South America Medium Voltage Switchgear Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

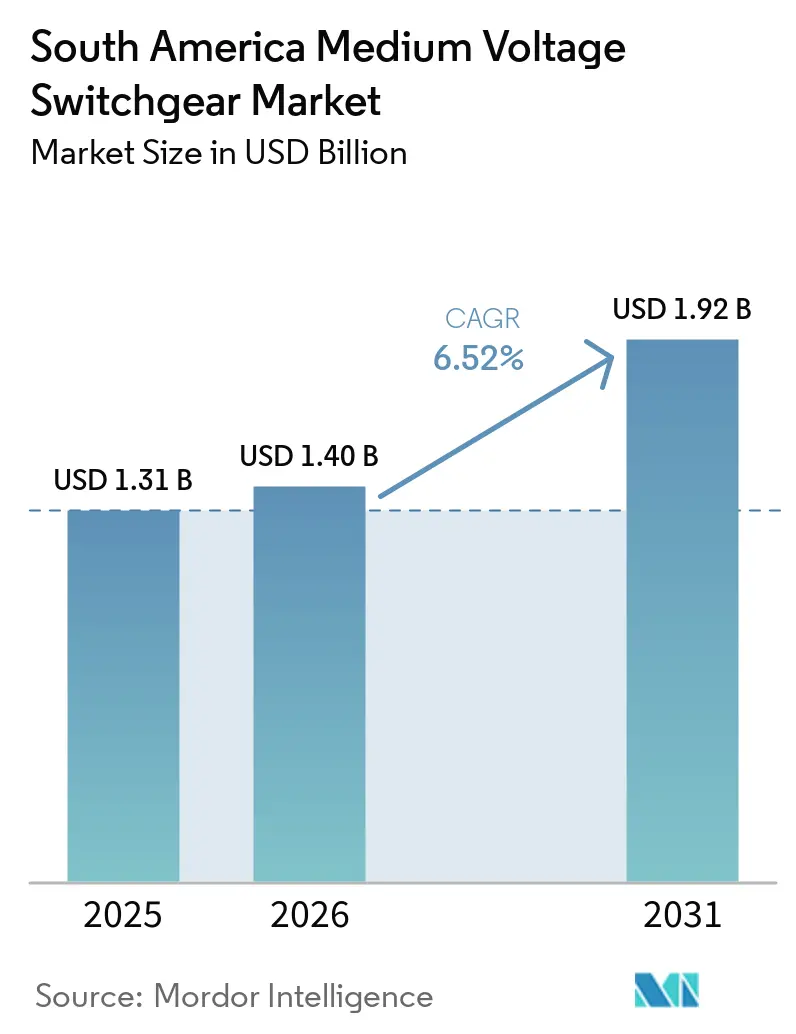

| Base Year Market Size (2025) | USD 1.31 Billion |

| Market Size (2026) | USD 1.40 Billion |

| Market Size (2031) | USD 1.92 Billion |

| Growth Rate (2026 - 2031) | 6.52% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South America Medium Voltage Switchgear Market Analysis by Mordor Intelligence

The South America Medium Voltage Switchgear Market size is expected to grow from USD 1.31 billion in 2025 to USD 1.40 billion in 2026 and is forecast to reach USD 1.92 billion by 2031 at 6.52% CAGR over 2026-2031. Robust grid-reinforcement mandates, accelerating renewable integration, and wide-ranging mining electrification programs underpin this trajectory. Brazil’s January 2026 approval of 687 reinforcement works worth BRL 1.05 billion raised near-term demand for 138 kV and 230 kV collector substations, while Chile’s 43-project 2026 plan allocates USD 647 million for new transformers, BESS, and GIS bays.[1]Strategic Energy, “Chile's transmission expansion plan 2026,” strategicenergy.eu Utilities are front-loading digital-substation rollouts that cut cabling by 80% and enable remote diagnostics, and industrial miners are wiring 220/33 kV feeders to electrify haul-truck fleets, increasing on-site loads by up to 40%.[2]BNamericas, “EPEC will build the country's first Clean GIS Transformer Station,” bnamericas.com Currency volatility and shortages of certified field technicians temper the outlook, but local-content incentives, SF₆-free regulations, and micro-grid loans continue to widen the addressable base for the South America medium voltage switchgear market.

Key Report Takeaways

- By insulation type, air-insulated switchgear led with 58.7% of the South America medium voltage switchgear market share in 2025, while gas-insulated switchgear is forecast to expand at a 7.2% CAGR to 2031.

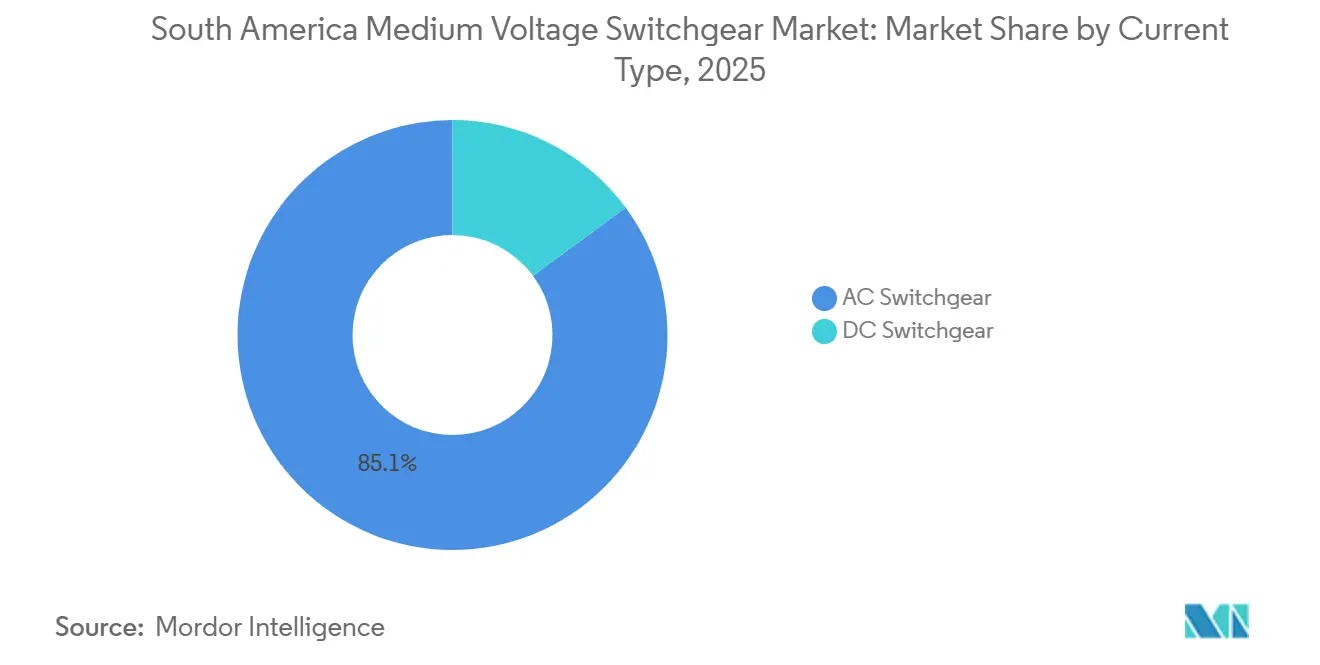

- By current type, AC switchgear accounted for 85.1% of the South America medium voltage switchgear market size in 2025 and DC switchgear is projected to record the fastest 7.7% CAGR through 2031.

- By installation, indoor systems held 70.5% revenue in 2025, whereas outdoor deployments are advancing at a 6.9% CAGR to 2031, fueled by high-altitude mining projects.

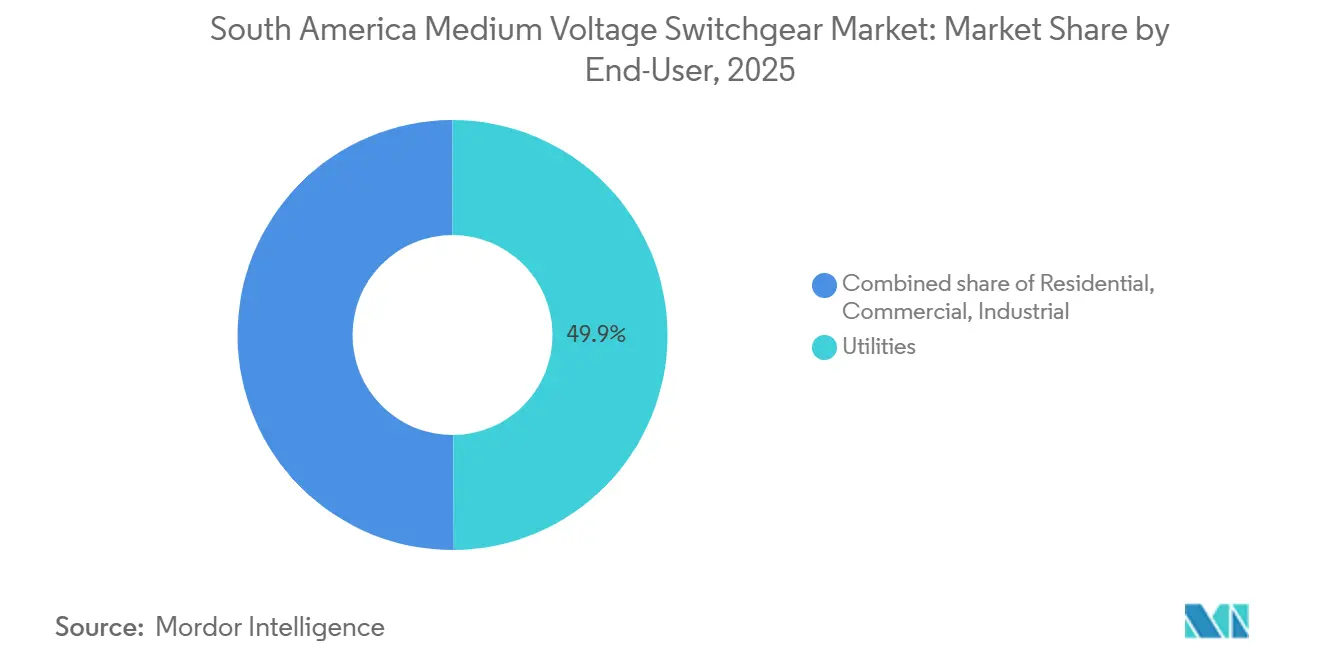

- By end-user, utilities represented 49.9% of 2025 demand and industrial buyers are slated to grow at 7.0% CAGR on the back of copper and lithium expansions.

- By geography, Brazil captured 40.3% revenue in 2025, while Chile is forecast to post the fastest 7.5% CAGR through 2031, anchored by the USD 1.5 billion Kimal–Lo Aguirre HVDC corridor.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

South America Medium Voltage Switchgear Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Grid-reinforcement programs in Brazil’s northeast | +1.2% | Brazil (Bahia, Pernambuco, Ceará) | Medium term (2-4 years) |

| Accelerating renewables-driven sub-transmission projects | +1.5% | Chile, Brazil, Colombia, Argentina | Long term (≥ 4 years) |

| Utility digital-substation modernization mandates | +0.9% | Brazil, Chile, Argentina | Medium term (2-4 years) |

| Electrification of mining operations in the Andean belt | +1.3% | Chile, Peru, Colombia | Long term (≥ 4 years) |

| Local-content incentives for MV equipment manufacturing | +0.7% | Brazil, Argentina | Short term (≤ 2 years) |

| Growth of private micro-grids for remote agribusinesses | +0.5% | Peru, Brazil, Colombia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surging Grid-Reinforcement Programs in Brazil’s Northeast

Brazil’s northeast corridor is executing the largest retrofit wave in two decades. ANEEL cleared 687 reinforcement works worth BRL 1.05 billion in January 2026, followed by BRL 572.6 million in March for 100 additional upgrades.[3]Agência Nacional de Energia Elétrica, “ANEEL autoriza 687 obras que constam do Plano de Outorgas de Transmissão planejado pelo MME,” gov.br Projects focus on 230 kV and 138 kV substations that need compact GIS bays to squeeze into energized yards, minimizing outages. The upcoming BRL 5.8 billion auction adds 4,800 MVA and 888 km of new lines, extending a multi-year tailwind for the South America medium voltage switchgear market.[4]Agência Nacional de Energia Elétrica, “ANEEL autoriza 687 obras que constam do Plano de Outorgas de Transmissão planejado pelo MME,” gov.br

Accelerating Renewables-Driven Sub-Transmission Projects

Renewable curtailment above 10% has pushed Chile and Brazil to commission 220 kV and 132 kV collector systems. Chile’s 1,346 km Kimal–Lo Aguirre HVDC link broke ground in 2025, employing 7,000 workers and integrating 2.5 GW of wind with 1.3 GW under development. Colombia’s UPME tenders for Corzo and Nueva Lorica substations include 25-year concessions with commissioning slated for 2027-2031. Sub-transmission collectors demand 40-50 kA-rated switchgear with IEC 61850 compliance, driving procurement of digital GIS in the South America medium voltage switchgear market.

Utility Digital-Substation Modernization Mandates

Digital architecture is becoming a procurement default. ISA CTEEP’s pilot in São Paulo trimmed substation footprint by 50% and cut control-room size by one-third. Transelec’s upgrades in Chile reduced maintenance downtime during the pandemic. Argentina is installing its first clean-air digital GIS in Córdoba, processing 72 million data points per day, with a sub-two-year payback. Utilities accept a 15-20% capex premium for lifetime OPEX gains, reinforcing digital demand in the South America medium voltage switchgear market.

Electrification of Mining Operations in the Andean Belt

Mining majors are wiring haul fleets to reduce diesel burn. BHP allocated USD 250 million to electrify trucks at Escondida, requiring new 220 kV and 33 kV feeders and a greenfield substation. Pucobre’s USD 870 million Tovaku project combines a 193 MW solar plant, 30 MWh BESS, and a 220/23 kV yard. These projects raise local demand for rugged, dust-proof switchgear rated for -20 °C to +50 °C, sustaining industrial orders across the South America medium voltage switchgear market.

Restraints Impact Analysis*

| Restraint | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Currency volatility inflating imported GIS costs | -0.8% | Brazil, Argentina | Short term (≤ 2 years) |

| Project delays from political regime changes | -0.6% | Argentina, Peru | Short term (≤ 2 years) |

| Shortage of certified field-service technicians | -0.5% | Brazil, Colombia, Chile | Medium term (2-4 years) |

| Slow utility tariff adjustments capping CAPEX | -0.4% | Brazil, Argentina | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Currency Volatility Inflating Imported GIS Costs

Brazil’s 7.2%–20% import duties and a weak real widened GIS landing costs by up to 25%, while Argentina’s peso slide forced utilities toward lower-cost AIS retrofits. Domestic makers quoting in local currency gain share, altering price points in the South America medium voltage switchgear market.

Project Delays from Political Regime Changes

Argentina’s austerity cut infrastructure spend to 0.3% of GDP in 2025, stalling substations and delaying switchgear tenders by 12-18 months. Restart of the USD 5 billion Santa Cruz dam shows recovery is possible but uneven.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Insulation: SF₆-Free Mandates Propel GIS Adoption

Gas-insulated switchgear will outpace the South America medium voltage switchgear market average at a 7.2% CAGR, yet AIS retains price leadership especially for 33 kV mining feeders. Siemens’ ARS 75 billion clean-air GIS in Córdoba sets a regional benchmark, halving footprint and eliminating greenhouse-gas insulation. Chile’s USD 79.6 million BESS-linked substations further confirm GIS as the urban default. Lifecycle savings, rising land prices, and environmental pressure ensure that GIS penetration will keep climbing within the South America medium voltage switchgear market.

AIS remains dominant in cost-sensitive applications with 58.7% 2025 share. In rural Brazil, greenfield 138 kV yards cost 30-40% less with AIS panels and allow quick spares interchange. The South America medium voltage switchgear market size for AIS will still grow in absolute terms, but its share will erode as regulators tighten SF₆ caps and urban projects migrate to compact bays.

By Current Type: DC Switchgear Gains Traction in Solar and EV Infrastructure

DC switchgear’s 7.7% CAGR through 2031 reflects mounting solar output, BESS coupling, and the regional roll-out of CCS2 fast chargers. Brazil’s projected 600,000 EVs in 2026 require clustered chargers tied to MV feeders, spurring orders for bidirectional protection panels. FPSO electrification projects also specify DC fault-limiters to secure offshore grids.

AC switchgear remains ubiquitous above 138 kV and in industrial motors. With 85.1% 2025 share, incremental growth follows GDP and utility reinforcement plans. Hybrid yards combining AC main transformers and DC battery strings will emerge, creating cross-over opportunities in the South America medium voltage switchgear market.

By Installation: Mining and Renewables Drive Outdoor Demand

Outdoor switchgear will close the gap with a 6.9% CAGR as miners electrify fleets at altitudes over 3,000 m. BHP’s Escondida requires IP54 AIS panels tolerant to dust and thermal shock. Wind-farm collector stations in Chile’s north similarly avoid enclosures to cut civil costs.

Indoor equipment sustains 70.5% share in cities where real-estate premiums justify climate-controlled rooms and digital protection hardware. Indoor GIS reduces noise and aids cybersecurity compliance, retaining its anchor status within the South America medium voltage switchgear market.

By End-User: Industrial Segment Leads Growth on Mining Electrification

Industrial buyers will log a 7.0% CAGR as copper, lithium, and LNG operators pour over USD 1 billion into electrical upgrades. New 23 kV feeders and 220/33 kV substations lift order volumes for medium-voltage panels with IEC 61850 gateways.

Utilities, holding 49.9% of 2025 demand, benefit from regulated remuneration and vast reinforcement backlogs. However, budget cycles and tariff politics inject variability, prompting some utilities to pace capex even as the South America medium voltage switchgear market expands steadily.

Geography Analysis

Brazil commands the largest slice of the South America medium voltage switchgear market. The nation expects 6,161 km of new lines and 14,653 MVA of substation additions in 2026, including dual 500 kV circuits from Xingó to Camaçari II and the 1,500 km Graça Aranha–Silvânia spine. Tariff-linked distributor capex of BRL 50 billion in 2026 underwrites solid baseline demand despite currency headwinds.

Chile is the fastest mover in the South America medium voltage switchgear market, riding the USD 1.5 billion HVDC corridor, 43-project 2026 plan, and mining electrification exceeding USD 250 million at Escondida. Compact GIS and battery-ready bays dominate specifications, supporting a 7.5% CAGR outlook.

Argentina’s fiscal restraint curtails near-term orders, yet restarts of the Santa Cruz dams and YPF’s USD 55 billion LNG chain hint at a medium-term rebound. Colombia and Peru advance rural electrification and 500 kV interconnections backed by multilateral loans, while Ecuador and Bolivia modernize 69–230 kV feeders, collectively adding volume to the South America medium voltage switchgear market.

Competitive Landscape

Global OEMs such as ABB, Siemens, Schneider Electric, and Hitachi Energy hold framework deals worth USD 100 million or more, supplying both GIS and AIS across seven countries. Technology edges revolve around SF₆-free insulation—Schneider’s GM AirSeT and Siemens’ clean-air GIS—and digital sensors that enable 24/7 condition monitoring.

Regional champions exploit proximity and cost. WEG’s USD 15.8 million transformer deal in Paraguay and synchronous-condenser supply to Chile underline its widening reach. Lucy Electric’s Araucária plant produces SF₆-free RMUs for Brazilian distributors.

White-space entrants focus on analytics and DC applications. VoltVision integrates cloud-based power-quality platforms with ABB’s SynerLeap accelerator, targeting mining electrification in Chile and Peru. Chinese EPCs linked to State Grid pursue large-scale transmission corridors that could further reshape supplier dynamics in the South America medium voltage switchgear market.

South America Medium Voltage Switchgear Industry Leaders

ABB Ltd.

Siemens AG

Schneider Electric SE

Eaton Corporation plc

WEG Industries SA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: ANEEL approved BRL 572.6 million for 100 upgrades to modernize Brazil’s transmission grid.

- March 2026: Siemens Energy and EPEC commissioned Argentina’s first clean-air GIS substation in Córdoba (132/33/13.2 kV, ARS 75 billion).

- March 2026: Construction resumed on Argentina’s USD 5 billion Santa Cruz hydro complex after a decade of delays.

- February 2026: WEG delivered three 500 MVA, 525 kV transformers to TAESA’s Assis substation in São Paulo.

South America Medium Voltage Switchgear Market Report Scope

MV switchgear, or Medium Voltage Switchgear, serves as a centralized hub, housing essential electrical components such as circuit breakers, fuses, and switches within a protective metal enclosure. Its primary function is to control, protect, and isolate electrical circuits in power systems. This ensures safe and efficient power distribution across industries, commercial buildings, and utilities.

The South America medium voltage switchgear market is segmented by insulation, current type, installation, end-user, and geography. By insulation, the market is segmented into gas-insulated switchgear, air-insulated switchgear, and others. By current type, the market is segmented into AC switchgear and DC switchgear. By installation, the market is segmented into indoor and outdoor. By end-user, the market is segmented into utilities, residential, commercial, and industrial. The report also covers the market size and forecasts for the South America medium voltage switchgear market across the regions. For each segment, the market sizing and forecasts have been done based on value (USD).

| Gas Insulated Switchgear (GIS) |

| Air Insulated Switchgear (AIS) |

| Others |

| AC Switchgear |

| DC Switchgear |

| Indoor |

| Outdoor |

| Utilities |

| Residential |

| Commercial |

| Industrial |

| Brazil |

| Argentina |

| Chile |

| Colombia |

| Peru |

| Rest of South America |

| By Insulation | Gas Insulated Switchgear (GIS) |

| Air Insulated Switchgear (AIS) | |

| Others | |

| By Current Type | AC Switchgear |

| DC Switchgear | |

| By Installation | Indoor |

| Outdoor | |

| By End-User | Utilities |

| Residential | |

| Commercial | |

| Industrial | |

| By Geography | Brazil |

| Argentina | |

| Chile | |

| Colombia | |

| Peru | |

| Rest of South America |

Key Questions Answered in the Report

What is the size of South America medium voltage switchgear market?

The South America medium voltage switchgear market stands at USD 1.4 billion in 2026 and is expected to reach USD 1.92 billion by 2031, expanding at a 6.52% CAGR over 2026-2031.

What is the forecast CAGR for medium voltage switchgear across South America?

The market is projected to grow at a 6.52% CAGR between 2026 and 2031.

Which insulation technology is growing fastest?

Gas-insulated switchgear, especially SF?-free designs, is forecast to expand at 7.2% CAGR to 2031.

Why is Chile the fastest-growing country segment?

A USD 1.5 billion HVDC corridor, 43 new transmission projects, and mining electrification push Chile to a 7.5% CAGR.

How are tariff policies affecting procurement?

Brazil's higher import duties and capped retail rates are raising costs and nudging buyers toward locally assembled switchgear.

What skills gap challenges suppliers?

A deficit of 75,000 certified electrical engineers in Brazil is extending commissioning schedules and elevating project costs.

Page last updated on: