South America Oil And Gas Drone Services Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

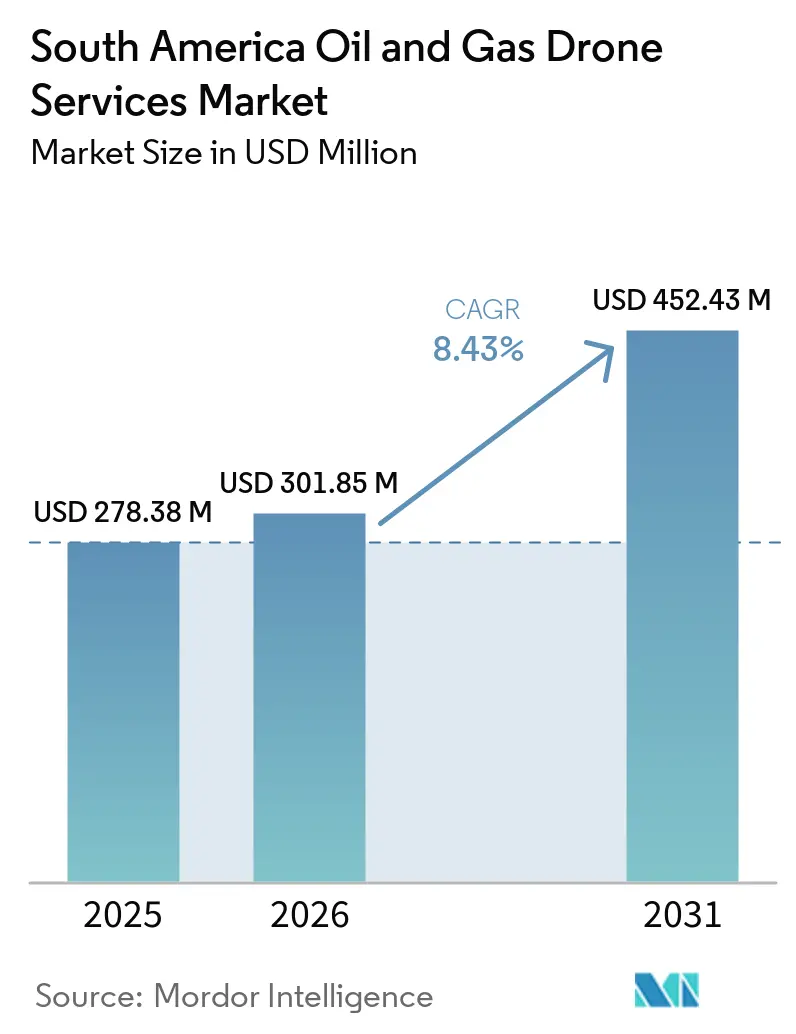

| Base Year Market Size (2025) | USD 278.38 Million |

| Market Size (2026) | USD 301.85 Million |

| Market Size (2031) | USD 452.43 Million |

| Growth Rate (2026 - 2031) | 8.43% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South America Oil And Gas Drone Services Market Analysis by Mordor Intelligence

The South America Oil And Gas Drone Services Market size is projected to expand from USD 278.38 million in 2025 and USD 301.85 million in 2026 to USD 452.43 million by 2031, registering a CAGR of 8.43% between 2026 to 2031. The South America oil and gas drone services market is expanding as operators across Brazil, Argentina, Guyana, Peru, and Ecuador rely more on remote inspection for assets spread across offshore basins, pipelines, and difficult inland terrain. Demand is also rising because methane measurement, leak detection, and auditable infrastructure records are moving from operational preferences to management priorities, especially where export standards and ESG scrutiny are getting tighter. The South America oil and gas drone services market is also benefiting from better sensor integration, as one drone system can now support visual inspection, thermal imaging, LiDAR capture, and gas detection within a single workflow. This is making service contracts more recurring in nature, especially for inspection, emissions monitoring, and digital asset documentation. Competitive conditions remain mixed, with Brazil showing deeper technical depth and stronger contract activity, while much of the rest of the region still depends on local operators for routine work and specialist firms for advanced offshore or emissions-heavy assignments.

Key Report Takeaways

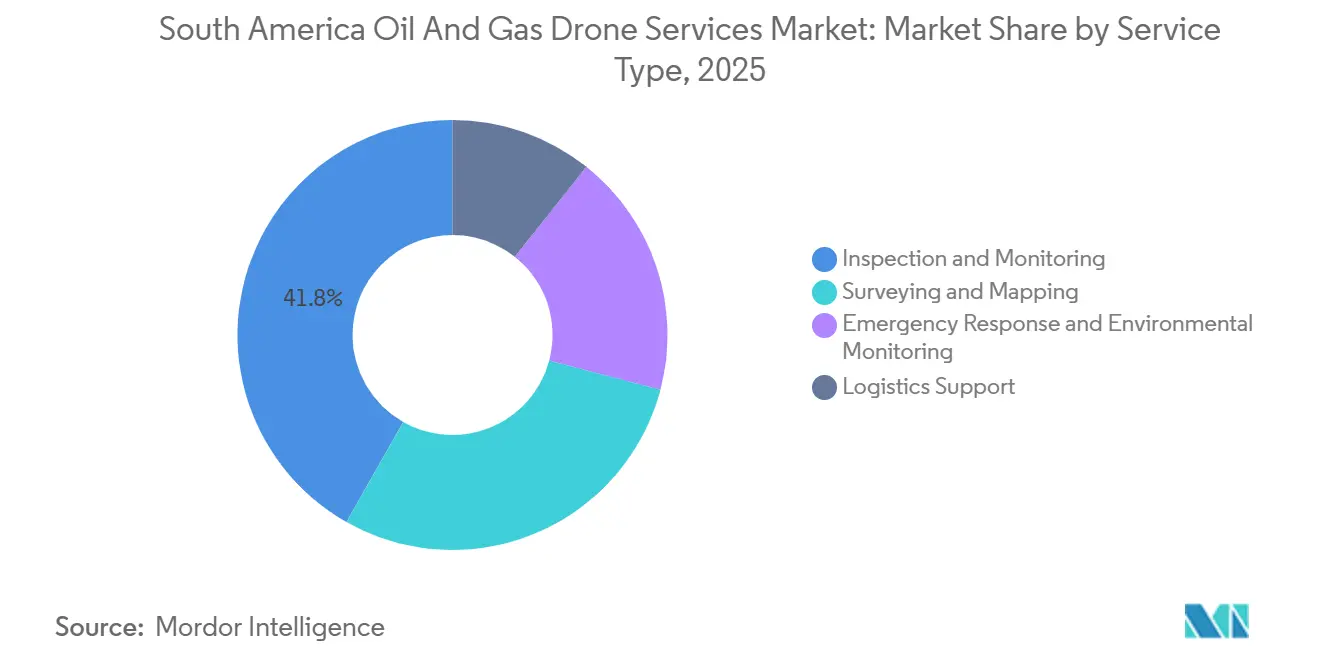

- By service type, Inspection and Monitoring held 41.8% of the South America oil and gas drone services market share in 2025, while Surveying and Mapping is expected to grow at 9.8% CAGR through 2031.

- By application, Pipeline Monitoring and Integrity accounted for 33.7% of the South America oil and gas drone services market size in 2025, while Offshore Platforms and FPSOs are projected to expand at 11.2% CAGR through 2031.

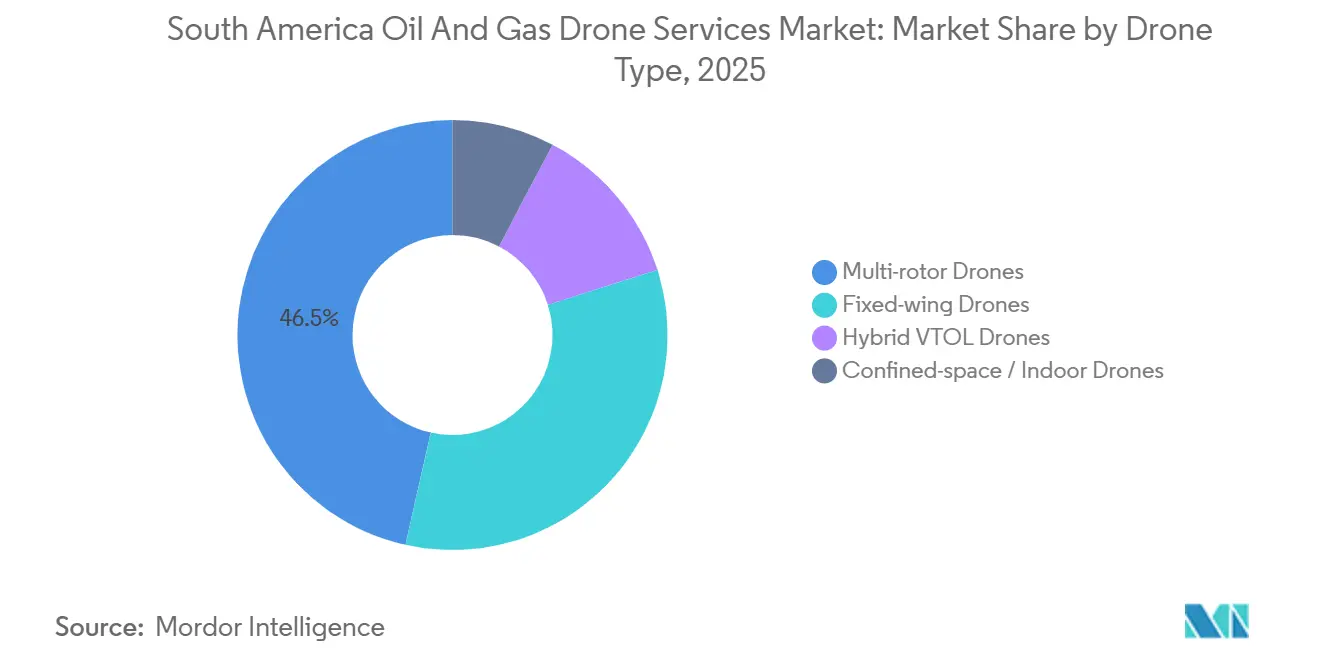

- By drone type, Multi-rotor drones captured 46.5% of the South America oil and gas drone services market size in 2025, while Hybrid VTOL drones are expected to grow at 10.3% CAGR through 2031.

- By geography, Brazil held 44.3% of the South America oil and gas drone services market share in 2025, while Guyana is expected to advance at 13.7% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

South America Oil And Gas Drone Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cost and Safety Gains Over Conventional Inspection Methods | +2.8% | Global, concentrated in Brazil, Argentina, Colombia | Short term (≤ 2 years) |

| Rising Pipeline and Critical Asset Integrity Requirements | +2.0% | Brazil, Argentina, Colombia, Ecuador | Medium term (2-4 years) |

| AI-Enabled Multi-Sensor Inspection Workflows | +1.6% | Brazil, Argentina, spillover to Guyana, Chile | Medium term (2-4 years) |

| Offshore Brazil and Guyana Development Expanding Remote Inspection Demand | +1.4% | Brazil, Guyana | Medium term (2-4 years) |

| Vaca Muerta Methane Monitoring Demand | +0.7% | Argentina, especially Neuquén, Río Negro, Mendoza | Short term (≤ 2 years) |

| Remote Pipeline Right-of-Way Surveillance in Hard-to-Access Corridors | +0.5% | Brazil Amazon, Peru, Colombia, Ecuador | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Cost and Safety Economics Are Reframing the Total Value Proposition

The South America oil and gas drone services market is seeing stronger adoption because operators are treating drone inspection as a safer and more repeatable alternative to confined-space entry, rope access, and other labor-heavy methods. This shift is especially visible in Brazil, where Transpetro reported savings of up to BRL 1 million, or USD 171,000, per tanker inspection cycle after moving to drone-based confined-space surveys, while inspection time fell from 1 week to 3 to 4 days. The commercial effect is important because once inspection moves into routine operating budgets, procurement becomes steadier and contract renewals become easier to justify. The South America oil and gas drone services market is also supported by growing comfort with drone-generated inspection data in formal survey environments, which reduces resistance from operators that previously viewed drone use as a pilot activity rather than a core process [1]Flyability, “Interview, ABS on UT Drone Inspections with the Elios 3,” Flyability, flyability.com. This combination of lower field exposure, shorter downtime, and clearer documentation is helping drone services move into long-cycle maintenance programs.

Pipeline and Critical Asset Integrity Requirements Drive Long-Cycle Contracts

The South America oil and gas drone services market continues to gain from the region’s large network of pipelines, terminals, storage systems, and offshore transfer assets that need regular visual and thermal review. Operators are placing more value on documented inspection history because asset failures now carry operational, financial, and reputational consequences well beyond the repair itself. That is especially relevant in remote corridors, where weather, terrain, and access limits make manual inspection slower and less consistent. In this setting, drone services are becoming part of integrity management programs rather than one-off field jobs, which supports longer contract duration and more frequent repeat work. The South America oil and gas drone services market therefore benefits not only from the need to inspect assets, but also from the need to preserve an auditable inspection trail across distributed infrastructure.

AI-Enabled Multi-Sensor Payloads Extend Inspection Scope Per Flight

The South America oil and gas drone services market is gaining depth as operators adopt platforms that combine thermal sensing, optical gas imaging, LiDAR, and AI-based image review in one inspection cycle. This matters because a single flight can now support structural checks, emissions screening, mapping, and digital record updates with less repeated mobilization. Percepto launched its AI emission detector in June 2025 for remote methane surveying, with automated detection, geolocation, timestamping, and component-level identification built into the workflow. Flyability also advanced autonomous inspection capability in March 2025 with Smart Return-to-Home for the Elios 3, using real-time LiDAR and onboard autonomy to support confined-space work in GPS-denied environments. The South America oil and gas drone services market is therefore moving beyond image capture into a service model where data interpretation, anomaly prioritization, and integration into maintenance systems carry much of the contract value.

Offshore Brazil and Guyana Development Expanding Remote Inspection Demand

The South America oil and gas drone services market is being pulled higher by offshore activity in Brazil and Guyana, where FPSOs, subsea systems, and related pipeline routes require frequent inspection in locations that are expensive and time-sensitive to access. MODEC and Terra Drone renewed their joint R&D agreement in June 2025 for non-destructive internal inspection of FPSO crude oil storage tanks, with the work focused on offshore Brazil and aimed at improving safety, reducing manpower, and raising inspection efficiency [2]Terra Drone, “Terra Drone and MODEC Renew Joint R&D Agreement for FPSO Crude Oil Storage Tanks Inspections,” Terra Drone, terra-drone.net. Their 2025 priorities included stronger airframe design, longer tether use, better maintainability, and a gel-free ultrasonic measurement method, which shows that offshore inspection is shifting toward more continuous and operationally ready deployment MODEC.COM. The South America oil and gas drone services market is also supported by Guyana’s fast project buildout, where new offshore developments are increasing the need for right-of-way surveillance, topside inspection, and related digital documentation. As offshore assets multiply, remote inspection demand rises not only during commissioning but also across the full maintenance cycle.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented Aviation Approvals and BVLOS Constraints | -1.0% | All countries, most acute in Venezuela, Ecuador, Peru | Medium term (2-4 years) |

| Weather, Salt Spray, Wind, and GPS-Denied Operating Conditions | -0.6% | Offshore Brazil, Guyana, Patagonian wind corridors | Short term (≤ 2 years) |

| Sparse Digital Maintenance Backbones at Regional Operators | -0.5% | Ecuador, Peru, Bolivia-adjacent operations, Venezuela | Long term (≥ 4 years) |

| Critical-Infrastructure Data Sovereignty and Security Sensitivity | -0.4% | Brazil, Colombia, national oil companies across the region | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Fragmented BVLOS Frameworks and Aviation Approval Overhead

The South America oil and gas drone services market still faces a major scaling challenge because operators must navigate separate drone approval systems across national borders. Brazil’s ANAC opened Public Consultation No. 09 in June 2025 and proposed RBAC 100, which shifts regulation toward a risk-based system with Open, Specific, and Certified categories and introduces a Specific Category operating framework tied to risk assessment methods such as SORA [3]ANAC Brazil, “Anac Abre Consulta Pública Para Atualizar Regras de Operação de Drones,” Gov.br, gov.br. Argentina also issued Resolution 550/2025 and moved to RAAC 100, 101, and 102, replacing its older class-based system with Open, Specific, and Certified categories aligned with ICAO and Latin American Aeronautical Regulations. Even with that progress, BVLOS missions in the Specific Category still require operational approvals and supporting risk mitigation, which adds lead time and raises deployment cost for cross-border corridor work. The South America oil and gas drone services market therefore favors firms with local entities, local compliance experience, and the ability to absorb country-specific approval delays.

Environmental and Infrastructure Limitations at the Operating Edge

The South America oil and gas drone services market also faces practical operating limits in offshore and remote inland environments where wind, salt spray, battery stress, and restricted navigation conditions can reduce mission consistency. These limits are especially relevant on FPSOs and large industrial assets, where confined spaces and steel-heavy structures create GPS-denied conditions and require purpose-built systems rather than standard commercial drones. Flyability’s Elios 3 gained formal acceptance for class inspections using drone-based ultrasonic thickness measurements, which shows that confined-space inspection is advancing where hardware and software are tailored to harsh environments [4]Flyability, “Interview, ABS on UT Drone Inspections with the Elios 3,” Flyability, flyability.com. The same platform’s Smart Return-to-Home release in 2025 also underlined the importance of onboard autonomy and LiDAR-driven navigation when inspection routes become difficult or signal conditions degrade. Even so, smaller operators in lower-budget markets often delay adoption of these premium systems until they can link the upfront service cost to a clear local return.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Inspection Anchors Revenue While Mapping Accelerates

Inspection and Monitoring retained a 41.8% share in 2025, which kept it as the largest service type in the South America oil and gas drone services market. The segment leads because it addresses the region’s most immediate need, which is frequent review of pipelines, tanks, flare stacks, offshore structures, and other integrity-sensitive assets. Its position is strongest in Brazil, where offshore maintenance programs and tanker inspections already support routine use of drone-based visual review and confined-space access. Formal acceptance of drone-based ultrasonic thickness workflows also strengthens this service line because it makes drone output more usable in recognized inspection and survey settings.

Surveying and Mapping is projected to expand at a 9.8% CAGR from 2026 to 2031, making it the fastest-growing service type in the South America oil and gas drone services industry. Growth is being supported by new route studies, pre-construction planning, right-of-way mapping, and digital twin development across emerging and expanding oil and gas projects. Emergency Response and Environmental Monitoring is also rising as emissions control and leak traceability become more regular contractual needs rather than occasional field exercises. In the South America oil and gas drone services industry, Logistics Support remains the smallest segment because payload limits and operating approvals still restrict routine cargo missions in controlled or complex airspace.

By Application: Pipeline Integrity Holds the Base While FPSOs Set the Pace

Pipeline Monitoring and Integrity held a 33.7% share in 2025 and remained the largest application in the South America oil and gas drone services market. That lead reflects the scale of the region’s transmission corridors and the need for regular, time-stamped inspection records across long assets that are costly to monitor manually. Pipeline use is also favored because drone patrols can cover remote stretches without exposing crews to the same field conditions required by traditional access methods. As a result, this application forms the operational backbone of recurring drone demand across both mature and developing oil and gas systems.

Offshore Platforms and FPSOs are projected to grow at an 11.2% CAGR from 2026 to 2031, making them the fastest-rising application in the South America oil and gas drone services industry. The segment is moving quickly because offshore operators need safer ways to inspect crude oil tanks, topsides, and related structures without repeated human entry into confined spaces. MODEC and Terra Drone renewed their offshore Brazil tank inspection work in 2025 and advanced tethered power, cleaning efficiency, and gel-free measurement development, which points to a broader shift toward more operationally embedded drone inspection on FPSOs. In the South America oil and gas drone services industry, emissions, spill, and ESG monitoring is also emerging quickly as exporters and operators face tighter scrutiny over methane detection, emissions records, and documented response capability.

By Drone Type: Multi-Rotor Leads Current Workflows While Hybrid VTOL Gains Reach

Multi-rotor drones held a 46.5% share in 2025, which made them the leading drone type in the South America oil and gas drone services market. Their position reflects a simple fit with current field work, since close-range visual inspection, stable hovering, and maneuverability are central to tank, flare stack, refinery, and platform surveys. The confined-space and indoor category is also growing because inspection programs increasingly need systems that can work safely inside storage tanks and other GPS-denied structures. Flyability’s Elios 3 acceptance for class inspection activity supports that direction and shows how specialized platforms are widening the use of drone-only workflows in demanding industrial spaces.

Hybrid VTOL drones are projected to grow at a 10.3% CAGR through 2031, making them the fastest-growing type in the South America oil and gas drone services industry. Their appeal lies in combining vertical takeoff and landing with longer range and better corridor coverage than standard multi-rotor platforms. That makes them well suited to pipeline routes where operators need both endurance across distance and the ability to pause for close review at stations or facilities. In the South America oil and gas drone services industry, this segment will depend heavily on how quickly Brazil and Argentina move from transitional approvals toward more practical BVLOS operating conditions for longer-range industrial missions.

Geography Analysis

Brazil accounted for 44.3% in 2025 and remained the largest national market in the South America oil and gas drone services market. The country leads because it combines a large offshore asset base, extensive pipeline and logistics infrastructure, and a more developed local ecosystem for commercial inspection services. Fugro announced a 175-day Petrobras contract addendum for fully remote subsea inspection surveys in Brazil, starting in January 2025, using the Blue Essence uncrewed surface vessel and Blue Volta electric ROV, with a stated 95% reduction in carbon emissions and support from its Rio das Ostras remote operations center. Brazil also has greater regulatory momentum than most peers, since ANAC’s 2025 consultation on RBAC 100 proposed a clearer risk-based path for commercial operations in categories beyond low-risk visual flying.

Argentina and Guyana are shaping the next phase of growth in different ways within the South America oil and gas drone services market. In Argentina, demand is closely tied to Vaca Muerta, where methane quantification, emissions traceability, and broader digital field management are creating space for higher-value drone services. The country’s 2025 regulatory update also matters because Resolution 550/2025 simplified the structure of drone categories and aligned national rules more closely with international practice, which should help formal industrial operations as implementation deepens. Guyana, by contrast, is expanding from a much smaller base but at a faster rate, with a forecast CAGR of 13.7% through 2031 as offshore developments continue to multiply. This makes Guyana the clearest high-growth pocket in the South America oil and gas drone services market, especially for inspection, right-of-way surveillance, and project-support work linked to offshore production and associated infrastructure.

The rest of South America remains uneven in maturity within the South America oil and gas drone services market. Colombia offers one of the stronger near-term opportunities outside Brazil and Argentina because remote terrain supports the case for aerial corridor surveillance and routine integrity reviews. Ecuador and Peru still show demand potential, but budget limits and weaker digital maintenance backbones tend to favor lower-cost, smaller-scale inspection activity over advanced multi-sensor programs. Chile and Venezuela remain more limited, though ESG-driven monitoring and selective thermal or gas-imaging work are gradually widening the service base where operators face stricter financing or compliance expectations.

Competitive Landscape

The South America oil and gas drone services market is semi-consolidated. Global specialists such as Fugro, Terra Drone, MODEC, Percepto, Cyberhawk, Saipem, and Flyability have stronger positions in technically demanding contracts, while local operators retain an advantage in lower-cost corridor patrols and country-specific mobilization. This produces a two-track market where local familiarity matters in day-to-day field work, but recognized technology and formal inspection acceptance matter in high-value projects. The South America oil and gas drone services market therefore rewards firms that can combine compliance readiness, specialized hardware, and scalable data handling.

One clear example is Fugro, which deepened its Petrobras relationship through fully remote subsea inspections in Brazil, supported from an onshore remote operations center and built around uncrewed survey technologies that reduce offshore personnel exposure. Another example is the MODEC and Terra Drone collaboration, where the competitive focus is not only on flying inside FPSO tanks but also on improving cleaning efficiency, tethered power continuity, measurement quality, and deployment readiness for offshore Brazil. Percepto has also pushed the field toward software-led differentiation through its AI emission detector, which automates remote methane surveying and supports compliance-oriented reporting rather than simple image collection. Flyability has strengthened its place in confined-space work because formal acceptance of Elios 3 ultrasonic thickness inspections makes its platform more relevant in tanker, vessel, and enclosed industrial settings where general-purpose drones are less effective. As a result, technological credibility is increasingly tied to whether the provider can shorten downtime, improve data usefulness, and reduce manual access risk.

The South America oil and gas drone services market still leaves room for smaller operators, especially in Argentina, Guyana, Colombia, Ecuador, and Peru, where customer decisions often depend on mobilization cost, local approvals, and field response time. Even so, the market is gradually shifting toward providers that can link aerial data to maintenance systems, emissions workflows, and formal integrity records instead of delivering raw images alone. This raises switching costs for customers once a provider becomes part of a broader digital asset process. Over time, competition will likely center less on flight capability by itself and more on who can turn inspection data into reliable operating decisions at scale.

South America Oil And Gas Drone Services Industry Leaders

Terra Drone Corporation

OMNI Táxi Aéreo

Cyberhawk Innovations Limited

TEXO DSI

Axess Glass Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: DOF Group has announced 12-year charter and service contracts in Brazil for four new ROV support vessels (RSVs). These vessels will support subsea inspection, maintenance, and repair activities for deepwater offshore operations associated with Petrobras. Although focused on ROV and subsea operations rather than aerial UAVs, these contracts enhance the offshore robotic inspection ecosystem within Brazil's oil and gas market.

- June 2025: Terra Drone and MODEC renewed their joint R&D agreement for non-destructive internal inspection of crude oil storage tanks on FPSOs operating offshore Brazil using the Terra UT drone. FY2025 development priorities include improved robustness for global deployment, extended tether cables for large tanks, and a new gel-free ultrasonic measurement method.

- June 2025: Percepto launched its AI Emission Detector for autonomous OGI drone-based methane surveying in the upstream oil and gas sector, capable of detecting emissions at 100 g/hr with 90% confidence. The system integrates Percepto Air Max OGI drone-in-a-box with real-time AI inference for remote, scalable compliance monitoring.

- March 2025: Flyability launched Smart Return-to-Home for the Elios 3, using onboard LiDAR and autonomy algorithms for safe autonomous path return in GPS-denied environments, directly relevant to FPSO and refinery tank inspection in South America.

South America Oil And Gas Drone Services Market Report Scope

Oil and gas drone services utilize UAVs and sensor technologies for inspection, monitoring, surveying, environmental assessment, and logistics support within oil and gas operations. These services enhance safety, lower operational costs, reduce downtime, and improve asset management by enabling quicker and more precise data collection in hazardous or remote areas. The increasing use of AI-enabled analytics, thermal imaging, LiDAR, and methane detection technologies is further amplifying the role of drones in contemporary oil and gas operations.

The South America oil and gas drone services market is segmented by service type, application, drone type, and geography. By service type, the market is segmented into inspection and monitoring, surveying and mapping, emergency response and environmental monitoring, and logistics support. By application, the market is segmented into pipeline monitoring and integrity, offshore platforms and FPSOs, refineries and petrochemical facilities, exploration, construction and ROW survey, and emissions, spill & ESG monitoring. By drone type, the market is segmented into multi-rotor, fixed-wing, hybrid VTOL, and confined-space/indoor drones. The report also covers the market sizes and forecasts for the South America oil and gas drone services market across major countries in the region. For each segment, the market sizing and forecasts have been done on the basis of value (USD).

| Inspection & Monitoring |

| Surveying & Mapping |

| Emergency Response & Environmental Monitoring |

| Logistics Support |

| Pipeline Monitoring & Integrity |

| Offshore Platforms & FPSOs |

| Refineries & Petrochemical Facilities |

| Exploration, Construction & ROW Survey |

| Emissions, Spill & ESG Monitoring |

| Multi-rotor Drones |

| Fixed-wing Drones |

| Hybrid VTOL Drones |

| Confined-space / Indoor Drones |

| Brazil |

| Argentina |

| Guyana |

| Colombia |

| Ecuador |

| Peru |

| Chile |

| Venezuela |

| Rest of South America |

| By Service Type | Inspection & Monitoring |

| Surveying & Mapping | |

| Emergency Response & Environmental Monitoring | |

| Logistics Support | |

| By Application | Pipeline Monitoring & Integrity |

| Offshore Platforms & FPSOs | |

| Refineries & Petrochemical Facilities | |

| Exploration, Construction & ROW Survey | |

| Emissions, Spill & ESG Monitoring | |

| By Drone Type | Multi-rotor Drones |

| Fixed-wing Drones | |

| Hybrid VTOL Drones | |

| Confined-space / Indoor Drones | |

| By Geography | Brazil |

| Argentina | |

| Guyana | |

| Colombia | |

| Ecuador | |

| Peru | |

| Chile | |

| Venezuela | |

| Rest of South America |

Key Questions Answered in the Report

What is the current size of South America oil and gas drone services?

The South America oil and gas drone services market reached USD 301.85 million in 2026 and is projected to reach USD 452.34 million by 2031 at an 8.43% CAGR.

Which service type leads regional demand?

Inspection and Monitoring led in 2025 with a 41.8% share because operators still prioritize asset integrity, confined-space inspection, and routine condition checks across pipelines, tanks, and offshore facilities.

Which application is growing the fastest in the region?

Offshore Platforms and FPSOs are the fastest-growing application, with an 11.2% CAGR through 2031, supported by Brazil’s offshore base and Guyana’s rapid project expansion.

Why are drone services becoming more important for oil and gas operators in South America?

Operators are using drones more often because they improve safety, reduce access time, support methane and emissions measurement, and create digital inspection records that fit compliance and maintenance programs.

Which country leads regional demand?

Brazil led the region in 2025 with a 44.3% share due to its offshore asset scale, Petrobras-linked activity, and a more mature drone inspection ecosystem.

Page last updated on: