South America Textile Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

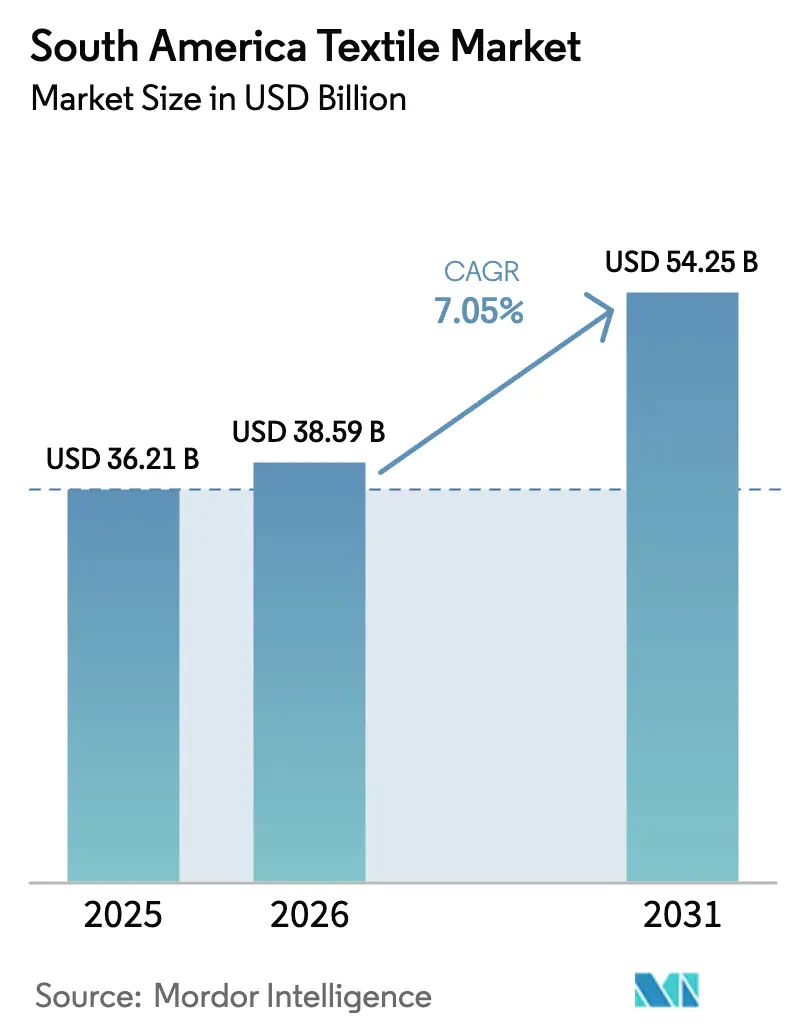

| Base Year Market Size (2025) | USD 36.21 Billion |

| Market Size (2026) | USD 38.59 Billion |

| Market Size (2031) | USD 54.25 Billion |

| Growth Rate (2026 - 2031) | 7.05% CAGR |

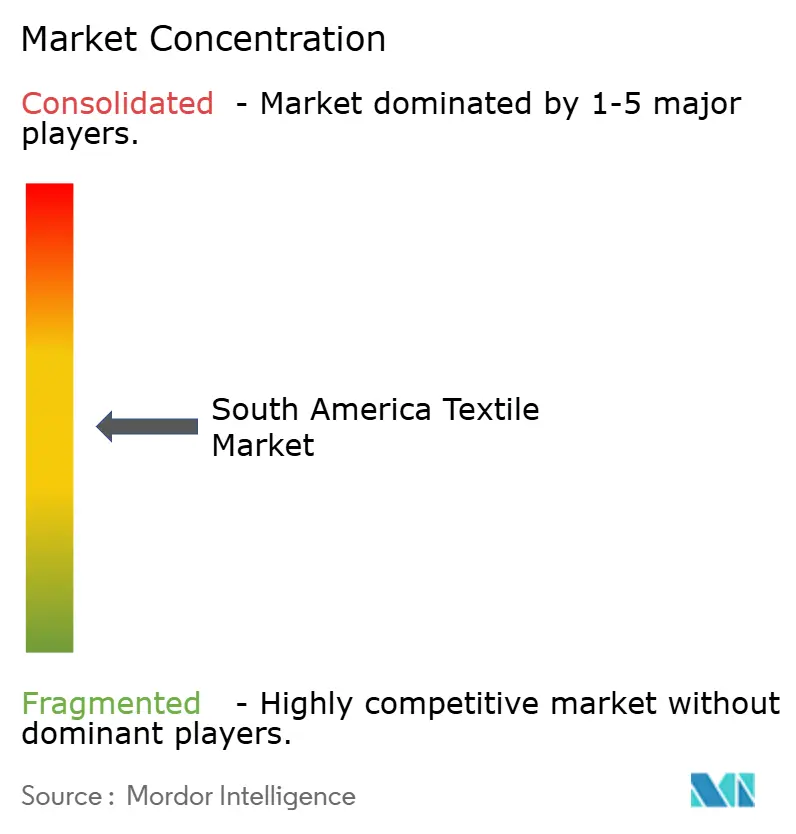

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

South America Textile Market Analysis by Mordor Intelligence

The South America Textile Market size is projected to expand from USD 36.21 billion in 2025 and USD 38.59 billion in 2026 to USD 54.25 billion by 2031, registering a CAGR of 7.05% between 2026 to 2031.

Benefits from apparel demand in Brazil and Argentina now overlap with structural gains in geotextiles, hygiene nonwovens, and recycled-polyester fiber, broadening the revenue base beyond fashion. Higher European circular-economy standards accelerated investment in traceable supply chains and Digital Product Passport pilots, positioning compliant exporters for tariff-free access to the EU. Foreign direct investment from Lenzing and Indorama secures regional feedstock, strengthens recycling infrastructure, and shields multinationals from cotton-price swings. At the same time, São Paulo’s informal hubs cut design-to-shelf cycles to under 14 days, forcing formal mills to adopt on-demand manufacturing or risk erosion of their share. Energy-price volatility, especially Brazil’s 12% electricity hike in 2025, continues to pressure dyeing and finishing margins.[1]UNECE. "Digital Product Passport Pilot Program." Accessed February 2026. https://unece.org

Key Report Takeaways

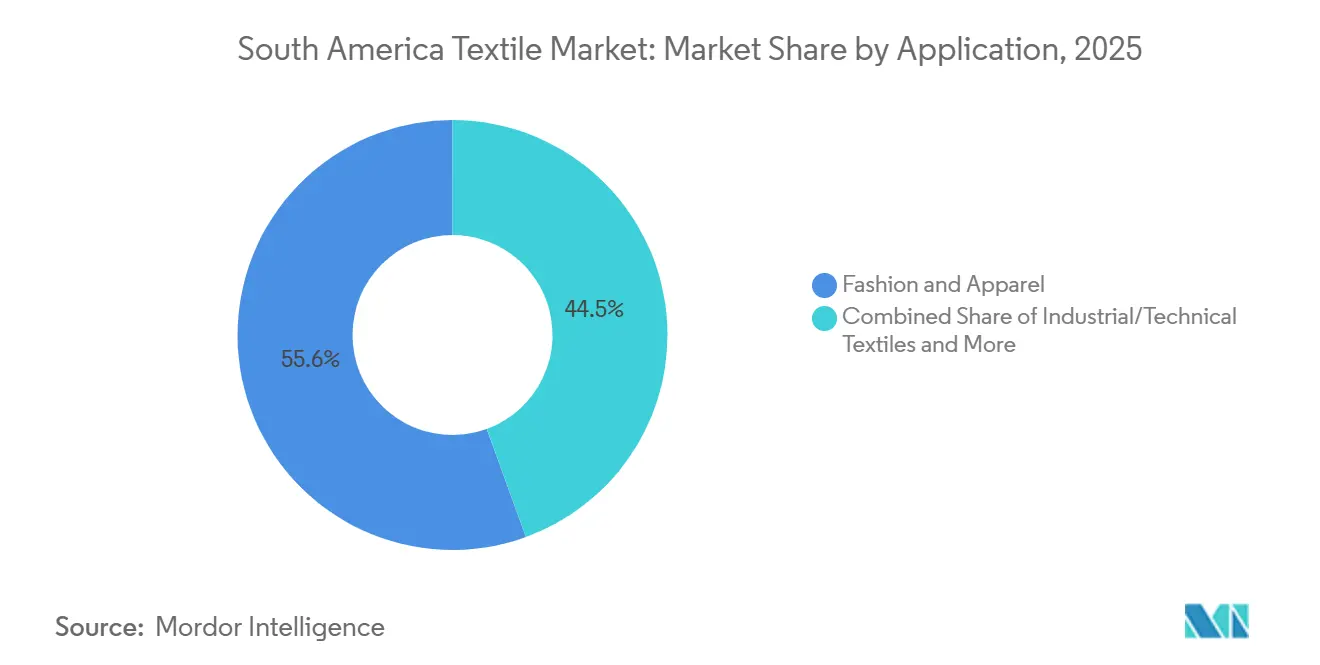

- By application, Fashion & Apparel commanded 55.55% of 2025 revenue, while Industrial/Technical Textiles is set to expand at a 6.15% CAGR through 2031.

- By raw material, Synthetic fibers held a 52.55% share in 2025; polyester is forecast to grow 6.56% annually, the fastest of all fiber types.

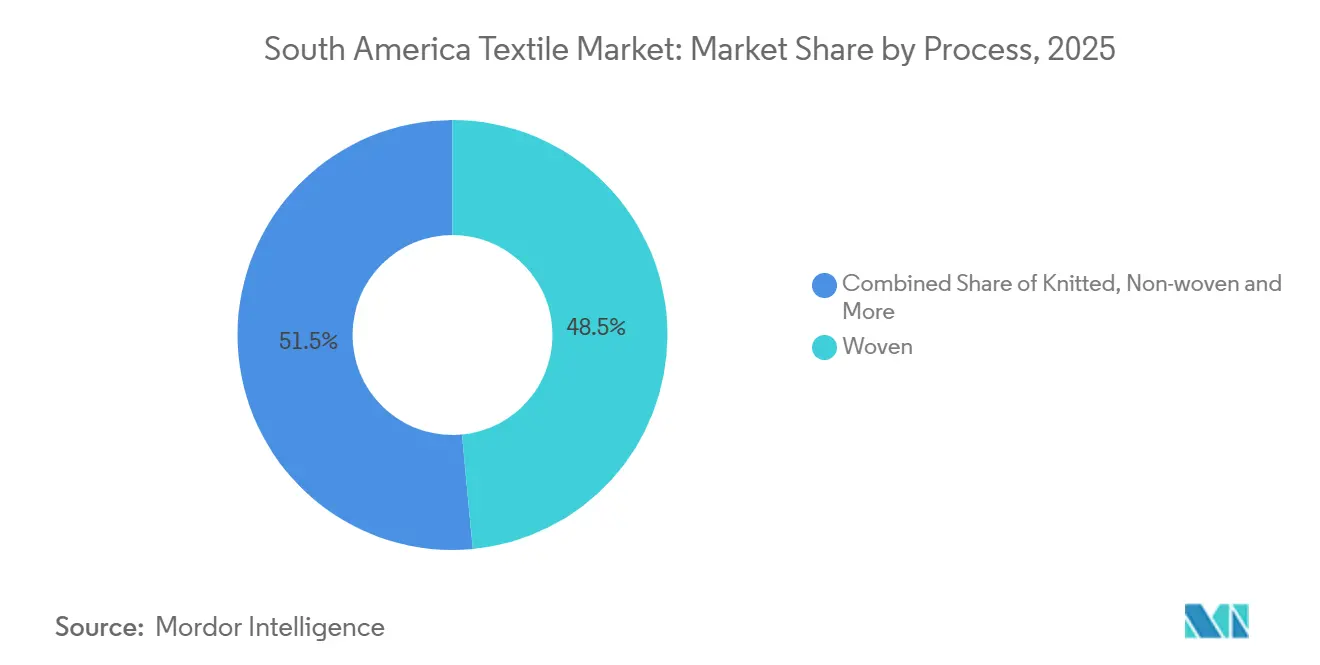

- By process, Woven fabrics accounted for 48.5% of 2025 sales, but Nonwovens will advance at a 6.05% CAGR driven by hygiene and automotive demand.

- By geography, Brazil led with 48.5% of 2025 revenue, whereas Argentina is projected to record the quickest 5.8% CAGR over 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Proportional positioning is established by comparing regional contributions against the global total, including that of South america. The textile market share in our global report expresses these relative weights.

South America Textile Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Uptake of technical textiles in regional mobility and infrastructure | +1.5% | Brazil (infrastructure projects), Argentina, Rest of South America | Long term (≥ 4 years) |

| Fast-fashion cycles and on-demand manufacturing | +1.2% | Brazil (São Paulo, Rio de Janeiro), Argentina (Buenos Aires) | Short term (≤ 2 years) |

| E-commerce and social-commerce compressing design-to-shelf time | +1.1% | Brazil, Argentina, with spillover to Peru | Short term (≤ 2 years) |

| Mandatory EU-27 separate textile-waste collection (2025) | +0.9% | Brazil, Argentina, Peru (export-oriented producers) | Medium term (2-4 years) |

| Surging investor interest in low-impact South-American natural fibers | +0.8% | Peru (alpaca, organic cotton), Argentina (wool), Brazil (organic cotton) | Medium term (2-4 years) |

| Blockchain-enabled Digital Product Passport pilots in MERCOSUR | +0.6% | Argentina, Brazil, Chile, Paraguay, Peru (UNECE pilot countries) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Uptake of Technical Textiles in Regional Mobility & Infrastructure

Brazil’s 2024-2030 infrastructure plan earmarks USD 56 billion for transport upgrades, many of which require nonwoven geotextiles that meet ASTM standards. Demand for high-tenacity polyester fabrics in Argentina’s Vaca Muerta shale projects rose 19% in 2025, reflecting stricter environmental protocols. Peru’s mining sector is now specifying tailings-dam reinforcement fabrics, attracting European suppliers through Lima distributors. Enforcement of engineering standards, such as Brazil’s ABNT NBR 12553, tilts procurement toward certified local producers. Consistent inspection remains critical, as lax oversight previously let substandard imports undercut compliant products.[2]World Bank. "Brazil Infrastructure and Logistics Costs Analysis." Accessed February 2026. https://www.worldbank.org

Fast-Fashion Cycles and On-Demand Manufacturing

Informal clusters in Sao Paulo’s Bras district and Buenos Aires’ La Salada market turn social-media trends into finished garments within two weeks. Micro-factories combine cutting, sewing, and finishing on a single site, bypassing wholesalers and selling on Instagram or WhatsApp. By 2025, these informal operations produced 38% of Brazil’s domestic apparel volume, underscoring their scale. Formal mills answer with digital printing and modular lines that trim minimum orders to 50 units, yet still struggle to match the agility without compromising traceability. Tension between speed and compliance will rise as EU buyers demand verified labor standards, pushing informal players either toward legalization or toward shrinking export avenues.[3]Government of Brazil. "Ministry of Economy Informal Textile Production Report 2024." Accessed February 2026. https://www.gov.br

E-Commerce and Social-Commerce Compressing Design-to-Shelf Time

Brazil’s online textile sales jumped 22% in 2025 on platforms that merge live-stream launches with same-day delivery. Small brands exploit influencer reach to test micro-collections, reducing forecasting errors and unsold stock. Argentine cooperatives dye base garments only after social-commerce pre-orders materialize, cutting dead inventory by 40%. This model raises working-capital needs for yarn and greige fabric but rewards vertically integrated mills such as Vicunha that command upstream capacity. Real-time feedback loops also shorten product lifecycles, intensifying pressure on mills to automate patterning and cutting.

Mandatory EU-27 Separate Textile-Waste Collection (2025)

The EU rule obliging members to collect textiles separately from municipal waste now acts as a de facto technical barrier for South American exporters. Buyers in Spain and Portugal insist on mono-material designs and recyclable dyes, inflating production costs by up to 12% but securing market access. Chile’s parallel draft law on extended producer responsibility signals that the compliance wave will spread regionally. Early adopters that re-engineer products for recyclability gain pricing power and longer contract tenures, while laggards face order cancellations and excess finished-goods inventory.[4]European Commission. "Waste Framework Directive - Separate Textile Collection." Accessed February 2026. https://ec.europa.eu

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile energy and raw-material prices | -1.4% | Brazil, Argentina (energy-intensive dyeing and finishing) | Short term (≤ 2 years) |

| High capex for advanced recycling / sorting capacity | -0.9% | Brazil, Argentina (SME-dominated markets) | Medium term (2-4 years) |

| SME fragmentation vs. new ESG / due-diligence compliance | -0.8% | Brazil, Argentina (fragmented producer base) | Long term (≥ 4 years) |

| Skilled-labor shortages (dyeing, finishing, automation) | -0.7% | Brazil, Argentina, Peru | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatile Energy and Raw-Material Prices

A 12% rise in Brazilian electricity tariffs during 2025 deepened margin pressure for energy-intensive dyeing and stentering operations. Cotton prices in Argentina spiked 18% in 2024 after the Chaco droughts, forcing mills to import at a premium. Polyester costs mirror crude-oil swings with a 60-day lag, leaving mills exposed under fixed-price apparel contracts. Producers with vertically integrated recycling, such as Indorama’s São Paulo rPET facility, hedge against volatility in virgin resin prices. Firms lacking such buffers delay capex, risking obsolescence as buyers gravitate toward price-stable suppliers.

High Capex for Advanced Recycling / Sorting Capacity

A mechanical recycling line capable of handling 5 000 t per year requires at least USD 10 million in equipment and civil works, a sum beyond most regional SMEs. Chemical depolymerization of polyester demands multiples of that outlay, illustrated by Lenzing’s USD 66 million closed-loop upgrade in Bahia. Multinationals can amortize such investments across global footprints, but local mid-tier players depend on concessional loans. Brazil’s BNDES released USD 560 million in green credit lines in 2024, yet drawdown has been slow given collateral requirements. Without pooled collection networks, payback periods exceed 10 years, dampening adoption.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Technical Textiles Outpace Apparel Growth

The South America textile market share of Fashion & Apparel remains dominant at 55.55% yet slowing discretionary spend and mounting second-hand imports temper its pace. The industrial/Technical Textiles segment is advancing at a 6.15% CAGR, faster than any other application. Demand originates from civil-engineering geotextiles for Brazil’s USD 56 billion transport overhaul and filtration fabrics keyed to Peru’s mining sector. Apparel houses still invest in near-shoring to Argentina to avoid tariffs, but performance fabrics for oil, gas, and construction now capture a growing share of procurement budgets.

Technical textile producers bank on public procurement that mandates ASTM and ABNT certification, favouring mills with in-house labs. Local champions like Ober add ISO 9001 systems, while newcomers partner with German specialist HUESKER to deliver turnkey erosion-control solutions. Success hinges on the rapid commercialization of recycled-polyester geogrids that align with EU buyers’ sustainability scorecards. Apparel mills counter by embedding QR-coded traceability to justify higher price points, signalling that both segments will coexist but with converging technology platforms.

By Raw Material: Polyester Leads Synthetic Fiber Growth

Synthetic fibers held 52.55% of 2025 revenue. The South American textile market for Polyester is expanding at a 6.56% CAGR, fueled by Indorama’s São Paulo rPET capacity, which supplies both apparel and nonwovens. Cotton acreage contracted in Argentina as farmers pivoted to soy, eroding the natural-fiber supply; nevertheless, Brazilian organic-cotton acreage grew 15% in 2025 on European brand demand. Recycled fibers remain a small fraction but ride on EU circular-economy incentives, gradually cannibalizing virgin inputs.

Nylon and acrylic serve the hosiery and knitwear niches but face blended polyester substitution due to cost. Rayon/viscose from Lenzing’s Bahia site offers a semi-synthetic compromise that mimics cotton drape while retaining process economies. Specialty aramid and UHMWPE capture high-margin protective-gear orders for energy and defense customers, yet volumes stay marginal. Long-term, recycled polyester’s compatibility with mechanical and chemical loops secures its leadership, provided bottle-collection rates improve.

By Process/Technology: Nonwovens Gain on Woven Fabrics

Woven fabrics still accounted for 48.5% of 2025 sales, yet Nonwovens are posting a 6.05% CAGR as hygiene, filtration, and automotive segments swell. The South America textile market share of spunbond and meltblown nonwovens rose notably after Freudenberg’s 15% capacity expansion in São Paulo. Hydroentangled wipes and medical drapes add higher-margin outlets, though capex intensity confines supply to multinationals with regional hubs. Knitted fabrics keep a steady base in casualwear, but margin compression from Asian imports urges local mills to specialize in quick-turn fashion linked to e-commerce drops.

Emerging 3D weaving techniques for carbon-fiber preforms receive pilot attention in aerospace yet remain cost-burdened. Needle-punched nonwovens for automotive carpeting migrate incrementally from Europe as OEMs source locally to shave freight costs. Sustainability also favors spunlaid nonwovens, which generate less wastewater than dyeing woven cotton, aligning with BNDES-backed green-loan criteria. Over the forecast horizon, process diversification rather than substitution will characterize capital spending, with hybrid lines that toggle between woven and nonwoven outputs gaining favor.

Geography Analysis

Brazil accounted for 48.5% of the region’s 2025 textile revenue, thanks to its large domestic consumer base, petrochemical inputs, and port infrastructure. Federal green-credit lines worth USD 560 million encouraged mills to retrofit with waterless dyeing and energy-recovery systems, though pervasive road freight and port congestion add 10 days to export lead times. Foreign investors such as Lenzing and Indorama are deepening Brazil’s recycling and viscose capacity, insulating the supply chain from volatility in cotton and virgin-PET prices while satisfying EU traceability requirements. Rising electricity tariffs remain a near-term profit drag, but planned renewable additions may temper costs by 2027.

Argentina is positioned for a 5.8% CAGR between 2026 and 2031 as peso devaluation improves export price competitiveness. Textile production rebounded 11% in 2025, principally in Buenos Aires and Córdoba, enabling local apparel makers to win orders shifted from Asia. Inflation moderation remains critical to sustaining wage advantages. Wool output fell 8% in 2024 due to land conversion, yet technical-textile demand linked to the Vaca Muerta shale project grew 19% in 2025, balancing the raw-material shortfall. Government talks on partial export-tax relief could further stimulate capital inflows.

The combined markets of Peru, Chile, Colombia, and Uruguay contribute a smaller share of revenue but carry niche growth vectors. Peru’s alpaca-fiber exports climbed 12% in 2025 on luxury-brand demand for traceable, low-impact fibers, aided by ATPDEA trade preferences. Mining activity drives geotextile uptake for tailings management, attracting European niche players through local distributors. Chile’s influx of 124,000 t of second-hand clothing in 2024 prompted draft EPR laws, foreshadowing tougher import screening and a push for recycling capacity. Colombia leverages free trade agreements but still faces infrastructure bottlenecks that deter scale investments. Overall, regional heterogeneity offers multinationals scope to tailor strategies to currency regimes, logistical realities, and resource endowments.[3]Government of Brazil. "Ministry of Economy Informal Textile Production Report 2024." Accessed February 2026. https://www.gov.br

Mordor Intelligence examines the textile market across diverse other regional markets as well, including North America, Middle East, and Africa.

Competitive Landscape

Competition is moderately fragmented: more than 200 Brazilian SMEs compete with integrated multinationals in nonwovens, recycled fibers, and technical textiles. European specialists such as Freudenberg, Ahlstrom-Munksjo, and HUESKER establish joint ventures to circumvent import duties and meet local-content rules, transferring R&D know-how in geotextiles and filtration media. Domestic leaders Vicunha Textil and Coteminas leverage end-to-end operations in spinning, weaving, and finishing, yet face price pressures from Asian imports and from informal producers selling direct to consumers via social media.

Vertical integration marks a key strategic response. Lenzing’s viscose mill in Bahia and Indorama’s PET-recycling plant in São Paulo secure fiber supply, shorten lead times, and anchor sustainability claims with scope-3 emission cuts. Joint R&D with automotive OEMs on lightweight nonwovens and with civil constructors on high-strength geogrids diversifies revenue beyond fashion cycles. SME clusters gravitate toward niche prints and small-lot services, increasingly adopting digital printing to compete on turnaround rather than scale.

Digital transparency becomes a differentiator as fewer than 5% of regional producers have integrated UNECE’s blockchain traceability. Early adopters lock in EU orders under proposed mandatory disclosure regimes, while laggards may pay compliance surcharges or lose market access. Automation in dyeing and finishing with robotic squeegees and AI color matching is gaining ground among firms with turnover above USD 100 million, but high capex and a shortage of technicians are slowing broader adoption. Consolidation pressures will intensify once MERCOSUR’s due diligence rules take effect in 2027, pushing under-capitalized mills toward acquisition or exit.[4]

South America Textile Industry Leaders

-

Vicunha Têxtil

-

Coteminas S.A.

-

Santana Textiles Group

-

Buddemeyer S.A.

-

Lenzing AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: The European Union and the Mercosur bloc (Brazil, Argentina, Paraguay, Uruguay) officially signed a historic Partnership Agreement. This pact is effectively a massive cross-border market merger, eliminating 35% import tariffs on clothing, textiles, and leather goods and drastically integrating European and South American supply chains.

- January 2026: The Association of Italian Textile Machinery Manufacturers (ACIMIT) led a 22-company coalition at Colombiatex 2026 to partner with local South American manufacturers, aiming to upgrade the region's production lines with advanced automation and digital printing technology.

- November 2025: The Saudi Fashion Commission launched a major collaborative platform in partnership with Collateral Good, IE University, Misk City, and Proaltus Capital Partners. This initiative was designed to connect local textile entrepreneurs with international investors and brands (including HUGO BOSS) to accelerate sustainable fashion and local manufacturing capabilities.

- January 2025: EU mandatory separate textile-waste collection began, raising South American exporters’ design-for-recycling costs by up to 12% while preserving Spanish and Portuguese orders.

South America Textile Market Report Scope

| Fashion & Apparel |

| Industrial/Technical Textiles |

| Household & Home Textiles |

| Medical & Healthcare Textiles |

| Automotive & Transport Textiles |

| Others (Protective, Sports Textiles, etc.) |

| Natural Fibers | Cotton |

| Wool | |

| Silk | |

| Synthetic Fibers | Polyester |

| Nylon | |

| Rayon / Viscose | |

| Acrylic | |

| Polypropylene | |

| Recycled Fibers | |

| Others (Speciality High-Performance Fibers (Aramid, Carbon, UHMWPE)) |

| Woven | |

| Knitted | |

| Non-woven | Spunlaid (Spunbond / Melt-blown) |

| Dry-laid Hydro-entangled | |

| Wet-Laid | |

| Needle-punched | |

| 3-D Weaving & Spacer Fabrics |

| Brazil |

| Argentina |

| Peru |

| Rest of South America |

| By Application | Fashion & Apparel | |

| Industrial/Technical Textiles | ||

| Household & Home Textiles | ||

| Medical & Healthcare Textiles | ||

| Automotive & Transport Textiles | ||

| Others (Protective, Sports Textiles, etc.) | ||

| By Raw Material | Natural Fibers | Cotton |

| Wool | ||

| Silk | ||

| Synthetic Fibers | Polyester | |

| Nylon | ||

| Rayon / Viscose | ||

| Acrylic | ||

| Polypropylene | ||

| Recycled Fibers | ||

| Others (Speciality High-Performance Fibers (Aramid, Carbon, UHMWPE)) | ||

| By Process / Technology | Woven | |

| Knitted | ||

| Non-woven | Spunlaid (Spunbond / Melt-blown) | |

| Dry-laid Hydro-entangled | ||

| Wet-Laid | ||

| Needle-punched | ||

| 3-D Weaving & Spacer Fabrics | ||

| By Geography | Brazil | |

| Argentina | ||

| Peru | ||

| Rest of South America | ||

Key Questions Answered in the Report

How fast is the South America textile market expected to grow between 2026 and 2031?

It is projected to expand at a 7.05% CAGR, climbing from USD 38.59 billion in 2026 to USD 54.25 billion by 2031.

Which application segment is gaining ground most quickly?

Industrial/Technical Textiles are forecast to rise at a 6.15% CAGR through 2031, outpacing traditional fashion and apparel.

Why is polyester still dominant in regional fiber demand?

Cost advantage, recycling compatibility, and new rPET capacity in São Paulo support a 6.56% CAGR for polyester, reinforcing its leadership.

What makes Brazil the key geography for textile investment?

Brazil accounts for 48.5% of 2025 revenue, offers green-credit Cost advantage Cost advantage, recycling compatibility, and new rPET capacity in São Paulo support a 6.56% CAGR for polyester, reinforcing its leadership., recycling compatibility, and new rPET capacity in São Paulo support a 6.56% CAGR for polyester, reinforcing its leadership. Incentives, and hosts major FDI projects in viscose and recycled polyester.

How will EU regulations affect South American textile exporters?

Mandatory separate collection and upcoming Digital Product Passports push exporters toward mono-material, recyclable designs and blockchain-verified traceability to retain EU market access.

Page last updated on: