South Korea Beauty And Personal Care Products Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2020 - 2023 |

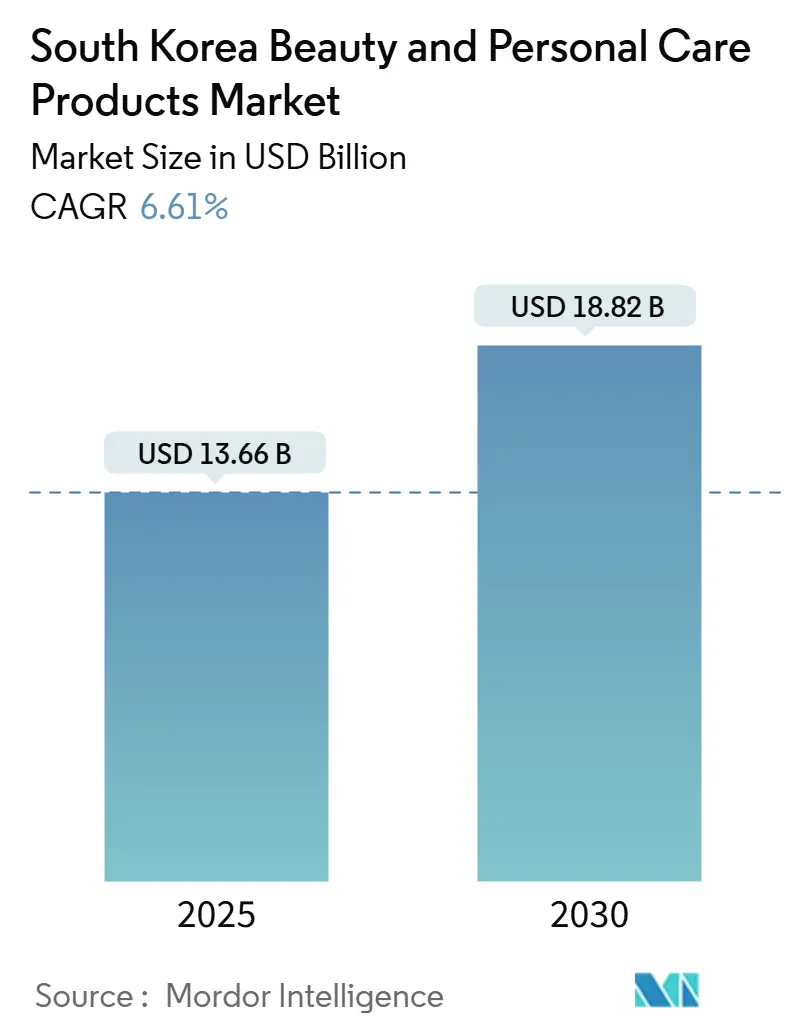

| Market Size (2025) | USD 13.66 Billion |

| Market Size (2030) | USD 18.82 Billion |

| Growth Rate (2025 - 2030) | 6.61% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

South Korea Beauty And Personal Care Products Market Analysis by Mordor Intelligence

The South Korea beauty and personal care products market size is estimated at USD 13.66 billion in 2025, and is expected to reach USD 18.82 billion by 2030, at a CAGR of 6.61% during the forecast period (2025-2030). South Korea has established itself as a global beauty innovator, becoming the fourth-largest cosmetics exporter by 2023, according to the International Trade Administration[1]Source: International Trade Organization, "South Korea Organic Beauty Market", trade.gov. This export strength has influenced domestic product development, with brands now developing formulations that comply with international regulations from the initial stages. Robust domestic R&D, digital retail leadership, and the global appeal of K-culture make South Korea a trend-setter whose product launches influence consumer routines from Tokyo to Los Angeles. Premiumisation gains ground as consumers accept higher prices in return for proven efficacy, while stricter ingredient rules motivate brands to reformulate and highlight safety credentials. Online retail already handles more than half of all category sales, with mobile-first shopping journeys, live commerce, and AI-driven recommendations turning every screen into a storefront. Competitive intensity remains moderate: heritage conglomerates still anchor the sector, yet health-and-beauty chain Olive Young and tech-enabled indies continually reset benchmarks for speed, data utilisation, and customer engagement.

Key Report Takeaways

- By product type, personal care products held 76.42% of the South Korean beauty and personal care market share in 2024 and are growing at a 6.95% CAGR through 2030.

- By category, mass products led with 51.63% share in 2024, while premium products posted the fastest 7.09% CAGR for 2025-2030.

- By ingredient, conventional/synthetic formulations accounted for a 71.32% share in 2024, whereas natural and organic products advanced at a 7.92% CAGR to 2030.

- By distribution channel, supermarkets/hypermarkets captured 38.63% of the South Korean beauty and personal care market size in 2024, and the online retail channel is forecast to expand at a 7.57% CAGR through 2030.

South Korea Beauty And Personal Care Products Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance (Key Provinces / Metro Cities) | Impact Timeline |

|---|---|---|---|

| Rising inclination towards natural and organic formulations | +1.2% | Seoul-Gyeonggi Capital Area; Jeju (eco-tourism retail corridors) | Medium term (2-4 years) |

| Increasing adoption of anti-aging/slow-aging solutions | +1.8% | Seoul, Busan, Daegu (high share of 60 + residents with premium spending power) | Long term (≥ 4 years) |

| Growing influence of social media and digital technology | +1.5% | Nationwide, strongest in Seoul, Busan, Incheon (highest smartphone and 5G penetration) | Short term (≤ 2 years) |

| Technological advancements and innovation | +1.0% | Pangyo Tech Valley (Gyeonggi-do), Osong Bio-cluster (Chungcheongbuk-do), Daejeon | Medium term (2-4 years) |

| Male grooming trends drive market demand | +0.8% | Seoul, Incheon, Gyeonggi urban belts; Gwangju youth districts | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Inclination Towards Natural and Organic Formulations

Consumer preference shifts toward natural and organic formulations reflect heightened safety consciousness and environmental awareness following the COVID-19 pandemic. The Ministry of Food and Drug Safety has set rigorous standards: mandating over 95% natural raw materials for product certification and requiring more than 10% organic ingredients for organic classification in January 2025. With a focus on ingredients, functionality, and certification, consumers are driving the market, bolstered by government initiatives promoting technology in bespoke cosmetics and personalized skin diagnostics. South Korea's regulatory framework not only surpasses U.S. standards, with its banned ingredient list, but also aligns closely with EU regulations, shaping global cosmetic formulations and bolstering consumer trust. As the clean beauty movement gains momentum, companies are prioritizing transparency in formulations and adopting sustainable practices in sourcing, manufacturing, and packaging. Meanwhile, advanced ingredient science is honing in on actives like Centella Asiatica, Niacinamide, and Mugwort, each delivering distinct benefits and adhering to stringent natural product regulations.

Increasing Adoption of Anti-Aging/Slow-Aging Solutions

Demographic shifts drive sustained demand for anti-aging solutions, with elderly consumers increasing cosmetics spending. According to the Ministry of the Interior and Safety (South Korea) data from 2024, the population aged 65 and older in South Korea was 10.26 million [2]Source: StatCounter Global Stats Data, " Social Media Stats in South Korea", gs.statcounter.com. Through open innovation strategies, the cosmeceutical market is swiftly addressing high R&D costs and navigating intricate value chains. With backing from the government and strides in technology, the market's growth potential is further amplified. Amorepacific's 'Concentrated Ginseng Rejuvenating' line, a testament to 60 years of ginseng expertise in July 2024, showcases premium anti-aging innovation. Infused with cutting-edge ingredients like GinsenomicsTM and Ginseng PeptideTM, it adeptly targets various signs of aging, including wrinkles, loss of elasticity, and dullness. Meanwhile, breakthroughs in gene regulation are reshaping anti-aging methodologies. Bioactive materials that adjust wrinkle-related genes are proving to be more effective than conventional retinol, all while sidestepping skin irritation issues. These advancements highlight the growing consumer demand for safer, more effective cosmeceutical solutions, driving further research and development in the market.

Growing Influence of Social Media and Impact of Digital Technology

Digital transformation accelerates through mobile commerce dominance, with transactions soaring via e-commerce, according to the International Trade Administration. Social media platforms drive ingredient-focused consumption trends, as the "Know-smetics" phenomenon emphasizes consumer knowledge of formulation components in product selection decisions. Also, Korean Wave cultural influence correlates directly with cosmetics export performance, with the trend for 'Korean drama' serving as a proxy for cultural trade impact across ASEAN markets. According to the StatCounter Global Stats data from 2025, 14.65% of the population in South Korea Used Facebook, and 3.21% used Instagram [3]Source: Ministry of the Interior and Safety (South Korea), "Population aged 65 years and older in South Korea", mois.go.kr. Beauty platforms like Hwahae expand internationally with English and Japanese versions, supporting K-beauty brands in global markets while providing ingredient-centered consumption data to manufacturers and consumers. Live commerce emerges as a significant distribution method, particularly among the MZ generation who prefer engaging and interactive shopping experiences during pandemic-driven restrictions on face-to-face interactions.

Technological Advancements and Innovation

Korean firms lead the charge in AI-driven product personalization, unveiling systems that match foundation shades by stimulating deeper skin layers uniformly. These innovations are transforming the beauty industry by offering highly accurate and tailored solutions for diverse skin tones. In collaboration with Korean startup NanoEnTek, L'Oréal introduced the Cell BioPrint device in January 2025. This portable lab-on-chip technology not only gauges biological age but also measures skin's responsiveness to ingredients, marking a significant leap in consumer skin intelligence. The device's compact design and advanced capabilities make it accessible for both professional and personal use, further enhancing its appeal. Meanwhile, advancements in gene regulation research are refining anti-aging formulations. By using bioactive materials to modulate EDAR and BNC2 gene expressions, researchers have achieved a notable wrinkle reduction, surpassing traditional retinol methods, all without the associated skin irritation. These breakthroughs are setting new benchmarks in the development of effective and gentle skincare solutions.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance (Key Provinces/Metro Cities) | Impact Timeline |

|---|---|---|---|

| Aging population and changing demographics | -0.8% | Jeollanam-do, Gyeongsangbuk-do, Gangwon-do (highest elderly ratios) | Long term (≥ 4 years) |

| Stringent regulatory requirements | -1.2% | Nationwide; compliance hubs in Osong (MFDS), Seoul, Gyeonggi manufacturing clusters | Medium term (2-4 years) |

| Consumer skepticism toward overhyped claims | -0.6% | Seoul-Gyeonggi (largest ingredient-tracking app usage), Busan | Short term (≤ 2 years) |

| Market saturation and intense competition | -1.0% | Retail-dense Seoul, Busan, Daegu metropolitan areas | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Consumer Skepticism Toward Overhyped Claims

South Korean shoppers now scrutinize product promises more closely, a shift fueled by ingredient-disclosure apps and the “Know-smetics” movement that encourages users to verify formulations before purchase. South Korea's Ministry of Food and Drug Safety reinforces this vigilance by banning PABA (para-aminobenzoic acid)-containing cosmetics and expanding the list of prohibited substances to 1,040, signaling zero tolerance for exaggerated efficacy that compromises safety. Retailers respond by demanding third-party test reports, while brands highlight clinically proven results rather than sensational marketing language to secure shelf space. Live-commerce hosts risk backlash if claims sound inflated, prompting platforms to tighten content guidelines and require real-time fact checks during broadcasts. As a result, even premium launches must publish transparent data on active concentrations and trial methodologies to win trust, tempering short-term sales spikes but enhancing long-term brand credibility.

Intense Competition Hinders Growth

Competitive intensity escalates through retail channel disruption. For instance, in 2023, CJ Olive Young's revenue surged to USD 2.85 billion, marking a 39% growth and eclipsing traditional giants Amorepacific and LG Household & Health Care for the first time. The health and beauty store market has become highly concentrated, with a few established players occupying a larger share. International expansion creates additional competitive pressure, as Korean cosmetics achieve top import rankings in the United States and Japan, forcing domestic players to compete globally while defending home market positions. Meanwhile, competitors such as GS Retail's Lalavla and Lotte Shopping's Lops grapple with dwindling store counts and mounting financial losses. Korean cosmetics have clinched top import rankings in both the U.S. and Japan, amplifying competitive pressures. This international success compels domestic players to not only defend their home turf but also vie on the global stage. Domestically, rivals like Daiso and Coupang are intensifying price competition, appealing to value-driven consumers, while premium brands grapple with squeezed margins.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Personal Care Dominates with Skincare Innovation

Personal care products command 76.42% of the South Korean beauty market in 2024 and are projected to maintain leadership with a 6.95% CAGR through 2025-2030. Within this category, skincare continues to be the cornerstone of K-beauty's global reputation, with facial care products driving significant innovation in formulations and delivery systems. The segment's growth is fuelled by continuous product advancement, particularly in specialized treatments addressing specific skin concerns such as hyperpigmentation and sensitivity.

Korean brands have successfully leveraged their expertise in skincare to expand into adjacent categories, with hair care emerging as a promising growth vector. For instance, in November 2024, Cosmecca Korea launched a range of its new skincare innovations. The products include 'Micro Hy-Balance Glow Cushion' and 'Pearless Radiant Boosting Serum'. The segment's evolution reflects a holistic approach to beauty, with increasing emphasis on the interconnection between skincare, haircare, and overall wellness, as evidenced by the rise of scalp-focused treatments that apply skincare principles to hair health.

By Category: Premium Segment Accelerates with Luxury Positioning

The mass segment holds 51.63% of the market in 2024, and the premium segment holds the fastest-growing segment at 7.09% CAGR from 2025-2030. This accelerated growth reflects a strategic upmarket shift by Korean brands seeking to enhance margins and global competitiveness. Mass products maintain market leadership through accessibility and functional effectiveness, supported by health and beauty store expansion reaching significant market value. CJ Olive Young's dominance in mass distribution, commanding a significant market share, enables smaller brands to access consumers while providing variety and convenience.

Premium positioning is increasingly defined by exclusive ingredients, advanced technology integration, and elevated packaging design rather than traditional luxury markers. Brands like Sulwhasoo and Dr. Jart+ have successfully established global premium positioning through rapid research and development cycles and sophisticated marketing narratives that emphasize cultural heritage and scientific innovation. The premium segment's expansion is further supported by rising disposable incomes and growing consumer willingness to invest in high-performance beauty products with demonstrable efficacy.

By Ingredient Type: Natural and Organic Formulations Lead Innovation

The natural and organic segment is growing at a 7.92% CAGR during 2025-2030, and conventional/synthetic holds the largest segment at 71.32% share. This growth stems from increased consumer focus on ingredient safety and environmental concerns, supported by the Korean government's implementation of natural and organic cosmetics standards. Korean manufacturers have developed extensive product lines utilizing local botanical ingredients, particularly Centella asiatica and ginseng derivatives, which clinical studies have shown to possess significant anti-aging benefits.

Companies are increasingly adopting transparent supply chains and environmentally conscious packaging methods, aligning with clean beauty principles and consumer demands for sustainability. Korean brands have established a strong market position through their comprehensive expertise in botanical extracts and fermentation technologies, enabling them to create innovative products that meet global consumer preferences for natural formulations. The integration of traditional herbal knowledge with modern manufacturing processes has allowed these companies to develop unique product offerings that combine efficacy with natural ingredients.

By Distribution Channel: Online Retail Reshapes Consumer Engagement

Online retail channels dominate the South Korean market at a 7.57% CAGR through 2025-2030, outpacing all other distribution formats. The largest segment is held by supermarkets/hypermarkets at 38.63%. This channel's growth is fueled by South Korea's advanced digital infrastructure, with 74.4% of e-commerce transactions now occurring via mobile devices, according to International Trade Administration data from 2023. Live commerce emerges as a significant distribution innovation, particularly among the MZ generation, who prefer engaging and interactive shopping experiences. The online beauty landscape is characterized by sophisticated content integration, with brands leveraging livestreaming, virtual try-on technologies, and AI-powered product recommendations to enhance the digital shopping experience.

Other channels like health and beauty stores are growing as consumer preferences shift toward convenience and variety offered these store formats. Olive Young, South Korea's leading health and beauty retailer, has implemented an omnichannel strategy that bridges online convenience with offline experiential elements. The shift toward online distribution has democratized market access, enabling smaller, innovative brands to gain visibility without extensive retail networks, while simultaneously creating new challenges in differentiation and customer loyalty in an increasingly crowded digital marketplace.

Competitive Landscape

The market shows moderate concentration with key players including Beiersdorf AG, L'Oreal S.A., Estée Lauder Companies Inc., Procter & Gamble Company, Unilever, among others. International companies strengthen their market positions through local partnerships, as demonstrated by L'Oréal's acquisition of Mibelle Group's South Korean division in February 2025. This acquisition highlights the importance that international companies place on domestic manufacturing expertise to maintain rapid product development cycles. A group of emerging companies, typically backed by venture capital, grows through social commerce platforms, focusing on influencer partnerships rather than conventional advertising methods.

Technology has emerged as a key differentiator in the market. Companies integrate AI customization, augmented reality for shade matching, and IoT beauty devices, creating significant competitive advantages and increasing customer retention. The collaboration between Samsung and Amorepacific on MicroLED mirror development demonstrates how consumer electronics companies are expanding into the beauty technology segment. This technological shift has influenced startup strategies, with new companies presenting both cosmetic formulations and sensor technologies to investors, combining elements of financial technology and cosmeceutical development.

Three strategic initiatives are pivotal, such as combining premium storytelling with scientifically validated efficacy, ensuring transparent supply chains through blockchain or QR traceability, and providing an omnichannel customer experience that integrates physical engagement with digital convenience. Companies that excel in these areas enhance customer loyalty and pricing power, reinforcing their competitive position in South Korea's beauty and personal care market. As the industry evolves, these strategies not only cater to the changing preferences of consumers but also set benchmarks for competitors. With a growing emphasis on sustainability and authenticity, brands adopting these initiatives are poised to lead the market in the coming years.

South Korea Beauty And Personal Care Products Industry Leaders

-

Beiersdorf AG

-

L'Oreal S.A.

-

Estée Lauder Companies Inc.

-

Procter & Gamble Company

-

Unilever PLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: LG Household and Health Co., Ltd, brand Dr. Groot, launched a new range of hair care products in South Korea to tackle hair loss problems. The products include hair shampoo, conditioners, and others. The products claim to improve the scalp environment and overall hair health.

- October 2024: In Seoul, Dolce & Gabbana unveiled its latest makeup collection, drawing in a star-studded crowd of top celebrities and key opinion leaders from the Asia-Pacific region. The highlight of the event was the introduction of the 'Rose Glow Cushion', a foundation tailored for the local market. This innovative product not only brightens and moisturizes but also boasts an impressive SPF 50 protection with PA++++. Promising 24-hour hydration, it ensures skin remains ever-bright.

- May 2024: LG Household and Healthcare Co. launched a range of body care products with niacinamide, polyhydroxy acids, peptides, and collagen. The products include body lotions, serums, firming cream, and others.

South Korea Beauty And Personal Care Products Market Report Scope

Beauty and personal care products encompass cosmetics, skincare, and hygiene items utilized for cleansing, aesthetic enhancement, and appearance improvement.

The South Korean beauty and personal care products market is segmented by product type, category, ingredients, and distribution channel. Based on product type, it is segmented into personal care products and cosmetics/makeup products. The personal care products are further segmented into hair care products, facial care products, bath and shower, oral care, men's grooming products, deodorants and antiperspirants, and perfumes and fragrances. Cosmetics/makeup products are further segmented into facial cosmetics, eye cosmetics, and lip and nail makeup products. Based on category, the market is segmented into premium products and mass products. By ingredient type, the market is segmented into natural & organic and conventional/synthetic. The market is segmented, based on distribution channels, into specialist retail stores, supermarkets/hypermarkets, online retail stores, and other distribution channels. The market sizing has been done in value terms in USD for all the abovementioned segments.

| Personal Care Products | Hair Care | Shampoo |

| Conditioner | ||

| Hair Colourant | ||

| Hair Styling Products | ||

| Others | ||

| Skin Care | Facial Care Products | |

| Body Care Products | ||

| Lip and Nail Care Products | ||

| Bath and Shower | Shower Gels | |

| Soaps | ||

| Others | ||

| Oral Care | Toothbrush | |

| Toothpaste | ||

| Mouthwashes and Rinses | ||

| Others | ||

| Men’s Grooming Products | ||

| Deodorants and Antiperspirants | ||

| Perfumes and Fragrances | ||

| Cosmetics/Make-up Products | Facial Cosmetics | |

| Eye Cosmetics | ||

| Lip and Nail Make-up Products | ||

| Premium Products |

| Mass Products |

| Natural and Organic |

| Conventional/Synthetic |

| Specialty Stores |

| Supermarkets/Hypermarkets |

| Online Retail Stores |

| Other Distribution Channels |

| By Product Type | Personal Care Products | Hair Care | Shampoo |

| Conditioner | |||

| Hair Colourant | |||

| Hair Styling Products | |||

| Others | |||

| Skin Care | Facial Care Products | ||

| Body Care Products | |||

| Lip and Nail Care Products | |||

| Bath and Shower | Shower Gels | ||

| Soaps | |||

| Others | |||

| Oral Care | Toothbrush | ||

| Toothpaste | |||

| Mouthwashes and Rinses | |||

| Others | |||

| Men’s Grooming Products | |||

| Deodorants and Antiperspirants | |||

| Perfumes and Fragrances | |||

| Cosmetics/Make-up Products | Facial Cosmetics | ||

| Eye Cosmetics | |||

| Lip and Nail Make-up Products | |||

| By Category | Premium Products | ||

| Mass Products | |||

| By Ingredient Type | Natural and Organic | ||

| Conventional/Synthetic | |||

| By Distribution Channel | Specialty Stores | ||

| Supermarkets/Hypermarkets | |||

| Online Retail Stores | |||

| Other Distribution Channels | |||

Key Questions Answered in the Report

What is the current size of the South Korean beauty and personal care market?

The market is valued at USD 13.66 billion in 2025 and is on track to hit USD 18.82 billion by 2030.

Which segment holds the largest share of spending?

Personal Care products dominate with a 76.42% share in 2024, driven by everyday skin and hair-care routines.

How fast is the premium segment growing?

Premium products are expanding at a 7.09% CAGR between 2025 and 2030, outpacing mass-market lines.

What regulatory changes should brands watch?

The MFDS has banned 1,040 ingredients and requires digital production records, making compliance a critical cost and timing factor.

Page last updated on: