South Korea AI Copilot Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

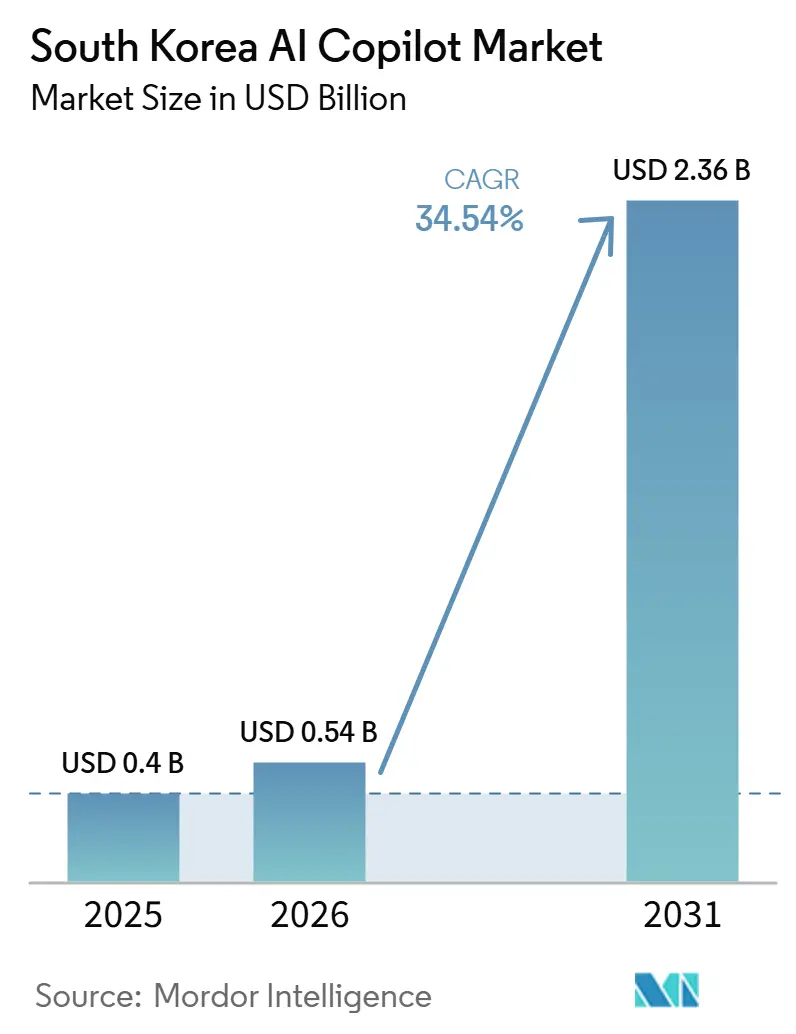

| Base Year Market Size (2025) | USD 0.4 Billion |

| Market Size (2026) | USD 0.54 Billion |

| Market Size (2031) | USD 2.36 Billion |

| Growth Rate (2026 - 2031) | 34.54% CAGR |

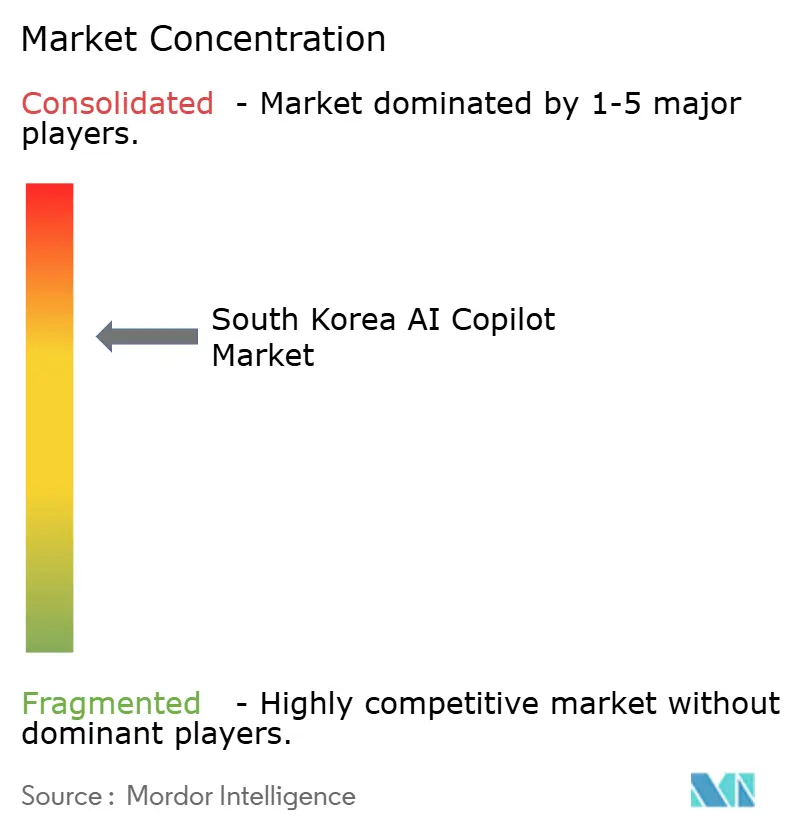

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South Korea AI Copilot Market Analysis by Mordor Intelligence

The South Korea AI copilot market size was valued at USD 0.40 billion in 2025 and estimated to grow from USD 0.54 billion in 2026 to reach USD 2.36 billion by 2031, at a CAGR of 34.54% during the forecast period (2026-2031). Growth is supported by strong enterprise readiness, as South Korea has moved faster than most countries from testing generative AI to embedding it in daily work. Productivity pressure in document-heavy and coordination-heavy roles is pushing companies to deploy copilots across communication, reporting, coding, and workflow support. Korean language performance also matters more here than in many other markets, which gives local platforms and localized deployments a clearer commercial role. At the same time, stricter data governance is changing how deployments are designed, increasing demand for hybrid, tightly managed enterprise setups. The remaining adoption gap among smaller firms leaves a clear runway for the South Korea AI copilot market as pricing, infrastructure access, and public support programs improve.

Key Report Takeaways

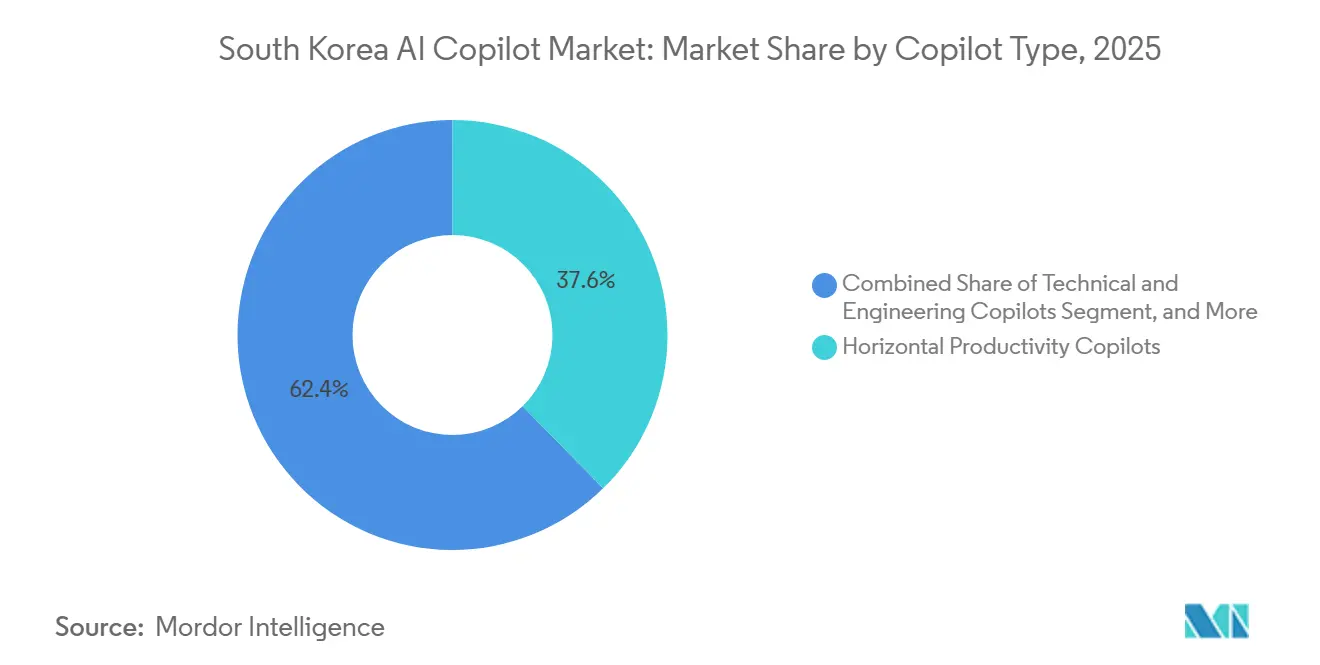

- By copilot type, Horizontal Productivity Copilots held 37.64% of the South Korea AI copilot market share in 2025, while Technical and Engineering Copilots are projected to expand at a 37.12% CAGR through 2031.

- By deployment mode, Cloud-Based deployment accounted for 71.28% of the South Korea AI copilot market size in 2025, while Hybrid deployment is projected to grow at a 36.84% CAGR through 2031.

- By organization size, Large Enterprises commanded a 72.41% share in 2025, while Small and Medium Enterprises are projected to expand at a 37.53% CAGR through 2031.

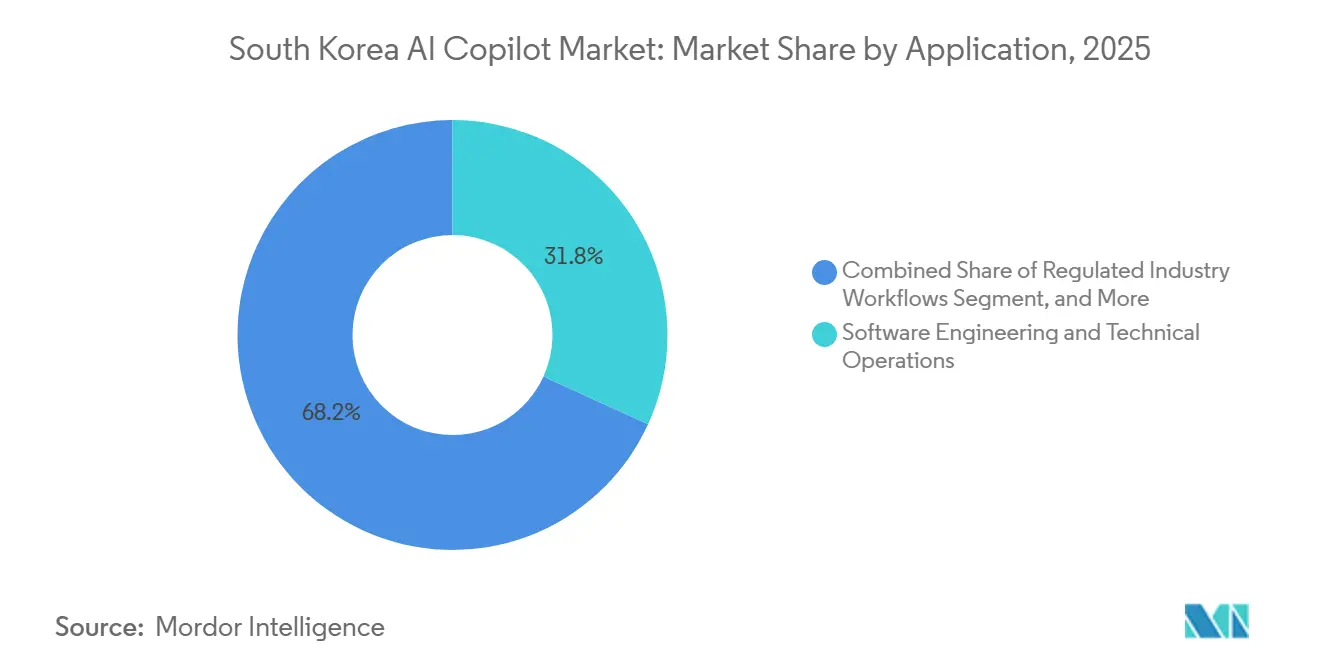

- By application, Software Engineering and Technical Operations accounted for a 31.82% share in 2025 and is projected to advance at a 38.14% CAGR through 2031.

- By end-user industry, IT and Telecommunication held a 25.73% share in 2025, while Industrial Manufacturing is projected to grow at a 36.92% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

South Korea AI Copilot Market Trends and Insights

Drivers Impact Analysis*

| river | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Enterprise Productivity Pressure In Knowledge Workflows | +8.5% | South Korea, strongest in Seoul and major enterprise clusters | Medium term (2-4 years) |

| Rapid Adoption of Generative AI In Enterprise Software Stacks | +7.2% | National, with strong spillover from large enterprise software rollouts | Short term (≤ 2 years) |

| Local Language and Workflow Personalization Needs | +5.8% | National, across enterprise, finance, and public sector use cases | Short term (≤ 2 years) |

| Domestic Cloud and LLM Ecosystem Expansion | +4.5% | National, with wider relevance across export-facing sectors | Long term (≥ 4 years) |

| Regulatory Push for Data Governance and Auditability | +3.2% | National, especially in regulated sectors | Medium term (2-4 years) |

| Labor Scarcity in White-Collar and Operations Functions | +2.8% | National, strongest in IT, manufacturing, and finance | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Enterprise Productivity Pressure in Knowledge Workflows

Korean companies are adopting copilots because a large share of office work still depends on repetitive document handling, internal coordination, and report creation. Samsung SDS found that 76% of Korean companies deployed generative AI at the organizational level in 2026, and time savings in routine knowledge work remained the primary driver of deployment.[1]Samsung SDS, “The Phased Journey of GenAI Adoption,” Samsung SDS, samsungsds.com LG U+ demonstrated how quickly this can scale when it adopted Microsoft 365 Copilot as a standard enterprise tool, achieving an 80% employee usage rate within 1 month of the full rollout. The same rollout reduced the time needed for data classification tasks by 90%, which shows why the South Korea AI copilot market is drawing demand from firms that want measurable labor efficiency instead of pilot activity alone. As more companies see direct time savings in writing, search, summarization, and review work, adoption is moving from selective teams into broader enterprise functions.

Rapid Adoption of Generative AI in Enterprise Software Stacks

The adoption curve has strengthened because Korean enterprises are no longer treating generative AI as a stand-alone experiment. Samsung SDS reported that firms in South Korea reviewed an average of 4.4 AI solutions simultaneously, indicating that companies are actively integrating copilots into broader software stacks rather than testing a single isolated tool. Microsoft also used Seoul in March 2026 to introduce new deep reasoning agents in Microsoft 365 Copilot, which signals that vendors see the country as a serious enterprise deployment environment.[2]Microsoft AI Economy Institute, “Q1 2026 AI Diffusion Report,” Microsoft, microsoft.com Samsung SDS noted that deployment formats are also diversifying, with self-build and enterprise versions becoming more common in sectors that require tighter system control. This broad software integration pattern supports the South Korea AI copilot market because demand is coming from both productivity suites and function-specific enterprise systems.

Local Language and Workflow Personalization Needs

Korean language performance remains a practical buying factor, especially when copilots are used for internal writing, compliance material, search, and task execution. NAVER released HyperCLOVA X THINK in 2025 and said the model ranked at the top of Seoul National University's KoBALT-700 benchmark while also delivering strong Korean-language reasoning performance.[3]NAVER Corporation, “NAVER Cloud Releases Reasoning Models for Free Commercial Use, Expanding Korea’s AI Ecosystem With Proprietary Technology,” NAVER, navercorp.com That matters because firms in finance, administration, and customer-facing operations need tools that can process Korean terminology with fewer errors and fewer manual corrections. NAVER Cloud also signed an agreement to provide the Bank of Korea with a HyperCLOVA X-based generative AI platform, which shows that language-native and domain-trained deployments are already reaching sensitive institutional settings. In the South Korea AI copilot market, strong localization is not a feature layer added after deployment, it is often part of the deployment decision itself.

Domestic Cloud and LLM Ecosystem Expansion

South Korea is building more of its enterprise AI stack in-house, reducing dependence on offshore processing and foreign infrastructure. NVIDIA announced in October 2025 that 260,000 Blackwell GPUs would be deployed across Samsung Electronics, SK Group, Hyundai Motor Group, NAVER Cloud, and the Korean government, lifting national installed AI GPU capacity from 65,000 to more than 300,000 units. NAVER also strengthened the developer side of the ecosystem by open-sourcing HyperCLOVA X SEED and later releasing HyperCLOVA X SEED 14B Think for free commercial use, widening access to Korean-language reasoning models. LG CNS added an enterprise infrastructure layer using its multilingual 111-billion-parameter LLM with Cohere, designed for on-premises deployment and lower GPU requirements. This domestic build-out improves the long-term supply conditions for the South Korea AI copilot market because it supports local inference, controlled deployments, and more sector-specific product development.[4]LG CNS and Korea Herald, “LG CNS Debuts New LLM Beating GPT-4o,” The Korea Herald, koreaherald.com

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Personal Data Localization and Cross-Border Transfer Friction | -3.8% | National, strongest in finance, public sector, and data-sensitive enterprise use cases | Medium term (2-4 years) |

| Integration Complexity Across Legacy Enterprise Systems | -2.9% | National, strongest in BFSI, manufacturing, and public sector | Medium term (2-4 years) |

| Trust, Hallucination, and Audit Risk In High-Stakes Workflows | -2.2% | National, strongest in healthcare, finance, and government | Long term (≥ 4 years) |

| Domestic Vendor Lock-In and Procurement Preference Barriers | -1.5% | National, especially in public procurement and chaebol-linked ecosystems | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Personal Data Localization And Cross-Border Transfer Friction

South Korea's privacy rules are becoming a stronger design constraint for enterprise copilots, especially when tools process internal records or customer data. IAPP reported that the 2026 PIPA reform introduced a 10% penalty ceiling on total turnover and personal supervisory liability for CEOs, which increased the practical risk associated with weak data handling. Shin and Kim also noted that the special AI provisions under PIPA allowed AI training on personal data only under strict review conditions, which adds another layer of compliance for systems trained on enterprise document sets. This is pushing vendors to redesign architecture around local hosting, controlled inference, and clearer audit trails. The result is slower procurement for some cloud-first products and stronger demand for hybrid deployment structures in the South Korea AI copilot market.

Integration Complexity Across Legacy Enterprise Systems

Many Korean enterprises still run large ERP, CRM, HR, and workflow systems that were not built for AI-native interaction. Samsung SDS identified a large gap between firms that had deployed generative AI and those that had internalized AI agents at an organization-wide scale, suggesting integration challenges rather than weak interest. The same company reported that enterprise and self-built deployment models often took more than 6 months, while 24% of self-built projects took over 1 year. For smaller manufacturers, the adoption rate remains very low, as the Ministry of SMEs and Startups' 2025 smart manufacturing survey found that only 0.1% of small and medium manufacturers had adopted AI at their production sites. This slows the South Korea AI copilot market in complex accounts, where the real challenge is connecting copilots to live systems and cleaning internal data.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Copilot Type: Horizontal Copilots Lead, Vertical Intelligence Accelerates

Horizontal Productivity Copilots held 37.64% of the South Korea AI copilot market in 2025, making this the largest category by revenue contribution. The segment expanded first because office productivity suites were easier to buy, test, and connect with common work tasks than narrower-use-case tools. Microsoft's collaboration with KT and other Korean enterprises helped establish a practical model for rolling out workplace copilots across communication, drafting, search, and workflow support. That early pattern also helped the South Korea AI copilot industry build demand in finance, telecom, and diversified enterprise groups where productivity improvement was the clearest entry point.

Technical and Engineering Copilots are projected to grow at a 37.12% CAGR during 2026-2031, the fastest among copilot types. This pace fits the country's heavy concentration in semiconductors, electronics, autos, industrial software, and developer-led workflows. Microsoft's March 2026 update showed that the Korean developer community on GitHub had surpassed 2.72 million members, underscoring strong demand for code generation, debugging, code review, and technical search assistants. NAVER's continued work on Korean reasoning models and LG CNS's multilingual enterprise LLM both expand the technical foundation for copilots used in specialized engineering environments. Functional Workflow Copilots and Industry-Specific Copilots remain smaller in scale, but they are gaining ground in finance, public services, healthcare, and enterprise operations as buyers move from generic task support to domain-specific use cases.

By Deployment Mode: Cloud Retains Scale While Hybrid Deployment Rises Quickly

Cloud-Based deployment accounted for 71.28% of the South Korea AI copilot market in 2025, which reflected the appeal of rapid deployment and lower upfront infrastructure demands. Many enterprises entered the market through cloud software because it reduced rollout time and made productivity gains visible early in the adoption cycle. Samsung SDS reported that Korean firms were reviewing multiple AI products at once, and that pattern favored cloud models during the first phase of adoption because they were easier to compare and activate. Cloud leadership also aligned with the strong pull of Microsoft 365 Copilot and similar platforms already tied to existing workplace software environments.

Hybrid deployment is forecast to grow at a 36.84% CAGR during 2026-2031, making it the fastest-growing format in the South Korea AI copilot market. This shift reflects stricter privacy obligations because organizations now need to balance model performance with tighter control over where enterprise information is stored and processed. IAPP, Shin, and Kim all showed that updated privacy rules raised the cost of weak governance and increased pressure for auditable, localized processing structures. LG CNS reinforced this direction with an on-premises multilingual LLM designed for companies seeking lower exposure to external data and greater direct control over their infrastructure. On-Premises deployment remains smaller today, but it is likely to stay important in finance, government, and other regulated settings where hybrid design can better align with local compliance expectations.

By Organization Size: Large Enterprises Drive Current Revenue While SMEs Build The Next Wave

Large Enterprises commanded a 72.41% share of the market in 2025, underscoring the strong concentration of initial spending in large accounts. These companies had the budget, procurement structure, internal data, and IT support needed to move faster than smaller firms. Samsung SDS found that 76% of Korean companies had already deployed generative AI at the organizational level in 2026, and the practical examples seen in telecom, finance, and large workplace environments came mainly from well-resourced enterprises. In revenue terms, large accounts still anchor the South Korea AI copilot market size because they can scale licenses, governance layers, and integration work at a level that smaller firms usually cannot match in the first phase.

Small and Medium Enterprises are projected to grow at a 37.53% CAGR during 2026-2031, which gives them the strongest forward pace by organization size. The Korea Chamber of Commerce and Industry, as cited by Seoul Economic Daily, reported a 13.8 percentage-point gap in generative AI usage between large enterprises and SMEs in June 2026, which highlights both the shortfall and the room for catch-up. Policy support is also becoming more direct because the Korea Small and Medium Venture Business Distribution Agency launched a 2025 initiative covering 70% of AI chatbot implementation costs for manufacturing SMEs. The Ministry of SMEs and Startups later set a broader path with Smart Manufacturing Innovation 3.0, aiming to reach 12,000 AI-enabled factories by 2030. Regional infrastructure support, including KakaoEnterprise's GPU-backed project in South Jeolla Province, should further improve access for firms outside the largest urban enterprise clusters.

By Application: Software Engineering And Technical Operations Leads In Scale And Growth

Software Engineering and Technical Operations accounted for 31.82% of the South Korea AI copilot market in 2025, making it the largest application area. The commercial logic is clear because coding, documentation, onboarding, testing, and debugging generate direct and visible productivity gains. Microsoft's March 2026 data on Korea's 2.72 million GitHub community members supports the strength of this application base, especially in enterprises with large software and technical workforces. The same segment is projected to grow at a 38.14% CAGR during 2026-2031, making it the most dynamic application track in current forecasts.

Knowledge Work and Productivity Assistance is another major use case because it meets the day-to-day needs of white-collar teams across many industries. Samsung SDS identified repetitive work such as document processing, report creation, and meeting summarization as the main demand driver for enterprise generative AI adoption. Customer and Employee Service Operations is also gaining wider adoption, with Samsung SDS's Woori Bank project set to deploy more than 175 AI agents across lending, asset management, internal controls, customer service, and process automation. Healthcare and regulated workflow applications are growing from a smaller base, but Yonsei University Health System already uses Azure OpenAI to support more than 80 specialized AI applications and plans to roll out Rounding Copilot for clinicians. Sales, marketing, internal operations, and regulated workflow assistants should continue to expand as buyers ask for tools that can act on enterprise content rather than just summarize it.

By End-User Industry: IT And Telecom Leads Today While Manufacturing Gains Momentum

IT and Telecommunication held a 25.73% share in 2025, so it remained the largest end-user segment in the South Korea AI copilot market. This position reflects both supply-side and demand-side strength, because telecom and IT companies are major users of enterprise software while also helping shape the wider AI ecosystem. KT worked with Microsoft on broad AI collaboration, and LG U+ moved quickly with workplace deployments, showing how this sector has served as an early operating ground for copilots in Korea. BFSI is closely followed because banks and financial institutions handle high volumes of process-heavy work and have strong incentives to automate search, drafting, review, and internal decision support.

Industrial Manufacturing is projected to grow at a 36.92% CAGR during 2026-2031, the fastest among end-user industries. The manufacturing base offers a large expansion pool, because the Ministry of SMEs and Startups' 2025 survey found that only 0.1% of small and medium manufacturers had adopted AI at production sites. The Manufacturing AI 2030 strategy announced in June 2026 committed 20 trillion KRW (USD 14.5 billion) by 2030 to embed AI across semiconductors, automotive, and shipbuilding, providing this vertical with a clear policy and investment backbone. Wider compute investments also support this shift, with the national Blackwell GPU deployment plan strengthening the local capacity needed for industrial AI workloads. Healthcare, education, media, government, and energy remain smaller in terms of current revenue, but each has clear use cases that should expand as compliance models and deployment templates mature.

Geography Analysis

Microsoft reported that South Korea had the highest AI adoption rate among surveyed economies at 81.4% in March 2026, while generative AI usage reached 37.1% in the first quarter of 2026. The Seoul metropolitan area remains the center of demand because it holds the headquarters of major enterprises, leading financial institutions, and much of the country's developer and enterprise IT base. Microsoft also used Seoul for high-profile product launches and partnership announcements, which reinforces the city's position as the main commercial hub for enterprise copilot deployment.

Geographic demand is now spreading beyond Seoul through industrial and policy-led channels. The Manufacturing AI 2030 strategy named Jeonbuk and Gyeongnam as regional testbeds for physical AI and autonomous manufacturing demonstrations inside existing industrial complexes. KakaoEnterprise's delivery of 40 NVIDIA B200 GPUs to South Jeolla Province under the regional AI transformation program shows that infrastructure support is reaching manufacturing regions that previously had limited access to advanced AI capacity. Microsoft also established a Busan Datacenter Academy with the City of Busan, which broadens the talent base for deployment in logistics, maritime, and heavy-industry settings. These regional moves matter because the South Korea AI copilot market cannot rely on Seoul alone if it is to deepen adoption in production-oriented sectors.

South Korea also serves as a lead-adoption environment that influences enterprise AI product strategy outside the country. Microsoft chose Korea in 2025 for expanded AI collaboration across major industries and returned in 2026 with another high-visibility launch, which shows that global vendors use this market to test enterprise readiness at scale. Yonhap reported that the Blackwell deployment plan would increase the country's installed AI GPU capacity to more than 300,000 units, strengthening South Korea's position in locally hosted AI processing. As regional programs, sovereign compute, and language-native models continue to expand, the South Korea AI copilot market is likely to remain both a domestic growth story and a proving ground for export-ready enterprise AI systems.

Competitive Landscape

The South Korea AI copilot market has a two-layer competitive structure made up of global platform vendors and domestic enterprise technology providers. Microsoft holds a strong position through its workplace software footprint, while NAVER, Samsung SDS, LG CNS, and KakaoEnterprise compete more directly on Korean-language performance, deployment flexibility, and depth of local integration. The field is active rather than tightly locked, because buyers are comparing multiple AI tools and deployment models rather than committing to a single universal stack. That keeps the South Korea AI copilot market competitive, even though a few large vendors have the broadest commercial reach.

Several recent strategic moves show that suppliers are trying to secure stronger positions in the enterprise. Samsung SDS signed a reseller agreement with OpenAI in 2025, becoming the first Korean company to serve as a domestic reseller of ChatGPT Enterprise and to add consulting and support services for deployment. In April 2026, Samsung SDS was also selected for Woori Bank's AI agent banking project, expanding its role from implementation support to multi-agent enterprise orchestration across core banking functions. NAVER strengthened its position by releasing HyperCLOVA X THINK and later open-sourcing commercial reasoning assets, which help it build both enterprise credibility and a wider domestic developer ecosystem. LG CNS added another route to differentiation through its multilingual LLM with Cohere and through deeper SAP-linked enterprise work, which is relevant for large accounts that want AI inside established systems rather than beside them.

Open space remains strongest in SME manufacturing, regulated workflows, and technical assistants built for Korean and multilingual industrial environments. The low AI base in small manufacturing sites means vendors that can package affordable, manageable copilots still have room to gain share. Compliance rules also create a real advantage for firms with local hosting options, stronger governance tools, and familiarity with Korean privacy requirements. At the same time, the expanding local model and infrastructure base should prevent the market from becoming overly dependent on a single foreign platform. Competition should therefore stay firm through 2031, with platform depth, language quality, and enterprise integration likely to matter more than simple brand recognition.

South Korea AI Copilot Industry Leaders

Microsoft Corporation

Alphabet Inc.

Salesforce, Inc.

ServiceNow, Inc.

SAP SE

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2026: NAVER Cloud released HyperCLOVA X SEED 14B Think as a free open-source commercial asset in July 2026. Developed entirely with proprietary technology using pruning and distillation techniques, the release aims to strengthen South Korea's AI technology ecosystem by providing a production-deployable Korean-language reasoning model at low compute cost.

- June 2026: SK Group Chairman Chey Tae-won announced a "one agent per person" initiative at the Icheon Forum on June 14, committing to deploy an individual AI assistant to every SK Group employee across all affiliates as part of the group's AI transformation roadmap. SK Group's 120,000-employee Microsoft 365 Copilot rollout, backed by a dedicated Copilot Command Center, underpins this initiative.

- June 2026: The Korean government and private sector announced the Manufacturing AI 2030 Strategy on June 29, committing a joint investment of 20 trillion KRW (USD 14.5 billion) by 2030 to embed AI across semiconductor, automotive, and shipbuilding manufacturing. The strategy targets over 100 trillion KRW in economic value creation and plans to position full-stack AI factories as a South Korean export product for advanced-economy and ASEAN markets.

- April 2026: Samsung SDS was selected as the preferred bidder for Woori Bank's AI agent banking project on April 7, 2026. The project deploys over 175 AI agents across 5 core banking domains, corporate lending, asset management, internal controls, customer service, and process automation, targeting a 30% improvement in operational processing speed. Approximately 90 AI agents are scheduled for initial deployment by December 2026.

South Korea AI Copilot Market Report Scope

The South Korea AI copilot market refers to the ecosystem of artificial intelligence-driven intelligent assistants integrated into enterprise and consumer software applications to enhance human capabilities and automate complex tasks within the country. These copilots leverage advanced foundation models, including large language models (LLMs) and generative AI, to provide real-time contextual suggestions, generate content, analyze data, and execute workflows seamlessly within existing digital tools. The market encompasses various copilot types ranging from general horizontal productivity tools to specialized functional, technical, and industry-specific solutions. Deployed across cloud-based, hybrid, and on-premises environments, these AI systems serve organizations of all sizes in South Korea. They are used across diverse applications, including knowledge work assistance, software development, customer service, and sales enablement, in industries such as IT, BFSI, manufacturing, and government. Driven by South Korea's highly advanced digital infrastructure, rapid adoption of emerging technologies by large conglomerates (chaebols) and SMEs alike, and strong government backing for AI integration, these copilots help local organizations drive operational efficiency, reduce manual cognitive load, and maintain a competitive edge in the global digital economy.

The South Korea AI Copilot Market Report is Segmented by Copilot Type (Horizontal Productivity Copilots, Functional Workflow Copilots, Technical and Engineering Copilots, and Industry-Specific Copilots), Deployment (Cloud-Based, Hybrid, and On-Premises), Organization Size (Large Enterprises, and Small and Medium Enterprises), Application (Knowledge Work and Productivity Assistance, Software Engineering and Technical Operations, Customer and Employee Service Operations, Sales, Marketing and Revenue Enablement, Business Process and Enterprise Operations, and Regulated Industry Workflows), and End-User Industry (IT and Telecommunication, BFSI, Healthcare and Life Sciences, Retail and E-Commerce, Industrial Manufacturing, Education and Research Institutions, Media and Entertainment, Government and Administration, Energy and Utilities, and Other End-User Industries). The Market Forecasts are Provided in Terms of Value (USD).

| Horizontal Productivity Copilots |

| Functional Workflow Copilots |

| Technical and Engineering Copilots |

| Industry-Specific Copilots |

| Cloud-Based |

| Hybrid |

| On-Premises |

| Large Enterprises |

| Small and Medium Enterprises |

| Knowledge Work and Productivity Assistance |

| Software Engineering and Technical Operations |

| Customer and Employee Service Operations |

| Sales, Marketing and Revenue Enablement |

| Business Process and Enterprise Operations |

| Regulated Industry Workflows |

| IT and Telecommunication |

| BFSI |

| Healthcare and Life Sciences |

| Retail and E-Commerce |

| Industrial Manufacturing |

| Education and Research Institutions |

| Media and Entertainment |

| Government and administration |

| Energy and Utilities |

| Other End-User Industries |

| By Copilot Type | Horizontal Productivity Copilots |

| Functional Workflow Copilots | |

| Technical and Engineering Copilots | |

| Industry-Specific Copilots | |

| By Deployment | Cloud-Based |

| Hybrid | |

| On-Premises | |

| By Organization Size | Large Enterprises |

| Small and Medium Enterprises | |

| By Application | Knowledge Work and Productivity Assistance |

| Software Engineering and Technical Operations | |

| Customer and Employee Service Operations | |

| Sales, Marketing and Revenue Enablement | |

| Business Process and Enterprise Operations | |

| Regulated Industry Workflows | |

| By End-User Industry | IT and Telecommunication |

| BFSI | |

| Healthcare and Life Sciences | |

| Retail and E-Commerce | |

| Industrial Manufacturing | |

| Education and Research Institutions | |

| Media and Entertainment | |

| Government and administration | |

| Energy and Utilities | |

| Other End-User Industries |

Key Questions Answered in the Report

What is the current size of the South Korea AI copilot market?

The South Korea AI copilot market was estimated at USD 0.54 billion in 2026 and is forecast to reach USD 2.36 billion by 2031, growing at a CAGR of 34.54%.

Which copilot type leads revenue in South Korea?

Horizontal Productivity Copilots led in 2025 with a 37.64% share, reflecting strong enterprise demand for workplace writing, search, summarization, and task support tools.

Which application is growing the fastest in South Korea AI copilots?

Software Engineering and Technical Operations is both the largest application segment at 31.82% in 2025 and the fastest-growing one at a 38.14% CAGR through 2031.

Why is hybrid deployment rising so quickly in Korea?

Hybrid deployment is projected to grow at a 36.84% CAGR because companies want better control over sensitive data while still using high-performance cloud-based AI functions.

Which end-user sector offers the strongest growth opportunity?

Industrial Manufacturing is projected to grow at a 36.92% CAGR through 2031, supported by the Manufacturing AI 2030 strategy and a still-low AI base in many production environments.

What is slowing broader adoption across smaller firms?

SMEs face higher barriers in cost, talent, and system integration, although public support programs and regional infrastructure projects are beginning to reduce these gaps.

Page last updated on: