South America Mobile Broadband Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

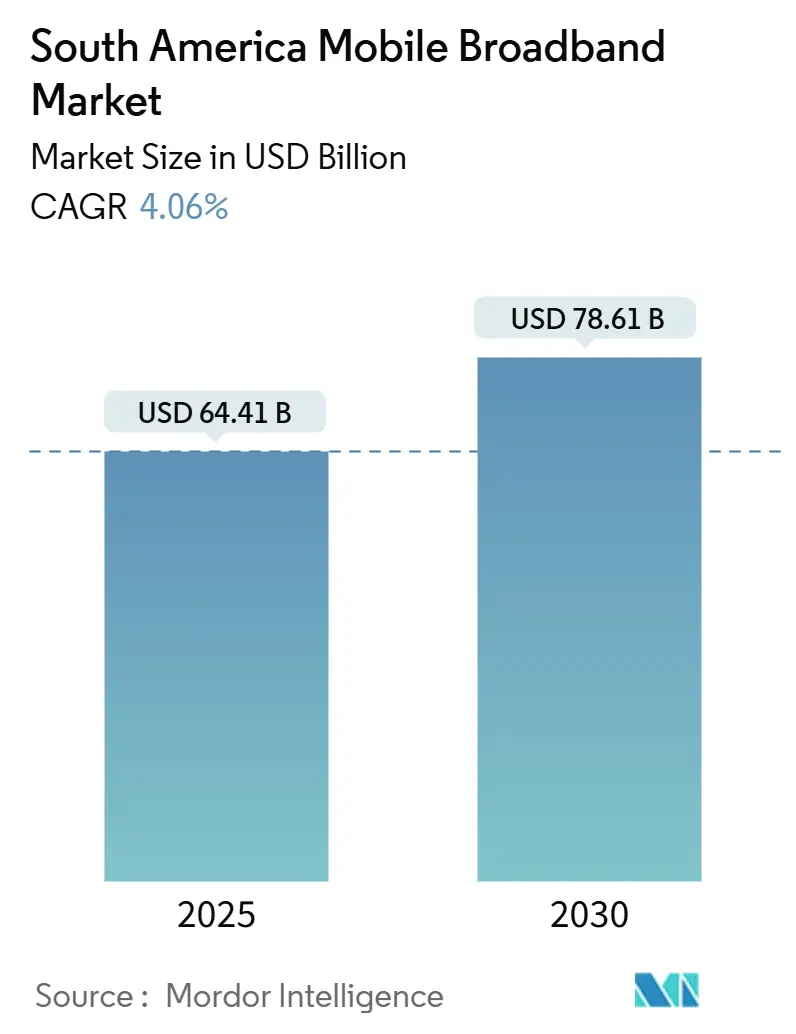

| Market Size (2025) | USD 64.41 Billion |

| Market Size (2030) | USD 78.61 Billion |

| Growth Rate (2025 - 2030) | 4.06% CAGR |

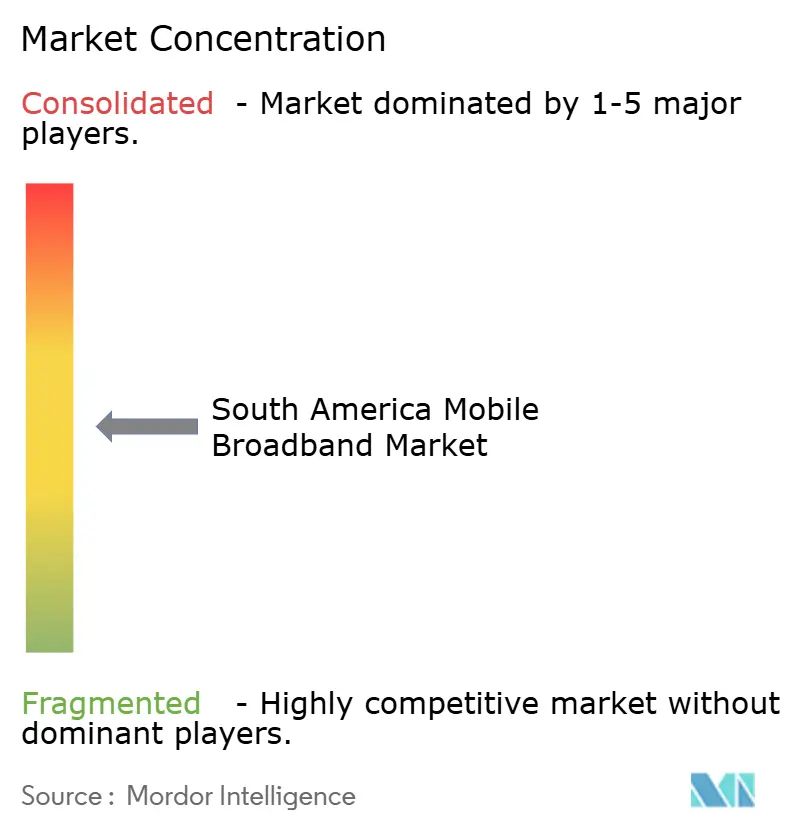

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South America Mobile Broadband Market Analysis by Mordor Intelligence

The South America Mobile Broadband Market size is estimated at USD 64.41 billion in 2025, and is expected to reach USD 78.61 billion by 2030, at a CAGR of 4.06% during the forecast period (2025-2030).

This trajectory reflects accelerated 5G rollouts, government-funded digital-inclusion programs, and falling smartphone prices that together widen addressable demand. Operators leverage network-sharing and satellite backhaul to extend coverage while controlling capital intensity, and enterprise digitization in manufacturing, mining, and finance unlocks premium connectivity revenue. Rising mobile video consumption, super-app penetration, and e-commerce integration further boost traffic volumes, prompting edge-computing investments that improve user experience. Regulatory agencies such as ANATEL, SUBTEL, and CRC continue to pair new spectrum releases with rural-coverage obligations, reinforcing structural growth for the South America mobile broadband market.

Key Report Takeaways

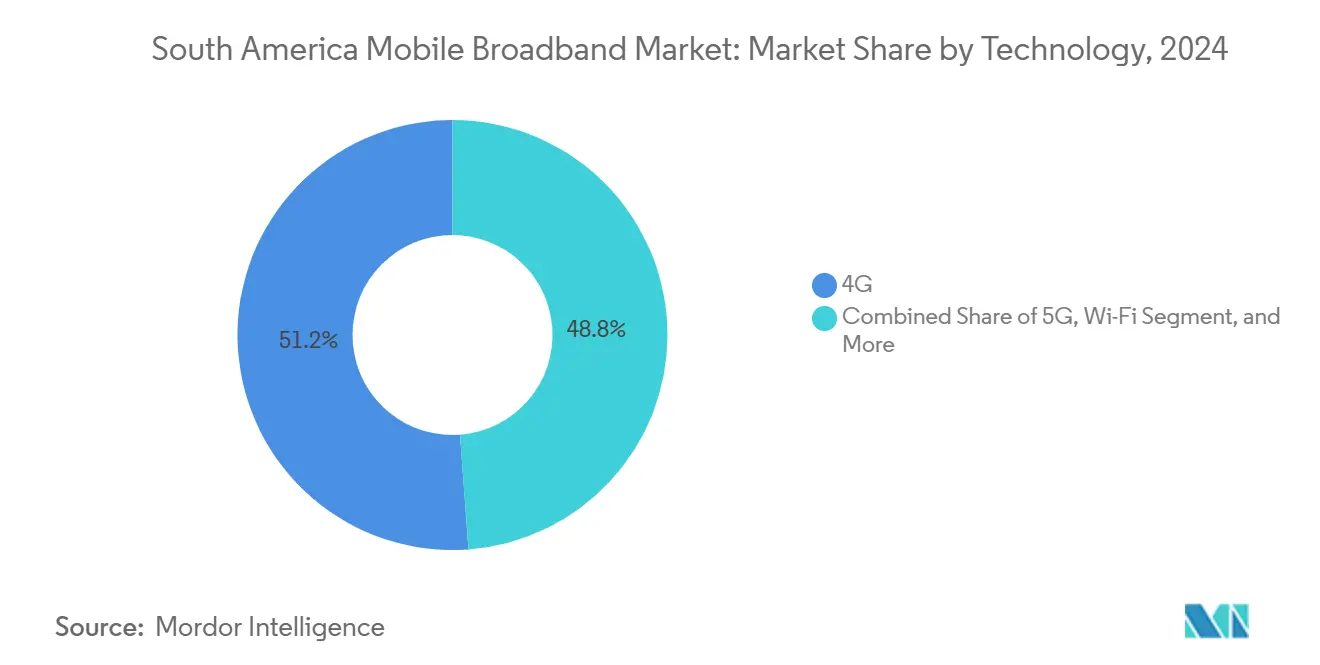

- By technology, 4G networks led with a 51.19% South America mobile broadband market share in 2024; 5G services are projected to expand at a 17.39% CAGR to 2030.

- By service type, mobile data plans accounted for 77.18% of the South America mobile broadband market size in 2024, while Voice-over-LTE is advancing at a 17.27% CAGR through 2030.

- By end-user, consumer connections held 86.09% of revenue in 2024; enterprise subscriptions are forecast to grow at a 10.89% CAGR between 2025-2030.

- By geography, Brazil commanded 32.80% of regional revenue in 2024, whereas the rest of South America is registering the fastest 7.18% CAGR across the same horizon.

- Three leading operators—América Móvil, Telefónica, and TIM Brasil—collectively captured roughly 65% revenue in 2024.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global valuation is built by aggregating outputs from multiple regions, with South america forming one of the important contributors. Mordor Intelligence's global mobile broadband market size report represents that cumulative total.

South America Mobile Broadband Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expanding 5G network deployments across major urban corridors | 2.1% | Brazil, Chile, Colombia urban centers | Medium term (2-4 years) |

| Surging mobile video-streaming consumption among Gen-Z and Millennials | 1.8% | Regional, strongest in Brazil and Argentina | Short term (≤ 2 years) |

| Government-backed digital-inclusion programs | 1.4% | Brazil dominant, expanding to Colombia and Peru | Long term (≥ 4 years) |

| Declining average smartphone prices below USD 120 threshold | 1.2% | Regional with emphasis on rural markets | Medium term (2-4 years) |

| Satellite backhaul integration for remote Amazon basin coverage | 0.9% | Brazil, Peru, Colombia Amazon regions | Long term (≥ 4 years) |

| Rapid fintech & super-app adoption requiring always-on connectivity | 0.6% | Urban centers across all major markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Expanding 5G Network Deployments Across Major Urban Corridors

Fifth-generation rollouts in São Paulo, Santiago, and Bogotá materially lift average revenue per user despite higher site-densification costs. TIM Brasil’s standalone 5G footprint spanned 89 cities by December 2024, and subscribers on these tiers generated 23% higher ARPU than 4G users, reflecting premium pricing for low-latency applications.[1]TIM Brasil, “Investor Presentation Q4 2024,” tim.com.br Telefónica reduced per-site capital outlay by roughly 35% using a passive-infrastructure sharing pact with América Móvil, accelerating coverage in mid-tier cities while retaining service differentiation through network-slice orchestration. [2]Telefónica, “Network Sharing Fact-Sheet,” telefonica.comChile’s Entel used mmWave spectrum to serve Santiago’s financial district and mining corridors, helping national 5G penetration reach 18% in late 2024. In Colombia, a December 2024 auction assigned 3.5 GHz licenses with a 40%-population coverage mandate within 24 months, creating predictable demand for radio and fiber vendors. [3]SUBTEL Chile, “Mobile Connectivity Statistics 2024,” subtel.cl

Surging Mobile Video-Streaming Consumption Among Gen-Z and Millennials

Video traffic already forms 78% of regional mobile data payload. Gen-Z users stream an average of 4.2 hours daily, compared with 2.8 hours for Millennials, compelling operators to add mid-band spectrum and deploy edge caches. Netflix lifted its Latin America production budget by 45% in 2024 to USD 800 million to localize content and deepen engagement. Unlimited video plans now comprise 42% of gross additions, though they compress per-gigabyte revenue as data volumes rise 38% annually. América Móvil and Telefónica have introduced metro-edge facilities that cut video latency by 40%, supporting 4K handsets and raising the attach-rate for premium tiers. Short-form clips on TikTok and Instagram Reels use 2.3 times more data than plain messaging, nudging networks toward distributed-content architectures.

Government-Backed Digital-Inclusion Programs

Brazil’s Programa Internet Brasil earmarks USD 1.2 billion through 2026 to connect 22 million rural residents, with fiber-to-home thresholds set for communities above 1,000 inhabitants. Colombia’s Plan Nacional de Conectividad channels USD 650 million into remote areas previously constrained by conflict, prioritizing 4G/5G fixed-wireless over fragile copper. Peru’s Internet Para Todos—jointly supported by Meta and IDB Invest—extends 4G to 6,500 villages through open-RAN towers and satellite backhaul, offering operators subsidized anchor-tenant demand and cutting first-year cash needs by about two-thirds. These initiatives stimulate incremental user growth in otherwise uneconomic territories.

Declining Average Smartphone Prices Below USD 120 Threshold

Component deflation and aggressive vendor financing have ushered sub-USD 120 5G handsets into mass retail, eliminating the top adoption barrier in low-income segments. Regional carriers bundle entry devices with zero-down, 24-month plans, reducing effective ownership cost to USD 8-12 per month including service. Samsung’s Galaxy A-series and multiple Chinese OEMs together populate most shelves, allowing prepaid subscribers to transition to 4G and 5G plans without sticker shock. Operator device subsidies still average USD 40 per unit, but faster ARPU uplift shortens payback periods to 18 months.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High spectrum acquisition and licensing costs | -1.3% | Regional, most severe in Brazil and Argentina | Medium term (2-4 years) |

| Persistent macro-economic volatility & local-currency depreciation | -0.9% | Argentina, Brazil secondary impact | Short term (≤ 2 years) |

| Regulatory uncertainty on mmWave allocations | -0.6% | Urban markets across all countries | Long term (≥ 4 years) |

| Power-grid instability raising OPEX for rural base-stations | -0.4% | Rural markets, Amazon basin emphasis | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Spectrum Acquisition and Licensing Costs

Brazil’s 2024 auction raised USD 1.8 billion, obliging TIM Brasil to invest USD 520 million merely for 3.5 GHz spectrum on top of USD 2.1 billion earmarked for network rollout through 2027. Argentina’s unit price of USD 0.08 per MHz-pop is roughly triple Colombia’s, reflecting macro-risk premiums that dent operator free cash flow. Yearly usage fees reach 2.8% of gross revenue in some markets, forcing carriers to pursue sharing or trading mechanisms not yet fully blessed by regulators, thereby deferring rural upgrades.

Persistent Macro-Economic Volatility and Local-Currency Depreciation

Local-currency weakness inflates imported-equipment costs by nearly one-quarter each year, while revenues remain denominated in pesos or reals. Argentina’s 54% devaluation during 2024 prompted quarterly tariff resets that stirred churn among price-sensitive prepaid users. In Brazil, lenders now require USD-linked guarantees for radio-access financing, widening interest spreads by 250 basis points. Such volatility lengthens modernization timelines and pressures margins until hedging, local content sourcing, or cost-sharing initiatives absorb shocks.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: 5G Standalone Architecture Drives Premium Service Differentiation

In 2024, 4G retained 51.19% South America mobile broadband market share as ongoing rural rollouts extend coverage. Yet the 5G cohort is poised for a 17.39% CAGR to 2030 on the back of ultra-low-latency use cases in mining, agriculture, and fintech. Petrobras already leases a private 5G slice from TIM Brasil for offshore monitoring that earns about USD 2.3 million annually per installation. Meanwhile, LTE will persist in remote zones where dense 5G radios remain uneconomical. Satellite-cellular hybrids, particularly for the Amazon basin, add incremental reach.

Operators craft differentiation through standalone-core upgrades that unlock dynamic network slicing. Regulatory agencies emphasize technology neutrality but pair spectrum awards with obligatory rural footprints, ensuring legacy 4G remains a parallel workhorse. mmWave deployments continue at a measured pace owing to tropical propagation and limited approved-vendor catalogs.

By Service Type: VoLTE Quality Improvements Accelerate Voice Migration

Mobile data bundles dominated 77.18% of the South America mobile broadband market size in 2024; still, Voice-over-LTE subscriptions are scaling at 17.27% CAGR as legacy circuit switching sunsets. VoLTE penetration already touches 68% in key metros, supported by call-setup reductions and HD-audio that lift net promoter scores. Enterprise-oriented mobile hotspots become commonplace for hybrid work, adding 31% higher ARPU compared with consumer data-only lines.

Operators now bundle VoLTE with messaging and video chat, defending against over-the-top cannibalization. Network optimizations have brought dropped-call ratios below 0.8%, well ahead of the 2.1% still seen on 3G voice. Average monthly data use hit 12.4 GB in 2024, with video commanding three-quarters of that load, underscoring the need for continued radio-capacity growth.

By End-User: Enterprise Digital Transformation Accelerates B2B Growth

Consumer lines delivered 86.09% of 2024 revenue, but enterprise circuits are scheduled to expand at a 10.89% CAGR. Corporate users yield 2.8× higher average revenue per connection, chiefly through IoT telemetry, cloud back-up, and slice-based service-level agreements sold at USD 120-180 monthly. Mining operators employ private 5G for autonomous haulage, saving up to 20% in operating costs, while banks prioritize always-on secure links for mobile payments.

Small and medium enterprises likewise migrate to SaaS tools that demand resilient wireless connectivity. Municipal smart-city tenders in São Paulo, Santiago, and Bogotá already exceed USD 50 million each in contracted value, ensuring stable multi-year cash flows for participating carriers.

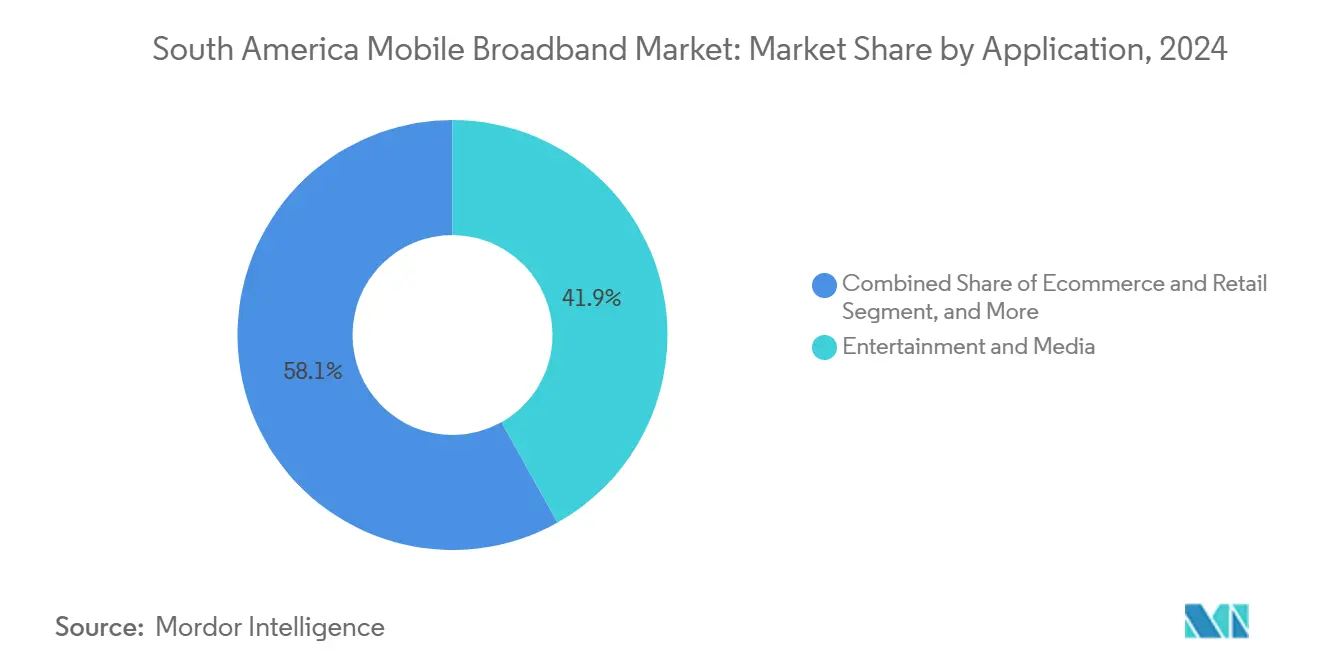

By Application: E-commerce Integration Drives Mobile Payment Ecosystem Growth

Entertainment and media held 41.87% share in 2024, buoyed by streaming and mobile gaming. E-commerce and retail-use cases are registering a 12% CAGR as super-apps integrate shopping, payments, and logistics, prompting merchants to pivot toward mobile checkout. Social and communication apps remain sticky, with WhatsApp Business APIs translating into fresh B2B messaging revenue for operators.

Telemedicine and distance education accelerate in rural zones where mobile represents first-ever broadband. Gaming, meanwhile, spurs premium-tier adoption: regional esports events stream exclusively over 5G, driving data-plan upgrades among younger demographics.

By Spectrum Band: mmWave Deployments Face Infrastructure Challenges

Sub-1 GHz frequencies accounted for 51.30% of active connections in 2024, favored for wide-area and rural economics. Mid-band (1-6 GHz) delivers the sweet spot of coverage and capacity for dense urban 5G, while mmWave above 6 GHz is set for 10.23% CAGR thanks to kiosk-style deployments in CBDs and factories. Carrier-aggregation and massive-MIMO improvements boost capacity by up to 60% relative to single-band setups, lifting utilization.

Regulators continue to refine cross-border coordination to protect satellite and broadcast incumbents. Equipment choice remains tight, keeping mmWave bill-of-materials roughly 20% above mid-band alternatives, a gap expected to narrow as more vendors gain certification.

Geography Analysis

Brazil’s 32.80% revenue share reflects a combination of robust spectrum policy and consistent operator capex. By end-2024 the Programa Internet Brasil pushed 4G reach to 89% of municipalities, while 5G covered two-thirds of residents in the nation’s two largest metros. Satellite backhaul is bridging Amazon dead-zones and enabling specific-slice services for forestry and conservation groups.

Chile and Colombia illustrate how regulatory clarity boosts adoption. Chile’s 78% 5G population reach rests on fiber ubiquity and pragmatic site-sharing, translating into swift premium tier uptake by both consumers and enterprises. Colombia’s rural stimulus blends public funds with private execution, ensuring profitable expansion into conflict-affected regions while meeting stringent quality benchmarks.

Elsewhere, Argentina’s macro volatility compels operators to balance pricing discipline with service continuity, whereas Peru’s mountainous geography promotes open-RAN and high-throughput satellite to extend broadband. Collectively, the rest of South America posted the highest 7.18% CAGR, helped by roaming, infrastructure pooling, and rising smartphone penetration.

Coverage of the mobile broadband market by Mordor Intelligence spans a wide geographic footprint, with regional analysis available for Africa, Europe, and Asia.

Competitive Landscape

Regional revenue remains moderately concentrated: América Móvil, Telefónica, and TIM Brasil together controlled about 65% in 2024. América Móvil exploits multi-country scale to offer one-stop enterprise connectivity, while Telefónica differentiates via 5G network slicing and edge-compute alliances with hyperscalers such as Microsoft Azure. TIM Brasil focuses on standalone-core leadership that secures industrial IoT clients in oil, gas, and agribusiness.

Medium-size challengers—including Entel, WOM, and Millicom—seek rural coverage niches or vertical-specific offerings. Infrastructure-sharing deals shave 30-40% off capex and accelerate rural timelines without eroding brand distinction, thanks to software-defined service layers.

New competitive vectors stem from satellite-terrestrial integration: Starlink now wholesales backhaul to TIM and Claro for Amazon coverage, giving rise to an infrastructure-as-a-service segment. Vendor rivalry among Ericsson, Nokia, and Huawei remains intense, with financing packages and local-manufacturing commitments serving as decisive contract levers amid currency-driven cost inflation.

South America Mobile Broadband Industry Leaders

América Móvil

Telefónica S.A.

Entel Chile S.A.

Millicom International Cellular S.A.

WOM S.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: TIM Brasil commits USD 1.2 billion to extend 5G coverage to 150 additional cities, emphasizing IoT slices for industry clients.

- December 2024: América Móvil acquires Colombia’s Columbus Networks for USD 580 million, deepening its regional fiber backbone.

- November 2024: Telefónica teams with Microsoft Azure to build edge nodes in São Paulo, Santiago, and Buenos Aires, cutting latency for financial-services workloads.

- October 2024: Entel Chile activates a standalone 5G core for mining-sector customers, signing USD 15 million in initial contracts.

South America Mobile Broadband Market Report Scope

| 4G |

| 5G |

| LTE |

| Wi-Fi |

| Other Technology |

| Mobile Data |

| Voice over LTE (VoLTE) |

| Mobile Hotspot |

| Consumers |

| Businesses/Enterprises |

| Entertainment and Media (Streaming, Gaming) |

| E-commerce and Retail |

| Social Media and Communication |

| Healthcare and Education |

| Other Applications |

| Sub-1 GHz (Coverage bands) |

| 1 - 6 GHz (Mid-band) |

| >6 GHz mmWave and Terahertz |

| Brazil |

| Chile |

| Colombia |

| Peru |

| Argentina |

| Rest of South America (Panama, Costa Rica, Uruguay, Guatemala, and Others) |

| By Technology | 4G |

| 5G | |

| LTE | |

| Wi-Fi | |

| Other Technology | |

| By Service Type | Mobile Data |

| Voice over LTE (VoLTE) | |

| Mobile Hotspot | |

| By End-User | Consumers |

| Businesses/Enterprises | |

| By Application | Entertainment and Media (Streaming, Gaming) |

| E-commerce and Retail | |

| Social Media and Communication | |

| Healthcare and Education | |

| Other Applications | |

| By Spectrum Band | Sub-1 GHz (Coverage bands) |

| 1 - 6 GHz (Mid-band) | |

| >6 GHz mmWave and Terahertz | |

| By Country | Brazil |

| Chile | |

| Colombia | |

| Peru | |

| Argentina | |

| Rest of South America (Panama, Costa Rica, Uruguay, Guatemala, and Others) |

Key Questions Answered in the Report

What is the projected revenue for South America mobile broadband by 2030?

Aggregate revenue is forecast to reach USD 117.85 billion in 2030, growing at a 7.98% CAGR from 2025.

Which technology segment is expected to add the most new revenue over the next five years?

5G services are poised for the largest incremental gain, expanding at a 17.39% CAGR on the back of premium consumer tiers, network slicing, and enterprise IoT use cases.

How rapidly will 5G subscriptions scale across South America?

Penetration is rising from the low-teens today toward 40% of total broadband lines by 2030 as operators complete standalone-core upgrades and widen mid-band coverage.

What portion of regional broadband revenue does Brazil generate?

Brazil contributes roughly 32.80% of total 2024 revenue and maintains double-digit annual capex to keep that lead.

How are carriers monetizing enterprise demand for mobile broadband?

Operators sell dedicated 5G slices, IoT connectivity, and mobile edge-compute services that yield 2.8× higher average revenue per connection than consumer plans.

What are the chief cost pressures on South American broadband operators?

High spectrum fees, currency depreciation that inflates equipment imports, and rising rural-site power expenses collectively trim cash flow and can delay network expansion.

Page last updated on: