South America Laundry Appliances Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

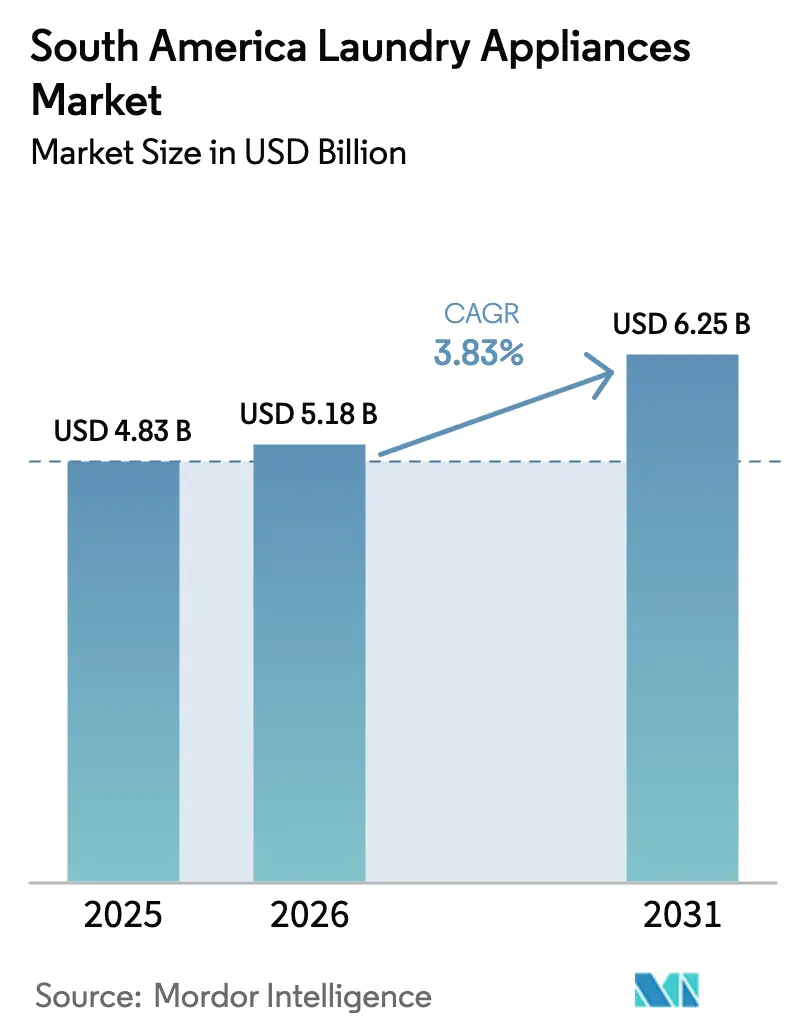

| Base Year Market Size (2025) | USD 4.83 Billion |

| Market Size (2026) | USD 5.18 Billion |

| Market Size (2031) | USD 6.25 Billion |

| Growth Rate (2026 - 2031) | 3.83% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South America Laundry Appliances Market Analysis by Mordor Intelligence

The South America laundry appliances market size reached USD 4.83 billion in 2025, is forecast at USD 5.18 billion in 2026, and is projected to reach USD 6.25 billion by 2031, reflecting a 3.83% CAGR during 2026–2031. The spending shift to embedded financing and instant payments moves browsing into purchases, which is most visible in Brazil, where PIX and retailer BNPL options compress checkout friction and expand approval rates for households with thin credit files. Argentina’s sharp unit upswing in 2025 came from import liberalization and tariff swings that deflated retail prices in dollar terms, which undermined local production economics and forced closures even as volumes rose. Chile pairs high per-capita e-commerce use with rapid 5G adoption and real-time payments to lift conversion and support cross-border buying behavior that exploits retail price gaps in neighboring markets. Peru’s strong import flows in 2025 point to opportunistic restocking as the exchange rate reduced landed costs and incentivized earlier orders ahead of expected 2026 policy reviews [1]Banco Central do Brasil, “PIX Statistics Dashboard,” Banco Central do Brasil, bcb.gov.br.

Key Report Takeaways

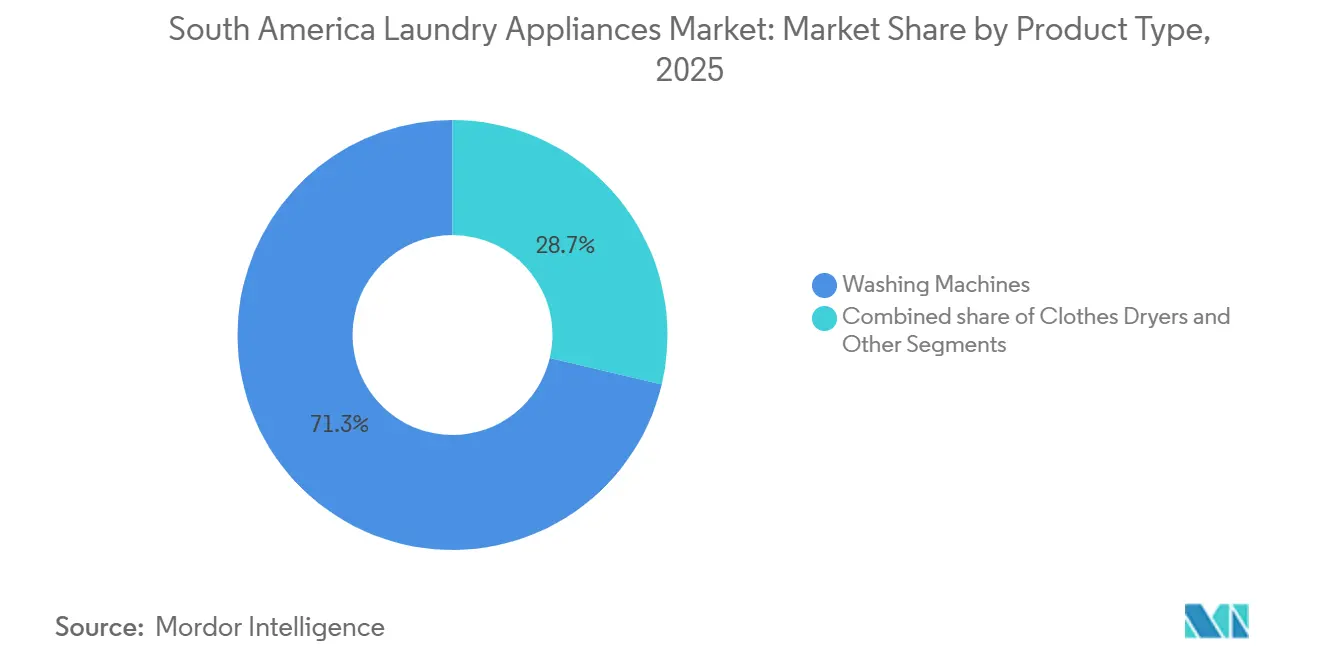

- By product type, washing machines led with 71.34% of the South America laundry appliances market share in 2025, and clothes dryers are forecast to expand at a 5.00% CAGR through 2031.

- By technology, fully automatic models held 65.12% of the South America laundry appliances market share in 2025, while semi-automatic models are projected to grow at a 5.50% CAGR through 2031.

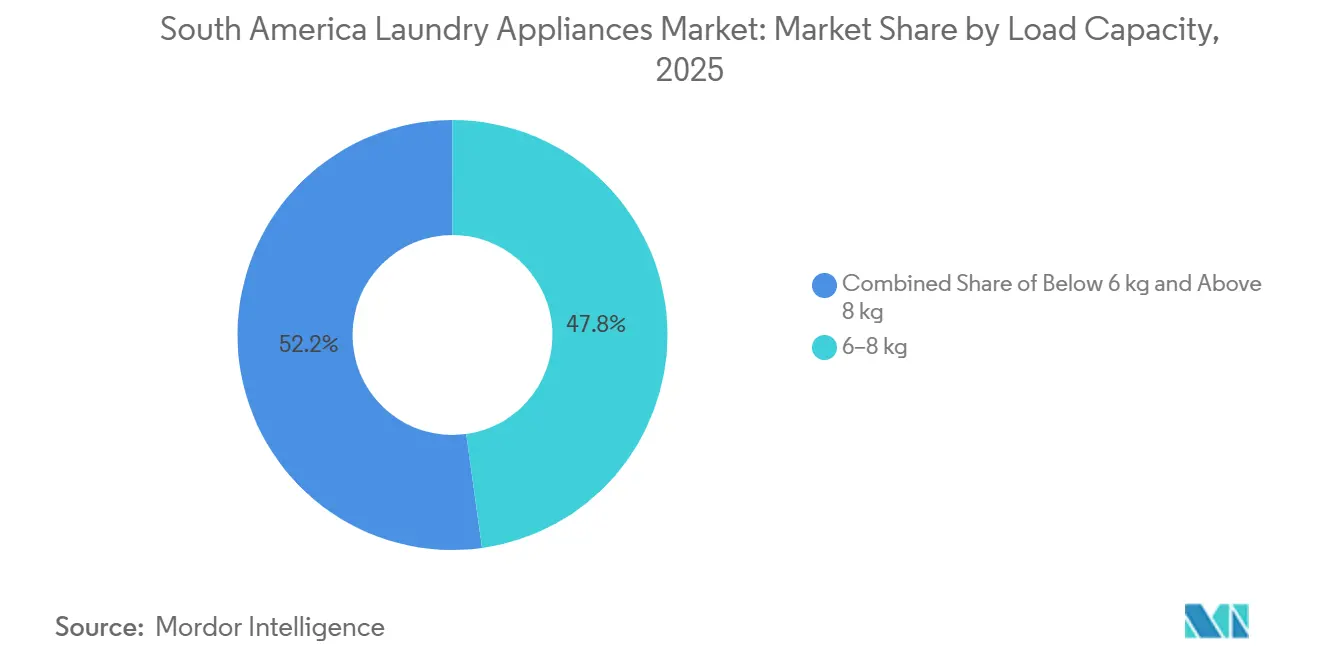

- By load capacity, 6–8 kg captured 47.81% of the South America laundry appliances market share in 2025, and above-8-kg units are projected to expand at a 5.20% CAGR through 2031.

- By distribution channel, multi-brand stores accounted for 48.92% of the South America laundry appliances market share in 2025, and online channels are projected to grow at a 7.00% CAGR through 2031.

- By geography, Brazil held 45.72% of the South America laundry appliances market share in 2025, and Chile is forecast to grow at a 5.50% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

South America Laundry Appliances Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Urban housing build-out and social housing programs are accelerating appliance purchases | +0.9% | Brazil, Chile, Colombia | Medium term (2-4 years) |

| Rising washing-machine ownership with headroom in underserved regions and Andean markets | +0.7% | Peru, Bolivia, Paraguay, Northeast Brazil, Colombian interior | Long term (≥ 4 years) |

| E-commerce scale and omnichannel financing are unlocking major domestic appliance purchases | +1.2% | Brazil, Chile, Argentina | Short term (≤ 2 years) |

| Energy efficiency and safety regulations are catalyzing replacement cycles and premiumization | +0.8% | Brazil, Chile, Colombia | Medium term (2-4 years) |

| Reverse logistics/EPR systems enabling trade-in promotions and take-back at scale | +0.3% | Chile, São Paulo state, and early pilots in Colombia | Long term (≥ 4 years) |

| Energy and water stress tilting demand to inverter washers and heat-pump dryers | +0.5% | Northeast Brazil, Santiago or Valparaíso, Buenos Aires, rationing zones | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Urban Housing Build-Out and Social Housing Programs Accelerating Appliance Purchases

Housing programs are translating handovers into immediate laundry-appliance purchases, which shortens the consideration cycle and advances demand from future periods into the present. In Brazil, the reinstated Minha Casa Minha Vida delivered 117,000 units during H1 2025, and each handover has been associated with financed appliance baskets in the USD 505.8 (BRL 2,800) range, which retailers attach to mortgages and social housing subsidies to increase conversion. In Chile, ministry-backed subsidies support first-time buyers who include front-load washers within renovation or move-in financing, and large chains coordinate zero-interest installments at the point of sale to close the loop. In Colombia, social-interest projects layer in water-connection incentives that strengthen the household case for an automatic washer rather than laundromat usage, which lifts penetration in secondary cities. The coupling of grid and water access upgrades with retail branch openings has increased stock pre-positioning around new housing clusters, which compresses delivery from weeks to days and improves sell-through of compliant models as labeling rules push buyers to formal channels [2]Midea Group, “Brazil Factory Investment and Commissioning,” Midea, midea.com.

Rising Washing-Machine Ownership with Headroom in Underserved Regions and Andean Markets

Penetration gaps across Peru’s interior and Bolivia’s urban cores leave large volumes untapped, and this gap remains despite falling entry prices due to import competition. Northeast Brazil also trails coastal metros on saturation, although targeted transfers and infrastructure investments are closing the distance and expanding the base for the South America laundry appliances market. If lagging regions close even part of the penetration gap by 2031, annual unit demand would skew to entry-tier machines that favor mechanical simplicity and low service costs. Logistics and last-mile costs constrain coverage in remote municipalities, which is why platforms have tested hub-and-spoke aggregation models to bring down per-order shipping costs and serve towns above specific population thresholds. Paraguay’s sales mix shows the persistence of semi-automatic models where water pressure and voltage instability still pose barriers for fully automatic machines, which underscores how utility reliability shapes purchase choices in the South America laundry appliances market.

E-Commerce Scale and Omnichannel Financing Unlocking Major Domestic Appliance Purchases

Brazil’s PIX system processed heavy volumes in 2024 and shifted online tender shares toward instant payments, which reduces merchant fees and enables cash discounts or BNPL plans that open access for informal workers. Major retailers now embed 24-to-60-month installments into checkout without traditional credit scoring by using transaction histories, and this has expanded approvals for high-ticket appliances in the South America laundry appliances market. Chile’s WebPay and leading digital wallets provide similar low-friction flows along with high mobile purchase rates that support one-tap checkouts. In Argentina, marketplace credit bundles zero-interest installments funded by OEMs during key events, which helps move inventory even during volatile macro windows. Omnichannel flows, such as buying online and picking up in store, create a handoff that builds trust for big-ticket purchases, and this reduces abandonment while boosting conversion for laundry appliances in the South America laundry appliances market.

Energy-Efficiency and Safety Regulations Catalyzing Replacement Cycles and Premiumization

Brazil’s INMETRO updated energy rules for refrigerators in April 2025 and signaled forthcoming washer updates that will tighten consumption thresholds for the category, which accelerates inverter adoption and shortens product cycles ahead of compliance deadlines. Chile’s Ministry of Energy and the SEC have advanced phased efficiency indices and safety protocols that require recertification and drive stock rotation toward conforming models through 2026 and beyond. Colombia’s draft update to RETIQ extends labels and testing to more appliances, adds third-party lab obligations, and raises per-SKU certification costs, which lifts hurdles for gray-market imports and focuses buyers on established brands. These measures enable replacement pitches that highlight lower electricity use and lifetime cost savings, which support premiumization where inverter models carry higher prices but deliver faster paybacks in high-tariff zones. Utility-backed labeling programs and municipal subsidies in Brazil also support swap-out campaigns that move aging stock into reverse-logistics loops while aligning with energy policy goals in the South America laundry appliances market [3]Banco Central do Brasil, “PIX Adoption and Transaction Volumes,” Banco Central do Brasil, bcb.gov.br.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Tariff volatility, anti-dumping actions, and CET exceptions are elevating costs and assortment risk | -0.6% | Argentina, Mercosur CET debates, Brazil, selective tariffs | Short term (≤ 2 years) |

| Cultural preference for line-drying and very low dryer penetration suppresses adoption | -0.4% | All markets, especially Argentina, rural Brazil, and Andean cities | Long term (≥ 4 years) |

| Compliance load from Inmetro 148/2022 recertification and evolving labeling/testing | -0.3% | Brazil, Chile, Colombia | Medium term (2-4 years) |

| Intra-Mercosur customs complexities and logistics raise delivered costs for bulky goods | -0.2% | Paraguay–Brazil crossings, Argentina–Chile transits, Uruguay transshipment | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Tariff Volatility, Anti-Dumping Actions, and CET Exceptions Elevating Costs and Assortment Risk

Argentina’s Decree 513/2025 raised tariffs on many washing machines below a capacity threshold and introduced a cumulative duty burden that reshaped price ladders and spurred cross-border purchases through personal-use channels. The mid-year change stranded inventory and forced re-export or loss-taking in some cases, which reduced assortment depth and delayed new-model introductions for the South America laundry appliances market. Mercosur’s CET framework still allows many exceptions and domestic adjustments, and the mix of unilateral tariff moves and defensive petitions raises sourcing risk and margin volatility. Duty policy, exchange swings, and interstate tax interpretations have flipped planned margins into losses for some retailers, which has fueled a more conservative approach to SKU commitments for seasonal events. Manufacturers have also disclosed tax and legacy regime contingencies that weigh on investment planning, which further raises the hurdle for local expansions while duty regimes remain fluid.

Cultural Preference for Line-Drying and Very Low Dryer Penetration Suppresses Adoption

Dryer ownership remains low across the region and is often concentrated in urban high-rise districts, which limits the ceiling for the category even when incomes rise. Many households prefer line-drying for perceived fabric care and to avoid electricity charges on non-essential cycles, which suppresses everyday dryer use. Chile has seen higher growth in dryers when smog alerts and condominium rules limit outdoor drying, yet owners still revert to line-drying when weather permits. Premium heat-pump dryers offer strong efficiency but carry price points that push paybacks far out of reach when compared with free sun-drying, which narrows their appeal to early adopters. Brands are using combined washer-dryer formats and premium narratives to nudge trial, yet usage data shows dryer functions are often used sparingly, which keeps the dryer portion of the South America laundry appliances market in a subscale posture.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Washing Machines Anchor Volume; Dryers Trail Despite Efficiency Gains

Washing machines accounted for 71.34% of the 2025 value, which equates to USD 3.64 billion within the South America laundry appliances market, while dryer volumes remained far smaller, even as the dryer segment is projected to grow at a 5.00% CAGR through 2031. In Brazil, shorter replacement cycles reflect stock rotations around new labeling rules and active trade-in programs that move households into inverter models with better energy profiles. Chile’s pollution alerts and urban construction codes raised the practical need for dryers in certain districts, but this remains a city-specific effect rather than a nationwide shift. Argentina’s preference for washer-dryer combos aligns with space constraints and price parity, yet field-use data suggests the dryer function is used only occasionally as insurance during wet weather. Small laundry devices such as irons and garment steamers represent a modest slice of value and are driven more by impulse placement and promotions than by durable replacement cycles.

The manufacturing footprint follows the volume reality, since washers justify localized assembly and automation investments while dryer lines remain import-based and carry longer lead times for promotional windows. Midea’s Pouso Alegre site came online in December 2024 and supports fast lead times for refrigerators and washing machines, which improve flexibility during high-demand events. Whirlpool disclosed significant automation capex to improve throughput and stabilize costs, and LG announced a large Paraná investment for 2026 to cut reliance on imports. These moves position major OEMs to navigate labeling changes, tariff variability, and promotions with shorter cycles from factory to store. The trajectory keeps washers at the center of scale strategies in the South America laundry appliances market, while dryers build from a smaller base [4]Ministerio de Energía, “Chile Energy Efficiency Law Implementation,” Gobierno de Chile, minenergia.gob.cl.

By Technology: Fully Automatic Dominant, But Semi-Automatic Grows Faster in Grid-Constrained Zones

Fully automatic models held 65.12% of the 2025 value, while semi-automatic units are expected to grow at a 5.50% CAGR and outpace automatics as utility instability shapes preferences in certain subregions. The semi-automatic segment benefits from resilience to voltage dips and water pressure swings, along with lower upfront prices and easier field repairs. Northeast Brazil and parts of Andean markets still record a strong semi-automatic mix, while large metros skew to fully automatic models with higher inverter penetration and longer motor warranties. Labeling rules and impending washer-efficiency updates are set to support inverter adoption in automatics, since they deliver faster paybacks where electricity tariffs remain high. This split implies parallel supply and service models that keep semi-automatic products in the portfolio while fully automatic lines anchor replacement and premiumization in the South America laundry appliances market.

Manufacturers support inverter sales with extended motor guarantees and reliability messages, which reduce service-call costs and increase buyer confidence. Grid constraints and underdeveloped technician networks in interior cities preserve the rationale for manual or twin-tub designs and sustain demand for gravity-fed cycles. Draft RETIQ extensions in Colombia draw sharper lines between labeled automatics and exempt semi-automatics, which could indirectly lock low-income cohorts into less efficient formats unless targeted subsidies close the gap. OEMs balance tooling and logistics by pairing regional assembly for automatics with import flows for semi-automatics from high-volume Asian lines. This dual-track posture supports coverage breadth while aligning with compliance in the South America laundry appliances market.

By Load Capacity: 6–8 kg Leads, but Above-8-kg Surges on Pet-Ownership and Bedding Cycles

The 6–8 kg band held 47.81% of the 2025 value and aligns with the median household size, while above-8-kg machines are projected to grow at a 5.20% CAGR due to a cycle breadth that accommodates bedding and pet-hair removal in fewer loads. Below-6-kg models lose share because households consolidate loads to improve energy-per-wash efficiency, and space-constrained dwellings still find 6 kg units more practical than smaller units that require more cycles. Doorway and counter-height constraints in social housing limit drum sizes for certain front-loaders, which caps capacity in many flats without requiring chassis design changes. Delivery surcharges for larger units also shape purchase decisions, especially outside metro cores, where two-person delivery is required for stairs and tight turns. Shared laundry rooms in new Chilean condominium towers also shift some replacement to property managers that buy on lifecycle economics rather than household aesthetics.

Pet-focused cycles and bundled hygiene features are now part of capacity-led upsizing in Brazil and Chile, supported by premium launches that pack large drums into compact widths. Washer-dryer combo ratios remain constrained by heat-exchanger sizing, which keeps dry capacities below wash capacities in most designs. Brands note a stated preference for larger dryer capacities, yet thermal limits in ventless systems require bigger condensers that raise retail prices past thresholds. These engineering trade-offs slow further growth in the combo segment even as households welcome the optionality when weather or building rules restrict outdoor drying. Capacity decisions will keep trending to larger wash volumes as apartments shrink and buyers seek to finish bulky items in fewer cycles within the South America laundry appliances market.

By Distribution Channel: Multi-Brand Stores Retain Edge, but Online Sprints at 7% CAGR

Multi-brand stores accounted for 48.92% of value in 2025 and keep the edge with display density, same-week delivery, and financing bundles that simplify checkout for first-time buyers. Exclusive brand outlets hold a smaller share and focus on white-glove service and loyalty benefits in premium districts where ASPs are higher, and service expectations justify premium pricing. Online channels are projected to grow at a 7.00% CAGR, which reflects marketplace traffic scale and the lift from instant payments and embedded credit that reduce abandonment and unlock approvals for thin-file shoppers. Marketplace BNPL has extended credit to millions of new users, while retailer fintech units have added 60-month terms for up to USD 632.2 (BRL 3,500) limits, which expands access for informal income segments. Offline and online now operate as a single path, since inventory is cross-allocated for store pickup and next-day city delivery through shared fulfillment nodes that raise conversion for the South America laundry appliances market.

Rural and remote zones still rely on local multi-brand floors for tactile evaluation and store-managed delivery that reduces damage and return risks. Hypermarkets have moved space to faster sellers outside of major appliances as sales turn lag small appliances and packaged goods. Retail media and cross-sell engines in major chains have raised basket size online through subscription add-ons for detergent and warranty bundles at the point of sale. Omnichannel fulfillment suites run by retailers now support third-party sellers in Chile and Brazil and bring next-day reach to most households in core corridors. These distribution plays will keep share fluid between store and marketplace in the South America laundry appliances market as payments and logistics continue to converge.

Geography Analysis

Brazil held 45.72% of 2025 revenue, and strong PIX adoption reduces checkout friction for online appliance purchases while embedded BNPL opens access to high-ticket items for thin-file households. Local manufacturing expansions have increased output and shortened retailer lead times, which supports promotional agility during key retail events. Automation investments at existing lines and a new announced plant for 2026 seek to reduce import exposure and stabilize costs against exchange-rate swings and tariff windows. The Northeast is forecast to grow faster than the Southeast as transfers and grid upgrades lift reliability and open the path to more fully automatic purchases. These trends reinforce Brazil’s anchor role in the South America laundry appliances market even as growth differentials narrow across subregions.

Argentina recorded 23%-unit growth in 2025, but margin compression and plant closures showed the strain on local producers, which face volatile policy and cross-border arbitrage through personal-use exemptions. A decree in July 2025 imposed a combined 55% burden on many washers below a capacity cutoff, which incentivized shopping trips to Chile, where retail prices remained far lower in dollar terms. The country’s largest local brand kept its share through vertical integration in Córdoba and in-house dryer and semi-automatic production, although export scalability stayed limited. Chile is forecast to grow at a 5.50% CAGR and shows the region’s highest per-capita e-commerce use, where 5G expansion and high mobile checkout shares lift conversion and reduce returns through AR fit tools. Dryer sales spikes tied to smog alerts and energy-efficiency targets have accelerated replacement cycles in pilot municipalities with subsidies that reward A-class purchases.

Colombia and Peru account for 22% combined and show distinct policy vectors that affect compliance costs and channel allocation. Colombia’s draft RETIQ update extends labeling and testing burdens and underscores the competitive benefit of certification for established brands with service networks. Peru’s durable-goods import surge through November 2025 tracked an exchange-rate tailwind that cut landed costs and allowed earlier restocking before potential 2026 changes. Smaller markets such as Paraguay and Uruguay present contrasting demand mixes, where water and grid constraints keep semi-automatics relevant and harmonized labeling rules improve intra-bloc flows. These national trajectories collectively shape the demand distribution within the South America laundry appliances market and affect how OEMs pace launches, manage stock, and set channel targets.

Competitive Landscape

The region’s structure resembles an oligopoly around global brands with strong local presence, while regional challengers and Chinese entrants press on entry tiers with price gaps sustained by sourcing advantages. Whirlpool reported USD 2.33 billion (BRL 12.9 billion) in 2024 Brazil revenue and invested USD 99.3 million (BRL 550 million) to automate São Paulo and Santa Catarina production, which raised throughput and shortened cycles for promotional periods. Electrolux improved operating margins in South America in late 2025 on cost takeout and supplier rebates, even as pricing pressure intensified in entry segments. Midea inaugurated its Pouso Alegre facility in December 2024, a USD 113.8 million (BRL 630 million) investment with an annual capacity of 1.3 million refrigerators and washing machines and sub-10-day lead times to retailers. LG announced a USD 0.27 billion (BRL 1.5 billion) Paraná plant planned for 2026, which aims to cut import dependency from 90% to 30% and hedge against foreign exchange volatility in the South America laundry appliances market.

Brands compete on manufacturing proximity, portfolio breadth, and embedded financing, and they use localized assembly to buffer tariffs and shorten promotion lead times. Mabe holds 50% of Argentina’s automatic-washer segment through the Drean portfolio and two Córdoba factories that cover washers and dryers, providing a moat when duty policy changes quickly. Financing integration is now a front-line lever, with retailer fintech arms authorized by the central bank to extend 60-month terms at checkout without traditional scoring and with marketplace wallets onboarding millions of new borrowers. Heat-pump dryer and AI-enabled washer launches secure premium price points and support higher gross margins where buyers accept the lifetime savings narrative. Certification regimes give incumbents an advantage because they maintain regulatory teams and accredited lab partnerships that gray-market resellers cannot match in the South America laundry appliances market.

Chinese brands leverage large export lines to undercut entry segments even after tariffs in specific countries, which pushes incumbents to defend with warranty length, service network density, and localized features. Premium differentiation centers on energy savings, smart cycles, and fabric care, while the mass tier consolidates around brand trust and checkout financing. Retail and OEM co-development is increasing in bundles that pair appliances, consumables, and warranties to raise lifetime value and smooth demand across quarters. Reverse logistics and EPR programs expand certified refurbishment streams that may recapture value that was previously lost to informal resellers. These competitive moves keep the top five’s share strong while allowing share shifts at the edges of the South America laundry appliances market.

South America Laundry Appliances Industry Leaders

Whirlpool Corporation

Electrolux Group

LG Electronics

Samsung Electronics

Midea Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Grupo FROTH, parent of 5àsec and LavPop in Brazil, reported 2025 revenue growth of 15.72% and a 370% revenue increase at LavPop with 44 new units opened, crossing 100 stores and targeting a network doubling in 2026 with a revenue goal of USD 57.8 million (BRL 320 million), highlighting the rise of autonomous laundry formats in dense corridors.

- December 2025: Brazil’s Lavtech trade fair reported USD 0.63 billion (BRL 3.5 billion) in generated business, with a new Maytag stack model securing over USD 1.8 million (BRL 10 million) in pre-launch orders and Oasis Laundry confirming entry to Brazil, signaling tighter links between commercial and premium residential technology.

- June 2025: Midea announced additional investments in Minas Gerais for factories and a logistics center to extend the benefits of its December 2024 plant and speed local product expansion.

- May 2025: Magazine Luiza said its fintech subsidiary Magalu Pay IF, approved by the central bank, offers 60-month BNPL terms without traditional scores by underwriting from transaction histories and limits of up to USD 632.2 (BRL 3,500).

South America Laundry Appliances Market Report Scope

Laundry Appliances refer to the machinery used to clean and maintain laundry in residential or commercial settings. Watching machines, Dryers, Irons, and others exist among the major used laundry appliances, with technological advancements equipping them with different models and features as required by users.

The study provides a brief overview of the South American laundry appliance market and details on sales, manufacturers' investments, and technological innovation. The South American laundry appliance market is segmented by product type, technology, load capacity, distribution channel, and region. By product type, the market is segmented into washing machines, clothes dryers, and others (Garment Steamers, Electric Irons, Laundry Dehumidifiers). By product, the market is segmented into washing machines, dryers, electric smoothing irons, and others. By technology, the market is segmented into fully automatic, semi-automatic/manual. By load capacity, the market is segmented into below 6 kg, 6-8 kg, and above 8 kg. By distribution channel, the market is segmented into multi-brand Stores, exclusive brand outlets, online, and other distribution channels. The report also covers market sizes and forecasts for the South American laundry appliance market, in value (USD), for all the above segments.

| Washing Machines |

| Clothes Dryers |

| Others (Garment Steamers, Electric Irons, Laundry Dehumidifiers) |

| Fully Automatic |

| Semi-Automatic / Manual |

| Below 6 kg |

| 6–8 kg |

| Above 8 kg |

| Multi-brand Stores |

| Exclusive Brand Outlets |

| Online |

| Other Distribution Channels |

| Brazil |

| Argentina |

| Chile |

| Colombia |

| Peru |

| Rest of South America |

| By Product Type | Washing Machines |

| Clothes Dryers | |

| Others (Garment Steamers, Electric Irons, Laundry Dehumidifiers) | |

| By Technology | Fully Automatic |

| Semi-Automatic / Manual | |

| By Load Capacity | Below 6 kg |

| 6–8 kg | |

| Above 8 kg | |

| By Distribution Channel | Multi-brand Stores |

| Exclusive Brand Outlets | |

| Online | |

| Other Distribution Channels | |

| By Region | Brazil |

| Argentina | |

| Chile | |

| Colombia | |

| Peru | |

| Rest of South America |

Key Questions Answered in the Report

What is the current size and growth outlook for the South America laundry appliances market?

The South America laundry appliances market size is USD 5.18 billion in 2026 and is projected to reach USD 6.25 billion by 2031 at a 3.83% CAGR during 2026–2031.

Which product category leads value in South America, and which will grow fastest?

Washing machines led with 71.34% of the 2025 value, while clothes dryers are forecast to grow fastest at a 5.00% CAGR through 2031 due to urban constraints and premium heat-pump models.

Which technology segment is gaining momentum in South America laundry appliances?

Fully automatic models dominate at 65.12%, but semi-automatic models are projected to grow faster at 5.50% CAGR in grid-constrained and price-sensitive areas.

Which country contributes the largest revenue, and who is growing fastest?

Brazil contributed 45.72% of 2025 revenue due to payments modernization and local capacity, while Chile is forecast to grow at a 5.50% CAGR on strong digital and regulatory momentum.

What channels are most important for selling major laundry appliances in South America?

Multi-brand stores held 48.92% share in 2025 for display and fulfillment advantages, while online channels are projected to grow at 7.00% CAGR on instant payments and embedded BNPL.

How do regulations affect replacement cycles in South America laundry appliances?

Tightening energy and safety rules in Brazil, Chile, and Colombia accelerate inverter adoption, increase certification costs, and push faster swap-outs into higher-rated models, which drives premiumization over time.

Page last updated on: