South America Supply Chain Consulting Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

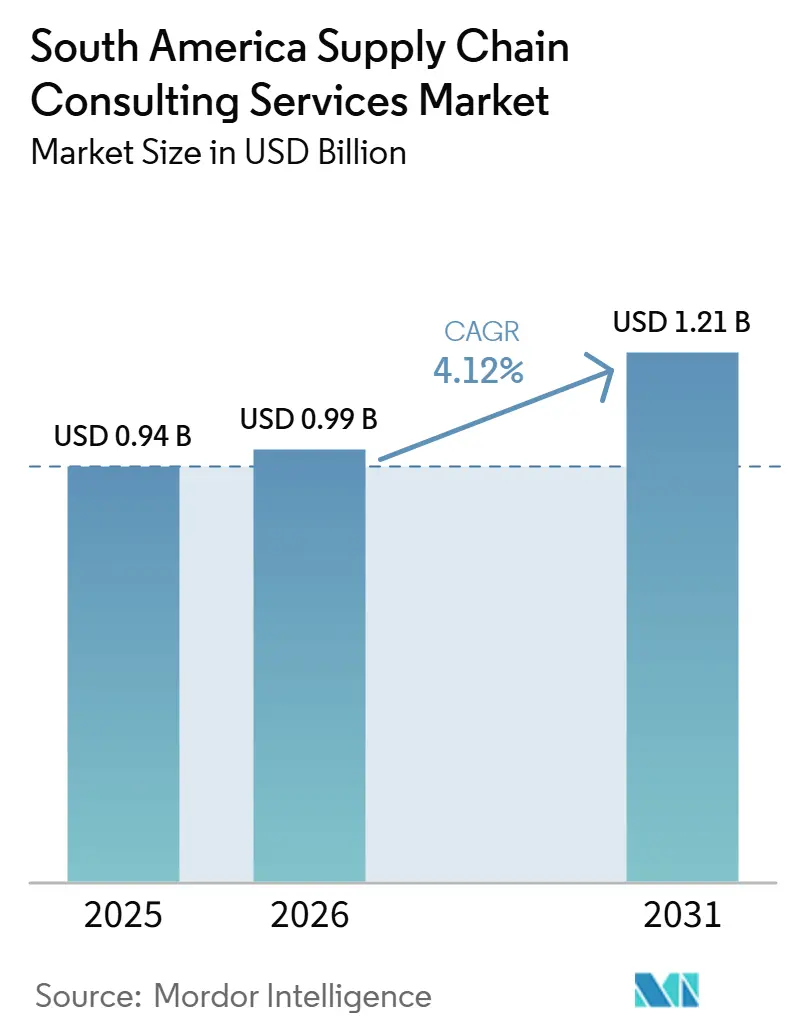

| Base Year Market Size (2025) | USD 0.94 Billion |

| Market Size (2026) | USD 0.99 Billion |

| Market Size (2031) | USD 1.21 Billion |

| Growth Rate (2026 - 2031) | 4.12% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South America Supply Chain Consulting Services Market Analysis by Mordor Intelligence

The South America supply chain consulting services market size was valued at USD 0.941 billion in 2025 and estimated to grow from USD 0.987 billion in 2026 to reach USD 1.208 billion by 2031, at a CAGR of 4.12% during the forecast period (2026-2031). Elevated logistics costs that average 14-16% of final product value, persistent infrastructure gaps, and a region-wide push to replace legacy platforms with cloud-native, AI-enabled solutions have kept consulting demand on an upward trajectory. Nearshoring strategies are reshaping network footprints as U.S. and European manufacturers re-evaluate Brazil, Peru, and Colombia as alternatives to Mexico, which is capacity-constrained, while green-finance incentives, such as Brazil’s National Climate Fund, are catalyzing sustainability roadmaps. At the same time, political volatility, talent shortages, and high professional-services fees temper the pace of adoption, reinforcing the need for flexible delivery models that blend project work with managed services. Competitive intensity remains high as global integrators battle regional boutiques for engagements that increasingly hinge on digital, data, and decarbonization capabilities.

Key Report Takeaways

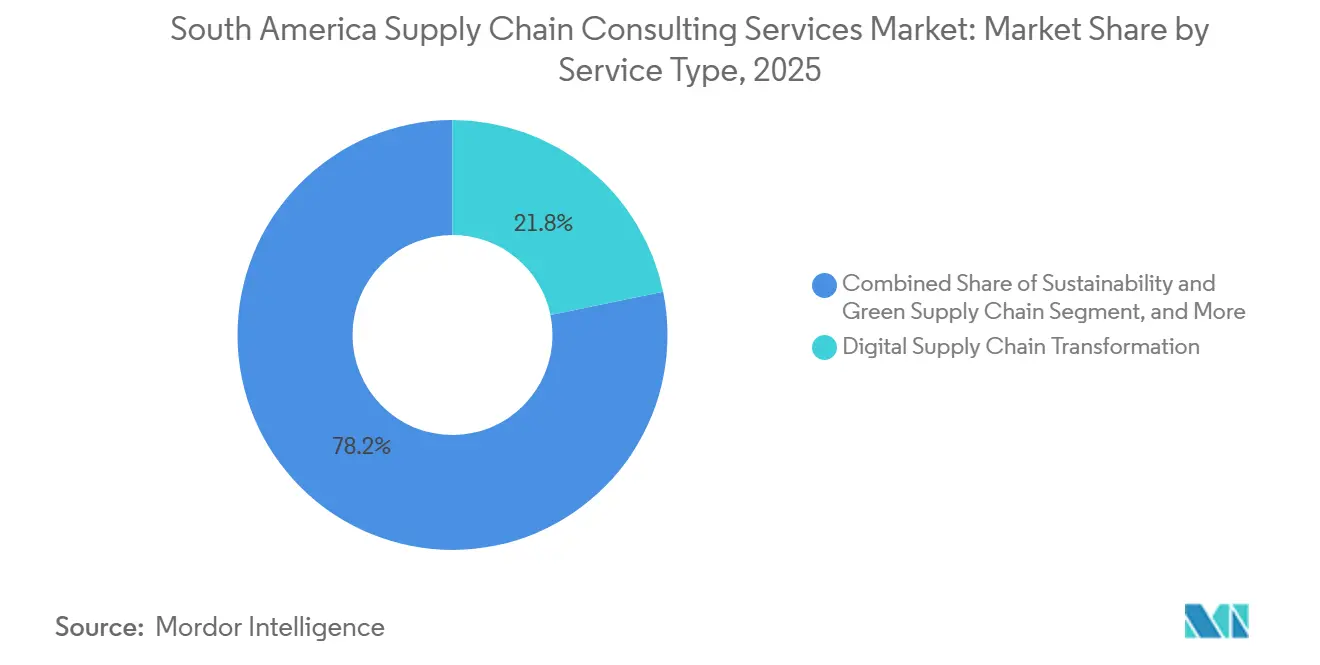

- By service type, Digital Supply Chain Transformation led with 21.78% of the South America supply chain consulting services market share in 2025; Sustainability and Green Supply Chain services are forecast to expand at a 7.31% CAGR through 2031.

- By end-user industry, manufacturing held 35.59% of 2025 revenue, while energy and utilities is projected to post the fastest growth at 6.02% CAGR to 2031.

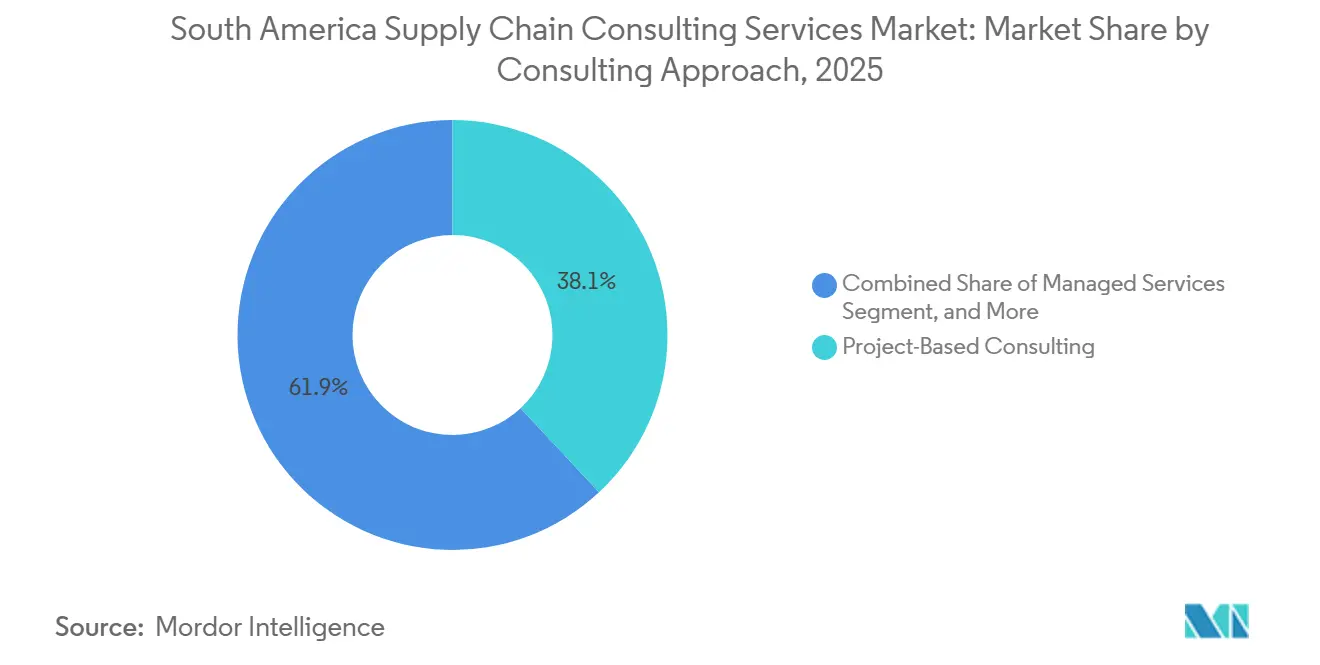

- By consulting approach, project-based work accounted for 38.07% of 2025 spending, yet managed services is advancing at a 5.43% CAGR over 2026-2031.

- By organization size, large enterprises represented 67.21% of 2025 demand, whereas small and medium enterprises are growing at 4.64% CAGR on the back of voucher and factoring programs.

- By geography, Brazil commanded 42.67% of the 2025 total, but Peru is expected to lead growth with a 5.26% CAGR during the forecast window.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

South America Supply Chain Consulting Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact |

|---|---|---|---|

| Rising Adoption of Digital Supply Chain Transformation | +1.2% | Brazil, Argentina, Colombia | Medium term (2-4 years) |

| Need for Cost Optimization Across Enterprises | +0.9% | Brazil, Chile, Peru | Short term (≤ 2 years) |

| Nearshoring Trends Driving Regional Supply Chain Reconfiguration | +0.8% | Brazil, Southern Cone | Long term (≥ 4 years) |

| Government Incentives for Green Logistics Initiatives | +0.7% | Brazil, Chile, Colombia | Long term (≥ 4 years) |

| Increasing Complexity of Regional Trade Regulations | +0.6% | Brazil, Argentina, Peru, Colombia | Medium term (2-4 years) |

| Rapid Growth of E-commerce Fulfillment Hubs in Secondary Cities | +0.5% | Brazil (Brasília, secondary metros), Chile, Colombia | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Adoption of Digital Supply Chain Transformation

Enterprises are consolidating fragmented ERP, procurement, and logistics systems onto cloud platforms that embed AI for process orchestration and predictive analytics. Vale’s program to unify more than 20 purchasing tools under Coupa, covering USD 14 billion in annual spend, showcases how large asset-heavy firms are moving from pilot projects to scaled execution.[1]Vale, “Vale launches innovative program for digital transformation of its supply chain,” vale.com Pharmaceutical manufacturer União Química is following a similar path with SAP Ariba, targeting a May 2026 go-live that adds intelligent proposal evaluation. The region is also experimenting with agentic AI, as YPF and Globant deployed 46 digital agents across procurement and inventory workflows, freeing staff for strategic sourcing. Consulting firms benefit because most enterprises need external support to blueprint data architecture, redesign processes, and run change-management programs.

Need for Cost Optimization Across Enterprises

Regional logistics inefficiencies remain a structural drain on profitability, with costs sitting at almost double those in developed economies. Platform deployments such as Amazon Brazil’s use of Optilogic’s Cosmic Frog for scenario modeling illustrate how shippers are quantifying trade-offs among speed, service, and cost. Surveys of retail executives indicate that 66% plan to reconfigure their networks or diversify suppliers if trade-related costs rise, feeding a robust pipeline of consulting engagements focused on network design and inventory rightsizing. The Inter-American Development Bank estimates digitalization can shave up to 15% off logistics costs, underscoring the tangible ROI narrative that consultants use to close deals.

Nearshoring Trends Driving Regional Supply Chain Reconfiguration

With Mexico grappling with capacity constraints and security concerns, multinationals are evaluating Brazil’s Southeast corridor and Andean nations for incremental production and final assembly. The Inter-American Development Bank projects an extra USD 78 billion in annual export potential for South America if it capitalizes on nearshoring openings. Consulting assignments range from supplier development to footprint strategy and local-content compliance. UNIDO’s 2026 Industrial Development Report argues that deepening intraregional value chains could lift manufacturing’s regional share of global value-added, providing a multi-decade runway for advisory work.[2]UNIDO, “Industrial Development Report 2026,” unido.org

Government Incentives for Green Logistics Initiatives

Policy frameworks are funneling capital toward low-carbon logistics. Brazil’s Programa Mover allocates BRL 3.5 billion (USD 0.69 billion) in 2024 and rises to BRL 4.1 billion (USD 0.80 billion) by 2028 in tax credits for mobility R&D, recycling, and domestic content. The Ministry of Transport’s Sustainable Logistics Plan embeds emissions targets across federal projects, compelling state-owned entities to commission lifecycle carbon assessments. Consultants thus gain mandates to structure finance, quantify emissions, and audit supply bases for ESG compliance.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shortage of Skilled Supply Chain Professionals | -0.4% | Brazil, Argentina, Colombia, Peru | Medium term (2-4 years) |

| High Consulting Fees for Small and Medium Enterprises | -0.3% | Peru, Colombia, smaller economies | Short term (≤ 2 years) |

| Political Instability Affecting Long-Term Consulting Contracts | -0.2% | Argentina, Peru, Colombia | Medium term (2-4 years) |

| Fragmented Infrastructure Limiting Consulting Implementation ROI | -0.2% | Landlocked countries, secondary cities | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Shortage of Skilled Supply Chain Professionals

OECD research shows that SMEs perform most routine tasks at high risk of automation yet lack access to advanced training programs, leaving a gap in data analytics and process-engineering talent.[3]Organisation for Economic Co-operation and Development, “SME Policy Index: Latin America and the Caribbean 2024,” oecd.org KPMG warns that staffing constraints lengthen project timelines and raise day rates across Brazil and Argentina, limiting the scalability of consulting engagements. To mitigate, firms are launching capacity-building boot camps and partnering with universities to create feeder programs for junior analysts.

High Consulting Fees for Small and Medium Enterprises

Surveys of more than 2,000 MSMEs reveal that 84% view certification and inspection costs as prohibitive and that lack of budget tops the list of export barriers. Voucher programs such as ProChile E-Exporta and Brasil Mais have begun to subsidize diagnostics and pilot projects, but coverage is still thin compared with demand. Consulting firms are responding with cohort-based accelerators and semi-standardized toolkits that lower entry pricing, yet margins remain tight in the SME segment.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Digital Platforms Dominate While Sustainability Accelerates

Digital Supply Chain Transformation captured 21.78% of the South America supply chain consulting services market share in 2025, underscoring companies' prioritization of end-to-end visibility and AI-driven decision engines. Vale’s program to automate more than 90 internal controls underscores the scale of multi-year digital mandates. Demand is reinforced by Amazon Brazil’s real-time network twin, which continuously tests fulfillment scenarios. Sustainability and Green Supply Chain mandates, although smaller, are expanding at a 7.31% CAGR to 2031 as sovereign green-bond proceeds and BRL-denominated tax credits finance decarbonization roadmaps. Consultants are thus integrating carbon accounting modules into core transformation work, shortening payback horizons and widening the South America supply chain consulting services market size for ESG-linked offerings.

Beyond the two fastest-moving areas, network design and procurement optimization remain evergreen lines. IDB’s projection of a potential USD 78 billion export uplift drives renewals of footprint analyses, while YPF’s agentic AI experiment signals a pivot toward autonomous supplier evaluation. The service mix is rounded out by risk and resilience modeling, with clients requesting digital twins that overlay cyber, climate, and geopolitical stress tests. These expansions illustrate how the South America supply chain consulting services market continues to evolve from siloed advisory toward integrated, platform-enabled solutions.

By End-User Industry: Manufacturing Still Leads, Energy Surges

Manufacturing commanded 35.59% of the South America supply chain consulting services market in 2025, led by complex automotive and mining value chains. Brazil’s auto-parts revenue reached BRL 259.1 billion (USD 50.8 billion) in 2024, drawing consulting assignments in supplier rationalization and packaging redesign. Mining majors seek throughput gains and digital permitting, illustrated by Peru’s USD 51.55 billion project pipeline that increasingly embeds supply-chain digitization. Energy and utilities, while smaller, is the fastest-growing vertical at 6.02% CAGR as IRENA forecasts USD 500 billion in annual renewable investment needs through 2050. This growth enlarges the South America supply chain consulting services market size devoted to grid logistics, electrolyser sourcing, and hydrogen corridor planning.

Retail and e-commerce engagements are riding a wave of fulfillment-center expansion. CEVA’s 67,000 square-meter Amazon site, capable of 135,000 daily packages, showcases the scale at which omnichannel brands require process mapping and warehouse automation. Pharma, food, and beverage firms are likewise hiring consultants to modernize cold chains, comply with recycled-content mandates, and integrate serialization. The broadening client mix underpins a resilient revenue base even when commodity cycles soften.

By Consulting Approach: Project Work Prevails But Managed Services Gain Share

Project-based engagements retained 38.07% South America supply chain consulting services market share in 2025, reflecting a preference for discrete, milestone-driven deliverables such as system selection, M&A integration, or customs compliance. Accenture’s acquisition of Verum Partners adds heavy-capital expertise to this model and deepens feasibility-through-commissioning coverage. Even so, managed services is rising at a 5.43% CAGR as clients opt for continuous optimization. Multi-year contracts such as DP World’s five-year warehouse deal with Suzano exemplify how providers embed teams inside operations to monitor KPIs and drive iterative gains.

Training and capacity-building offerings form a bridge between project and managed models. OECD’s skills-gap findings have prompted consultants to bundle workshops with technology rollouts. Advisory-plus-subscription constructs, epitomized by Globant’s AI Pods, allow clients to scale AI agents while leveraging expert oversight, extending the lifetime value of engagements, and expanding the South America supply chain consulting services market share captured by hybrid services.

By Organization Size: Large Enterprises Anchor Demand, SMEs Accelerate

Large enterprises contributed 67.21% of 2025 revenue, sustained by wide geographic footprints that need synchronized planning, regulatory compliance, and advanced analytics. Their willingness to invest in AI-driven platforms and green-finance structuring keeps them the anchor segment of the South America supply chain consulting services market. Yet small and medium enterprises are forecast to expand at a 4.64% CAGR as digital vouchers, factoring schemes, and cloud SaaS lower entry barriers. SUNAT Peru’s electronic factoring platform, which processed PEN 34 billion (USD 8.7 billion) in 2023, illustrates how faster working-capital cycles unlock consulting budgets.

Consultants targeting SMEs increasingly deploy standardized diagnostics, remote delivery, and pay-as-you-grow models. These approaches contain costs and allow firms to penetrate secondary cities where traditional day-rate economics do not scale. As such, the opportunity pool is widening beyond large resource majors toward exporters in agribusiness, textiles, and cosmetics that previously operated below the advisory radar.

Geography Analysis

Brazil retained 42.67% of the South America supply chain consulting services market in 2025, underpinned by its scale and government incentive frameworks. Vale’s USD 14 billion procurement digitization and Amazon’s nationwide network twin typify flagship transformation deals. Tax-credit pools under Programa Mover, totaling BRL 3.5-4.1 billion (USD 0.69-0.80 billion) per year, are steering automotive and logistics firms toward compliance with the circular economy. Expansions such as CEVA’s warehouse build-out to a 620,000 square-meter footprint by 2028 sustain a deep pipeline of facility design, automation, and inventory-planning assignments.

Peru is projected to record the fastest growth, at 5.26% CAGR to 2031, driven by a USD 8.3 billion amendment program that accelerates PPP pipelines and by the USD 420 million Chancay-Sierra Central railway concession. Mining investments exceeding USD 4 billion in 2023 require consultants for logistics engineering, energy PPAs, and permitting acceleration. Nonetheless, political volatility compels scenario planning to hedge against regulatory swings.

Argentina is undergoing structural realignment as import liberalization shifts activity toward distribution. Plant closures such as Whirlpool’s Pilar site release real estate and spark consolidation studies. Simultaneously, digital leaders such as YPF deploy 46 AI agents across supply-chain workflows, signaling that select corporates remain innovation-hungry even amid macro headwinds. Chile, Colombia, and secondary markets like Uruguay and Paraguay contribute niche demand centered on mining logistics, free-zone optimization, and agrifood chains, but limited scale and infrastructure gaps cap their aggregate weight in the South America supply chain consulting services market size.

Competitive Landscape

The South America supply chain consulting services industry features a fragmented mix of global strategy houses, technology integrators, and regional specialists. Accenture, Deloitte, KPMG, McKinsey, and EY continue to win enterprise-wide transformations, leveraging cross-border teams and proprietary AI accelerators. Accenture’s February 2026 purchase of Verum Partners adds 180 engineers skilled in capital-project controls, strengthening the firm’s play in Brazil’s USD-scale infrastructure wave. Andersen Consulting’s expansion via Albieri e Associados brings operational-optimization depth to mid-market clients.

Regional boutiques such as Integration Consulting and Ábaco Consulting thrive on local regulatory knowledge and rapid deployment. Ábaco’s acquisition of Tangotech broadens its SAP IBP bench and opens cross-selling routes into Southern Cone automotive clusters. Technology disruptors, including Optilogic for network twins and Globant’s AI Pods, circumvent traditional man-hour models by offering SaaS-plus-services bundles that deliver faster ROI. To compete, incumbents are vertically integrating managed services, creating subscription diagnostic portals, and investing in talent academies to offset chronic skills shortages.

Pricing pressure remains acute outside Tier-1 cities, pushing firms to adopt remote delivery and offshore centers. Nonetheless, the top five players are estimated to hold no more than 35-40% combined revenue, leaving ample share for specialists focused on green finance, cold-chain engineering, or omnichannel fulfillment. Partnerships with carriers, fintechs, and sustainability rating agencies are becoming a key differentiation lever as clients demand outcome-based contracts.

South America Supply Chain Consulting Services Industry Leaders

Accenture plc

Deloitte Touche Tohmatsu Ltd

KPMG International Ltd

PricewaterhouseCoopers International Ltd

Bain & Company Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: DP World signed a five-year contract to manage Suzano’s tissue-division warehouse operations in Espírito Santo, Brazil.

- February 2026: Amazon Brazil deployed Optilogic’s Cosmic Frog and DataStar platforms to continuously optimize the network across all 27 states.

- January 2026: PROINVERSIÓN announced amendments worth USD 8.3 billion to accelerate investments in health, transport, and energy PPPs.

- January 2026: Peru awarded a USD 420 million freight-rail concession linking Chancay port with central highland mining zones.

South America Supply Chain Consulting Services Market Report Scope

The South America Supply Chain Consulting Services Market Report is Segmented by Service Type (Supply Chain Strategy and Network Design, Procurement and Sourcing, Logistics and Distribution Optimization, Inventory and Demand Planning, Digital Supply Chain Transformation, Sustainability and Green Supply Chain, Risk and Resilience Consulting), End-User Industry (Retail and E-commerce, Manufacturing, Food and Beverage, Healthcare and Pharmaceuticals, Automotive, Consumer Packaged Goods, Energy and Utilities), Consulting Approach (Project-Based Consulting, Managed Services, Training and Capacity Building, Advisory and Benchmarking), Organization Size (Large Enterprises, Small and Medium Enterprises), and Geography (Brazil, Argentina, Colombia, Chile, Peru, Rest of South America). The Market Forecasts are Provided in Terms of Value (USD).

| Supply Chain Strategy and Network Design |

| Procurement and Sourcing |

| Logistics and Distribution Optimization |

| Inventory and Demand Planning |

| Digital Supply Chain Transformation |

| Sustainability and Green Supply Chain |

| Risk and Resilience Consulting |

| Other Service Types |

| Retail and E-commerce |

| Manufacturing |

| Food and Beverage |

| Healthcare and Pharmaceuticals |

| Automotive |

| Consumer Packaged Goods |

| Energy and Utilities |

| Other End-User Industries |

| Project-Based Consulting |

| Managed Services |

| Training and Capacity Building |

| Advisory and Benchmarking |

| Other Consulting Approaches |

| Large Enterprises |

| Small and Medium Enterprises |

| Brazil |

| Argentina |

| Colombia |

| Chile |

| Peru |

| Rest of South America |

| By Service Type | Supply Chain Strategy and Network Design |

| Procurement and Sourcing | |

| Logistics and Distribution Optimization | |

| Inventory and Demand Planning | |

| Digital Supply Chain Transformation | |

| Sustainability and Green Supply Chain | |

| Risk and Resilience Consulting | |

| Other Service Types | |

| By End-User Industry | Retail and E-commerce |

| Manufacturing | |

| Food and Beverage | |

| Healthcare and Pharmaceuticals | |

| Automotive | |

| Consumer Packaged Goods | |

| Energy and Utilities | |

| Other End-User Industries | |

| By Consulting Approach | Project-Based Consulting |

| Managed Services | |

| Training and Capacity Building | |

| Advisory and Benchmarking | |

| Other Consulting Approaches | |

| By Organization Size | Large Enterprises |

| Small and Medium Enterprises | |

| By Geography | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America |

Key Questions Answered in the Report

How large will consulting spend on supply-chain services in South America be by 2031?

It is projected that the South America supply chain consulting services market will reach USD 1.208 billion by 2031, growing at a 4.12% CAGR from 2026.

Which service line is expanding fastest?

Sustainability and Green Supply Chain engagements are expected to register the quickest growth, advancing at a 7.31% CAGR through 2031.

What is driving the rise of managed services contracts?

Companies want continuous optimization, so they are shifting from one-off projects toward multi-year agreements that embed consultants into daily planning, inventory, and warehouse functions.

Why is Peru forecast to outpace other countries?

A USD 8.3 billion PPP amendment pipeline, large mining investments, and the Chancay-Sierra Central freight railway are accelerating demand for supply-chain consulting in Peru.

How are SMEs accessing consulting support despite high fees?

Government voucher schemes, electronic factoring platforms that unlock working capital, and standardized diagnostic toolkits are making advisory services more affordable for smaller firms.

What technologies are most in demand across client engagements?

AI-driven network twins, autonomous procurement agents, cloud-native ERP modules, and carbon-accounting dashboards are currently topping enterprise shopping lists for supply-chain transformation.

Page last updated on: