South Korea HBM Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

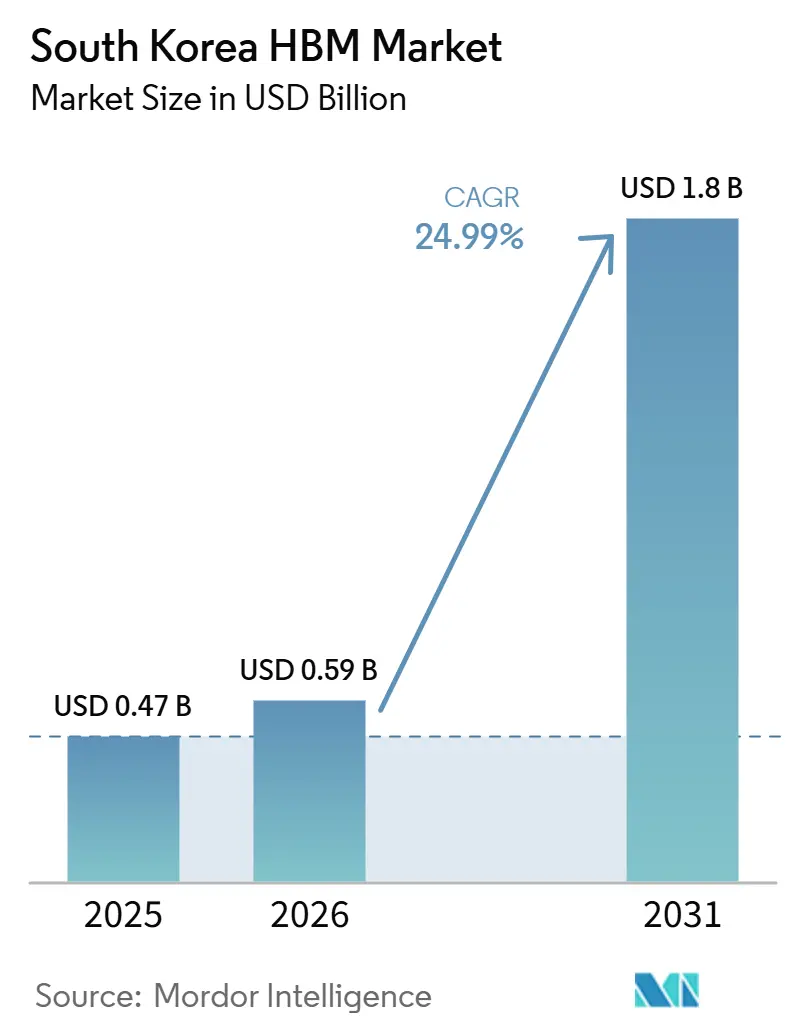

| Base Year Market Size (2025) | USD 0.47 Billion |

| Market Size (2026) | USD 0.59 Billion |

| Market Size (2031) | USD 1.8 Billion |

| Growth Rate (2026 - 2031) | 24.99% CAGR |

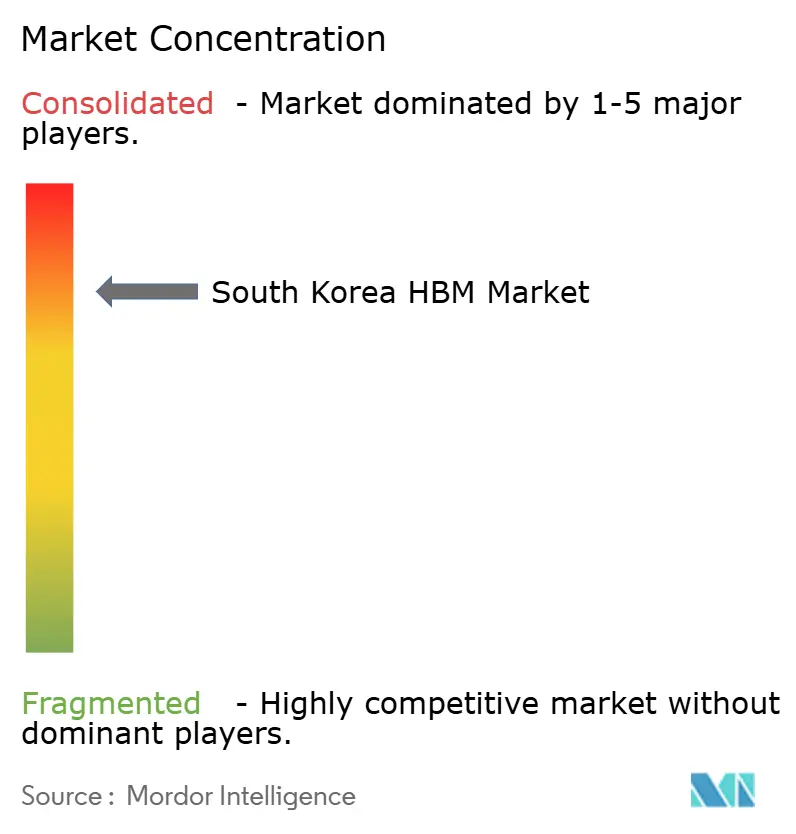

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South Korea HBM Market Analysis by Mordor Intelligence

The South Korea HBM market was valued at USD 0.47 billion in 2025 and estimated to grow from USD 0.59 billion in 2026 to reach USD 1.80 billion by 2031, at a CAGR of 24.99% during the forecast period 2026-2031. This expansion reflects a clear shift in memory economics, where HBM now sits at the center of AI system performance rather than serving as a supporting component. The South Korean HBM market is also closely tied to AI chip demand because AI accelerators accounted for the overwhelming share of HBM revenue in 2025, leaving domestic suppliers highly exposed to GPU and hyperscaler spending cycles. The South Korea HBM market remains concentrated around SK hynix Inc. and Samsung Electronics Co., Ltd., and that concentration supports pricing discipline when qualification cycles restrict the number of suppliers that can ship at scale. The South Korea HBM market also benefits from the policy backdrop created in 2026, as the semiconductor competitiveness act gave a firmer legal basis for cluster development, capacity expansion, and faster project execution. Export controls on China further reinforced this pattern, pushing more of the South Korea HBM market toward U.S.-linked AI infrastructure demand and making customer qualification, packaging access, and product timing central to future revenue capture.

Key Report Takeaways

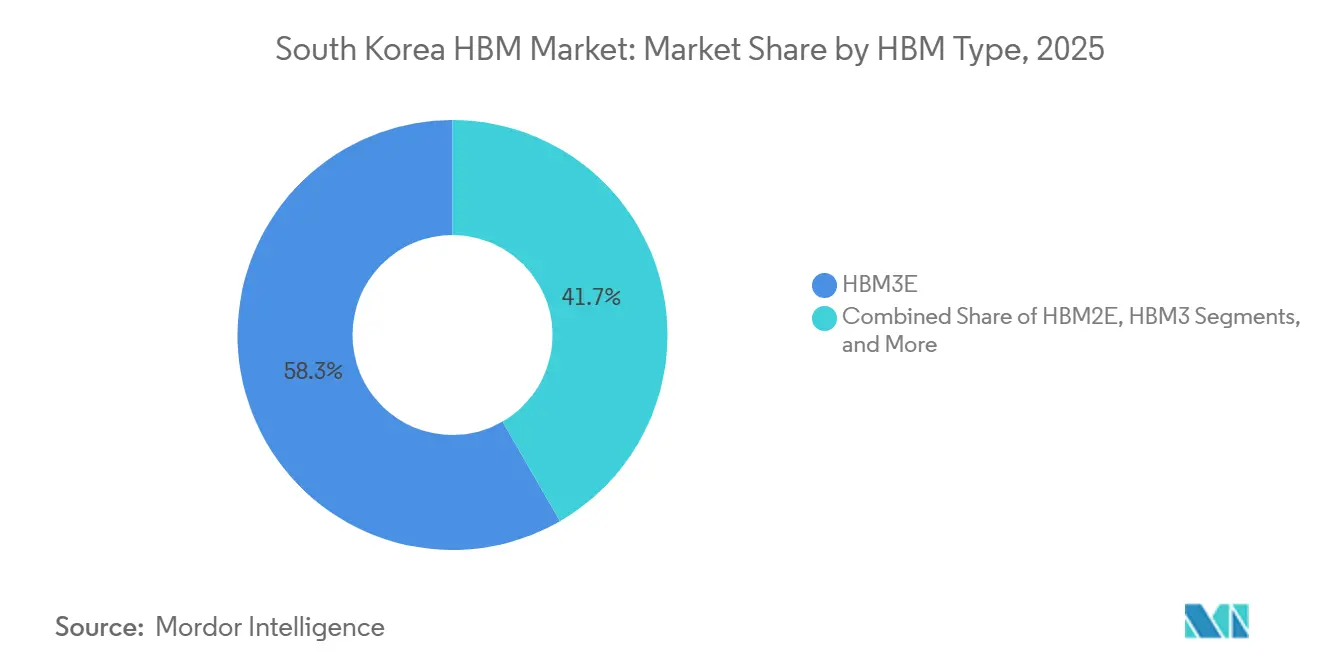

- By HBM type, HBM3E led with 58.33% market share in the South Korea HBM market in 2025, while HBM4 is projected to expand at a 25.91% CAGR through 2031.

- By technology node, 1α (1-Alpha) held 49.81% of revenue in 2025, while 1β and beyond are projected to grow at a 26.09% CAGR through 2031.

- By end use industry, data centers held 86.12% of South Korea HBM market share in 2025 and are projected to grow at a 26.01% CAGR through 2031.

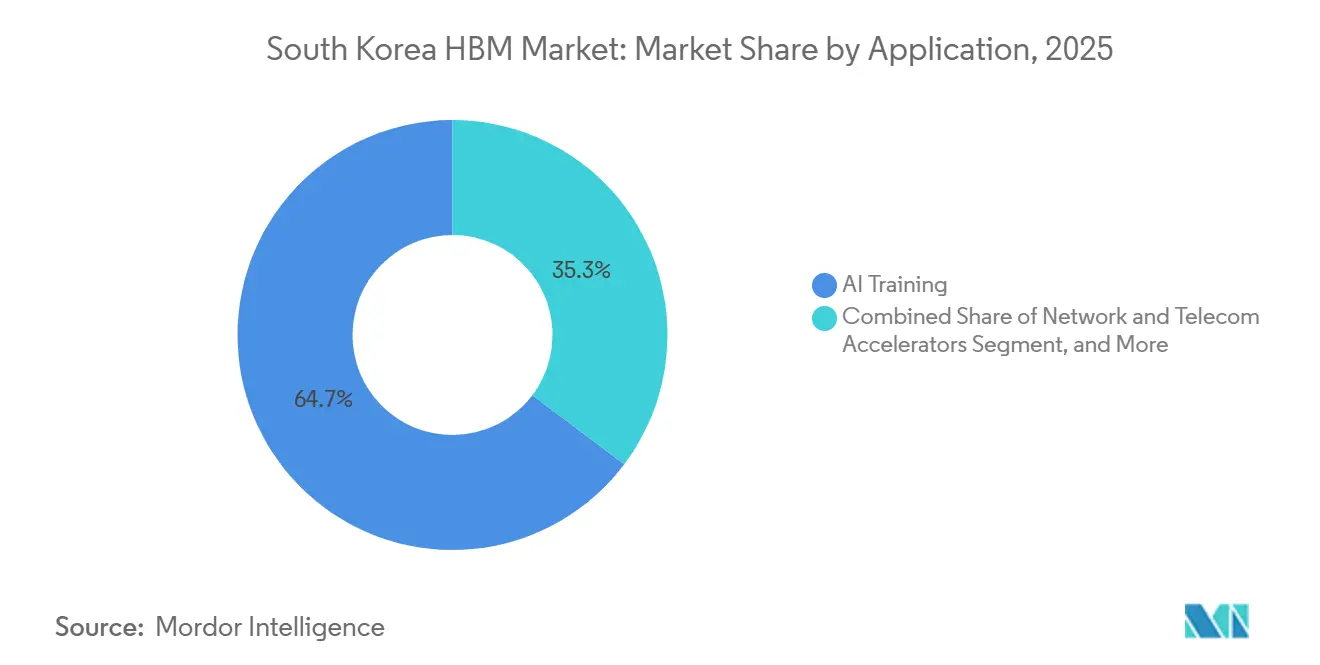

- By application, AI training accounted for 64.73% of revenue in 2025, while AI inference is expected to expand at a 25.03% CAGR through 2031.

- By packaging type, 2.5D interposer-based packaging accounted for 94.22% of the South Korea HBM market size in 2025, while hybrid and next-generation advanced packaging are projected to grow at a 25.64% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

South Korea HBM Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising AI Accelerator Deployment in Domestic and Export Markets | +6.5% | Global, with primary demand centered in North America and supply sourced from South Korea | Short term (≤ 2 years) |

| South Korea Foundry and Packaging Co-Development Improving HBM Ramp Rates | +4.5% | South Korea, especially Cheongju, Icheon, and Pyeongtaek, with packaging links to Taiwan | Medium term (2-4 years) |

| Hyperscaler Qualification Cycles Rewarding Early HBM3E and HBM4 Capacity | +4.0% | Global, with the strongest benefit accruing to South Korea-based suppliers | Short term (≤ 2 years) |

| Growing Server Memory Intensity per AI Node | +3.5% | Global, driven by North American hyperscaler capital spending | Medium term (2-4 years) |

| Shift Toward Higher Stack Counts and Higher Bandwidth Per Package | +3.0% | Global, with production strength concentrated in South Korea | Medium term (2-4 years) |

| Yield Improvement Through Advanced Thermal and Bonding Process Control | +2.0% | South Korea, especially Cheongju and Icheon fabs, with global supply effects | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising AI Accelerator Deployment in Domestic and Export Markets

AI accelerator deployment remains the clearest demand engine for the South Korea HBM market because the customer base is narrow and each large order can redirect a meaningful share of national output. AI chips accounted for more than 90% of global HBM revenue in 2025, underscoring how closely HBM demand has become linked to the AI hardware buildout. The South Korean HBM market also gained a domestic demand node after Rebellions Inc. and Sapeon Korea merged in December 2024, forming Korea’s first AI chip unicorn at KRW 1.3 trillion (USD 929.8 million). Rebellions’ REBEL accelerator uses 144 GB of HBM3E, giving South Korea’s memory suppliers at least one local AI hardware customer outside the U.S. hyperscaler chain.[1]Rebellions Inc., “Rebellions and SAPEON Korea Complete Merger, Launching Korea’s First AI Chip Unicorn,” Rebellions Inc., rebellions.ai That matters for the South Korea HBM market because it creates a small but relevant domestic outlet at a time when export controls have narrowed the addressable geography for advanced HBM. The presence of a strategic SK Group link to Rebellions also supports a more vertically aligned Korean AI hardware stack, which could strengthen local demand resilience if external demand timing becomes uneven.

South Korea Foundry and Packaging Co-Development Improving HBM Ramp Rates

The South Korea HBM market is also being shaped by closer coordination between memory producers, foundries, and packaging partners because time to qualification now matters almost as much as raw wafer capacity. SK hynix built its HBM4 around a logic base die manufactured with TSMC’s advanced process, giving it access to leading foundry capabilities without building that logic stack internally. SK hynix also committed more than KRW 20 trillion (USD 14 billion) to the Cheongju M15X fab, which entered trial operations in early 2026 and was expected to reach 70,000 DRAM wafers per month by year-end. The adjacent P&T7 project adds another KRW 19 trillion (USD 13 billion) in packaging and testing investment, supporting tighter integration between front-end production and HBM stacking. Samsung followed a parallel path in Pyeongtaek, where P4 was being equipped with 1c DRAM tooling and EUV use was expanded to support HBM4 production plans. These moves improve ramp rates in the South Korea HBM market by shortening logistics, reducing handling risk for tall stacks, and tightening the link between node migration and package readiness.

Hyperscaler Qualification Cycles Rewarding Early HBM3E and HBM4 Capacity

Qualification cycles now serve as a practical market-access gate in the South Korean HBM market, as a supplier cannot capture leading AI demand until it passes customer validation. Those tests cover thermal behavior, reliability, signal integrity, and stack-level quality across very high bandwidth interfaces, so a failure can delay revenue for an entire product cycle. SK hynix completed NVIDIA’s HBM4 qualification path and began mass shipments in February 2026, which gave it first-mover access to the Vera Rubin platform and other custom AI programs. Samsung’s 12-layer HBM3E required an extended qualification process before it entered NVIDIA’s supply chain in September 2025, leaving the earlier revenue window largely with SK hynix and Micron. This structure keeps the South Korean HBM market closely tied to process maturity because early validation directly translates into multiyear supply commitments and stronger pricing. It also means that testing infrastructure, package reliability controls, and stack consistency carry strategic weight comparable to fab expansion.

Growing Server Memory Intensity per AI Node

The South Korea HBM market is also benefiting from a steady rise in memory content per AI system because each new accelerator generation carries more HBM capacity than the last one. Industry tracking cited in the source material showed HBM capacity per AI ASIC moving from 96 GB or 192 GB configurations toward 216 GB or 288 GB per package in newer systems. Micron stated at Computex 2026 that memory content per server had doubled during the prior 3 years and that AI context lengths had been growing rapidly, which supports a rising memory requirement per deployment. Deloitte also projected global AI data center capital expenditure at USD 400-450 billion in 2026 and near USD 1 trillion by 2028, which reinforces the scale of infrastructure spending now tied to advanced memory demand. In the South Korean HBM market, that intensity effect matters because additional memory per accelerator or per rack increases HBM demand even without a corresponding increase in server unit volumes. The result is a growth path that depends not only on the number of AI systems installed, but also on the memory each node requires to support larger models and longer context windows.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Qualification Risk from Stringent Customer Validation Gates | -4.0% | Global, with uniform implications for all South Korea-based HBM suppliers | Short term (≤ 2 years) |

| Advanced Packaging Bottlenecks Limiting Shipment Conversion | -3.5% | Concentrated in Taiwan's packaging capacity, with spillover effects on South Korea suppliers | Medium term (2-4 years) |

| High Capital Intensity for Sub-1Z and Next-Gen HBM Ramp-Up | -2.5% | South Korea clusters, including Cheongju, Pyeongtaek, and Icheon, with global capex effects | Long term (≥ 4 years) |

| Thermal and Signal Integrity Constraints at Higher Stack Heights | -1.5% | Global, affecting all suppliers, though South Korean firms are active in mitigation | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Qualification Risk from Stringent Customer Validation Gates

Qualification risk remains one of the main constraints on the South Korea HBM market because each new HBM generation restarts a lengthy validation process before volume shipments can begin. These reviews cover thermal behavior, interface stability, at-speed testing, and Known Good Stack consistency, so a defect or reliability issue can stall a supplier for months. The Samsung example made this risk visible because its 12-layer HBM3E went through multiple validation rounds before clearing NVIDIA’s requirements in September 2025. That delay effectively handed the highest-value early part of the product cycle to faster-qualified rivals. The South Korea HBM market, therefore, depends not only on making advanced stacks but also on proving that those stacks can operate reliably in the most demanding accelerator platforms. This risk is structural because each generation pushes higher density, tighter thermal margins, and tougher customer thresholds, which keeps the penalty for late qualification very high.

Advanced Packaging Bottlenecks Limiting Shipment Conversion

The South Korea HBM market also faces a packaging bottleneck because HBM stacks do not generate end-customer revenue until they move through advanced interposer packaging and become deployable accelerator modules. In practice, that means Korean HBM supply can outpace the number of finished accelerator packages the ecosystem can assemble. The source material notes that TSMC’s CoWoS capacity was moving toward 120,000-130,000 wafers per month by late 2026, up from 35,000 wafers per month at the end of 2024, yet lines remained heavily booked through 2027. This creates a real conversion constraint for the South Korea HBM market because more upstream memory output does not automatically translate into more deliverable systems. SK hynix’s KRW 19 trillion (USD 13 billion) packaging and testing commitment in Cheongju shows that local players are trying to reduce this dependency over time. Amkor’s 2026 capex increase into 2.5D and high-density fan-out packaging also points to the same issue, though those facilities serve a broader packaging mix than the most advanced AI accelerator configurations.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By HBM Type: HBM3E Leads by Volume but HBM4 Changes the Revenue Mix

HBM3E accounted for 58.33% of revenue in 2025 and remained the volume anchor of the South Korean HBM market, as it supported the main accelerator platforms in commercial use during that period. It served as the working memory layer for NVIDIA Blackwell and AMD MI350 programs, which kept it at the center of near-term production demand. HBM4 is projected to grow at a 25.91% CAGR through 2031, and that pace reflects the transition of NVIDIA Rubin and AMD MI400 systems into larger commercial deployment. HBM2E and HBM3 remain in the mix, but they are increasingly tied to legacy HPC and professional graphics deployments rather than the newest AI clusters. The South Korean HBM market, therefore, shows a split pattern in which an established generation still accounts for most current shipment volume, while the next generation is beginning to pull the growth profile upward.

That transition will not be governed solely by capacity, because qualification timing continues to determine which supplier captures the earliest and highest-value demand windows. SK hynix moved early with HBM4, using its 1bnm process and Advanced MR-MUF packaging, which enabled volume shipments in 2026. Samsung took a different route by tying its HBM4 base die strategy to Samsung Foundry’s 4nm process and targeting hybrid copper bonding for HBM4E. This creates a competitive structure where HBM4 revenue will be divided by validation success and customer timing rather than simple wafer availability. The South Korea HBM industry is therefore moving through a stage where the installed base still depends on HBM3E, but future pricing and strategic positioning will increasingly be shaped by HBM4 qualification. That is why the South Korea HBM market continues to carry both a mature volume layer and a faster-growing premium layer at the same time.

By Technology Node: 1α Holds the Base While 1β and Beyond Drives Expansion

The 1α node held 49.81% of revenue in 2025 and formed the foundation for current HBM3E output, which gave it the largest share of the South Korea HBM market at that point in time. Both SK hynix and Samsung relied on this node generation, as they supplied the dominant HBM products used in current AI deployments. The fastest growth is in 1β and beyond, which is projected to rise at a 26.09% CAGR from 2026 to 2031, as it underpins HBM4 production. SK hynix used its 1bnm-class process for HBM4 and indicated that yield levels were comparable to those of 12-layer HBM3E production, reducing a major execution risk for the next generation. Samsung was preparing 1c DRAM for its HBM4 path and reported internal performance evaluations at 11.7 Gbps, with the Pyeongtaek P4 facility being prepared around that node direction.

Older node families, such as 1X and 1Y, are losing relevance for advanced HBM allocation because the South Korean HBM market is steadily shifting capacity toward denser, more efficient generations. The 1Z node still has a role in transitional HBM3 volume and legacy HPC support, so it is not disappearing at once. JEDEC’s revision of the HBM4 package height ceiling to 775µm extended the commercial life of microbump-based packaging and eased the urgency of an immediate shift to hybrid bonding. That standards change matters because it gives current 1β process investments a longer revenue runway before the next packaging transition becomes unavoidable. The South Korea HBM industry therefore gains time to monetize present node investments before HBM4E and later products force a deeper change in bonding architecture. This keeps the node roadmap of the South Korea HBM market aligned with a more staged packaging transition rather than a sudden break.

By End Use Industry: Data Centers Dominate While Adjacent Demand Channels Begin to Form

Data centers accounted for 86.12% of revenue and 86.12% of the South Korea HBM market in 2025, making them the near-exclusive demand center for advanced HBM. The same segment is projected to grow at a 26.01% CAGR through 2031, which shows that the dominant segment is also expected to remain the fastest-expanding end-use base. That combination reflects the practical buyer universe for advanced HBM, where hyperscalers, cloud providers, and GPU platform vendors account for most of the available output. The South Korea HBM market is therefore still driven overwhelmingly by AI infrastructure procurement rather than broad-based electronics demand. Even where adjacent uses exist, they are small compared with the scale of data center training and inference clusters being deployed globally.

Consumer electronics remain a minor category because current HBM generations are too expensive and power-intensive for broad device integration, so this segment reflects optionality more than present commercial weight. Automotive electronics is more credible over the long term because vehicle-based AI inference is expected to grow as autonomy and advanced driver assistance systems evolve. That path still involves a distinct validation burden because automotive qualification standards such as ISO 26262 extend approval cycles for memory devices in vehicle systems. Telecommunication infrastructure also remains relevant as AI-enabled networking and next-generation wireless systems create possible future demand for bandwidth-intensive memory. These categories collectively matter because they show where diversification could emerge once the data center buildout absorbs slightly less of the addressable supply. The South Korea HBM market is still far from balanced across end uses, but the structure already hints at where secondary demand pools may develop later in the forecast period.

By Application: AI Training Leads Current Revenue While Inference Becomes the Next Structural Driver

AI training accounted for 64.73% of application revenue in 2025, making it the largest role in the South Korean HBM market during the base period. Large-model pre-training clusters need maximum bandwidth per accelerator, so training workloads naturally consume the biggest share of advanced HBM allocation. HPC servers remained a stable secondary application because scientific computing and national supercomputing deployments still require very high memory bandwidth. AI inference is projected to grow at a 25.03% CAGR from 2026 to 2031, making it the fastest-growing application in the South Korean HBM market. That growth pattern is important because inference workloads are increasingly memory-bandwidth-bound as model sizes increase, and full models cannot fit in the limited on-chip cache. The market is therefore beginning to shift from a training-led revenue base toward a more balanced mix where inference becomes much more important to future bit demand.

Graphics and visualization remain present, but their share is constrained because HBM allocation has shifted toward AI customers who can pay more for the limited, leading-edge supply. Network and telecom accelerators are still at an early stage and depend on future router ASIC upgrades and edge inference use cases. The deeper implication for the South Korea HBM market is that performance priorities may change as inference scales, with bandwidth per watt and thermal efficiency becoming more visible alongside raw bandwidth. The source material also notes an expectation that inference could surpass training as the dominant workload type by 2029, which would reinforce that shift in optimization priorities. Suppliers that improve thermal control and bonding precision earlier will be better positioned for that application mix. The South Korea HBM market therefore faces a future where application growth remains strong, but product design priorities gradually move away from only serving the largest training clusters.

By Packaging Type: 2.5D Interposer-Based Packaging Holds the Base While Hybrid Packaging Defines the Next Step

2.5D interposer-based packaging accounted for 94.22% of revenue in 2025 and 94.22% of the South Korean HBM market, demonstrating how thoroughly this architecture dominates current commercial deployments. Every major AI accelerator family in production depends on CoWoS-class interposer integration, so this packaging route remains the standard delivery path for advanced HBM systems. Capacity expansion at the packaging layer has been significant, yet the ecosystem remains constrained because demand for AI accelerators rose faster than the available advanced packaging throughput. Fan-out advanced packaging held only a small share, though it remains relevant for lower-tier accelerators and selected edge AI use cases where CoWoS access is limited. The South Korea HBM market, therefore, remains heavily tied to one packaging architecture, and that dependence reinforces the importance of external packaging capacity allocation.

Hybrid and next-generation advanced packaging is projected to grow at a 25.64% CAGR through 2031, which makes it the fastest-growing packaging category in the South Korea HBM market. JEDEC’s updated height specification delayed mandatory adoption of hybrid bonding for HBM4, but it did not change the long-term direction toward bump-less copper-to-copper interconnection. Samsung has been developing hybrid copper bonding for HBM4E, and SK hynix has also targeted that generation for hybrid bonding adoption with 20-layer stacks in view.[2]Samsung Electronics, “Samsung Electronics Advances Next-Generation Memory Technology for AI Era,” Samsung Electronics, samsung.com As stack heights increase and bandwidth per package rises, packaging moves from being a support function to being a core performance constraint. That makes the next packaging transition one of the most important technology issues in the South Korea HBM market over the outer forecast years. The shift will take time, but the commercial logic already points to hybrid-style architectures becoming the eventual volume path.

Geography Analysis

South Korea’s role in the global HBM supply chain is unusually concentrated because its production capacity is concentrated within a very small number of companies and manufacturing clusters. SK hynix alone accounted for around 62% of global HBM shipments in Q2 2025, and the South Korean HBM market remained anchored by SK hynix and Samsung, its only domestic HBM manufacturers. This gives South Korea a structurally dominant position in advanced memory supply, even though end demand is concentrated outside the country. The main production footprint is in Icheon and Yongin for SK Hynix, in Cheongju for the M15X fab and P&T7 project, and in Pyeongtaek for Samsung’s P3 and P4 campuses. The South Korea HBM market also gained a stronger institutional base after the semiconductor competitiveness act was passed in January 2026 and created a clearer mechanism for cluster designation outside the Seoul metropolitan area.

That legal change matters because it supports the geographic diversification of semiconductor investment within the country. The source material identifies the southwestern Honam region as a second semiconductor hub under this broader policy direction. Export geography is even more concentrated than production geography, as advanced HBM shipments are now closely aligned with U.S. AI infrastructure demand. The U.S. Bureau of Industry and Security extended HBM export controls to China in December 2024, targeting products above a memory bandwidth density threshold of 2 GB/s per mm². As a result, the South Korea HBM market became even more linked to U.S. hyperscaler and GPU procurement cycles, with NVIDIA relationships carrying special weight for SK hynix. That directional concentration deepens dependence on North American AI capex, even though the manufacturing base remains almost entirely within South Korea.

Private investment plans have matched that strategic importance at a very large scale. Samsung Electronics and SK Group pledged KRW 800 trillion (USD 519 billion) for 4 new memory fabs in the Honam region and KRW 81 trillion (USD 52 billion) for HBM packaging infrastructure in Chungcheong.[3]SK hynix Newsroom, “2026 Market Outlook, SK hynix’s HBM to Fuel AI Memory Boom,” SK hynix Newsroom, news.skhynix.com Amkor also committed to expand advanced packaging capacity in Gwangju, which adds more domestic support at the OSAT layer. These commitments show that the South Korea HBM market is not only expanding output, but also broadening the national footprint that supports future supply growth. In geographic terms, South Korea is moving from a concentrated production base toward a more distributed semiconductor network, while still remaining tightly exposed to overseas AI demand concentration.

Competitive Landscape

The South Korea HBM market is highly concentrated because only SK Hynix and Samsung Electronics produce HBM domestically, and both companies sit at the center of the country’s strategic position in global AI memory supply. SK hynix built a strong lead by qualifying early across NVIDIA product cycles and by commercializing advanced multilayer stacks ahead of most rivals. Its position was reinforced by Advanced MR-MUF packaging, early HBM4 readiness, and close coordination with TSMC on the logic base die. Samsung’s competitive approach has leaned more heavily on technical differentiation through foundry integration and its push toward hybrid copper bonding for HBM4. The South Korean HBM market, therefore, does not revolve around a large number of similar suppliers, but around 2 very large rivals using different execution paths to reach the same premium customer set.

Recent strategic moves underline that pattern. SK hynix began mass shipments of 12-layer HBM4 in February 2026 after final validation for NVIDIA’s Vera Rubin platform, which gave it a first-qualified advantage in the newest revenue tier. Samsung re-entered the NVIDIA supply chain for 12-layer HBM3E in September 2025 after an extended qualification period, which restored it as a credible supplier for future HBM4 contracts. SK hynix also committed large capital programs in Cheongju and continued to build out its HBM4 and future packaging path, which shows how capacity, packaging, and qualification are now being planned together. Samsung, for its part, tied its HBM roadmap more tightly to Samsung Foundry and the Pyeongtaek P4 investment cycle, which could matter if integrated memory and logic design becomes a larger source of differentiation. The South Korea HBM market remains concentrated, but it is not static because each product generation can shift relative momentum between the 2 leaders.

A second competitive layer is forming around packaging, equipment, and domestic AI chip design. Amkor Technology’s capex increase for 2026 shows that advanced packaging is becoming more strategically important inside the South Korea HBM market, especially as CoWoS bottlenecks limit shipment conversion. Rebellions also matters because it is the only domestic Korean AI chip company in the source material deploying HBM3E at commercial scale, and that makes it a meaningful local demand-side participant. JEDEC’s standards role also remains strategically important because package rules now shape when new bonding approaches become necessary for the whole supplier base.[4]JEDEC, “High Bandwidth Memory DRAM Standard JESD235,” JEDEC Solid State Technology Association, jedec.org Taken together, the competitive structure of the South Korea HBM market combines a very concentrated manufacturing core with a broader outer layer of packaging, equipment, and design players that influence how quickly new capacity can turn into revenue.

South Korea HBM Industry Leaders

SK hynix Inc.

Samsung Electronics Co., Ltd.

Micron Technology, Inc.

NVIDIA Corporation

Advanced Micro Devices, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: South Korea unveiled a combined KRW 800 trillion (USD 519 billion) investment plan from Samsung Electronics and SK Group for 4 new memory fabs in the southwestern Honam region, specifically targeting HBM production, alongside KRW 81 trillion (USD 52 billion) for HBM packaging infrastructure in the Chungcheong region, the largest coordinated semiconductor investment commitment in the country’s history, designed to double national memory production capacity within 5 years.

- June 2026: Samsung Electronics’ HBM4 revenue surpassed USD 1 billion within the first 4 months of commercial availability, with ongoing supply discussions for both NVIDIA-adjacent and hyperscaler-custom ASIC programs including Broadcom and AMD.

- May 2026: SK hynix received direct investment proposals from global technology companies, including offers to co-fund the Yongin Y1 fab with total committed investment of KRW 31 trillion (USD 22.8 billion), along with funding support for ASML EUV lithography equipment procurement, reflecting hyperscaler interest in securing future HBM supply.

- March 2026: Amkor Technology announced plans to increase capital expenditure to USD 2.5-3 billion in 2026, prioritizing 2.5D and high-density fan-out packaging expansion at its Songdo, Incheon and Taiwan facilities, with advanced packaging revenues expected to nearly triple year over year.

South Korea HBM Market Report Scope

South Korea HBM Market refers to the market for high bandwidth memory (HBM) products and solutions in South Korea, covering their development, manufacturing, distribution, and use across applications such as artificial intelligence, high-performance computing, graphics processing, data centers, and advanced semiconductor systems.

The South Korea HBM Market Report is Segmented by HBM Type (HBM2E, HBM3, HBM3E, and HBM4), Technology Node (1X/1Y Nodes, 1Z Node, 1α (1-Alpha), and 1β and Beyond), End Use Industry (Data Centers, Consumer Electronics, Automotive Electronics, Telecommunication Infrastructure, and Other End User Industries), Application (AI Training, AI Inference, HPC Servers, Graphics and Visualization, Network and Telecom Accelerators), and Packaging Type (2.5D Interposer-Based Packaging, Fan-Out Advanced Packaging, and Hybrid/Next-Generation Advanced Packaging). The Market Forecasts are Provided in Terms of Value (USD).

| HBM2E |

| HBM3 |

| HBM3E |

| HBM4 |

| 1X/1Y Nodes |

| 1Z Node |

| 1α (1-Alpha) |

| 1β and Beyond |

| Data Centers |

| Consumer Electronics |

| Automotive Electronics |

| Telecommunication Infrastructure |

| Other End User Industries |

| AI Training |

| AI Inference |

| HPC Servers |

| Graphics and Visualization |

| Network and Telecom Accelerators |

| 2.5D Interposer-Based Packaging |

| Fan-Out Advanced Packaging |

| Hybrid/Next-Generation Advanced Packaging |

| By HBM Type | HBM2E |

| HBM3 | |

| HBM3E | |

| HBM4 | |

| By Technology Node | 1X/1Y Nodes |

| 1Z Node | |

| 1α (1-Alpha) | |

| 1β and Beyond | |

| By End Use Industry | Data Centers |

| Consumer Electronics | |

| Automotive Electronics | |

| Telecommunication Infrastructure | |

| Other End User Industries | |

| By Application | AI Training |

| AI Inference | |

| HPC Servers | |

| Graphics and Visualization | |

| Network and Telecom Accelerators | |

| By Packaging Type | 2.5D Interposer-Based Packaging |

| Fan-Out Advanced Packaging | |

| Hybrid/Next-Generation Advanced Packaging |

Key Questions Answered in the Report

What is the size and growth outlook for the South Korea HBM market?

The South Korea HBM market was valued at USD 0.47 billion in 2025, reached USD 0.59 billion in 2026, and is projected to reach USD 1.80 billion by 2031 at a 24.99% CAGR.

Which end-use area drives most HBM demand in South Korea?

Data centers dominate demand, holding 86.12% of revenue in 2025, because hyperscalers and GPU platforms absorb most advanced HBM output.

Which HBM generation leads current revenue in South Korea?

HBM3E led the revenue mix in 2025 with a 58.33% share, reflecting its role across the largest commercial AI accelerator programs.

What is the fastest-growing application for HBM in South Korea?

AI inference is the fastest-growing application, with a projected 25.03% CAGR through 2031 as model serving becomes more memory-bandwidth intensive.

Why is packaging so important for South Korea’s HBM supply chain?

Advanced packaging is critical because HBM stacks must move through interposer-based assembly before they become usable accelerator modules, and packaging limits can restrict shipment conversion.

How concentrated is competition among South Korea HBM suppliers?

Competition is highly concentrated because SK hynix and Samsung Electronics are the only domestic HBM manufacturers, and customer qualification cycles make it hard for additional suppliers to scale quickly.

Page last updated on: