South Korea Electronics Manufacturing Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

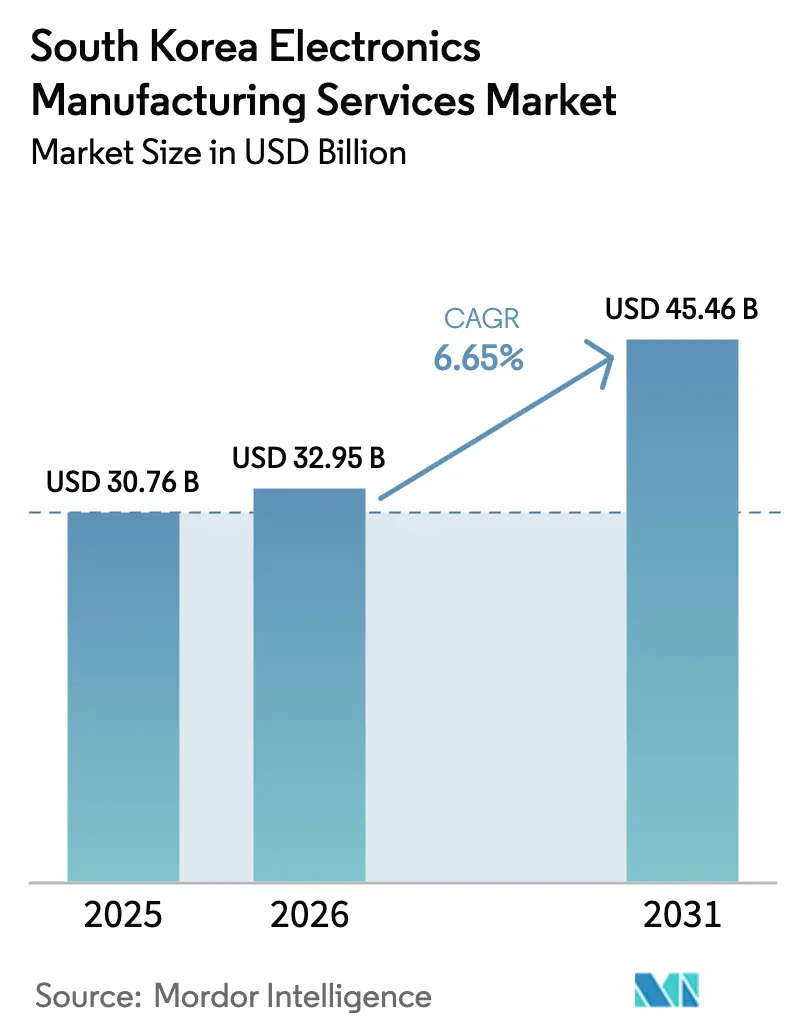

| Base Year Market Size (2025) | USD 30.76 Billion |

| Market Size (2026) | USD 32.95 Billion |

| Market Size (2031) | USD 45.46 Billion |

| Growth Rate (2026 - 2031) | 6.65% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South Korea Electronics Manufacturing Services Market Analysis by Mordor Intelligence

The South Korea Electronics Manufacturing Services Market was valued at USD 30.76 billion in 2025 and expected to grow from USD 32.95 billion in 2026 to reach USD 45.46 billion by 2031, at a CAGR of 6.65% during the forecast period (2026-2031). Robust sovereign incentives, the reshoring of server-board assembly from China, and surging demand for advanced packaging for AI accelerators anchor near-term momentum. Tier-2 providers are upgrading to smart-factory lines that pair collaborative robots with machine-vision inspection, which trims cycle time and defects even as electricity tariffs edge higher. Automotive OEMs are shifting power-electronics outsourcing to domestic partners, while global contract manufacturers open Korean engineering hubs to capture design-for-manufacturability work. Together, these forces position the South Korea electronics manufacturing services market as a dependable option for brand owners seeking resilient, turnkey supply chains.

Key Report Takeaways

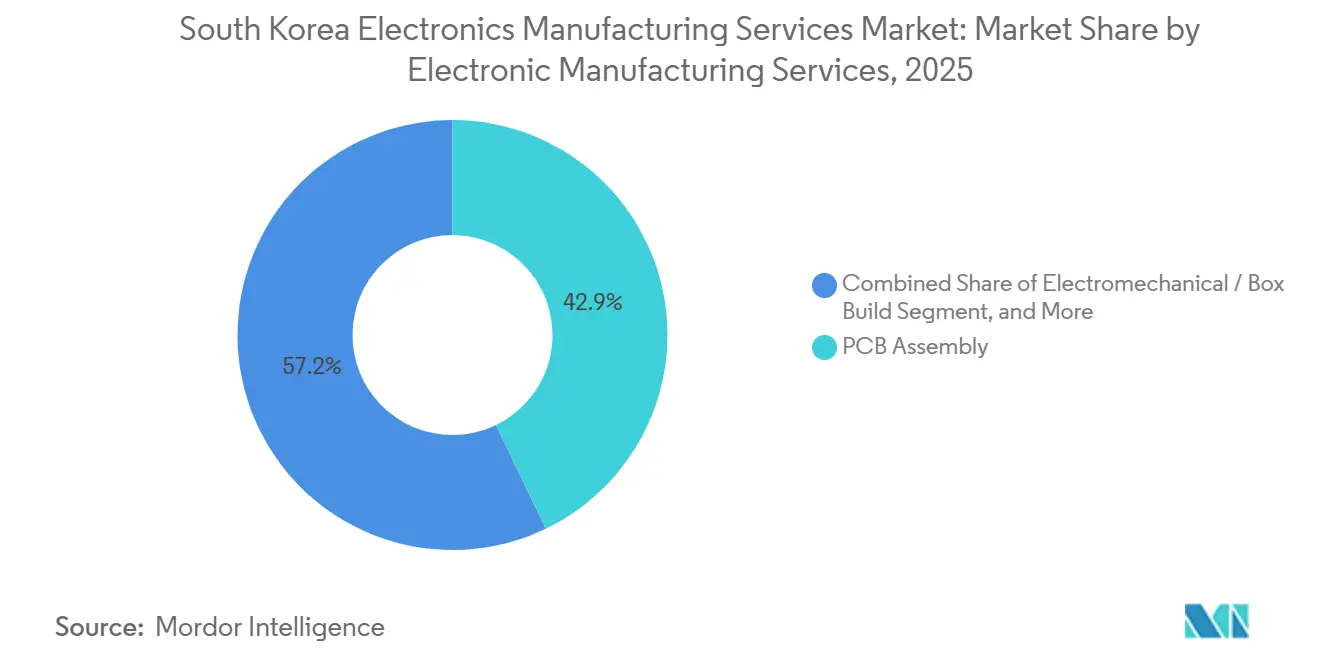

- By electronic manufacturing services, printed-circuit-board assembly led with 42.85% revenue share in 2025, whereas electromechanical and box-build services are advancing at a 7.54% CAGR through 2031.

- By business model, contract manufacturing accounted for 63.76% of the South Korea electronics manufacturing services market share in 2025, while hybrid / turnkey / other business model arrangements are expanding at a 7.62% CAGR to 2031.

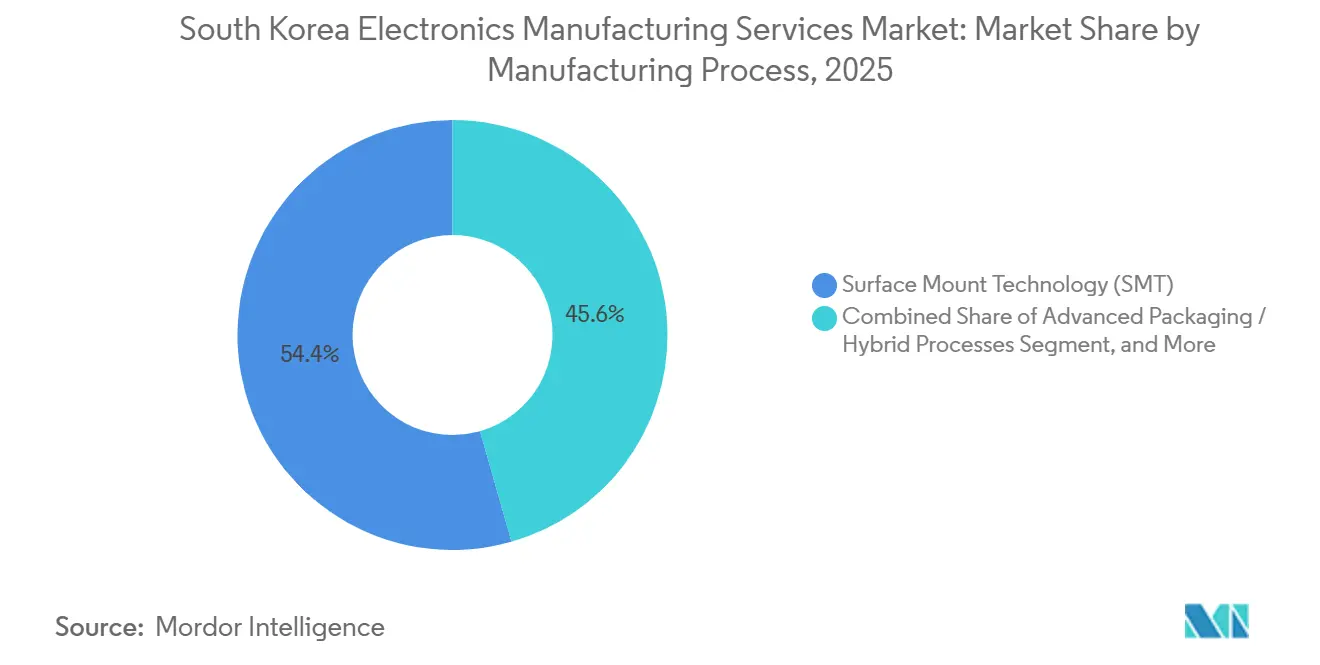

- By manufacturing process, surface-mount technology held a 54.43% share of the South Korea electronics manufacturing services market size in 2025, and advanced packaging / hybrid processes is growing at 7.88% through 2031.

- By end user, consumer electronics retained 38.68% share in 2025, and automotive is posting the fastest 7.18% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

National developments in South korea connect differently with activity unfolding across other parts of the world. In the global electronics manufacturing services market coverage, Mordor Intelligence integrates these into a single analytical framework.

South Korea Electronics Manufacturing Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| AI-Driven Demand for High-Bandwidth Memory and Advanced Packaging | +1.8% | National, spillover to broader APAC supply chains | Medium term (2-4 years) |

| Reshoring of Server-Board Assembly from China to Korea | +1.5% | Gyeonggi and Chungcheong provinces | Short term (≤ 2 years) |

| Government K-Chips Act Tax Incentives for System-Semiconductor ODMs | +1.3% | National | Medium term (2-4 years) |

| Increasing Outsourcing of EV-Power Electronics by Korean Automakers | +1.0% | Ulsan and Gwangju automotive clusters | Long term (≥ 4 years) |

| Expansion of Smart-Factory Adoption among Tier-2 EMS Providers | +0.8% | Gyeonggi and Incheon | Medium term (2-4 years) |

| Growth of Same-Day e-Commerce Logistics Requiring Modular EMS for IoT Devices | +0.6% | Seoul and Busan metropolitan areas | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

AI-Driven Demand for High-Bandwidth Memory and Advanced Packaging

Generative-AI clusters absorb huge volumes of HBM3E and HBM4 stacks, pushing Korean EMS firms into thermal-compression bonding, through-silicon-via alignment, and non-destructive X-ray inspection for 12- to 16-die packages. Assembly fees reach USD 4.20 per stack, five times the rate for legacy DRAM packaging, so value migrates upstream toward firms with advanced packaging lines. [1]Ministry of Trade, Industry and Energy, “Advanced Packaging Subsidy Details,” motie.go.kr Seoul has allocated KRW 6 trillion in capital subsidies for panel-level and wafer-level equipment, widening the domestic capability gap over Chinese OSAT rivals. Tier-2 specialists such as Nepes are already running 600 mm × 600 mm glass panels that cut die cost 35% and enable heterogeneous logic-and-memory integration. These moves let the South Korea electronics manufacturing services market capture workloads that previously flowed to Taiwan or Singapore.

Reshoring of Server-Board Assembly from China

U.S. export controls added in October 2024 triggered a shift of AI-server motherboards into Pyeongtaek and Incheon, shortening HBM logistics loops from 72 hours to 12 hours and saving Foxconn USD 18 million in inventory costs per year. [2]Asia Nikkei, “Foxconn Relocates AI-Server Boards,” asia.nikkei.com Flex followed with a USD 150 million clean room that satisfies U.S. compliance requirements and begins production in 2027. [3]Flex, “Incheon Server Board Facility Announcement,” investors.flex.com Layer-count jumps to 32 copper layers, pushing Daeduck Electronics and Korea Circuit to 95% utilization and stretching lead times to 16 weeks. Permits for two new substrate fabs were fast-tracked in Chungcheongnam-do, but the first output will not arrive until mid-2027. Until then, Korean EMS houses enjoy premium pricing for high-layer boards as hyperscale buyers avoid Chinese assemblers.

Government K-Chips Act Tax Incentives

Passed in February 2025, the K-Chips Act grants 25-30% tax credits to small- and medium-sized EMS investors and 15-20% to conglomerates that place new lines in Korea for at least 5 years. Accelerated three-year depreciation trims the effective cost of USD 12 million automated-test cells by roughly 35%, lowering the entry hurdle for Tier-2 shops. ODM registrations jumped 47% year over year in 2025, with nearly 70% coming from firms employing fewer than 500 people. Hanwha Systems already booked KRW 42 billion in credits for a Seongnam ASIC design center geared to automotive radar. The new incentives deepen the local design ecosystem and lock future production inside Korea’s borders.

Increasing Outsourcing of EV-Power Electronics

Hyundai and Kia will source 60% of power-electronics modules from domestic EMS partners by 2027, avoiding the USD 45 million capital outlay per silicon-carbide production cell. LG Innotek committed KRW 380 billion to three new inverter and charger lines capable of assembling 1.2 million units annually and meeting ISO 26262 ASIL-D. Samsung Electro-Mechanics added two Busan lines to chase a 25% share of Hyundai’s e-platforms by 2028. EMS providers now offer thermal simulation, EMC testing, and functional-safety validation services, which carry 18-22% margins versus 8-12% for board stuffing. These richer scopes raise overall profitability inside the South Korea electronics manufacturing services market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Tight High-End Substrate (FC-BGA) Supply Constraining PCB Assembly | -0.7% | Gyeonggi manufacturing belt | Short term (≤ 2 years) |

| Volatility in Memory-Chip Pricing Compressing EMS Margins | -0.6% | National | Short term (≤ 2 years) |

| Shortage of Skilled SMT Operators Amid Aging Workforce | -0.4% | Legacy hubs in Gumi, Cheonan | Medium term (2-4 years) |

| Rising Electricity Tariffs for Clean-Room Lines | -0.3% | National | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Tight High-End Substrate Supply

Flip-chip BGA substrates with via densities finer than 150 µm remain undersupplied, keeping domestic fabs at 94-96% utilization and forcing Tier-2 EMS firms to decline hyperscale orders worth USD 420 million in annual revenue. Simmtech secured only 40% of its 2026 needs and paid a 22% premium, eroding gross margin by 140 basis points. Two Chungcheongnam-do fabs will add 240,000 m² per month, but volume output will not arrive until mid-2027. In the interim, EMS shops must import substrates from Japan at spot prices 30-35% above contract prices, squeezing working capital. The bottleneck caps near-term growth for AI-server board projects within the South Korea electronics manufacturing services market.

Volatility in Memory-Chip Pricing

DDR5 spot prices plunged 22% in early 2025, then rebounded 18% in Q3, leaving EMS contracts misaligned with weekly procurement costs. Aggregate write-downs totaled USD 340 million and cut the sector's gross margin from 11.2% to 9.4% over the past two quarters. Samsung Electronics and SK Hynix cut wafer starts by 12% in 2024, yet AI-server demand outpaced expectations, producing a shortage by September 2025. EMS buyers try to hedge through quarterly price reviews, but OEM contracts cap pass-through adjustments at 5%, leaving suppliers exposed. A proposed pooled-buying platform remains lightly adopted because firms fear sharing customer data, prolonging exposure to memory swings. [4]Korea Printed Circuit Association, “Q3 2025 Substrate Utilization Report,” kpca.or.kr

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Electronic Manufacturing Services: Box-Build Integration Edges Ahead

PCB assembly contributed 42.85% of 2025 revenue in the South Korea electronics manufacturing services market, yet the box-build segment is expanding at a 7.54% CAGR, lifting the overall South Korea electronics manufacturing services market size at the upper end of management forecasts. Electromechanical integration brings enclosure fabrication, cable harnessing, thermal interface application, and final test under one roof, creating a one-stop value proposition that protects margins from commodity swings. The shift also raises average selling prices because customers bundle design-for-manufacturability and failure-mode-effects-analysis services into the same purchase order.

Engineering, test, and development services ride the same wave. Samsung Electro-Mechanics reported a 34% surge in engineering revenue, largely from automotive clients seeking ISO 26262 validation. Rapid-prototyping cells, such as Partron’s 72-hour mixed-technology line, compress development cycles by up to three weeks, a critical advantage for EV platforms with sub-three-year lifespans. Even logistics services gain relevance because same-day e-commerce channels require buffer stock and four-hour configure-to-order fulfillment windows.

By Business Model: Hybrid Turnkey Solutions Gain Momentum

Contract manufacturing maintained 63.76% share in 2025, but hybrid turnkey projects now deliver the highest 7.62% CAGR, improving the South Korea electronics manufacturing services market share captured by suppliers who can absorb inventory risk. Gross margins on turnkey agreements reached 14.2% versus 8.4% for pure build-to-print work, thanks to bundled component sourcing and after-sales services. Automotive electronics leads adoption, with Hanwha Systems signing KRW 180 billion in five-year agreements that transition to licensing after a two-year exclusivity period.

Turnkey preference is spreading to server-board programs as hyperscale operators lock in capacity against export-control shocks. Korea Electronics Association data show turnkey contracts represented 28% of new EMS awards in 2025, up nine percentage points year-on-year. These arrangements embed design ownership inside the South Korea electronics manufacturing services market, further insulating it from low-cost overseas alternatives.

By Manufacturing Process: Advanced Packaging Moves Up The Value Chain

Surface-mount technology still held 54.43% of 2025 process revenue, yet advanced packaging is racing ahead at a 7.88% CAGR and is crucial to the projected South Korea electronics manufacturing services market size. Chiplet architectures demand fan-out panel-level, through-silicon via, and micro-bump techniques that few offshore competitors can match at scale. SK Hynix’s HBM4 launch requires sub-micron alignment and 5-micron void detection capability, both available at select Korean EMS sites.

Nepes invested KRW 150 billion to install 600 mm glass-panel equipment that lowers per-die cost by 35%, allowing heterogeneous system-in-package builds for 5G smartphones. Hybrid process demand grows in automotive sensor fusion boards that mix legacy microcontrollers with next-generation AI processors, illustrating how the South Korea electronics manufacturing services market blends mature and emerging techniques to maintain competitiveness.

By End User: Automotive Electronics Pulls Ahead

Consumer electronics accounted for 38.68% of 2025 revenue, but automotive electronics is forecast to grow at a 7.18% CAGR, steering incremental growth in the South Korea electronics manufacturing services market through 2031. Hyundai and Kia’s outsourcing of traction inverters, on-board chargers, and DC-DC converters sparks large capital commitments from LG Innotek and Samsung Electro-Mechanics. Each new EV platform brings modular sub-assemblies that must meet ISO 26262 ASIL-D, thereby commanding higher unit pricing.

Industrial automation runs close behind as Korean factories adopt collaborative robots, with shipments up 41% year-over-year. Medical electronics also expands at 7.3%, leveraging ISO 13485 certifications to court North American OEMs. These diversified verticals enhance the resilience of the South Korea electronics manufacturing services market during consumer device downcycles.

Geography Analysis

Greater Seoul remains the epicenter of the South Korea EMS market, accounting for a plurality of advanced-packaging capacity and hosting co-located memory fabs that shorten logistics loops. The Gyeonggi cluster benefits from Samsung’s Pyeongtaek megafab and Foxconn’s new server-board line, creating a regional workforce fluent in surface-mount and fan-out panel-level techniques. Neighboring Incheon attracts Flex and multiple Tier-2 providers that specialize in high-layer-count PCBs, reinforcing the supply chain's depth.

Chungcheongnam-do is emerging as a substrate hub after environmental permits were fast-tracked for two FC-BGA plants, which together will add 240,000 m² of monthly capacity by mid-2027. This move aims to alleviate the substrate bottleneck constraining the South Korean electronics manufacturing services market. The region also offers lower land costs and proximity to ports, enabling efficient export of high-value PCB assemblies to Japan and the United States.

Ulsan and Gwangju anchor automotive electronics expansion. Hyundai’s and Kia’s plants there spur EMS investment in inverter and battery-management subsystems. Provincial governments provide payroll subsidies for ISO 26262 training, mitigating the skilled-labor shortfall flagged by the Korea Labor Institute. Collectively, these geographic dynamics disperse risk and scale across the South Korea electronics manufacturing services market, ensuring capacity is not overly concentrated in a single province.

Mordor Intelligence's coverage of the electronics manufacturing services market extends across other regions including Europe, Asia, and North America, while country-specific intelligence is also available for Malaysia, China, France, United States, Mexico, and Taiwan, each offering a view on the jurisdiction-level dynamics as applicable.

Competitive Landscape

The market is moderately concentrated. Conglomerate affiliates channel internal semiconductor and display know-how into turnkey automotive and AI-chip modules, while pure-play EMS specialists adopt smart-factory automation that cuts touch labor 40% and first-pass escapes 60%. Patent filings for chiplet interconnects reached 47 in 2025 at Samsung Electro-Mechanics, underscoring the technology arms race.

Emerging disruptors such as Nepes and Korea Circuit leverage 600 mm glass-panel packaging to undercut offshore OSAT pricing without sacrificing yield. Their advantage lies in combining substrate fabrication and final assembly under one roof, eliminating cross-border freight costs. Global players Jabil, Flex, and Foxconn expand Korean engineering centers, but their reliance on build-to-print models limits design fee capture versus domestic turnkey specialists.

Medical-device and same-day e-commerce niches offer white-space opportunities. Providers holding ISO 13485 certification can win North American contracts looking to diversify away from China. Urban micro-factories in Seoul support four-hour IoT device turnaround, tapping the surge in rapid-fulfillment retail. These differentiated strategies collectively enhance the resilience and global standing of the South Korea electronics manufacturing services market.

South Korea Electronics Manufacturing Services Industry Leaders

Samsung Electro-Mechanics Co., Ltd.

LG Innotek Co., Ltd.

Hanwha Systems Co., Ltd.

Hansol Technics Co., Ltd.

Partron Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Samsung Electro-Mechanics committed KRW 420 billion to two new advanced-packaging lines in Busan targeting 180 million units annual capacity by 2028.

- December 2025: LG Innotek secured a five-year KRW 680 billion supply deal with Hyundai Motor Group for on-board chargers and DC-DC converters starting Q2 2026.

- November 2025: Hanwha Systems acquired 60% of KC EMS for KRW 95 billion to bolster ISO 26262 automotive capacity.

- September 2025: SK Hynix began HBM4 mass production, with local EMS houses providing die-to-wafer bonding.

South Korea Electronics Manufacturing Services Market Report Scope

The Electronics Manufacturing Services (EMS) Market is the industry that provides a range of services, including the design, assembly, production, and testing of electronic components and products for original equipment manufacturers (OEMs). These services enable OEMs to outsource manufacturing processes, allowing them to focus on core competencies such as research and development and marketing.

The South Korea Electronics Manufacturing Services (EMS) Market Report is Segmented by Service Type (Electronic Manufacturing Services [PCB Assembly, Electromechanical Assembly/Box Build, Prototyping, Other Electronic Manufacturing Services], Engineering Services, Test and Development Implementation, Logistics Services, and Other Service Types), Business Model (Contract Manufacturing, Original Design Manufacturing, and Hybrid / Turnkey / Other Business Models), Manufacturing Process (Surface Mount Technology, Through-Hole Technology, and Advanced Packaging / Hybrid Processes), and End-User (Mobile Devices, Consumer Electronics, Computer, Industrial, Automotive, Communication, Lighting, Medical, and Other End-Users). The Market Forecasts are Provided in Terms of Value (USD).

| Electronic Manufacturing Services | PCB Assembly |

| Electromechanical Assembly/Box Build | |

| Prototyping | |

| Other Electronic Manufacturing Services | |

| Engineering Services | |

| Test and Development Implementation | |

| Logistics Services | |

| Other Service Types |

| Contract Manufacturing (CM) |

| Original Design Manufacturing (ODM) |

| Hybrid / Turnkey / Other Business Models |

| Surface Mount Technology (SMT) |

| Through-Hole Technology (THT) |

| Advanced Packaging / Hybrid Processes |

| Mobile Devices (Smartphones and Tablets) |

| Consumer Electronics |

| Computer (PCs/Desktop/Laptops) |

| Industrial |

| Automotive |

| Communication |

| Lighting |

| Medical |

| Other End-Users |

| By Service Type | Electronic Manufacturing Services | PCB Assembly |

| Electromechanical Assembly/Box Build | ||

| Prototyping | ||

| Other Electronic Manufacturing Services | ||

| Engineering Services | ||

| Test and Development Implementation | ||

| Logistics Services | ||

| Other Service Types | ||

| By Business Model | Contract Manufacturing (CM) | |

| Original Design Manufacturing (ODM) | ||

| Hybrid / Turnkey / Other Business Models | ||

| By Manufacturing Process | Surface Mount Technology (SMT) | |

| Through-Hole Technology (THT) | ||

| Advanced Packaging / Hybrid Processes | ||

| By End-User | Mobile Devices (Smartphones and Tablets) | |

| Consumer Electronics | ||

| Computer (PCs/Desktop/Laptops) | ||

| Industrial | ||

| Automotive | ||

| Communication | ||

| Lighting | ||

| Medical | ||

| Other End-Users |

Key Questions Answered in the Report

What is the projected value of the South Korea electronics manufacturing services market by 2031?

Forecasts place the market at USD 45.46 billion in 2031, equating to a 6.65% CAGR from 2026.

Which service type is growing fastest within South Korean EMS?

Electromechanical and box-build integration is advancing at a 7.54% CAGR, outpacing traditional PCB assembly.

How are government incentives shaping the sector?

The K-Chips Act provides up to 30% tax credits and accelerated depreciation, driving a 47% rise in ODM project filings in 2025.

Why is automotive electronics important for Korean EMS providers?

Hyundai and Kia will outsource 60% of power-electronics modules by 2027, fueling a 7.18% CAGR for automotive electronics assembly.

What constraint most threatens near-term EMS capacity?

Persistent tight supply of high-end FC-BGA substrates, with domestic fabs running at 95% utilization, currently limits server-board output.

How are Korean EMS firms mitigating skilled-labor shortages?

Providers deploy collaborative robots and machine-vision systems that replace manual tasks and cut touch labor by 40%.

Page last updated on: