Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2020 - 2024 |

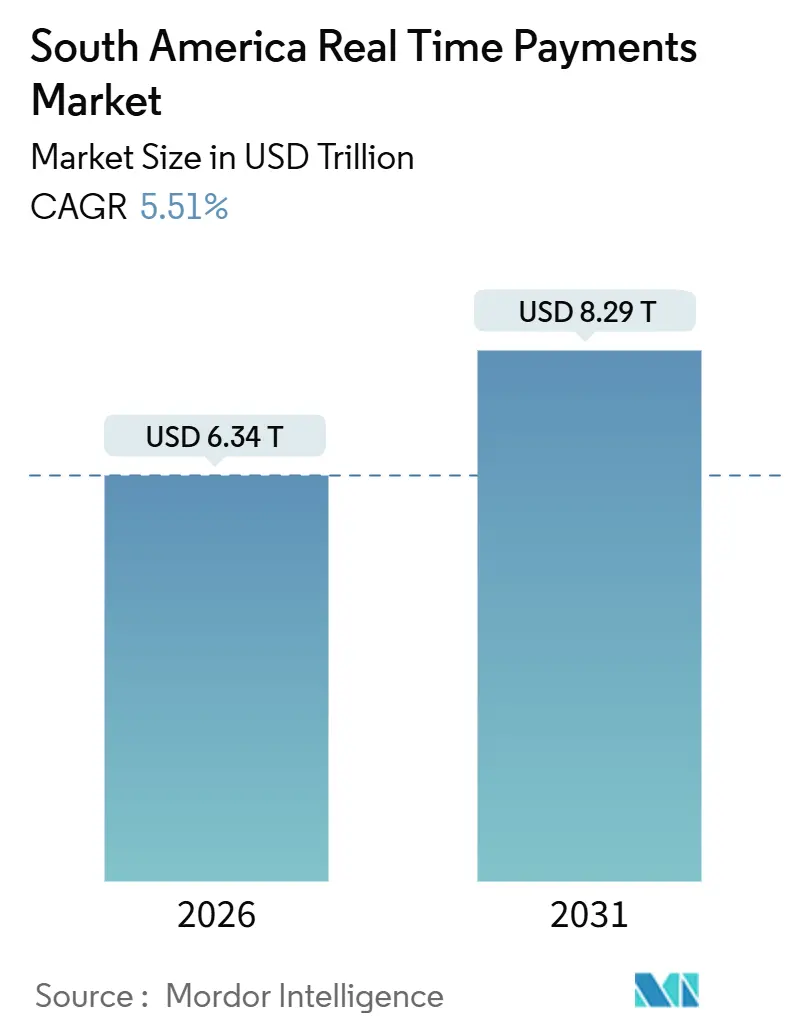

| Market Size (2026) | USD 6.34 Trillion |

| Market Size (2031) | USD 8.29 Trillion |

| Growth Rate (2026 - 2031) | 5.51% CAGR |

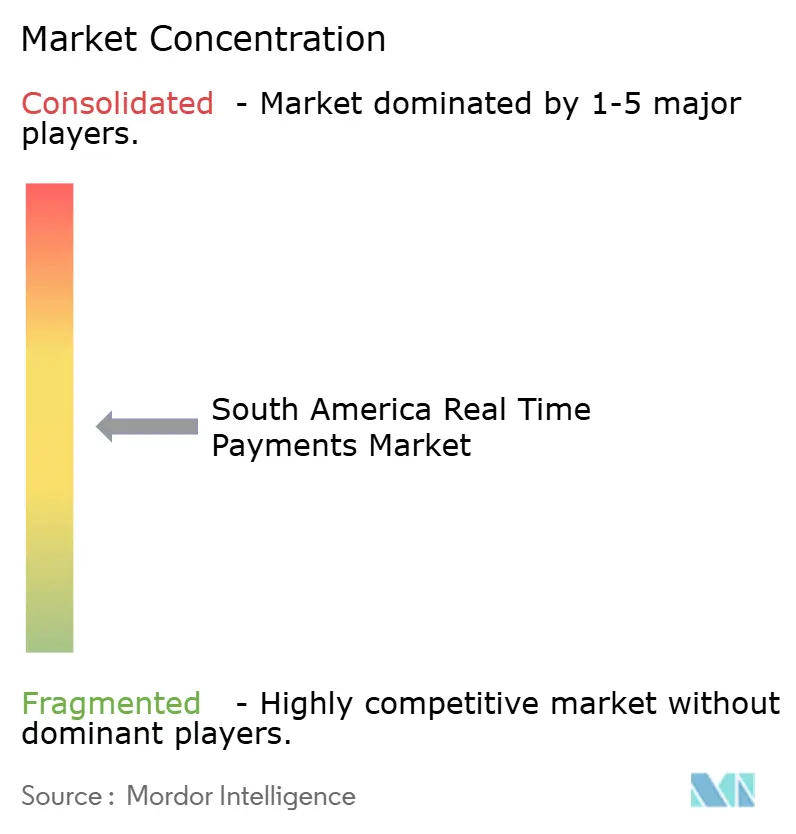

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South America Real Time Payments Market Analysis by Mordor Intelligence

The South America real time payments market size is valued at USD 6.34 trillion in 2026 and is forecast to reach USD 8.29 trillion by 2031, advancing at a 5.51% CAGR. Momentum stems from Brazil’s Pix rail, rising mobile-commerce volumes, and a regulatory push toward instant settlement across the region. Merchants reduce working-capital drag by shifting away from card-network rails, while open-banking mandates shorten integration cycles for fintechs seeking to embed payment initiation. Cloud deployment, now the preferred architecture, lowers unit processing costs and accelerates feature rollouts. Competition is moving to the application layer where data monetization, fraud analytics, and credit scoring services differentiate otherwise commoditized transaction routing.

Key Report Takeaways

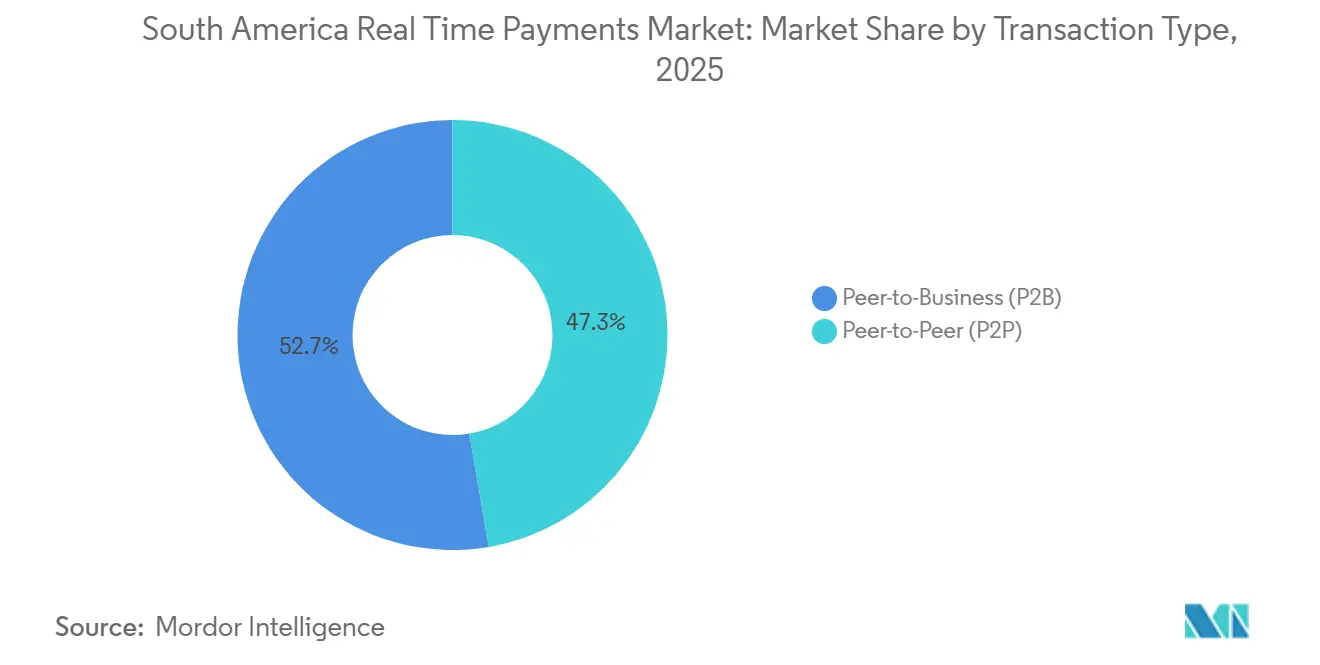

- By transaction type, peer-to-peer transfers held 47.31% of South America real time payments market share in 2025, whereas peer-to-business flows are projected to post the fastest 5.78% CAGR through 2031.

- By component, platform, and solution providers commanded 60.83% of the revenue share in 2025, yet services are the fastest-growing line, advancing at a 6.21% CAGR.

- By deployment mode, cloud-based implementations captured 68.34% of South America real time payments market size in 2025; on-premises installations trail with limited growth.

- By enterprise size, small and medium enterprises accounted for 51.36% of adoption in 2025 and will expand at a 5.76% CAGR, the highest among user cohorts.

- By end-user industry, retail and e-commerce led with 33.67% of transaction value in 2025 and will post a 6.27% CAGR through 2031.

- By country, Brazil generated 86.12% of 2025 transaction value, yet Colombia is set to grow the fastest at a 7.41% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

South America Real Time Payments Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government-Led National Instant Payment Schemes (e.g., Pix) | +1.80% | Brazil, Colombia, Argentina, with spillover to Chile and Peru | Medium term (2-4 years) |

| Increasing Smartphone Penetration | +1.20% | Brazil, Colombia, Argentina, Chile, Peru, Rest of South America | Long term (≥ 4 years) |

| Surge in Mobile E-Commerce and Digital Wallet Adoption | +0.90% | Brazil, Argentina, Colombia, with early gains in Santiago, Bogotá, Buenos Aires | Medium term (2-4 years) |

| Open Banking Frameworks Accelerating RTP Integration | +1.00% | Brazil, Colombia, Chile, with regulatory influence from Banco Central do Brasil, Superintendencia Financiera de Colombia | Short term (≤ 2 years) |

| QR-Code Standardisation Mandates Boosting Merchant Acceptance | +0.70% | Argentina, Chile, Peru, with ISO 20022 and EMVCo compliance frameworks | Medium term (2-4 years) |

| Cross-Border Interoperability Pilots Expanding B2B RTP Flows | +0.50% | Brazil-Argentina corridor, Colombia-Peru pilot zones | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Government-Led National Instant Payment Schemes

Brazil’s Pix counted 156 million active users 73% of adults by December 2024 and processed BRL 17.2 trillion (USD 3.44 trillion) that year.[1]Banco Central do Brasil, “Pix Statistics and Transaction Data,” BCB.GOV.BR Colombia’s Bre-B, launched in November 2024, signed up 12 million users within 90 days, outpacing initial projections by 40%. Argentina’s Transferencias 3.0 unified fragmented rails, enabling QR interoperability across 47 banks by 2024.[2]Banco Central de la República Argentina, “Transferencias 3.0 Framework,” BCRA.GOB.AR Eliminating interchange fees sharply lowers acceptance costs, forcing banks to shift revenue models toward data analytics, credit underwriting, and value-added APIs.

Increasing Smartphone Penetration

Regional smartphone penetration hit 78% in 2025, led by Brazil, Chile, and Argentina above 80%.[3]International Telecommunication Union, “ICT Statistics 2025,” ITU.INT Subsidized 4G handsets pushed Colombia to 74%, while Peru’s rural adoption accelerated to 52% on government connectivity programs.[4]GSMA, “Mobile Economy Latin America 2025,” GSMA.COM Affordable Android devices let micro-merchants accept QR-based instant payments without POS terminals, trimming acceptance costs by up to 70% compared with card infrastructure. This device ubiquity cements QR payments as the default checkout option for informal economies.

Open Banking Frameworks Accelerating RTP Integration

Brazil’s phased open-banking rollout finished in 2024, mandating standardized payment-initiation APIs for large banks. Colombia issued similar rules in 2024, requiring banks to expose APIs by mid-2025. Chile adopted real-time payment initiation standards the same year. These rules remove integration friction, letting third-party apps embed instant checkout seamlessly and forcing banks to compete on API reliability and settlement speed

QR-Code Standardization Mandates Boosting Merchant Acceptance

Argentina mandated QR interoperability under the DEBIN standard in 2024, eliminating multiple proprietary codes. Chile’s guidelines aligned domestic QR codes with ISO 20022 messaging, opening cross-border acceptance with Peru and Colombia. Brazil’s Pix adopted EMVCo QR specs in 2024, allowing merchants to accept any compliant wallet via a single static or dynamic code. Streamlined acceptance drives network effects, giving early adopters a durable merchant-coverage lead.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Payment Fraud and Social-Engineering Attacks | -0.80% | Brazil, Colombia, Argentina, with spillover to Chile and Peru | Short term (≤ 2 years) |

| Legacy Core-Bank Integration and Cost Barriers | -0.60% | Argentina, Peru, Rest of South America, with limited impact in Brazil | Medium term (2-4 years) |

| Fragmented Interoperability Outside Major Schemes | -0.40% | Chile, Peru, Ecuador, Bolivia, with national-level constraints | Long term (≥ 4 years) |

| Rural Connectivity Gaps in Amazon and Andean Regions | -0.30% | Peru, Colombia, Brazil (Amazon states), with infrastructure deficits in remote areas | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Payment Fraud and Social-Engineering Attacks

Social-engineering scams made up 68% of Pix-related fraud attempts in 2024, with losses surpassing BRL 2.5 billion (USD 500 million). Colombia recorded a 42% jump in instant-payment fraud during Bre-B’s first six months of operation. Argentina imposed biometric checks for transfers above ARS 50,000 (USD 500) in 2025 to combat account takeovers. Instant and irrevocable settlement shifts liability to users and banks, eroding trust among first-time adopters and prompting stricter but sometimes friction-inducing security measures.

Legacy Core-Bank Integration and Cost Barriers

Core systems in Argentina average 18 years of age, requiring costly middleware to connect to ISO 20022 APIs. Peruvian mid-tier banks face USD 2 million-USD 5 million outlays for real-time compatibility, equating to over 15% of annual IT budgets. Chile reported that nearly one-quarter of institutions missed its 2024 open-banking deadline due to technical debt. Smaller lenders risk losing high-growth segments as integration delays push customers toward digital-first competitors.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Transaction Type: Peer-To-Business Uptake Accelerates

Peer-to-business flows accounted for 52.69% of incremental value added in 2025 and are forecast to grow at a 5.78% CAGR. Merchant adoption pivots on cash-flow predictability and avoidance of card-network interchange, benefits underscored by Colombia’s Bre-B onboarding of 300,000 SMEs in its first quarter. Peer-to-peer transfers still dominate in absolute terms but have plateaued in Brazil’s metropolitan centers as usage nears saturation. The South America real time payments market size attached to merchant flows will therefore expand faster than the broader consumer segment. Providers that prioritize reconciliation APIs, automated refunds, and loyalty hooks can capture higher-value tickets Brazil’s 2024 Pix merchant average ticket stood at BRL 287 (USD 57) versus BRL 142 (USD 28) for P2P.

The strategic implication is a shift in monetization from volume-based fees to data-driven lending and embedded-finance services. Argentina processed 80 million DEBIN merchant transactions in 2024, primarily for utilities and e-commerce, while Chile leverages instant business payments to improve supply-chain liquidity. As cross-border pilots mature, B2B corridors will add incremental fee pools, further enhancing the peer-to-business value proposition.

By Component: Services Emerge as Margin Engine

Platforms and solutions delivered 60.83% of 2025 revenue, yet services will outpace with a 6.21% CAGR as banks outsource integration, fraud monitoring, and regulatory compliance. Colombia’s Bre-B migration required 40 banks to adopt ISO 20022 and advanced fraud detection within 12 months, driving demand for managed services. Argentina’s banks spent an estimated USD 180 million on compliance consulting in 2024 to meet Transferencias 3.0 timelines. Vendors bundling fraud-as-a-service, API gateways, and analytics achieve stickier contracts and recurring revenue.

Recurring service lines improve gross margins as infrastructure routing fees commoditize. Brazil’s 2024 Pix ecosystem generated roughly USD 500 million in compliance and fraud service revenue, a figure expected to rise as biometric mandates extend to smaller transactions. For integrators, the South America real time payments market share of service revenue is therefore primed for steady gains.

By Deployment Mode: Cloud Consolidates Lead

Cloud deployments captured 68.34% of 2025 South America real time payments market share and will climb further at a 5.76% CAGR. Pix’s 42 billion transactions in 2024 would have required prohibitive on-premises scaling; multi-cloud approval removed a key regulatory hurdle. Colombia designed Bre-B as a cloud-native service, onboarding 12 million users without latency issues. On-premises persists mainly among state-owned banks sensitive to data-sovereignty concerns, particularly in Argentina and Chile.

Cloud elasticity speeds feature deployment Peru’s 2024 pilot pushed fraud-detection algorithm updates region-wide within hours. Long term, on-premises holdouts confront rising maintenance expense and slower innovation cycles, tilting competitive advantage toward cloud-first players able to offer lower fees and richer functionality per transaction.

By Enterprise Size: SMEs Anchor Volume Growth

Small and medium enterprises represented 51.36% of 2025 adoption and will maintain a 5.76% CAGR, the highest among user groups. Pix’s zero merchant discount rate appeals to Brazil’s micro-merchants earning under BRL 360,000 (USD 72,000) annually. Argentina enabled 150,000 SMEs to accept instant payments in 2024, with 62% citing improved cash flow as the primary benefit. Colombia’s smartphone-only merchant onboarding slashed enrolment friction by 80%.

Large enterprises leverage instant payments for treasury optimization and cross-border supplier payouts, demanding ERP integration and real-time liquidity tools. Vendors must therefore deliver tiered products: streamlined, low-cost packages for SMEs and full-stack APIs for corporates. The dual strategy maximizes South America real time payments market size capture across segments.

By End-User Industry: Retail and E-Commerce Dominate

Retail and e-commerce accounted for 33.67% of transaction value in 2025 and will post a 6.27% CAGR. Mobile-first consumers favour one-tap Pix or Mercado Pago checkout, reducing cart abandonment tied to boleto or credit-card authorization holds. Utilities and telecom providers processed 1.2 billion instant payments in Brazil during 2024, shrinking bill-collection cycles from 5 days to 10 seconds. Government agencies disbursed BRL 120 billion (USD 24 billion) in social benefits via Pix in 2024, trimming leakage and cash-handling costs.

Although banking and insurance remain sizable, regulatory constraints temper growth. Healthcare, logistics, and hospitality are emerging but fragmented. Providers that embed vertical-specific features inventory sync for retailers, tax-ID validation for government payouts create switching costs and deepen wallet share within the South America real time payments market.

Geography Analysis

Brazil generated 86.12% of 2025 transaction value, processing 42 billion Pix payments in 2024 and peaking at 180 million transactions on Black Friday. Yet Colombia’s 7.41% forecast CAGR illustrates that infrastructure maturity can be overtaken by aggressive fee waivers; zero merchant charges for Bre-B’s first 24 months accelerated SME uptake. Argentina contributed 8% of value, but peso-linked capital controls limit cross-border flows despite 1.5 billion domestic instant payments in 2024.

Chile and Peru collectively hold under 6% share, hindered by staggered rollouts and fragmented schemes. Peru’s phased approach begins in Lima and Arequipa before rural extension, slowing near-term volumes. Smaller markets Ecuador, Bolivia, Paraguay, Uruguay, Venezuela face dollarization, limited banking penetration, or political instability, pushing meaningful adoption outside the 2026-2031 window.

Cross-border pilots point to a hub-and-spoke future with Pix as the anchor. Brazil-Argentina tests executed 50,000 transactions under 60 seconds, proving technical feasibility but exposing foreign-exchange complexities. Colombia-Peru pilots impose USD 500 caps and manual compliance checks, limiting early volumes. The topology suggests bilateral links will expand piecemeal rather than through a single South American clearinghouse.

Competitive Landscape

State-backed rails Pix, Bre-B, and Transferencias 3.0 dominate the scene, routing over 75% of transactions. However, competition is heating up at the application layer. In 2024, Mercado Pago capitalized on same-day credit offers at checkout, processing 2 billion Pix payments accounting for 4.8% of the total Pix volume. By bundling credit offers with checkout, Mercado Pago has positioned itself as a key player in the instant payments ecosystem. Meanwhile, Nubank, integrating Pix for its 95 million users, transformed instant-payment histories into rapid 10-second approvals for unsecured loans. This innovation has allowed Nubank to streamline loan approvals and enhance customer experience. Card schemes are also shifting: Mastercard’s Move platform now settles cross-border corporate payments in under a minute, enabling faster and more efficient international transactions. Similarly, Visa’s B2B Connect is honing in on supply-chain financing, addressing critical needs in global trade and logistics.

Local players PagSeguro and StoneCo are leveraging instant-payment data to boost working-capital loans, resulting in a credit portfolio growth exceeding 20% in 2024. By utilizing real-time payment data, these acquirers are expanding their financial services offerings and strengthening their market presence. On a global scale, processors Adyen and Stripe are simplifying the landscape for multinational merchants with unified APIs that mask the complexities of Pix and Bre-B.

These APIs enable seamless integration for merchants, reducing operational hurdles and enhancing cross-border payment capabilities. As ISO 20022 mandates reshape routing dynamics, the South American real-time payments market sees fraud analytics, uptime, and ecosystem partnerships emerge as pivotal differentiators. These factors are becoming increasingly critical for stakeholders aiming to maintain a competitive edge in this rapidly evolving market.

South America Real Time Payments Industry Leaders

ACI Worldwide Inc.

Mastercard Inc.

Visa Inc.

Fiserv Inc.

Fidelity National Information Services Inc. (FIS)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Banco Central do Brasil extended biometric requirements to all Pix transfers above BRL 500 (USD 100), targeting residual social-engineering fraud.

- October 2025: Banco de la República Colombia confirmed Bre-B crossed 500 million cumulative transactions within its first year, maintaining zero merchant fees.

- August 2025: Peru’s central bank expanded its instant-payment pilot to Cusco and Trujillo, onboarding 4,000 merchants within two months.

- November 2024: Banco de la República Colombia launched Bre-B, enrolling 12 million users in 90 days and processing 200 million transactions in its first quarter.

South America Real Time Payments Market Report Scope

The South America Real Time Payments Market Report is Segmented by Transaction Type (Peer-to-Peer, Peer-to-Business), Component (Platform/Solution, Services), Deployment Mode (Cloud, On-Premise), Enterprise Size (Large Enterprises, Small and Medium Enterprises), End-User Industry (Retail and E-Commerce, BFSI, Utilities and Telecom, Healthcare, Government and Public Sector, Other End-User Industries), and Geography (Brazil, Argentina, Chile, Colombia, Peru, Rest of South America). The Market Forecasts are Provided in Terms of Value (USD).

By Transaction Type

| Peer-to-Peer (P2P) |

| Peer-to-Business (P2B) |

By Component

| Platform / Solution |

| Services |

By Deployment Mode

| Cloud |

| On-Premise |

By Enterprise Size

| Large Enterprises |

| Small and Medium Enterprises |

By End-User Industry

| Retail and E-Commerce |

| BFSI |

| Utilities and Telecom |

| Healthcare |

| Government and Public Sector |

| Other End-User Industries |

By Country

| Brazil |

| Argentina |

| Chile |

| Colombia |

| Peru |

| Rest of South America |

| By Transaction Type | Peer-to-Peer (P2P) |

| Peer-to-Business (P2B) | |

| By Component | Platform / Solution |

| Services | |

| By Deployment Mode | Cloud |

| On-Premise | |

| By Enterprise Size | Large Enterprises |

| Small and Medium Enterprises | |

| By End-User Industry | Retail and E-Commerce |

| BFSI | |

| Utilities and Telecom | |

| Healthcare | |

| Government and Public Sector | |

| Other End-User Industries | |

| By Country | Brazil |

| Argentina | |

| Chile | |

| Colombia | |

| Peru | |

| Rest of South America |

Key Questions Answered in the Report

What is the current transaction value of the South America real time payments market?

The market processed USD 6.34 trillion in 2026.

How fast is the market expected to grow?

It is projected to achieve a 5.51% CAGR, reaching USD 8.29 trillion by 2031.

Which country is expanding the quickest?

Colombia shows the fastest trajectory with a 7.41% CAGR forecast.

Why are merchants adopting instant payments?

Instant settlement improves cash flow, avoids interchange fees, and lowers acceptance costs by up to 70%.

What share do cloud deployments hold?

Cloud implementations represented 68.34% of 2025 deployments and continue to rise.

Which segment leads by industry?

Retail and e-commerce command 33.67% of transaction value and are growing at a 6.27% CAGR.

What technological capabilities differentiate leading FM providers?

Digital work-order platforms, IoT-enabled predictive maintenance, and real-time energy dashboards help providers cut downtime, lower costs, and meet ESG targets.

Page last updated on: