Southeast Asia Adhesives And Sealants Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

| Market Size (2025) | USD 3.79 Billion |

| Market Size (2030) | USD 5.14 Billion |

| Growth Rate (2025 - 2030) | 6.30% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Southeast Asia Adhesives And Sealants Market Analysis by Mordor Intelligence

The Southeast Asia Adhesives and Sealants Market size is estimated at USD 3.79 billion in 2025, and is expected to reach USD 5.14 billion by 2030, at a CAGR of 6.30% during the forecast period (2025-2030). Manufacturing capacity shifting from China into Vietnam, Indonesia, and other ASEAN hubs is lifting demand for bonding solutions in electronics, construction, and packaging. E-commerce growth has doubled flexible-film consumption since 2020, while government infrastructure budgets continue to funnel volume into construction sealants. Automotive electrification policies such as Thailand’s 30@30 program are accelerating the uptake of structural adhesives that replace spot welding and enable lightweight battery trays. At the same time, low-VOC building standards in Singapore and Malaysia are pushing formulators toward water-borne and bio-based chemistries that command premium pricing.

Key Report Takeaways

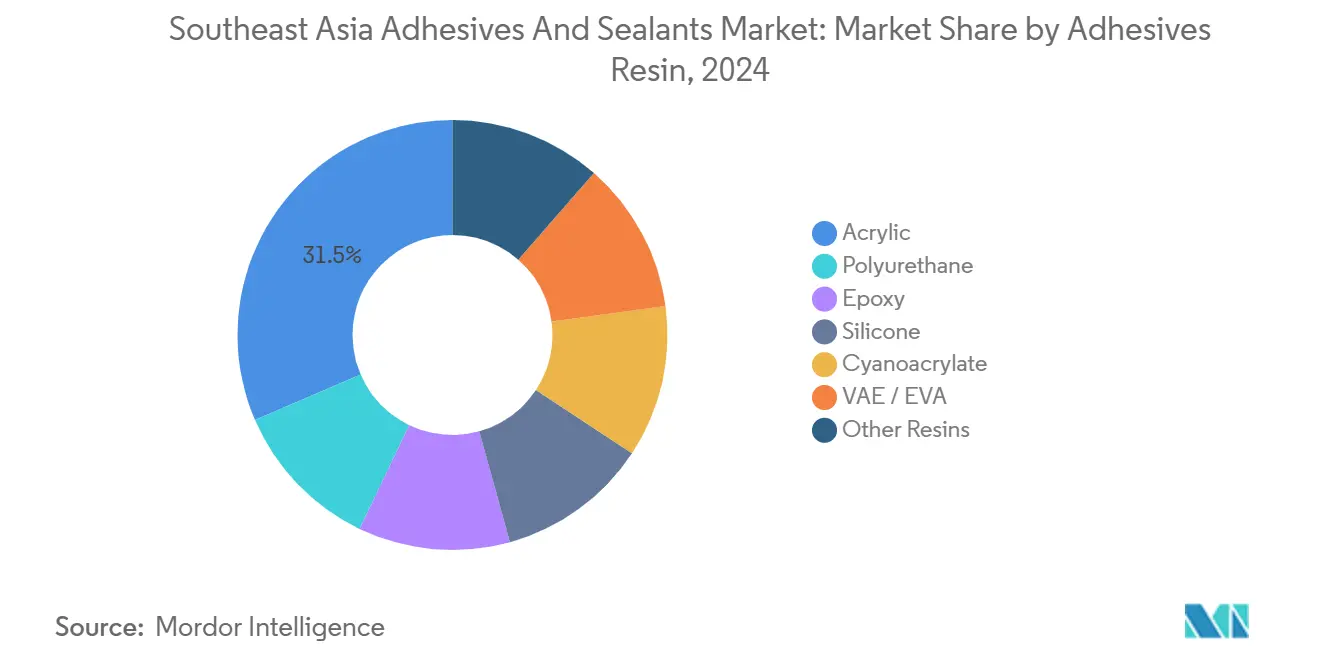

- By adhesives resin, acrylics captured 31.46% of 2024 revenue, while polyurethanes are projected to advance at a 6.67% CAGR to 2030.

- By adhesives technology, water-borne formulations held 42.37% share in 2024; UV-cured systems are poised for a 6.58% CAGR through 2030.

- By sealant resin, silicones commanded 45.28% of 2024 revenue, whereas polyurethane sealants will accelerate at a 6.88% CAGR to 2030.

- By end-user industry, packaging accounted for 34.63% of the Southeast Asia adhesives and sealants market size in 2024; automotive bonding is set to grow at a 6.39% CAGR through 2030.

- By geography, Indonesia led with 28.41% of the Southeast Asia adhesives and sealants market share in 2024. Vietnam is forecast to expand at a 6.77% CAGR through 2030, the fastest rate among all countries.

Southeast Asia Adhesives And Sealants Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid infrastructure and affordable-housing boom | +1.8% | Indonesia, Philippines, Vietnam; spillover to Thailand | Medium term (2-4 years) |

| Expansion of FMCG and e-commerce flexible packaging | +1.5% | Vietnam, Indonesia, Thailand; urban Malaysia, Philippines | Short term (≤ 2 years) |

| Accelerating electronics-assembly investments | +1.4% | Vietnam, Malaysia, Thailand; emerging Philippines | Medium term (2-4 years) |

| Automotive lightweighting adoption | +0.9% | Thailand, Indonesia, Malaysia; pilot Vietnam | Long term (≥ 4 years) |

| Growth of low-VOC green-building certifications | +0.7% | Singapore, Malaysia; spreading to Indonesia, Thailand | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid Infrastructure and Affordable-Housing Boom

In 2024, Indonesia allocated a significant budget for public works, along with an additional commitment to the IKN capital-city project, positioning the nation to absorb substantial construction materials. These projects are projected to utilize tile mortars, waterproofing membranes, and façade sealants, potentially consuming a notable portion of the region's incremental capacity by 2028. Meanwhile, the Philippines has dedicated resources to transportation and social housing initiatives. These projects specifically call for ISO 11600-compliant sealants in seismic joints, steering demand towards silicone and polyurethane products[1]Sika AG, “Sika significantly expands its mortar production in Indonesia,” sika.com. In Vietnam, with urbanization surpassing 60% in 2024, there's a surge in sales of pre-mixed tile adhesives, which notably reduce on-site labor. Multinational companies are rapidly expanding their footprint: Sika has not only more than doubled its mortar production in Bekasi, Indonesia, but has also broadened its retail presence to numerous outlets, a feat challenging for smaller competitors. Furthermore, green-building initiatives like Green Mark and GBI are now mandating low-VOC adhesives. While this requirement adds extra certification costs per product line, it simultaneously raises the entry barriers for players with limited capital.

Expansion of FMCG and E-Commerce Flexible Packaging

In 2024, Shopee, Lazada, and Tiki collectively handled a significant volume of parcels. This surge led brand owners to transition from rigid containers to lighter laminated pouches, reducing weight and consequently lowering freight costs[2]Thanh Van, “SCG to pour USD 700 million into ethane feedstock,” vir.com.vn. Water-borne acrylic and VAE emulsions, favored for their compatibility with high-speed lines, dominate the flexible-packaging laminate market. Meanwhile, solvent-borne polyurethanes, essential for retort pouches needing sterilization, maintain a notable market presence. Deli Group's investment in Hai Duong, set to roll out additional adhesive units annually from Q4 2026, targets stationery SKUs for regional e-commerce, amplifying the demand for low-migration grades. As FMCG buyers increasingly shun APEO and NMP, converters face pressure to adopt cleaner portfolios or risk delisting. In Gujarat, Toyo Ink's ambitious capacity expansion, with a focus on export tonnage, underscores the intensifying competition from Indian suppliers, particularly in the ASEAN market.

Accelerating Electronics-Assembly Investments

In 2024, Vietnam attracted substantial electronics foreign direct investment (FDI). Major players like Foxconn, Pegatron, and Intel expanded their modular assembly plants in the country. These plants have a specific requirement for UV-cured and dual-cure adhesives, emphasizing a need for sub-5-second tack-free times. Meanwhile, Malaysia's Penang tech cluster drew in investment from Elite Material. This investment focuses on producing semiconductor substrates, which are bonded using thermally conductive silicones that efficiently dissipate heat. Luxshare, operating six factories in Vietnam, utilizes DELO adhesives. These adhesives are compliant with the IPC-TM-650 ionic-contamination limits, underscoring the rising demand for on-site testing capabilities. Such testing comes at a significant price. This scenario presents an opportunity: adhesive suppliers that choose to co-locate can potentially slash end-user inventory holding costs significantly.

Automotive Lightweighting Adoption

In 2024, Thailand produced vehicles and is targeting a significant penetration of electric vehicles (EVs) by 2030. This ambition opens up structural bonding opportunities, displacing spot welds per vehicle. Sika's Power epoxies and Force polyurethanes achieve a high lap-shear strength on aluminum-to-composite joints, reducing assembly time and cutting EV weight. Covestro and Dow provide polyurethane and silicone gap fillers, effective in a wide temperature range. These performance benchmarks pose a challenge for local converters, especially in replicating them without specialty silanes. SEKISUI is making a significant move with its expansion in Thailand. This investment will produce HUD and acoustic films for vehicles each year, a process that necessitates ISO 12543-qualified PVB adhesives. However, the qualification cycles for these adhesives span several years, creating a barrier that favors established players.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent VOC and chemical-import rules | -0.6% | Singapore, Malaysia; emerging in Thailand, Indonesia | Short term (≤ 2 years) |

| Petro-feedstock price volatility | -0.9% | Regional; acute in Indonesia, Thailand, Vietnam | Short term (≤ 2 years) |

| Limited local feedstock capacity | -0.6% | Vietnam, Philippines, Thailand; moderate impact in Indonesia, Malaysia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent VOC and Chemical-Import Rules

Singapore has set VOC caps at levels aligning with EU standards. Malaysia, under its Environmental Quality Act, adopts these same limits, leading to significant reformulation costs for each product. In Thailand, the 2024 chemical-import registry mandates toxicology dossiers for isocyanates and epoxy hardeners, extending launch timelines. Meanwhile, Indonesia and Vietnam's lack of harmonized tests allows local converters to sell solvent lines at lower prices. This disparity is splintering the adhesives and sealants market across Southeast Asia. Looking ahead, ASEAN's potential REACH-like frameworks might introduce registration fees per substance by 2028, a move that could benefit multinational firms boasting in-house toxicology expertise.

Petro-Feedstock Price Volatility

In 2024, naphtha prices swung significantly, leading to a compression of converter margins. This was due to pass-through clauses lagging behind spot prices. SCG's ethane cracker in Vietnam is set to deliver cost savings on ethylene starting in 2027, thereby tilting the cost curve in favor of gas feedstocks. Nippon Shokubai's expansion of acrylic acid in Cilegon is poised to reduce Indonesia's import reliance and cut delivered costs. While specialty monomers are still heavily reliant on imports, making supply chains vulnerable to delays during peak construction, bio-based polyols command a premium over their petrochemical counterparts. However, this price gap diminishes when Brent crude prices surpass a certain threshold.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Adhesives Resin: Polyurethane Gains as Automotive and Packaging Converge

Polyurethane adhesives are set to grow at 6.67% CAGR through 2030, chipping away at acrylics’ 31.46% 2024 share. This shift is driven by the rising demand for elastomeric bonds in EV battery trays, composite body panels, and high-flex laminates, all of which require bonds that can endure thermal cycling. Polyurethane resins are expected to increase their presence in the Southeast Asia adhesives and sealants market over the forecast period. Acrylics maintain their volume leadership due to their cost-effectiveness and ability to bond polar substrates. This makes them essential for tile adhesive powders, PSA labels, and tapes that demand high lap-shear strength. However, lightweighting initiatives in Thailand and Indonesia are steering OEMs towards polyurethanes. For instance, SikaForce, a polyurethane, achieves commendable strength on aluminum-composite joints and can replace numerous welds in an EV. While epoxies are preferred for structural metal assemblies and electronics potting, their requirement for 2-component mixing and lengthy curing time can be a bottleneck for high-speed production lines. Silicones, with their impressive elasticity range, are favored for gaskets and weatherproofing. However, they come at a premium, commanding higher prices. On the sustainability front, bio-based polyurethanes derived from palm kernel oil and kraft lignin are making waves. Achieving renewable carbon content and meeting ASTM D6866 standards, they are unlocking green-procurement premiums in markets like Singapore and the EU.

Acrylic converters are poised for gains as Nippon Shokubai’s Cilegon plant gears up for domestic production of acrylic acid esters. This move is set to reduce landed monomer costs. Despite this, the share of polyurethane is anticipated to rise. This is largely because automotive and flexible-packaging specifications are increasingly favoring chemistries that offer both structural strength and resistance to flex-cracking. These are qualities that traditional acrylics and epoxies struggle to deliver without hybrid formulations. Cyanoacrylates, known for their rapid curing time, have carved out niches in the medical and consumer-electronics sectors. However, their inherent brittleness limits their application to low-stress joints. VAE and EVA emulsions find utility in woodworking and paper packaging. Yet, their limited moisture resistance poses challenges for exterior applications unless they undergo cross-linking. In summary, the Southeast Asia adhesives and sealants market is gravitating towards multifunctional polyurethane grades that adeptly balance adhesion, toughness, and compliance with regulatory standards.

By Adhesives Technology: UV-Cured Systems Disrupt Electronics Assembly

Water-borne adhesives controlled 42.37% of technology share in 2024, lauded for their low-VOC compliance and a solids window that curtails drying energy. This is particularly beneficial in applications like tile mortars and label stock. Yet, as electronics manufacturers push for rapid cycle times to avoid oven bottlenecks, UV-cured systems are forecast to post a 6.58% CAGR through 2030. In Southeast Asia's adhesives and sealants market, UV products currently capture a notable portion of the technology share, with potential to rise further by the decade's close. LED-UV lamps, operating at 395 nm, offer a substantial reduction in electricity consumption compared to traditional mercury arcs, translating to significant annual savings per production line. While solvent-borne grades hold a notable share in retort-pouch and footwear applications—thanks to their wet-out capabilities on non-polar substrates and resistance to high steam temperatures—regulatory pressures are nudging the industry towards exempt solvents like acetone.

In the realm of automotive structural bonding, reactive chemistries such as epoxies, polyurethanes, and methacrylate hybrids play a pivotal role, especially where gap filling and minimal shrinkage are paramount. Hot-melts, while dominant in case sealing and bookbinding at high speeds, face a limitation: they soften at elevated temperatures, restricting their use in tropical logistics. Toyo Ink's recent capacity expansion signals heightened competition in the solvent-borne specialty arena. Meanwhile, DELO's innovative dual-cure range offers a unique advantage, enabling surface UV setting followed by a thermal post-cure for shaded areas—a crucial feature for sensor die attachment. Coastal factories, grappling with high humidity levels, witness a doubling in drying times for water-borne adhesives. This not only diminishes bond strength but also steers specifiers towards the more expensive reactive or hot-melt alternatives.

By Sealants Resin: Polyurethane Captures Façade Air-Tightness Mandates

Silicone sealants kept a 45.28% grip on 2024 revenue, celebrated for their impressive UV resistance and elasticity, functioning effectively in a wide temperature range. These attributes make them a top choice for applications in curtain walls and automotive gaskets. Yet polyurethane sealants are on track for a 6.88% CAGR to 2030. This surge is largely attributed to the ISO 11600 Class 25LM standards, which are integral to the Green Mark and GBI schemes, both of which prioritize air-tight façades. In Southeast Asia, the market for adhesives and sealants indicates that polyurethane sealants are projected to grow. Polyurethane's unique ability to bond with porous concrete or masonry without the need for a primer, coupled with its paintability, renders it a cost-effective choice for non-glazing joints. While acrylics serve as effective interior gap fillers, their susceptibility to UV degradation and limitations in low temperatures restrict their use in exterior applications. Epoxy sealants, known for their durability on chemical-resistant floors, cure to a rigid state, limiting their application primarily to plant rooms. Meanwhile, hybrid silane-terminated polyethers are emerging as formidable competitors to silicones, delivering a significant portion of silicone's performance at a reduced price, making them particularly attractive for mid-tier projects.

Wacker has strategically positioned its new Asian silicone capacity to emphasize low-modulus grades. These grades are adept at withstanding joint movement, a crucial feature for tall façades that face the challenges of tropical thermal stress. In Singapore, the Green Mark Platinum has raised the bar by mandating independent ASTM C920 testing. This requirement, while adding an extra compliance cost per sealant, underscores the growing significance of multinationals equipped with in-house labs. As Indonesia embarks on a massive housing initiative, the spotlight is on polyurethane. Its advantages, such as paintability and a more economical unit cost, are set to overshadow silicone's renowned longevity, especially for façade and flooring joints.

By End-User Industry: Automotive Bonding Outpaces Packaging Volume

Packaging consumed 34.63% of the Southeast Asia adhesives and sealants market in 2024, driven by a surge in e-commerce parcels that has doubled the demand for flexible films since 2020. However, automotive bonding is projected to deliver a 6.39% CAGR through 2030. Components like EV battery trays and composite body panels are now utilizing 2-component epoxies or polyurethanes, which offer high lap-shear strength. This advancement not only replaces the need for traditional welds but also streamlines assembly cycles. The building and construction sector remains robust, with Indonesia’s infrastructure projects potentially consuming a notable portion of the region's added capacity. In footwear manufacturing, both Indonesia and Vietnam are opting for solvent-borne polyurethanes and neoprenes, ensuring durability against flex-cracking over extensive cycles.

Users in labels, tapes, and corrugated sectors favor water-borne acrylics for their low-VOC compliance and rapid machine speeds. In contrast, makers of retort pouches rely on solvent-borne polyurethanes, essential for achieving sterilization. While healthcare bonding is a specialized niche, it commands impressive gross margins, thanks to the stringent ISO 10993 and USP VI standards. Aerospace MRO centers in Singapore and Malaysia are on the lookout for high-performance epoxy film adhesives, specifically those certified to meet Boeing and Airbus specifications. Yet, it's worth noting that this aerospace segment constitutes a small portion of the region's total tonnage.

Geography Analysis

Vietnam commands the fastest trajectory, expanding at a 6.77% CAGR through 2030. This surge is fueled by electronics FDI in 2024 from industry giants like Foxconn, Pegatron, and Intel, boosting the consumption of UV-cured and thermally conductive grades. Despite a substantial annual import bill, component localization remains low. This scenario bestows co-located converters with a notable inventory cost advantage. Furthermore, SCG’s ethane cracker, set to yield olefin savings from 2027, bolsters Vietnam’s aspirations of emerging as a regional hub for adhesive production.

Indonesia held 28.41% of the 2024 revenue for the Southeast Asia adhesives and sealants market size. This dominance is anchored by a construction sector contributing notably to the GDP and a substantial state infrastructure investment. Sika, with its expanded Bekasi mortar output and a sprawling network of stores, is eyeing a significant share in the local tile-adhesive market by 2027. Meanwhile, Nippon Shokubai’s move to expand acrylic acid production is poised to reduce import dependence, translating to a notable drop in raw material costs for local converters.

Thailand, having produced a substantial number of vehicles in 2024, is setting its sights on a significant penetration of electric vehicles (EVs) by 2030. This shift is set to boost the demand for structural adhesives, especially for battery trays and composite panels, which are increasingly replacing traditional spot welds. In Malaysia, Penang’s semiconductor cluster has attracted investments, with Elite Material and MKS Instruments pouring in funds for a new lithography-equipment plant. This influx is expected to elevate the demand for thermally conductive silicones. Singapore, guided by its Land Transport Master Plan 2040, is steering its construction projects towards sustainability. The plan emphasizes the use of Green Mark Platinum standards, mandating sealants with low VOC levels. In the Philippines, a significant investment has been allocated for rail and port upgrades as of September 2024. These upgrades specifically call for ISO 11600 sealants to ensure seismic resilience. Meanwhile, Cambodia, Laos, Myanmar, and Brunei, collectively representing a small portion of the volume, are witnessing growth from modest bases. However, their high dependence on imports renders logistics costs unpredictable.

Competitive Landscape

The Southeast Asia adhesives and sealants market is moderately fragmented. Sika’s CHF 50 million Bekasi scale-up and 30,000 retail outlets reinforce cost leadership difficult for smaller firms to replicate. In Singapore and EU export markets, bio-based polyurethane adhesives, sourced from palm kernel oil and kraft lignin, are seizing white-space opportunities. These adhesives boast renewable carbon content and command green-procurement premiums. UV-cured technology leadership rests with DELO, whose dual-cure grades meet AEC-Q100 for automotive sensors and cure shadow areas thermally.

Southeast Asia Adhesives And Sealants Industry Leaders

Henkel AG & Co. KGaA

Sika AG

Arkema

H.B. Fuller Company

3M

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Henkel rolled out Loctite Liofol LA 7837/LA 6265, a solvent-free aliphatic polyurethane for high-heat pet-food retort packaging.

- December 2024: Arkema’s Bostik unit completed the acquisition of Dow’s flexible-packaging laminating-adhesives business, enhancing its Southeast Asian footprint.

Southeast Asia Adhesives And Sealants Market Report Scope

Adhesives are substances that bond two or more surfaces together to create a strong, lasting connection. Sealants are materials that are used to fill gaps to create a barrier against air, moisture, or other elements.

The Southeast Asia adhesives and sealants market is segmented by adhesives resin, adhesives technology, sealants resin, end-user industry, and geography. By Adhesives Resin, the market is segmented into polyurethane, epoxy, acrylic, silicone, cyanoacrylate, VAE/EVA, and other resins. By Adhesives Technology, the market is segmented into water-borne, solvent-borne, reactive, hot-melt, and UV-cured. By Sealants Resin, the market is segmented into silicone, polyurethane, acrylic, epoxy, and other resins. By End-user Industry, the market is segmented into aerospace, automotive, building and construction, footwear and leather, healthcare, packaging, woodworking and joinery, and other end-user industries. The report also covers the market size and forecasts for the adhesives and sealants market in 6 countries across the Southeast Asia region. For each segment, the market sizing and forecasts have been done based on revenue (USD).

| Polyurethane |

| Epoxy |

| Acrylic |

| Silicone |

| Cyanoacrylate |

| VAE / EVA |

| Other Resins |

| Water-borne |

| Solvent-borne |

| Reactive |

| Hot-Melt |

| UV Cured |

| Silicone |

| Polyurethane |

| Acrylic |

| Epoxy |

| Other Resins |

| Aerospace |

| Automotive |

| Building and Construction |

| Footwear and Leather |

| Healthcare |

| Packaging |

| Woodworking and Joinery |

| Other End-user Industries |

| Indonesia |

| Malaysia |

| Philippines |

| Singapore |

| Thailand |

| Vietnam |

| Rest of Southeast Asia |

| By Adhesives Resin | Polyurethane |

| Epoxy | |

| Acrylic | |

| Silicone | |

| Cyanoacrylate | |

| VAE / EVA | |

| Other Resins | |

| By Adhesives Technology | Water-borne |

| Solvent-borne | |

| Reactive | |

| Hot-Melt | |

| UV Cured | |

| By Sealants Resin | Silicone |

| Polyurethane | |

| Acrylic | |

| Epoxy | |

| Other Resins | |

| By End-user Industry | Aerospace |

| Automotive | |

| Building and Construction | |

| Footwear and Leather | |

| Healthcare | |

| Packaging | |

| Woodworking and Joinery | |

| Other End-user Industries | |

| By Geography | Indonesia |

| Malaysia | |

| Philippines | |

| Singapore | |

| Thailand | |

| Vietnam | |

| Rest of Southeast Asia |

Key Questions Answered in the Report

What is the 2025 value of the Southeast Asia adhesives and sealants market?

The market is valued at USD 3.79 billion in 2025.

How fast is the Vietnam segment growing?

Vietnam is forecast to register a 6.77% CAGR through 2030, the fastest in the region.

Which resin category is gaining the most share?

Polyurethane adhesives are expanding at a 6.67% CAGR, outpacing acrylics.

Why are UV-cured adhesives gaining traction?

Electronics assemblers favor sub-5-second cures that eliminate oven bottlenecks and lower energy costs.

What regulations influence adhesive formulations in Singapore?

Green Mark Platinum requires VOC emissions under 50 g/L and formaldehyde below 0.05%.

Page last updated on: