South America Injection Molding Machines Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

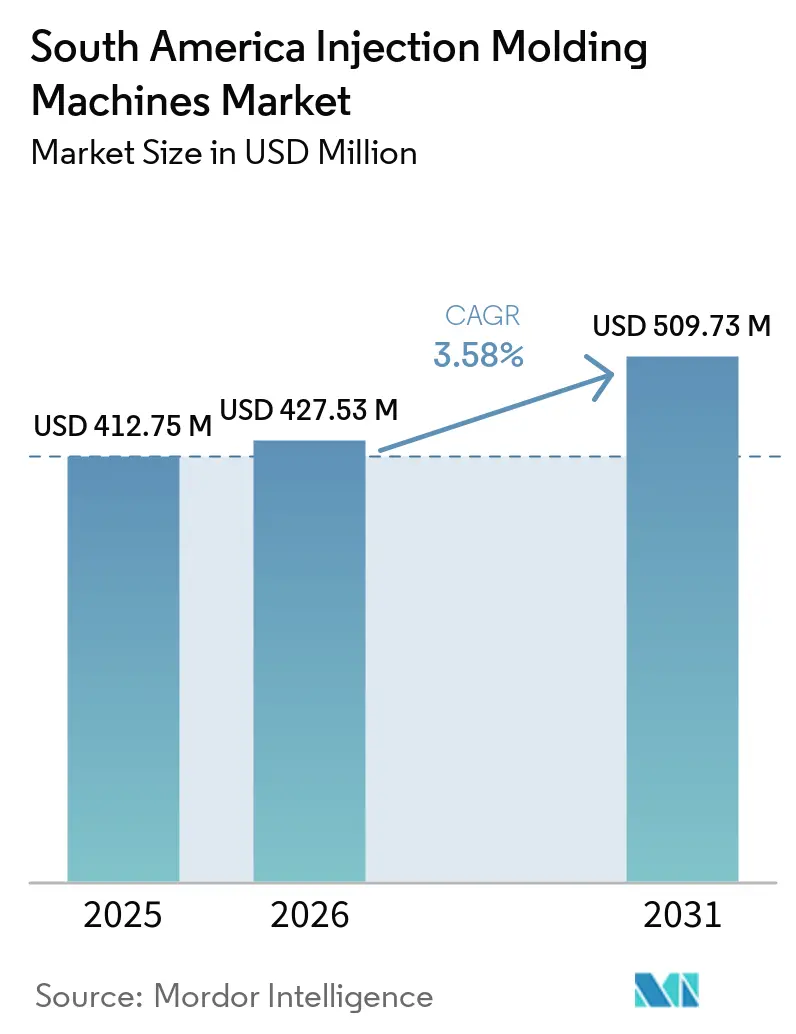

| Base Year Market Size (2025) | USD 412.75 Million |

| Market Size (2026) | USD 427.53 Million |

| Market Size (2031) | USD 509.73 Million |

| Growth Rate (2026 - 2031) | 3.58% CAGR |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South America Injection Molding Machines Market Analysis by Mordor Intelligence

The South America Injection Molding Machines Market size is projected to expand from USD 412.75 million in 2025 and USD 427.53 million in 2026 to USD 509.73 million by 2031, registering a CAGR of 3.58% between 2026 to 2031. Brazil drives demand through Banco Nacional de Desenvolvimento Econômico e Social (BNDES) Financiamento de Máquinas e Equipamentos (FINAME) equipment financing, which subsidizes up to BRL 150 million (USD 27 million) per operation and provides tenors of up to 120 months. Capital expenditures are being stimulated by growth in packaging, automotive lightweighting, and the nearshoring of North American molded-parts supply chains. However, currency volatility and high borrowing costs are slowing the pace of large-tonnage equipment purchases. All-electric presses are gaining traction due to their ability to reduce energy consumption by 25%–80% compared to conventional hydraulic systems, a significant advantage in a region where industrial power tariffs vary widely.

Key Report Takeaways

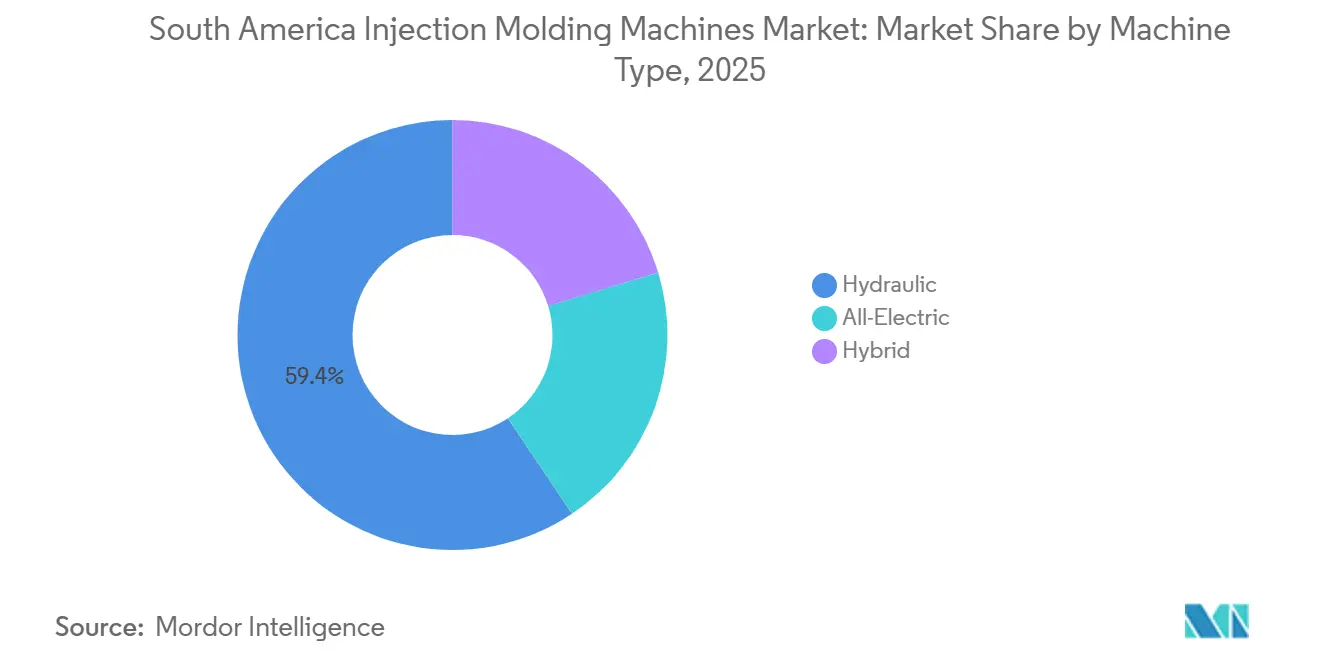

- By machine type, hydraulic led with 59.37% of the South America injection molding machines market share in 2025, while all-electric is projected to expand at a 4.96% CAGR through 2031.

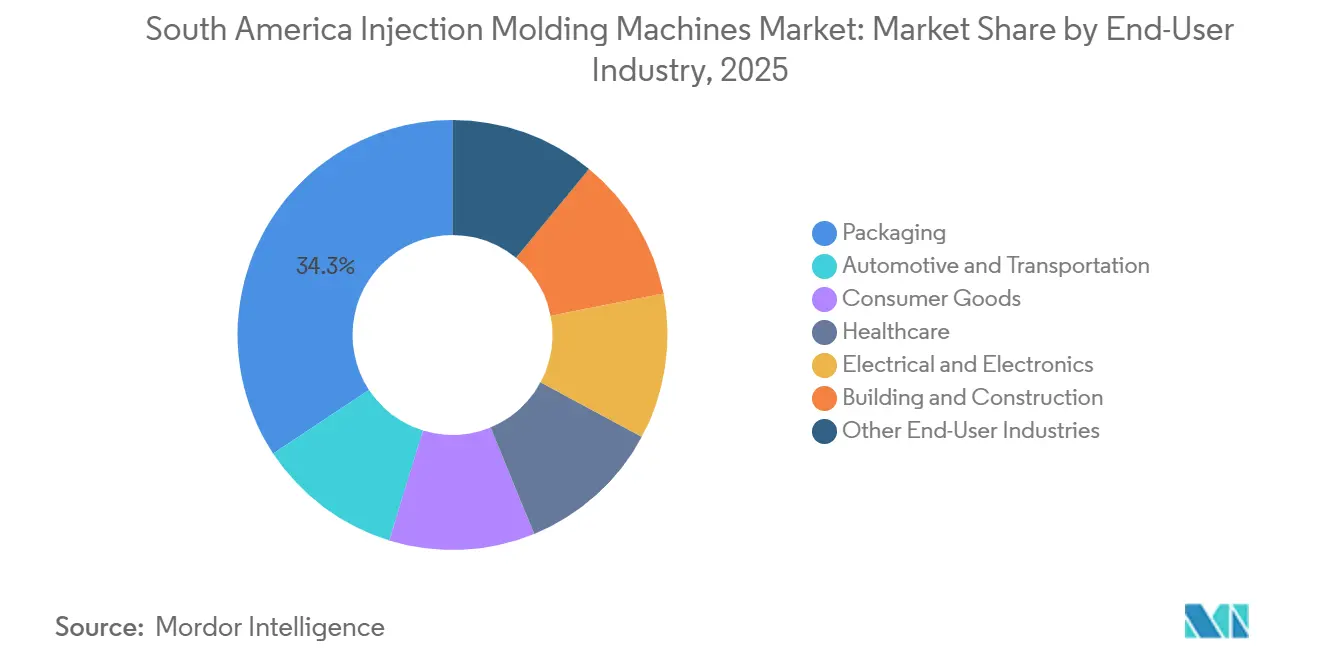

- By end-user industry, packaging commanded 34.28% of the South America injection molding machines market share in 2025, while healthcare is forecast to grow at a 5.16% CAGR through 2031.

- By geography, Brazil captured 47.05% of the South America injection molding machines market share in 2025 and is expected to post a 4.05% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

South America Injection Molding Machines Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High demand from packaging converters | +1.2% | Brazil, Colombia, Argentina | Medium term (2-4 years) |

| Automotive lightweighting push | +0.8% | Brazil (São Paulo), Argentina, Colombia (Antioquia) | Long term (≥ 4 years) |

| Acceleration of electric and hybrid IMM adoption | +0.9% | Global, with early gains in Brazil, Colombia | Short term (≤ 2 years) |

| Brazil's FINAME-2030 tax incentives for capital equipment | +0.5% | Brazil (national) | Medium term (2-4 years) |

| Nearshoring of North-American moulded-parts supply chains | +0.6% | Brazil (São Paulo), Colombia (Bogotá, Medellín), Mexico spillover | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Demand from Packaging Converters

Packaging converters supply food, beverage, and fast-moving consumer goods, and they represented 34.28% of 2025 machine shipments. Thin-wall cycle times under five seconds and the ability to process high levels of recycled content without shot-weight drift top purchasing criteria. Brazil’s plastics transformation industry expects BRL 168 billion (USD 30 billion) in 2026 sales and plans BRL 31.7 billion (USD 5.7 billion) in sustainability-oriented investments through 2027[1]Associação Indústria S/A, “Brazilian Plastics Transformation Outlook 2026,” industriasa.com.br. Colombia imported USD 102 million of plastics machinery during the first nine months of 2024, 43% of which were injection presses, marking a 17% year-on-year gain that underscores an upgrade wave toward high-cavitation, energy-efficient systems. Demonstrations at Plástico Brasil 2025 reinforced the shift: ARBURG molded four 250 ml margarine containers in under five seconds on a hybrid Allrounder 720 H, while Haitian’s all-electric Zhafir Zeres F hit a 3.2-second cycle for thin-wall food containers. Brazil’s Decreto 12.688 of October 2025 obliges reverse logistics for plastic packaging, pushing converters toward presses with active melt-control and real-time compensation so recycled resins run reliably.

Automotive Lightweighting Push

Automotive OEMs are replacing metal with fiber-reinforced thermoplastics and engineering polymers to reduce vehicle weight and enable electrification targets. Polyamide for engine parts is forecast to grow at 6.2% CAGR from 2025-2030, while carbon-fiber-reinforced plastics could advance at 9.3%. KraussMaffei’s Chopped Fiber Processing technology dispenses glass-fiber and polypropylene directly in the barrel, cutting material cost up to 30% and delivering payback within a year, an appealing proposition in markets exposed to resin import premiums. Brazil’s MOVER program offers BRL 19 billion (USD 3.4 billion) in tax credits for automakers investing at least 2% of revenue in R&D, incentivizing local production of lightweight parts. Colombia’s draft decree granting zero-tariff imports on green-vehicle components, combined with 17 free-trade agreements, positions Antioquia and Bogotá to serve regional EV supply chains.

Acceleration of Electric and Hybrid IMM Adoption

The energy-saving advantage of all-electric presses, 25% to 80% versus hydraulics, has translated into a 4.96% CAGR outlook through 2031. ARBURG’s Allrounder Trend series (56-225 tons) introduced at K 2025 offers gestica lite control and four-week lead times aimed at cost-sensitive converters. KraussMaffei relaunched its PX line with 25% higher efficiency and a 23% smaller footprint, embedding web-based MC7 controls that satisfy emerging cybersecurity mandates. ENGEL localized e-mac output at its new Querétaro facility, trimming logistics time for Brazilian buyers. In Argentina, large industrial users pay USD 0.07-0.08 per kWh, a level that accelerates electric-press paybacks, whereas small molders face higher blended tariffs that make hybrids or efficient hydraulics more practical.

Brazil’s FINAME-2030 Tax Incentives for Capital Equipment

FINAME credits finance up to 100% of equipment cost for micro, small, and midsize firms, with tenors to 120 months and grace periods of up to 24 months. Dedicated lines such as FINAME Máquinas 4.0 and FINAME Baixo Carbono encourage presses equipped with IoT connectivity, predictive maintenance, and servo drives. Effective rates remain well below commercial lending, lifting replacement cycles and favoring OEMs that register their machines in the FINAME database.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront capex for large-tonnage machines | -0.7% | Brazil, Argentina, Colombia | Short term (≤ 2 years) |

| Currency volatility and macro-economic risk | -0.5% | Argentina, Brazil (exchange-rate exposure) | Medium term (2-4 years) |

| Grid-electricity cost spikes impacting OPEX | -0.3% | Argentina (SMEs), Brazil (high Selic) | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Upfront Capex for Large-Tonnage Machines

Standard presses list at USD 10,000-30,000 across Latin America, while units above 300 tons exceed USD 100,000. Roughly 75% of purchases in Brazil and Argentina rely on internal cash flow because commercial interest rates remain elevated at 15% Selic in December 2025. Argentina’s Régimen de Incentivo para Grandes Inversiones (RIGI) scheme provides 30-year tax stability on projects over USD 200 million, but typical molding investments fall below that threshold, leaving most buyers exposed to policy swings. Refurbished presses sell at discounts of more than 50% yet carry 8%–10% annual maintenance costs versus 2%–3% for new units.

Currency Volatility and Macro-Economic Risk

Argentina’s inflation eased from 37% in 2025 toward a projected 15% in 2026, but the peso is expected to weaken 14.6% year-on-year, inflating the local-currency cost of dollar-denominated press imports. Brazil’s packaging trade registered a 284.9% increase in net tonnage surplus, yet persistent real fluctuations eroded dollar revenue, complicating return-on-investment math for imported machinery.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Machine Type: Hydraulic Dominance Faces Electric Disruption

Hydraulic machines accounted for 59.37% of the South America injection molding machines market in 2025, supported by lower purchase price and compatibility with existing large-tonnage molds. All-electric machines are set to expand at a 4.96% CAGR to 2031. Hybrid systems, mixing electric clamping with hydraulic injection, offer a compromise that delivers faster dry cycles and meaningful efficiency gains without the full electric price premium. At Plástico Brasil 2025, ARBURG’s hybrid Allrounder 720 H produced four in-mold-labeled 250 ml containers in under five seconds. KraussMaffei’s revamped PX all-electric showed a 25% efficiency bump and a 23% footprint reduction, features in demand among converters adopting Industry 4.0 monitoring.

Across Brazil and Argentina, large industrial users paying wholesale power tariffs can achieve two- to three-year payback periods on electric presses, while small and medium-sized enterprises (SMEs) facing higher blended rates weigh hybrids or servo-hydraulics. ENGEL’s e-mac machines built in Querétaro now reach Brazilian buyers in weeks instead of months, improving uptime planning. Sumitomo (SHI) Demag’s IntElect platform, demonstrated on 100% recycled polypropylene with activeMeltControl, aligns with rising requirements for post-consumer resin usage under Brazil’s Decreto 12.688.

By End-User Industry: Packaging Leads, Healthcare Accelerates

Packaging captured 34.28% of 2025 revenue across the South America injection molding machines market, fueled by food and beverage demand and by BRL 31.7 billion (USD 5.7 billion) in sustainability investments through 2027. Healthcare is forecast to grow at a 5.16% CAGR through 2031 as pharmaceutical packaging, pre-filled syringes, and diagnostic consumables require all-electric presses with validated process controls. Automotive applications rely increasingly on polyamide, polycarbonate, and Polyether Ether Ketone/Polyphenylene Sulfide (PEEK/PPS) to replace metal, translating to steady demand for presses capable of processing high-temperature filled polymers.

Brazil’s flexible-packaging segment reported BRL 40.1 billion (USD 7.2 billion) in 2025 revenue and operates at 70.4% utilization, a level that leaves headroom for productivity upgrades rather than outright capacity builds. Colombia posted a 3% real production gain in July-September 2025 across its plastics sector, with exports of processed products up 1.4% to USD 587 million, confirming that export-oriented packaging and automotive parts are spurring machine imports. Husky’s HyperSync cell, cycling recycled polypropylene cups in 3.8 seconds, illustrates the high-speed, recycled-content capability packaging players now require. KraussMaffei’s CFP retrofits unlock lower-cost direct glass-fiber compounding, attracting automotive molders under pressure to trim material outlays.

Geography Analysis

Brazil commanded 47.05% of the South America injection molding machines market in 2025 and is projected to grow at a 4.05% CAGR to 2031. Its 12,400-firm plastics transformation sector turned 7.49 million tons of output into BRL 123 billion (USD 22 billion) revenue in 2023, backed by FINAME credits that subsidize machinery for digitalization and energy efficiency. ARBURG’s São Paulo technology center supports roughly 3,000 customers, and Haitian’s local subsidiary offers turnkey cells and spares, underscoring the depth of service infrastructure. Yet high interest rates keep capacity utilization modest, shifting focus toward retrofits and energy-efficient replacements that lower unit costs.

Argentina shows upside potential with GDP set to climb 4.3% in 2026, plus a 29.8% surge in gross fixed capital formation in 2025. Inflation remains stubborn, and April 2025 removal of capital controls adds exchange-rate risk, but the competitive wholesale power tariff of USD 0.07-0.08 per kWh favors energy-intensive molding in large plants. The RIGI investment regime secures 30-year fiscal stability for projects above USD 200 million, a bar that excludes most converters yet signals a pro-investment orientation.

Colombia imported 17% more presses year-on-year in the first nine months of 2025; injection machines made up 43% of plastics-equipment acquisitions. Antioquia hosts the largest concentration of national plastics employment and recorded 4.9% production growth in January-September 2025, buoyed by free-trade agreements that ease component exports. Rest of the region markets such as Chile and Peru remain smaller but capitalize on political stability and transparent regulatory climates that lower investment risk for niche, high-value projects[2]FDI Latin America, “Chile Investment Climate 2025,” fdi-latinamerica.com.

Competitive Landscape

The South America injection molding machines market is highly concentrated, with the five largest companies being Haitian Group, ROMI S.A., ENGEL AUSTRIA GmbH, ARBURG GmbH + Co KG, and Milacron Holdings, LLC. ENGEL’s Querétaro plant, opened March 2025, can supply 180-200 units annually, cutting lead times and freight for buyers across Brazil and Colombia. ARBURG celebrated 25 years in Brazil in 2025 and runs a 700 m² technology center with training and spare-parts stock, a high-touch model that supports premium pricing. Haitian delivered 53,000 presses globally in 2024 and leverages scale to price aggressively, with a 20-year Brazilian presence that assures rapid service.

Differentiation now centers on energy efficiency, recyclate processing, and digital connectivity. KraussMaffei’s CFP retrofits slash fiber-reinforced part costs by 30%, ENGEL’s iQ weight control and HT-Xtend AI adjust parameters in real time, and Husky’s Advantage+Elite monitors more than 70 variables across fleets of up to 1,500 presses. Domestic producer ROMI taps FINAME accreditation to serve price-sensitive converters, while Chinese entrants add Industry 4.0 features to escape a pure-cost position. ISO 9001:2015, FDA, and INVIMA compliance have become table stakes for machines targeting export-grade medical and food packaging, prompting converters to favor suppliers with robust validation track records.

Market entrants see opportunity in midsized hybrids and affordable electrics that promise power savings without full-premium pricing, as well as in retrofit packages that modernize hydraulic fleets via servo upgrades and IoT gateways. Service depth, spare-parts logistics, and financing partnerships remain decisive, given long average machine lifecycles and the working-capital constraints typical of the region’s converter base.

South America Injection Molding Machines Industry Leaders

Haitian Group

ROMI S.A.

ENGEL AUSTRIA GmbH

ARBURG GmbH + Co KG

Milacron Holdings, LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Italy-based Mech-I-Tronic acquired RK Ferramentaria in Curitiba, Brazil, which marked the group’s entry into the Americas as part of its growth strategy. Mech-I-Tronic specializes in automated assembly, plastic extrusion, and mold manufacturing for the medical, food and beverage packaging, industrial, and other markets.

- March 2025: At Plástico Brasil 2025, Tederic showcased its high-performance NEO series, which included both two-platen and electric injection molding machines. The presentation emphasized the integration of advanced technology and sustainable, environmentally friendly manufacturing solutions for the Brazilian plastics supply chain.

South America Injection Molding Machines Market Report Scope

An injection molding machine is an industrial system designed to manufacture plastic components by injecting molten material into a mold. It consists of an injection unit, a clamping unit, and control systems. These machines, available in hydraulic, electric, or hybrid configurations, operate in cycles typically ranging from 30 to 90 seconds. They melt plastic pellets and apply high pressure to produce uniform, precise parts.

The South America Injection Molding Machines Market is segmented into machine type, end-user industry, and geography. By machine type, the market is segmented into hydraulic, all-electric, and hybrid. By end-user industry, the market is segmented into packaging, automotive and transportation, consumer goods, healthcare, electrical and electronics, building and construction, and other end-user industries. By geography, the market is segmented into Brazil, Argentina, Colombia, and the rest of South America. For each segment, the market sizing and forecasts have been done on the basis of value (USD).

| Hydraulic |

| All-Electric |

| Hybrid |

| Packaging |

| Automotive and Transportation |

| Consumer Goods |

| Healthcare |

| Electrical and Electronics |

| Building and Construction |

| Other End-User Industries |

| Brazil |

| Argentina |

| Colombia |

| Rest of South America |

| By Machine Type | Hydraulic |

| All-Electric | |

| Hybrid | |

| By End-User Industry | Packaging |

| Automotive and Transportation | |

| Consumer Goods | |

| Healthcare | |

| Electrical and Electronics | |

| Building and Construction | |

| Other End-User Industries | |

| By Geography | Brazil |

| Argentina | |

| Colombia | |

| Rest of South America |

Key Questions Answered in the Report

What is the size of the South America injection molding machines market?

The South America injection molding machines market size stands at USD 427.53 million in 2026 and is projected to reach USD 509.73 million by 2031.

Which country accounts for the largest share of machine demand?

Brazil leads with 47.05% of 2025 demand and is forecast to expand at a 4.05% CAGR through 2031.

Which end-user industry is growing fastest through 2031?

Healthcare is set to grow at a 5.16% CAGR to 2031, driven by demand for cleanroom-compatible all-electric presses used in pharmaceutical packaging and diagnostic consumables.

How quickly are all-electric machines forecast to grow?

All-electric machines are forecast to expand at a 4.96% CAGR through 2031, propelled by 25% - 80% energy savings versus hydraulics and increasingly strict sustainability mandates.

Page last updated on: