South Asia Customer Data Platform Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

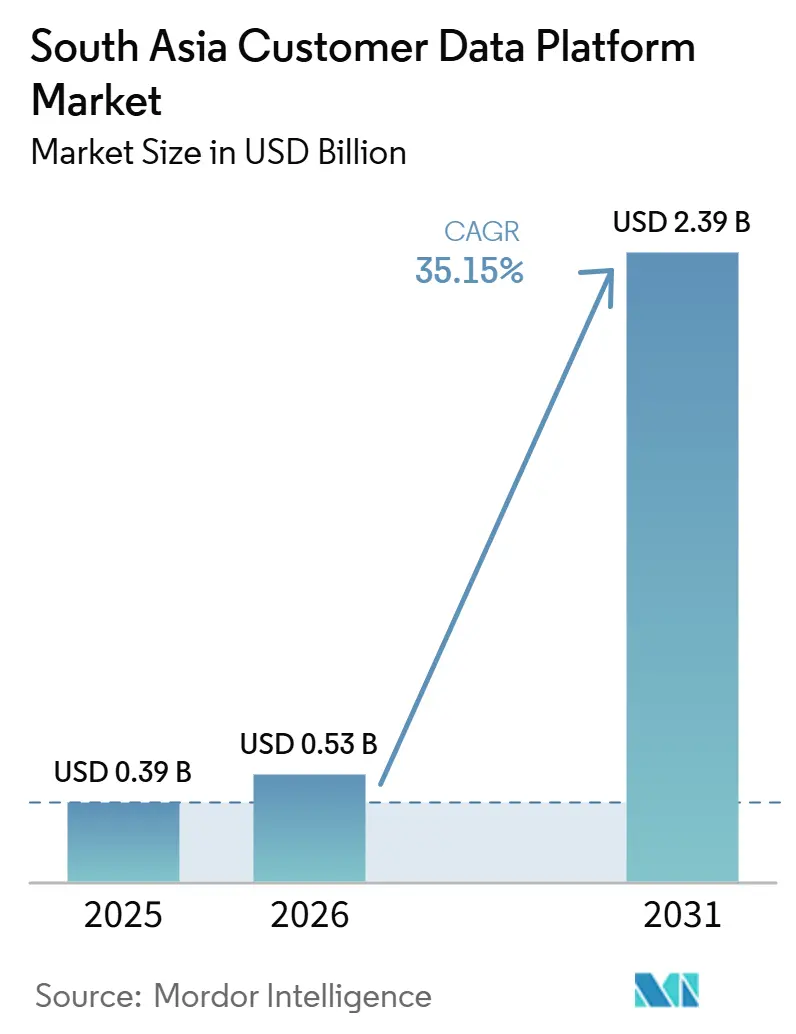

| Base Year Market Size (2025) | USD 0.39 Billion |

| Market Size (2026) | USD 0.53 Billion |

| Market Size (2031) | USD 2.39 Billion |

| Growth Rate (2026 - 2031) | 35.15% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South Asia Customer Data Platform Market Analysis by Mordor Intelligence

The South Asia customer data platform market was valued at USD 0.39 billion in 2025 and estimated to grow from USD 0.53 billion in 2026 to reach USD 2.39 billion by 2031, at a CAGR of 35.15% during the forecast period (2026-2031). The South Asia customer data platform market is gaining momentum because enterprises now treat consented first-party data as a core operating requirement rather than a marketing add-on. The 2025 DPDP Rules in India moved customer data governance higher on board agendas, especially across financial services, retail, healthcare, and government-facing organizations. The South Asia customer data platform market is also benefiting from faster digital adoption, rising customer engagement complexity, and stronger demand for unified profiles that can work across mobile apps, websites, messaging channels, and physical locations. Competition is sharpening as global enterprise suites pursue large and complex deployments, while India-native platforms defend positions with WhatsApp-native design, regional language support, and mobile-first delivery. The main short-term constraint for the South Asia customer data platform market is the shortage of specialized implementation talent, which is stretching delivery timelines and increasing the value of managed services and partner-led deployment support.

Key Report Takeaways

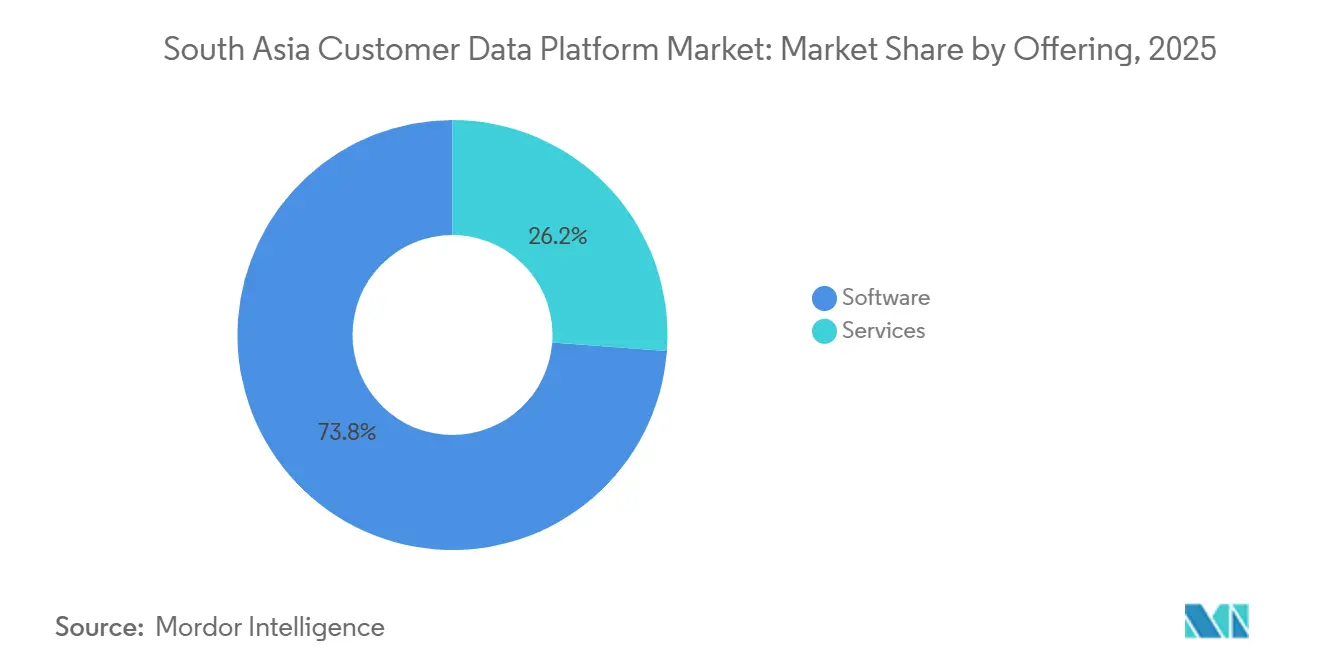

- By offering, software held 73.81% revenue share in the South Asia customer data platform market in 2025, while services are projected to expand at a 35.91% CAGR through 2031.

- By deployment mode, cloud accounted for 69.53% revenue share in 2025, while hybrid is expected to record the highest CAGR at 36.19% through 2031.

- By organization size, large enterprises accounted for 69.26% of revenue share in 2025, while SMEs are projected to grow at a 35.87% CAGR through 2031.

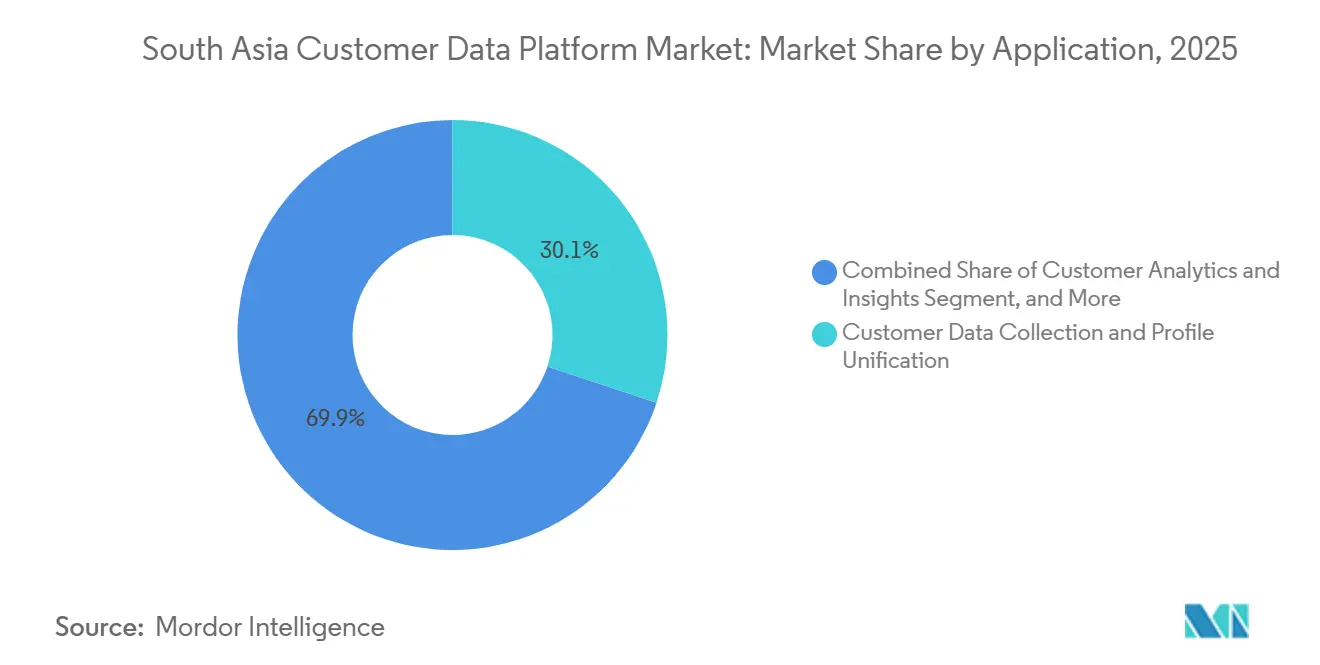

- By application, customer data collection and profile unification accounted for a 30.11% share of the South Asia customer data platform market size in 2025, while audience segmentation and personalization are projected to advance at a 36.82% CAGR through 2031.

- By end-user industry, retail and e-commerce held 33.27% revenue share in 2025, while healthcare and life sciences are projected to expand at a 37.12% CAGR through 2031.

- By geography, India held 78.67% share of the South Asia customer data platform market in 2025 and is also projected to record the fastest regional CAGR at 36.91% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

South Asia Customer Data Platform Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Rising First-Party Data Monetization Pressure Across Retail and BFSI | +7.2% | India, with early replication across Bangladesh and Pakistan | Short term (≤ 2 years) |

| Privacy-By-Design Demand From India’s Data Localization and Consent Rules | +6.8% | India as primary driver, spill-over to Sri Lanka and Rest of South Asia | Short term (≤ 2 years) |

| Rapid Growth of Omnichannel Commerce and Super-App Data Streams | +5.5% | India core, spill-over to Bangladesh and Pakistan | Medium term (2-4 years) |

| AI-Enabled Next-Best-Action Orchestration in Customer Engagement | +4.8% | Global, with concentrated execution in India’s digital-first enterprise sector | Medium term (2-4 years) |

| Rising Demand for Real-Time Identity Resolution and Event-Driven Activation | +4.5% | India and Bangladesh e-commerce ecosystems | Medium term (2-4 years) |

| Expansion of Warehouse-Native and Composable Data Architectures | +3.6% | India tech product companies, early entry in Pakistan SaaS sector | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising First-Party Data Monetization Pressure Across Retail and BFSI

The South Asia customer data platform market is benefiting from the rapid shift away from loose and fragmented customer targeting models toward consent-based first-party data activation. India’s 2025 DPDP Rules made it harder for regulated sectors to rely on weak consent practices, which pushed banks, insurers, and organized retailers toward systems that can capture, store, and apply customer permissions across channels.[1]Government of India, “Digital Personal Data Protection Rules, 2025,” Ministry of Electronics and Information Technology, cadp.in This pressure is commercial as well as regulatory, because marketers still need unified profiles to improve conversion efficiency, retention, and cross-sell performance in mobile-first customer journeys. Salesforce reported in 2026 that 81% of marketers in India had adopted AI, but fragmented and irrelevant data were still limiting results, which raised the value of a stronger data foundation. When customer records sit across 5 or more systems, the South Asia customer data platform market gains relevance because profile unification becomes necessary for both compliance and revenue generation.

Privacy-By-Design Demand From India’s Data Localization and Consent Rules

The South Asia customer data platform market is also being pushed forward by the need to build privacy controls directly into customer data operations. The official 2025 DPDP Rules required clear and purpose-specific consent, easier withdrawal, breach reporting obligations, and stronger control over how personal data is processed, which closely matches the governance features that many CDPs are designed to support. This shift matters because older CRM and campaign tools were not built to act as a central layer for consent tracking, purpose limitation, and controlled customer activation. For healthcare, the pressure is even sharper because digital health workflows depend on consent-linked data exchange, and that has made unified patient engagement infrastructure more relevant across providers and private hospital networks.[2]National Health Authority of India, “Ayushman Bharat Digital Mission - ABHA Health ID Statistics,” National Health Authority of India, abdm.gov.in The South Asia customer data platform market is therefore seeing stronger buying urgency from regulated sectors that need systems capable of joining personalization with auditability.

Rapid Growth of Omnichannel Commerce and Super-App Data Streams

The South Asia customer data platform market is expanding alongside a consumer journey that now moves across discovery, browsing, chat, rewards, and purchase in several connected environments. In India, brands often interact with the same consumer across apps, websites, marketplaces, messaging, and stores, which creates disconnected records unless there is a system built to unify them. This complexity is spreading across South Asia as digital commerce becomes more mobile-led and messaging-led, especially for customer support and repeat purchases. The shift is also changing the balance of power because brands that do not build their own customer data layer risk depending too heavily on platform intermediaries for targeting and customer insight. That makes the South Asia customer data platform market more important as companies try to preserve direct visibility into customer behavior and long-term engagement economics.

AI-Enabled Next-Best-Action Orchestration in Customer Engagement

The South Asia customer data platform market is moving beyond batch segmentation toward real-time decisioning that can recommend or trigger the next best action for each user. Salesforce’s 2026 findings showed broad AI adoption among Indian marketers, but the same research also pointed to fragmented data as the main barrier to value capture, which reinforced the need for a unified customer data layer. This matters because rule-based campaign management becomes harder to scale when brands need to coordinate app notifications, email, SMS, and WhatsApp at the same time. MoEngage’s 2026 acquisition of Aampe also showed how the competitive focus is shifting toward per-user autonomous decisioning and faster engagement optimization at production scale. As a result, the South Asia customer data platform market is increasingly judged by how quickly it can turn customer signals into actions instead of only how well it stores customer records.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| High Implementation Complexity Across Fragmented Enterprise Data Stacks | -3.2% | India large enterprises, Bangladesh and Pakistan across enterprise sizes | Short term (≤ 2 years) |

| Shortage of Reverse-ETL, Identity Resolution, and CDP Architecture Talent | -2.6% | Pan-South Asia, most acute outside India’s metropolitan technology hubs | Medium term (2-4 years) |

| Compliance Costs From Data Residency, Consent, and Audit Requirements | -1.9% | India and cross-border operators across South Asia | Short term (≤ 2 years) |

| Vendor Lock-In Concerns in Suite-Led CDP Purchasing Decisions | -1.5% | India large enterprise, with spill-over to BFSI buyers in Bangladesh and Sri Lanka | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Implementation Complexity Across Fragmented Enterprise Data Stacks

The South Asia customer data platform market still faces friction because many enterprises keep customer records across disconnected CRM, ERP, analytics, commerce, and campaign systems. That setup makes profile unification a long integration program rather than a quick software rollout. The challenge is sharper in South Asia because many companies added new cloud tools on top of older systems during the last wave of digital transformation, which widened the gap between data sources instead of simplifying it. Buyers in Bangladesh and Pakistan often face extra work because local connectors, regional payment integrations, and implementation support remain less mature than in India. This is why the South Asia customer data platform market is creating more room for vendors and partners that can provide prebuilt connectors, managed services, and stronger deployment support.

Shortage of Reverse-ETL, Identity Resolution, and CDP Architecture Talent

The South Asia customer data platform market is also constrained by a shortage of engineers who can design reverse-ETL pipelines, identity graphs, warehouse-native setups, and consent-ready schemas. India has a large engineering base, but the deepest CDP-specific talent remains concentrated in Bengaluru, Hyderabad, and Mumbai, which leaves buyers in secondary cities with fewer local options. The challenge is broader in Bangladesh and Pakistan, where digital commerce and digital marketing are growing faster than specialized data engineering capacity. This slows implementations, increases dependence on partners, and can delay expansion from pilot use cases into full production deployment. The South Asia customer data platform market will continue to reward vendors with strong enablement models because skill availability is still shaping the pace of adoption.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Offering: Services Growth Reshapes the Software-Led Delivery Model

Software accounted for 73.81% share of the South Asia customer data platform market size in 2025, while services are projected to expand at a 35.91% CAGR through 2031. This pattern shows that the South Asia customer data platform market still relies on packaged platforms for initial entry because software deployment usually offers a faster path to operational use. It also shows that buyers are not stopping at the license layer, because more advanced activation use cases need sustained configuration, integration, and optimization support. The software base remains important, but growth is shifting toward the support work needed to make the platform effective in live business environments.

The customer data platform industry in South Asia is following a path where services grow as implementations become deeper and more business critical. Once buyers move from profile unification into real-time identity resolution, consent-linked activation, and AI-supported decisioning, the amount of partner and service work rises with them. RudderStack’s warehouse-native model reflects this shift because open and composable architectures usually need more specialized implementation and tuning work than simpler boxed deployments.[3]RudderStack, “Warehouse-Native Architecture Explained,” RudderStack, rudderstack.com This means service revenue is expanding not because software is weakening, but because the South Asia customer data platform market is moving into a more operational and embedded stage of use.

By Deployment Mode: Cloud Becomes the Default Architecture

Cloud held 69.53% revenue share in 2025, while hybrid is projected to record the highest CAGR at 36.19% through 2031. The current lead for cloud shows that most buyers still favor managed infrastructure that reduces hardware burden and shortens deployment time. This is especially important for mid-market companies that need scale and flexibility without building heavy internal infrastructure first. At the same time, the faster growth of hybrid shows that compliance and agility now need to coexist in the same architecture.

The South Asia customer data platform market is therefore not moving in a simple direction where cloud fully replaces all other models. On-premises remains relevant for government and highly regulated BFSI use cases where audit controls, security rules, and sovereignty concerns still carry more weight than speed alone. Hybrid growth reflects the need to keep sensitive data and consent controls closer to local infrastructure while using cloud layers for broader processing and activation. Vendors with clearer hybrid blueprints and stronger compliance controls are likely to stay more competitive in regulated buying cycles.[4]Tealium, “Customer Data Layer vs CDP in 2026: Understanding the Critical Difference for Data Collection and Activation,” Tealium, tealium.com

By Organization Size: Large Enterprises Lead While SMEs Gain Ground Faster

Large enterprises held 69.26% revenue share in 2025, while SMEs are projected to grow at a 35.87% CAGR through 2031. This lead was expected because larger companies encountered customer data fragmentation earlier through multi-channel commerce, cross-sell programs, and retention efforts at scale. They also had bigger budgets and more pressure to coordinate data across multiple products, channels, and business units. Even so, the faster growth of SMEs shows that barriers to entry are easing across the South Asia customer data platform market.

Cloud-native delivery, modular onboarding, and local pricing structures are helping smaller buyers adopt these tools earlier in their digital maturity cycle. Many digital-first SMEs in India built meaningful customer bases before they ever adopted a formal enterprise CRM, so a CDP is becoming their first organized customer data layer rather than a replacement for an older system. That greenfield path can reduce integration complexity and improve early payback when compared with enterprise replacement programs. This gives India-native platforms an opening because they are often better positioned to serve leaner teams with mobile-first workflows and lower implementation overhead.

By Application: Activation Moves Ahead of Foundational Data Buildout

Customer Data Collection and Profile Unification accounted for 30.11% share of the South Asia customer data platform market size in 2025, while Audience Segmentation and Personalization is projected to grow at a 36.82% CAGR through 2031. The leading share for collection and unification shows that many buyers are still building the core customer record that makes later activation possible. The faster growth for personalization shows that more deployments are now moving from foundational data work into business use cases tied to conversion, retention, and customer lifetime value. This is a clear sign that the South Asia customer data platform market is becoming more outcome-driven.

Marketing campaign and customer journey orchestration remain important because brands want to automate communication across app, email, SMS, and WhatsApp without relying on manual campaign logic. Customer analytics and insights also gain budget as companies learn that unified profiles alone do not create value unless they support better targeting and faster decisions. Consent and preference management has moved from a narrow compliance feature into a trust-building tool because clearer preference controls can improve opt-in quality over time. The South Asia customer data platform market is therefore showing a normal maturity curve where data collection leads first, but activation and decisioning rise faster once the base layer is in place.

By End-User Industry: Retail Leads While Healthcare Accelerates the Fastest

Retail and E-Commerce held 33.27% of the South Asia customer data platform market share in 2025, while Healthcare and Life Sciences are projected to expand at a 37.12% CAGR through 2031. Retail leads because South Asia’s mobile-first buying journey creates multiple identity points that must be connected before brands can personalize at scale. BFSI remains one of the largest user groups because banks and insurers need stronger consent control, cross-sell visibility, and customer views that stretch across digital and physical interactions. Healthcare’s faster growth shows how digital patient engagement is becoming more structured and more data-dependent.

India’s Ayushman Bharat Digital Mission had crossed 380 million ABHA Health IDs by 2026, which shows the scale of consent-linked digital health infrastructure now taking shape. That environment supports the use of CDPs in patient journey management, provider communication, and other engagement workflows tied to authorized health data exchange. IT and Telecom operators are also using these platforms to reduce churn and improve retention through predictive engagement models. The customer data platform industry is widening beyond early retail use cases because more sectors now need unified data, compliance control, and personalized communication in the same stack.

Geography Analysis

India held 78.67% of the South Asia customer data platform market share in 2025 and is projected to grow at a 36.91% CAGR through 2031. That lead reflects more than overall economic size, because India also has the region’s deepest vendor base, broader enterprise digitization, and the strongest regulatory push tied to customer data governance. The DPDP Rules created a direct need for systems that can support purpose-linked consent, data control, and breach response in a more structured way. Salesforce’s move to make Data 360 and Agentforce available on the AWS Marketplace in India in June 2026 also showed how global vendors are adapting procurement and distribution models for faster local access. The South Asia customer data platform market is therefore anchored in India, and that anchor is being reinforced by both demand depth and local execution capability.

Bangladesh and Pakistan form the next meaningful growth frontier for the South Asia customer data platform market. Bangladesh had 131.9 million internet subscribers as of August 2024, which supports a large and growing pool of digital customer signals across commerce and mobile services.[5]Bangladesh Telecommunication Regulatory Commission, “Internet Subscribers Report - August 2024,” Bangladesh Telecommunication Regulatory Commission, btrc.gov.bd Pakistan’s large internet and mobile user base is also supporting stronger first-party data strategies as brands look for better control over targeting and customer retention. In both countries, e-commerce players are likely to lead early demand, while BFSI and telecom can widen adoption as data protection expectations become more formal.

Sri Lanka and the Rest of South Asia remain smaller in absolute demand, but they still matter for the long-term shape of the South Asia customer data platform market. Sri Lanka shows stronger digital marketing maturity than its size alone would suggest, especially in hospitality, financial services, and IT services. Smaller South Asian economies are also positioned to leap directly into cloud-native and composable architectures because many buyers have less legacy on-premises infrastructure to replace. As cross-border digital commerce expands, these markets could create new demand for customer identity resolution that works across multiple South Asian operating environments.

Competitive Landscape

The South Asia customer data platform market has a split structure where global enterprise suites compete for the largest and most complex deals, while India-founded platforms remain strong in the mid-market and digital-native enterprise segment. Local players have built defensible advantages through WhatsApp-native workflows, regional language support, mobile-first engagement design, and local pricing models that fit growth-stage buyers more closely. The top tier appears moderately concentrated, with 4 or 5 platforms capturing much of enterprise contract value, but the broader field remains crowded with more than 60 CDP-adjacent vendors. This balance means no single group controls the entire South Asia customer data platform market, even though the largest players still shape product expectations and pricing benchmarks. Buyers, therefore, evaluate vendors not only on core profile unification, but also on implementation support, local readiness, and the ability to fit sector-specific data rules.

AI and agentic decisioning are now the most visible near-term differentiators in the South Asia customer data platform market. MoEngage strengthened its position in June 2026 when it acquired Aampe and added per-user autonomous AI decisioning capabilities into its Merlin AI suite. Salesforce also expanded its local enterprise route in India by making Agentforce, Data 360, Slack, and Tableau Next available through the AWS Marketplace, which reduced procurement friction for buyers already committed to AWS budgets. Amperity’s emphasis on AI-led identity resolution also shows how incumbents are using proprietary matching and record-linking capability to defend against lower-cost alternatives.

Go-to-market structure is changing as well, which adds another layer to competition in the South Asia customer data platform market. CleverTap’s alliance with KPMG in India in May 2026 showed how CDP decisions can increasingly be shaped inside broader transformation programs rather than through standalone software buying cycles. Vendor lock-in remains a live concern, especially in BFSI, because proprietary data models can make later migration expensive and operationally disruptive. Platforms that offer open APIs, clearer data portability, and alignment with common data model practices are likely to gain trust where risk management carries as much weight as feature depth.

South Asia Customer Data Platform Industry Leaders

Salesforce, Inc.

Adobe Inc.

Oracle Corporation

SAP SE

Twilio Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: MoEngage acquired AI startup Aampe in an all-cash deal, integrating Aampe's per-user autonomous AI agent infrastructure, which processes over 200 billion decisions weekly, into MoEngage's Merlin AI suite. The acquisition is intended to deliver 1:1 agentic customer decisioning at production scale and was valued at tens of millions of dollars. Aampe's technology had demonstrated a 40% revenue uplift and 120-150 times the efficiency of paid advertising for returning-customer engagement.

- June 2026: MoEngage launched Merlin AI Custom Agents, introducing marketer-defined guardrails, full activity-log visibility, and an open Model Context Protocol (MCP) server with connectivity to external AI systems including Claude and ChatGPT. The launch positions MoEngage to serve enterprise buyers seeking transparent, auditable AI workflows, a differentiator for enterprise buyers navigating heightened accountability and audit requirements.

- June 2026: Salesforce made its Agentforce, Data 360, Slack, and Tableau Next products available on the AWS Marketplace in India, enabling enterprises to procure Salesforce tools through existing AWS cloud budgets and consolidated billing. The availability reduces procurement friction for the estimated 81% of Indian marketers who have adopted AI but face barriers from complex purchasing and siloed data infrastructure.

- May 2026: MoEngage announced a strategic partnership with Swiggy, India's leading on-demand convenience platform, to power AI-driven customer journey automation and personalized engagement across Swiggy's multi-category user base. The deployment includes MoEngage's Merlin AI Decisioning feature for real-time engagement optimization.

South Asia Customer Data Platform Market Report Scope

The South Asia customer data platform market includes platforms and services across countries such as India, Bangladesh, Pakistan, Sri Lanka, and others in the region. These solutions consolidate customer data from multiple sources into unified, centralized profiles. They support identity resolution, real-time integration, segmentation, personalization, and analytics, enabling enterprises to deliver consistent omnichannel customer experiences. India’s large digital commerce and fintech ecosystems drive market growth, while neighboring countries are seeing emerging adoption. Evolving data privacy regulations and the growing need for scalable martech solutions across retail, banking, telecom, and healthcare sectors also shape the market.

The South Asia Customer Data Platform Market Report is Segmented by Offering (Software, and Services), Deployment Mode (Cloud, On-Premises, and Hybrid) Organization Size (Large Enterprises, and Small and Medium Enterprises), Application (Customer Data Collection and Profile Unification, Audience Segmentation and Personalization, Marketing Campaign and Customer Journey Orchestration, Customer Analytics and Insights, Consent and Preference Management, and Other Applications), End-User Industry (Retail and E-Commerce, Banking, Financial Services, and Insurance (BFSI), Healthcare and Life Sciences, IT and Telecom, Media and Entertainment, Industrial Manufacturing, Government and Public Administrationm and Other End-User Industries), and Country (India, Bangladesh, Pakistan, Sri Lanka, and Rest of South Asia). The Market Forecasts are Provided in Terms of Value (USD).

| Software |

| Services |

| Cloud |

| On-Premises |

| Hybrid |

| Large Enterprises |

| Small and Medium Enterprises |

| Customer Data Collection and Profile Unification |

| Audience Segmentation and Personalization |

| Marketing Campaign and Customer Journey Orchestration |

| Customer Analytics and Insights |

| Consent and Preference Management |

| Other Applications |

| Retail and E-Commerce |

| Banking, Financial Services, and Insurance (BFSI) |

| Healthcare and Life Sciences |

| IT and Telecom |

| Media and Entertainment |

| Industrial Manufacturing |

| Government and Public Administration |

| Other End-User Industries |

| India |

| Bangladesh |

| Pakistan |

| Sri Lanka |

| Rest of South Asia |

| By Offering | Software |

| Services | |

| By Deployment Mode | Cloud |

| On-Premises | |

| Hybrid | |

| By Organization Size | Large Enterprises |

| Small and Medium Enterprises | |

| By Application | Customer Data Collection and Profile Unification |

| Audience Segmentation and Personalization | |

| Marketing Campaign and Customer Journey Orchestration | |

| Customer Analytics and Insights | |

| Consent and Preference Management | |

| Other Applications | |

| By End-User Industry | Retail and E-Commerce |

| Banking, Financial Services, and Insurance (BFSI) | |

| Healthcare and Life Sciences | |

| IT and Telecom | |

| Media and Entertainment | |

| Industrial Manufacturing | |

| Government and Public Administration | |

| Other End-User Industries | |

| By Country | India |

| Bangladesh | |

| Pakistan | |

| Sri Lanka | |

| Rest of South Asia |

Key Questions Answered in the Report

How large is the South Asia customer data platform market in 2026?

The South Asia customer data platform market stands at USD 0.53 billion in 2026 and is projected to reach USD 2.39 billion by 2031 at a 35.15% CAGR.

What is driving adoption across South Asia?

Stronger demand for consented first-party data, India’s 2025 DPDP Rules, rising omnichannel engagement complexity, and broader use of AI in customer decisioning are driving adoption.

Which deployment model leads today, and which one is growing the fastest?

Cloud led with 69.53% revenue share in 2025, while hybrid is projected to grow the fastest at a 36.19% CAGR through 2031.

Which buyer group is expanding the fastest?

SMEs are projected to grow at a 35.87% CAGR through 2031 as cloud-native delivery, modular onboarding, and lower entry barriers improve access.

Which application area is seeing the fastest growth?

Audience Segmentation and Personalization is projected to grow at a 36.82% CAGR, showing that buyers are moving beyond data collection into direct activation and engagement use cases.

Why does India dominate regional demand?

India held 78.67% of regional revenue in 2025 and is projected to grow at 36.91% through 2031 because it combines stronger enterprise digitization, a deeper vendor base, and a clearer regulatory push.

Page last updated on: