South America Wealth Management Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

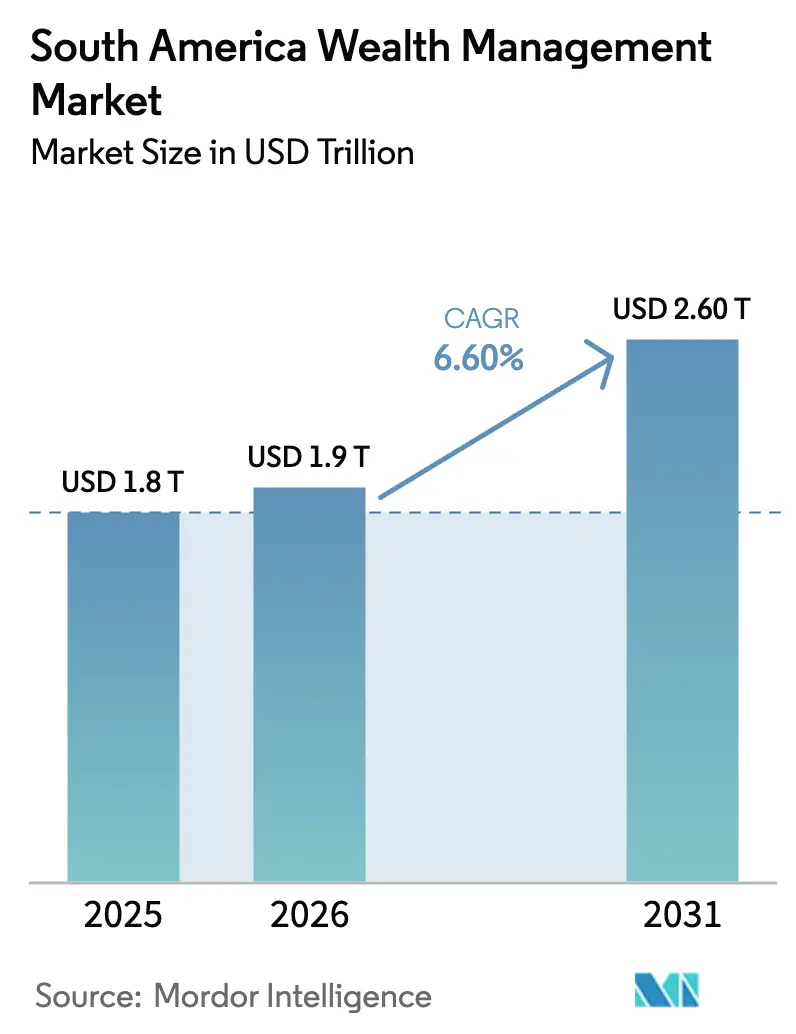

| Base Year Market Size (2025) | USD 1.8 Trillion |

| Market Size (2026) | USD 1.9 Trillion |

| Market Size (2031) | USD 2.60 Trillion |

| Growth Rate (2026 - 2031) | 6.60% CAGR |

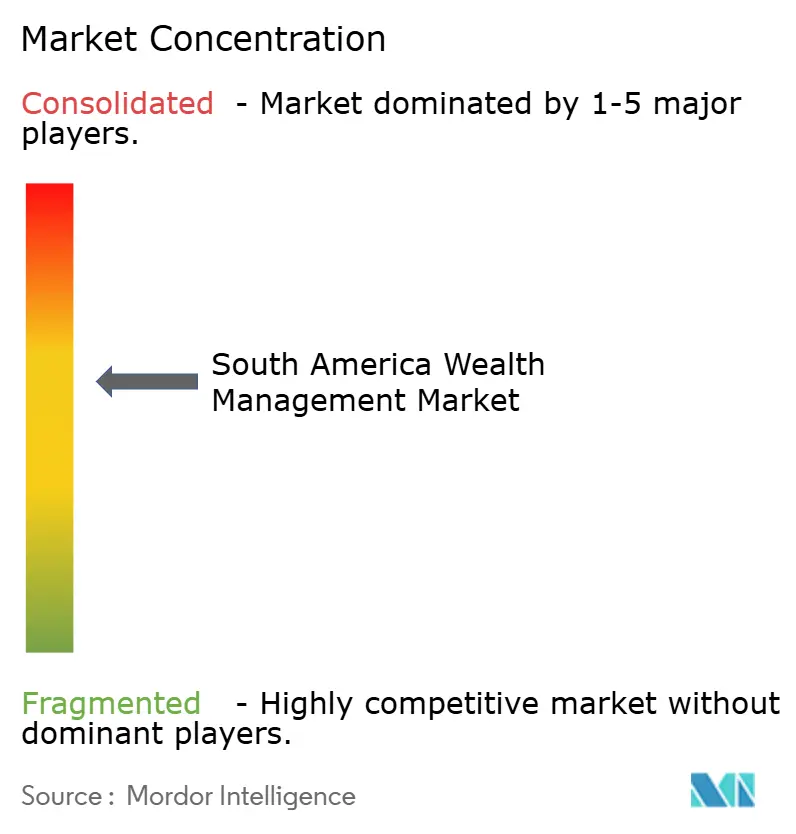

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South America Wealth Management Market Analysis by Mordor Intelligence

The South America Wealth Management Market size is expected to grow from USD 1.8 trillion in 2025 to USD 1.9 trillion in 2026 and is forecast to reach USD 2.60 trillion by 2031 at 6.60% CAGR over 2026-2031.

The South America wealth management market is anchored by regulatory modernization, digital distribution, and deepening advisory adoption across client tiers. Wealth platforms are aligning to Open Finance frameworks that enable data sharing and, when investment portability arrives at scale, lower switching frictions that favor advice-led relationships and broader product penetration. Portfolio construction is shifting as clients respond to high domestic rates in Brazil that pulled assets into fixed income while alternatives scale through private credit and infrastructure funds that deliver higher spreads at controlled default rates. Firms with credible cross-border capabilities are capturing fee-rich offshore mandates as tax reform and diversified booking centers make advisory on global allocations more complex and valuable. Consolidation among universal banks and specialist multifamily offices raises competitive benchmarks on scale, product breadth, and technology investment across the South America wealth management market.

Key Report Takeaways

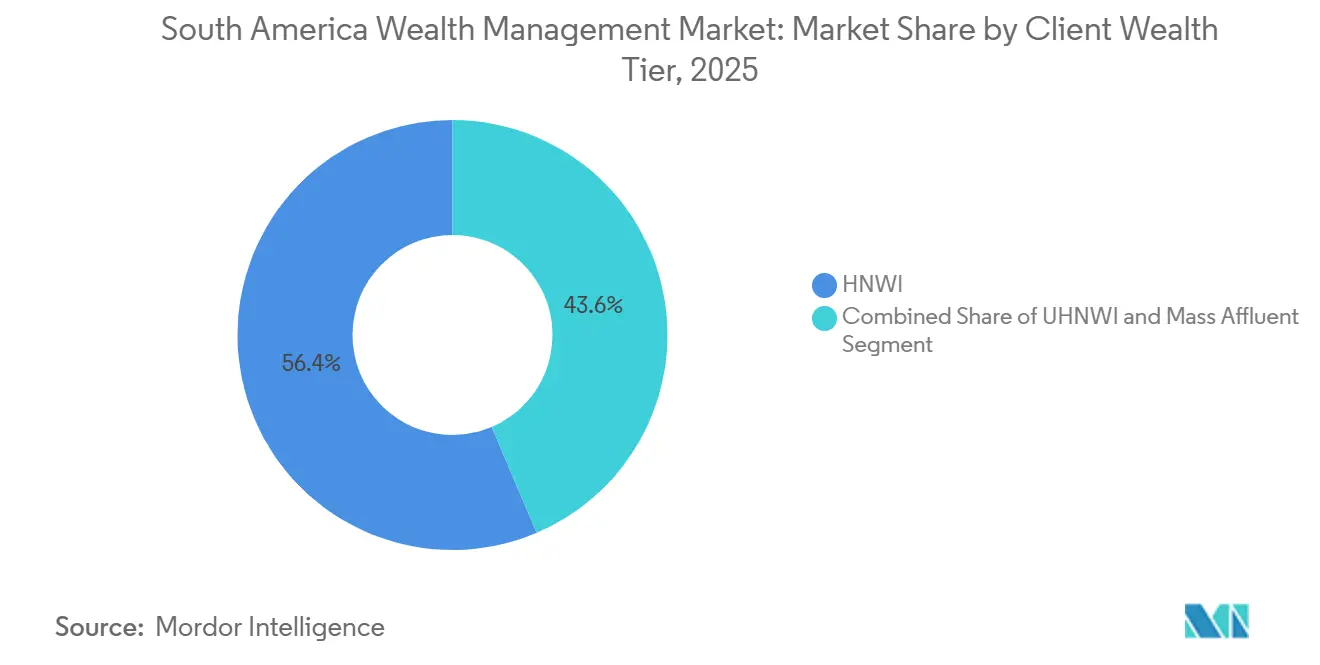

- By client wealth tier, high-net-worth individuals accounted for 56.4% of the assets of the South America wealth management market in 2025. The mass-affluent segment is projected to grow at a 9.4% CAGR to 2031.

- By firm type, private banks held an 82.7% share of the South America wealth management market in 2025. Family offices are expected to post the fastest 11.2% CAGR through 2031.

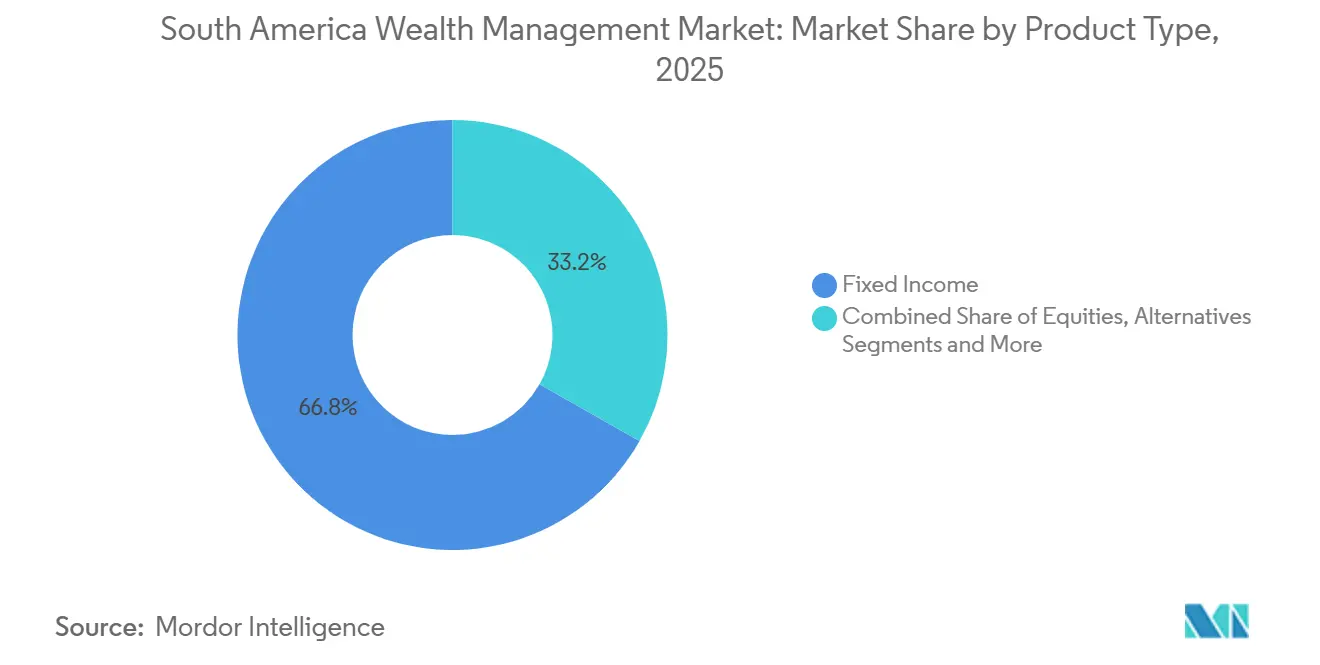

- By product type, fixed income captured 66.8% of the South America wealth management market in 2025. Alternatives are projected to advance at a 13.7% CAGR through 2031.

- By geography, Brazil led with 75.9% of the South America wealth management market share in 2025. Peru is forecast to expand at an 11.2% CAGR through 2031, the fastest among regional markets.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

South America Wealth Management Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Open Finance enables scalable digital wealth | +2.1% | Brazil operational, Chile 2027–2029 rollout | Medium term (2–4 years) |

| Yield rotation anchors AuM growth | +1.9% | Brazil dominant, Chile and Peru moderate | Short term (≤ 2 years) |

| Cross-border diversification lifts advisory revenues | +1.6% | Brazil, Chile, Peru, Argentina offshore demand | Medium term (2–4 years) |

| Family-office professionalization boosts UHNW demand | +1.4% | Brazil leading, Chile and Peru emerging | Long term (≥ 4 years) |

| Tax reform drives portfolio replatforming | +1.2% | Brazil primary, Argentina evolving, Chile stable | Short term (≤ 2 years) |

| Private credit expands advised allocations | +1.0% | Brazil dominant, Andean cross-border mandates | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Open Finance Enables Scalable Digital Wealth

Brazil’s Open Finance now serves 52 million clients with 103 million active data-sharing authorizations across more than 700 institutions and processes 3.5 billion data requests weekly as of September 2025[1]Banco Central do Brasil, “Open Finance Ecosystem Data and Investment Portability Workstreams,” Banco Central do Brasil, bcb.gov.br . Investment and salary portability are the next milestones, with the central bank coordinating with securities regulators to enable asset transfers without liquidation, a change expected to lower switching frictions while protecting client tax lots. Platforms that already embed pre-integration APIs and comprehensive planning tools are monetizing data aggregation. Outside Brazil, Chile’s formal Open Finance rulemaking positions the country for a 2027–2029 go-live, creating an interoperable environment that can extend digital onboarding and portability benefits to South American investors. Adoption still faces a trust gap because fewer than half of eligible Brazilian accounts opted into sharing, even with Open Finance at scale, which currently advantages incumbents with brand equity and robust security practices. As portability matures, advisory-led models within the South America wealth management market should gain share due to seamless rebalancing and cross-institution product comparability.

Yield Rotation Anchors AuM Growth

Brazil’s SELIC ended 2025 at 15%, which reinforced a migration into fixed income and supported USD 14.9 billion in net inflows to fixed-income funds during FY2025, within USD 1.9 trillion in total fund AuM that grew 15.2% year over year[2]ANBIMA, “Fund Flows and Category Performance, FY2025,” ANBIMA, anbima.com.br . Free duration and free credit categories together gained USD 26.2 billion in positive flows as wealth managers emphasized carry strategies and real yields above 5% after inflation. BTG Pactual closed 2025 with USD 219.1 billion in wealth assets and USD 38.0 billion in net new money, citing breadth in fixed-income solutions that layered duration and credit exposure to stabilize returns. The same dynamic raises reinvestment risk if rate easing resumes in 2026 or 2027, which would encourage rebalancing toward equities and alternatives unless portfolios are proactively positioned in blended strategies. XP Inc. reflected this shift as fixed income overtook equities in retail revenue, while the company grew loans to USD 11.9 billion and retirement assets to USD 14.4 billion to diversify income sources. Argentina presents a different pathway, where policy recalibration and a currency band of USD 0.7 to USD 1.0 per USD equivalent range guide a cautious rebuild of risk assets with a preference for dollar-linked structures.

Cross-Border Diversification Lifts Advisory Revenues

Only 30% of South American family-office investments remain within the region, a share that underscores how policy and currency risk push UHNW allocations offshore and increase the value of cross-border structuring advice[3]Julius Baer, “Global Family Barometer 2025,” Julius Baer, juliusbaer.com . Brazil’s framework for fund structures permits up to 100% allocation to foreign assets, and the local fund industry reported USD 46.2 billion in foreign investments at the fund level, which excludes private-banking offshore mandates. BTG Pactual accelerated its offshore platform by adding books in Miami and New York, aligning with a strategy to capture fee-rich cross-border mandates that typically carry higher advisory spreads than domestic fixed income. Brazil’s December 2025 tax reform introduced a 10% levy on foreign-sourced profits and dividends and interacts with rules that tax offshore income annually, which is prompting portfolio replatforming into treaty-protected or onshore-advantaged vehicles. UBS formed a dedicated Global Wealth Management South America unit and completed the migration of most ex-Swiss Credit Suisse assets by late 2024, reinforcing that cross-border capabilities are now core to competitive positioning in the South America wealth management market.

Family-Office Professionalization Boosts UHNW Demand

Family-office adoption in South America sits at 38% of UHNW families, below Asia’s 43%, yet the number of single-family offices has surged, signaling a structural shift toward institutional governance and specialized services. The change is tied to generational wealth transfer and the complexity of multijurisdictional portfolios that outstrip the capacity of generalist private banking teams. BTG Pactual became Brazil’s largest multifamily office by consolidating Julius Baer Brasil’s USD 11 billion family-office AuM, JGP’s USD 3.4 billion, and M.Y. Safra’s USD 391 million in mandates through 2025. Mass-affluent households that exhibit family-office behaviors but sit below the UHNW scale are being onboarded into comprehensive planning frameworks, as XP Inc. shows higher inflows and cross-sell when assets exceed the ~USD 54,200 threshold. Brazil’s central bank is advancing investment portability within Open Finance, which would let family offices switch custodians without liquidating positions and lower operational stickiness in the South America wealth management market. Trust frictions remain a hurdle because only 103 million authorizations are active among 52 million Open Finance users, and many UHNW families are selective about data sharing even under a regulated framework.

Restraints Impact Analysis*

| Restraint | % Impact on CAGR | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility suppresses risk appetite and inflows | -1.8% | Argentina (acute currency/policy volatility), Brazil (political uncertainty), Chile and Peru (commodity exposure) | Short term (≤ 2 years) |

| Fee compression pressures platform profitability | -1.3% | Brazil (digital disruptors), Chile (Open Banking preparation), regional competition from neobanks | Medium term (2–4 years) |

| Open Finance trust gaps slow portability | -0.9% | Brazil (fewer than 50% eligible accounts opted in), Chile and Colombia (early adoption phase) | Medium term (2–4 years) |

| Tax-regime fluidity raises compliance friction | -0.7% | Brazil (Law 15,270/2025 implementation complexity), Argentina (IMF-linked fiscal adjustments), regional divergence | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Tax Reform Drives Portfolio Replatforming

Brazil enacted Law 15,270/2025 in December 2025, which raised monthly income-tax exemptions to USD 879 and annual exemptions up to USD 10,549 for lower-income filers, while introducing a 10% rate on foreign profits and dividends and a minimum-tax mechanism for high-income dividend recipients. The update interacts with Law 14,754/2023, which applies annual taxes up to 15% on income from offshore investments that are tied to Brazil, which is now pushing wealth managers to reconfigure vehicles toward tax-advantaged domestic options or treaty-aligned structures. Itaú Private Bank is channeling sustainable-finance mandates as part of a plan to mobilize USD 175.8 billion by 2030 and has recommended 1% to 3% Bitcoin allocations for diversification since December 2025 within a controlled risk framework. The minimum-tax design raises planning complexity because advisors must model total taxable income before recommending dividend withdrawal strategies and entity choices. Argentina’s IMF program sets fiscal targets that affect tax and capital-account policies, and with no harmonized dividend or wealth-tax guidance published in 2025, long-term after-tax projections remain challenging for repatriation scenarios. Chile’s regulator is focused on Basel III Pillar 2 implementation, which may indirectly influence leverage-driven strategies that rely on bank intermediation for private-banking clients.

Private Credit Expands Advised Allocations

South America’s corporate credit system is about USD 2.3 trillion in size, while private credit remains below 1% penetration, creating structural headroom for intermediated lending in the South America wealth management market. Patria Investments deployed USD 3.1 billion across more than 210 transactions spanning seven countries and closed its first dedicated private credit fund with USD 314 million in commitments while reporting a 15.6% gross unlevered IRR. The asset class still offers spreads of 100 to 150 basis points over US high yield with lower observed default rates, and leading wealth desks recommend 5% to 20% sleeves depending on liquidity needs and client goals. Performance dispersion is widening across managers, which elevates due diligence demands and suitability controls for wealth platforms that onboard clients into 3 to 5-year lockups. BTG Pactaual’s AuM growth to a multi-trillion reais scale includes an expanding private credit platform, though allocations remain a mid-single-digit share of total mandates as advisors pace client education around illiquidity and covenants. Local rules continue to evolve valuation, disclosure, and fiduciary responsibilities, and managers rely on quota fund structures while regulators refine standardized guidance for private credit vehicles.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Client Wealth Tier: Mass Affluent Gains Through Digital Onboarding

High-net-worth individuals accounted for 56.4% of total assets in 2025, reinforcing that upper wealth tiers anchor fee pools in the South America wealth management market. The mass-affluent cohort is expanding fastest with a 9.6% CAGR to 2031 as digital onboarding and Open Finance aggregation cut acquisition costs and enable scaled financial planning. UHNW households, though fewer in number, drive high-touch mandates that include succession planning, philanthropy structuring, and co-investments that stretch beyond the capacity of standard relationship teams. Family-office adoption, at 38% of UHNW families in South America, continues to rise as governance needs grow and portfolios span multiple jurisdictions with varied tax and reporting regimes.

The South America wealth management market is also widening access to alternative investments once limited to UHNW clients, including private credit sleeves in the 5% to 20% range, depending on liquidity profiles. Regulatory support for data portability should further normalize advice-led distribution as clients move providers without forced liquidations once investment portability is launched. The South America wealth management market size for this segment is set to benefit from rules that raise disposable income and enhance digital trust, which can redirect savings into advisory channels. As Open Finance matures in Chile and consumer protections advance in Peru, spillover effects from Brazil’s digital playbook are likely to expand the adviceable base.

By Firm Type: Family Offices Scale Amid Private Bank Dominance

Private banks held 82.7% of assets in 2025, reflecting the distribution power of Brazil’s universal banks that plug wealth offerings into retail deposits, lending, and custody. Family offices are growing at an 11.2% CAGR through 2031 as UHNW clients institutionalize governance and cross-border strategies beyond the scope of generalist private banking. Independent and external asset managers are also using transparency and portability to compete on specialized mandates without bearing the full cost of proprietary custody infrastructure. Households are seeking curated access to alternatives, structured solutions, and global custody, which benefits firms that assemble multi-jurisdiction platforms and tax-optimized vehicles. BTG Pactual’s roll-up of Julius Baer Brasil, JGP, M.Y. Safra, and Greytown shows how M&A can accelerate a shift toward multifamily-office scale within the South America wealth management market.

Private banks are countering by broadening product menus and upgrading advice layers that tie clients to managed accounts while leveraging their lending capabilities for securities-backed finance. Sustainable-finance mobilization targets and the introduction of crypto as a diversifier in model portfolios illustrate how incumbents are defending share in fee-accretive categories. The South America wealth management market size for family-office mandates is projected to rise as open-architecture fund rules enable 100% cross-border allocations through domestic vehicles, which simplifies reporting while keeping custody onshore[4]Comissão de Valores Mobiliários, “ESG Disclosure Standards and Cross-Border Rules,” CVM, cvm.gov.br. Open Finance investment portability can reduce the stickiness of custodial relationships and shift competition toward planning depth and alternative access rather than pure product distribution. These changes create a more level field where boutiques can win on expertise while banks compete on breadth and balance sheet.

By Product Type: Alternatives Gain as Fixed Income Normalizes

Fixed income accounted for 66.8% of allocations in 2025, supported by Brazil’s 15% SELIC as clients sought real yields above inflation. Alternatives are the fastest-growing sleeve at a projected 13.7% CAGR through 2031 as private credit, real assets, and hedged strategies spread from UHNW to HNW and mass-affluent tiers. Equities remain part of strategic plans, but volatility tied to commodities and macro policy creates episodic redemption pressure in Chile, Peru, and Argentina that can slow net inflows without complementary downside buffers. Cash and deposits continue to serve as tactical shock absorbers, though advisors often rotate clients into money-market funds or ultra-short duration mandates to maintain optionality without surrendering too much carry. As rates stabilize or decline, the South America wealth management market is likely to see incremental rebalancing from pure fixed income toward alternatives and equities that offer risk premiums and diversification.

Private credit illustrates the return profile driving this shift, with leading managers reporting 15.6% gross unlevered IRRs and spreads 100 to 150 basis points above US high yield, coupled with conservative leverage and strong interest coverage. The South America wealth management market size tied to alternatives will also benefit from standardized ESG disclosures under IFRS S1 and S2 that improve comparability for infrastructure and renewable funds. Brazil’s virtual-asset resolutions clarify custody and compliance, enabling wealth desks to incorporate crypto exposures in tightly risk-managed sleeves where suitability and operational controls are robust. Itaú’s 1% to 3% Bitcoin allocation guidance for model portfolios shows how incumbents are adding uncorrelated exposures to reduce drawdowns during periods of equity stress. As Open Finance deepens, execution will be commoditized, which should steer product-led competition toward advice and outcomes rather than transactional pricing.

Geography Analysis

Brazil accounted for 75.4% of the South America wealth management market in 2025, supported by the region’s most advanced Open Finance system with 52 million clients, 103 million authorizations, and 3.5 billion weekly data calls. Peru is the fastest-growing market at an expected 11.2% CAGR through 2031, supported by HNWI formation linked to mining and by strengthening platforms that cross-sell to corporate clients and deploy alternatives. Chile maintains a well-developed wealth ecosystem and is preparing a 2027–2029 Open Finance rollout that should enable portability-driven competition against Brazilian incumbents. Argentina remains a smaller market because currency and policy volatility keep long-term peso allocations subdued, which sustains client preference for dollar-linked instruments and offshore custody. In the rest of South America, global players with multi-local footprints are relevant for UHNW clients who prioritize cross-border diversification and treaty-aware advisory.

Growth dynamics have accelerated as Open Finance frameworks, tax reform, and private credit penetration reinforce advice-led portfolios in the South America wealth management market. In Peru, mining-linked income and diversified AuM platforms support broadening allocations and cross-border mandates in a market that is still consolidating. Chile’s moderate rate environment reduces headline fixed-income attraction but sets the stage for portable account architectures that will increase price transparency and product comparability. Argentina’s IMF program defines a path to stabilization and could unlock re-risking by local UHNW investors if the currency regime normalizes, though advisors will likely maintain a conservative tilt until inflation is anchored. Regional expansion by Brazilian platforms is rising, including steps toward new licenses and booking centers that position firms to serve clients across borders with consistent advice layers.

Brazil’s rule set integrates cross-border allocations under local vehicles and clarifies crypto custody, which gives domestic platforms competitive tools to retain assets onshore while delivering global exposures. The South America wealth management market size in Brazil will remain dominant due to scale benefits in technology and product manufacturing that are hard to replicate in smaller markets. Peru’s faster growth rate reflects earlier-stage digital penetration that has room to catch up as Open Finance concepts extend beyond Brazil. Chile’s steady regulatory posture supports innovation within a predictable policy framework, while Argentina presents optionality if stabilization gains credibility. Global franchises like UBS and Santander will continue to compete for UHNW flows that require cross-border coordination and treaty-aware structuring.

Competitive Landscape

The South America wealth management market exhibits high concentration, with the top five franchises in Brazil and the broader region exerting outsized influence over distribution, product origination, and custody networks. Industry bodies also note that the largest asset managers hold a substantial share of total fund AuM, reflecting the advantages of operating scale and integrated ecosystems that combine deposits, lending, and securities services. Consolidation accelerated through 2025 as BTG Pactual acquired Julius Baer Brasil’s USD 11 billion family-office AuM, JGP’s USD 3.4 billion, M.Y. Safra’s USD 391 million, and Greytown’s USD 1 billion offshore book. UBS, after integrating Credit Suisse’s regional business, established a standalone Global Wealth Management South America unit to sharpen its competitive focus. XP Inc. built a scaled digital franchise with a record-low efficiency ratio and rising client assets by pairing comprehensive planning with an open-architecture product shelf.

Strategy has bifurcated between digital-first and universal-bank models across the South America wealth management market. Digital leaders emphasize planning, automation, and transparent pricing, while universal banks defend share with lending, custody synergies, and deep product menus that now include structured solutions and alternatives. BTG Pactual’s record results in 2025 reflected strong net new money and operating leverage gained from M&A and platform scale. Sustainable-finance pipelines are a differentiator for incumbents that mobilize large balance sheets to channel tax-advantaged infrastructure and ESG-linked instruments. Private credit, still below 1% of the regional corporate credit market, is emerging as a cross-firm priority due to attractive risk-adjusted spreads and a growing opportunity set.

Regulation is both a moat and a catalyst in the South America wealth management market. Brazil’s virtual-asset resolutions clarify custody and compliance, while Chile’s Open Finance roadmap brings portability and transparency into scope. CVM’s adoption of IFRS-aligned ESG reporting standards reduces information asymmetry for private-market funds and supports scale in sustainable investing. Platforms that bundle planning and protection around an open product shelf are winning a higher share of wallet, as evidenced by XP’s inflow and cross-sell metrics at mass-affluent thresholds. Cross-border capabilities remain decisive because only a minority of family-office allocations stay in-region, and Brazil’s tax updates make treaty-aware structures and multi-booking-center orchestration more valuable.

South America Wealth Management Industry Leaders

Itaú Private Bank

BTG Pactual Wealth Management

Bradesco Private Bank

Banco do Brasil Private

Santander Private Banking

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: BTG Pactual secured a full US banking license, acquired JGP’s USD 3.4 billion AuM, purchased M.Y. Safra’s USD 391 million New York book and Greytown’s USD 1 billion Miami assets, and issued USD 750 million in 5-year senior notes at 5.5% yield.

- December 2025: Itaú Asset Management recommended 1% to 3% Bitcoin allocations for 2026 model portfolios and established a dedicated crypto division in September 2025, with plans to expand products for private-banking clients.

- March 2025: BTG Pactual completed the acquisition of Julius Baer Brasil Gestão de Patrimônio, purchasing USD 11 billion in family-office assets under management for CHF 91 million (USD 115 million) in cash, consolidating its position as Brazil’s largest multifamily office

- March 2025: Itaú Unibanco partnered with IFC and IDB Invest to structure a USD 280 million biodiversity and social bond, advancing a plan to mobilize USD 184.4 billion in sustainable finance by 2030.

South America Wealth Management Market Report Scope

| UHNWI |

| HNWI |

| Mass Affluent |

| Private Banks |

| Family Offices |

| Others (Independent/External Asset Managers) |

| Fixed Income |

| Equities |

| Alternatives |

| Cash and Deposits |

| Others |

| Brazil |

| Peru |

| Chile |

| Argentina |

| Rest of South America |

| By Client Wealth Tier | UHNWI |

| HNWI | |

| Mass Affluent | |

| By Firm Type | Private Banks |

| Family Offices | |

| Others (Independent/External Asset Managers) | |

| By Product Type | Fixed Income |

| Equities | |

| Alternatives | |

| Cash and Deposits | |

| Others | |

| By Geography | Brazil |

| Peru | |

| Chile | |

| Argentina | |

| Rest of South America |

Key Questions Answered in the Report

What is the current size and growth outlook for the South America wealth management market?

The South America wealth management market size is USD 1.9 trillion in 2026 and is projected to reach USD 2.64 trillion by 2031 at a 6.6% CAGR.

Which client tier is expanding fastest within South America wealth management?

The mass-affluent segment is growing the fastest at a projected 9.5% CAGR to 2031, driven by digital onboarding and Open Finance data aggregation that scale financial planning.

Which geography leads and which is growing fastest across South America wealth management?

Brazil leads with 75.4% of the South America wealth management market in 2025, while Peru is forecast to grow at 11.2% through 2031.

How is regulation influencing competition in South America wealth management?

Open Finance, cross-border fund rules, and virtual-asset custody standards are lowering switching frictions and clarifying product frameworks, which push firms to compete on advice and outcomes rather than execution alone.

Which firms have recently made notable strategic moves in South America wealth management?

BTG Pactual consolidated multi-family office mandates through acquisitions, XP Inc. scaled planning-led distribution with record efficiency, and UBS formed a dedicated Latin America wealth unit post-integration.

What product category is gaining the most momentum in South America wealth management?

Alternatives are scaling fastest with a 13.7% projected CAGR, as private credit, real assets, and hedged strategies complement fixed income, which held 66.8% of 2025 allocations.

Page last updated on: