South Korea Customer Data Platform Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

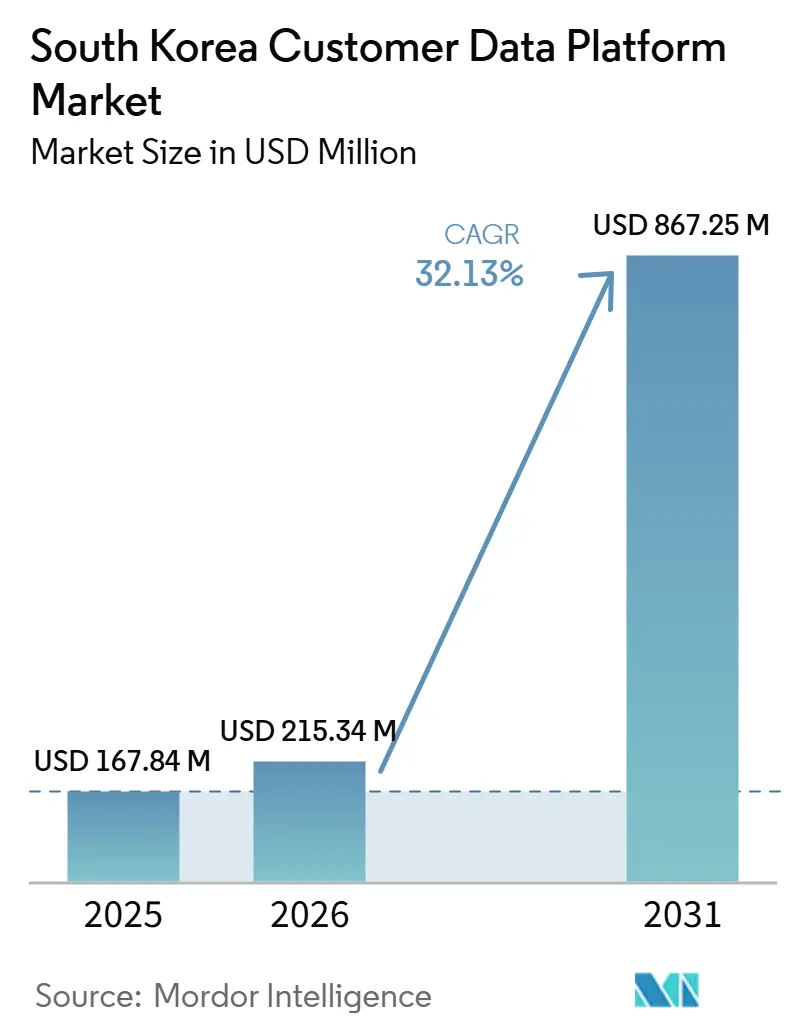

| Base Year Market Size (2025) | USD 167.84 Million |

| Market Size (2026) | USD 215.34 Million |

| Market Size (2031) | USD 867.25 Million |

| Growth Rate (2026 - 2031) | 32.13% CAGR |

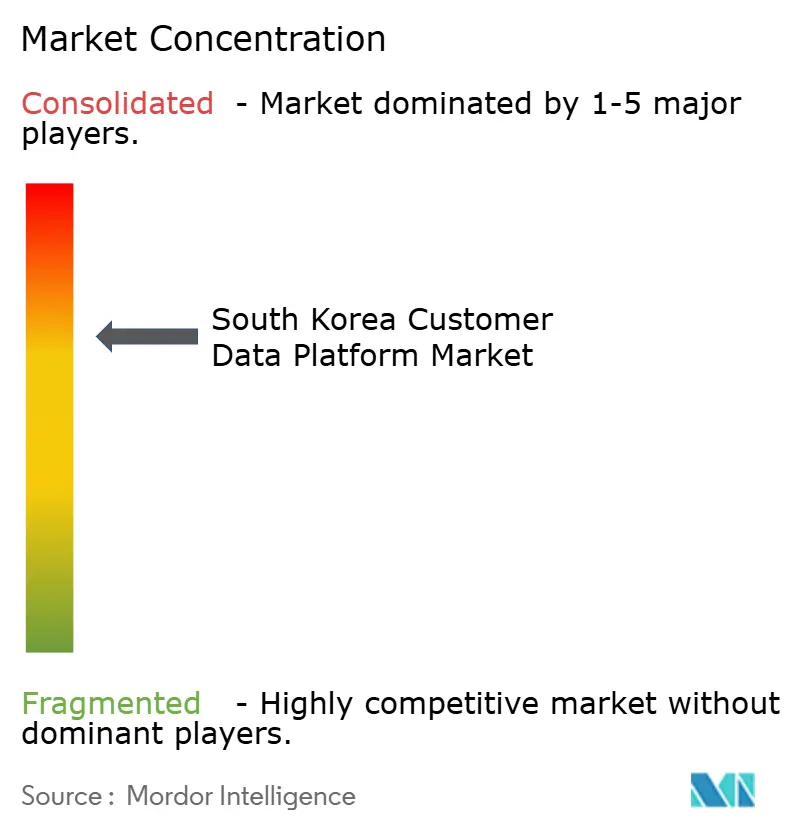

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South Korea Customer Data Platform Market Analysis by Mordor Intelligence

The South Korea customer data platform market size was valued at USD 167.84 million in 2025 and estimated to grow from USD 215.34 million in 2026 to reach USD 867.25 million by 2031, at a CAGR of 32.13% during the forecast period (2026-2031). The South Korea customer data platform market is being lifted by strong digital engagement, widespread smartphone usage, and a commerce system built around high-frequency mobile interactions. The shift away from reliance on third-party data is making first-party customer data more valuable, prompting enterprises to invest in unified profile management, consent management, and faster channel activation. The South Korea customer data platform market is also moving into a more execution-focused phase, where buyers that already selected platforms are now spending more on integration, analytics, and managed services to turn those systems into measurable business tools. Competitive positioning increasingly depends on how well vendors support AI-driven identity resolution, Korean-language workflows, and integration with local enterprise systems. The opportunity remains strongest where real-time personalization, regulatory compliance, and domestic ecosystem connectivity must work together within a single customer data environment.

Key Report Takeaways

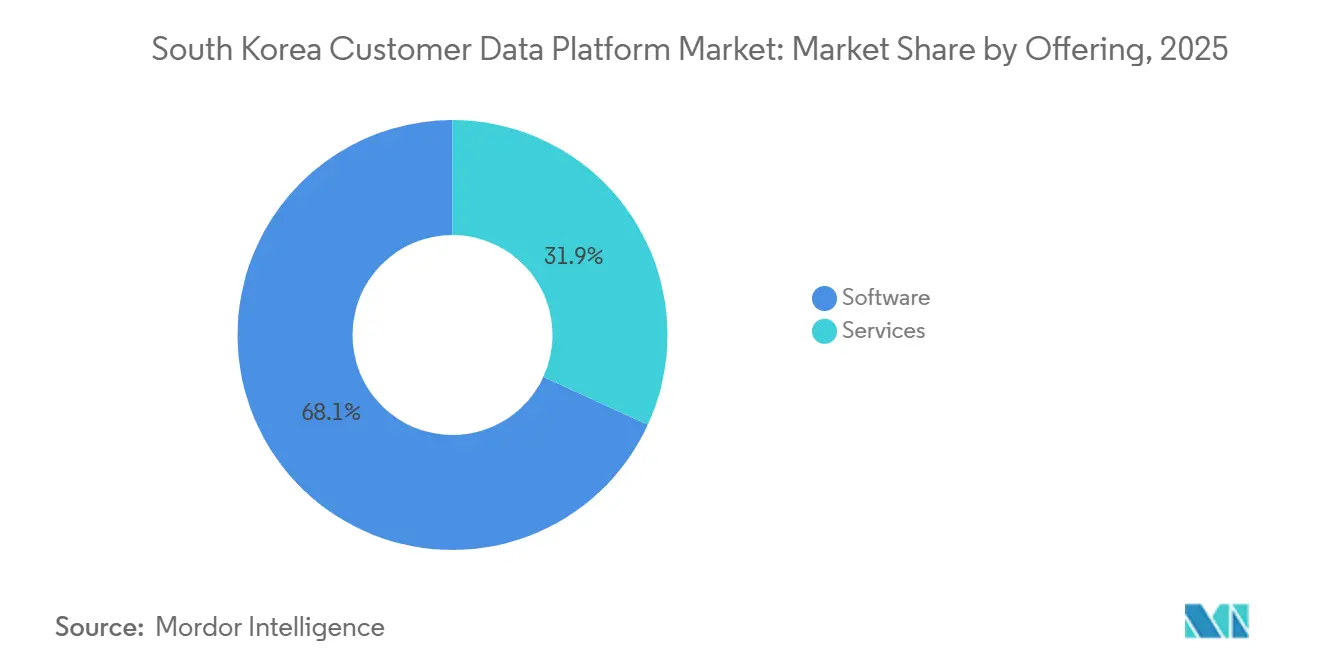

- By offering software led with a 68.14% of the South Korea customer data platform market share in 2025, while services are projected to expand at a 35.11% CAGR through 2031.

- By deployment mode, cloud held 66.31% of the South Korea customer data platform market share in 2025, while no faster-growing deployment sub-segment was provided in the input.

- By organization size, large enterprises accounted for 70.12% of the South Korea customer data platform market in 2025, while SMEs are projected to expand at a 34.85% CAGR through 2031.

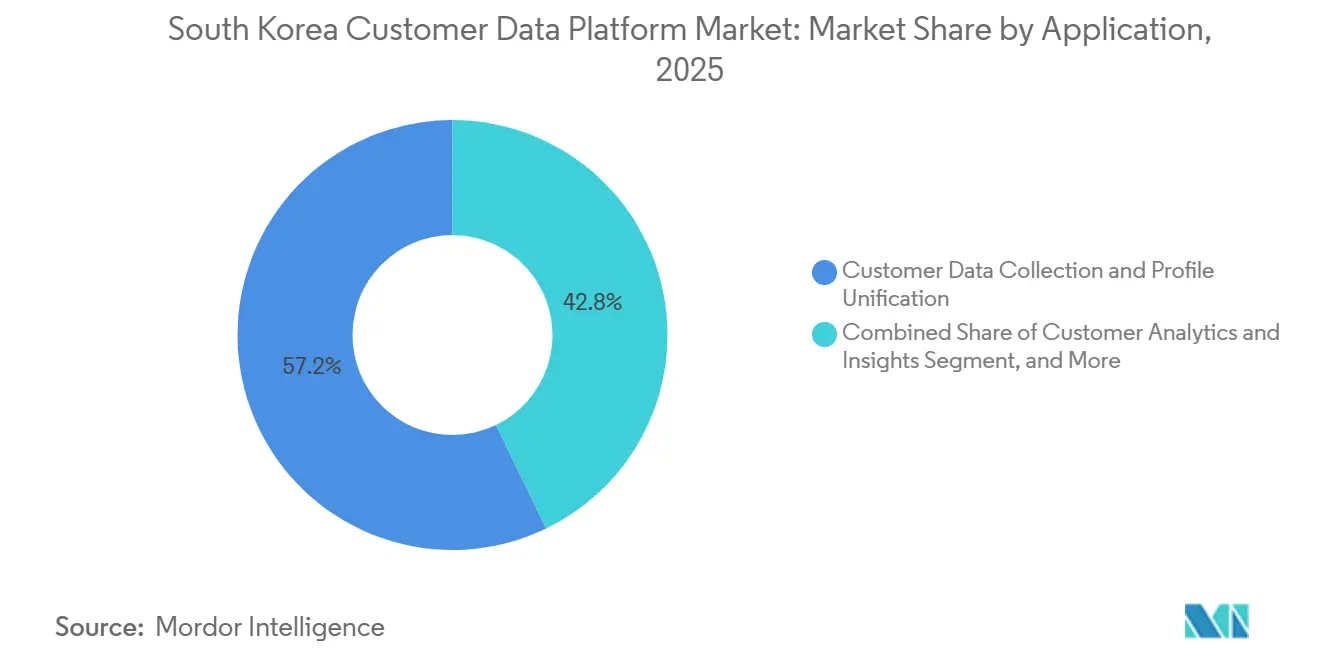

- By application, customer data collection and profile unification captured 57.18% share in 2025, while audience segmentation and personalization are projected to grow at a 34.05% CAGR through 2031.

- By end-user industry, retail and e-commerce held 30.59% of the South Korea customer data platform market share in 2025, while BFSI is projected to advance at a 33.68% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

South Korea Customer Data Platform Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| First-Party Data Unification for Omnichannel Personalization | +5.8% | South Korea, with spillover to broader APAC | Medium term (2-4 years) |

| Privacy-First Replacement of Third-Party Cookies | +4.2% | Global, with acute impact in South Korea given PIPA opt-in mandates | Short term (≤ 2 years) |

| AI-Driven Real-Time Identity Resolution | +6.5% | Global, South Korea early adopter via BFSI and retail | Medium term (2-4 years) |

| Composable CDP Adoption by Data Teams | +4.8% | APAC core markets, deepening in South Korea large-enterprise segment | Medium term (2-4 years) |

| Super-App and Commerce Ecosystem Integration in South Korea | +5.6% | South Korea-specific, limited direct spillover | Short term (≤ 2 years) |

| Data Warehouse-Native Activation to Reduce Data Movement Costs | +3.2% | Global, accelerating in data-mature South Korean conglomerates | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

AI-Driven Real-Time Identity Resolution

Real-time identity resolution is becoming central to the South Korea customer data platform market because enterprises want personalization systems to react while the customer interaction is still happening. Customer data tools are no longer expected to clean records in the background alone; they are now expected to support live decisioning across marketing and service workflows. Amperity introduced its Identity Resolution Agent in April 2025 to shorten the time required to unify fragmented customer records, raising the performance bar for the wider vendor group.[1]Amperity, “Amperity Unveils Industry's First Identity Resolution Agent,” Amperity, amperity.com This direction fits the South Korea customer data platform market well because local buyers in banking, retail, and telecom increasingly want AI-ready data layers rather than static marketing databases. Vendors that cannot resolve identity quickly and reliably are likely to lose relevance as enterprises connect customer data platforms more closely with automated decision engines.

First-Party Data Unification for Omnichannel Personalization

The South Korea customer data platform market is also being driven by the need to unify customer activity across mobile apps, websites, stores, loyalty systems, and messaging channels. Retailers are facing more fragmented behavior because the same buyer often moves between search, chat, storefront, and payment touchpoints before completing a purchase. NAVER said its AI-powered Plus Store app delivered daily purchase conversions that were more than 2 times higher than its existing shopping experience during the first quarter after launch, which shows the value of acting on unified behavioral data. In the South Korea customer data platform market, this keeps foundational profile building at the center of spending because enterprises need clean and connected records before they can scale personalization. It also strengthens demand for platforms that can combine CRM data, transaction histories, and event streams without slowing down activation.

Super-App and Commerce Ecosystem Integration in South Korea

The South Korea customer data platform market has a distinct local growth pattern because customer journeys are shaped by tightly connected digital ecosystems rather than isolated channels. Enterprise buyers want customer data systems that can fit into high-traffic environments, including those linked to messaging, search, shopping, and app-based commerce. This makes integration quality especially important because value depends on how quickly first-party signals can move from local touchpoints into usable profiles and campaign logic. The South Korea customer data platform market benefits from this structure because enterprises see unified customer data as a practical way to improve conversion, retention, and relevance inside dense digital ecosystems. The same structure also gives domestic and localized vendors a better chance to compete by enabling them to connect more easily with Korean enterprise systems and commerce workflows.

Composable CDP Adoption by Data Teams

Composable architecture is gaining ground in the South Korea customer data platform market because large enterprises want to keep customer data closer to their existing cloud data environments. Instead of duplicating data into separate packaged platforms, these buyers prefer modular tools that work with their established warehouse and analytics stacks. Tealium expanded into the AWS Singapore Region in March 2026 to support APAC customers that need regional data residency and low-latency orchestration, which aligns with this architecture shift. In the South Korea customer data platform market, this favors organizations that already have strong data engineering capacity and want tighter control over movement, storage, and governance. It also deepens the split between large enterprises that can adopt composable models and SMEs that still prefer packaged cloud products with lower setup demands.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Integration Complexity with Legacy Enterprise Stacks | -4.5% | South Korea and APAC enterprise segment broadly | Medium term (2-4 years) |

| Strict Personal Information Protection Act Compliance Burden | -3.8% | South Korea-specific | Short term (≤ 2 years) |

| Shortage of Reverse-ETL and Customer Identity Engineering Talent | -3.2% | South Korea, with partial spillover to APAC | Medium term (2-4 years) |

| Vendor Lock-In and Unclear ROI in Mid-Market Deployments | -2.8% | Global, pronounced in South Korea mid-market | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Integration Complexity with Legacy Enterprise Stacks

A major brake on the South Korea customer data platform market is the difficulty of connecting modern customer data tools with older enterprise systems. Many large Korean organizations still manage customer records across long-standing ERP, CRM, loyalty, and subsidiary-level databases that were not built for real-time interoperability. This can stretch implementation timelines and raise the cost of turning a purchased platform into a working business system. The South Korea customer data platform market feels this most clearly in retail and financial services, where the most valuable customer data often sits inside older operational environments. Vendors that offer stronger connector libraries and more practical integration support are better placed to reduce this barrier and win complex enterprise projects.

Strict Personal Information Protection Act Compliance Burden

The South Korea customer data platform market also faces a direct regulatory constraint from the 2026 amendment to the Personal Information Protection Act, which strengthened penalties and sharpened accountability. The International Association of Privacy Professionals reported that the amendment tied serious violations to fines of up to 10% of total turnover and introduced personal supervisory liability for chief executive officers. In practice, this pushes procurement teams to examine consent propagation, audit trails, data handling controls, and purpose-limitation enforcement much more closely before approving a deployment. The South Korea customer data platform market is likely to see longer sales cycles because compliance design is now part of the buying decision, not a later operational issue. This burden is harder for mid-sized organizations to absorb because they usually have fewer internal privacy engineering resources than large conglomerates and banks.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering: Services Gain Speed While Software Holds the Spend Base

Software accounted for 68.14% of revenue in 2025, making it the largest segment of the South Korea customer data platform market. This lead reflects the stage of adoption, as many enterprises first prioritize platform licensing, core data unification, and customer profile management before expanding into more intensive support work. Software remains the base of current deployments because it houses the profile engine, segmentation logic, consent workflows, and orchestration features that buyers need to establish a working customer data layer. The South Korea customer data platform market still depends on software-led buying because enterprises need a stable system of record before they can widen activation and analytics use cases.

Services are projected to grow at a 35.11% CAGR through 2031, making them the fastest-growing segment. The South Korea customer data platform industry is moving into a phase where enterprises that bought platforms in earlier years now need integration, governance, and ongoing analytics support to extract value from those investments. That shift gives domestic IT service providers a stronger role because they are often better positioned to work with Korean enterprise stacks and local process requirements. In the South Korea customer data platform market, the faster rise of services suggests that implementation quality and operational support will increasingly shape vendor success, not just software functionality.

By Deployment Mode: Cloud Keeps its Structural Lead

Cloud captured 66.31% of the market by value in 2025, giving it the largest deployment position in the South Korea customer data platform market. This reflects enterprise preference for scalable infrastructure, subscription-style spending, and easier access to cloud-native upgrades and integrations. Cloud deployment is especially attractive for organizations that want to roll out faster across multiple customer-facing channels without committing to heavier on-site infrastructure. It also fits the current shape of the South Korea customer data platform market because many buyers want to connect customer data tools with other cloud-based analytics and activation systems.

On-premises and hybrid models still matter for regulated users, especially where internal controls, legacy environments, or data-handling requirements remain stricter. Even so, their combined position is under pressure as vendors expand compliance-aligned cloud options for APAC customers. Tealium’s March 2026 regional infrastructure expansion is one example of how vendors are addressing data governance expectations through regional deployment design. In the South Korea customer data platform market, cloud leadership is therefore not only a cost or flexibility story, it is also becoming a governance and localization story.

By Organization Size: Large Enterprises Lead, SMEs Accelerate

Large enterprises held 70.12% of the 2025 market, which shows that buyers still led the South Korea customer data platform market with the deepest budgets and the most complex customer data estates. Conglomerates, major retailers, and tier-1 financial institutions were the first to enter because they had the strongest need to reconcile large volumes of customer data across subsidiaries and channels. Their early buying activity established the enterprise base of the South Korea customer data platform market and helped anchor demand around full-suite platforms with broad integration scope. This also explains why implementation depth and governance controls remain so important in current vendor competition.

SMEs are forecast to grow at a 34.85% CAGR through 2031, making them the fastest-growing segment by organization size. Subscription-tier packaging and cloud delivery are lowering the barrier for smaller and mid-sized companies that want segmentation, messaging, and customer insight tools without building large internal data teams. LG CNS launched Clairvo in November 2025 with subscription-based and on-premise formats, signaling that vendors see real growth potential in more accessible deployment models. In the South Korea customer data platform market, this SME rise points to broader adoption beyond large enterprise identity programs and toward lighter personalization and workflow automation use cases.

By Application: Profile Unification Stays Dominant While Activation Expands

Customer data collection and profile unification held 57.18% of application revenue in 2025, making it the largest use case in the South Korea customer data platform market. That share shows the market is still grounded in foundational work, because enterprises must bring fragmented records together before downstream use cases can scale. It also means buyers continue to view a reliable unified profile as the basic requirement for consent management, segmentation, and journey orchestration. Customer data collection and profile unification, therefore, remained the clearest anchor of the South Korea customer data platform market in 2025.

Audience segmentation and personalization are projected to grow at a 34.05% CAGR through 2031, making it the fastest-growing application segment. This points to a shift from infrastructure build-out toward revenue-facing activation as more enterprises move beyond basic data consolidation. NAVER’s reported conversion gains from its AI-powered shopping experience support this direction by showing how better use of unified customer signals can influence buying behavior.[2]NAVER Corp., “Naver Plus Store AI Shopping Results,” NAVER Corp., navercorp.com In the South Korea customer data platform market, the next step after unification is increasingly clear, enterprises want to turn connected data into more targeted offers, faster journey responses, and better closed-loop measurement.

By End-User Industry: Retail Leads While BFSI Builds Fastest

Retail and e-commerce accounted for 30.59% of the South Korea customer data platform market size in 2025, which made it the largest end-user segment. This leadership comes from a highly competitive digital commerce environment where brands are under pressure to improve recommendation quality, repeat purchase rates, and cross-channel relevance. The South Korea customer data platform market is especially important to this segment because dense app-based shopping journeys and frequent digital interactions shape customer expectations. Retail buyers, therefore, continue to invest in systems that unify browsing, transaction, and loyalty activity into a single usable profile.

BFSI is projected to grow at a 33.68% CAGR through 2031, making it the fastest-growing vertical in the South Korea customer data platform market. Financial institutions are using customer data platforms to move away from broad product-push campaigns and toward behavior-triggered personalization across banking touchpoints. Obzen signed a March 2026 contract with BNK Kyongnam Bank to build an AI-based hyper-personalized marketing system using customer behavior and transaction data across mobile and internet banking channels. This reinforces that BFSI growth is tied not only to marketing demand, but also to the need for faster decisioning on top of regulated and high-value customer data.

Geography Analysis

The South Korea customer data platform market growth pattern is closely tied to the country’s digital infrastructure and enterprise technology base. South Korea combines near-universal mobile connectivity, high online commerce activity, and a strong preference for digital customer engagement, giving the market a large volume of first-party behavioral data to organize and activate. The South Korea customer data platform market also benefits from continued public support for advanced technologies that strengthen the broader data and AI environment. In 2025, the government allocated budgets for R&D across strategic technologies, including AI and semiconductors, supporting the wider ecosystem on which enterprise data platforms depend. Seoul remains the main commercial center because major enterprise headquarters, integration projects, and product development activity are concentrated there.

Within APAC, the South Korea customer data platform market stands out for its mix of regulatory maturity, commerce density, and readiness for AI-linked customer data use cases. Japan is also mature, but the enterprise environment is more fragmented due to architectural and deployment history. India and Southeast Asia are expanding quickly from smaller bases, yet they do not combine the same level of cloud depth, regulatory clarity, and buyer readiness seen in South Korea. This makes the South Korean customer data platform market an important localization target for global vendors seeking deeper traction across advanced APAC demand pockets.

The South Korea customer data platform market is also shaped by the concentration of digital commerce activity across the northern metropolitan corridor, especially Seoul, Incheon, and Suwon. Demand in these areas is driven by large retail groups, banks, and service providers that need to connect store, branch, web, app, and messaging interactions into one customer view. At the same time, national retail and financial networks extending into Busan, Daegu, and Gwangju are creating wider online-to-offline unification needs. As regional digital infrastructure and loyalty programs continue to develop, the South Korea customer data platform market is likely to see a more even spread of implementation activity across the country over time.

Competitive Landscape

The South Korea customer data platform market is moderately concentrated in large-enterprise deployments, but it remains more open in mid-market, industry-specific, and services-led opportunities. Global vendors such as Adobe, Salesforce, Tealium, Twilio, Segment, and Treasure AI compete alongside domestic players such as LG CNS and Obzen. The South Korea customer data platform market is no longer defined solely by data ingestion and segmentation breadth, as buyers now weigh AI-readiness, consent controls, localization, and integration quality much more heavily. This raises the value of vendors that can act as long-term customer data partners rather than standalone software suppliers. It also means competition is becoming more execution-focused as enterprises move from platform selection to full operational use.

Several strategic moves since 2025 show where vendor competition is heading. Adobe unveiled CX Enterprise in Seoul in April 2026, positioning Adobe Real-Time CDP as the core data layer for agentic customer experience orchestration across the customer lifecycle.[3]Adobe Korea, “Adobe Redefines Customer Experience in Agentic AI Era with CX Enterprise,” Adobe Korea, news.adobe.com Tealium’s expansion into the AWS Singapore Region in March 2026 was aimed at customers who need regional data residency and lower-latency orchestration in APAC. Treasure AI also rebranded in April 2026 to reflect a broader move from a traditional customer data platform position toward an agentic experience platform model.

Domestic positioning remains important because Korean buyers often value a strong fit with local enterprise systems and customer engagement channels. LG CNS used its November 2025 Clairvo launch to target both subscription and on-premise demand with an AI-led operating model designed to simplify campaign work. Obzen strengthened its presence in financial services through the BNK Kyongnam Bank contract announced in March 2026, further deepening its BFSI personalization capabilities. In the South Korean customer data platform market, vendors that combine deep local integration with stronger AI and governance features are likely to hold the clearest competitive advantage.

South Korea Customer Data Platform Industry Leaders

Adobe Inc.

Oracle Corporation

Salesforce, Inc.

Twilio Inc.

SAP SE

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2026: Madup, a South Korea-based AI marketing solution company, debuted on the KOSDAQ exchange with shares surging approximately 140% on its first trading day, attracting KRW 6.6 trillion (approximately USD 4.7 billion) in subscription deposits. The company plans to deploy IPO proceeds into AI infrastructure, engineering talent, and expansion into the North American market for its LEVER Xpert AI marketing platform.

- May 2026: Tealium launched Audience Discovery for Snowflake as a Snowflake Native App, enabling enterprise customers to build, govern, and activate customer audiences directly within their Snowflake environment without data movement or duplication. The solution eliminates data egress costs and accelerates time-to-insight for composable CDP deployments.

- April 2026: Adobe unveiled CX Enterprise in Seoul on April 21, 2026, an end-to-end agentic AI system that integrates Adobe Real-Time CDP with AI orchestration for full customer lifecycle management. The launch positioned Adobe's CDP as the core data layer for autonomous customer experience agents operating across acquisition, engagement, and loyalty stages.

- April 2026: Treasure Data officially rebranded as Treasure AI on April 20, 2026, repositioning its product from a Customer Data Platform to an Agentic Experience Platform. The rebrand reflects a product evolution in which AI agents continuously run the Customer Intelligence Loop, with all existing APIs and SDKs remaining backward-compatible for current enterprise customers.

South Korea Customer Data Platform Market Report Scope

The South Korea Customer Data Platform Market comprises software platforms and related services that enable organizations to collect, unify, manage, and activate customer data from multiple digital and offline touchpoints into centralized customer profiles. These platforms support audience segmentation, personalization, customer journey orchestration, analytics, and consent management, helping enterprises improve customer engagement and marketing effectiveness. Advanced digital adoption, growing investments in data-driven marketing, and increasing demand for personalized customer experiences across industries drive the market. Customer data platforms enable enterprises to optimize customer interactions, improve campaign performance, and derive actionable insights from customer data.

The South Korea Customer Data Platform Market Report is Segmented by Offering (Software, and Services), Deployment Mode (Cloud, On-Premises, and Hybrid), Organization Size (Large Enterprises, and Small and Medium Enterprises), Application (Customer Data Collection and Profile Unification, Audience Segmentation and Personalization, Marketing Campaign and Customer Journey Orchestration, Customer Analytics and Insights, Consent and Preference Management, and Other Applications), and End-User Industry (Retail and E-Commerce, Banking, Financial Services, and Insurance (BFSI), Healthcare and Life Sciences, Information Technology and Telecom, Media and Entertainment, Industrial Manufacturing, Government and Public Administration, and Other End-User Industries). The Market Forecasts are Provided in Terms of Value (USD).

| Software |

| Services |

| Cloud |

| On-Premises |

| Hybrid |

| Large Enterprises |

| Small and Medium Enterprises |

| Customer Data Collection and Profile Unification |

| Audience Segmentation and Personalization |

| Marketing Campaign and Customer Journey Orchestration |

| Customer Analytics and Insights |

| Consent and Preference Management |

| Other Applications |

| Retail and E-Commerce |

| Banking, Financial Services, and Insurance (BFSI) |

| Healthcare and Life Sciences |

| Information Technology and Telecom |

| Media and Entertainment |

| Industrial Manufacturing |

| Government and Public Administration |

| Other End-User Industries |

| By Offering | Software |

| Services | |

| By Deployment Mode | Cloud |

| On-Premises | |

| Hybrid | |

| By Organization Size | Large Enterprises |

| Small and Medium Enterprises | |

| By Application | Customer Data Collection and Profile Unification |

| Audience Segmentation and Personalization | |

| Marketing Campaign and Customer Journey Orchestration | |

| Customer Analytics and Insights | |

| Consent and Preference Management | |

| Other Applications | |

| By End-User Industry | Retail and E-Commerce |

| Banking, Financial Services, and Insurance (BFSI) | |

| Healthcare and Life Sciences | |

| Information Technology and Telecom | |

| Media and Entertainment | |

| Industrial Manufacturing | |

| Government and Public Administration | |

| Other End-User Industries |

Key Questions Answered in the Report

What is the South Korea customer data platform market size in 2026 and where is it headed by 2031?

The South Korea customer data platform market stands at USD 215.34 million in 2026 and is projected to reach USD 867.25 million by 2031, growing at a 32.13% CAGR.

Which offering segment is growing fastest in South Korea?

Services is the fastest-growing offering segment, with a projected CAGR of 35.11% through 2031, while software remained the largest revenue contributor in 2025.

Why are enterprises in South Korea investing more in customer data platforms?

Demand is being driven by first-party data unification, stronger privacy requirements, and the need to support AI-led personalization across commerce, banking, and digital service channels.

Which application area accounts for the largest share of spending?

Customer data collection and profile unification led with 57.18% share in 2025, showing that most buyers still prioritize building a reliable unified customer record first.

Which end-user group is adopting these platforms the fastest?

BFSI is the fastest-growing end-user segment, with a projected CAGR of 33.68% through 2031, as banks shift toward behavior-triggered and real-time personalized engagement.

How concentrated is the competitive environment in South Korea?

The market is concentrated in large-enterprise deployments, with leading global and domestic vendors holding strong positions, while smaller and sector-specific opportunities remain more open.

Page last updated on: