South America Pumps Market Size and Share

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2020 - 2023 |

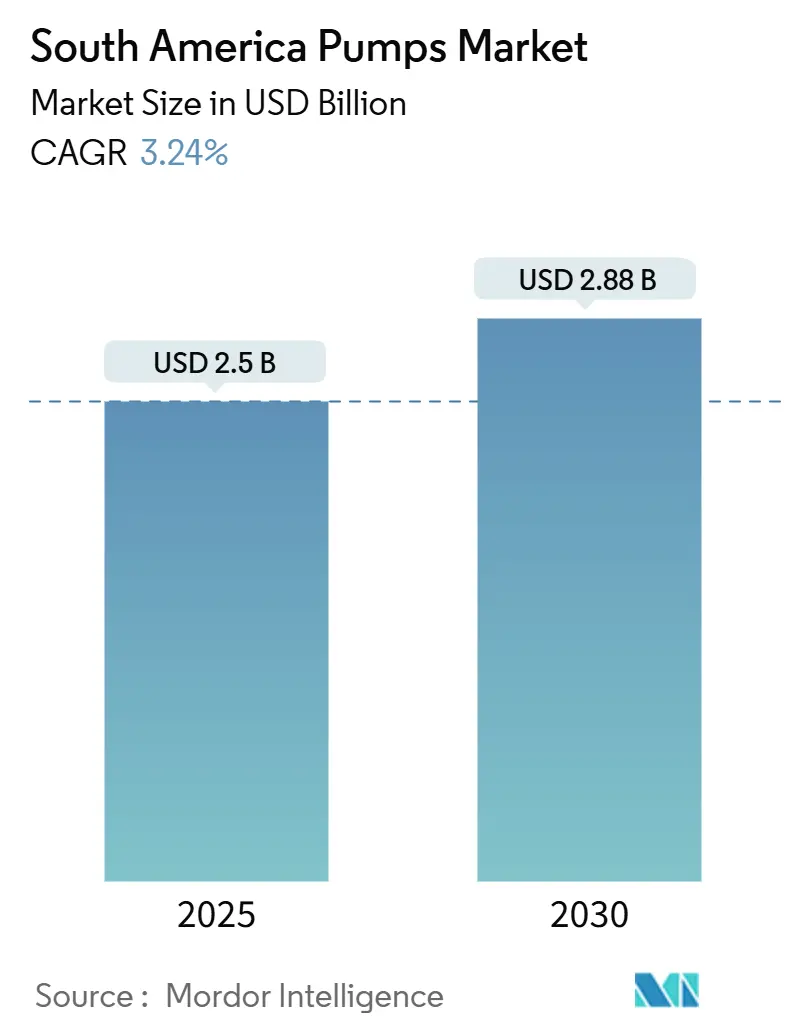

| Market Size (2025) | USD 2.5 Billion |

| Market Size (2030) | USD 2.88 Billion |

| Growth Rate (2025 - 2030) | 3.24% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South America Pumps Market Analysis by Mordor Intelligence

The South America Pumps Market size is estimated at USD 2.5 billion in 2025, and is expected to reach USD 2.88 billion by 2030, at a CAGR of 3.24% during the forecast period (2025-2030).

Legacy municipal networks still underpin baseline volumes, yet the growth catalyst is shifting to Petrobras’ USD 111 billion pre-salt program, lithium-brine projects in the Atacama, and copper-mine expansions that demand high-pressure, corrosion-resistant designs.[1]Petrobras, “2025-2029 Strategic Plan Highlights,” petrobras.com.br Chile and Peru together have more than USD 120 billion in approved mining capital, lifting the call for solar-powered submersible and slurry pumps that can run at altitudes above 4,000 meters.[2]Comisión Chilena del Cobre (COCHILCO), “Mining Investment Outlook 2024-2033,” cochilco.cl Simultaneously, Brazil’s 2024 sanitation privatization wave unlocked USD 100 billion for water infrastructure upgrades, accelerating fleet replacement cycles in the South America pumps market.

Key Report Takeaways

- By pump type, centrifugal pumps held 49.9% of the South America pumps market share in 2024 and are forecast to expand at a 4% CAGR through 2030.

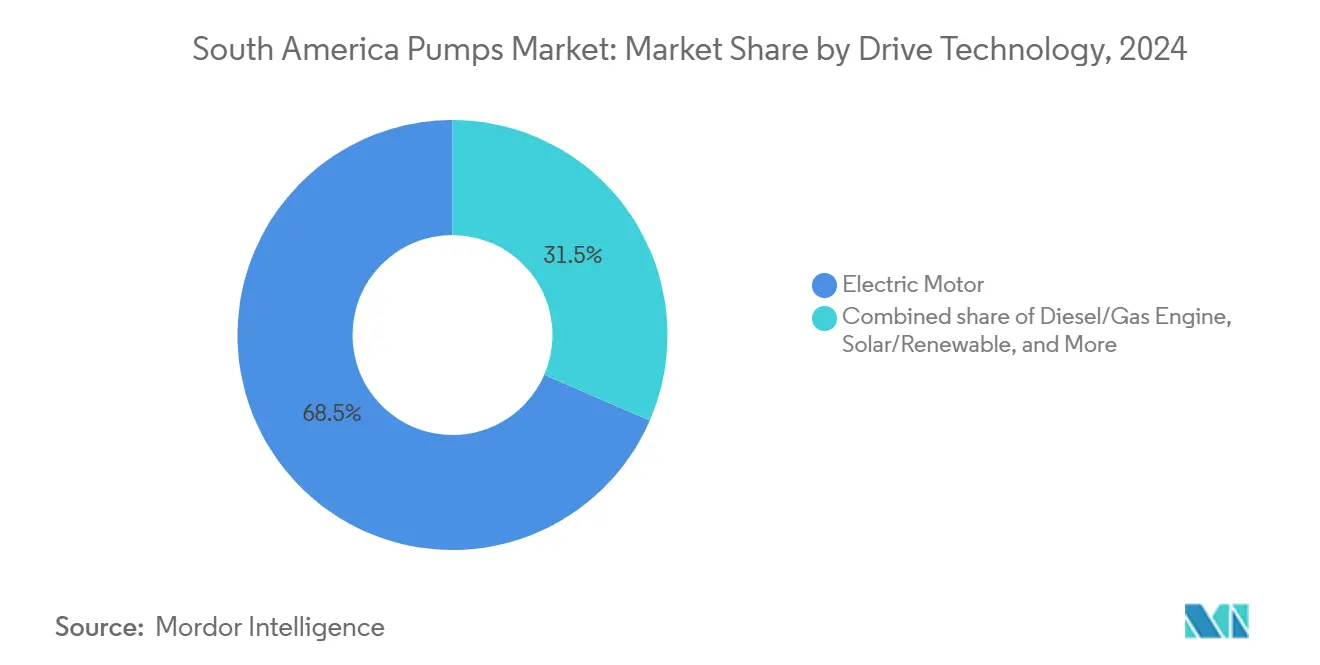

- By drive technology, electric-motor units commanded a 68.5% share in 2024, while solar and other renewables posted the fastest 9.2% CAGR to 2030.

- By position, surface pumps accounted for 53.7% of revenue in 2024; submersible pumps are advancing at a 6.3% CAGR through 2030.

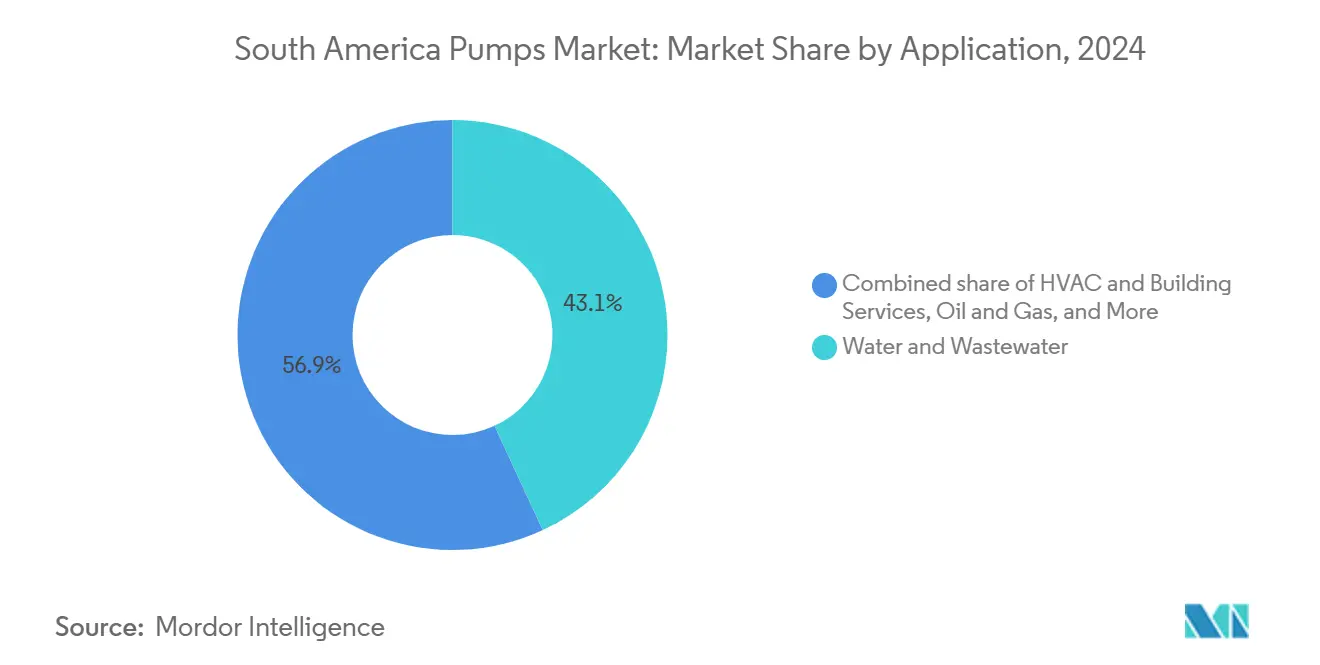

- By application, water and wastewater captured 43.1% of the South America pumps market size in 2024 and is projected to grow at a 3.8% CAGR through 2030.

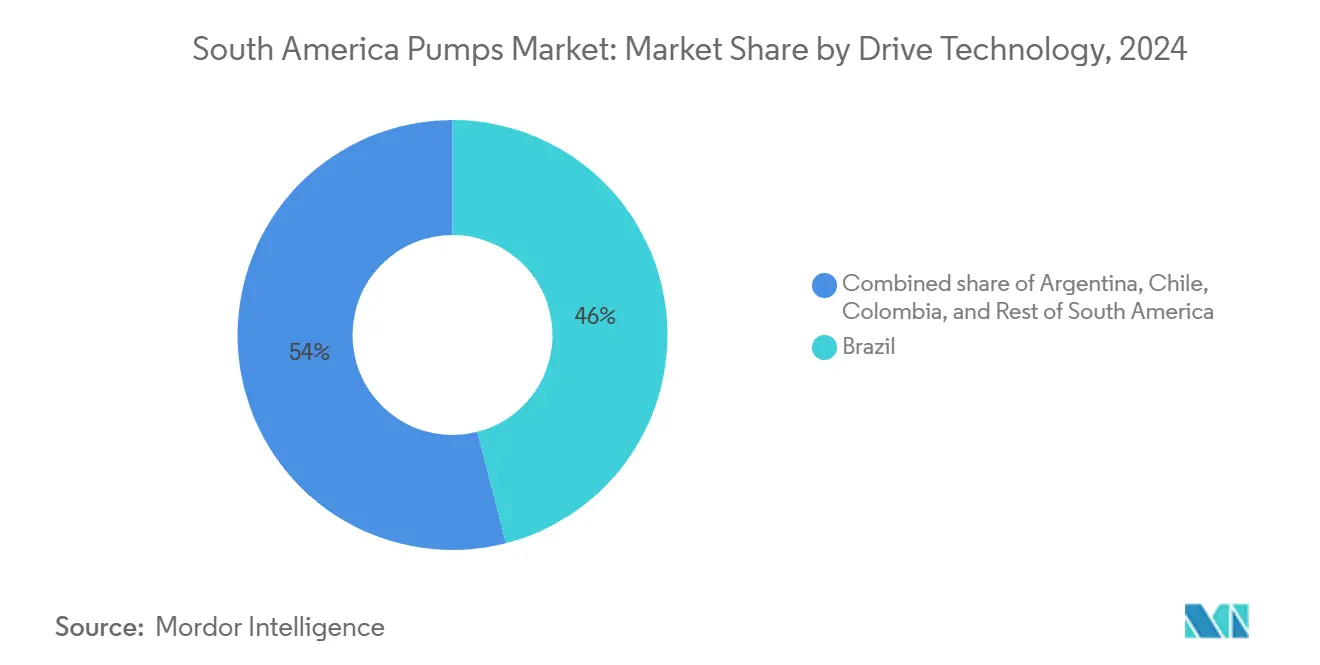

- By geography, Brazil dominated with 46% revenue share in 2024 and is set to grow at a 3.6% CAGR up to 2030.

South America Pumps Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid expansion of water & wastewater infrastructure | 0.8% | Brazil (São Paulo, Rio de Janeiro, Minas Gerais), Colombia (Bogotá, Medellín), Peru (Lima, Arequipa) | Medium term (2-4 years) |

| Oil & gas offshore revitalization in Brazil & Guyana | 0.7% | Brazil (Santos Basin, Campos Basin), spill-over to fabrication hubs in Rio de Janeiro, Niterói | Long term (≥ 4 years) |

| Growth in agriculture & irrigation spending | 0.5% | Brazil (Cerrado, Mato Grosso), Peru (Ica, Arequipa valleys), Chile (Central Valley), Argentina (Pampas region) | Medium term (2-4 years) |

| Mining-sector CAPEX surge (Chile & Peru copper/lithium) | 0.6% | Chile (Atacama, Antofagasta, Coquimbo), Peru (Arequipa, Moquegua, Tacna) | Long term (≥ 4 years) |

| Lithium-brine extraction projects needing specialty pumps | 0.3% | Chile (Atacama Salar), Argentina (Salta, Jujuy, Catamarca provinces) | Medium term (2-4 years) |

| Early CCS & blue-hydrogen pilot plants creating niche demand | 0.1% | Brazil (Santos Basin offshore), Chile (Haru Oni project, Magallanes), early pilots in Argentina | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Expansion of Water & Wastewater Infrastructure

Brazil’s 2024 sanitation privatization placed 17 state utilities under private operation, unlocking USD 100 billion for network renewal that prioritizes high-efficiency pumps sized above 85% hydraulic efficiency.[3]Brazilian Ministry of Cities, “Sanitation Concession Tracker 2025,” gov.br Sabesp alone committed USD 3.5 billion to reach 95% sewage-collection coverage by 2029, an initiative that will need roughly 12,000 submersible and vertical-turbine units. Bogotá’s Salitre plant, commissioned in 2024, already runs 24 submersible pumps rated for 4 m³/s and sets a regional benchmark for secondary treatment. Peru’s irrigation public-private partnerships, led by Chavimochic III, require centrifugal designs able to raise water 200 m from coastal aquifers, and each installation specifies ISO 9906 testing to screen out low-efficiency imports. Chile’s USD 2 billion desalination pipeline needs reverse-osmosis feed pumps built from duplex stainless steel to handle 60–80 bar duty cycles.

Oil & Gas Offshore Revitalization in Brazil & Guyana

Petrobras earmarked USD 111 billion for 14 floating production units through 2029, each fitted with subsea multiphase pumps that must sustain 15,000 psi and gas fractions of 90%. The Búzios field deploys Curtiss-Wright systems engineered to extend well life by up to 10 years while reducing hydrate risk. TechnipFMC and Sulzer are supplying CO₂-injection pumps for the HISEP separation pilot that plans 2 million t y of carbon reinjection by 2027, opening a niche for super-critical service designs. Guyana’s Stabroek block will lift South American offshore output past 1.2 million b/d by 2027, which feeds demand for topside water-injection and produced-water pumps assembled in Rio de Janeiro yards to satisfy local-content rules. Baker Hughes’ USD 350 million flexible-pipe award in 2024 signals that the associated pump packages will remain a procurement priority to 2030.

Mining-Sector CAPEX Surge in Chile & Peru Copper/Lithium

Chile approved USD 83 billion in copper investment through 2033; projects at El Teniente and Spence need tailings pumps that push 60–70% solids at elevations above 4,000 m, where air density cuts motor cooling by 40%. Peru hosts a USD 40 billion project queue led by Tía María, which specifies high-head centrifugal units rated 150–200 hp for ore transport. Closed-loop water circuits that recycle 90% process water boost corrosion exposure, so duplex and high-chrome alloys are now standard in slurry casings. Metso trimmed lead times to 8–10 weeks by opening assembly hubs in Lima and São Paulo, a move that raises aftermarket service capture while anchoring the South America pumps market to OEM parts. Argentina’s high-altitude lithium and copper sites in Salta and Catamarca also require pumps capable of solar-powered duty cycles, reinforcingthe adoption of battery-hybrid drives.

Lithium-Brine Extraction Projects Needing Specialty Pumps

SQM and Albemarle produced 180,000 t LCE in 2024 at the Atacama Salar using submersible brine pumps rated for 40 °C fluids and densities 1.3 × water. Twelve Argentine projects plan 250,000 t y by 2028, each calling for 20–30 extraction pumps engineered for 24-hour salt exposure. Direct lithium extraction pilots by Lilac Solutions and Eramet need high-pressure filtration pumps cycling brine at 50–100 bar, lifting unit values even as volumes fall 30–40%. Unit ASPs can rise 70% because wetted parts shift from 316 SS to Hastelloy, tilting revenue toward suppliers with chemical-processing know-how. Bolivia’s Uyuni salar remains untapped but represents a latent call for 500–700 specialty pumps should political risk ease, a future upside already tracked by global OEMs.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Exchange-rate volatility inflating import costs | -0.5% | Argentina (national impact), Brazil (import-dependent states), spill-over to Paraguay, Uruguay | Short term (≤ 2 years) |

| High electricity & maintenance expenditures | -0.3% | Argentina (post-subsidy reform), Chile (high industrial tariffs), Brazil (regional variations in energy costs) | Short term (≤ 2 years) |

| Climate-driven droughts causing intermittent water supply | -0.2% | Chile (Atacama, Coquimbo regions), Brazil (southern states, São Paulo), Argentina (Cuyo region) | Medium term (2-4 years) |

| Proliferation of counterfeit/low-spec imported pumps | -0.2% | Brazil (São Paulo, Rio de Janeiro industrial zones), Argentina (Buenos Aires), Peru (Lima), Colombia (Bogotá) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Exchange-Rate Volatility Inflating Import Costs

Argentina’s peso lost 90% against the dollar in 2024, lifting landed costs for European pumps by up to 60% and pushing many mines to defer replacements or opt for local refurbishment. Brazil’s real traded between 4.8 and 5.6 per dollar, introducing 20% budget swings that favor domestic brands sourcing 70% of components locally. Chile’s 12% currency slide eroded miner purchasing power and encouraged trials of lower-priced Asian units that lack ISO 9906 but undercut list price by 35%. Bogotá’s Salitre project absorbed an extra USD 15 million when the Colombian peso dipped 8%, sharpening attention on currency hedges in municipal tenders.[4]World Bank, “Bogotá Salitre Wastewater Plant Overview,” worldbank.org Limited adoption of forward contracts leaves utilities exposed to spot moves that can shift total installed cost by 15% in a single year.

Proliferation of Counterfeit or Low-Spec Imported Pumps

Brazil recorded a 30% rise in non-certified pump imports priced 40% below branded equivalents, but showing failure within 24 months due to inferior bearings. Argentine buyers, squeezed by inflation, sourced an estimated 40% of 2024 volumes from suppliers that offer no third-party performance data, increasing lifecycle energy spend by double digits. Peru’s copper mines linked a 15% jump in unplanned downtime to counterfeit wear parts lacking high-chrome alloys able to withstand 2 mm particles. Chile’s standards body issued a public alert after a high-rise fire was traced to an HVAC pump that overheated because the motor lacked thermal overload protection. Absent harmonized Mercosur import rules, non-compliant hardware moves freely across borders, so buyers increasingly demand ISO 9906 certification at the bid stage.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Pump Type: Centrifugal Designs Dominate Flow-Intensive Duties

Centrifugal models held a 49.9% share in 2024 and are forecast to advance at 4.0% through 2030, supported by Sabesp tenders that require 8,000–10,000 high-flow units.[5]Hydraulic Institute, “Pump Market Statistics 2024,” hydraulicinstitute.org Sulzer’s 15 MW packages at São Lourenço lift water 300 m and exemplify the segment’s scale. Positive-displacement pumps address metering roles to 20,000 psi, but their 40–60% price premium keeps them in niche service. Growing closed-loop circuits in Chilean copper mines add demand for corrosion-proof centrifugal casings, reinforcing the South America pumps market.

Centrifugal upgrades also curb energy spend because dual-volute casings cut radial thrust by 20%, extending bearing life. Positive-displacement designs gain ground in direct lithium extraction but stay a minority. Counterfeit parts remain a risk, yet OEM ceramic-lined impellers now push mean time between failures to 12,000 hours, safeguarding municipal budgets and stabilizing the South America pumps industry.

By Drive Technology: Solar Growth Outpaces the Grid

Electric motors kept a 68.5% share in 2024 thanks to urban grids and tariffs near USD 0.10 kWh. Solar-battery hybrids, expanding at a 9.2% CAGR, let Cerrado farms avoid USD 50,000 per km grid extensions. Grundfos units with 10 kWh lithium packs run 24 hours and cut diesel by 95%. Chile’s carbon tax adds USD 20 t CO₂, pressing miners to adopt hybrid packages that trim fuel 70%.

IE3 motor rules now appear in most Brazilian and Chilean procurements, barring IE1 imports and lifting wire-to-water efficiency by four points. Magnetically driven pumps grow in petrochemicals under CONAMA 382 zero-leak mandates. Argentina’s tariff hike trebled industrial power prices, pushing factories to variable-frequency drives that drop consumption 30% within a year, deepening the South America pumps market case for premium controls.

By Position: Surface Still Leads, Submersibles Accelerate

Surface pumps captured a 53.7% share in 2024 because they are easy to maintain and cost 30% less to install in tailings lines. Yet submersible demand rises 6.3% annually as aquifers fall 20 m in São Paulo and rivers dry across Argentina. KSB vertical turbines in Peru’s Chavimochic project show 200 m lift at 3 m³/s flow, proving deep-well competence.

Vertical in-line designs earn retrofit orders from Santiago’s 15,000 towers after the 2024 building code required variable-speed drives above 5 hp. Submersibles run 15 dB quieter, helping Buenos Aires meet 55 dB night limits. Sabesp now replaces 2,000 surface units with vandal-proof submersibles, a shift that adds resilience and enlarges the South America pumps market size for below-ground equipment.

By Application: Water and Wastewater Anchor Long-Term Volume

Water and wastewater represented 43.1% of 2024 revenue and grew 3.8% to 2030 as Brazil targets 90% treatment coverage. São Paulo alone will buy 50,000–60,000 new pumps, including clog-resistant submersibles for 80 mm solids. Peru’s irrigation PPPs need 1,000 hp centrifugal sets to lift coastal aquifers, strengthening the South America pumps market size for agricultural services.

Oil and gas come second because Petrobras plans 2,500 subsea and topside units through 2029. Mining tailings pumps must move 2 mm particles in slurries at 70% solids, and Codelco specifies 100 heavy-duty models for El Teniente. HVAC retrofits follow with 3,000–4,000 variable-speed pumps in Santiago’s towers. Sanitary duties in food and pharma claim high margins thanks to 3-A certified electropolished designs.[6]3-A Sanitary Standards, “Hygienic Pump Design,” 3-a.org Thermal power projects add 1,500 boiler-feed units by 2028, rounding out demand for the South America pumps market.

Geography Analysis

Brazil retained 46% of 2024 revenue and, at 3.6% CAGR, remains the growth anchor for the South America pumps market. Pre-salt wells at 2,800 m depths rely on multiphase pumps rated 15,000 psi, while Sabesp’s USD 3.5 billion modernization drives large municipal orders. Domestic makers use 70% local content and cut downtime by 30%, an edge over imports.

Chile’s pipeline of USD 83 billion in mining spend and USD 2 billion in desalination projects lifts pump demand despite chronic drought. Tailings duty at 4,000 m requires oversized motors to counter low air density, and lithium ponds need corrosion-proof casings. Santiago codes now oblige variable-speed HVAC drives above 5 hp, birthing a retrofit niche inside the South America pumps market.

Argentina wrestles with currency turmoil that inflates import price tags by up to 60%, spurring used-pump trade yet opening counterfeit risk. Lithium salars in Salta and Jujuy will still procure 30 extraction units per site. Colombia’s Salitre plant and Peru’s USD 24 billion irrigation PPPs keep municipal orders steady. Paraguay, Uruguay, and Bolivia remain small but show upside from Itaipu dam upgrades and pulp-mill builds, adding incremental flow to the South America pumps industry.

Competitive Landscape

The top five global suppliers, Grundfos, Flowserve, Sulzer, Xylem, and KSB, collectively hold a 35% share, while Brazilian firms Schneider Motobombas, IMBIL, and Bombas Leão secure another 20% through after-sales reach. Metso’s 2024 hubs in Peru and Brazil chopped delivery times to 8 weeks and locked in parts revenue at 45% gross margin METSO.COM. Ebara bought Uruguay’s Asanvil to deepen service density south of the Amazon.

Technology alliances shape the South America pumps market: TechnipFMC and Sulzer co-develop CO₂-ready subsea modules, while Grundfos and Wilo blend solar arrays with integrated batteries that cut diesel by 90% on Cerrado farms. Netzsch opened a multi-screw plant in Brazil to meet 60% domestic-content rules. Chinese entrants Kaiquan and Leo price 30% below European rivals yet struggle with ISO 9906 compliance, keeping adoption limited to price-sensitive users.

M&A stays active; Flowserve bought MOGAS for USD 305 million to fold severe-service valves into its pump offering, extending reach in Petrobras projects. Alfa Laval pursues lithium brine contracts, leveraging chemical know-how to offset lower unit counts but higher ASPs. Local OEMs aim at refurbishment services because exchange-rate swings favor rebuilds over imports, cushioning revenue when capital budgets tighten in the South America pumps market.

South America Pumps Industry Leaders

Grundfos Holding A/S

Flowserve Corporation

Xylem Inc.

Sulzer Ltd.

KSB SE & Co. KGaA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: Swiss Sulzer clinched a contract to deliver water injection package systems for Seatrium's P-84 and P-85 FPSO units, set to operate under Petrobras in Brazil. The contract encompasses integrated pump skids for both floating production vessels, earmarked for deployment by Petrobras in the Atapu and Sépia fields, located roughly 200 kilometers off the coast of Rio de Janeiro.

- July 2025: Sulzer inaugurated its third facility in Argentina, bolstering its operational footprint. The newly opened service center in Ezeiza, dedicated to turbomachinery and pump services, covers an expansive 2,600 square meters.

- June 2024: TechnipFMC has chosen Sulzer Flow Equipment to partner in crafting innovative subsea CO2 pump solutions. Petrobras' groundbreaking HISEP technology allows for the seabed separation of CO2-rich natural gas from oil.

South America Pumps Market Report Scope

Pumps, mechanical devices, convert energy to elevate, transport, or compress fluids, be it liquids or gases. By transforming mechanical energy into hydraulic or pneumatic energy, pumps generate a pressure difference, propelling fluids from lower to higher pressure zones.

The South America pumps market is segmented by pump type, drive technology, position, application, and geography. By pump type, the market is segmented into centrifugal and positive-displacement. By drive technology, the market is segmented into electric motor, diesel/gas engine, solar/renewable, and magnetically-driven/sealless. By position, the market is segmented into surface, submersible, and vertical in-line. By application, the market is segmented into water and wastewater, chemical and petrochemical, HVAC and building services, oil and gas, food and beverage, mining and metals, power generation, pharmaceuticals and biotech, and others. The report also covers the market sizes and forecasts for the South America pumps market across major countries. For each segment, the market sizing and forecasts have been done on the basis of value (USD).

| Centrifugal |

| Positive-Displacement |

| Electric Motor |

| Diesel/Gas Engine |

| Solar/Renewable |

| Magnetically-Driven/Sealless |

| Surface |

| Submersible |

| Vertical In-Line |

| Water and Wastewater |

| Chemical and Petrochemical |

| HVAC and Building Services |

| Oil and Gas (Upstream, Midstream, Downstream) |

| Food and Beverage |

| Mining and Metals |

| Power Generation (Thermal, Nuclear, Renewables) |

| Pharmaceuticals and Biotech |

| Others |

| Brazil |

| Argentina |

| Chile |

| Colombia |

| Rest of South America |

| By Pump Type | Centrifugal |

| Positive-Displacement | |

| By Drive Technology | Electric Motor |

| Diesel/Gas Engine | |

| Solar/Renewable | |

| Magnetically-Driven/Sealless | |

| By Position | Surface |

| Submersible | |

| Vertical In-Line | |

| By Application | Water and Wastewater |

| Chemical and Petrochemical | |

| HVAC and Building Services | |

| Oil and Gas (Upstream, Midstream, Downstream) | |

| Food and Beverage | |

| Mining and Metals | |

| Power Generation (Thermal, Nuclear, Renewables) | |

| Pharmaceuticals and Biotech | |

| Others | |

| By Geography | Brazil |

| Argentina | |

| Chile | |

| Colombia | |

| Rest of South America |

Key Questions Answered in the Report

What revenue will the South America pumps market generate by 2030?

Sales are projected to reach USD 2.88 billion, up from USD 2.50 billion in 2025, reflecting a 3.24% CAGR for 2025-2030.

What drives pump demand growth in South America?

Sanitation privatization, pre-salt oil projects, and mining CAPEX expand the South America pumps market.

Which pump type holds the largest share?

Centrifugal models lead with 49.9% share thanks to their high flow efficiency.

How fast is solar-powered pumping growing?

Solar-battery systems record a 9.2% CAGR to 2030 as off-grid farms skip costly grid extensions.

Why are submersible pumps gaining popularity?

Falling water tables in Brazil and Argentina make deep-well submersibles essential for reliable extraction.

How concentrated is supplier competition?

The field is moderately fragmented, with the top five firms controlling about 35% of revenue.

Page last updated on: