South Korea Robotics CNC Turning Centers Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

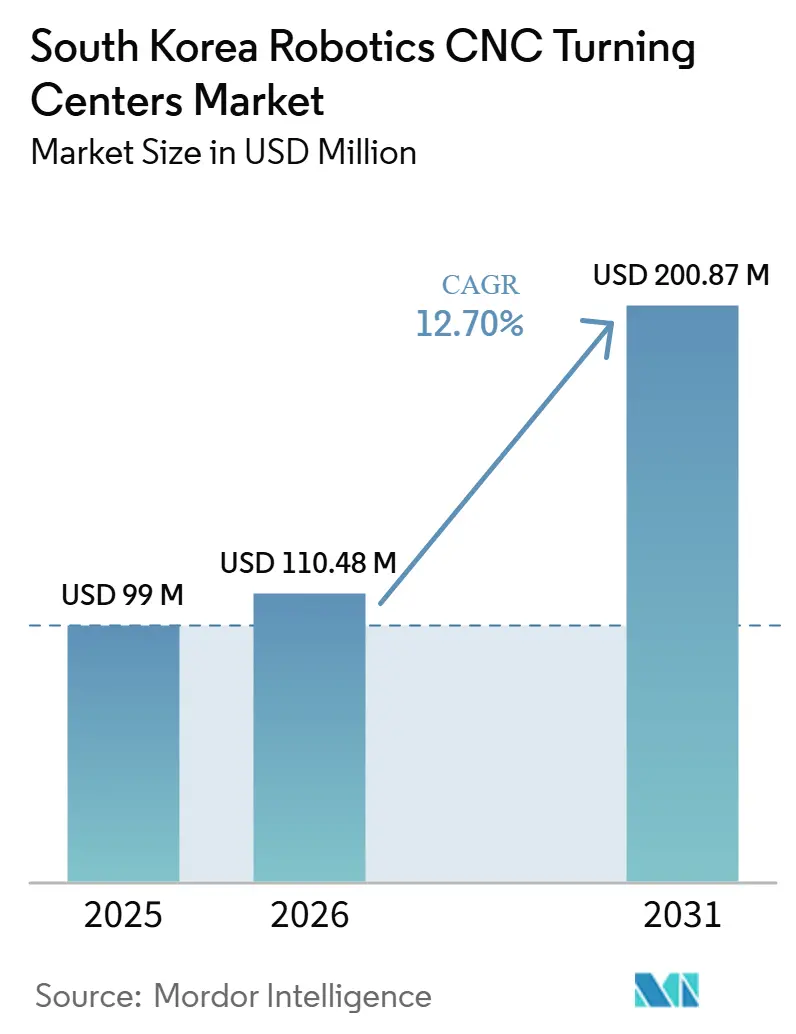

| Base Year Market Size (2025) | USD 99 Million |

| Market Size (2026) | USD 110.48 Million |

| Market Size (2031) | USD 200.87 Million |

| Growth Rate (2026 - 2031) | 12.70% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South Korea Robotics CNC Turning Centers Market Analysis by Mordor Intelligence

The South Korea Robotics CNC Turning Centers Market size is projected to expand from USD 99 million in 2025 and USD 110.48 million in 2026 to USD 200.87 million by 2031, registering a CAGR of 12.70% from 2026 to 2031.

The South Korea robotics CNC turning centers market is expanding in a manufacturing environment where automation is already embedded into day-to-day production, with robot density reaching 1,220 units per 10,000 manufacturing employees in 2024, far above the global average of 177. The South Korea robotics CNC turning centers market is also being supported by a structural labor shortage, as the country entered a super-aged society status in December 2024, and the prime working-age population is projected to contract sharply over the next 2 decades. Demand remains broad rather than concentrated in a single vertical, because electronics, semiconductors, automotive, medical device, aerospace, defense, and energy manufacturers all require tighter tolerances and more stable output than manual loading can sustain at scale. Government policy is widening adoption across the buyer base through robot investment plans, strategic technology support, and SME-focused automation programs, helping reduce reliance on a few large conglomerates. The South Korea robotics CNC turning centers market is therefore moving forward on a mix of demographic pressure, established automation depth, diversified end-user demand, and stronger domestic integration capability.

Key Report Takeaways

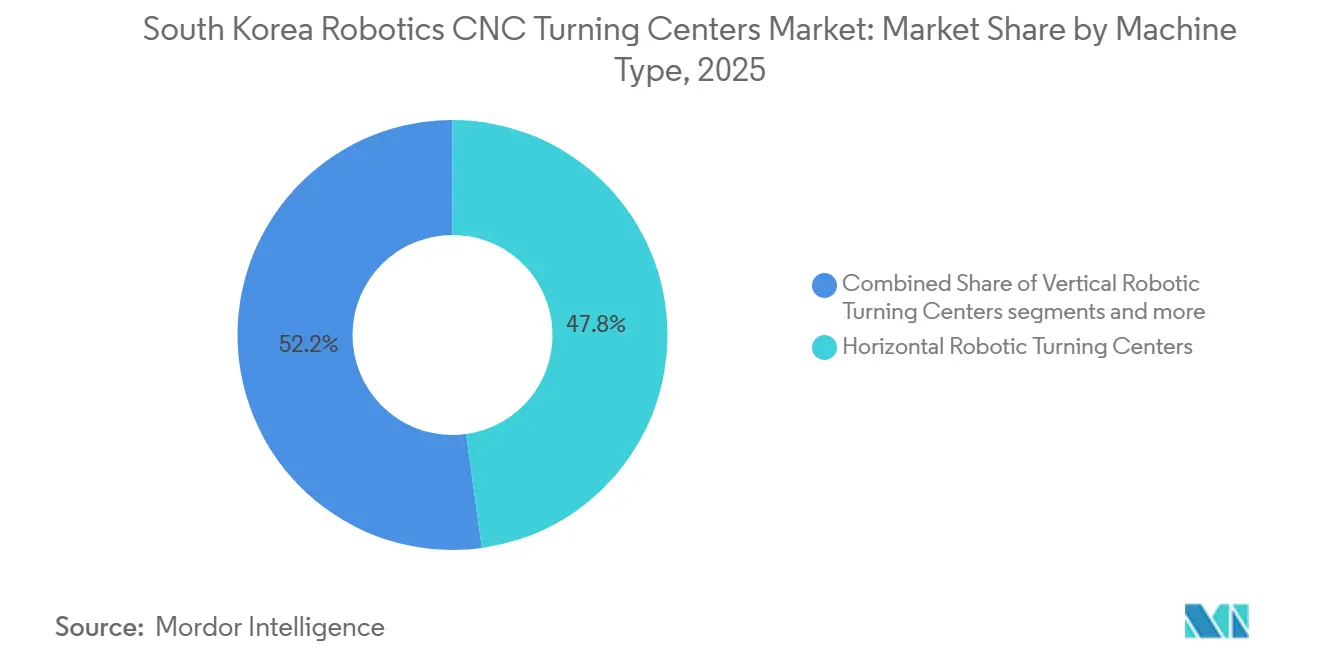

- By machine type, horizontal robotic turning centers held 47.8% share in 2025, while multi-tasking robotic turning centers are projected to expand at a 13.5% CAGR through 2031.

- By robot type, articulated robots accounted for 57.2% of the South Korean robotics CNC turning centers market size in 2025, while collaborative robots are forecast to record the fastest growth at a 14.2% CAGR through 2031.

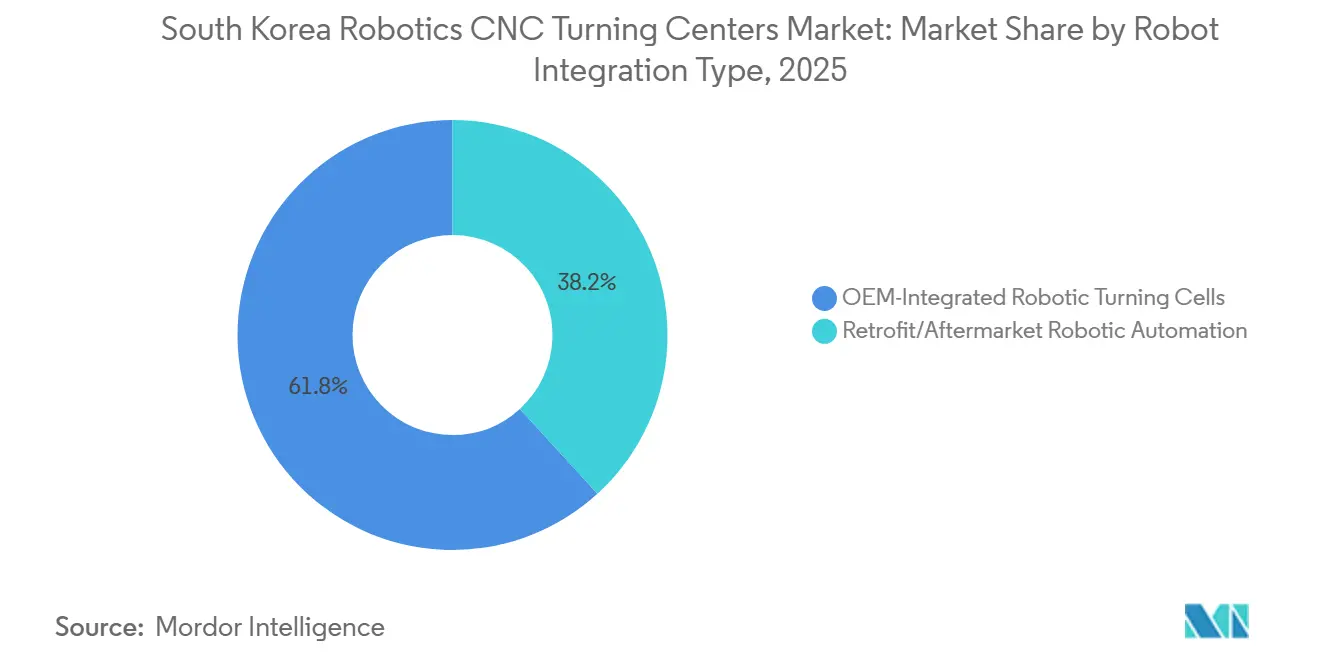

- By robot integration type, OEM-integrated robotic turning cells accounted for 61.8% of the South Korea robotics CNC turning centers market share in 2025, while retrofit/aftermarket robotic automation is expected to grow fastest at a 13.8% CAGR through 2031.

- By end-user industry, automotive and commercial vehicles captured 36.7% of the market in 2025, while medical devices and surgical instruments are projected to advance at a 14.9% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

South Korea Robotics CNC Turning Centers Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Highest Robot Density Globally | +2.5% | National, concentrated in Gyeongnam, Gyeonggi, and Ulsan industrial corridors. | Short term (≤ 2 years) |

| National Automation Policy Linked to Demographic Crisis | +2.3% | National, with early adoption gains in large-scale manufacturing zones | Medium term (2-4 years) |

| Robot-Friendly Industrial Base Led by Electronics and Automotive Conglomerates | +2.1% | National, with concentrated demand in semiconductor clusters such as Pyeongtaek and Hwaseong, and the Ulsan automotive zone | Short term (≤ 2 years) |

| Domestic OEMs Embedding Robotics in Next-Generation Turning Platforms | +1.8% | National, led by Changwon and Busan machine tool manufacturing clusters | Medium term (2-4 years) |

| Growth in Industrial Robot Installations Supporting CNC Turning Automation | +1.7% | National, with early gains in EV and electronics component manufacturing zones | Medium term (2-4 years) |

| Government-Backed SME Automation Programs Lowering Barriers for Smaller Machine Shops | +1.4% | National, with early gains in SME manufacturing hubs across Gyeongnam and Incheon | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Highest Robot Density Globally

The South Korea robotics CNC turning centers market benefits from an installed automation base deeper than that of any other manufacturing economy. South Korea recorded 1,220 industrial robots per 10,000 manufacturing employees in 2024, and that density has increased at an average annual rate of 7% since 2019.[1] International Federation of Robotics, “Robot Density Surges in Europe, Asia, and Americas,” IFR, ifr.org The global average stood at 177 units in 2024, which means Korean manufacturers already operate in a production environment where robotics is routine rather than experimental. This benefits the South Korea robotics CNC turning centers market because systems integration, maintenance support, programming capability, and operator familiarity are already present across major industrial corridors. That installed support structure reduces commissioning friction, shortens deployment time, and helps manufacturers move from standalone CNC equipment to robotic turning cells with less disruption than peers in less-automated countries.

National Automation Policy Linked to Demographic Crisis

The South Korea robotics CNC turning centers market is also being boosted by a policy response directly tied to labor and population pressures. MOTIE (Ministry of Trade, Industry and Energy) finalized the 4th Basic Plan for Intelligent Robots in January 2024, with more than KRW 3 trillion (USD 2.1 billion) in public and private investment and a target to deploy 1 million advanced robots by 2030.[2]InvestKorea and MOTIE, “All Eyes on K-Robots, The Status and Strategy of Korea’s Robotics Industry,” InvestKorea, investkorea.org South Korea entered super-aging status in December 2024, and the ILO (International Labor Organization) projects the prime working-age population to fall from 51% to 31% of the total population by 2044. The fertility rate remained at 0.75 in 2024, keeping South Korea at the bottom of the OECD and reinforcing the persistence of the labor shortfall. Robotics was added to the list of 19 national strategic technologies in May 2025, thereby strengthening funding priorities and regulatory support for manufacturing automation.[3]Yonhap News Agency, “S. Korea Newly Adds Robotics, Defense on List of National Strategic Technologies,” Yonhap, en.yna.co.kr These conditions keep the South Korea robotics CNC turning centers market tied to a long-term labor-replacement need rather than a short-lived investment cycle.

Robot-Friendly Industrial Base Led by Electronics and Automotive Conglomerates

The South Korea robotics CNC turning centers market is supported by large buyers in the electronics and automotive production sectors that already run advanced, automation-heavy operations. The IFR (International Federation of Robotics) identifies those 2 sectors as the country’s dominant industrial robot end users, and South Korea accounted for 6% of global robot installations in 2024. This concentration matters because leading OEMs are raising supplier expectations on process control, traceability, and repeatability, which are harder to meet with manually loaded turning setups. Hyundai WIA demonstrated a fully automated EV component manufacturing cell at SIMTOS (Seoul International Manufacturing Technology Show) 2024 that combined autonomous mobile robots, collaborative robots, and machine tools in a single unmanned solution. The South Korea robotics CNC turning centers market, therefore, gains not only from direct capital spending by conglomerates but also from the pressure those firms place on tier-1 and tier-2 suppliers to meet tighter quality and automation standards. This supports ongoing demand for precision components, including connectors, housings, shafts, motor parts, and battery-related hardware.

Domestic OEMs Embedding Robotics in Next-Generation Turning Platforms

The South Korea robotics CNC turning centers market is also being strengthened by machine tool builders that are designing robotics compatibility into new platforms from the start. DN Solutions introduced its DNX multi-tasking turning series with a clear focus on consolidating turning and milling and simplifying future automation integration. The company also launched the PV 6300 vertical turning center, compatible with its ROBOSOL robotic cell solution, which supports lights-out, uncrewed operation. This design direction reduces the integration burden that once slowed adoption, especially for buyers without large in-house engineering teams. South Korea’s national robot plan also targets a rise in domestic core component self-sufficiency from 44% to 80% by 2030, which improves the case for locally engineered, robot-ready machine platforms. As a result, the South Korea robotics CNC turning centers market is becoming easier to scale through domestic OEM ecosystems rather than through one-off external integration projects.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Upfront Investment Required for Robot-Integrated CNC Turning Cells | -2.3% | National, with greater constraints in SME-dominated precision machining sub-sectors | Short term (≤ 2 years) |

| Chinese OEM Competition Pressures the Domestic Machine Tool Industry | -1.9% | National, with intensified price pressure in mid-tier turning center segments | Medium term (2-4 years) |

| Tacit Knowledge Capture Limits Automation of Precision Turning | -1.5% | National, particularly in aerospace and medical precision component manufacturing | Long term (≥ 4 years) |

| Concentrated Robot Demand Creates Market Dependency Risk | -1.2% | National, concentrated in electronics and automotive end-user clusters | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Upfront Investment Required for Robot-Integrated CNC Turning Cells

The South Korea robotics CNC turning centers market still faces a clear capital barrier for smaller buyers. A complete robotic turning cell includes the turning center, robot, safety systems, grippers, and integration engineering, and that full package remains difficult for many smaller firms to fund. More than 99% of South Korean companies are SMEs, meaning a large share of the potential buyer base lacks the same balance sheet capacity as large conglomerates. MSS (Ministry of SMEs and Startups) and KITECH (Korea Institute of Industrial Technology) addressed this issue through support programs that offer grants of up to KRW 95 million (USD 65.9 thousand) and cover up to 50% of project costs for eligible automation projects. The OECD also documented that Korea’s Smart Manufacturing Innovation Initiative can fund up to 50% of smart factory project costs through a tiered public-private model. Even with support, the remaining co-investment burden and financing cost still slow adoption in the South Korea robotics CNC turning centers market, especially for sub-scale machine shops.

Chinese OEM Competition Pressures the Domestic Machine Tool Industry

The South Korea robotics CNC turning centers market also faces price pressure from Chinese machine tool manufacturers moving upward from entry-level offerings into the mid-tier range. The USCC (United States-China Economic and Security Review Commission) reported that Chinese producers reached more than 99% domestic share in low-end machines and raised the localization rate of mid-range CNC machine tools from 62.6% to 73.5%, while becoming net exporters of CNC machines from 2021 onward. A 2024 study in the Asian Review of Political Economy stated that the rise of Chinese CNC machine tool firms had weakened the competitiveness of Korean counterparts, particularly in price bands accessible to SMEs. This matters in the USD 80,000 to USD 250,000 range, where performance gaps are narrowing, and purchase decisions remain highly cost-sensitive. South Korea has responded through a domestic CNC controller commercialization effort led by KIMM (Korea Institute of Machinery and Materials), in partnership with DN Solutions, Wia Machine Tools, Hwacheon Machinery, and SMEC, with full-scale domestic sales targeted for 2026. The South Korea robotics CNC turning centers market, therefore, remains exposed to external price competition even as local OEMs try to strengthen control over critical automation components.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Machine Type: Horizontal Configurations Anchor Demand as Multi-Tasking Platforms Lead Growth

Horizontal robotic turning centers held 47.8% of the South Korea robotics CNC turning centers market share in 2025, keeping them in the lead across machine types. Their large installed base came from long use in automotive and electronics production, where robot loading patterns are already well established. Horizontal layouts fit articulated and gantry loading systems with less process disruption, and that keeps them practical for suppliers that need stable throughput on shafts, discs, and flanges. The segment also benefits from familiar tooling practices and operator experience, which lowers the burden when a shop moves from standalone CNC equipment to robotic cells. Vertical robotic turning centers retained an important position for heavy or large-diameter components, because vertical fixturing improves chip flow and helps stabilize the workpiece during demanding cuts.

Multi-tasking robotic turning centers are projected to grow at a 13.5% CAGR through 2031, making them the fastest-growing segment of the South Korea robotics CNC turning centers market by machine type. The appeal lies in the ability to combine turning and milling in a single robotic cell, reducing handling steps and limiting tolerance loss between operations. This is especially relevant in EV motor shafts, rotor hubs, battery cooling manifolds, aerospace structures, and other parts that need more than one machining process in a tightly controlled sequence. DN Solutions launched its DNX series with a stated goal of making multitasking machining more accessible, suggesting that OEMs see this platform moving toward broader use rather than a narrow, premium niche. The South Korea robotics CNC turning centers market is therefore keeping horizontal systems as the volume base, while multi-tasking platforms are taking a larger share of new demand.

By Robot Type: Articulated Arms Dominate While Cobots Open Access for Smaller Buyers

Articulated robots accounted for 57.2% of the South Korea robotics CNC turning centers market share in 2025, reflecting their broad utility in machine tending. Their multi-axis reach, payload flexibility, and ability to work in tighter cell geometries make them the preferred option for heavier parts and more complex handling paths. These robots also support in-cell inspection, deburring, and marking, helping manufacturers combine multiple steps into a single controlled process. That flexibility is especially valuable in automotive, heavy industrial, and mixed-part production, where the workpiece mix changes more often than in fully standardized lines. Gantry and Cartesian systems remained relevant in structured, high-volume environments, particularly in electronics manufacturing, where linear precision and repeatability stay important.

Collaborative robots are forecast to expand at a 14.2% CAGR through 2031, making them the fastest-growing robot type in the South Korea robotics CNC turning centers market. Their growth is tied to a different buyer profile, because many SME machine shops could not justify the footprint and cost of safety-caged articulated cells. Cobots reduce that barrier by operating with less infrastructure and by fitting shops that need automation without a full plant redesign. Hanwha Robotics and Wia Machine Tools signed a strategic MOU in September 2025 to co-develop turnkey cobot and machine tool automation solutions specifically targeting this buyer group. The South Korea robotics CNC turning centers market is also benefiting from government subsidy programs that can cover up to 50% of qualifying project costs, making cobot tending one of the most practical first steps into robotic automation for smaller manufacturers.

By Robot Integration Type: OEM Cells Hold the Lead While Retrofit Demand Expands Faster

OEM-integrated robotic turning cells accounted for 61.8% of the market in 2025, indicating a preference among larger manufacturers for factory-engineered solutions. These buyers value one-source warranty support, tuned CNC-to-robot communication, and established service coverage that can reduce downtime after installation. Native integration also shortens setup time because the programming environment, hardware match, and commissioning logic are designed together rather than assembled from separate suppliers. That is particularly useful in automotive and electronics facilities where utilization targets are high and production interruptions are costly. The South Korea robotics CNC turning centers market, therefore, still leans toward OEM cells when the buyer has the capital and the need for full-scale, highly reliable automation.

Retrofit and aftermarket robotic automation is projected to grow at a 13.8% CAGR through 2031, making it the fastest-growing segment of the South Korea robotics CNC turning centers market. The installed fleet of conventional CNC turning centers built up over decades provides a strong base for retrofit demand, as many firms can automate existing machines rather than replace them outright. That choice is especially attractive for SMEs that already own depreciated turning centers and want a lower-risk entry path into robotic loading. Korea’s process automation subsidy was designed for this use case, supporting established facilities that want to automate labor-intensive or hazardous processes. The South Korea robotics CNC turning centers market gains stability from this trend, as retrofit activity can continue even as spending on new machine tools slows.

By End-User Industry: Automotive Holds the Base While Medical Devices Set the Growth Pace

Automotive and commercial vehicles accounted for 36.7% of the market in 2025, making the segment the largest end-user segment in the South Korea robotics CNC turning centers market. Its lead came from South Korea’s deep vehicle production base in Ulsan, Asan, and Gwangju, along with a large network of machining suppliers. The move toward EV platforms is increasing demand for precise turned parts in motors, reduction gears, and battery management housings, where repeatability matters as much as output. Hyundai WIA’s Total Mobility Manufacturing Solution at SIMTOS 2024 demonstrated how unmanned cells combining machine tools, AMRs (Autonomous Mobile Robots), and cobots can support EV component manufacturing at scale. Electronics and semiconductor equipment also represent a major demand pool, as connectors, housings, and thermal-management components require strict dimensional control and a stable surface finish.

Medical devices and surgical instruments are expected to grow at a 14.9% CAGR through 2031, which gives them the strongest growth rate in the South Korea robotics CNC turning centers market. This segment is being lifted by the same aging trend that is increasing demand for surgical tools, orthopedic implants, and interventional device components inside the country. Aerospace and defense adds another layer of growth because export momentum requires turned parts with certified dimensional traceability and repeatable process control. ISO 13485 compliance requirements in medical production also support robotic adoption, as integrated monitoring and traceability are more reliable in robotic turning cells than in manually loaded setups. The South Korea robotics CNC turning centers market, therefore, shows a broad end-user mix, but the growth premium is clearly moving toward precision-critical and compliance-heavy applications.

Geography Analysis

Gyeongnam and the Busan area remain central to the South Korea robotics CNC turning centers market because this corridor hosts major domestic machine tool builders and a dense supporting supplier base. Changwon and Busan form the core manufacturing base for DN Solutions, Hyundai WIA, and SMEC, which keeps buyers close to OEM engineering, service, and demonstration capacity. That physical proximity shortens feedback loops between end users and equipment builders, helping accelerate the adoption of newer robotic turning formats once they reach commercial launch. DN Solutions broke ground in October 2025 on its Busan Global Unit Advanced Manufacturing Center, investing KRW 100 billion (USD 69.4 million) on a 34,681 m² site, signaling continued production expansion in this southern machine tool cluster. In practical terms, the South Korea robotics CNC turning centers market remains strongly anchored in regions where machine tool supply capability and buyer demand meet within short industrial networks.

Gyeonggi Province and the wider Seoul Capital Region make up the electronics and semiconductor heartland of the South Korea robotics CNC turning centers market. Semiconductor complexes in Pyeongtaek and Hwaseong impose some of the strictest turning requirements in the country, because fabrication equipment components and advanced electronic assemblies require very fine dimensional control. The region also benefits from access to public R&D support linked to the national robot plan, which directs applied robotics investment toward manufacturing use cases. This region’s deep automation culture partly shapes its high national robot density, making lights-out turning-cell adoption a realistic next step rather than a distant objective.

Ulsan remains the automotive center of the South Korea robotics CNC turning centers market, with strong pull from vehicle assembly and precision supplier networks. The shift from internal combustion systems to EV production is creating new demand for machining new material sets and part forms, especially where repeatability becomes harder to maintain with manual loading. Incheon adds support from aerospace and logistics equipment subcontractors, as smaller firms move toward robotic cells to meet precision and traceability requirements. National programs such as the Smart Manufacturing Innovation Initiative and current AI smart factory projects help spread this adoption beyond one or two large regions, which keeps the South Korea robotics CNC turning centers market geographically concentrated but not narrowly confined.

Competitive Landscape

The South Korea robotics CNC turning centers market shows moderate concentration, with domestic OEMs holding strong positions because they operate close to local buyers and maintain long-standing service relationships. DN Solutions, Hyundai WIA, and SMEC benefit from installed machine bases, familiarity with Korean production needs, and alignment with national efforts to strengthen robotics and manufacturing capability. Japanese participants compete more strongly where precision and CNC control depth are critical, while European suppliers are more visible in advanced robotics architecture and collaborative automation layers. Chinese manufacturers continue to pressure the mid-tier range, especially where smaller buyers weigh price heavily, and performance differences have narrowed. This leaves the South Korea robotics CNC turning centers market as a field where domestic presence matters, but technology differentiation still decides who captures new automation spending.

Company strategy is moving in three clear directions across the South Korea robotics CNC turning centers market. One is co-development between machine tool and robot specialists, as shown by the September 2025 MOU between Hanwha Robotics and Wia Machine Tools to build turn-key automation solutions around collaborative robots and CNC machines. Another is the push toward more complete unmanned production cells, demonstrated by Hyundai WIA’s Total Mobility Manufacturing Solution for EV component production. A third is platform design that makes it easier to add automation, as seen in DN Solutions’ robot-ready turning systems and its broader push toward higher-value manufacturing solutions.

The South Korea robotics CNC turning centers market also presents a significant opportunity in retrofit automation, as many buyers seek productivity improvements without replacing core machine assets. Lower cobot costs and public co-funding create a practical path for shops that could not support a full greenfield cell. Digital layers such as AI vision, predictive maintenance, and digital simulation are becoming more important because they extend vendor influence after equipment installation and improve machine utilization over time. Companies that combine retrofit engineering, compliance support, and scalable service coverage are likely to capture more value than players focused only on selling standalone hardware. This makes the South Korea robotics CNC turning centers market competitive but still open to sharing gains by firms that can simplify adoption for mid-sized and smaller manufacturers.

South Korea Robotics CNC Turning Centers Industry Leaders

DN Solutions Co., Ltd.

Hyundai WIA Corporation

Hwacheon Machinery Co., Ltd.

FANUC Corporation

Yaskawa Electric Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: DN Solutions showcased EV-focused automation and advanced CNC machining solutions at the China CNC Machine Tool Fair (CCMT 2026) in Shanghai, presenting machines including the NHP 5505 (second generation) and DEF 5005 with explicit focus on addressing EV sector productivity demands and labor-shortage-driven operational cost pressures.

- October 2025: DN Solutions broke ground on its Busan Global Unit Advanced Manufacturing Center, committing approximately USD 69.4 million (KRW 100 billion) to a 34,681 m² facility in Busan's International Industrial Logistics City, expected to be completed in the second half of 2026, expanding CNC machine tool production and advanced manufacturing capability.

- September 2025: DN Solutions announced Vision 2032 at EMO Hannover 2025. They reported reaching the milestone of 300,000 machines deployed globally across 66 countries, positioning its long-term strategy to become a technology-based total manufacturing solutions leader integrating machine tools, factory automation, and additive manufacturing.

- September 2025: Hanwha Robotics and Wia Machine Tools, a division of Hyundai WIA, signed a strategic MOU for collaborative robot and machine tool automation co-development, with their first jointly engineered solutions combining cobots with CNC turning centers presented at EMO Hannover 2025, targeting growing demand for turn-key precision automation.

South Korea Robotics CNC Turning Centers Market Report Scope

The South Korea Robotics CNC Turning Centers Market is Segmented by Machine Type (Horizontal Robotic Turning Centers, Vertical Robotic Turning Centers, and more), by Robot Type (Articulated Robots, and more), by Robot Integration Type (OEM, Retrofit/Aftermarket Robotic Automation), by End-User Industry (Oil, Gas, & Energy, Aerospace & Defense, and more), The Market Forecasts are Provided in Terms of Value (USD) and Volume (Units).

| Horizontal Robotic Turning Centers |

| Vertical Robotic Turning Centers |

| Multi-Tasking Robotic Turning Centers |

| Others |

| Articulated Robots |

| Collaborative Robots (Cobots) |

| Gantry/Cartesian Robots |

| OEM-Integrated Robotic Turning Cells |

| Retrofit/Aftermarket Robotic Automation |

| Automotive and Commercial Vehicles |

| Aerospace & Defense |

| Medical Devices and Surgical Instruments |

| Oil, Gas, and Energy |

| Electrical, Electronics and Semiconductor Equipment |

| General Industrial Machinery |

| Others |

| By Machine Type | Horizontal Robotic Turning Centers |

| Vertical Robotic Turning Centers | |

| Multi-Tasking Robotic Turning Centers | |

| Others | |

| By Robot Type | Articulated Robots |

| Collaborative Robots (Cobots) | |

| Gantry/Cartesian Robots | |

| By Robot Integration Type | OEM-Integrated Robotic Turning Cells |

| Retrofit/Aftermarket Robotic Automation | |

| By End-User Industry | Automotive and Commercial Vehicles |

| Aerospace & Defense | |

| Medical Devices and Surgical Instruments | |

| Oil, Gas, and Energy | |

| Electrical, Electronics and Semiconductor Equipment | |

| General Industrial Machinery | |

| Others |

Key Questions Answered in the Report

What is the current outlook for the South Korea robotics CNC turning centers market?

The South Korea robotics CNC turning centers market was valued at USD 99 million in 2025, reached USD 110.5 million in 2026, and is projected to reach USD 200.9 million by 2031 at a 12.7% CAGR.

Which machine type leads demand in South Korea?

Horizontal robotic turning centers led demand, with a 47.8% share in 2025, because they fit established automotive and electronics production flows and support common robot loading formats.

Which robot format is expanding the fastest in CNC turning applications?

Collaborative robots are growing fastest at a 14.2% CAGR through 2031 because they lower space, safety, and capital barriers for smaller machine shops.

Why is automation demand rising so strongly in South Korea’s precision machining base?

Labor pressure is a major reason, as South Korea entered super-aging status in 2024, and the prime working-age population is projected to shrink materially over time.

Which end-user segment is creating the strongest growth opportunity?

Medical devices and surgical instruments are the fastest-growing end-user group, with a 14.9% CAGR through 2031, driven by aging-related healthcare demand and stringent traceability requirements.

What is the biggest barrier for smaller buyers?

Upfront costs remain the main barrier, though subsidy programs that cover up to 50% of qualifying automation project costs are helping more SMEs adopt robotic turning cells.

Page last updated on: