South America Low-Density Polyethylene (LDPE) Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

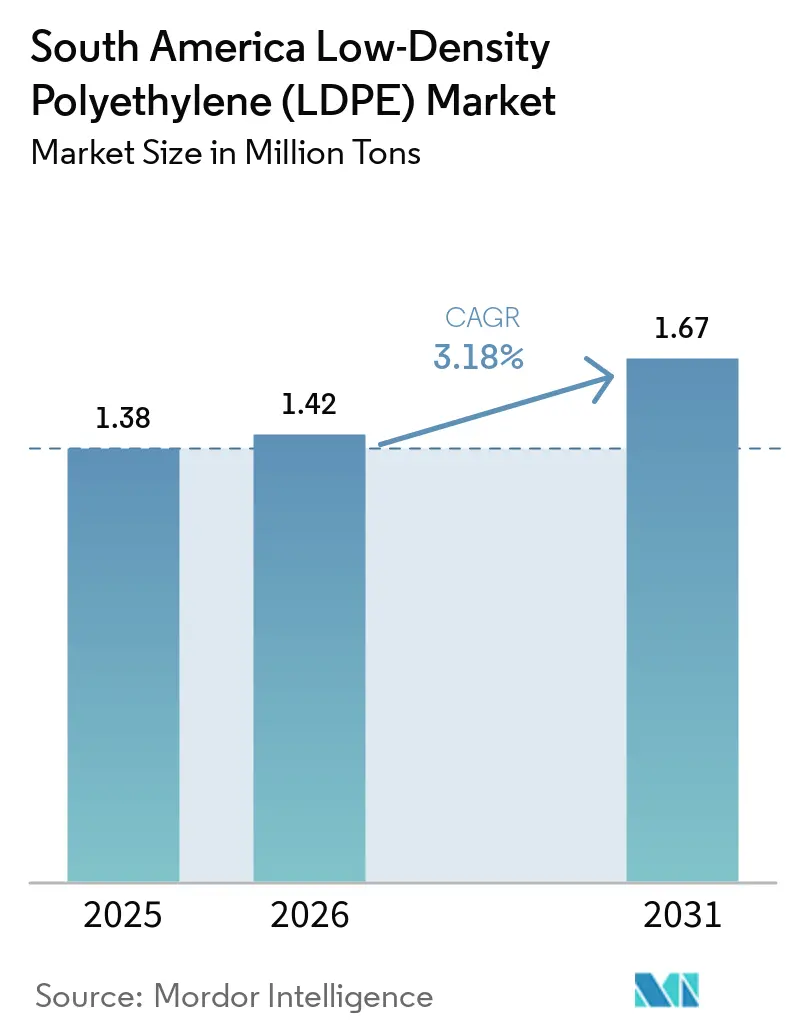

| Base Year Market Size (2025) | 1.38 Million tons |

| Market Volume (2026) | 1.42 Million tons |

| Market Volume (2031) | 1.67 Million tons |

| Growth Rate (2026 - 2031) | 3.18% CAGR |

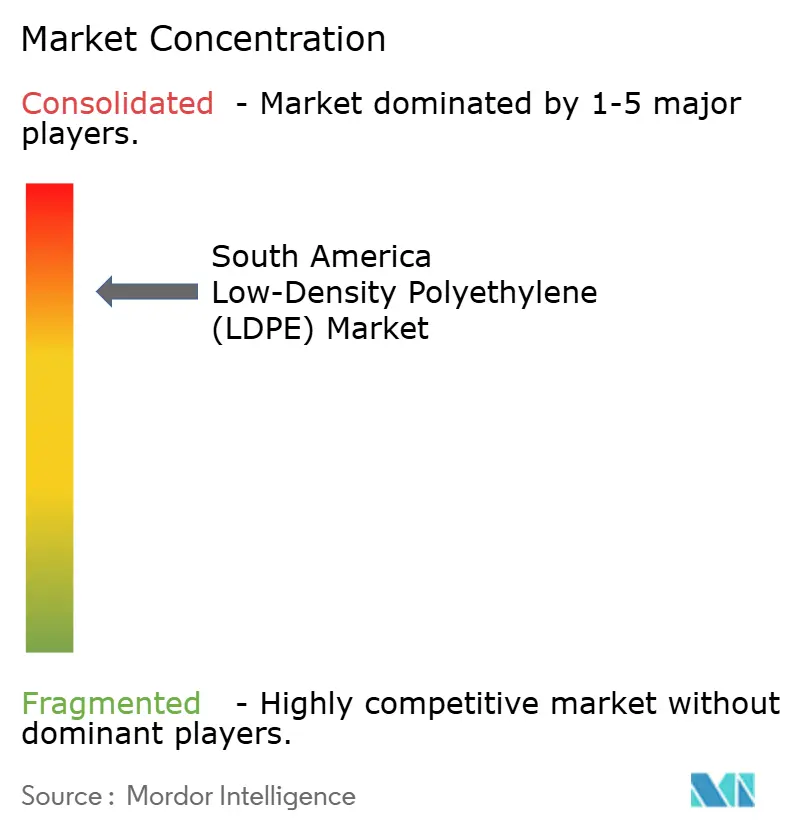

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South America Low-Density Polyethylene (LDPE) Market Analysis by Mordor Intelligence

The South America Low-Density Polyethylene Market size is projected to expand from 1.38 Million tons in 2025 and 1.42 Million tons in 2026 to 1.67 Million tons by 2031, registering a CAGR of 3.18% between 2026 to 2031. The South America Low-Density Polyethylene (LDPE) market is expanding because converters are investing in higher-output flexographic presses, bio-based capacity is scaling at Braskem’s Triunfo complex, and automotive lightweighting incentives under Brazil’s Programa Mover are stimulating polymer demand. Sustained e-commerce growth in São Paulo, Buenos Aires, and Lima is translating into higher stretch-film throughput at modern distribution hubs, while pipe-coating projects tied to offshore oil and new gas pipelines preserve a niche for LDPE adhesives despite the dominance of polypropylene topcoats. Feedstock-price swings remain the principal headwind: ethylene–naphtha spreads narrowed below USD 105 per ton in Q1 2026, squeezing converter margins and sharpening the focus on operational efficiency. Meanwhile, an anti-dumping probe against United States and Canadian polyethylene is tilting the trade balance in favor of domestic producers and reinforcing the medium-term pricing floor.

Key Report Takeaways

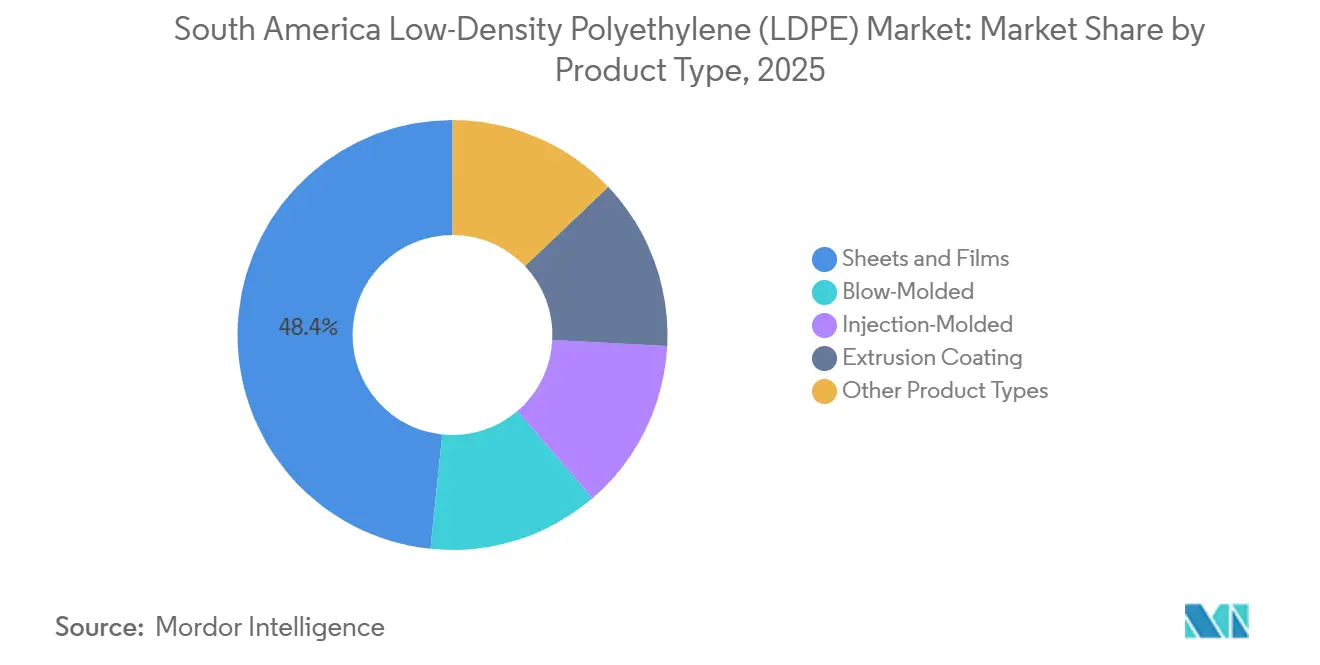

- By product type, sheets and films held 48.37% of the South America Low-Density Polyethylene (LDPE) market share in 2025 and are forecast to advance at a 3.46% CAGR through 2031.

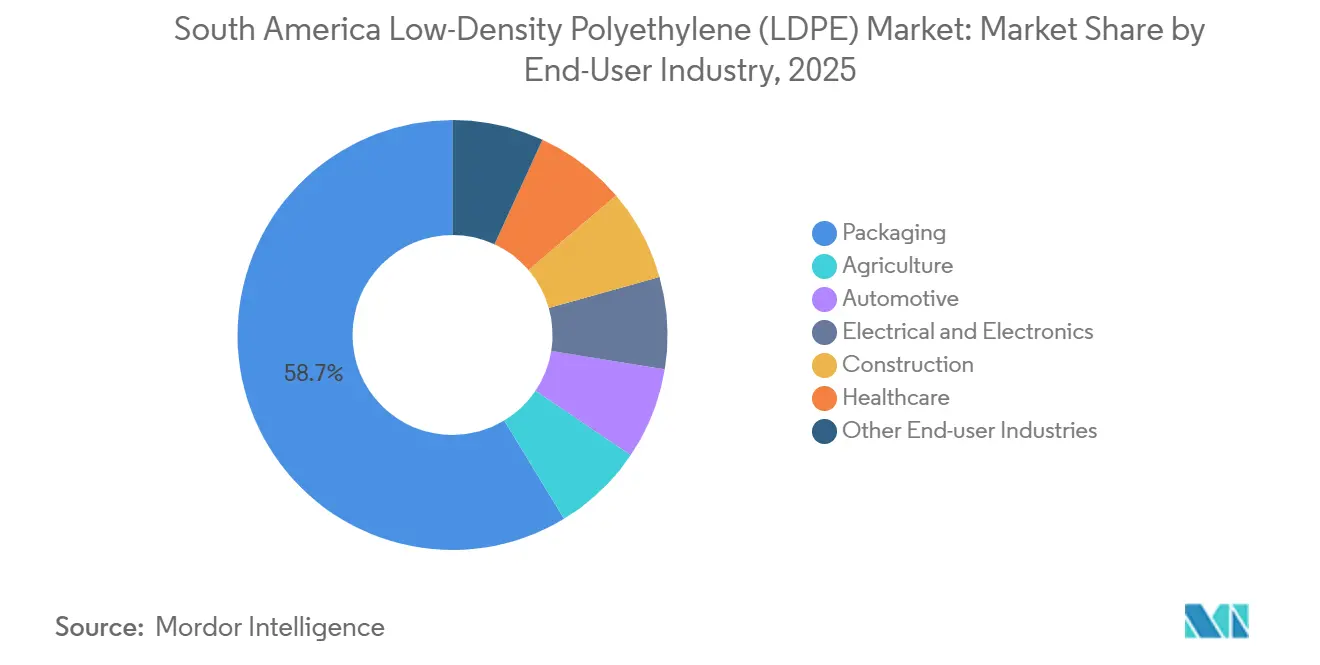

- By end-user industry, packaging held 58.68% of the South America Low-Density Polyethylene (LDPE) market share in 2025, while healthcare is projected to advance at a 4.16% CAGR through 2031.

- By geography, Brazil accounted for 57.05% of the South America Low-Density Polyethylene (LDPE) market share in 2025 and is forecast to grow at a 3.59% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

South America Low-Density Polyethylene (LDPE) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Implementation of government incentives for lightweight plastic adoption in automotive | +0.6% | Brazil, with spillover to Argentina automotive clusters | Medium term (2-4 years) |

| Expansion of flexible-packaging converters in Brazil | +0.8% | Brazil core, secondary gains in Colombia and Chile | Short term (≤ 2 years) |

| Infrastructure upgrades opening new pipe-coating demand corridors | +0.4% | Brazil offshore oil fields, Argentina pipeline networks | Long term (≥ 4 years) |

| E-commerce boom accelerating stretch-film consumption | +0.7% | Brazil and Argentina urban centers, expanding to Peru and Colombia | Short term (≤ 2 years) |

| Bio-LDPE capacity build-out at Braskem's Triunfo complex | +0.5% | Brazil production hub, export reach across South America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Implementation of Government Incentives for Lightweight Plastic Adoption in Automotive

Brazil’s Programa Mover injects BRL 3.5-4.1 billion each year into technologies that cut vehicle weight, mandating recyclability thresholds and differentiated taxation for compliant models[1]Government of Brazil, “Lei 14.902/2023 – Programa Mover,” planalto.gov.br . Automakers are substituting metal and glass with LDPE-based interior films, reducing curb weight by 5%-8% and improving fuel economy by as much as 5%. RadiciGroup’s 17,000 m² plant opened in March 2025 to localize polymer-compound supply for tier-one suppliers. Argentine original equipment manufacturer (OEM) platforms are preparing to align with comparable standards by 2027, extending demand beyond Brazil. The 2-to-4-year horizon reflects vehicle-platform redesign cycles and validation protocols.

Expansion of Flexible-Packaging Converters in Brazil

Brazilian converters are installing high-output lines to preempt demand from rapid e-commerce and food-delivery growth. Bomplastic’s Comexi F2 MB press contributes 350 tons per month of high-barrier film, while COEXPAN-EMSUR’s Jundiaí plant went on-stream in 2024, strengthening supply in the southeast corridor. Oben Group’s purchase of Vitopel intensifies contest for sealant-layer business by adding a strong BOPP portfolio. Sheets and films already claim nearly half of South American LDPE volume, and rapid line ramp-ups usually reach nameplate in 12-18 months, underscoring the short-term boost to the South America Low-Density Polyethylene (LDPE) market.

Infrastructure Upgrades Opening New Pipe-Coating Demand Corridors

Offshore field development and pipeline rehabilitation are enlarging demand for LDPE-based adhesive primers. Tenaris won a 102 km pipe order for Petrobras’s Búzios 9 project, Mattr secured more than USD 50 million in coating work at its Serra plant, and Mattr logged South American awards surpassing USD 80 million. Although polypropylene dominates three-layer systems, cumulative LDPE use in adhesive layers could reach 20,000 tons per year by 2030. Project permitting and ISO 21809 qualification extend the payoff to the long-term window.

E-Commerce Boom Accelerating Stretch-Film Consumption

Digital retail penetration continues to soar. Brazil’s January 2025 polyethylene exports totaled USD 40.05 million, up 3.69% year on year, a sign that local demand is siphoning off export volume. Stretch-film now represents about 13% of South American LDPE usage, and automated pallet-wrappers in new logistics centers increase film throughput by roughly 25% per site. Fulfillment-center construction in Buenos Aires and Rosario is closing the gap with Brazil, preserving double-digit growth in near-term consumption of LDPE film grades.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Substitution by LLDPE and emerging biodegradable films | -0.5% | Brazil and Argentina packaging sectors, with early adoption in Chile | Medium term (2-4 years) |

| Feedstock (ethylene) price volatility linked to regional naphtha differentials | -0.3% | Argentina import-dependent markets, Brazil cracker-integrated producers | Short term (≤ 2 years) |

| PCR-content limits above 20% degrading mechanical properties | -0.2% | Brazil recycling hubs, Argentina urban collection networks | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Substitution by LLDPE and Emerging Biodegradable Films

Film processors prefer Linear Low-Density Polyethylene (LLDPE) for puncture resistance and downgauging; automated pallet-wrappers in Brazil’s warehouses have already cut LDPE usage in stretch-hood films by about 15%. Biodegradable polylactic acid (PLA) and polyhydroxyalkanoate (PHA) structures are gaining traction in premium single-use food packaging, especially in Chilean retail pilots, but high resin premiums and scarce composting infrastructure keep volumes marginal. Converter re-tooling typically takes two years, explaining the medium-term drag on the South America Low-Density Polyethylene (LDPE) market.

Feedstock (Ethylene) Price Volatility Linked to Regional Naphtha Differentials

Argentina’s ethylene hit USD 610 per ton in Q3 2025 after an 11.34% quarterly surge, and September alone brought a 12.48% jump, forcing small extruders to idle lines. Brazil looked cushioned by domestic naphtha that fell 20.5% year on year, yet ethylene–naphtha spreads shrank to USD 105 per ton in Q1 2026, pressuring even integrated players. Such cost swings are transmitted to LDPE prices within weeks, classifying the restraint as short term.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Sheets and Films Widen Their Lead

Sheets and films captured 48.37% of regional LDPE volume in 2025 and are forecast to rise at a 3.46% CAGR through 2031. Bomplastic’s 350 tons per month line and COEXPAN-EMSUR’s ramp-up feed Brazil’s southeast, where fulfillment centers dictate demand for high-clarity overwraps. Agricultural mulch films in Brazil’s Cerrado and Argentina’s Pampas also contribute to the South America Low-Density Polyethylene (LDPE) market size for this segment. Blow-molded bottles trail because brand owners shift squeezable formats to (High-Density Polyethylene) for cost reasons, while collapsible cosmetic tubes keep a foothold for LDPE’s flexibility and soft-touch feel.

Oben Group’s Vitopel takeover escalates competition as Biaxially Oriented Polypropylene (BOPP) producers pursue LDPE sealant layers given the latter’s unmatched hot-tack range. Injection-molding grades, only 7% of demand, face polypropylene substitution amid end-user cost discipline, but still thrive in premium closures that need secure tamper evidence. Extrusion-coating remains steady in liquid cartons, though Polyethylene Terephthalate (PET)-based laminates grow in shelf-stable dairy. Together these dynamics keep the South America Low-Density Polyethylene (LDPE) market share for sheets and films firmly ahead through 2031.

By End-User Industry: Packaging Dominates, Healthcare Accelerates

Packaging absorbed 58.68% of regional volume in 2025 thanks to LDPE’s sealability and moisture barrier, sustaining its dominance in flexible snacks and stand-up pouches. Healthcare, however, is set to grow fastest at a 4.16% CAGR through 2031 as hospitals adopt single-use sterile wraps under stricter infection-control codes. Device makers also prefer LDPE’s clarity for blister and intravenous (IV)-bag windows that must pass ISO 10993 cytotoxicity tests. Agriculture benefits from rising greenhouse acreage in Peru’s coastal valleys and precision farming in Argentina, lifting film usage per hectare despite feedstock cost pressure.

Automotive applications now represent moderate volume of the South America Low-Density Polyethylene (LDPE) market size, buoyed by Programa Mover’s lightweighting incentives that encourage LDPE dash insulators and protective covers. Electrical cable-jacketing demand tracks regional grid expansions, as aluminum takes up larger share of conductor builds. Construction uses, vapor barriers, damp-proof sheets are an inch ahead with housing refurbishments in Colombia. RadiciGroup’s capacity expansion in São Paulo anchors multi-industry supply chains that demand consistent resin quality and technical service.

Geography Analysis

Brazil commanded 57.05% of LDPE volume in 2025 and is projected to enlarge tonnage at 3.59% through 2031, sustained by Braskem’s Rio de Janeiro expansion that adds 220,000 tons per year of new capacity. Domestic production already crowds out imports; Q1 2025 volumes fell 20.3% year on year to 459,173 tons. The anti-dumping case against North American resin could further insulate local producers and uphold margins, though converters lacking specialty grades worry about cost pass-through.

Argentina remains volume runner-up but wrestles with feedstock volatility and currency depreciation. Ethylene spiked to USD 610 per ton in Q3 2025, compelling small extruders to cut shifts. Dow’s pact with Reciclar for 6,500 tons per year of post-consumer resin illustrates multinationals’ dual focus on cost containment and circular branding. Colombia, Chile, and Peru together account for a lower share of the South America Low-Density Polyethylene (LDPE) market; Colombia’s urban packaging needs are growing, while Chile’s mining liners track copper-price cycles.

The remaining markets, such as Uruguay, Paraguay, Bolivia, Ecuador, Venezuela are hampered by infrastructure gaps and political risk. Nevertheless, Paraguay’s rising soy-film cultivation hints at incremental volume that could modestly raise sub-regional tonnage by the decade’s end. Across the continent, rising logistics sophistication and automotive shifts keep Brazil at the epicenter of the South America Low-Density Polyethylene (LDPE) market.

Competitive Landscape

The South America low-density polyethylene (LDPE) market is highly concentrated, with the five largest firms being Braskem SA, Dow, LyondellBasell Industries Holdings B.V., SABIC, and Exxon Mobil Corporation. Dow, LyondellBasell, SABIC, and the soon-to-merge Borealis-Borouge-Nova group compete largely on specialty formulations and global trade flows. LyondellBasell’s Americas capacity, including a 200 kilo tons stake in a Louisiana joint venture, grants flexibility to swing tonnage between hemispheres as arbitrage opens[2]LyondellBasell, “Form 10-K 2023,” lyondellbasell.com. The Borealis-Borouge-Nova union, which finalized in March 2026, has injected fresh imported supply as Borouge 4's 1.4 Mt pa unit ramps, potentially softening spot prices in Brazil’s southeast.

Circular-economy alliances are multiplying. Dow’s memorandum with Ambipar aims for 2,000–60,000 tons per year of recycling capacity by 2030. ALPLA took a stake in Clean Bottle to secure 150,000 tons per year of rHDPE, a move that indirectly challenges LDPE recyclers by funneling collection streams toward HDPE. Local converters such as Bomplastic and COEXPAN-EMSUR are scaling film capacity faster than demand; if spreads tighten further, backward integration into resin could surface as a strategic hedge.

Technological raceways revolve around chemical recycling. Capital outlays of USD 50–100 million for a 30,000 tons per year unit deter newcomers, but Braskem’s July 2025 commercial sale to Copobras demonstrates first-mover momentum. Policy too shapes rivalry: if Brazil levies tariffs on North American PE, Braskem stands to tighten its grip, whereas specialty-grade importers could face supply bottlenecks. Combined, these currents render the South America Low-Density Polyethylene (LDPE) market a battleground where integration, sustainability credentials, and trade policy set the rules.

South America Low-Density Polyethylene (LDPE) Industry Leaders

Braskem SA

Dow

LyondellBasell Industries Holdings B.V.

SABIC

Exxon Mobil Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Braskem SA reached a notable milestone in the circular economy by completing South America's first commercial sale of circular polyethylene (PE) produced through chemical recycling to the Copobras Group. The circular Low-Density Polyethylene (LDPE) was used by Copobras to manufacture flexible packaging, particularly for the pet food segment.

- January 2025: ALPLA Group announced the acquisition of a majority stake in Clean Bottle, a Brazilian high-density polyethylene (HDPE) recycler. This move is expected to influence the low-density polyethylene (LDPE) market by enhancing the regional recycling network and promoting sustainable practices in South America.

South America Low-Density Polyethylene (LDPE) Market Report Scope

Low-density polyethylene (LDPE) is a flexible, durable, and transparent thermoplastic characterized by its highly branched molecular structure and low density (0.910–0.940 g/cm³). Manufactured through high-pressure polymerization, it is commonly utilized in plastic films, grocery bags, squeezable bottles, and food packaging due to its strong moisture resistance and chemical stability.

The South America Low-Density Polyethylene (LDPE) Market is segmented into product type, end-user industry, and geography. By product type, the market is segmented into sheets and films, blow-molded, injection-molded, extrusion coating, and other product types. By end-user industry, the market is segmented into packaging, agriculture, automotive, electrical and electronics, construction, healthcare, and other end-user industries. By geography, the market is segmented into Brazil, Argentina, Colombia, Chile, Peru, and rest of South America. For each segment, the market sizing and forecasts have been done on the basis of volume (tons).

| Sheets and Films |

| Blow-Molded |

| Injection-Molded |

| Extrusion Coating |

| Other Product Types |

| Packaging |

| Agriculture |

| Automotive |

| Electrical and Electronics |

| Construction |

| Healthcare |

| Other End-user Industries |

| Brazil |

| Argentina |

| Colombia |

| Chile |

| Peru |

| Rest of South America |

| By Product Type | Sheets and Films |

| Blow-Molded | |

| Injection-Molded | |

| Extrusion Coating | |

| Other Product Types | |

| By End-user Industry | Packaging |

| Agriculture | |

| Automotive | |

| Electrical and Electronics | |

| Construction | |

| Healthcare | |

| Other End-user Industries | |

| By Geography | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America |

Key Questions Answered in the Report

What is the size of the South America low-density polyethylene (LDPE) market?

The South America low-density polyethylene (LDPE) market stands at 1.42 million tons in 2026 and is expected to reach 1.67 million tons by 2031.

Which product type commands the biggest share in 2025?

Sheets and films led with 48.37% of the South America Low-Density Polyethylene (LDPE) market share in 2025.

Which end-user industry is expanding fastest through 2031?

Healthcare is projected to grow at a 4.16% CAGR through 2031.

Why is Brazil central to regional LDPE supply?

Brazil hosts integrated cracker capacity, holds 57.05% of volume in 2025, and is adding 220,000 tons per year of new output by 2028 through Braskem’s Rio de Janeiro project.

Page last updated on: