korea turning machine and equipment market, as advanced systems still depend on operators, programmers, and technicians who can use them effectively. MOTIE’s 2025 survey recorded a shortage of 39,834 skilled industrial technology workers, and the machinery sector alone needed 4,292 additional professionals. Root manufacturing industries, including precision machining, also reported rising unfilled positions, with vacancies increasing from 22,595 in 2023 to 22,662 in 2024. In March 2026, the government announced an immigration overhaul with new high-skilled visa channels and easier employment permits for manufacturing roles, indicating that the current labor gap is serious enough to warrant national policy action. The Board of Audit and Inspection also warned in 2025 that the semiconductor sector could face an 81,000-worker shortfall by 2031, and that pressure could spread into adjacent precision-machining functions. As a result, the South Korea turning machine and equipment market faces not only a question of equipment demand, but also a question of how quickly buyers can build the workforce needed to absorb more advanced machine platforms.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Horizontal Dominance Persists as Multi-Tasking Emerges

Horizontal turning machine and equipment held 60% of South Korea turning machine and equipment market share in 2025, keeping it well ahead of every other product category. That lead reflects the format’s broad use across automotive parts, semiconductor equipment sub-assemblies, and general industrial machining. Many SMEs in Changwon and Daegu have built long-standing production cells around horizontal CNC lathes, so replacement demand still tends to favor the same platform. This installed base gives the South Korea turning machine and equipment market a stable core of repeat demand even when buyers slow major process changes. It also means product decisions are often shaped by operator familiarity, service support, and fixture compatibility rather than by machine design alone.

Multi-tasking turning machine and equipment is forecast to record the fastest growth at a 7.2% CAGR from 2026 to 2031, which reflects rising demand for process consolidation in aerospace, semiconductor equipment, and medical device production. Buyers in these fields want to reduce setups per part because fewer transfers lower positional error and shorten total cycle time. Swiss-type turning machine and equipment serves a different market segment for medical devices, electronic connectors, and optical parts, where small-diameter precision remains critical. Vertical turning machine and equipment stays relevant in energy equipment and heavy machinery applications that involve larger workpieces. Conventional turning machine and equipment continues to lose ground as smart factory support programs move more buyers in the South Korea turning machine and equipment market toward CNC-based replacements.

By Automation Type: CNC Penetration Deepens Across Industrial Tiers

Fully automatic CNC turning machine and equipment accounted for 86% share of the South Korea turning machine and equipment market size in 2025, and the same category is projected to grow at a 7% CAGR through 2031. That combination shows that the South Korea turning machine and equipment market is already centered on CNC systems and is still moving deeper into automation. The transition began with large industrial groups, but government subsidy programs have pushed it into the SME base as well. The 2026 smart manufacturing program supports 400 AI-specialized factory deployments, and those projects depend on machine tools that can connect with wider production systems. That funding structure keeps CNC adoption central to near-term purchasing patterns across the South Korea turning machine and equipment market.

The semi-automatic turning machine and equipment still serves SMEs that need moderate output and tighter capital control. Still, its role keeps narrowing as subsidies cover part of the upgrade cost to full CNC. Manual lathes remain in training environments and small-batch shops, but they now sit on the edge of commercial demand rather than at its center. MOTIE’s autonomous factory support program provides up to KRW 1.2 billion per company over 2 years, which gives smaller firms a direct path to more capable CNC systems. Open communication protocols, predictive maintenance output, and digital twin compatibility are becoming standard buying requirements rather than optional features. This transition raises the average value mix within the South Korea turning machine and equipment market, even when total unit growth remains measured.

By End-User Industry: Automotive Anchors Demand While Aerospace and Defense Accelerate

Automotive and commercial vehicles accounted for 33% share of the South Korea turning machine and equipment market size in 2025, making this the largest end-user group. South Korea produced 4.1 million vehicles in 2025 and recorded automobile exports of USD 72 billion, which kept demand active for drivetrain, chassis, and body component machining. This scale matters because automotive still provides the broadest base of machine usage among domestic suppliers. Even as product requirements shift, the vehicle sector continues to anchor utilization across much of the South Korea turning machine and equipment market. That base also helps sustain demand for both standard and advanced CNC systems.

Aerospace and defense is the fastest-growing end-user segment, with a projected 7.4% CAGR from 2026 to 2031. Defense exports reached USD 15.4 billion in 2025, and the 4 major defense firms posted combined revenue of KRW 40.5 trillion (USD 29.3 billion), supporting durable demand for high-precision turned components. In June 2026, KASA launched a KRW 42.9 billion (USD 31 million) 5-year program to develop aircraft engine structural materials and precision parts, strengthening the domestic aerospace supply base. Electrical, electronic, and semiconductor equipment also represents a major demand stream, but this demand often falls outside traditional automotive purchasing channels and requires greater precision. Medical devices, general industrial machinery, and oil, gas, and energy round out the South Korea turning machine and equipment market with stable but slower demand for standard CNC and swiss-type platforms.

Geography Analysis

The South Korea turning machine and equipment market is concentrated in a few industrial corridors, and this concentration shapes both demand volume and equipment specifications. The Gyeonggi and Chungnam semiconductor belt, which includes Pyeongtaek, Yongin, Hwaseong, and Cheongju, is the fastest-growing region for precision CNC demand because it is closely tied to the national semiconductor cluster plan. Samsung’s fifth Pyeongtaek fab and SK Hynix capacity expansion keep this corridor at the center of new equipment planning. The Semiconductor Special Act, passed in January 2026, gives legal priority to infrastructure installation in these clusters, shortening delays that had often slowed plant buildout and machine ordering. This makes the corridor important not only because of scale, but also because demand there is led by specification, cleanliness, and process stability.

The southern corridor, centered on Changwon, Ulsan, and Busan, remains the historical production base for machine tools and automotive manufacturing in the South Korea turning machine and equipment market. Changwon hosts major domestic machine tool builders and their component suppliers, which makes it important on both the supply and demand sides. Ulsan remains central to Hyundai Motor Group production and supports a wide machining ecosystem tied to vehicle output. Busan adds logistics strength and depth in precision manufacturing, and DN Solutions’ January 2026 Heller deal also supports its broader global manufacturing position from South Korea. MOTIE’s Southern Semiconductor Innovation Belt, linking Gwangju, Busan, and Gumi, extends precision machining demand in this corridor beyond its older automotive base.

The Daegu and Gyeongbuk region forms a secondary cluster in the South Korea turning machine and equipment market, with strong roots in textile machinery, molds, dies, and general metalworking. This installed base still leans more toward older semi-automatic and manual configurations than the leading semiconductor corridor. Government support for AI transformation of industrial complexes is important here because it can turn a replacement opportunity into active CNC demand. The result is a geographic pattern in which the north-central belt drives high-specification demand, the southern corridor sustains large industrial volumes, and the inland cluster provides a gradual upgrade path for future CNC adoption.

Competitive Landscape

The South Korea turning machine and equipment market has a moderately concentrated domestic tier led by DN Solutions, Hwacheon Machinery, SMEC, and Hanwha Precision Machinery, while German, Japanese, and Swiss brands remain well established in higher-performance categories. Domestic suppliers benefit from faster service response, easier local customization, and stronger alignment with Korean smart factory requirements. These advantages matter in a market where downtime costs are high, and buyers often want local engineering support during installation and ramp-up. International suppliers still compete strongly where buyers place the highest value on technology depth, specialized machining capability, and long-proven premium performance. The result is a South Korea turning machine and equipment market where domestic and foreign players are both firmly present, but they often compete on different strengths.

DN Solutions’ January 2026 agreement to acquire Germany’s Heller for EUR 150 million (USD 176 million) is the clearest strategic move in the current competitive cycle. The combined entity reports more than USD 2.4 billion in consolidated sales and annual production of more than 13,400 machines, extending Korean reach into a broader global manufacturing network. Samsung’s AI Megafactory partnership with NVIDIA is another important move because it raises the bar for suppliers on digital integration, data compatibility, and automated process control. SK Group’s AI factory partnership with NVIDIA reinforces this direction and shows that IT systems and machine tool specifications are becoming increasingly closely linked in advanced production environments. These moves support the premium end of the South Korea turning machine and equipment market, where capability and integration matter more than initial purchase price.

Competition is sharper in standard CNC segments, where Chinese suppliers continue to apply price pressure and narrow margins for more basic horizontal platforms. That pressure is strongest where buyers view machines as close substitutes and where service or software differences are smaller. White space remains strongest in AI-ready turning systems and in turnkey machining solutions for semiconductor equipment suppliers that still source multiple sub-processes from different vendors. Hanwha Precision Machinery remains well-positioned in Swiss-type CNC automatic lathes, and its local standing supports growth in medical device and fine electronics applications. Overall, the South Korea turning machine and equipment market rewards firms that can combine local service reach, digital readiness, and application-specific precision rather than competing solely on price.

South Korea Turning Machine and Equipment Industry Leaders

DN Solutions

Takisawa Machine Tool Co., Ltd.

Hwacheon Machinery

SMEC Co., Ltd.

Hanwha Precision Machinery

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: The Korea Aerospace Administration (KASA) launched a KRW 42.9 billion (USD 31 million) five-year R&D program to develop five aircraft gas turbine engine materials and four core components, expanding South Korea’s aerospace precision machining supply chain and demand for aerospace-grade CNC turning machine and equipment.

- January 2026: DN Solutions agrees to acquire Germany's Heller Holding SE & Co. for EUR 150 million (USD 176 million), creating a combined entity with consolidated sales of approximately USD 2.4 billion and annual production exceeding 13,400 machines. The acquisition broadens DN Solutions' horizontal machining center portfolio and extends its European production network across five Heller plants in Germany, the United Kingdom, the United States, Brazil, and China.

- October 2025: Samsung Electronics announced a KRW 450 trillion (USD 326 billion) five-year domestic investment program, including the construction of a fifth semiconductor fab at Pyeongtaek campus, and a partnership with NVIDIA to deploy over 50,000 GPUs in a new AI Megafactory, embedding AI throughout Samsung's semiconductor, mobile, and robotics manufacturing flows.

South Korea Turning Machine and Equipment Market Report Scope

The South Korea Turning Machine and Equipment Market Report is Segmented by Product Type (Horizontal, Vertical, Swiss-Type, Multi-Tasking, and Conventional), by Automation Type (Manual, Semi-Automatic, and Fully Automatic CNC), and by End-User Industry (Automotive and Commercial Vehicles, Aerospace & Defense, and More). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Units).

| Horizontal |

| Vertical |

| Swiss-Type |

| Multi-Tasking |

| Conventional |

| Manual |

| Semi-Automatic |

| Fully Automatic CNC |

| Automotive & Commercial Vehicles |

| Aerospace & Defense |

| Medical Devices & Surgical Instruments |

| Oil, Gas, & Energy |

| Electrical, Electronics & Semiconductor Equipment |

| General Industrial Machinery |

| Others (Consumer Goods, Defense Ordnance) |

| By Product Type | Horizontal |

| Vertical | |

| Swiss-Type | |

| Multi-Tasking | |

| Conventional | |

| By Automation Type | Manual |

| Semi-Automatic | |

| Fully Automatic CNC | |

| By End-User Industry | Automotive & Commercial Vehicles |

| Aerospace & Defense | |

| Medical Devices & Surgical Instruments | |

| Oil, Gas, & Energy | |

| Electrical, Electronics & Semiconductor Equipment | |

| General Industrial Machinery | |

| Others (Consumer Goods, Defense Ordnance) |

Key Questions Answered in the Report

What is the market size of the South Korea turning machine and equipment market in 2026, and how is it expected to grow by 2031?

The South Korea turning machine and equipment market size stood at USD 0.30 billion in 2025, reached USD 0.32 billion in 2026, and is projected to hit USD 0.42 billion by 2031 at a 5.92% CAGR.

Which product category leads demand in South Korea?

The horizontal segment led the market in 2025 with a 60% share, as it remains widely used across automotive, semiconductor, and general industrial applications.

Which automation format is expanding the fastest in South Korea?

Fully automatic CNC segment already held 86% share in 2025 and is also the fastest-growing automation segment with a 7% CAGR through 2031.

Why is semiconductor investment important for machine tool demand in South Korea?

Semiconductor cluster expansion is driving demand for precision turned parts used in wafer handling, deposition, and utility systems, which supports high-precision CNC procurement.

Which end-user sector is growing the fastest for turning machine and equipment in South Korea?

Aerospace and defense is the fastest-growing end-user segment, with a projected 7.4% CAGR through 2031, supported by defense exports and new aircraft engine component programs.

What are the main limits on market growth in South Korea?

High equipment cost, a shortage of skilled workers, competition in standard CNC categories, and long replacement cycles continue to hold back faster adoption across smaller manufacturers.

Page last updated on: