South America Packaging Automation Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2020 - 2024 |

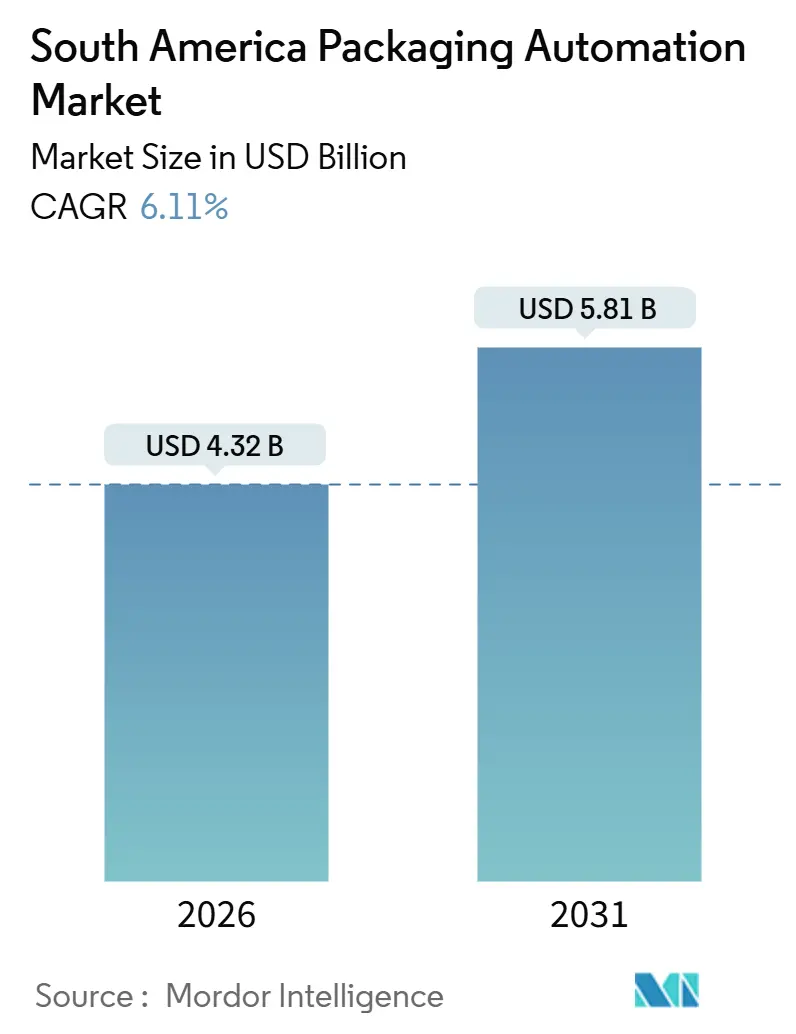

| Market Size (2026) | USD 4.32 Billion |

| Market Size (2031) | USD 5.81 Billion |

| Growth Rate (2026 - 2031) | 6.11% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South America Packaging Automation Market Analysis by Mordor Intelligence

The South America packaging automation market size stands at USD 4.32 billion in 2026 and is projected to reach USD 5.81 billion by 2031, reflecting a 6.11% CAGR during the forecast period. Currency volatility, labor-cost inflation, and policy incentives are reshaping investment priorities, while e-commerce fulfillment hubs and food-safety traceability mandates continue to raise automation thresholds. Brazil’s “Made in Brazil” stimulus, Argentina’s RIGI duty-waiver regime, and the forthcoming EU-Mercosur trade pact lower tariff walls; yet prolonged interest-rate cycles lengthen payback horizons for small and medium-sized enterprises. At the plant floor, predictive-maintenance platforms, modular palletizing cells, and fully automatic sortation systems dominate capital budgets, driven by the scarcity of cross-disciplinary technicians and the imperative to absorb mixed-SKU throughput surges. Against this backdrop, global integrators and regional specialists are re-engineering service models to capture recurring aftermarket revenue, an approach endorsed by 98% of end-users who expect stable or rising parts and service spending.

Key Report Takeaways

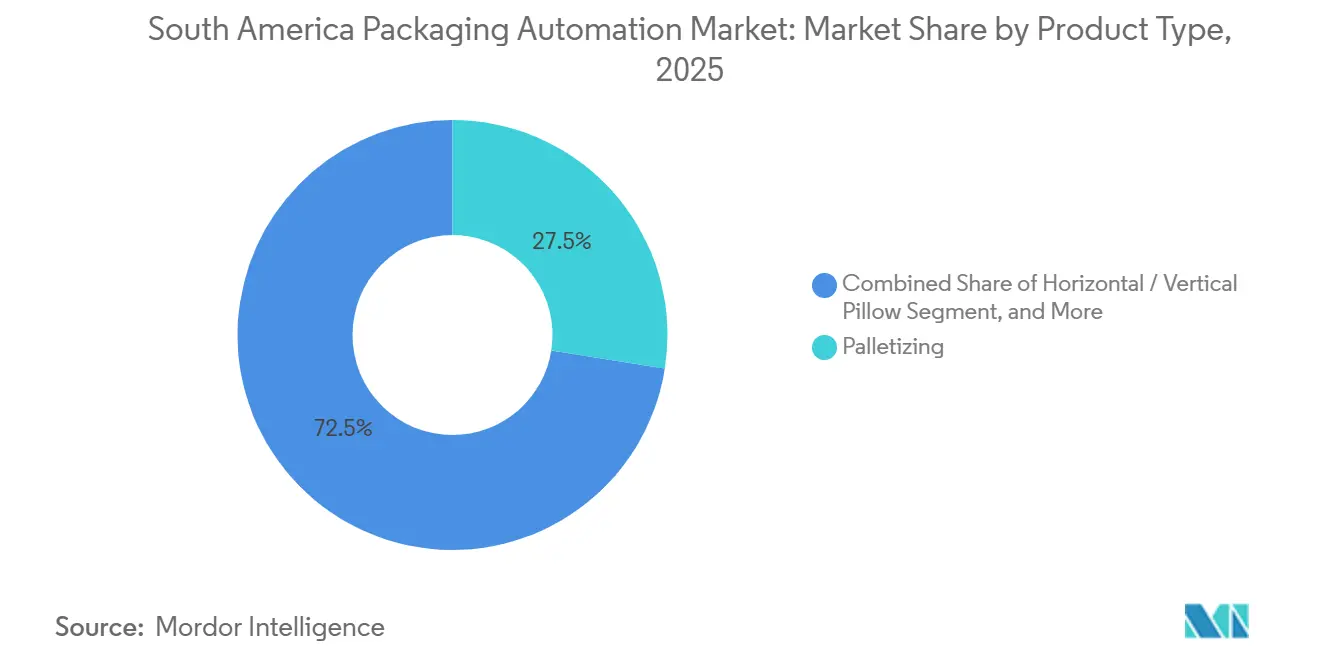

- By product type, palletizing equipment captured 27.49% of the South America packaging automation market share in 2025.

- By automation level, the South America packaging automation market size for fully automatic systems is projected to grow at an 8.32% CAGR between 2026-2031.

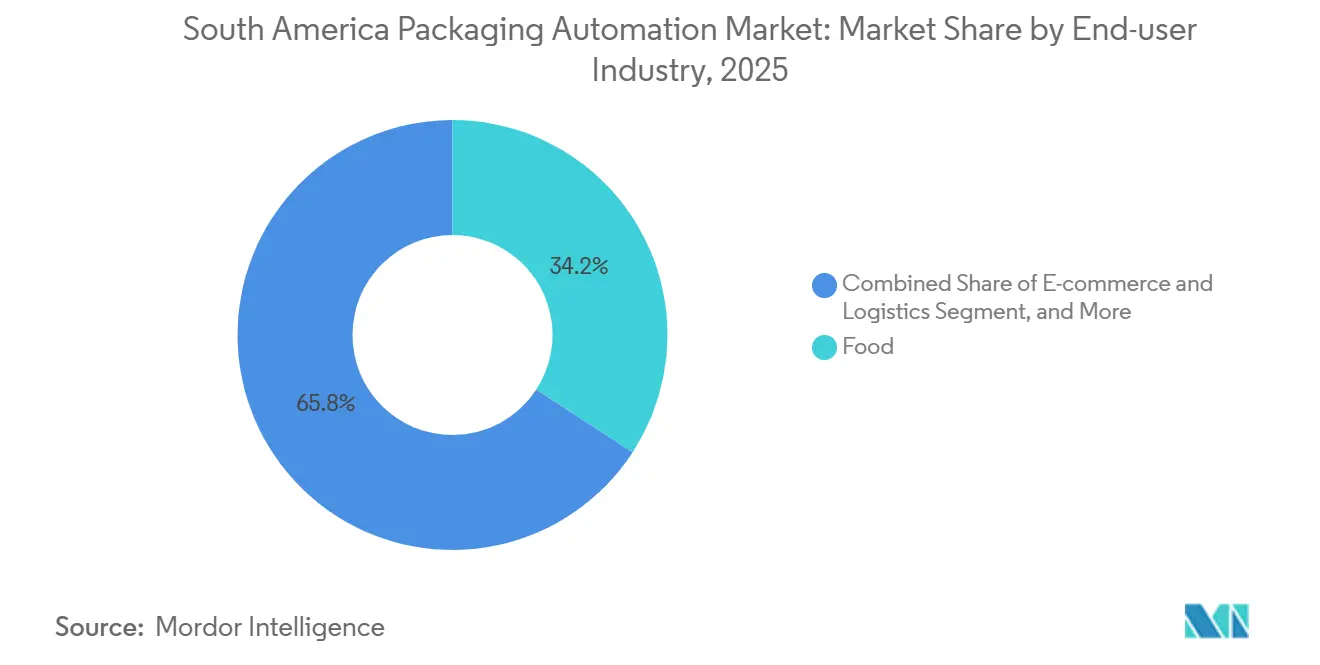

- By end-user industry, food processors captured 34.19% of the South America packaging automation market share in 2025.

- By country, the South America packaging automation market size for Argentina is projected to grow at a 7.65% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

South America Packaging Automation Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Labour-Cost Inflation Across Brazil and Chile | +1.2% | Brazil core, Chile secondary | Medium term (2-4 years) |

| E-Commerce Fulfilment Throughput Requirements | +1.5% | Brazil and Argentina, spillover to Colombia | Short term (≤ 2 years) |

| Food-Safety Traceability Mandates | +0.9% | Brazil, Argentina, and Chile export-oriented segments | Medium term (2-4 years) |

| Energy-Efficient Machinery Incentives in Mercosur | +0.6% | Mercosur member states | Long term (≥ 4 years) |

| AI-Enabled Predictive-Maintenance Value Capture | +0.8% | Brazil and Argentina, early adopters in Chile | Medium term (2-4 years) |

| Near-Shoring of Consumer-Goods Manufacturing to Brazil | +0.7% | Brazil, indirect gains in Argentina's supplier base | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

E-Commerce Fulfilment Throughput Requirements

MercadoLibre’s BRL 23 billion (USD 4.6 billion) expansion, which aims to double the number of Brazilian distribution centers to 21 by 2025, illustrates how online retail is redefining capacity planning. Argentina mirrored the surge, with online sales climbing 248% year-over-year in the first half of 2024, prompting Andreani to install sorters that now handle 26,000 packages per hour. Reverse-logistics inflows, accounting for 15%-20% of urban inbound volume, force integrators to design bidirectional conveyors and automated inspection islands. Colombia’s food warehouses anticipate a 28% annual growth in the adoption of automated systems through 2028, accompanied by a corresponding increase in the handling of perishable goods. These pressures favor palletizing and case-packing modules that can switch rapidly among thousands of SKUs, as demonstrated by Duravant's localization of conveyor engineering through the 2025 BVSP acquisition.

AI-Enabled Predictive-Maintenance Value Capture

Packaging lines are transitioning from break-fix maintenance toward data-driven uptime strategies. PMMI’s 2024 operational-excellence study documented the cumulative value lift from machine vision, digital twins, and anomaly detection that accumulates over successive runs.[1]PMMI, “2024 Operational Excellence in Packaging Report,” pmmi.org Rockwell Automation’s Plex MES, released for South American SMEs in 2024, embeds real-time monitoring and FSMA-compatible traceability, shrinking service dispatch needs in remote areas. Schneider Electric’s EcoStruxure rollout at its Blumenau plant reduced the mean time to repair by around 30%, validating predictive analytics at scale. OEMs are therefore pivoting from one-off equipment sales to subscription-based service models; 75% of end-users now rank spare-parts availability above initial price, lifting barriers for new entrants without regional warehouses.

Food-Safety Traceability Mandates

ANVISA’s RDC 843/2024 introduced digital package inserts and serialization pilots for pharmaceutical lines, while tightening the notification and registration paths for food-contact materials. The European Union Deforestation Regulation, effective since 2024, requires geolocation data for exports such as soy and beef, prompting processors to retrofit QR-code printers and implement blockchain databases. By 2023, 35% of Colombian food companies had adopted blockchain traceability, with adoption expected to exceed 50% by 2026. Scanware’s May 2025 installation at Libbs Farmacêutica demonstrates the complexity of case- and pallet-level data aggregation. Retrofit costs range from USD 50,000 for basic vision systems to USD 500,000 for integrated track-and-trace modules, favoring large processors that can amortize upgrades across multiple site footprints.

Near-Shoring of Consumer-Goods Manufacturing to Brazil

Foreign direct investment is pivoting toward Brazil’s industrial corridor. Novo Nordisk committed USD 243 million to expand its pharmaceutical capacity in 2024, and Honda invested USD 807 million in automotive expansion, both citing proximity to the Mercosur market and Brazil’s 85% renewable electricity matrix. The BRL 300 billion (USD 54 billion) “Made in Brazil” program offers subsidized BNDES loans and tax relief for equipment with over 50% local content, encouraging packaging machinery assemblers to localize structural steel and controls while importing servo drives. The EU-Mercosur trade agreement will phase out up to 20% of machinery duties over a decade, further tilting the cost calculus in favor of regional production. Yet port dwell times of 5-7 days and complex customs procedures temper near-shoring gains, underlining the need for automation players to factor logistical bottlenecks into ROI models.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Upfront CAPEX for SMEs | -0.9% | Brazil, Argentina, Colombia | Short term (≤ 2 years) |

| Shortage of Automation-Skilled Technicians | -0.7% | Brazil core, Argentina secondary, Chile emerging | Medium term (2-4 years) |

| Currency Volatility Affecting Payback | -0.5% | Argentina and Brazil import-dependent segments | Short term (≤ 2 years) |

| Fragmented After-Sales Service Ecosystem | -0.4% | Rest of South America, rural Brazil, secondary Argentine cities | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Upfront CAPEX for SMEs

Collateral demands often exceed 150% of asset value, hindering access to automation loans, as detailed in the 2024 OECD SME Policy Index. Brazil’s FIESP survey indicated that machinery investment sentiment was 36.1 in the fourth quarter of 2024, reflecting the deterrent effect of the 11.25% Selic rate on capital goods imports. Although BNDES offers ESG-linked credit, the application process, which requires audited financial and environmental studies, excludes many firms with fewer than 100 employees. Consequently, SMEs stretch their manual labor longer, widening productivity gaps compared to automated multinationals.

Shortage of Automation-Skilled Technicians

FIESP’s December 2024 poll revealed 54.5% of São Paulo executives could not fill automation roles. OECD data show that 40% of regional manufacturers lack cross-disciplinary talent that combines mechanical, electrical, and software skills. While augmented-reality work instructions reduce error rates, broadband coverage outside major metropolitan areas remains inconsistent, limiting widespread deployment. Rockwell Automation’s ABDI MetaIndústria labs trained more than 100 companies in 2024, but the pipeline still trails demand.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: palletizing Systems Capture Volume and Speed Gains

Palletizing systems generated 27.49% of 2025 revenue in the South America packaging automation market, and this share is forecast to widen as the segment records an 8.43% CAGR to 2031. Mixed-SKU distribution centers that handle thousands of stock-keeping units daily tend to gravitate toward robotic palletizers with multi-gripper heads and automated pattern-generation software, thereby minimizing manual intervention. MercadoLibre’s expansion to 21 Brazilian facilities created a multiplier effect for high-payload robots and autonomous mobile pallet movers. Filling, labeling, and wrapping lines follow in importance, catering to beverage, dairy, and snack segments that value aseptic integrity and film economy.

The rapid adoption of collaborative palletizing cells aligns with labor-scarce pressures and frequent batch changeovers typical in South American plants. ABB’s Flexley Mover P603 robots and Agilox’s autonomous forklifts exemplify decentralized layouts that remove conveyor interlocks. SACMI’s 90 compression-molding units installed in Brazil underscore the trend of integrating closure applications. Combined, these shifts reinforce the position of palletizing within the South America packaging automation market share hierarchy.

By Automation Level: Fully Automatic Lines Anchor Investment Plans

Fully automatic configurations accounted for 63.31% of 2025 revenue and are projected to post an 8.32% CAGR through 2031, reflecting the need to sidestep wage escalation and compress order-cycle times. Andreani’s 26,000-package-per-hour sorter installation in December 2024 illustrates how thresholds accelerate full automation. While semi-automatic systems persist in cosmetics and specialty food facilities, the South America packaging automation market size premium increasingly gravitates toward lights-out lines with integrated PLCs, vision cameras, and servo positioning.

Remote diagnostics embedded in Schneider Electric’s EcoStruxure and Siemens digital-twin commissioning protocols reduce on-site service calls, a critical advantage amid technician shortages. Argentina’s RIGI duty waivers enhance capital savings on imported servos and vision modules, further favoring the adoption of fully automatic systems. All told, full automation remains both the largest and fastest-growing layer of the South America packaging automation market.

By End-user Industry: Food Remains Core as E-Commerce Accelerates

Food processors delivered 34.19% of 2025 demand and continue to anchor the South America packaging automation market, benefiting from Brazil’s world-leading positions in soy, sugar, and poultry exports. Victam Latin America 2025 highlighted AI-driven feed-mill automation and EUDR-aligned traceability, exemplifying the sector’s automation bias. Pharmaceuticals and cosmetics follow, driven by RDC 843/2024 serialization rules that compel blister and bottle traceability.

E-commerce and logistics applications, however, are set to expand to a 7.89% CAGR, making them the fastest-growing demand pool within the South America packaging automation industry. Colombia’s forecast of 28% annual growth for automated food warehouses validates spillover effects into perishables logistics. As mixed-SKU volumes proliferate, OEMs design modular platforms that reuse conveyors, sorters, and palletisers across end-user verticals, reinforcing economies of scale and stabilizing the broader South America packaging automation market size outlook.

Geography Analysis

Brazil generated 41.81% of 2025 regional revenue, and its growth pace aligns with the 6.11% regional CAGR as manufacturing output approaches USD 300 billion. The BRL 300 billion “Made in Brazil” program subsidizes equipment embedding over 50% local content, helping assemblers blunt currency volatility. MercadoLibre’s USD 4.6 billion logistics build-out, Novo Nordisk’s USD 243 million pharmaceutical expansion, and Honda’s USD 807 million automotive investment underscore sustained foreign direct-investment inflows. Yet FIESP’s sentiment index, at 36.1, signals lingering caution as imported components become costlier in an 11.25% Selic-rate environment. Rockwell Automation’s MetaIndústria labs aim to bridge the skills gap that half of executives identify as a hiring challenge.

Argentina is projected to record a 7.65% CAGR, the fastest in the region, buoyed by the RIGI regime, which waives customs duties for projects exceeding USD 200 million and stabilizes hard-currency access. ARLOG’s 2024 survey found that 82% of logistics operators plan to set automation budgets for 2025, and Andreani’s high-speed sorters reflect concrete follow-through.[2]Asociación Argentina de Logística Empresaria, “Encuesta de Inversiones en Logística 2025,” arlog.org AdePIA’s 2024 study on food machinery revealed that multinational retailers now require ISO 22000 and FSSC 22000 certifications, thereby accelerating upgrades in traceability along the value chain.

Colombia, Chile, and the rest of South America account for the residual share, yet they also present pockets of rapid adoption. Colombia’s 28% growth forecast for automated food warehouses, combined with Chile’s extended producer responsibility law, is pushing local packagers toward flexible wrapping lines. Sistemo’s 2025 expansion beyond Chile into Brazil validates spillover opportunities for mid-tier system integrators. Ratification of the EU-Mercosur agreement promises tariff relief across the bloc, but port inefficiencies and customs complexity remain structural challenges.

Competitive Landscape

Moderate fragmentation characterizes the South America packaging automation market, with global integrators such as Rockwell Automation, Siemens, and Schneider Electric competing against specialist OEMs like Coesia, Duravant, GEA, and Sidel. Duravant’s 2025 acquisition of BVSP enables localized engineering, compressing lead times from 6-9 months to under 4 months and sidestepping import tariffs. Cloud-based predictive-maintenance platforms, exemplified by EcoStruxure, Plex MES, and Siemens MindSphere, convert transactional capital-equipment relationships into subscription revenue streams, an approach reinforced by PMMI findings that 98% of customers expect their aftermarket budgets to rise.

White space opportunities persist in semi-automatic configurations priced below USD 100,000, appealing to SMEs constrained by collateral requirements. Premier Tech’s Jundiaí plant, resulting from the acquisition of Almeida Martins, showcases how modular bagging and palletizing lines can serve both the agricultural and consumer packaged goods segments.[3]Premier Tech, “Almeida Martins Acquisition and Jundiaí Plant Establishment,” premiertech.com Chinese sorter vendors undercut European pricing by up to 30%, as evidenced by Andreani’s December 2024 contract, intensifying price competition and pressuring incumbents to bundle financing and local-service packages.

Regulatory complexity favors vendors with in-house compliance expertise. ANVISA’s RDC 843/2024 and ISO-based audits pose entry barriers for newcomers lacking serialization expertise and a track record with inspectors. Simultaneously, OEMs are embedding operator-training modules and financing options pegged to local currencies to mitigate foreign-exchange exposure for customers, thereby enhancing stickiness across the South America packaging automation market.

South America Packaging Automation Industry Leaders

Rockwell Automation, Inc.

Siemens AG

Schneider Electric SE

Mitsubishi Electric Corporation

ProMach, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Duravant established a Brazilian entity and acquired BVSP to localize engineering and cut delivery lead times below four months.

- May 2025: Scanware completed ANVISA-compliant serialization deployment at Libbs Farmacêutica, enabling unit-level traceability.

- March 2025: Victam Latin America 2025 convened in São Paulo with a 50% jump in attendance, spotlighting AI-driven feed-mill automation.

- January 2025: Sistemo secured its first Brazilian distribution-center robotics project in partnership with GreyOrange, with go-live slated for late 2025.

South America Packaging Automation Market Report Scope

The South America Packaging Automation Market refers to the regional industry segment focused on the development, supply, and integration of automated machinery and systems that streamline packaging processes. These solutions include robotic case packers, palletizers, automated filling and sealing machines, and integrated control systems designed to reduce manual intervention and enhance productivity.

The South America Packaging Automation Market Report is Segmented by Automation Level (Fully-Automatic, and Semi-Automatic), Product Type (Filling, Labelling, Horizontal/Vertical Pillow, Case Packaging, Bagging, Palletizing, Conveying/Handling, Capping, and Wrapping), End-User Industry (Food, Pharmaceuticals, Cosmetics, Household, Beverages, Chemicals, E-Commerce and Logistics, and Other End-User Industries), and Country. The Market Forecasts are Provided in Terms of Value (USD).

| Fully Automatic |

| Semi-Automatic |

| Filling |

| Labelling |

| Horizontal / Vertical Pillow |

| Case Packaging |

| Bagging |

| palletizing |

| Conveying / Handling |

| Capping |

| Wrapping |

| Food |

| Pharmaceuticals |

| Cosmetics |

| Household |

| Beverages |

| Chemicals |

| E-commerce and Logistics |

| Other End-user Industries |

| Brazil |

| Argentina |

| Colombia |

| Chile |

| Rest of South America |

| By Automation Level | Fully Automatic |

| Semi-Automatic | |

| By Product Type | Filling |

| Labelling | |

| Horizontal / Vertical Pillow | |

| Case Packaging | |

| Bagging | |

| palletizing | |

| Conveying / Handling | |

| Capping | |

| Wrapping | |

| By End-user Industry | Food |

| Pharmaceuticals | |

| Cosmetics | |

| Household | |

| Beverages | |

| Chemicals | |

| E-commerce and Logistics | |

| Other End-user Industries | |

| By Country | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Rest of South America |

Key Questions Answered in the Report

What is the current value of the South America packaging automation market?

The market is expected to reach USD 5.81 billion by 2031, up from USD 4.32 billion in 2026.

How fast is the market growing?

The market is expanding at a 6.11% CAGR over the 2026-2031 period.

Which product category leads to revenue?

Palletizing systems lead with 27.49% of 2025 revenue and are also the fastest-growing segment.

Which country offers the strongest growth outlook?

Argentina is projected to record a 7.65% CAGR through 2031, outpacing other South American countries.

Why are fully automatic systems gaining share?

Labor shortages, wage inflation, and e-commerce throughput requirements make fully automatic lines the most cost-effective option, despite their higher upfront costs.

What is the main barrier facing SMEs?

High collateral requirements and elevated interest rates limit access to financing for automation equipment.

Page last updated on: