Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

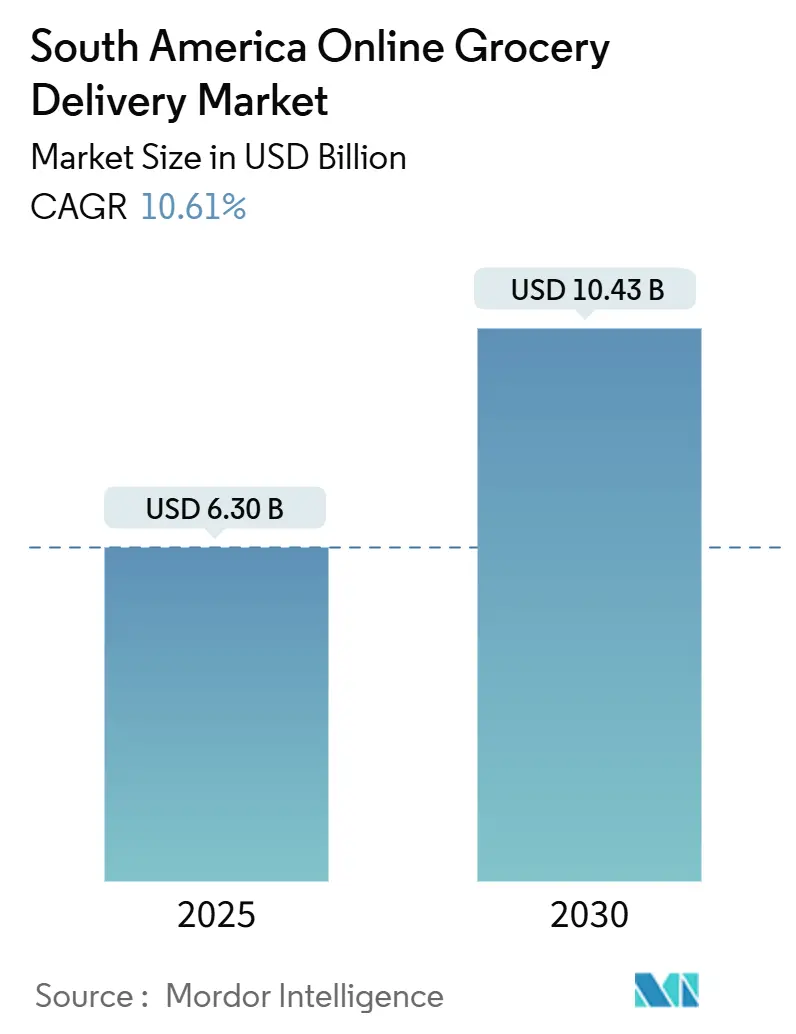

| Market Size (2025) | USD 6.30 Billion |

| Market Size (2030) | USD 10.43 Billion |

| Growth Rate (2025 - 2030) | 10.61% CAGR |

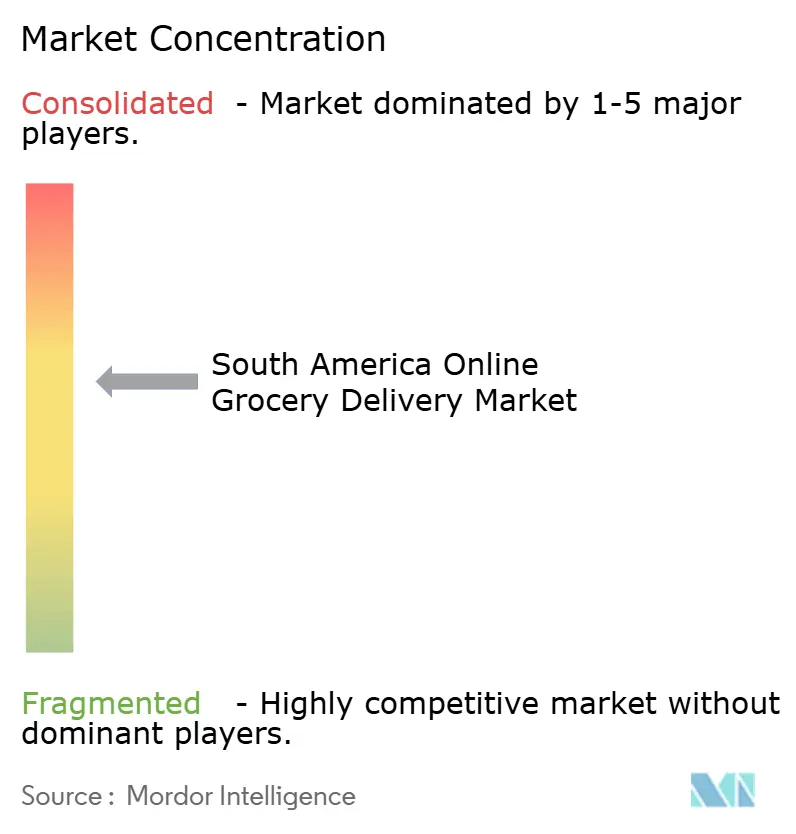

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

South America Online Grocery Delivery Market Analysis by Mordor Intelligence

The South America Online Grocery Delivery Market size is estimated at USD 6.30 billion in 2025, and is expected to reach USD 10.43 billion by 2030, at a CAGR of 10.61% during the forecast period (2025-2030). Ongoing digital transformation, spearheaded by widespread smartphone ownership, the PIX instant‐payment rail, and venture investment in last-mile cold-chain hubs, underpins the market’s expansion. Platforms continue to gain from consumer preference for mobile-first experiences, friction-free checkout, and an enlarging selection of fresh and packaged products. Capital inflows flow chiefly to Brazil, Argentina, and Chile, where scale benefits offset rising fulfillment costs. Competitive intensity stays moderate as marketplace aggregators, dark-store specialists, and omnichannel retailers vie to shorten delivery windows and build customer loyalty. Regulatory shifts around worker status, data privacy, and cross-border trade create a patchwork compliance landscape, encouraging well-capitalized incumbents to invest in governance and localized operating models.

Key Report Takeaways

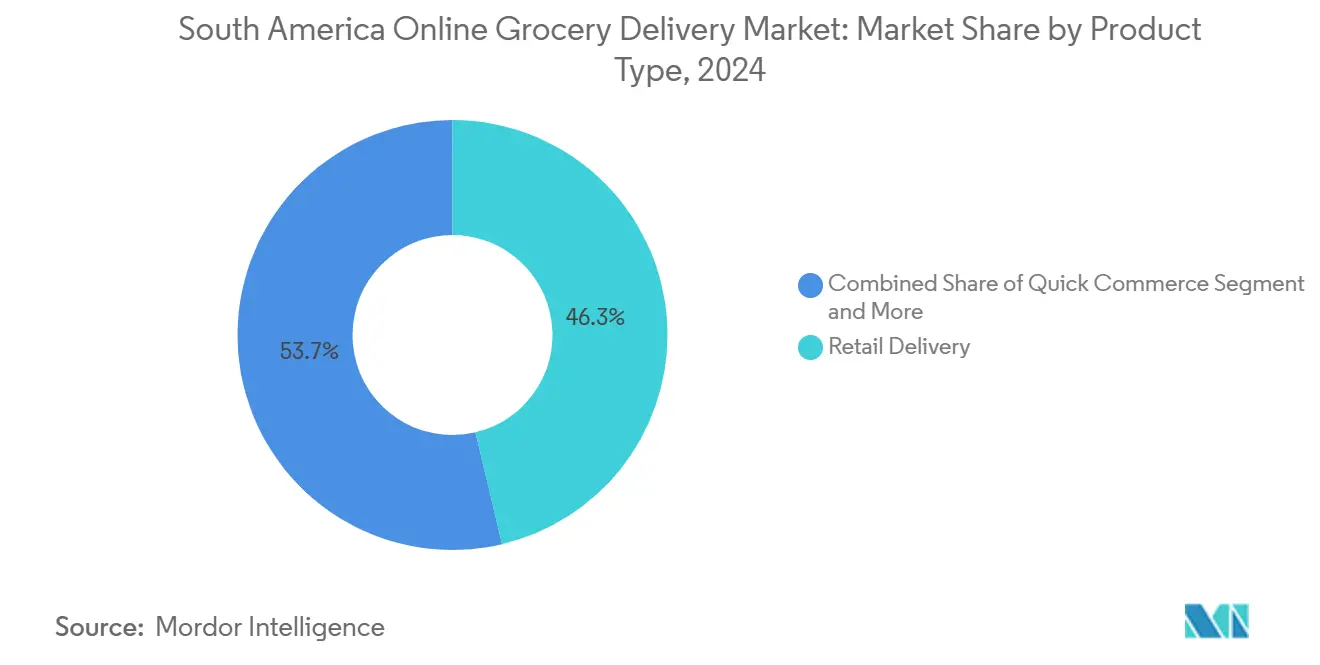

- By product category, retail delivery led with 46.30% revenue share of the South America online grocery delivery market in 2024; quick commerce is projected to expand at a 12.90% CAGR through 2030.

- By platform model, marketplace aggregators held 39.70% of the South America online grocery delivery market share in 2024, while pure-play dark-store operators record the highest projected CAGR at 13.40% to 2030.

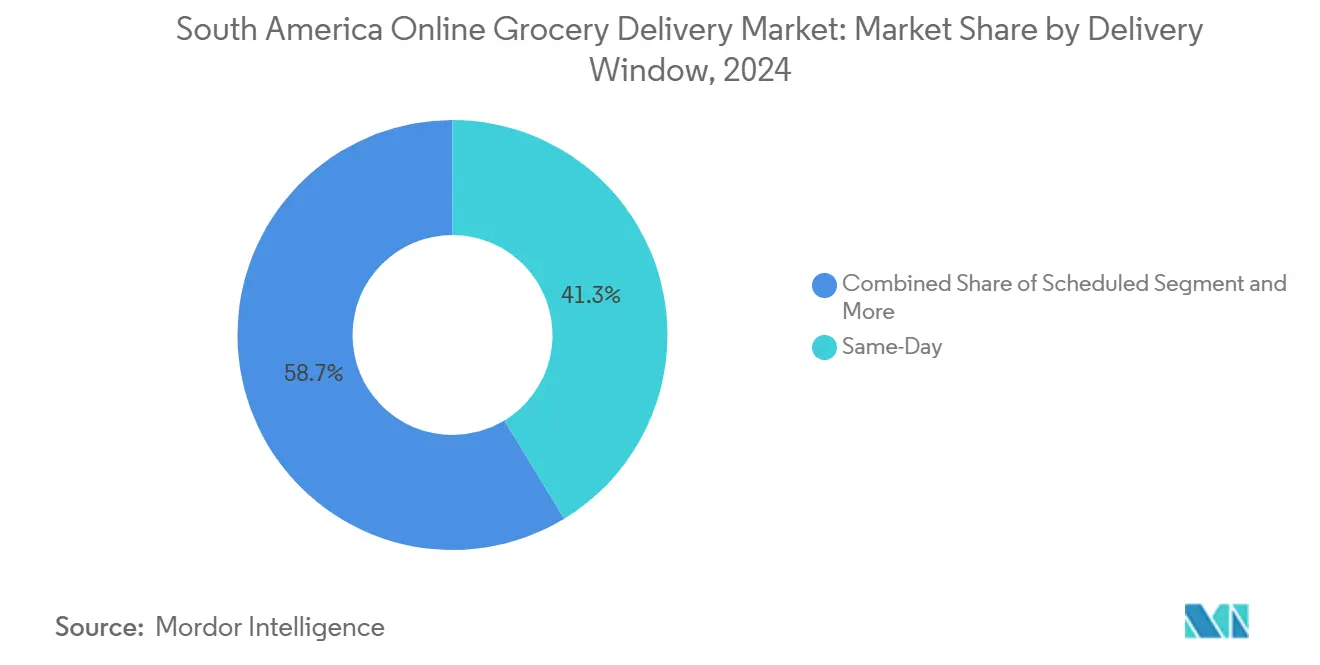

- By delivery window, same-day fulfillment captured 41.30% of the South America online grocery delivery market size in 2024, and instant delivery is advancing at a 14.10% CAGR to 2030.

- By payment method, digital wallets and PIX accounted for 52.60% share of the South America online grocery delivery market size in 2024, and credit/debit cards are rising at an 11.90% CAGR over the forecast horizon.

- By country, Brazil contributed 42.00% of the South America online grocery delivery market share in 2024, whereas Peru registers the fastest forecast CAGR at 11.50% between 2025-2030.

Global valuation is built by aggregating outputs from multiple regions, with South america forming one of the important contributors. Mordor Intelligence's global online grocery delivery market size report represents that cumulative total.

South America Online Grocery Delivery Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid smartphone and Pix-enabled payment adoption | +2.3% | Brazil dominant; spreading to Argentina and Colombia | Short term (≤ 2 years) |

| Expanding dark-store quick-commerce networks | +1.8% | Urban centers across Brazil, Argentina, Chile | Medium term (2-4 years) |

| Surging VC and corporate investment in last-mile cold-chain | +1.5% | Regional; concentrated in Tier-1 metros | Medium term (2-4 years) |

| AI-driven hyper-personalization boosting basket value | +1.2% | Technology hubs in São Paulo, Buenos Aires, Santiago | Long term (≥ 4 years) |

| Mainstream omnichannel push by big-box retailers | +0.9% | Global retailers in major South American markets | Short term (≤ 2 years) |

| Cross-border fulfilment via regional trade corridors | +0.7% | MERCOSUR economies; Bioceanic Corridor participants | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Smartphone and PIX-Enabled Payment Adoption

PIX processed 42 billion transactions during 2024, representing 70% of Brazil’s digital payment volume and eliminating checkout friction for millions of unbanked shoppers. [1]Central Bank of Brazil, “PIX Statistics,” BCB.GOV.BR Real-time settlement strengthens platform cash flow and cuts working-capital buffers, letting operators reinvest in logistics and marketing. Argentina’s QR-payment mandate rolling out from May 2025 signals policy convergence on instant rails, while Peru’s Yape- and PLIN-centered wallet ecosystem already touches 85% of urban smartphone users. Together, these systems remove cash-handling risk, accelerate repeat purchases, and allow loyalty programs to integrate payment and delivery data streams. The result is an enlarged addressable base for the South America online grocery delivery market as households shift their routine spending online.

Expanding Dark-Store Quick-Commerce Networks

Dark-store density rose 340% in São Paulo and 280% in Buenos Aires during 2024, enabling sub-60-minute delivery for high-rotation SKUs. Purpose-built micro-fulfillment hubs optimize picking speed, enforce cold-chain compliance, and carry curated assortments reflecting neighborhood demographics. JOKR’s rebrand to DAKI and its consolidation spree underscore the scale economics and capital intensity of instant commerce. Third-party cold-storage specialists such as Emergent Cold supply temperature-controlled nodes, letting platforms avoid heavy fixed-asset outlays while preserving service levels. [2]Emergent Cold, “Company Overview,” EMERGENTCOLD.COMAs urban consumers grow accustomed to near-immediate grocery arrival, operators without dark-store footprints risk churn, pushing the industry toward higher investment thresholds.

Surging VC and Corporate Investment in Last-Mile Cold-Chain

Logistics capital deployment topped USD 2.8 billion in 2024, with 35% allocated to temperature-controlled builds, reflecting investor confidence in perishables delivery. Amazon’s USD 4 billion cloud region in Chile provides compute power for route optimization and demand forecasting, indirectly catalyzing e-grocery innovation. MercadoLibre plans to double Brazilian distribution centers by 2025, integrating grocery payloads into its broader marketplace backbone and capturing network synergies. These moves plug historical infrastructure gaps that limited fresh distribution beyond tier-1 metros, raising service reliability and enlarging geographic coverage for the South America online grocery delivery market.

AI-Driven Hyper-Personalization Boosting Basket Value

Early AI pilots lifted average order values by up to 25% through predictive replenishment cues, coupon targeting, and dynamic bundling. [3]Walmart Chile, “Walmart Chile Deploys AI-Powered Smart Carts,” WALMART.COM Computer-vision-equipped smart carts in Walmart Chile stores feed SKU-level demand signals into online recommendation engines, creating closed-loop merchandising. Region-wide AI frameworks adopted in 2024 promote algorithmic transparency, pushing platforms to explain model outputs and prune bias, which may slow rollout but enhances consumer trust [4]Access Now, “AI Regulation Policies in Latin America,” ACCESSNOW.ORG. Operators that design explainable AI pipelines gain reputational capital and regulatory readiness while converting behavioral data into higher lifetime value.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High logistics and fuel costs compressing margins | -1.8% | Regional; acute in Andes corridors of Peru and Colombia | Short term (≤ 2 years) |

| Regulatory pressure on gig-worker models | -1.4% | Mexico and Colombia leading; spreading to Brazil | Medium term (2-4 years) |

| Patchy cold-chain outside Tier-1 metros | -0.6% | Chile, secondary cities in Argentina | Medium term (2-4 years) |

| Eco-packaging mandates raising unit costs | -0.5% | MERCOSUR trade lanes; Argentina, Paraguay | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Logistics and Fuel Costs Compressing Margins

Last-mile costs make up 35-45% of order value in Peru and Colombia, where mountainous terrain demands specialized vehicles and routing algorithms. Import reliance for refined fuel exposes operators to currency swings, inflating diesel bills, and squeezing contribution margins. Dynamic pricing partially offsets variability, but frequent surcharges risk dampening order frequency among price-sensitive households. Platforms counter by pooling volume across merchants, deploying electric mopeds in flat geographies, and lobbying governments for infrastructure upgrades, yet cost pressure remains a structural drag on the South America online grocery delivery market.

Regulatory Pressure on Gig-Worker Models

Mexico’s December 2024 labor reform reclassifies platform couriers as employees within 180 days, foreshadowing 25-40% labor-cost jumps once social-security contributions and minimum-wage floors apply. Colombia’s congress and Brazil’s senate debate similar bills, spurred by rising union activity and judicial scrutiny. Compliance spend, workflow redesign, and potential productivity dips weigh on EBIT margins, particularly for asset-light marketplace aggregators.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Retail Delivery Maintains Scale While Quick Commerce Surges

Retail delivery represented 46.30% of the South America online grocery delivery market in 2024, reflecting household stock-up missions that favor broad assortments and scheduled slots. Quick commerce grows at a 12.90% CAGR to 2030, capturing impulse purchases and meal-time gaps in dense urban clusters. JOKR’s transition to DAKI illustrates capital requirements: sub-60-minute promises strain unit economics unless order density and basket value rise concurrently. Segment players refine SKU mix, higher share of ready-to-eat and fresh-cut produce, to expand contribution margins and loyalty retention. Meanwhile, meal-kit providers target affluent city cores but lag in scale due to cold-chain gaps and price sensitivity.

Retail delivery operators counter instant rivals by trimming lead times through store-picking optimization, micro-fulfillment pods, and expanded same-day cut-off windows. Their omnichannel models leverage existing brick-and-mortar footprints, giving access to thousands of SKUs and supplier rebates unattainable for dark-store start-ups. The South America online grocery delivery market share of retail delivery may narrow slightly, yet remains the anchor segment because planned weekly shops drive larger baskets and predictable demand. Inventory algorithms adjust stock-keeping levels to reduce spoilage, while partnership with local farms shortens supply chains and differentiates on freshness. This dual strategy preserves scale economics against fast-delivery challengers.

By Platform Model: Marketplace Aggregators Retain Breadth; Dark-Store Operators Scale Depth

Marketplace aggregators held 39.70% of the South America online grocery delivery market share in 2024, capturing volume by onboarding supermarkets and specialty stores without owning inventory. Their asset-light model accelerates international expansion, evidenced by Rappi’s presence in nine countries. However, the South America online grocery delivery market size for pure-play dark-store operators is projected to expand at a 13.40% CAGR to 2030 as investors back controlled-environment fulfillment that ensures speed and quality.

Grocery-owned apps, spearheaded by Carrefour Brasil and Cencosud Chile, integrate loyalty points, in-store pickup, and dynamic pricing engines to shield share against aggregators. MercadoLibre’s ecosystem approach overlays marketplace breadth with proprietary logistics, capturing value across apparel, electronics, and groceries while amortizing infrastructure over multiple verticals. Platform rivalry pivots on data ownership: aggregators gather cross-category behavioral signals, dark-store players harvest granular SKU-level preferences, and grocers combine loyalty and payment histories. Each cohort races to deepen personalization while balancing capex and profitability, with strategic mergers likely as growth moderates post-2030.

By Delivery Window: Same-Day Asserts Reach, Instant Builds Prestige

Same-day service (2-24 hours) commanded 41.30% of the South America online grocery delivery market size in 2024, prized for citywide reach and predictable routing. Instant delivery (< 2 hours) propels a 14.10% CAGR through 2030, initially restricted to São Paulo, Buenos Aires, Bogotá, and Santiago cores, where dark-store grids enable 3-mile fulfillment radii. Scheduled drop-offs (> 24 hours) persist for bulk orders in peri-urban and rural belts, especially in Argentina’s Pampas and Brazil’s interior.

Address-verification software and geolocation APIs raise first-attempt success in Chile from 85.69% toward the 95% benchmark, trimming redelivery costs that impede instant economics. Argentina’s flat topography affords a 1.29-day average domestic transit, positioning the network to extend instant to Córdoba and Rosario without radical infrastructure build-out. Operators price delivery tiers dynamically: free scheduled slots for high-value baskets, paid upgrades for same-day, and premium fees for instant, balancing consumer willingness to pay against fulfillment cost curves. Continued drone-delivery pilots in sparsely populated Andean valleys could redefine segment boundaries after 2030.

By Payment Method: Digital Wallets Outweigh Cards; Cash Shrinks Yet Persists

Digital wallets and PIX together processed 52.60% of South America's online grocery delivery transactions in 2024, owing to easy onboarding, QR support, and cashback incentives. Credit/debit cards rise at 11.90% CAGR as tokenization, 3-D Secure, and issuer promotions entice cardholders wary of fraud. Cash-on-delivery dips steadily but remains relevant in low-banked pockets of Bolivia, Paraguay, and outer Amazonia.

Payment orchestration layers lower decline rates by auto-routing between acquiring banks, enhancing conversion for international cards in cross-border checkout scenarios. For marketplace aggregators, instant-settlement rails improve courier tipping transparency and reduce cash leakage. The South America online grocery delivery market size gains USD 600 million in gross merchandise value each year, solely from lower cart abandonment attributable to wallet adoption. Governments encourage digital rails for tax traceability, cementing a virtuous cycle of cashless uptake and e-grocery penetration.

Geography Analysis

Brazil remains the fulcrum of South America's online grocery delivery activity, supported by PIX ubiquity, venture-backed dark-store rollouts, and Prosus-owned iFood’s USD 226 million EBIT contribution in 2024. São Paulo’s metropolitan area, with 21 million residents, sustains order density high enough for 15-minute delivery promises, while Rio de Janeiro’s tourism economy encourages premium baskets that lift average order value. Beyond tier-1 hubs, networks expand into Porto Alegre, Brasília, and Recife, spurred by tax incentives for cold-storage builds. Government-funded fiber-optic corridors enhance rural connectivity, paving the way for hybrid pick-up points in agricultural zones and broadening the reach of the South America online grocery delivery market.

Peru posts the region’s steepest growth curve on the back of Yape- and PLIN-mediated financial inclusion, 85% smartphone adoption in urban clusters, and municipal grants for refrigerated lockers that sidestep delivery-hour constraints. Investments concentrate along the Pacific corridor, linking Lima’s port to textile hubs in Arequipa. Terrain challenges in the Andes push platforms to experiment with micro-distribution centers at 3,000 meters elevation, where electric van battery performance drops, yet alternative biofuel fleets show promise. Regulatory clarity around digital invoices accelerates merchant onboarding, giving platforms long-run optionality to evolve into multi-vertical super-apps.

Argentina, Colombia, and Chile form a secondary triangle of opportunity. Argentina’s flat Pampas enable low-cost inter-city trucking, achieving a 1.29-day average domestic transit and boosting same-day feasibility in secondary cities. Colombia faces higher operating expenditures due to rugged topography, but Bogotá’s 9 million inhabitants drive sufficient density for venture-funded cold-chain clusters. Chile, despite its narrow geography, commands high basket values, yet address ambiguity causes 14% redelivery rates. Emerging regulatory cooperation under MERCOSUR’s Electronic Commerce Agreement harmonizes customs procedures, trimming cross-border dwell times by 20%, though currency swings still pressure import margins.

Coverage of the online grocery delivery market by Mordor Intelligence spans a wide geographic footprint, with regional analysis available for Middle East and Africa and Asia.

Competitive Landscape

The market exhibits moderate fragmentation, with three region-wide leaders, iFood, Rappi, and PedidosYa, holding double-digit shares across Brazil, Colombia, and Uruguay, respectively. iFood leverages Prosus’ capital to scale its proprietary courier fleet, payment wallet, and AI-powered location clustering that cuts drop-off distance per order by 18%. Rappi, listed in TIME100’s 2024 roster, runs a multi-vertical super-app model encompassing groceries, pharmacy, and travel bookings, securing USD 125 million in fresh capital and debt in 2025 to extend working capital cycles. PedidosYa, backed by Delivery Hero, focuses on southern cone markets and invests in smart-locker grids to cut failed deliveries in Montevideo and Santiago.

Walmart Chile implements computer-vision smart carts and transforms select stores into micro-fulfillment nodes, trimming pick-pack times by 40%. Carrefour Brasil adopts a hub-and-spoke model, pooling dark stores around existing hypermarkets, while Cencosud integrates loyalty points across store-pickup and doorstep modes. Global logistics providers such as CPKC and Americold build temperature-controlled cross-docks, renting space to retail chains and online platforms alike. These shared assets dilute capital burden and heighten service competition.

Technology is the decisive differentiator. AI-driven demand forecasting minimizes spoilage; real-time route optimization raises courier utilization to 2.5 orders per hour in Sao Paulo peaks. Payment innovations, embedded wallets, BNPL for staples, and driver tipping features, boost retention. Market consolidation is likely as growth normalizes post-2030, favoring players with proprietary data moats and multi-country governance capabilities aligned with emerging labor and AI regulations.

South America Online Grocery Delivery Industry Leaders

-

iFood S.A.

-

Rappi S.A.S.

-

PedidosYa SA

-

Cornershop Limited (Uber)

-

Mercado Libre, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Rappi secured USD 25 million in Series F funding with Amazon participating, reinforcing super-app expansion ambitions.

- August 2025: Rappi obtained USD 100 million in conventional debt financing from Santander to bolster working capital for logistics upgrades.

- May 2025: Argentina implemented QR-code payment regulations for public transportation, standardizing digital payment rails that can extend to retail checkouts.

South America Online Grocery Delivery Market Report Scope

An online grocery is either a physical supermarket or grocery store that accepts online orders or a separate e-commerce operation that sells grocery items. This service normally comes with a delivery fee. Online grocers are traditional supermarkets that have created internet channels to serve their customers better.

The South America Online Grocery Delivery Market is segmented by product type (Retail Delivery, Quick Commerce, Meal Kit Delivery) and by Geography (Brazil, Mexico, Argentina, and Rest of South America).

The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

By Product Type

| Retail Delivery |

| Quick Commerce (<60 min) |

| Meal-Kit Delivery |

By Platform Model

| Marketplace Aggregators |

| Grocery-Owned Apps |

| Pure-play Dark-Store Operators |

By Delivery Window

| Scheduled (>24 h) |

| Same-Day (2–24 h) |

| Instant (<2 h) |

By Payment Method

| Digital Wallet/PIX |

| Credit/Debit Card |

| Cash on Delivery |

By Country

| Brazil |

| Argentina |

| Colombia |

| Chile |

| Peru |

| Rest of South America |

| By Product Type | Retail Delivery |

| Quick Commerce (<60 min) | |

| Meal-Kit Delivery | |

| By Platform Model | Marketplace Aggregators |

| Grocery-Owned Apps | |

| Pure-play Dark-Store Operators | |

| By Delivery Window | Scheduled (>24 h) |

| Same-Day (2–24 h) | |

| Instant (<2 h) | |

| By Payment Method | Digital Wallet/PIX |

| Credit/Debit Card | |

| Cash on Delivery | |

| By Country | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America |

Key Questions Answered in the Report

How large is the South America online grocery delivery market in 2025?

It is valued at USD 6.3 billion and is projected to grow at a 10.61% CAGR to 2030.

Which country contributes the most sales?

Brazil accounts for 42.00% of 2024 revenues due to PIX ubiquity, smartphone penetration, and dense logistics corridors.

What segment is expanding fastest?

Instant delivery under two hours posts a 14.10% CAGR through 2030, propelled by dark-store rollouts in major cities.

How important are digital wallets in checkout mix?

Digital wallets and PIX drive 52.60% of 2024 transactions and reduce cart abandonment by offering instant settlement.

Which players lead the competitive landscape?

IFood, Rappi, and PedidosYa dominate regionally, while Carrefour, Walmart, and Cencosud push omnichannel strategies to narrow the gap.

What regulatory shift could affect operating costs most?

Gig-worker reclassification laws in Mexico and proposed legislation in Colombia and Brazil could lift labor costs by up to 40% for delivery platforms.

Page last updated on: