Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2020 - 2024 |

| Market Size (2026) | USD 2.66 Billion |

| Market Size (2031) | USD 5.09 Billion |

| Growth Rate (2026 - 2031) | 13.89% CAGR |

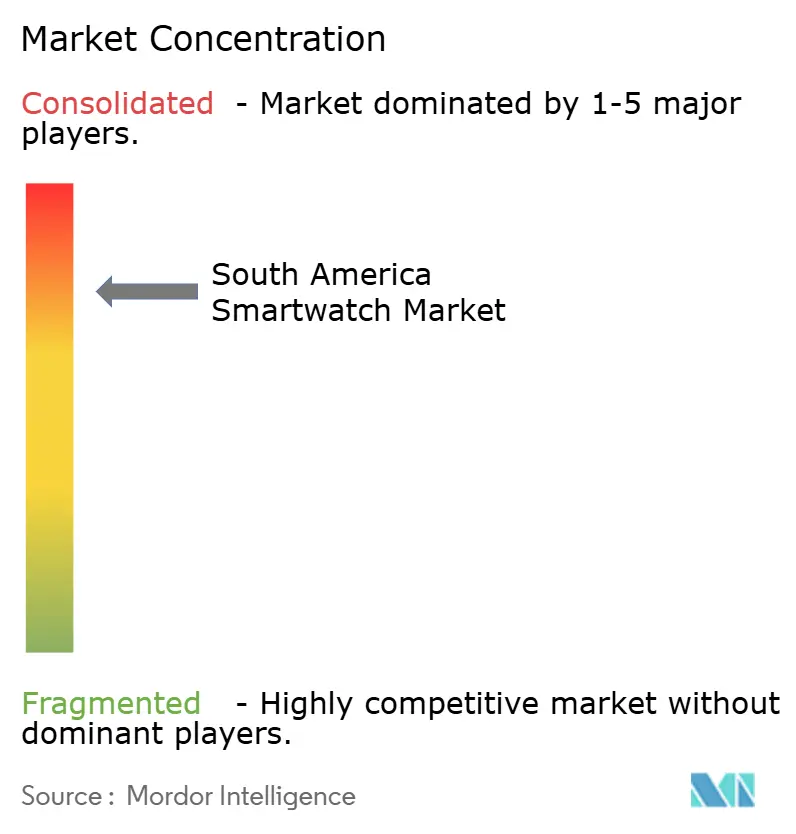

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South America Smartwatch Market Analysis by Mordor Intelligence

The South America smartwatch market size stands at USD 2.66 billion in 2026 and is projected to climb to USD 5.09 billion by 2031, translating into a 13.89% CAGR. The rise reflects falling Android device prices, aggressive e-commerce promotions, and expanding contactless payment rails. Rapid 5G deployment in Brazil and Chile, tariff reductions in Argentina, and the emergence of corporate wellness procurement further accelerate adoption. Vendors that localize assembly in Brazil gain a 10–15% landed-cost edge, while insurers in Brazil and Chile begin linking premiums to wearable data, deepening demand for clinically validated sensors. Momentum also comes from Pix NFC payments, which turn smartwatches into wallets, and from ANVISA rules that clarify how medical-grade wearables can qualify for reimbursement.

Key Report Takeaways

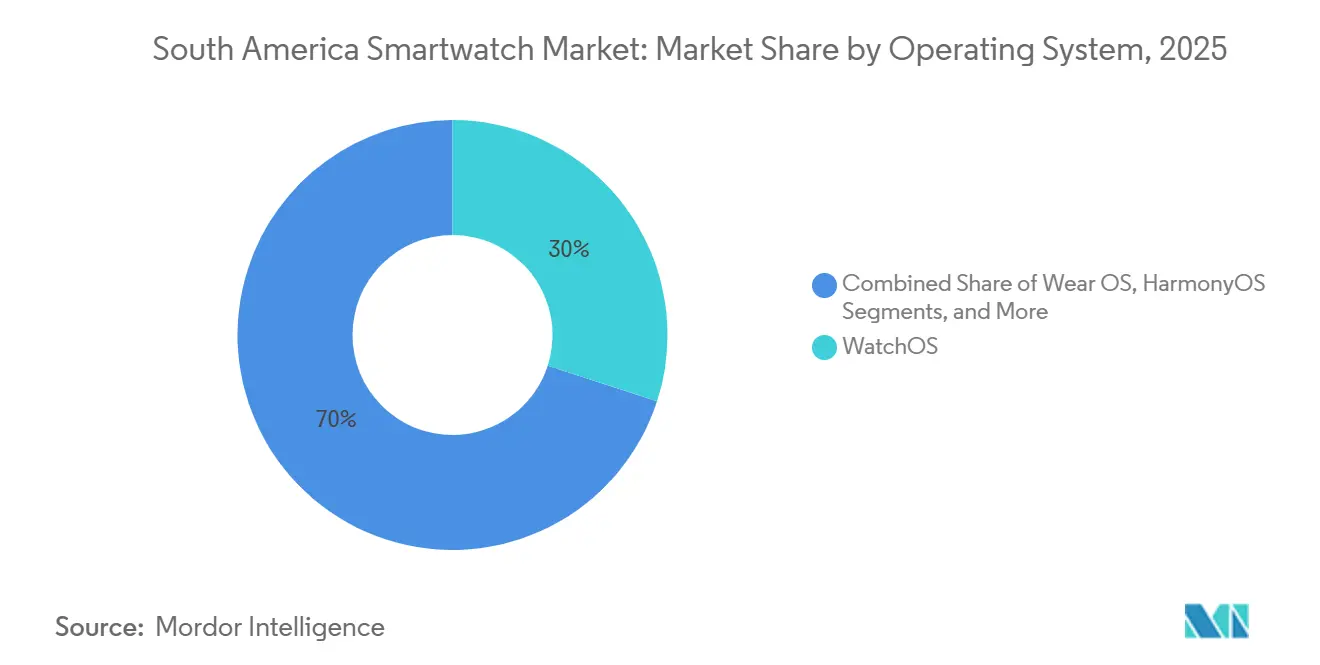

- By operating system, WatchOS led with 29.98% revenue share in 2025, while HarmonyOS is forecast to expand at a 14.43% CAGR through 2031.

- By display technology, AMOLED captured 68.12% of 2025 shipments; Micro-LED is projected to grow at a 14.65% CAGR to 2031.

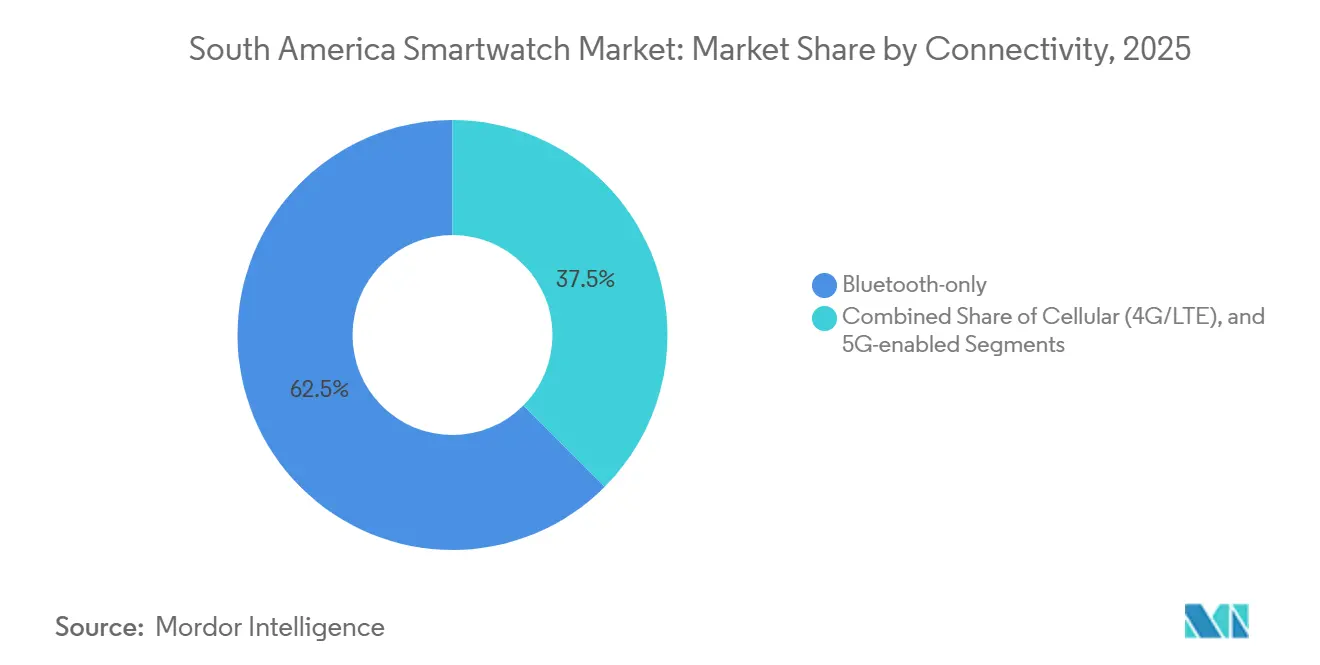

- By connectivity, Bluetooth-only models held 62.53% share of the South America smartwatch market size in 2025; 5G variants are advancing at a 14.78% CAGR.

- By application, fitness and wellness accounted for 48.23% of the South America smartwatch market size in 2025, whereas medical and chronic-care monitoring is set to climb at a 14.12% CAGR.

- By country, Brazil commanded 63.42% of regional revenue in 2025; Chile is the fastest-growing geography at a 14.92% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

South America Smartwatch Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Expansion of Affordable Android-Based Models | +3.2% | Brazil, Argentina, Rest of South America | Short term (≤ 2 years) |

| Growing Health-Insurance Incentives Tied to Wearable Data | +2.8% | Brazil, Chile, with pilot programs in Argentina | Medium term (2-4 years) |

| Integration of Contactless Payment Ecosystems | +2.5% | Brazil (Pix), Argentina (Modo), Chile (Transbank) | Medium term (2-4 years) |

| Corporate Wellness Programs Fueling Bulk Procurement | +1.9% | Brazil, Chile, with early adoption in mining and logistics sectors | Medium term (2-4 years) |

| 5G-Enabled Edge-Analytics Improving Battery Efficiency | +1.6% | Chile, urban Brazil (São Paulo, Rio de Janeiro), Buenos Aires | Long term (≥ 4 years) |

| Rise of E-commerce Flash-Sales in Brazil and Argentina | +1.4% | Brazil, Argentina | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rapid Expansion of Affordable Android-Based Models

Entry-level Wear OS and proprietary real-time operating system (RTOS) watches now retail 40–60% below Apple’s Watch SE, creating a volume surge in the South America smartwatch market. Xiaomi’s Redmi Watch 5 Lite debuted at BRL 171 (USD 31), and Huawei’s Watch GT 5 arrived at BRL 1,499 (USD 275), both undercutting Samsung’s Galaxy Watch 7 by roughly one-third. In Brazil, Samsung’s Manaus plant and Positivo’s Curitiba line suppress landed costs, letting brands hold price points even when the real weakens. Argentina’s inflation cooldown from 211% in late 2023 to 47% in April 2025 revives discretionary spending, so sub-BRL 500 (USD 92) options quickly capture first-time buyers.

Growing Health-Insurance Incentives Tied to Wearable Data

Brazilian and Chilean insurers have begun testing premium discounts tied to step counts, heart-rate variability, and sleep scores. SulAmérica and Bradesco Saúde are negotiating data-sharing APIs with wearable vendors while awaiting final guidance from the national health regulator ANS.[1]Agência Nacional de Saúde Suplementar, “Health Insurance Regulation,” ans.gov.br In Chile, the Superintendencia de Salud permits non-discriminatory wellness incentives, encouraging Isapre plans to bundle watches in annual policies. International precedents show actuarial upside: a RAND study on Vitality Active Rewards found a 4.8% claims reduction over 24 months when members met exercise goals. The upshot is sustained demand for sensors robust enough to pass medical audits.

Integration of Contactless Payment Ecosystems

Pix added NFC and biometric authentication in May 2024, letting watches tap-to-pay without smartphones.[2]Banco Central do Brasil, “Exchange Rate Statistics,” bcb.gov.br Pix handled 42 billion transactions in 2024, 31% of Brazil’s electronic payments, and its zero-fee model motivates merchants to accept wearables. Samsung’s Galaxy Watch Ultra embeds tokenized payment credentials directly in a secure element, trimming checkout latency by 200 milliseconds. Argentina’s Modo and Chile’s Transbank are following, although terminal penetration still trails Pix’s footprint, leaving room for growth.

Corporate Wellness Programs Fueling Bulk Procurement

Brazilian platform RadarFit supplies more than 60 corporate clients, rewarding employees who meet step targets with redeemable points. In Chile, NIXTEM equips mining and transport firms with fatigue-monitoring bands that track heart-rate variability and skin temperature. The Ministry of Labor in Brazil now allows companies to subsidize wearables as part of safety programs, so long as data collection meets LGPD consent rules. As enterprise demand scales, vendors with fleet-management dashboards and long warranties gain an edge.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Currency Volatility Elevating Import Prices | -2.1% | Argentina, Brazil, with spillover to Chile | Short term (≤ 2 years) |

| Data-Privacy Compliance Costs (LGPD) | -1.3% | Brazil, with extraterritorial implications for regional platforms | Medium term (2-4 years) |

| Limited After-Sales Service Network Outside Tier-1 Cities | -0.9% | Rest of South America, tier-2 cities in Brazil and Argentina | Medium term (2-4 years) |

| Competition from Smart Rings and Ear-Worn Devices | -0.6% | Urban Brazil, Chile, Argentina | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Currency Volatility Elevating Import Prices

The real lost 8.2% against the dollar in early 2025, while the peso slid 12.3%, forcing importers to reprice inventory mid-quarter. Components priced in CNY, KRW, or TWD add a 15–20% cost premium when currencies swing. Samsung’s Manaus and Positivo’s Curitiba plants hedge this risk by invoicing in reais, but brands reliant on Asian imports face margin compression or lost share during depreciation cycles.

Data-Privacy Compliance Costs (LGPD)

LGPD requires explicit consent for biometric data, 72-hour breach disclosures, and impact assessments for algorithms that infer health status. ANVISA’s Technical Note 12/2024 adds regularization for diagnostic claims, aligning medical-grade watches with Class II device rules. Start-ups spend 8–12% of gross margin on counsel, servers, and audits, versus 2–3% for Apple and Samsung, effectively raising entry barriers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Operating System: HarmonyOS Gains Ground on Localized Pricing

WatchOS secured 29.98% of 2025 revenue, underscoring Apple’s grip on the premium tier of the South America smartwatch market share. HarmonyOS, however, is projected to expand at a 14.43% CAGR, propelled by Huawei’s BRL 1,499 (USD 275) Watch GT 5, which undercuts Apple’s entry model by roughly 35%. Wear OS dominates the mid-priced bracket through Samsung and Fossil, while proprietary RTOS devices from Xiaomi and Amazfit control sub-BRL 500 price points, sacrificing app breadth for battery endurance.

Regulation now shapes operating-system uptake. ANVISA clearance for Apple Watch ECG shifts medical and chronic-care demand toward platforms with proven diagnostics, helping WatchOS capture prescription-driven sales that push the South America smartwatch market size for medical applications higher.[3]ANVISA, “Technical Note 12/2024,” gov.br/anvisa HarmonyOS and RTOS vendors must fund clinical validation studies, creating a 12-18 month lag before they can claim similar functionality in Brazil and Chile. In Argentina, where guidance remains incomplete, price elasticity prevails and favors lower-cost RTOS watches.

By Display Technology: Micro-LED Emerges Despite Cost Barriers

AMOLED panels commanded 68.12% of 2025 shipments, supported by falling costs and vivid 100,000:1 contrast ratios. Micro-LED, forecast to grow at 14.65% CAGR, offers 30% lower power draw and 50% higher peak brightness, key for equatorial sunlight. Premium demand in São Paulo, Santiago, and Buenos Aires has begun migrating toward Micro-LED prototypes as early adopters chase multi-day batteries and outdoor legibility.

Entry-level TFT-LCD displays persist in sub-USD 100 watches, but their limited 1,000:1 contrast and 30-millisecond response time confine them to price-sensitive geographies. As PlayNitride’s Gen 6 fab reaches volume in 2027, Micro-LED panels should drop near AMOLED cost parity, giving vendors a 15–20% margin lift on flagship SKUs. Brands able to articulate this battery-life edge will widen their South America smartwatch market share among outdoor sports enthusiasts.

By Connectivity: 5G Models Unlock Edge Analytics

Bluetooth-only units captured 62.53% of 2025 shipments thanks to lower bills of materials and the reality that 78% of users keep smartphones within arm’s reach. LTE watches sell chiefly to runners and parents, but their monthly data fees raise total ownership costs by about 25%, muting uptake. 5G variants are projected to grow at a 14.78% CAGR as network slicing and edge computing trim battery drain, with Samsung’s Galaxy Watch Ultra LTE leading adoption across São Paulo and Santiago.

Infrastructure readiness splits the region. Chile’s 86% 5G coverage fosters standalone watches for enterprise safety programs and elderly monitoring, boosting the South America smartwatch market size for connected wearables. Brazil’s capitals follow closely, yet Argentina lags because only three metro areas have commercial 5G service, forcing most buyers to stay with Bluetooth models. Vendors must balance radio power budgets with the multi-day battery life prized by endurance athletes.

By Application: Medical Use Cases Gain Regulatory Tailwinds

Fitness and wellness retained 48.23% share of the South America smartwatch market size in 2025, covering step counts, guided workouts, and sleep scores. Medical and chronic-care monitoring is now the fastest-rising slice, forecast at a 14.12% CAGR through 2031 as ANVISA charts a reimbursement path for devices with diagnostic claims. Apple Watch ECG clearance already lets cardiologists prescribe the device for atrial-fibrillation screening, and Huawei’s Watch D2 awaits blood-pressure approval.

Payment, transit, and access-control functions are converging into a “super-app” experience. Pix NFC upgrades let users tap-to-pay without phones, while Chile’s ClaveÚnica digital ID integrates watches into public-transport fare systems. As consumers demand one device for health, finance, and security, brands lacking broad developer ecosystems could see their South America smartwatch market share erode in favor of platforms that aggregate these services seamlessly.

Geography Analysis

Brazil’s dominance in the South America smartwatch market stems from scale, local manufacturing, and a Pix-enabled payments culture that turns watches into day-to-day wallets. Brands assembled in Manaus enjoy a 10–15% cost cushion, letting them flood massive Black Friday campaigns without eroding margins. Carrier bundles that waive the first six months of LTE fees further improve uptake in São Paulo and Rio de Janeiro.

Chile, although smaller, sets the pace in infrastructure readiness. Its 86% 5G coverage, pervasive fiber backbone, and high regulatory clarity invite insurers and mining firms to adopt real-time health analytics. The result is a higher attach rate for LTE or 5G variants that stream biometric data directly to enterprise dashboards.

Argentina’s resurgence hinges on tariff relief and moderating inflation, yet currency swings still compress reseller margins. Distributors prefer just-in-time shipments, causing frequent sell-outs of popular SKUs in Córdoba and Mendoza. Growth in Colombia, Peru, and Ecuador trails due to fragmented retail and limited after-sales service, but rising e-commerce penetration could unlock catch-up demand through 2028.

Competitive Landscape

The South America smartwatch market is moderately concentrated. Apple and Samsung collectively controlled major share of 2025 revenue, but Xiaomi, Huawei, Zepp Health, and Positivo drive intense competition below USD 150. Premium brands rely on ecosystem lock-in, while budget rivals pack blood-oxygen sensors and 14-day batteries at one-third of flagship pricing. Huawei’s HarmonyOS devices added 2 percentage points of share regionally in 2025 by combining LTE eSIM with aggressive pricing.

Local production is the core strategic lever. Samsung’s Manaus site launched three SKUs within 90 days, benefiting from tax incentives and rapid logistics cycles. Apple’s vertical silicon and sensor stack cushions currency dents but remains exposed to shipping delays. Huawei’s BRL 1,499 Watch GT 5 puts price pressure on Samsung’s mid-tier Galaxy Watch FE. Vendors unable to localize assembly or secure regional component contracts face widening cost gaps, especially when currencies slide.

White-space opportunities cluster around medical wearables, enterprise wellness, and remote-area tracking for mining or agriculture. LGPD compliance costs deter under-capitalized entrants, inadvertently protecting incumbents with legal and engineering resources. Over the forecast horizon, supply-chain resilience will outweigh pure brand equity as the primary determinant of share shifts in the South America smartwatch market.

South America Smartwatch Industry Leaders

Apple Inc.

Samsung Electronics Co., Ltd.

Huawei Technologies Co., Ltd.

Garmin Ltd.

Xiaomi Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Samsung launched the Galaxy Watch Ultra LTE with 5G standalone connectivity and MEC offload.

- March 2025: Mercado Libre committed BRL 100 million (USD 18.5 million) in Black Friday coupons for electronics, including smartwatches.

- January 2025: Argentina eliminated 16% cell-phone import tariffs, lifting smartwatch affordability.

- November 2024: Huawei released four HarmonyOS watches in Brazil, led by the BRL 1,499 Watch GT 5.

South America Smartwatch Market Report Scope

The South America Smartwatch Market refers to the market for wearable devices designed to perform various functions such as fitness tracking, health monitoring, communication, and personal assistance, integrated with advanced technologies like operating systems, display technologies, and connectivity options. These devices cater to diverse applications across fitness, medical care, and personal assistance.

The South America Smartwatch Market Report is Segmented by Operating System (WatchOS, Wear OS, HarmonyOS, and Proprietary/RTOS), Display Technology (AMOLED, Micro-LED, and TFT-LCD), Connectivity (Bluetooth-only, Cellular 4G/LTE, and 5G-enabled), Application (Fitness and Wellness, Medical and Chronic-care, Personal Assistance and Payments, and Other Applications), and Geography (Brazil, Argentina, Chile, Rest of South America). The Market Forecasts are Provided in Terms of Value (USD).

By Operating System

| WatchOS |

| Wear OS |

| HarmonyOS |

| Proprietary / RTOS |

By Display Technology

| AMOLED |

| Micro-LED |

| TFT-LCD |

By Connectivity

| Bluetooth-only |

| Cellular (4G/LTE) |

| 5G-enabled |

By Application

| Fitness and Wellness |

| Medical and Chronic-care |

| Personal Assistance and Payments |

| Other Applications |

By Country

| Brazil |

| Argentina |

| Chile |

| Rest of South America |

| By Operating System | WatchOS |

| Wear OS | |

| HarmonyOS | |

| Proprietary / RTOS | |

| By Display Technology | AMOLED |

| Micro-LED | |

| TFT-LCD | |

| By Connectivity | Bluetooth-only |

| Cellular (4G/LTE) | |

| 5G-enabled | |

| By Application | Fitness and Wellness |

| Medical and Chronic-care | |

| Personal Assistance and Payments | |

| Other Applications | |

| By Country | Brazil |

| Argentina | |

| Chile | |

| Rest of South America |

Key Questions Answered in the Report

How large is the South America smartwatch market in 2026?

The market is valued at USD 2.66 billion in 2026 and is on track to reach USD 5.09 billion by 2031.

What CAGR is forecast for smartwatches in South America?

The market is expected to grow at a 13.89% CAGR during 2026-2031.

Which country shows the fastest growth?

Chile is forecast to expand at a 14.92% CAGR, helped by widespread 5G and high internet penetration.

Which operating system is gaining share fastest?

HarmonyOS leads growth with a projected 14.43% CAGR as Huawei undercuts premium rivals on price.

How does Pix influence smartwatch adoption?

Pix’s NFC upgrade lets watches perform tap-to-pay, boosting everyday utility and accelerating device uptake.

What is the main restraint for new entrants?

LGPD compliance costs and medical-device regulations raise entry barriers, favoring well-capitalized incumbents.

Page last updated on: