Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2020 - 2024 |

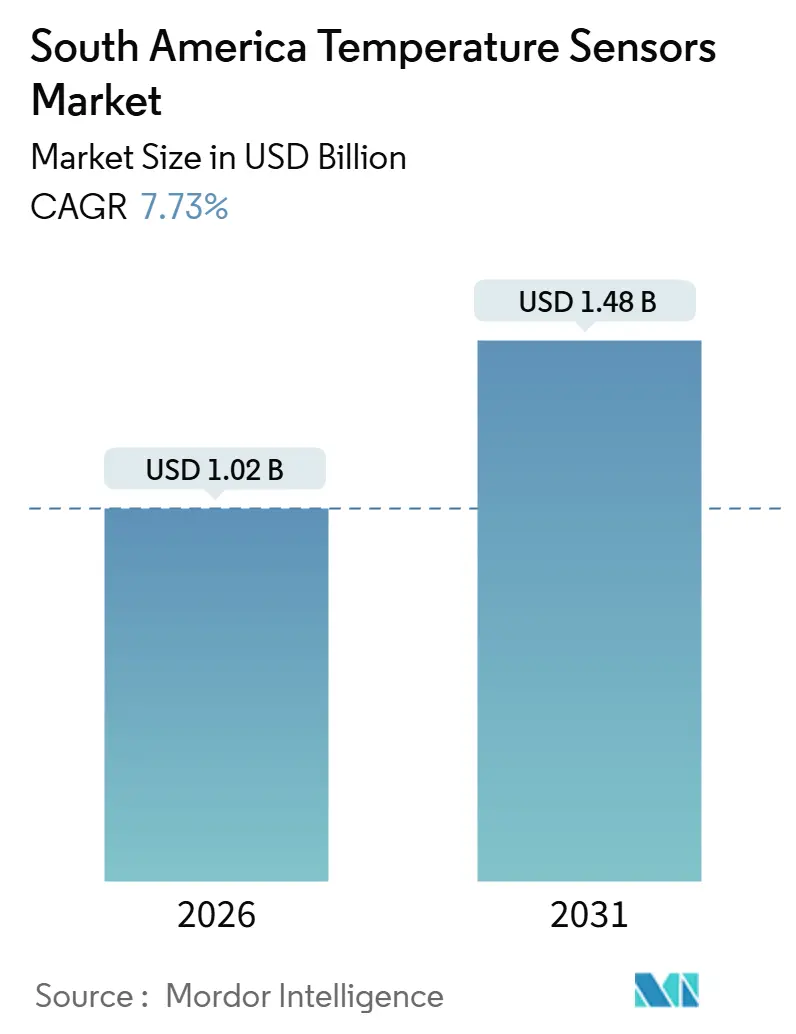

| Market Size (2026) | USD 1.02 Billion |

| Market Size (2031) | USD 1.48 Billion |

| Growth Rate (2026 - 2031) | 7.73% CAGR |

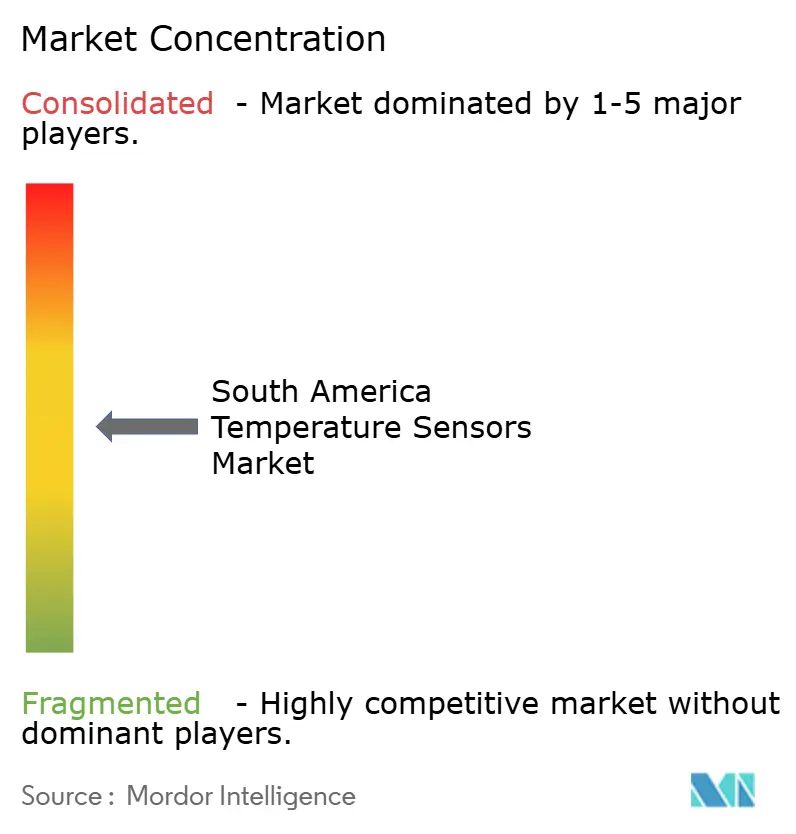

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South America Temperature Sensors Market Analysis by Mordor Intelligence

The South America temperature sensors market size is estimated at USD 1.02 billion in 2026, and is expected to reach USD 1.48 billion by 2031, at a CAGR of 7.73% during the forecast period (2026-2031). This growth reflects active factory digitization programs, lithium-battery gigafactory buildouts, and precision agriculture deployments that together sustain healthy order pipelines for both traditional wired instruments and next-generation wireless nodes. Robust federal incentives in Brazil, mounting electrification of regional vehicle fleets, and the region’s emergence as a critical node in the global battery supply chain further enlarge the addressable base for temperature-monitoring solutions. Suppliers also benefit from the rising adoption of edge analytics, which pushes forward sensor purchases as plants upgrade instrumentation to feed higher-frequency data streams into predictive-maintenance platforms. At the same time, lingering import tariffs, calibration-lab bottlenecks, and raw-material cost swings complicate margins and supply strategies, forcing vendors to localize assembly, bundle connectivity, and secure longer-term commodity contracts.

Key Report Takeaways

- By connectivity, wired devices held 64.54% of the South America temperature sensors market share in 2025, while wireless nodes are tracking an 8.43% CAGR through 2031.

- By technology, thermocouples led with a 32.65% share in 2025, whereas fiber-optic sensors are set to expand at an 8.54% CAGR to 2031.

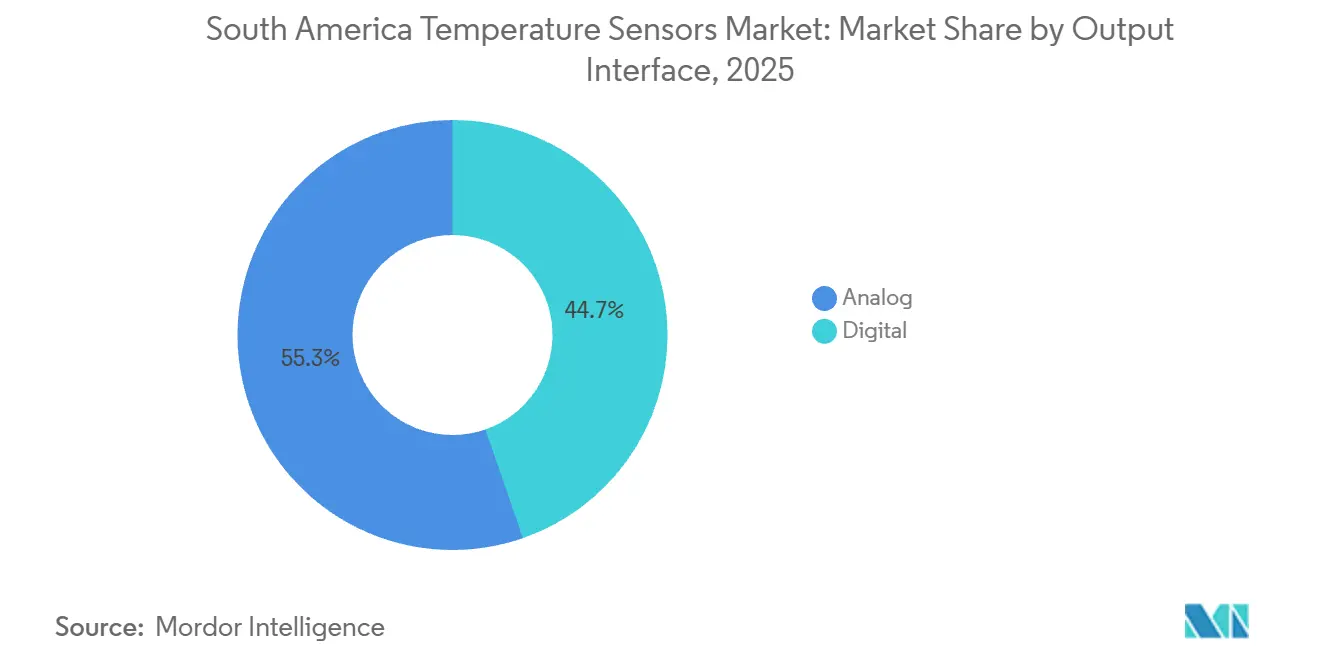

- By output interface, analog circuits accounted for 55.32% of the South America temperature sensor market in 2025, but digital outputs are advancing at an 8.63% CAGR through 2031.

- By end user industry, automotive captured 24.54% of the South America temperature sensors market size in 2025, and medical applications are pacing a 9.16% CAGR through 2031.

- By country, Brazil commanded a 63.42% share of the South America temperature sensor market in 2025, while Chile is forecast to grow at a 9.27% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

South America Temperature Sensors Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growth in Industry 4.0 and Rapid Factory Automation | +2.1% | Brazil, Argentina | Medium term (2-4 years) |

| Government Incentives for Industrial Digitalization in Brazil | +1.6% | Brazil | Long term (≥ 4 years) |

| Accelerated Electric Vehicle Manufacturing Expansion in South America | +1.4% | Brazil, Argentina, Chile | Long term (≥ 4 years) |

| Increasing Adoption of Thermal Monitoring in Lithium-Battery Gigafactories | +1.3% | Chile, Argentina | Long term (≥ 4 years) |

| Rising Deployment of Smart Farming Technologies in Agricultural Exports | +1.2% | Brazil, Argentina, Chile | Medium term (2-4 years) |

| Increasing Demand for Wearables in Consumer Electronics | +0.9% | Brazil | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growth in Industry 4.0 and Rapid Factory Automation

Brazilian manufacturers reported 46% penetration of sensor-based process control in 2024, up 12 points from 2022, underscoring momentum toward fully digitized plants.[1]Confederação Nacional da Indústria, “Industry 4.0 Adoption in Brazilian Manufacturing,” portaldaindustria.com.br Federal and provincial programs reward investments that align with ISO 9001 practices, and temperature sensors stand out because calibrated thermal data is a precondition for process certification. Vendors therefore position complete packages, probe, transmitter, gateway, and analytics, to help factories cross the compliance threshold quickly. Medium-term impact concentrates in São Paulo and Buenos Aires corridors where export-oriented plants need near-real-time quality data to meet overseas traceability rules. As these corridors adopt predictive-maintenance playbooks, refresh cycles for legacy 4-20 mA loops accelerate, bringing incremental demand for higher-accuracy digital transmitters.

Government Incentives for Industrial Digitalization in Brazil

The Nova Indústria Brasil initiative earmarks BRL 300 billion (USD 60 billion) to 2033 for modernization projects that explicitly score bids on sensor-enabled automation. Grant recipients must maintain calibration traceability to INMETRO, effectively turning temperature sensors from optional line items into mandated purchases. Funds also cover worker training, which expands the local calibration talent pool and stimulates demand for reference-grade platinum resistance thermometers. Because the program runs through 2033, its pull on the South America temperature sensors market is sustained, allowing suppliers to rationalize local manufacturing lines and pursue tariff exemptions for modules that still lack domestic equivalents.

Accelerated Electric Vehicle Manufacturing Expansion in South America

Regional electric-vehicle assembly lines, battery-pack integration centers, and charging-infrastructure rollouts all require dense thermal monitoring. Cell packs incorporate multi-point sensors to detect hotspots before runaway, triggering procurement of high-accuracy digital ICs that can survive automotive qualification. Long-term influence stems from announced gigafactories in Brazil’s Minas Gerais and Argentina’s Córdoba regions, each scheduling volume production after 2028. Suppliers winning design-ins today can expect recurring unit demand through vehicle life cycles, while aftermarket opportunities emerge for replacement probes and upgraded battery-management modules as fleets age.

Increasing Adoption of Thermal Monitoring in Lithium-Battery Gigafactories

Chile’s Atacama lithium basin anchors new hydroxide and cathode plants, all of which embed distributed temperature sensing along mixing vessels, formation chambers, and aging racks.[2]International Council on Clean Transportation, “Chile Lithium Battery Supply Chain Projections,” theicct.org Fiber-optic DTS lines supply thousands of readings per second without electromagnetic interference, justifying their premium in zones where even small thermal deviations downgrade yield. Argentina’s triangle projects follow a similar blueprint, and operators are already issuing tenders specifying ±0.25 °C accuracy. Because most facilities go live between 2028 and 2031, current sensor vendors are racing to lock framework agreements that cover commissioning, calibration, and ongoing digital-twin analytics.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Import Tariffs on Advanced Sensor Modules | -0.9% | Brazil, Argentina | Long term (≥ 4 years) |

| Supply-Chain Disruptions from Semiconductor Capacity Constraints | -0.7% | Global | Short term (≤ 2 years) |

| Fluctuation in Raw Material Prices | -0.8% | Global, South America | Short term (≤ 2 years) |

| Shortage of Skilled Calibration Professionals | -0.6% | Brazil, Chile, Argentina | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Import Tariffs on Advanced Sensor Modules

Brazil adds import duty, industrialized product tax, federal social contributions, and state ICMS tax, elevating landed prices by roughly 60% over FOB quotes.[3]U.S. International Trade Administration, “Brazil – Import Tariffs,” trade.gov Automotive and petrochemical plants therefore pressure suppliers to localize final assembly or, at minimum, build sub-assemblies inside free-trade zones. While ex-tarifário programs can waive duties for equipment not produced domestically, approvals take months, stretching project timelines and encouraging buyers to favor vendors with in-country assembly footprints.

Supply-Chain Disruptions from Semiconductor Capacity Constraints

Global shortages of 8-inch foundry capacity for high-precision analog and MEMS dice periodically delay deliveries of digital temperature-sensor ICs. South American importers lack volume leverage to secure priority allocation, so lead times extend to 30 weeks or more during peak crunch periods. While some OEMs dual-source dies, cross-qualification costs and regulatory re-testing slow adoption, pressuring local distributors to hold larger safety stock. Short-term project delays may cascade if critical automation upgrades must align with broader plant shutdown schedules.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Connectivity: Wireless Gains Ground in Remote Applications

Wired installations, representing 64.54% of South America temperature sensors market share in 2025, dominate continuous-process industries because intrinsically safe 4-20 mA loops deliver deterministic communication and avoid battery maintenance. Analog-loop inertia is especially strong in oil refineries, thermal power stations, and petrochemical crackers where unplanned downtime carries million-dollar penalties. Yet wireless nodes are expanding at an 8.43% CAGR thanks to ruggedized battery chemistries and mesh-network protocols that guarantee five-nines availability over kilometer-scale sites. ABB’s STX300 transmitter exemplifies the shift, offering ten-year field life and WirelessHART compliance, which reduces integration headaches when plants retrofit legacy distributed-control systems.

Adoption also rises in agriculture and mining where cable trenching costs dwarf sensor hardware prices. Remote irrigation pivots in Mato Grosso leverage LoRaWAN gateways to collect canopy and soil temperature, while Chilean copper mines mount self-powered sensors on rotating mills to avoid slip-ring failures. Conversely, safety-critical emergency-shutdown loops retain wired preferences because latency tolerance is only a few milliseconds. As a result, the South America temperature sensors market balances two trajectories: entrenched wired demand for high-risk assets and accelerating wireless uptake in cost-constrained field deployments.

By Technology: Fiber-Optic Sensors Disrupt Traditional Architectures

Thermocouples delivered 32.65% market share in 2025 because their wide measurement range (-200 °C to +2,300 °C) and low bill-of-materials cost satisfy smelters and glass furnaces. RTDs fill precision niches, pharmaceutical fermenters, dairy pasteurizers, where ±0.1 °C accuracy outweighs higher platinum prices. Thermistors serve volume electronics, while infrared pyrometers enable non-contact reads on moving webs and molten metal. The South America temperature sensors market now sees fiber-optic sensors rising at an 8.54% CAGR as pipeline operators and power-transmission utilities pilot distributed temperature sensing lines that localize leaks and hotspots over tens of kilometers.

Chile’s lithium gigafactories specify fiber grids inside formation chambers to capture cell-level anomalies, and Brazilian offshore operators are qualifying optical cables for riser monitoring where electromagnetic immunity trumps cost. Photonic thermometry research at NIST, promising 10 mK uncertainty, foreshadows eventual step-change in calibration standards. Even so, fiber install costs and specialized splicing skills slow blanket adoption, keeping thermocouples and RTDs firmly entrenched for general-purpose duties.

By Output Interface: Digital Interfaces Align With Edge Computing

Analog loops held 55.32% of South America temperature sensors market share in 2025, valued for immunity to electrical noise and ability to span 1 km stretches without repeaters. However, as plants add edge servers and analytics gateways, digital outputs, HART, Modbus, Foundation Fieldbus, IO-Link, gain favor, accelerating at an 8.63% CAGR. Emerson’s 3144S transmitter illustrates the hybrid approach, shipping with dual analog and digital channels so brownfield users can switch protocols over time.

Digital paths embed self-diagnostics that alert technicians to drift or wiring faults before they balloon into downtime events. Microchip’s MCP998x sensors integrate resistance error correction plus hardware shutdown thresholds, features that only digital ASICs can deliver. Edge-ready interfaces also cut cabinet space by feeding data directly to microcontrollers, skipping analog signal conditioners. Adoption remains uneven because brownfield DCS systems still aggregate 4-20 mA loops, yet new-build gigafactories and EV battery lines increasingly bypass analog altogether.

By End-User Industry: Medical Segment Outpaces Traditional Industrials

Automotive plants consumed 24.54% of South America temperature sensors market size in 2025, leveraging up to 50 sensors per internal-combustion vehicle and double that for battery-electric models. Battery modules deploy high-density digital ICs to track cell temperatures within ±2 °C windows that preserve lifespan. Petrochemical, metal, and power-generation users collectively form the bulk of traditional industrial demand, ordering rugged probes that survive vibration, corrosive media, and sustained 600 °C service.

The medical segment, although smaller now, is projected to post a 9.16% CAGR to 2031, outstripping legacy industrial verticals. Expansion of vaccine distribution networks after COVID-19 and regulatory mandates for ±0.5 °C logging spur sales of calibrated data loggers and cloud-linked cold-chain tags WHO.INT. Remote patient-monitoring wearables also multiply sensor counts as private insurers in Brazil pilot telehealth packages. This structural shift insulates the South America temperature sensors market from cyclical swings in commodity industries, anchoring a steadier revenue stream tied to public-health budgets and consumer wellness spending.

Geography Analysis

Brazil accounted for 63.42% of South America temperature sensors market share in 2025, supported by its diverse industrial base and 216 million consumers. São Paulo’s auto hubs, Rio’s offshore rigs, and agribusiness clusters across Paraná all rely on continuous temperature data for yield and safety. Nova Indústria Brasil subsidies reinforce momentum by subsidizing ISO-compliant automation. Yet Brazil’s tax stack inflates import costs by 60%, nudging suppliers toward local assembly or ex-tarifário relief. INMETRO’s calibration labs underpin trust in locally built probes and support export paperwork under the CIPM MRA framework.[4]Bureau International des Poids et Mesures, “CIPM Mutual Recognition Arrangement,” bipm.org

Chile, forecast to grow at 9.27% CAGR through 2031, rides lithium-battery investments in the Atacama Desert. Battery-grade hydroxide plants, cathode lines, and 30 GWh-scale cell factories all specify multi-point temperature sensing to prevent runaway during formation and charging cycles. Chilean fruit exporters equally deploy fiber-optic lines in cold stores to curb spoilage, reinforcing year-round sensor demand beyond mining. Limited domestic calibration capacity means high-accuracy instruments often travel to Argentine or Brazilian labs, adding cost and time but also creating brownfield opportunity for mobile calibration service providers.

Argentina faces currency volatility and triple-digit inflation, yet automotive lines in Córdoba and lithium projects in Salta ensure steady baseline demand. Buyers prefer dollar-priced quotes and extended terms, hence distributors with export insurance and inventory financing outperform peers. Elsewhere, Uruguay, Paraguay, Peru, and Colombia form a long-tail segment focused on food processing, mining, and infrastructure. Uruguay’s LATU metrology institute, despite backlog challenges, anchors regional calibration cooperation, enabling cross-border acceptance of certificates and supporting niche export contracts.

Competitive Landscape

Multinational automation majors, semiconductor houses, and niche probe makers together shape a moderately fragmented playing field in South America. The global brands leverage decades-old installed bases in petrochemical complexes and aerospace assembly lines, reinforcing customer lock-in through multi-year calibration and maintenance contracts. Regional distributors and systems integrators seize cost-sensitive segments such as HVAC, food processing, and building automation by offering localized support in Portuguese and Spanish and by carrying inventory that sidesteps lengthy customs delays. Asian value suppliers keep commodity prices in check on thermocouples and thermistors, forcing incumbents to differentiate through higher-accuracy specifications, dual analog-digital outputs, and longer warranties. As a result, no single vendor controls more than a quarter of total revenue, giving buyers bargaining room even in safety-critical applications.

Consolidation has begun to tighten the field at the silicon level. STMicroelectronics’ pending purchase of NXP’s MEMS sensor line is expected to fuse temperature, inertial, and pressure functions in a single die, compressing bill-of-materials and reducing board real estate for electric-vehicle battery packs. Emerson and ABB are on parallel tracks, bundling transmitters with cloud gateways and analytics subscriptions that convert one-off hardware sales into recurring service revenue. These moves aim to protect margins as low-cost competitors erode pricing on standalone probes.

Localization strategies increasingly decide contract awards. Brazilian import tariffs add about 60% to landed costs, so leading brands assemble transmitters inside free-trade zones or partner with contract manufacturers in Campinas and Manaus to qualify for tax incentives. Vendors also fund joint training programs with INMETRO-accredited labs to ease calibration backlogs and cement brand loyalty among plant technicians. Semiconductor shortages remain a wildcard, prompting suppliers to dual-source critical ICs and maintain safety stock in bonded warehouses close to São Paulo’s port. Looking ahead, buyers will likely favor integrated sensor-connectivity packages that shorten installation time and feed predictive-maintenance platforms, keeping competitive pressure high on firms slow to adopt an end-to-end offering model.

South America Temperature Sensors Industry Leaders

Siemens AG

Honeywell International Inc.

Emerson Electric Co.

ABB Ltd

Texas Instruments Incorporated

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Emerson launched the Rosemount 3144S transmitter with 0.05 °C accuracy and dual analog/digital outputs, targeting pharmaceutical and food-processing retrofits.

- July 2025: STMicroelectronics agreed to acquire NXP’s MEMS sensor business for USD 950 million, with closure expected H1 2026.

- June 2025: ABB introduced the SIL2-certified NINVA TSP341-N transmitter for emergency-shutdown loops in petrochemical and power plants.

- May 2025: ABB rolled out the STX300 wireless temperature transmitter rated for ten-year battery life in pipeline and rotating-machinery deployments.

South America Temperature Sensors Market Report Scope

The South America Temperature Sensors Market refers to the industry focused on the development, production, and distribution of devices that measure temperature by sensing heat energy and converting it into readable data. These sensors are widely used across various industries to ensure process efficiency, safety, and quality control.

The South America Temperature Sensors Market Report is Segmented by Connectivity (Wired, and Wireless), Technology (Thermocouple, Resistance Temperature Detector (RTD), Thermistor, Infrared (IR), Fiber Optic, Temperature Transmitter, and Other Technologies), Output Interface (Analog, and Digital), End-User Industry (Chemical and Petrochemical, Oil and Gas, Metal and Mining, Power Generation, Food and Beverage, Automotive, Medical, Aerospace and Military, Consumer Electronics, and Other End-User Industries), and Country (Brazil, Argentina, Chile, and Rest of South America). The Market Forecasts are Provided in Terms of Value (USD).

By Connectivity

| Wired |

| Wireless |

By Technology

| Thermocouple |

| Resistance Temperature Detector (RTD) |

| Thermistor |

| Infrared (IR) |

| Fiber Optic |

| Temperature Transmitter |

| Other Technologies |

By Output Interface

| Analog |

| Digital |

By End-User Industry

| Chemical and Petrochemical |

| Oil and Gas |

| Metal and Mining |

| Power Generation |

| Food and Beverage |

| Automotive |

| Medical |

| Aerospace and Military |

| Consumer Electronics |

| Other End-User Industries |

By Country

| Brazil |

| Argentina |

| Chile |

| Rest of South America |

| By Connectivity | Wired |

| Wireless | |

| By Technology | Thermocouple |

| Resistance Temperature Detector (RTD) | |

| Thermistor | |

| Infrared (IR) | |

| Fiber Optic | |

| Temperature Transmitter | |

| Other Technologies | |

| By Output Interface | Analog |

| Digital | |

| By End-User Industry | Chemical and Petrochemical |

| Oil and Gas | |

| Metal and Mining | |

| Power Generation | |

| Food and Beverage | |

| Automotive | |

| Medical | |

| Aerospace and Military | |

| Consumer Electronics | |

| Other End-User Industries | |

| By Country | Brazil |

| Argentina | |

| Chile | |

| Rest of South America |

Key Questions Answered in the Report

How large is the South America temperature sensors market today?

It was valued at USD 1.02 billion in 2026 and is predicted to hit USD 1.48 billion by 2031.

What is the expected growth rate for temperature sensors in South America?

The market is projected to register a 7.73% CAGR from 2026 to 2031.

Which connectivity segment is expanding fastest in the region?

Wireless nodes are advancing at an 8.43% CAGR thanks to reduced battery-replacement cycles and improved industrial protocols.

Why is Chile viewed as a high-growth destination for sensor vendors?

Lithium-battery gigafactories in the Atacama Desert are driving a forecast 9.27% CAGR through 2031, demanding high-density thermal monitoring.

Which end-user industry shows the highest future growth?

Medical applications, including vaccine cold-chain and remote patient monitoring, are expanding at a projected 9.16% CAGR.

What is the main hurdle for importing advanced sensor modules into Brazil?

A layered tax system can lift landed costs by about 60%, encouraging local assembly or tariff exemptions.

Page last updated on: