South Korea Printed Circuit Board Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

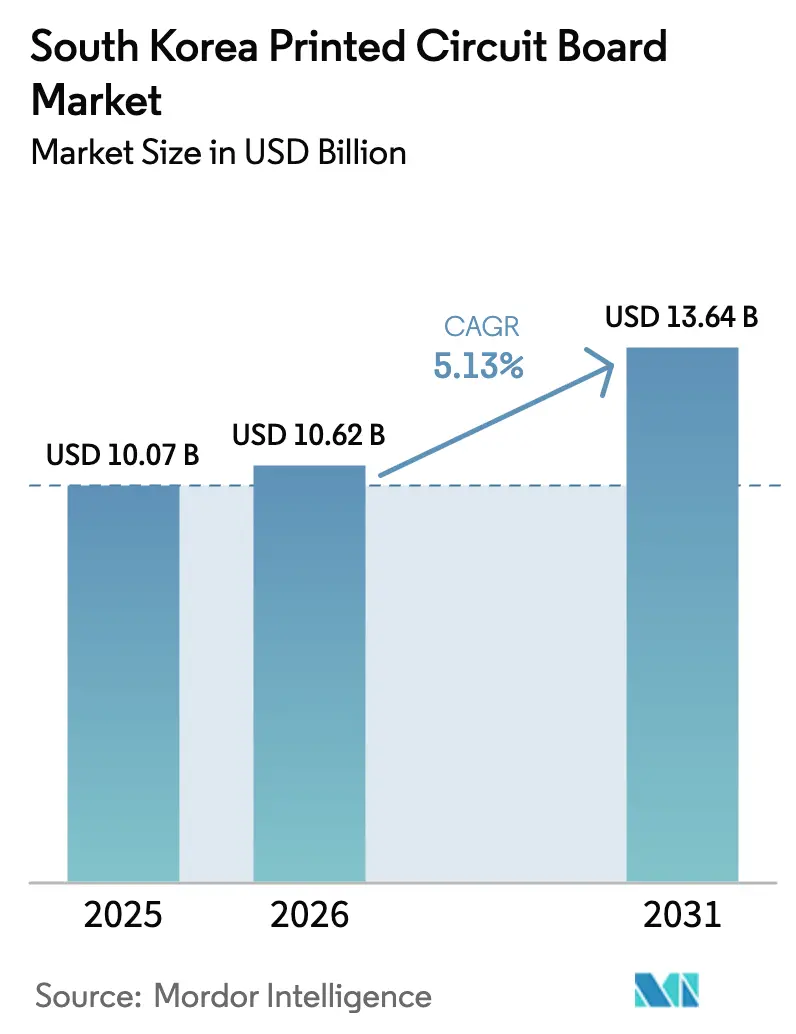

| Base Year Market Size (2025) | USD 10.07 Billion |

| Market Size (2026) | USD 10.62 Billion |

| Market Size (2031) | USD 13.64 Billion |

| Growth Rate (2026 - 2031) | 5.13% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South Korea Printed Circuit Board Market Analysis by Mordor Intelligence

The South Korea printed circuit board market size in 2026 is estimated at USD 10.62 billion, growing from 2025 value of USD 10.07 billion with projections showing USD 13.64 billion, growing at 5.13% CAGR over 2026-2031. Government tax credits under the K-Chips Act, sustained capital outlays by Samsung Electro-Mechanics and LG Innotek, and relocation of defense-electronics demand from offshore vendors are reshaping capacity deployment, pricing power, and technology roadmaps. Flip-chip ball-grid-array substrates for AI accelerators command the highest margins, while Chinese producers continue to undercut standard multilayer prices by as much as 20%. Flexible circuits, driven by foldable smartphones and electric-vehicle battery-management systems, are on track for the fastest unit growth. Supply risk persists for ABF resin and copper foil, intensifying cost volatility. On balance, momentum favors higher-layer, high-speed substrates that align with 5G, AI, and EV use cases.

Key Report Takeaways

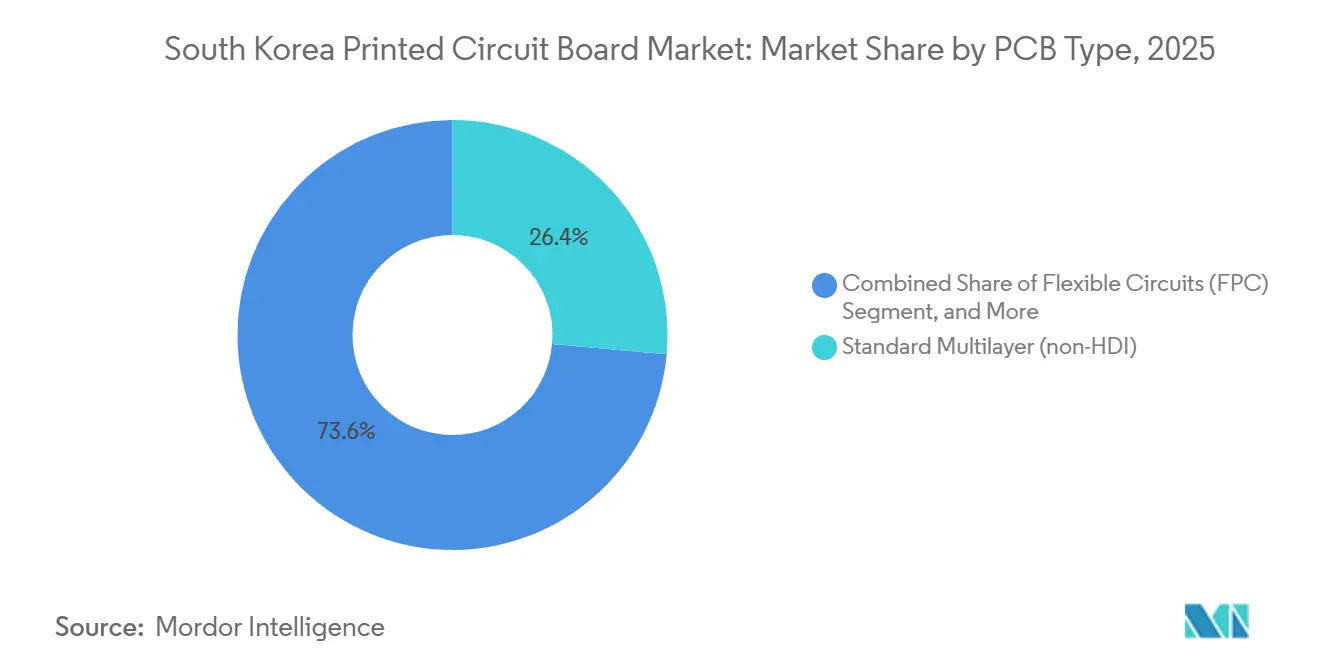

- By PCB type, flexible circuits captured 6.57% growth, the fastest annual pace through 2031, while standard multilayer boards retained 26.43% of the South Korea PCB market share in 2025.

- By substrate material, glass-epoxy FR-4 held 42.33% of the South Korea PCB market in 2025, whereas high-speed, low-loss laminates posted the highest 6.19% CAGR to 2031.

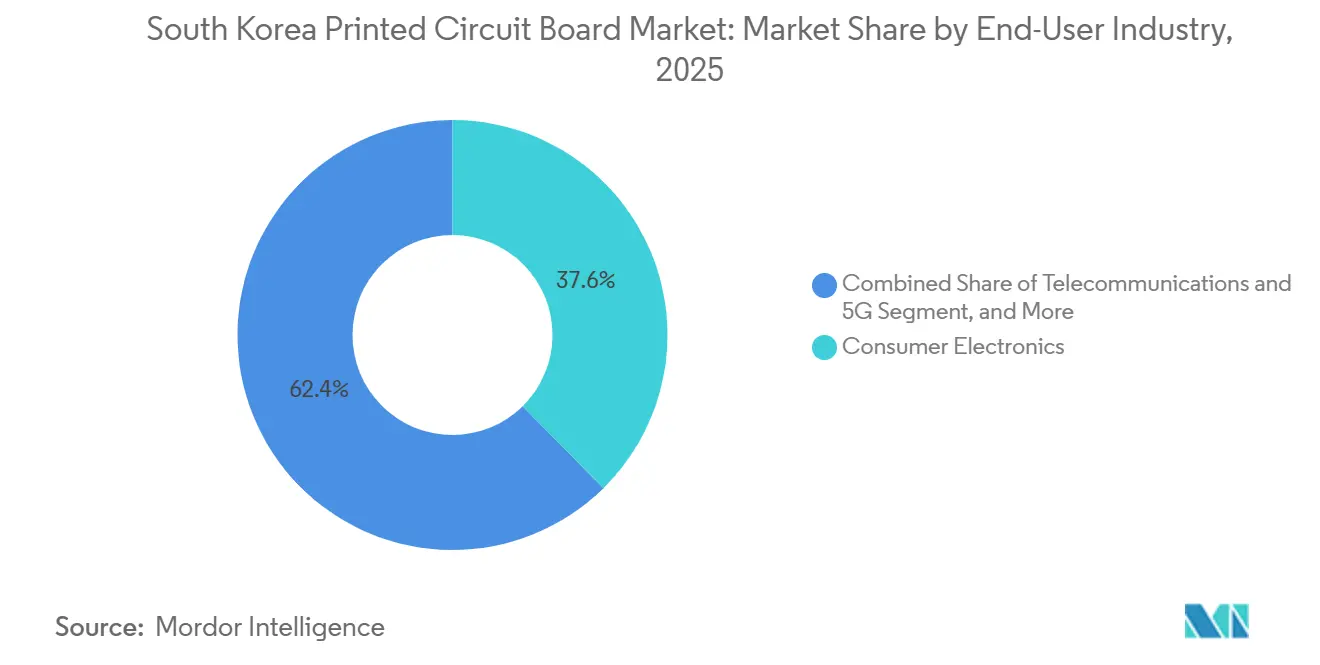

- By end-user industry, telecommunications and 5G infrastructure are advancing at a 6.79% CAGR between 2026-2031, compared with consumer electronics, which accounted for 37.62% of the South Korea Printed Circuit Board Market in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

South Korea Printed Circuit Board Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging demand for HDI boards in 5G smartphones | +1.2% | National, with spillover to Vietnam assembly hubs | Medium term (2-4 years) |

| Rising automotive electronics content in EV platforms | +0.9% | National, concentrated in Ulsan and Gwangju automotive clusters | Long term (≥ 4 years) |

| Government tax incentives for domestic packaging substrate lines | +0.8% | National, focused on Gyeonggi and Chungcheong provinces | Short term (≤ 2 years) |

| Growth of South Korea's system-on-chip foundry ecosystem | +0.7% | National, anchored in Pyeongtaek and Hwaseong | Medium term (2-4 years) |

| Increasing adoption of AI accelerators in data centers | +1.0% | National and regional exports to North America and EU | Medium term (2-4 years) |

| On-shoring of defense radar and missile systems | +0.5% | National, with early gains in Daejeon and Busan defense corridors | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surging Demand for HDI Boards in 5G Smartphones

Samsung introduced the Galaxy S26 in January 2026, integrating 14-layer any-layer HDI boards that raise printed-circuit content per handset by 18% compared with the previous generation.[1]Samsung Electronics, “Samsung Unveils Galaxy S26 Series,” Samsung.com Apple’s iPhone supply chain is mirroring the trend toward greater complexity, sustaining local HDI orders. Korean fabricators are leveraging proximity to Samsung Display’s upcoming 8.6-generation OLED lines to co-design rigid-flex assemblies for foldable panels. Chinese HDI specialists have compressed lead times to 7 days and cut prices by 12-15%, forcing Korean peers to compete on design-for-manufacturability rather than unit cost. The Ministry of Science and ICT allocated KRW 1.2 trillion for next-generation radio access network R&D, reinforcing domestic demand.

Rising Automotive Electronics Content in EV Platforms

Hyundai Motor Group’s Integrated Modular Architecture increases the PCB footprint by threefold by consolidating battery, thermal, and software-update control onto a single domain controller.[2]Hyundai Motor Group, “Integrated Modular Architecture Technical Overview,” Hyundaimotorgroup.com Hyundai Mobis has earmarked KRW 11 trillion for electrification components through 2028, with about 18% directed to PCB procurement. The migration to 800-volt drivetrains demands substrates with higher dielectric strength, pushing suppliers toward polyimide and ceramic-filled epoxy blends that carry 30-40% premiums over FR-4. Korea’s Automotive Electronics Standardization Committee tightened IPC-6012 Class 3 rules in May 2025, raising qualification hurdles. Smaller shops such as Korea Circuit are shifting production from consumer to automotive lines to protect margins.

Government Tax Incentives for Domestic Packaging Substrate Lines

The K-Chips Act provides a 15% investment tax credit and accelerated depreciation, catalyzing KRW 3.8 trillion in announced substrate projects since 2024. LG Innotek’s KRW 600 billion Gumi expansion and Samsung Electro-Mechanics’ undisclosed Busan project focus on flip-chip BGA and RF system-in-package formats.[3]LG Innotek, “Gumi Facility Expansion Announcement,” Lginnotek.com Defense Acquisition Program Administration co-funding of semiconductor packaging elevates the dual-use business case. However, incentives sunset in December 2027, adding urgency to capacity ramp-up decisions.

Increasing Adoption of AI Accelerators in Data Centers

SK Hynix began shipping 12-high HBM3E stacks to NVIDIA in Q3 2025, each requiring complex interposers and high-amp substrates. Samsung Electro-Mechanics reported that AI-accelerator substrates climbed to 34% of its substrate revenue in Q2 2025. OpenAI’s Stargate program is sourcing 40% of its server PCBs from Korean vendors, diversifying away from China. Yield remains a bottleneck, with FC-BGA defect rates around 8%, prompting LG Innotek to invest in laser-direct-imaging tools to halve defect density by late 2026.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in copper foil prices | -0.6% | Global, with acute exposure in spot-indexed contracts | Short term (≤ 2 years) |

| Supply bottlenecks for BT and ABF resin | -0.7% | Global, concentrated in Japan-sourced materials | Medium term (2-4 years) |

| Intensifying price competition from Chinese PCB makers | -0.8% | Regional, affecting ASEAN and North American export lanes | Medium term (2-4 years) |

| Skilled labor shortage in advanced substrate manufacturing | -0.5% | National, most acute in Gyeonggi and Chungcheong | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatility in Copper Foil Prices

Copper averaged USD 8,500-10,200 per metric ton in 2025, swinging 20% on supply-side disruptions, compressing operating margins for mid-tier fabricators locked into 60-day contracts. Samsung Electro-Mechanics hedged 70% of its copper exposure, muting the earnings hit, while smaller firms endured cancellations in price-sensitive IoT orders. The Korea Fair Trade Commission investigated five domestic distributors for alleged premium inflation but found insufficient evidence in December 2025. The International Copper Study Group projects a refined-copper deficit of 180,000 metric tons in 2026, implying sustained volatility.

Supply Bottlenecks for BT and ABF Resin

Ajinomoto Fine-Techno and Mitsubishi Gas Chemical control roughly 70% of global ABF capacity and are reluctant to add lines despite surging AI-server demand, extending substrate lead times by up to 12 weeks. Samsung Electro-Mechanics and LG Innotek resorted to BT resin for some stackups, sacrificing thermal conductivity and layer counts. Doosan Electronics BG gained share in standard epoxy laminates, reporting 92% revenue growth in H1 2025, yet lacks ABF coating prowess. Persistent shortages threaten ramp schedules for high-bandwidth memory substrates through 2027.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By PCB Type: Flexible Circuits Lead Growth While Commoditized Multilayer Boards Face Margin Pressure

Flexible circuits are advancing at a 6.57% CAGR through 2031, the fastest among PCB categories, as foldable smartphones and EV battery-management systems seek lighter, bendable interconnects. Standard multilayer boards retained a 26.43% share of the South Korea printed circuit board (PCB) market in 2025, but Chinese price competition erodes profitability. High-density interconnect boards, essential for 3-nanometer processors in flagship phones, deliver higher average selling prices. Rigid 1-2-sided boards persist in home appliances but are ceding volume to integrated modules.

IC substrates occupy the premium tier and generated 55% of domestic IC-substrate revenue for Samsung Electro-Mechanics, LG Innotek, and Ibiden Korea in 2025, underscoring differentiation through flip-chip BGA and wafer-level chip-scale technologies. Rigid-flex boards are gaining traction in wearables and automotive clusters, where vibration resistance justifies a 40-50% cost premium. Metal-core and ceramic substrates serve LED lighting and power modules, respectively, offering niche but stable demand within the South Korea printed circuit board (PCB) market.

By Substrate Material: High-Speed Low-Loss Laminates Capture Next-Generation Design Wins

Glass-epoxy FR-4 captured 42.33% of the material revenue in the South Korea PCB market in 2025, reflecting its cost advantage in commodity multilayer applications. High-speed low-loss laminates deliver the fastest 6.19% growth as 5G, and 800-gigabit Ethernet switches require dielectric constants below 3.5. Leading suppliers Rogers Corporation and Isola command price premiums of 3.5-4 times FR-4, yet designers accept higher costs to meet signal-integrity budgets.

Polyimide substrates benefit from Samsung Display’s late-2026 OLED ramp, driving volume for rigid-flex assemblies. Packaging resins BT and ABF remain capacity-constrained, hindering some AI-accelerator ramps. Ceramic-filled epoxy and metal-core laminates address thermal management in EV inverters and LED modules, filling specialized yet growing niches within the South Korea printed circuit board (PCB) market.

By End-User Industry: Telecommunications and Defense Outpace Consumer Electronics

Telecommunications and 5G infrastructure expand at 6.79% annually through 2031, lifted by Korea Telecom’s AI-RAN rollout and a government requirement to upgrade 8,500 base stations by 2027. Consumer electronics contributed 37.62% of 2025 demand, but replacement cycles are lengthening. Computing and data-center volume accelerate as OpenAI and hyperscalers source AI server substrates locally.

Automotive PCB demand grows alongside Hyundai’s shift to 800-volt EV architectures, increasing board area and material complexity. Industrial power gear, such as LS Electric’s HVDC transformers, incorporates high-current boards. Aerospace and defense orders rise after Wavevis secured a KRW 265 billion radar contract, highlighting onshoring in defense. Healthcare maintains a high-margin niche with implantable devices requiring IPC Class 3 reliability. These vertical dynamics collectively shape the revenue mix of the South Korea printed circuit board (PCB) market.

Geography Analysis

Korean PCB production is geographically concentrated in Gyeonggi and Chungcheong provinces, which host most advanced substrate fabs. Proximity to Samsung and SK Hynix foundries in Pyeongtaek and Hwaseong shortens logistics cycles for flip-chip BGA substrates, supporting time-critical AI-server builds. Ulsan and Gwangju automotive hubs increasingly draw rigid-flex and high-current multilayer boards as Hyundai accelerates EV output. Defense corridors in Daejeon and Busan absorb high-reliability rigid-flex assemblies for radar and missile systems, reinforcing domestic strategic autonomy.

Export-focused factories in Incheon and Busan ship flexible circuits and standard multilayer boards to Vietnam and North American assembly plants. However, margin pressure from Chinese producers prompts smaller exporters to pivot toward high-speed laminates for 5G radios. The Ministry of Science and ICT’s 5G+ initiative channels R&D funding into rural base-station upgrades, broadening domestic demand beyond Seoul metropolitan projects. Collectively, these regional dynamics underpin the distributed yet interlinked footprint of the South Korea Printed Circuit Board Market.

Jeju and Gangwon provinces play minor roles, mainly serving as hosts to niche suppliers of metal-core boards for renewable-energy inverters. Logistics improvements along the Eastern coastal rail line, completed in late 2025, cut transit time to Pohang steelworks, indirectly stabilizing copper-foil supply. While provincial incentives compete for new fabs, capital remains concentrated near existing semiconductor clusters, ensuring sustained capacity for the South Korea Printed Circuit Board Market.

Competitive Landscape

The premium substrate segment is moderately consolidated, with Samsung Electro-Mechanics, LG Innotek, and Ibiden Korea controlling 55% of revenue. LG Innotek’s KRW 600 billion Gumi expansion, announced in March 2025, internalizes flip-chip BGA capacity and aims to cut defect density to 4% by late 2026. Samsung Electro-Mechanics raised AI-substrate exposure to 34% of its substrate revenue in Q2 2025, leveraging hedged copper positions to protect margins. Ibiden Korea focuses on server CPU interposers for U.S. hyperscalers, benefiting from ABF allocation secured under long-term contracts.

Mid-tier firms such as Simmtech and Korea Circuit pivot toward automotive and memory-module substrates to offset falling standard multilayer prices. Simmtech is preparing SO-CAM lines for LPDDR6 deployment in 2026, while Korea Circuit is upgrading process control to meet the tightened IPC-6012 Class 3 rules. BH Company retains an 80-90% share of Apple iPhone flexible-circuit orders, insulating itself from smartphone cyclicality.

Price competition from Shenzhen and Suzhou PCB makers is most acute in four- to six-layer boards, forcing Korean incumbents to exit commoditized products or emphasize design services. Copper and ABF supply constraints further differentiate well-capitalized leaders from balance-sheet-constrained rivals. Overall, the South Korea PCB market continues to balance consolidation at the high end with fragmentation in legacy tiers.

South Korea Printed Circuit Board Industry Leaders

Samsung Electro-Mechanics Co., Ltd.

LG Innotek Co., Ltd.

IBIDEN Korea Co., Ltd.

Unimicron Technology Korea Co., Ltd.

Korea Circuit Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Korea Telecom completed AI-RAN validation on its commercial 5G network, demonstrating 22% energy savings and 18% capacity gains compared with legacy architectures.

- May 2025: Defense Acquisition Program Administration selected five semiconductor-packaging projects for KRW 450 billion co-funding, prioritizing gallium-nitride and silicon-carbide power modules for radar systems.

- May 2025: ETRI and Wavevis developed gallium-nitride MMICs for AESA radar, achieving 45-watt output power at 10 GHz with 50% efficiency.

- April 2025: Wavevis secured a KRW 265 billion contract to supply L-SAM radar modules, the largest defense-electronics onshoring win in the domestic PCB sector.

South Korea Printed Circuit Board Market Report Scope

The South Korea Printed Circuit Board Market Report is Segmented by PCB Type (Standard Multilayer (non-HDI), Rigid 1-2 Sided, High-Density Interconnect (HDI), Flexible Circuits (FPC), IC Substrates (Package Substrates), Rigid-Flex, Other PCB Types), Substrate Material (Glass Epoxy (FR-4), High-Speed / Low-Loss, Polyimide (PI), Packaging Resins (BT / ABF), Other Substrate Materials), End-user Industry (Consumer Electronics, Computing and Data Centers, Telecommunications and 5G, Automotive and EV, Industrial and Power, Healthcare / Medical, Aerospace and Defense, Other End-user Industries). The Market Forecasts are Provided in Terms of Value in USD.

| Standard Multilayer (non-HDI) |

| Rigid 1-2 Sided |

| High-Density Interconnect (HDI) |

| Flexible Circuits (FPC) |

| IC Substrates (Package Substrates) |

| Rigid-Flex |

| Other PCB Types |

| Glass Epoxy (FR-4) |

| High-Speed / Low-Loss |

| Polyimide (PI) |

| Packaging Resins (BT / ABF) |

| Other Substrate Materials |

| Consumer Electronics |

| Computing and Data Centers |

| Telecommunications and 5G |

| Automotive and EV |

| Industrial and Power |

| Healthcare / Medical |

| Aerospace and Defense |

| Other End-user Industries |

| By PCB Type | Standard Multilayer (non-HDI) |

| Rigid 1-2 Sided | |

| High-Density Interconnect (HDI) | |

| Flexible Circuits (FPC) | |

| IC Substrates (Package Substrates) | |

| Rigid-Flex | |

| Other PCB Types | |

| By Substrate Material | Glass Epoxy (FR-4) |

| High-Speed / Low-Loss | |

| Polyimide (PI) | |

| Packaging Resins (BT / ABF) | |

| Other Substrate Materials | |

| By End-user Industry | Consumer Electronics |

| Computing and Data Centers | |

| Telecommunications and 5G | |

| Automotive and EV | |

| Industrial and Power | |

| Healthcare / Medical | |

| Aerospace and Defense | |

| Other End-user Industries |

Key Questions Answered in the Report

How large is the South Korea PCB market in 2026 and what growth is expected?

South Korea PCB market size is USD 10.62 billion in 2026 and is forecast to rise at a 5.13% CAGR to USD 13.64 billion by 2031.

Which PCB type is growing fastest in South Korea?

Flexible circuits are expanding at a 6.57% CAGR through 2031, driven by foldable smartphones and EV battery-management systems.

What is driving higher material costs for Korean PCB makers?

Price swings in copper foil and supply bottlenecks for ABF resin from Japanese suppliers are increasing input volatility.

Who are the leading companies in Korean IC substrates?

Samsung Electro-Mechanics, LG Innotek, and Ibiden Korea together hold 55% of premium substrate revenue.

How will 5G upgrades affect PCB demand?

Korea Telecom’s AI-RAN rollout and a government mandate to reallocate 28 GHz spectrum require 8,500 base-station upgrades, boosting demand for high-speed low-loss PCBs.

What incentives are available for new PCB capacity?

The K-Chips Act offers a 15% investment tax credit and accelerated depreciation for domestic substrate lines until December 2027.

Page last updated on: